Assessing uncertainty in the American

Indian Trust Fund

Abstract

Fiscal year-end balances of the Individual Indian Money System (a part of the Indian Trust) were constructed from data related to money collected in the system and disbursed by the system from 1887 to 2007. The data set of fiscal year accounting information had a high proportion of missing values, and much of the available data did not satisfy basic accounting relationships. Instead of just calculating a single estimate and arguing to the Court that the assumptions needed for the computation were reasonable, a distribution of calculated balances was developed using multiple imputation and time series models. These provided information to assess the uncertainty of the estimate due to missing and questionable data.

doi:

10.1214/09-AOAS274keywords:

.T1Work performed under Department of the Interior, Minerals Management Service contract number GS-10F-0033M, 62817.

, and

1 Introduction

Starting in the later part of the 19th century, the U.S. Department of the Interior has administered accounts of funds held in trust for Indian tribes within Tribal Trust accounts, and for individual Indians within Individual Indian Money (IIM) accounts. The funds in the accounts derive from diverse sources such as funds from litigation judgments or settlements and funds derived from revenue producing activity on lands. There have been numerous criticisms of the Interior’s management of the trust fund system over the years. In 1994 Congress enacted the American Indian Trust Fund Management Reform Act (Pub. L. No. 103–412, 108 Stat. 4239) requiring the Interior to account for the balances of funds in these accounts.

In June of 1996, a class action lawsuit was filed in the U.S. District Court for the District of Columbia seeking to compel a historical accounting of Individual Indian Money (IIM) accounts. The case is complex, and has been in litigation for over 13 years. We will not attempt to summarize all the events that have occurred, but Court filings and hearing transcripts can be found at the Department of Justice website dedicated to thecase, http://www.usdoj.gov/civil/cases/cobell/index.htm, as wellas the Plaintiffs’ website, http://www.indiantrust.com/. Additionally,http://indianz.com has many news items on the case.

The event associated with the case that is relevant to the statistical problem that is the focus of this paper is the outcome of an October 2007 trial held to evaluate the Interior’s progress toward completing its historical accounting for IIM accounts. In its January 2008 findings of the October trial, the Court held that a historical accounting of IIM accounts was impossible given the level of Congressional funding, and concluded “that a remedy must be found for the Department [of the Interior’s] unrepaired, and irreparable, breach of its fiduciary duty over the last century.” In subsequent hearings, the Court described the remedy as determining “monies that were in fact collected and made it into Treasury—into trust funds in some way, but have not been adequately accounted for” (March 5, 2008 Transcript of Status Conference before the Honorable James Robertson United States District Judge).

As the statistical contractor for the Department of the Interior Office of Historical Trust Accounting (OHTA), our approach to the problem was to try to limit modeling assumptions and let the available data speak for themselves. Instead of just calculating a single estimate and arguing to the Court that the assumptions needed for the computation were reasonable, a distribution of calculated balances was developed to assess the uncertainty of the estimate due to missing and questionable data.

2 Understanding the data

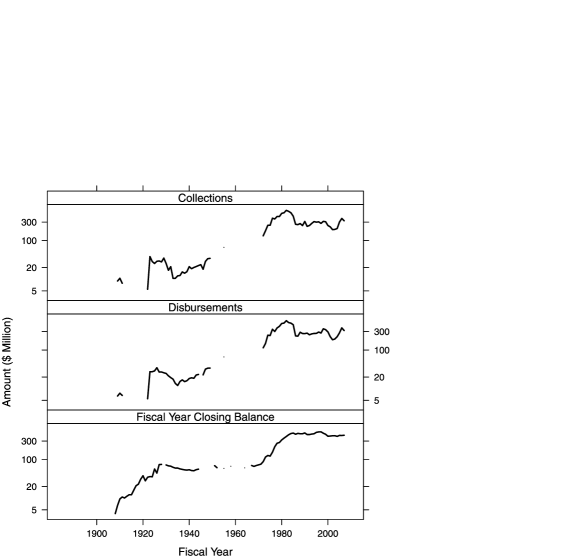

An Excel spreadsheet of the data that were used in our analysis of the aggregate IIM System balance is available for download at http://www.norc.org/iim. These include annual IIM System collections, disbursements and balance data obtained by OHTA contractors from IIM System government reports, and Osage headright222A “headright” is the right to receive a quarterly distribution of funds derived from the Osage Mineral Estate, which is the oil, gas and other mineral subsurface of the approximately 1.47 million acre Osage Reservation. data obtained from the Osage Nation website. The historical IIM System accounting data provide a basis for analyzing IIM System information to see if there were monies that were “not adequately accounted for.” Figure 1 is a graphical display of key system accounting variables—collections, disbursements and balance data—over the time period of interest (1887–2007). It is evident visually that a large proportion of data are missing, and there appears also to be some questionable observations.

