Optimal mean-variance investment strategy under value-at-risk constraints

Abstract

This paper is devoted to study the effects arising from imposing a

value-at-risk (VaR) constraint in mean-variance portfolio selection

problem for an investor who receives a stochastic cash flow which

he/she must then invest in a continuous-time financial

market. For simplicity, we assume that there is only one investment

opportunity available for the investor, a risky stock. Using

techniques of stochastic linear-quadratic (LQ) control, the optimal

mean-variance investment strategy with and without VaR constraint

are derived explicitly in closed forms, based on solution of

corresponding Hamilton-Jacobi-Bellman (HJB) equation. Furthermore,

some numerical examples are proposed to show how the addition of the

VaR constraint

affects the optimal strategy.

keywords:

Value-at-risk , Mean-variance portfolio , Hamilton-Jacobi-Bellman equation , Optimal investment strategy.MSC:

C02 , C61 , IM01.1 Introduction

The mean-variance model of Markowitz (1952, 1959) is a cornerstone of modern portfolio theory. The most important contribution of this model is that it enables an investor to optimally select mean-variance efficient portfolios for seeking the highest return after specifying his acceptable risk level. Since Markowitz’s pioneering work, the mean-variance model was extended from single-period case to multi-period discrete-time case (see Hakansson, 1971; Pliska, 1997; Samuelson, 1969, etc.) and continuous time case during the last decades (see Cox and Huang, 1989; Duffie and Richardson, 1991; Karatzas et al., 1987; Schweizer, 1996, etc.). However, when studying these two kinds of dynamic portfolio selection models, most research works have been dominated by those of maximizing expected utility functions of the terminal wealth. Nevertheless, when using this approach, the tradeoff information between the risk and the expected return is implicit, which makes the investment decision less intuitive. In 2000, Zhou and Li introduce the stochastic linear-quadratic (LQ) control as a general framework to study the mean-variance optimization problem. Within this framework they have established a natural connection of the portfolio selection problems and standard stochastic control models and attained some elegant results for a continuous-time mean-variance model with determined coefficients.

When using stochastic LQ control approach to deal with continuous time mean-variance problem, the terminal wealth is a random variable with a distribution that is often extremely skewed and shows considerable probability in regions of small values of the terminal wealth. This means that the optimal terminal wealth may exhibit large shortfall risks. In order to prevent investors from extremely dangerous positions in the market, it is thus more reasonable to consider asymmetric risk measures, e.g. value-at-risk (VaR), to limit the exposure to market risks.

In market risk management, it is widely accepted that VaR is a useful summary measure of market risks which regulatory authorities sometimes enforced investors to use. VaR is actually the maximum expected loss over a given horizon period at a given level of confidence. For comprehensive introduction to risk management using VaR, we refer the reader to Jorion (1997).

Recognizing that risk management is typically not an investor’s primary objective, the investors would like to limit their risks while maximizing expected utility. This leads to stochastic control problems under restrictions on such risk measures. There has been considerable interest in the study of portfolio selection models subject to a VaR constraint. Kluppelberg and Korn (1998), Alexander and Baptista (2004, 2007) investigate the optimal portfolio choices subject to a VaR or conditional VaR (CVaR) constraint in a static (one-period) setting. The similar problems in a dynamic setting has started to draw more attentions recently, Basak and Shapiro (2001) focus on the optimal portfolio policies of a utility-maximizing agent by imposing the VaR constraint at one point in time. Cuoco et al. (2008) developed a realistic dynamically consistent model of the optimal behavior of a trader subject to risk constraints. They assume that the risk of the trading portfolio is re-evaluated dynamically by using the conditioning information, and hence the trader must satisfy the risk limit continuously. Yiu (2004) explicitly derived the standard VaR constraint on total wealth and obtained optimal trading strategy(without consideration of re-insurance). Pirvu (2005) started with the model of Cuoco et al. (2008) and found the optimal growth portfolio subject to these risk measures. Pirvu (2007) extended those results by extensively studying the optimal investment and consumption strategies for both logarithmic utility and non-logarithmic CRRA utilities.

Motivated by Zhou and Li (2000) and Yiu (2004), this paper addresses the problem of an investor who receives an uncontrollable stochastic cash flow which he must then invest in a complete continuous-time financial market in order to maximize the weighted average of the expectation and the variance of his terminal wealth at a horizon time. The main focus in this paper is on the mean-variance optimization problem of the investor subject to a risk limit specified in terms of VaR on his future net worth. To our knowledge, this problem has not yet received a complete treatment in the existing literature. In this paper, we derive the optimal mean-variance investment strategy under a standard VaR constraint by solving the corresponding Hamilton-Jacobi-Bellman (HJB) equation and explore how the addition of a risk constraint affects the optimal solution.

