On Calibrating Stochastic Volatility Models with time-dependent Parameters111With best thanks to Cédric de Masson d’Autume who contributed some of the code used in the numerical example.

Abstract

We consider stochastic volatility models using piecewise constant parameters. We suggest a hybrid optimization algorithm for fitting the models to a volatility surface and provide some numerical results. Finally, we provide an outlook on how to further improve the calibration procedure.

1 Introduction

Over the past two decades various stochastic volatility models have been introduced to explain stylized facts observed in the market. Some of the most popular models are the Heston stochastic volatility model and an extension allowing for jumps, cf. Heston (1993) and Bates (1996), respectively, the Variance-Gamma model introduced by Madan et al. (1998), the model introduced by Barndorff-Nielsen and Shephard (2001) and Lévy models with stochastic time, see Carr et al. (2003).

There are basically two approaches to calibrate a stochastic volatility model. It is possible to calibrate the model to historical data or to (liquid) present option prices. For the first approach there exist various methods like maximum likelihood methods, efficient method of moments, or Markov Chain Monte Carlo methods, see Aït-Sahalia and Kimmel (2007); Gallant and Tauchen (1996) and Frühwirth-Schnatter and Soegner (2007), respectively, and the references therein. For various applications the second approach is favorable since the fitted model explains current prices observed on the market, hence we will subsequently consider the latter approach.

For fitting the model we use a hybrid optimization algorithm consisting of a genetic algorithm to roughly locate the minimum and subsequently a pattern search algorithm with the objective to refine the result. This algorithm allows to take nonlinear constraints like the Feller condition for the Heston model into account. Evolutionary algorithms like the genetic algorithm have already been used for calibration e.g. by Hamida and Cont (2005).

2 Model Setup

Let denote the stock price process and the characteristic function of the log-price , defined by

For ease of notation we assume the risk-free interest rate to be constant.

2.1 The Heston Model

Heston (1993) introduced a stochastic volatility model which satisfies a lot of stylized facts like fat tails, volatility clustering, skewness etc., cf. Cont (2001). The Heston model is defined under the risk neutral measure by the coupled two-dimensional SDE

| (2.1) | ||||

| (2.2) |

where and are one-dimensional Brownian motions with correlation and denotes the variance process. The involved parameters are the rate of mean reversion , the long term variance , the volatility of variance (often called the vol of vol), the correlation , and the initial variance . If the Feller condition is satisfied, then the variance process is always positive and cannot reach zero. In absence of the stochastic factor, we have an exponential attraction to long term variance, the equilibrium point being . Typically, the correlation is negative, hence a down-move in the stock price is positively correlated with an up-move in the volatility.

2.1.1 Time-Independent Parameters

Note that there are two representations of the characteristic function. The first one used e.g. by Heston (1993) or Kahl and Jäckel (2005) reads

and the second one e.g. used by Schoutens et al. (2004) and Gatheral (2006) is given by

| (2.3) | ||||

where

| (2.4) | ||||

| (2.5) |

Albrecher et al. (2007) prove in a detailed analysis that is unstable under certain conditions whereas is stable under the full parameter space.

2.1.2 Piecewise Constant Parameters

To obtain a good fit for a volatility surface, i.e., for several maturities at once, is fairly difficult to obtain using a stationary process. One way to obtain a good fit is to use processes for the price process having piecewise constant parameters. The solution for the characteristic function for piecewise constant parameters is given by Mikhailov and Nögel (2003) who derived it using a Computer Algebra system. The full derivation of the solution is provided by Elices (2007) who also presents a formula which is in line with the findings of Albrecher et al. (2007). The solution is given by

where

The solution is close to the Heston one (2.3). The time interval to maturity is divided into sub-intervals where is the time of model parameter jumps. Model parameters are constant during but different for each sub interval. The initial condition for the first sub interval from the end is zero. For the second sub interval we use and from the first sub interval for and , the initial conditions. The same procedure is repeated at each time of the parameters jumps.

2.2 The Heston Model with Jumps

Bates (1996) extended the Heston model by introducing jumps in the asset price. The coupled two-dimensional SDE (2.1)–(2.2) becomes

with the same notations as in (2.1) and (2.2) and with being an independent Poisson process with intensity (i.e., ) and is the percentage jump size that is log-normally i.i.d. over time with mean . The standard deviation of is and

2.2.1 Time-Independent Parameters

Since the jumps and the diffusion part are independent, the characteristic function for is defined by

where as in (2.3) is the characteristic function for the diffusion part and the characteristic function corresponding to the jump part is given by

2.2.2 Piecewise Constant Parameters

We still define the characteristic function as with corresponding to as in Section 2.1.2 and given by

where and are the parameters of the jumps during the sub interval and .