The Court’s view is that the issue “is about dollars into the IIM, dollars in and dollars out” (April 28, 2008 Transcript of Status Conference Before the Honorable James Robertson, United States District Judge, 115 at 18). Thus, collections–dollars in and disbursements–dollars out are two key variables, but they have a large amount of missing information.

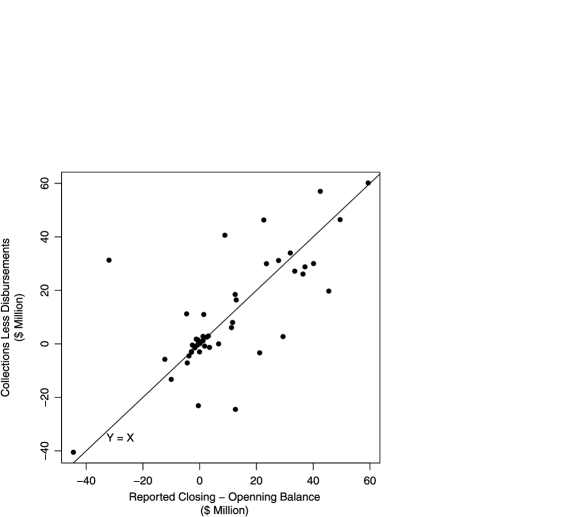

A close look at the data also reveals that for years after 1911 and before 1996, where collections, disbursements and balance data are available, values do not “foot,” that is, the opening balance (prior fiscal year ending balance) plus collections less disbursements does not equal the ending balance. Figure 2 is a graphical depiction of this: the difference between yearly collections less disbursements is plotted against the yearly change in balance (closing less opening balance). If the data do foot, all the plotted points would lie on the line. But this is generally not true for these data. There may be legitimate reasons why the numbers do not foot, for example, collections and disbursements values come from different types of government reports than do balance values; government reports are created for different purposes and perhaps at different time periods. Even so, Figure 2 lends credence to the Court’s notion that there may be uncertainty in the accounting of IIM System funds.

While these data have their weaknesses, they are the only IIM System data available for determining an estimate of how much of the System funds may be “not adequately accounted for.” We decided that a two-step approach was needed to fully assess the uncertainties exhibited in these data: (1) an imputation modeling step to assess the uncertainty due to missing data, and (2) a synthetic modeling step to assess the uncertainty due to accounting irregularities, which we refer to as government reporting uncertainties.

3 Multiple imputation modeling

After considering imputation modeling alternatives, we decided that multiple imputation [Rubin (1987)] was applicable for this accounting application even if its reported weaknesses [Binder (1996), Fay (1996)] were such that the methodology would lead to an overstatement of the uncertainty; an outcome favorable to the Plaintiffs. The government, when informed that there was such a risk, accepted our approach as the best of available options.

Multiple imputation replaces each missing value with a set of plausible values. The distribution of these “plausibles” gives us a way to represent the uncertainty about the right value to impute. Each completed multiply imputed data set can be analyzed using standard procedures for complete data, and the results across these analyses combined, so that all the uncertainty components in the analysis—model uncertainty and missing value uncertainty—are accounted for in the analysis.

General advice is to include (within reason) as many variables as you can in the multiple imputation model. This includes variables that are potentially related to both the imputed variables and the missingness of the imputed variables [Schafer (1997)]. The Osage headright variable is related to the economic conditions that existed over time in Indian Country, and it is known for the whole time period of interest, so we included it in our analysis. In terms of variables that are potentially related to the missingness of the imputed variables, we conducted diagnostic modeling of the probability of a missing collections or disbursements value. The diagnostics indicate that fiscal year, Osage headright and balance are all potentially related to the missingness of collections and disbursements [Pramanik (2008)].

A number of other variables, for example, the portion of the balance invested in government securities, were also available for a small portion of the time period of interest. These data were considered, but, ultimately, not included in our analysis. Having too many variables with a considerable number of values missing—in fact, more missing values than for the two variables of primary interest—might have made it harder to construct a credible imputation model. In the end, therefore, we proceeded with developing an imputation model based only on fiscal year, Osage headright, balance, collections and disbursements.