The rest of the paper is organized as follows. Section 2 describes the model, including the definition of the VaR on the future net worth process. Section 3 contains the main characterization result of the VaR constraint and formulates the portfolio optimization problem that can be eventually discussed as a stochastic LQ problem. Section 4 gives the explicit solution of the optimal mean-variance strategy without VaR constraint by solving the corresponding HJB equation. Section 5 discusses the optimal mean-variance strategy with VaR constraint. Finally, Section 6 provides some numerical examples to show how the addition of the VaR constraint affects the optimal strategy.

2 The Model

2.1 Continuous-time investment in stochastic cash flow

All stochastic processes introduced below are supposed to be adapted in a filtered probability space , where is a filtration satisfying the usual conditions. Moreover, it is assumed throughout this paper that all inequalities as well as equalities hold -almost surely.

Following the framework of Browne (1995), for simplicity, and without any loss of generality, we assume that there is only one risky stock available for investment, whose price at time will be denoted by which satisfies the following stochastic differential equation

| (1) |

where is the appreciation rate and is the volatility or the dispersion of the stock. is a standard Brownian motion.

Since we are concerned with investment behavior in the presence of a stochastic cash flow, or an external risk process denoted by , which is another Browian motion with drift and diffusion parameter , that is

| (2) |

where and are possibly correlated with correlation coefficient . In case there would only be one source of randomness left in the model, we also assume that .

We will define an investment strategy as an admissible adapted control process , satisfying that , a.s., for all . Note that represents the amount invested in risky stock at time , and we will not put more constraints on . In particular, we will allow , which means short-selling would be allowed, the circumstance that is also permitted so that the investor can borrow money to buy stock.

Assume that the trading takes place continuously and transaction cost is not considered. Therefore, following the investment strategy , the wealth process of the investor at time , which will be denoted by , can be given by the following stochastic differential equation with initial condition

| (3) |

2.2 Value-at-risk

Now we want to introduce the definition of value-at-risk. Here we start by rewriting (3) into integration form

| (4) |

where denotes the initial value of the portfolio. Notice that (4) leads to

| (5) |

for any .

If we assume that the investment strategy were kept constant during the time period , i.e. , for any , then it follows immediately from (5) that, given the strategy and the associated wealth value at time , the random variable would be the future value of the wealth at time

| (6) |

Therefore we define the future net worth of the wealth process in horizon period by .

Definition 1 (Value-at-risk).

Given a probability level and a horizon , the value-at-risk of the future net worth of the wealth process with investment strategy at time , denoted by , is defined as

| (7) |

where

| (8) |

and

Consequently, is the quantile of the projected portfolio gain over the time interval . In other words, is the greatest loss over the next period of length which would be exceeded only with a small conditional probability if the current portfolio were kept the same.

Proposition 1 (Computation of value-at-risk).

We have

| (9) |

where and denote the standard normal distribution and inverse distribution functions respectively.

Proof of Proposition 1.

We have

where follows standard normal distribution conditionally. Thus, from

we know that

which gives rise to

And therefore

which immediately gives (9). ∎

Note that even when , which means there is no investment

in risky stock, is also

positive if . This results from the

incompleteness of the model, in which the cash flow cannot be

traded and therefore the risk cannot be eliminated as long as

.

3 Statement of the Problem

We consider the optimal control problem of the investor who starts with an initial wealth and must select a strategy so as to maximize the weighted average of the expectation and the variance of his terminal wealth, subjected to the constraint that the VaR with the chosen portfolio is no larger than a given level at any time . In mathematical terms, this problem can be described as

| (10) |

where the parameter (representing the weight) is positive. We denote the optimal solution of problem (10) by if it exists. Note that the upper bound can be dependent on and , however in this paper, we set to be a constant in order to obtain the explicit solution.

Proposition 2 (Computation of the value-at-risk constraint).

The explicit form of the VaR constraint in problem(10) is

| (11) |

where , , and

| (12) |

if and . We also assume that is always larger than .

Proof of Proposition 2.

The VaR constraint can be written as

which is equivalent to

that is, after some simplifications,

where , . Note that when , always holds. This observation will help us in the second case when and the third case when .

Therefore we have a group of inequalities

| (13) |

First we study the degeneration case: ,i.e. .

In this case, if , i.e. , then the first inequality of (13) would imply

however

which, together with the second inequality of (13), leads to .