2.3 The Variance Gamma Process

The Variance-Gamma (VG) process is obtained by evaluating Brownian motion (with constant drift and volatility ) at a random time change given by a Gamma process. Let

where is a Brownian motion. Then is a Brownian motion with drift and volatility .

The Gamma process with mean rate and variance rate is a process of independent Gamma increments over time intervals . The VG process is then defined by

The involved parameters are the volatility of the Brownian motion , the variance rate time change and the drift in the Brownian motion . We can control the skewness of the distribution via and the kurtosis with . The resulting risk-neutral process for the stock price is

where .

2.3.1 Time-Independent Parameters

The characteristic function of reads

From this formula, one can obtain a closed formula for both the density function and the option price, for details we refer to Madan et al. (1998).

2.3.2 Piecewise Constant Parameters

For piecewise constant parameters we can use the same method as in Section 2.2.2. For readability we use the notation instead of , and . Note that and that the increments are independent. Then is given by

where , and are the parameters of the models during the sub interval and .

3 Fitting the Model

To fit a stochastic volatility model to a given volatility surface, we first have to compute option prices, then to compute the implied volatility from these prices and finally to resolve the Optimization Problem.

3.1 Optimization Problem

We assume a set of option prices for different maturities and strikes as given. To calibrate a stochastic volatility model, we have to minimize an objective function. We strive to minimize the mean squared error (MSE) of volatilities, i.e.,

where is a given vector of market Black-Scholes implied volatilities and are the implied Black-Scholes volatility resulting from pricing the option with a stochastic volatility model. Instead of fitting the implied volatilities we could also fit option prices. Further it is possible to weight the differences between the given and the fitted prices. The choice of the weights may depend on the liquidity of a given option which can be assessed from the bid-ask spread. (Cont and Tankov, 2004, Chapter 13) suggest to weight the option prices by squared Black-Scholes vegas evaluated at the implied volatilities of the market option prices. If we have a prior distribution, e.g. based on the posterior distribution from parameter estimation from historical data based on a Markov Chain Monte Carlo method, we may apply regularization techniques for which we refer to (Cont and Tankov, 2004, Chapter 13).

3.2 Computation of Option prices

For our application it is crucial to have an efficient method to price plain vanilla options. Therefore we use the Fast Fourier Transform (FFT) introduced for option pricing by Carr and Madan (1999). The basic idea of this method is to develop an analytical expression for the Fourier transform of the option price and then to get the price back by Fourier inversion. Assuming no dividends and constant interest rates , the initial value of a plain vanilla European call option is determined as

where

with being the characteristic function of . Corresponding plain vanilla European put option prices can be derived via the Put-Call-parity equation. Since we cannot evaluate the integral using the FFT, we rather use the expression

where denotes the log of the strike and the risk-neutral density of the log price of the underlying. Since the call pricing function is not square integrable, we consider the modified call price defined by

for a suitable . We consider now the Fourier transform of given by

Then we can use the inverse transform to obtain

and the FFT to compute an approximation of via

where is the distance of the points of the integration grid and . For more details we refer to Carr and Madan (1999). This method is very fast since efficient implementations of the FFT exist. Moreover, this approach allows to compute the option prices for several strikes at once. Note that this approach only depends on the specific models via the characteristic function .

3.3 Hybrid Optimization Algorithm

We suggest a hybrid optimization algorithm which consists of a genetic algorithm with the purpose of locating a minimum within the specified bounds for the parameters and a subsequent direct search method to refine the solution. For a detailed reference concerning genetic algorithms we refer to Bäck et al. (2000).

3.3.1 Genetic Algorithm (GA)

Outline of the Algorithm

The following outline summarizes how the genetic algorithm works:

-

(i)

The algorithm begins by creating randomly an initial population. The population is chosen such that possible constraints (e.g. upper or lower bounds on the variables) are satisfied. It is also possible to provide an initial population or to specify only some members of the initial population.

-

(ii)

The algorithm evaluates the fitness of each individual in the population.

-

(iii)

The algorithm then creates iteratively a sequence of populations. At each step, the algorithm creates the next population based on the current generation. Therefore the following steps are performed:

-

(a)

The algorithm evaluates the fitness of each individual in the population. The fitness is a measure on how well the optimization problem is solved.

-

(b)

A certain number of individuals in the current population (called the Elite count) that have the highest fitness values are chosen as elite children and are passed on to the next population.