We assumed that the data are from a continuous multivariate distribution and contain missing values that can occur for any of the variables. Furthermore, the missing values are assumed to be missing at random [MAR, Rubin (1976)], so that the probability that an observation is missing can depend on observed values (), but not on missing values (). The effect of assuming that the missingness is entirely MAR, as is typical in most settings [Scheuren (2005a)], is to introduce some uncertainty in the measurement of the uncertainty. For missing completely at random (MCAR), using an MAR model would tend to lead to some overstatement of the uncertainty but probably not much, assuming the variables chosen to do the imputations are related to the variables that are missing. For nonignorable, not missing at random (NMAR) missingness we cannot speculate, in general, about the nature and size of any effects that may arise. All three types are conceptually possible in any given setting, that is, they can all be present [e.g., Scheuren (2005b)]. However, given our belief that NMAR missingness is minimal likely for our set of historical data, the impacts cannot be large.

A good robust multivariate model for use with multiple imputation is the multivariate normal model with a noninformative prior [Schafer (1997)]. The complete-data posteriors, which are used to generate imputations, are

where denotes the inverse Wishart distribution, is the completed data matrix (which is composed of the observed values, , and the filled-in missing values, ), is a row in the data matrix, is the number of years in the data matrix to be completed,333The starting data matrix has 128 rows; one for each year in the 1880–2007 timeframe, but the focus of our analysis is for the 1887–2007 timeframe, which is 121 years. Because of the time series modeling described in Section 4 of this paper, we needed to go back to 1880 in order to forecast values starting in 1887. is the sample covariance matrix, is the sample mean vector, and denotes the multivariate normal distribution.

The imputation of the missing annual collections, disbursements and balance values for the IIM System was completed using the SAS MI procedure, which uses an MCMC algorithm to generate observations from the posterior distribution. The SAS program that implements this can be found at http://www.norc.org/iim. The imputation of each missing collections, disbursements and balance value was done 10,000 times.

The multiple imputation literature, written 30 years ago during an era of expensive computing, generally suggests that 3-to-5 imputations would be sufficient for assessing the contribution to an estimated value’s uncertainty due to missing information. The theory behind this relies on the use of a multivariate normal distribution, which is also the basis for our imputation modeling. Since we live in an era of less expensive computing, we chose to use a much larger number of imputations, 10,000. Our computing power was sufficient for this many imputations, and our data matrix was not so large that it would have taken an inordinate amount of time to complete the imputation process.

4 Synthetic modeling for addressing the uncertainty inherent in available data

The footing errors for the available data from 1908–1995 (see Figure 2), and under-reporting issues for the 1922–1949 collections and disbursements data,444Collections and disbursements values from 1922–1949 came from “Statement of Money Received and Expended by Disbursing Agents of the Indian Service Without being Paid into General Treasury of the United States” reports. Thus, we know that monies held within the Treasury were not accounted for in these reports. lead us to conclude that the pre-1996 data are questionable. Therefore, we feel that the results of our analysis should reflect more uncertainty than if all the data used for modeling were thought to be reliable.

To introduce this uncertainty into the data so that it would be reflected in the confidence bounds, we first fit a model to all the annual data (1880–2007) for each of the 10,000 imputed data sets. We then created a realization from each model for the years in question (1887–1995), which included a random noise component. This provided us with 10,000 “synthetic” data sets. We use the term “synthetic” here because the processing steps we have used are similar to the creation of synthetic data, as described by Reiter (2002). As noted by Rubin (1993), the result of using this type of modeling approach will still produce valid statistical inference, but the variance will be larger than the variance from the original data “because there is a reduction in information relative to the actual microdata”

Given that we have annual accounting observations in each of our 10,000 complete data sets, a natural way to model the data is through time series techniques. At this point it is important to recall that our goal is to estimate the 2007 year-end balance by estimating total collections and total disbursements over the time period 1887–2007, and then taking the difference between the total collections and total disbursements. Therefore, we restricted out attention to just the collections and disbursements variables.

In using time series techniques for modeling these data, we must not only take into account the serial correlation within each of the collections and disbursements series, we must also take into account the cross-correlation between the two variables—both contemporaneous and prior value correlations. Vector autoregressive moving average (VARMA) processes are a class of models that handle such correlation structures. Following Brockwell and Davis (1987), is a bivariate VARMA() process if is stationary and

where and are series of bivariate vectors, is a bivariate constant (mean) vector, and are matrices, and , a bivariate white-noise process with common covariance matrix .