If , i.e. , then the first inequality of (13) would imply

which leads to a contradiction. Thus there is no solution.

Secondly, we study the case: .

In this case, . are two points of intersection of the parabola and the lateral axis. Using the observation we have mentioned just now, we know that the first inequality of (13) will not hold if , which leads to . Therefore in this case, the constraint is .

Thirdly, we study the case: .

In this case, if , i.e.

The constraint becomes . Also by using the observation, we have or . And therefore we have

or

where is the symmetry axis of the parabola.

If , then the parabola is strictly above the lateral axis, and thus no solution can satisfy even the first inequality of (13). ∎

4 Optimal Mean-variance Strategy without VaR Constraints

Before we finally solve the problem (10), we consider the corresponding optimal control problem without the VaR constraint

| (14) |

Here we denote the optimal solution of problem (14) by .

To proceed, let be the optimal value function attainable by the investor starting from the state at time . And we will give the explicit form of the optimal strategy in the following theorem.

Therom 1 (The optimal mean-variance strategy without VaR constraints).

The optimal strategy to maximize expected utility at terminal time is to invest, at each time ,

| (15) |

and then the optimal value function is

| (16) |

where

| (17) |

and , , .

Proof.

From Fleming and Rishel (1975), the corresponding HJB equation is given by

| (18) |

Assume that the HJB equation (18) has a classic solution , which satisfies . Then differentiating with respect to gives the optimizer

| (19) |

Substituting (19) back into (18), the HJB equation becomes, after some simplification, equivalent to the following nonlinear Cauchy problem for the value function

| (20) |

where the constants , , .

In order to simplify the boundary condition, let

| (21) |

and rewrite the HJB equation (20) into the form

| (22) |

To solve this partial differential equation (22), we try to fit a solution of the form

| (23) |

where , and are suitable coefficient, and note that by the form of (23) we have

| (24) | |||||

The boundary condition is naturally satisfied by the solution form of (23). By substituting (24) into (22), we have

| (25) |

which requires , and to satisfy

| (26) |

Solving equations (26), we derive (17), and hence (16) after replacing by . Since we have the value function in explicit form, it becomes easy for us to obtain the optimal control of (15) by substituting the value for and from (24) into (19).

∎

5 Optimal Mean-variance Strategy under VaR Constraints

In this section, we come back to the problem (10). Our objective is to give the optimal control as well as the corresponding value function in explicit form. Since in Theorem 1 we have already found the optimal control which optimize the problem of (14) without the VaR constraint Therefore, we obtain as long as satisfies the VaR constraint. However, the global optimizer can not be the local optimizer when fails the VaR constraint.

Remind ourselves of the proof in Theorem 1, by applying the dynamic programming approach we are tackling with a static optimization problem (18). Rewrite the problem and add the VaR constraint to it and we have

| (27) |

where the intervals have the same forms of (11) in Proposition 2, therefore, the constraint is equivalent to the VaR constraint in problem (10). Since we know that , it becomes a simple problem to find the peak of the parabola, which opens down, on each interval . Specifically,

- Case 1

-

when ,

(28) - Case 2

-

when ,

(29) - Case 3

-

when ,

(30)

Except these three cases listed above, there is no solution which can satisfies the constraint. Here and have the same expressions as shown in Proposition 2, and has the expression of (15) in Theorem 1.

Before giving the optimal control as well as the corresponding value function in explicit form, we have to admit that we are going to omit the first case, i.e. when happens. On the one hand, this case could hardly happen so that we can benefit little from studying them in practice, on the other hand, the procedures of studying the first case is quite similar with the other two, it will be therefore a mere repetition.

Therom 2 (The optimal mean-variance strategy under VaR constraints).

The optimal strategy to maximize expected utility at terminal time subjected to the VaR constraint is to invest .

When ,

| (31) |

and the optimal value function is

| (32) |

Proof.

Since the explicit form (31) and (33) of the optimal control in this theorem are only the rescript of (29) and (30), we only have to work out with the corresponding value function .

Since we have already solved the first equation of (35) in Theorem 1, we will focus on the second equation which appears to be much more easier to handle for its linearity.

Using the notation of and , the second equation of (35) with the terminal condition can be written as another Cauchy problem

| (36) |

Applying the same trick by letting , then

| (37) |

In order to apply the Fourier transform, change the terminal condition into initial condition by letting

| (38) |

Then we have

| (39) |

which immediately gives the second part of (32).

Similarly when , the corresponding Cauchy problem is described as

| (40) |

with terminal condition .