-

(c)

A certain number of children of the next generation are produced by combining a pair of parents (crossover). The number is specified as fraction of the current population (Crossover fraction).

-

(d)

The remaining children are produced by making random changes to a parent (Mutation).

-

(e)

The children of the current population form the next generation.

-

(a)

-

(iv)

The algorithm runs until one of the stopping criteria is met (e.g. maximum number of (stall) generations/time reached, average change in fitness function less than a certain value, certain fitness value reached)

For the Heston and Bates model we sample an initial population uniformly distributed between lower and upper bounds on the variables such that they satisfy the Feller condition. If parameter estimates from historical data are available these parameters may be included in the initial population. If the parameter estimates are based on a Markov Chain Monte Carlo method such that we get a posterior distribution for each parameter we may sample the initial population from the posterior distributions and the bounds on the parameters may be derived from the posterior distribution as well, e.g. as a quantile of the distribution.

We use a crossover method that creates children as a linear combination of two parents, i.e., that lie on the line containing the two parents. We may choose the child randomly on the line between the two parents or alternatively a small distance away from the parent with the better fitness value in the direction away from the parent with the worse fitness value. Note that for the Heston model if parent1 and parent2 with parameters satisfy the Feller condition for , then the Feller condition is also satisfied for a parameter set on the line between the two parents since

for .

For mutation we randomly generate directions that are adaptive with respect to the last successful or unsuccessful generation. A step length is chosen along each direction so that upper and lower bounds as well as the Feller constraint are satisfied.

3.3.2 Direct Search Method

After applying the GA with the purpose to locate a minimum in the specified bounds we use a pattern search algorithm to refine the result. We use complete polling to avoid local minima and only poll if the Feller constraint is satisfied.

3.4 Fitting for Piecewise Constant Parameters

For piecewise constant parameters we apply a bootstrapping method, i.e., after calibrating to one maturity we calibrate for the subsequent maturity, starting with the first maturity. We use as initial population for calibration the fitted parameters of the previous maturities.

If the calibration has to be done frequently, e.g. daily, we can achieve a fast recalibration by supplying additionally the parameters from the previous run as initial population for the new run (for the respective maturity).

3.5 Numerical Example

In this section we provide numerical results for fitting the Heston model. We consider an FX volatility surface for the Yen/Dollar exchange rate from 21/05/2008 with values for a given set of delta values . Since we need the volatility surface in terms of strikes, we transform into using

where denotes the standard normal cumulative distribution function. Moreover, for at the money options, we have to substitute the strike with the corresponding forward price. To obtain , we compute the option prices and retrieve the corresponding Black-Scholes model implied volatilities via a standard bisection method. For the computation of option prices we use the FFT as described in Section 3.2. We use since Schoutens et al. (2004) show in an empirical study that with this value prices are well replicated for many model parameters. The parameters and turned out to be a reasonable trade-off between accuracy and speed.