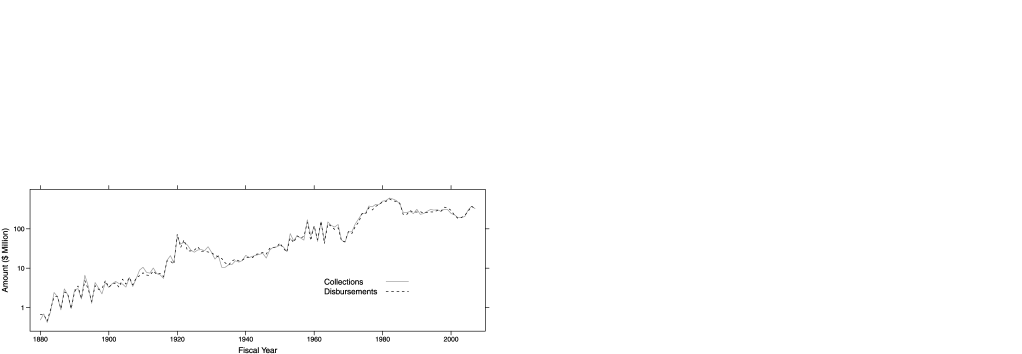

A basic assumption for this type of model is that the time series process is stationary. Figure 3 shows time series plots the log transformed collections and disbursements data for one of the 10,000 bivariate time series generated from the multiple imputation process. It is plausible that log collections and log disbursements time series are stationary, or stationary after removing an increasing trend over time, and we proceeded to fit VARMA models to the transformed series, that is, (Collections) and (Disbursements) for years .

For each of the 10,000 bivariate time series, we need to estimate the unknown coefficients , and , and then use the fitted model to create a different realization from the time series model. It would have been overly time consuming to check for stationarity and fit the “best” VARMA model to each of the 10,000 time series produced from the multiple imputation procedure. So we checked a small set time series from the 10,000, and ran some high level diagnostics on a larger subset.

We checked the small subset of times series using the tentative order identification routines found in Spliid (1983), Koreisha and Pukkila (1989), Quinn (1980), which are based on identifying the and orders that minimized a statistical information criterion. A VAR process with order between 2 and 5 was consistently identified as the VARMA process that produced the minimum AICC value. In order to produce realizations of a VAR() model for the time period of interest (1887–1995), we needed to have the starting time series go back further in time (before 1887) by years. Of the data available to us before we started the multiple imputation process, the Osage data went back furthest in time to 1880. So, we had 7 years of available data that predated the time period of interest. Therefore, the highest order value we could choose that would not predate our available data was = 7. We settled on fitting a VAR(7) process to each of the 10,000 series. We used the VAR models fit to each series to generate synthetic collections and disbursements values for each fiscal year in the 1887–1995 time period. The SAS program found at http://www.norc.org/iim provides the details of how this was implemented.

Figure 4 shows the mean value of collections for each fiscal year of the 10,000 values assigned to the year from the modeling process, and 95 percent confidence intervals are shaded in two ways to provide a visual of the uncertainty of the collections values. The lighter shading shows the variation of the imputed values from the initial multiple imputation modeling. The darker shading shows the additional variation added to the collections values due to the reporting uncertainty. We see the largest amount of variation present in the time periods where collections values were missing. For time periods with questionable reported data, a relatively small amount of variation has been added for fiscal years immediately preceding 1996, but the additional variation due to reporting uncertainty gets larger as we go further back in time. Similar features are found in an analogous graph of disbursements (not shown).

For each completed data matrix, total collections and total disbursements across the 121-year period between 1887 and 2007 were calculated. The difference between these two values, which we will refer to as the “calculated balance,” was found for each of the 10,000 completed data matrices. The calculated balance distribution is fairly symmetric about the median value of $580.4. The 25th and 75th percentiles of the distribution are $502.0 million and $661.7 million, respectively.

5 Discussion

We developed a methodology for estimating the 2007 fiscal year-end balance of the IIM System based on estimating the total amount of money collected in the system and disbursed by the system from 1887 to 2007. Because the available annual collections and disbursements data were not available for about one-third of the years in the time frame, we used a multiple imputation methodology to fill-in the missing values. Additionally, many of the reported collections and disbursements values exhibited questionable behavior, and in some cases were known to be underreported. Therefore, our approach for determining the balance for the 1887–2007 time frame concentrated on assessing the distribution of possible balance values, which provides an evaluation of the uncertainty of the estimated balance due to missing information and reporting uncertainty in the available data.