Almost the same steps can be taken if we replace the notation , and with , and respectively, and (34) will be obtained.

∎

6 Illustration of the Solutions

In this section we will illustrate the result of Theorem 1 and Theorem 2. Without loss of generality, we set the initial wealth level between . The VaR horizon period is chosen to be 1 trading day, nearly 1/260 calendar year, while the terminal year is set to be 10 calendar year. Confidence level is , and the upper VaR limit is , which is of the initial wealth. For the stochastic cash flow, we use , . In the market, the risk-free interest , as we always assumed, and for the stock, , . the correlation coefficient of and is set to be , and the parameter in the quadratic utility function is . We summarize these parameters below in the Table 1.

| 1 | 0.05 | 0.3 | 0.01 | 0.14 | 0.2 | 1 | 10 | 1/260 | 0.01 | 0.02 |

The setting of the parameters in Table 1 satisfies the three conditions of case 3:

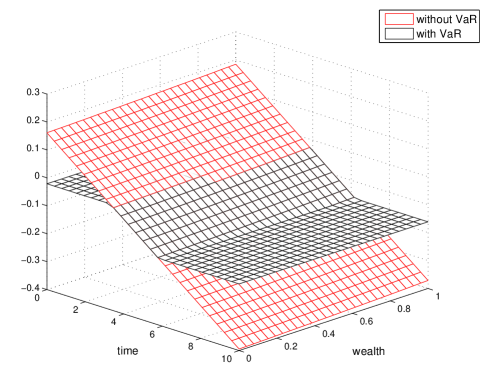

where , . Therefore the optimal control has the expression . We show the optimal strategy without the VaR limit as well as the constrained one on in the Figure 1 below.

As shown in this figure, the VaR constraint actually gives an upper and a lower bound surface to the strategy surface. From the expression of (12), we know that are independent of and , and strictly negative in this case. Therefore the bound surfaces are horizontal and below level zero, which actually constrain the behavior of short-selling.

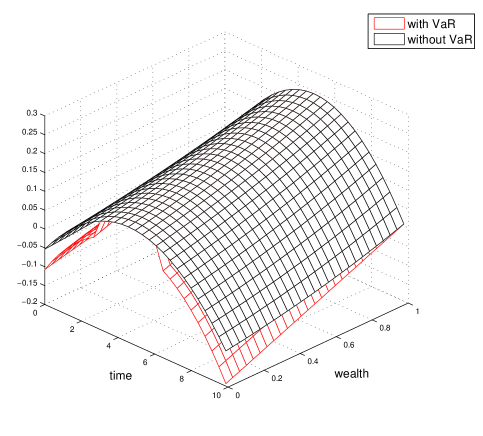

We could also compare the optimal value function with and without the VaR constraint, which are illustrated in Figure 2 for case 3. In both figures we could observe that the VaR constraint is active during the time period of approximately . The optimal function of constrained problem is identical to that of the unconstrained one during , and it becomes inferior when the constrain is active.

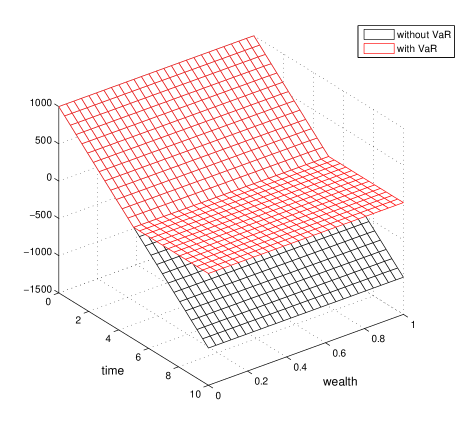

By changing the value of drift and diffusion parameter of the risky stock, investment in them becomes much more promising than in case 3. See the table below, note that we do not change the values of other parameters.