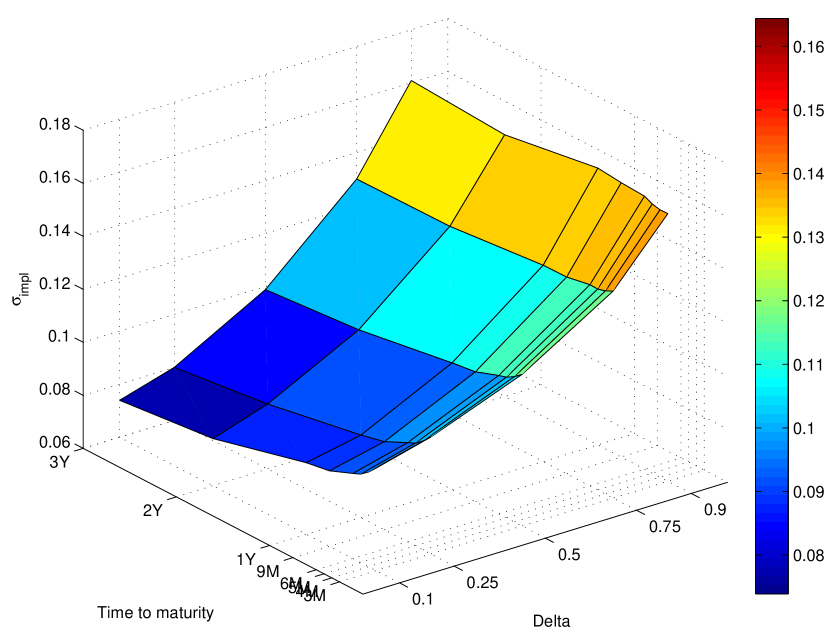

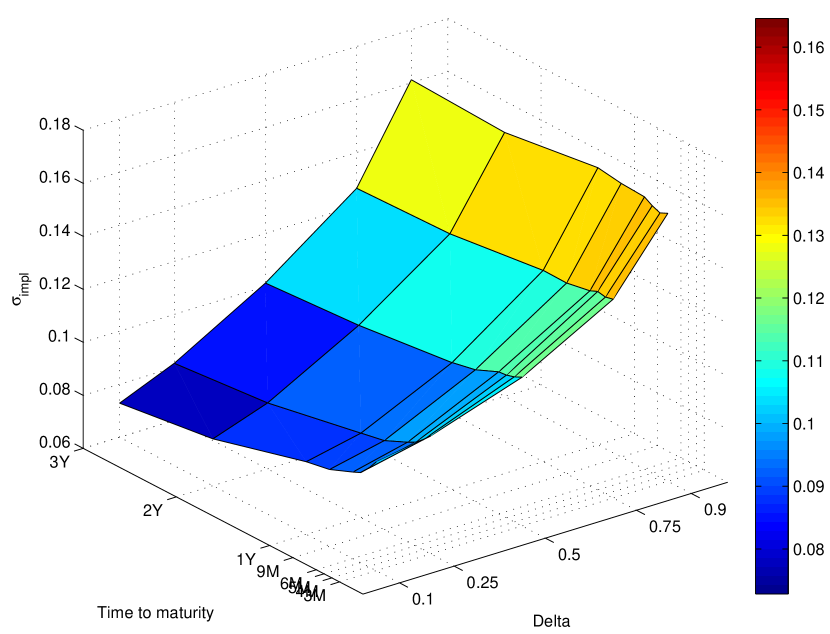

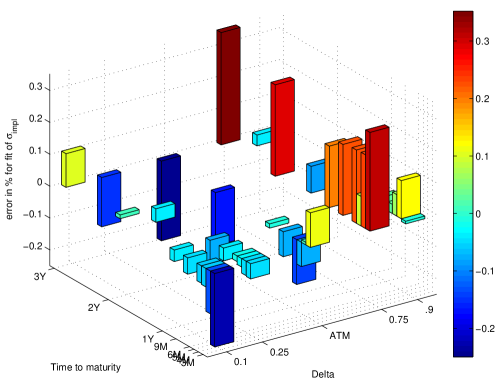

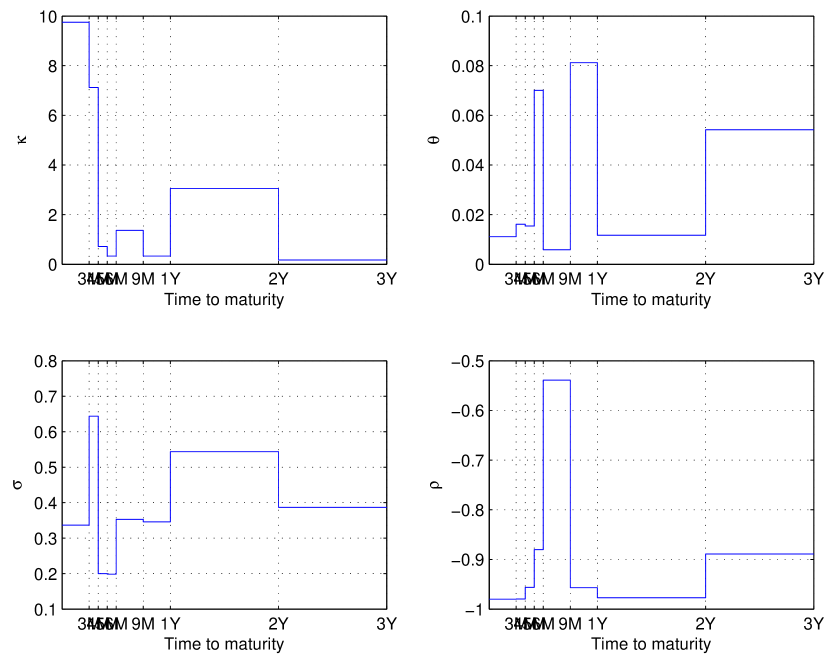

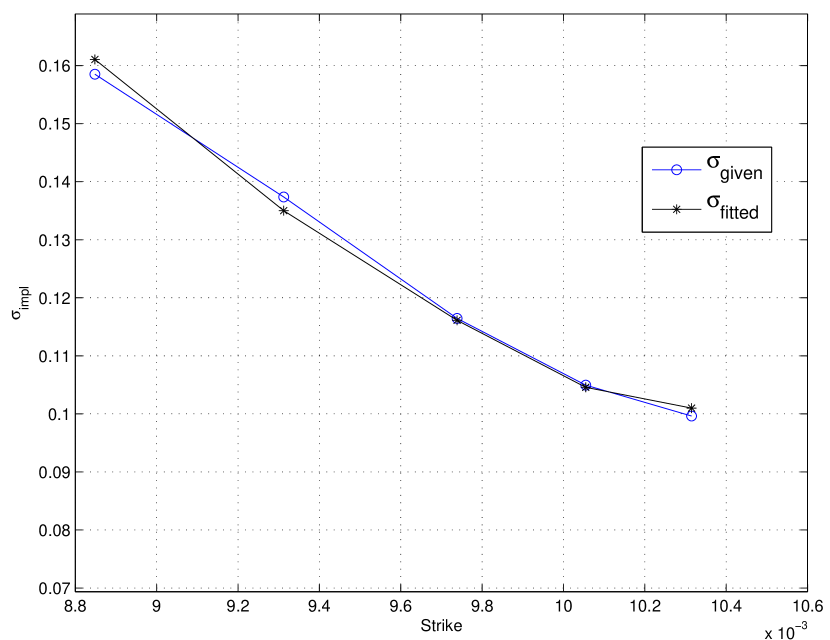

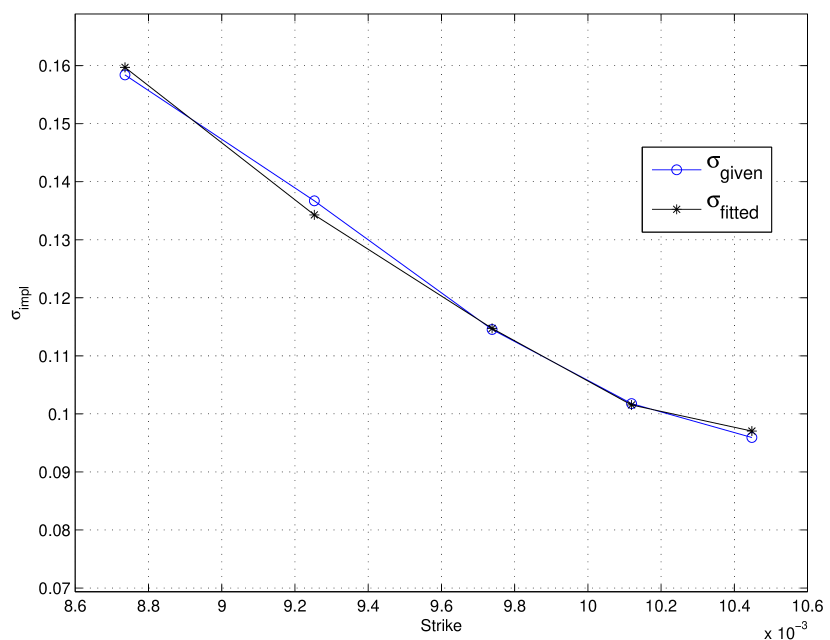