Our final assessment is that the calculated balance for the 1887–2007 time frame has an average value of $583.6 million, which is $159.9 million higher than the stated 2007 balance of $423.7 million. However, the distribution of the calculated balances has large variation, as exhibited by a 95 percent confidence interval that ranges from a lower bound of $353.1 million to an upper bound of $833.5 million.

The calculated balance distribution does not reflect any inflation or interest adjustment on the dollar amounts. The Court ruled that it could not award interest in the U.S. District Court. Generally, only the Court of Federal Claims may award interest in a suit against the Government.555This is a legal issue that is not simple to explain. We refer the interested reader to the August 7 2008, United States District Court for The District Of Columbia, Cobell v. Kempthorne Memorandum, which can be found at http://www.usdoj.gov/civil/cases/ cobell/index.htm.

The uncertainty reflected in the distribution of the calculated balance is a result of the government’s inability to find a consistent set of documents that shows the IIM system balances over the time frame of interest. In other such circumstances, the government compensates those on whom uncertainty is imposed by choosing a point on the distribution favorable to the other party. For example, the Internal Revenue Service666IRS Internal Revenue Manual, 4.47.3.3.1. uses the 95th percentile of the distribution, which means that the taxpayer or person being audited is 95% sure of not overpaying. DHHS777DHHS Centers for Medicare and Medicaid Services, Program Integrity Manual, Section 3.10.5.1. uses the 90th percentile in similar circumstances, which is slightly less favorable to those being audited.

In its August 8, 2008 memorandum following the June 2008 Cobell v. Kempthorne trial, the Court found that our model (the government’s model) was imperfect, but that it presented “a plausible estimate of funds withheld,” and that it was “useful in evaluating the uncertainty in the existing trust data,” particularly the “overall uncertainty at the balance level.”

The Court chose to use the 99 percentile of the calculated balance distribution, $879.3 million, as a point on the distribution favorable to the plaintiffs. This more conservative limit was chosen because “there is more uncertainty in the data historical reports are not biased but may be understated, [Integrated Records Management System] data has important reliability problems, and the qualified audit data is, after all, only qualified, and was not even subjected to the time-series remodeling step.” Adjusting for the stated fiscal year-end IIM system balance of $423.7 million produces a $ 455.6 million understatement of the system balance, which was awarded to the Plaintiffs.888Plaintiffs have appealed this decision. In particular, the Plaintiffs argue that the judgment should include interest because the government benefited over the years from having extra money in the US Treasury. If the Appeals Court rules in the Plaintiffs’ favor on the interest issue, an interest-adjusted, calculated balance distribution can be derived by applying agreed-upon annual interest rates to each of the 10,000 time series.

6 Alternate modeling approaches

The timeline we were given to complete the analysis of the IIM System data was short. While we believe that the uncertainty modeling presented to the court was appropriate, hindsight suggests a number of competing models. For example, we did not include a trend term in the time series model. Even though the diagnostic checks we performed suggested that a VAR(7) model was a reasonable choice, Figure 3 suggests an increasing trend over time. We have rerun the model with a linear time trend, and have found that the distribution of calculated balances does not change appreciably. But, another alternative that we have not investigated is to use differencing of the collections and disbursement data to remove trends.

Given that the multiple imputation modeling is a Bayesian hierarchical model, maybe we should have used a Bayesian vector autoregressive model [BVAR Litterman (1986), Brandt and Freeman (2006)] to incorporate the additional uncertainty in the calculated balance distribution. But it is not clear to us that this was needed. The validity of multiple imputation does not require one to fully subscribe to the Bayesian paradigm [Rubin (1987)], so it is not clear that we needed to use a Bayesian model for the second stage. We have also questioned whether the two-step model should have been completed in one modeling process. A BVAR could be included in the multiple imputation hierarchical model, possibly along with a measurement error model [Ghosh, Sinha and Kim (2006)] for the collections and disbursement observation. We have not yet attempted this.

We encourage others to explore these data and suggest ways in which they can be analyzed. The data set, as noted, is available for download at http://www.norc.org/iim. We would be interested to know if other modelers using all of the available data, plus perhaps additional economic indicators, provide estimates that are consistent with our own.