| 1 | 0.8 | 0.02 | 0.01 | 0.14 | 0.2 | 1 | 10 | 1/260 | 0.01 | 0.02 |

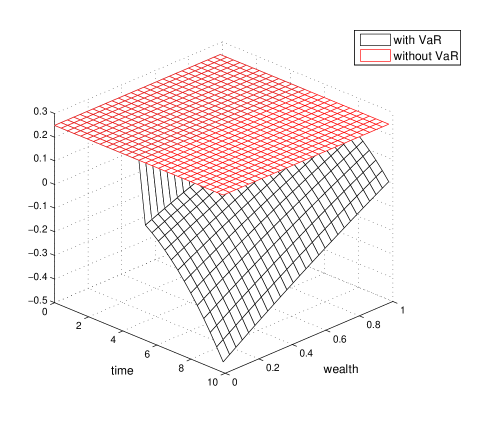

The setting of the parameters in Table 2 satisfies the condition of case 2, i.e. , where . In Figure 3, we observe that when time is near 0, the investment in risky asset appears to be rather radical. This results from the superiority of the stock, and the investor can hardly get any loss under such circumstance, and therefore do not activate the VaR constraint. When time goes to approximately , the constraint becomes active and gives the optimal strategy a lower bound near level zero, which is the only bound surface brought by the VaR constraint in case 2. The optimal value function surfaces are shown in Figure 4, where the surface of the constrained problem remains identical to that of the unconstrained problem until . All as we expected, the constrained surface becomes inferior since then. Note that in this case, the optimal value without VaR constraint appears almost horizontal, which seems unreasonable. This results from the uncommon condition that , which directly leads to the huge absolute value of . Look at the expressions of (16) and (17), the factor almost annihilate the first three terms in , which makes becomes a constant of approximately.

References

- Alexander and Baptista (2004) Alexander, G.J., Baptista, A.M., 2004. A comparison of VaR and CVaR constraints of portfolio selection with the mean-variance model. Management Science 50, 1261–1273.

- Alexander and Baptista (2007) Alexander, G.J., Baptista, A.M., 2007. Mean-variance portfolio selection with ‘at-risk’ constraints and discrete distributions. Journal of Banking and Finance 31, 3761–3781.

- Basak and Shapiro (2001) Basak, S., Shapiro, A., 2001. Value-at-risk-based risk management: Optimal policies and asset prices. Review of Financial Studies 14, 371–405.

- Browne (1995) Browne, S., 1995. Optimal investment policies for a firm with a random risk process: exponential utility and minimizing the probability of ruin. Mathematics of Operation Research 20, 937–958.

- Cox and Huang (1989) Cox, J.C., Huang, 1989. Optimal consumption and portfolio policies when asset prices follow a diffusion process. Journal of Economic Theory 49, 33–83.

- Cuoco et al. (2008) Cuoco, D., He, H., Issaenko, S., 2008. Optimal dynamic trading strategies with risk limits. Operations Research 56, 358–368.

- Duffie and Richardson (1991) Duffie, D., Richardson, H.R., 1991. Mean-variance hedging in continuous time. Annals of Applied Probability 1, 1–15.

- Hakansson (1971) Hakansson, N.H., 1971. Multi-period mean-variance analysis: toward a general theory of portfolio choice. Journal of Finance 26, 857–884.

- Jorion (1997) Jorion, P., 1997. Value at Risk: the New Benchmark for Controlling Market Risk. Irwin, Chicago, IL.

- Karatzas et al. (1987) Karatzas, I., Lehoczky, J.P., Shreve, S.E., 1987. Optimal portfolio and consumption decisions for a small investor on a finite time-horizon. SIAM Journal on Control and Optimization 25, 1557–1586.

- Kluppelberg and Korn (1998) Kluppelberg, C., Korn, R., 1998. Optimal portfolios with bounded value-at-risk. Working paper, Munich University of Technology.

- Markowitz (1952) Markowitz, H., 1952. Portfolio selection. Journal of Finance 7, 77–91.

- Markowitz (1959) Markowitz, H., 1959. Portfolio Selection: Efficient Diversification of Investment. New York: John Wiley & Sons.

- Pirvu (2005) Pirvu, T.A., 2005. Maximizing portfolio growth rate under risk constraints. Doctoral Dissertation, Department of Mathematics, Carnegie Mellon University.

- Pirvu (2007) Pirvu, T.A., 2007. Portfolio optimization under the value-at-risk constraint. Quantitative Finance 7, 125–136.

- Pliska (1997) Pliska, S.R., 1997. Introduction to Mathematical Finance. Blackwell, Malden.

- Samuelson (1969) Samuelson, P.A., 1969. Lifetime portfolio selection by dynamic stochastic programming. The Review of Economics and Statistics 51, 239–246.

- Schweizer (1996) Schweizer, M., 1996. Approximation pricing and the variance-optimal martingale measure. The Annals of Probability 24, 206–236.

- Yiu (2004) Yiu, K.F.C., 2004. Optimal portfolios under a value-at-risk contraint. Journal of Economic Dynamics and Control 28, 1317–1334.

- Zhou and Li (2000) Zhou, X.Y., Li, D., 2000. Continuous-time mean-variance portfolio selection: a stochastic LQ framework. Applied Mathematics and Optimization 42, 19–33.