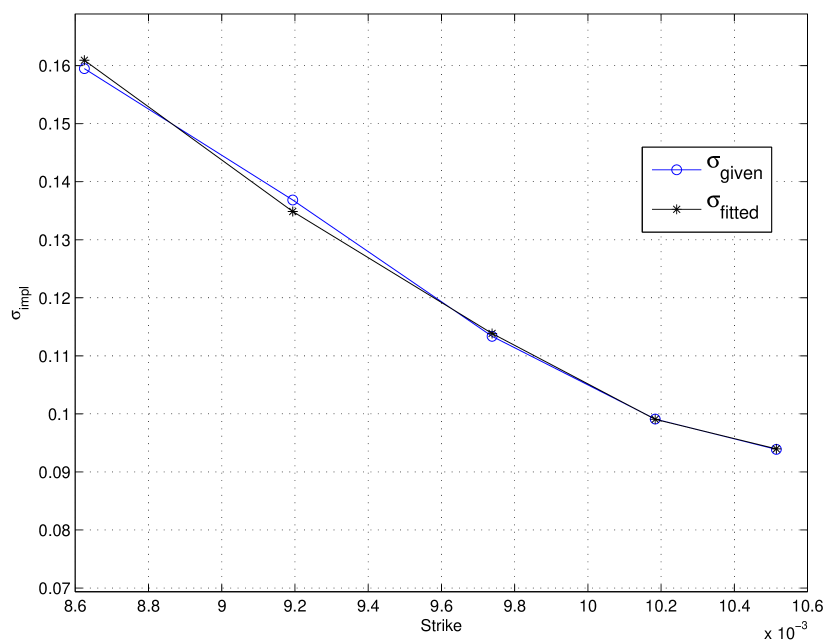

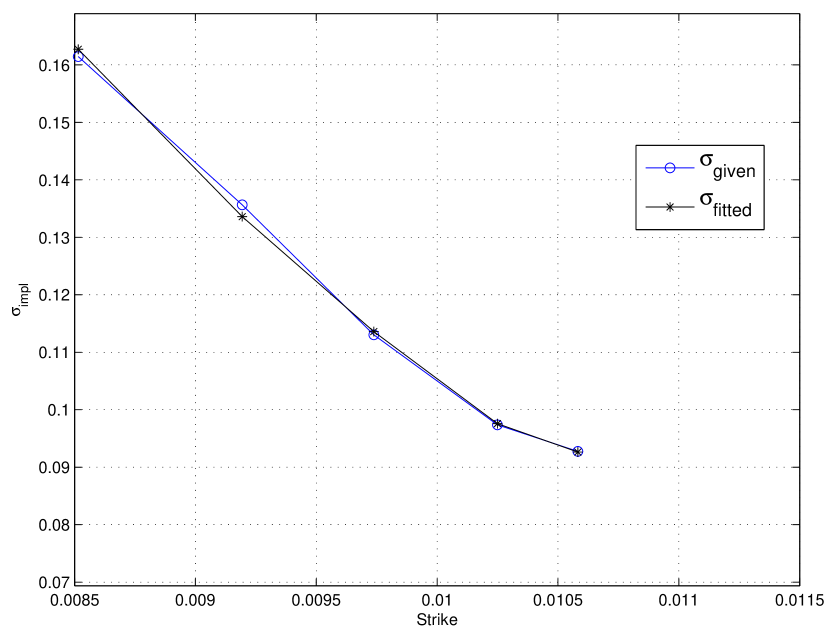

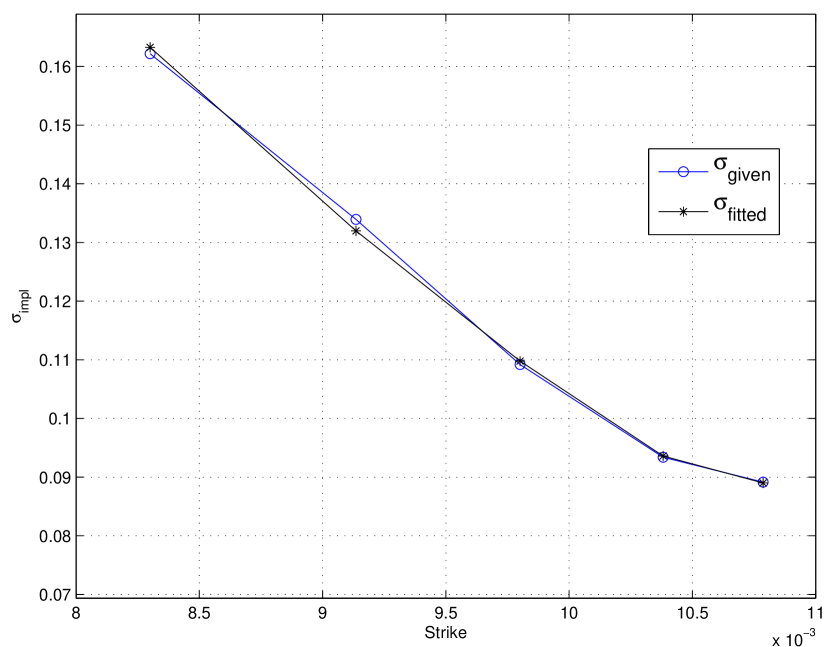

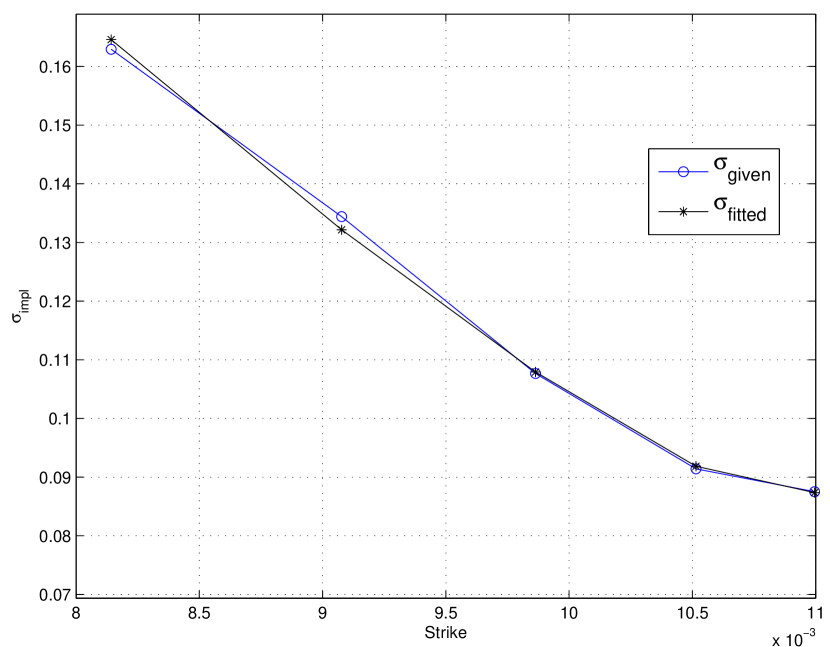

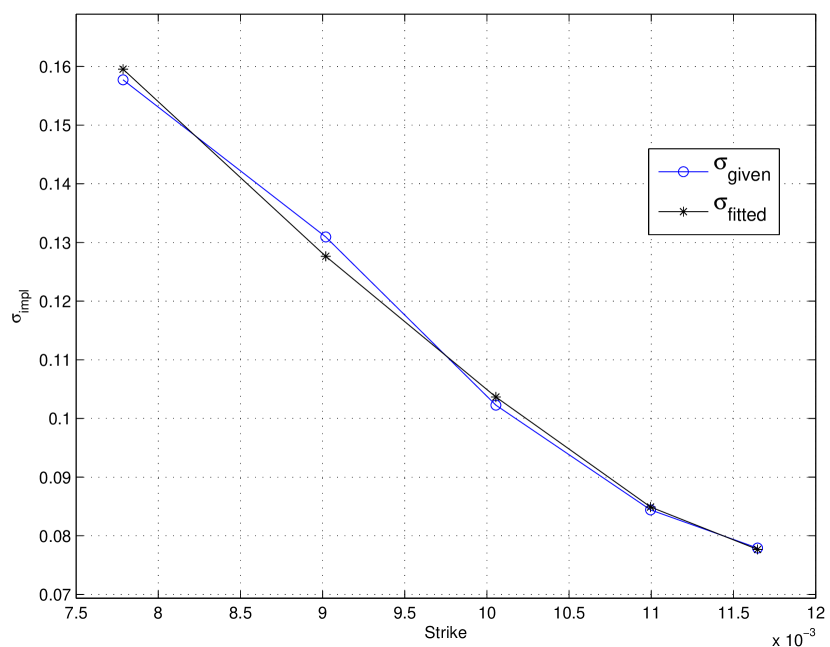

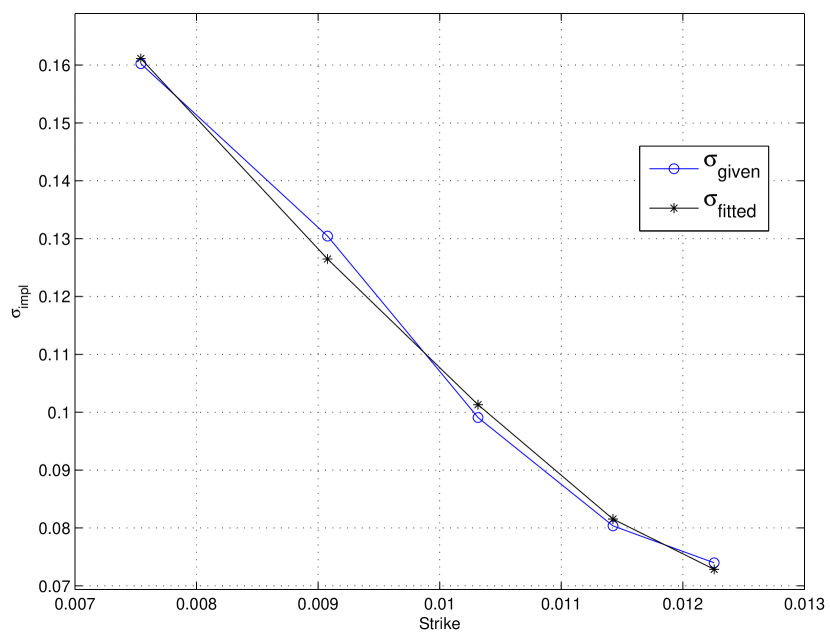

Figure 2 shows the given volatility surface quoted in terms of Deltas and Figure 2 is the surface produced by our fitted model. Figure 3 gives the difference between the quoted surface and the fitted surface. Figure 4 illustrates how the parameters evolve over time. Due due the fact that the calibration is an ill posed problem, i.e. the solution might not be unique and the parameters don’t depend continuously on the data, we see considerable jumps of the time dependent parameters. Figure 12–12 show the given smile and the fitted smile for the various maturities.