Supplement A \stitleData Set \slink[doi]10.1214/09-AOAS274SUPPA \slink[url]http://lib.stat.cmu.edu/aoas/274/Supp%20A%20-%20IIM%20System%20Uncertainty%20Modeling%20Data.xls \sdescriptionThe data set (IIMSystemUncertaintyModelingData.xls) is available for download at http://www.norc.org/iim. \sdatatype.xls {supplement} \snameSupplement B \stitleSAS Code \slink[doi]10.1214/09-AOAS274SUPPB \slink[url]http://lib.stat.cmu.edu/aoas/274/Supp%20B%20-%20IIM%20System%20Uncertainty%20model.sas \sdescriptionThe SAS program that we used to read the input data, apply the modeling methodologies, and produce the outputs used in summaries and graphs is available at http://www.norc.org/iim. \sdatatype.xls

References

- Binder (1996) Binder, D. A. (1996). On variance estimation with imputed survey data: Comment. J. Amer. Statist. Assoc. 91 510–512.

- Brandt and Freeman (2006) Brandt, P. T. and Freeman J. R. (2006). Advances in Bayesian time series modeling and the study of politics: Theory testing, forecasting, and policy analysis. Political Analysis 14 1–36.

- Brockwell and Davis (1987) Brockwell, P. J. and Davis, R. A. (1987). Times Series: Theory and Methods. Springer Series in Statistics. Springer, New York. \MR0868859

- Cleveland (1993) Cleveland, W. S. (1993). Visualizing Data. Hobart Press, Summit, NJ.

- Fay (1996) Fay, R. E. (1996). Alternative paradigms for the analysis of imputed survey data. J. Amer. Statist. Assoc. 91 490–498.

- Ghosh, Sinha and Kim (2006) Ghosh, M., Sinha, K. and Kim, D. (2006). Empirical and hierarchical Bayesian estimation in finite population sampling under structural measurement error models. Scand. J. Statist. 33 591–608. \MR2298067

- Koreisha and Pukkila (1989) Koreisha, S. and Pukkila, T. (1989). Fast linear estimation methods for vector autoregressive moving average models. J. Time Ser. Anal. 10 325–339. \MR1038466

- Litterman (1986) Litterman, R. B. (1986). Forecasting with Bayesian vector autoregressions: Five years of experience. J. Bus. Econom. Statist. 4 25–38.

- Mulrow, Shin, and Scheuren (2009a) Mulrow, E., Shin, H. and Scheuren, F. (2009a). Supplement A to “Assessing uncertainty in the American Indian Trust Fund.” DOI: 10.1214/09-AOAS274SUPPA.

- Mulrow, Shin, and Scheuren (2009b) Mulrow, E., Shin, H. and Scheuren, F. (2009b). Supplement B to “Assessing uncertainty in the American Indian Trust Fund.” DOI: 10.1214/09-AOAS274SUPPB.

- Pramanik (2008) Pramanik, S. (2008). Examining the role of balance in the missingness of collections and disbursements in the historical IIM system accounting data. In NORC Memorandum.

- Quinn (1980) Quinn, B. G. (1980). Order determination for a multivariate autoregression. J. Roy. Statist. Soc. Ser. B 42 182–185. \MR0583353

- Reiter (2002) Reiter, J. P. (2002). Satisfying disclosure restrictions with synthetic data sets. Journal of Official Statistics 18 531–544.

- Rubin (1976) Rubin, D. B. (1976). Inference and missing data. Biometrika 63 581–592. \MR0455196

- Rubin (1987) Rubin, D. B. (1987). Multiple Imputation for Nonresponse in Surveys. Wiley, New York. \MR0899519

- Rubin (1993) Rubin, D. B. (1993). Discussion: Statistical disclosure limitation. Journal of Official Statistics 9 462–468.

- Schafer (1997) Schafer, J. L. (1997). Analysis of Incomplete Multivariate Data. Chapman & Hall, New York. \MR1692799

- Scheuren (2005a) Scheuren, F. (2005a). Multiple imputation: How it began and continues. Amer. Statist. 59 315–319. \MR2196356

- Scheuren (2005b) Scheuren, F. (2005b). Seven model motivated rules of thumb or equations. In Presentation at NISS Affiliates Workshop on Total Survey Error. Available at http://www.niss.org/sites/default/files/Scheuren.pdf.

- Spliid (1983) Spliid, H. (1983). A fast estimation for the vector autoregressive moving average models with exogenous variables. J. Amer. Statist. Assoc. 78 843–849. \MR0727569