4 Conclusion and Outlook

We get a good fit of the given volatility surface for stochastic volatility models using piecewise constant parameters using a hybrid optimization algorithm and can use this fit to price exotic derivatives. We also note that the piecewise constant parameters may jump considerably. This is due to the fact the the calibration problem per se is ill posed giving evidence to the necessity of regularization techniques. If the posterior distribution from parameter estimation from historical data is available, we may apply regularization techniques. Further, the bounds for the parameters for the optimization algorithm could be derived from (quantiles of) the posterior distribution and also the initial population could be sampled from the posterior distribution.

References

- Aït-Sahalia and Kimmel [2007] Y. Aït-Sahalia and R. Kimmel. Maximum likelihood estimation of stochastic volatility models. J. Finan. Econ., 83(2):413–452, 2007.

- Albrecher et al. [2007] H. Albrecher, P. Mayer, W. Schoutens, and J. Tistaert. The Little Heston Trap. Wilmott Magazine, 2007.

- Bäck et al. [2000] T. Bäck, D.B. Fogel, and Z. Michalewicz. Evolutionary Computation 1. Institute of Physics Publishing, 2000.

- Barndorff-Nielsen and Shephard [2001] O.E. Barndorff-Nielsen and N. Shephard. Non-Gaussian Ornstein-Uhlenbeck-Based Models and Some of Their Uses in Financial Economics. J. Roy. Statistical Society, 63(2):167–241, 2001.

- Bates [1996] D.S. Bates. Jumps and stochastic volatility: exchange rate processes implicit in deutsche mark options. Rev. Finan. Stud., 9(1):69–107, 1996.

- Carr and Madan [1999] P. Carr and D. Madan. Option valuation using the FFT. J. Comp. Finance, 2:61–73, 1999.

- Carr et al. [2003] P. Carr, H. Geman, D. B. Madan, and M. Yor. Stochastic volatility for Lévy processes. Math. Finance, 13(3):345–382, 2003.

- Cont [2001] R. Cont. Empirical properties of asset returns: stylized facts and statistical issues. Quant. Finance, 1:223–236, 2001.

- Cont and Tankov [2004] R. Cont and P. Tankov. Financial Modelling with Jump Processes. Chapman & Hall/CRC, 2004.

- Elices [2007] A. Elices. Models with time-dependent parameters using transform methods: application to Heston’s model. Arxiv preprint arXiv:0708.2020, 2007.

- Frühwirth-Schnatter and Soegner [2007] S. Frühwirth-Schnatter and L. Soegner. Bayesian estimation of the heston stochastic volatility model. IFAS Research Paper Series 2007-29, 2007.

- Gallant and Tauchen [1996] A.R. Gallant and G. Tauchen. Which Moments to Match? Econometric Theory, 12(4):657–681, 1996.

- Gatheral [2006] J. Gatheral. The Volatility Surface: A Practitioner’s Guide. Wiley, 2006.

- Hamida and Cont [2005] S.B.E.N. Hamida and R. Cont. Recovering Volatility from Option Prices by Evolutionary Optimization. J. Comp. Finance, 8(4), 2005.

- Heston [1993] S.L. Heston. A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options. Rev. Finan. Stud., 6(2):327–343, 1993.

- Kahl and Jäckel [2005] C. Kahl and P. Jäckel. Not-so-complex logarithms in the Heston model. Wilmott Magazine, pages 94–103, 2005.

- Madan et al. [1998] D.B. Madan, P.P. Carr, and E.C. Chang. The Variance Gamma Process and Option Pricing. Europ. Finance Rev., 2(1):79–105, 1998.

- Mikhailov and Nögel [2003] S. Mikhailov and U. Nögel. Heston’s stochastic volatility model. Implementation, calibration and some extensions. Wilmott Magazine, pages 74–94, 2003.

- Schoutens et al. [2004] W. Schoutens, E. Simons, and J. Tistaert. A perfect calibration! Now what? Wilmott Magazine, 8, 2004.