Optimal Timing to Purchase Options

Abstract

We study the optimal timing of derivative purchases in incomplete markets. In our model, an investor attempts to maximize the spread between her model price and the offered market price through optimally timing her purchase. Both the investor and the market value the options by risk-neutral expectations but under different equivalent martingale measures representing different market views. The structure of the resulting optimal stopping problem depends on the interaction between the respective market price of risk and the option payoff. In particular, a crucial role is played by the delayed purchase premium that is related to the stochastic bracket between the market price and the buyer’s risk premia. Explicit characterization of the purchase timing is given for two representative classes of Markovian models: (i) defaultable equity models with local intensity; (ii) diffusion stochastic volatility models. Several numerical examples are presented to illustrate the results. Our model is also applicable to the optimal rolling of long-dated options and sequential buying and selling of options.

Keywords: optimal stopping, delayed purchase premium, martingale measures, risk premia

1 Introduction

In most financial markets, one fundamental problem for investors is to decide when to buy a derivative at its current trading price. A potential buyer has the option to acquire the derivative immediately, or wait for a (possibly) better deal later. Naturally, the optimal timing for the derivative purchase involves comparing the buyer’s subjective price and the prevailing trading price, which directly depend on the price of the underlying asset and the market views of the buyer and the market.

The majority of option pricing literature is concerned with sell-side perspective and focuses on hedging of options. In this view, the derivative contract is already given and the goal is to efficiently price it and then hedge it to monetize the transaction value with zero (or rather minimal) risk. In contrast, from a buy-side perspective (that of hedge fund managers, proprietary traders, etc.), the aim is to extract profit by finding mispriced contracts in the market. Portfolio managers will survey the entire traded derivative landscape to find options that from their view are improperly priced. They will then try to exploit this mismatch to make profit. Similarly, for over-the-counter (OTC) derivatives that are traded bilaterally off the exchange, the manager will look for a counterparty that offers an attractive price.

Consequently, two key aspects emerge. First, the market is naturally assumed to be incomplete. Indeed, by the standard no-arbitrage pricing theory, the price of a derivative is given by the expected discounted payoff under some equivalent martingale measure, also known as the risk-neutral pricing measure. If the market is arbitrage-free and complete, there is only one pricing measure, and no “mispricing” is possible. However, when the market is incomplete, there exist many candidate equivalent martingale measures that will yield no-arbitrage prices. Derivative buyers and sellers with different pricing measures (or market views) will assign different prices to derivatives over time. Therefore, the buyer’s (resp. seller’s) objective is to take advantage of the price discrepancy and optimally purchase (resp. sell) a contingent claim given the knowledge of the trading prices. Second, optimal timing of trades is necessary to extract maximum profit. Indeed, even if a mispricing exists today, it is not clear whether it should be immediately exploited or rather one should wait for an even larger mispricing in the future. Thus, the time-dynamics of prices under different measures become crucial.

In this paper, we study the optimal purchasing decision from the perspective of a derivative buyer. This leads to the analysis of a number of optimal stopping problems over a finite horizon. As is common in the literature, these problems do not admit closed-form solutions, so our focus is to analyze the corresponding probabilistic representations and variational inequalities, and illustrate the optimal purchasing strategies through numerical examples. For instance, using a martingale argument, we can deduce whether the buyer will purchase immediately or never purchase based on the pricing measures used and the contract type (e.g. a Put or Call), and determine what factors accelerate or delay the purchasing decision. We also introduce the idea of the delayed purchase premium to provide alternative mathematical and financial explanations to the buyer’s purchase timing. We show that this delayed purchase premium is closely related to the stochastic bracket between the market price and the state price deflator, and it provides a connection between the families of martingale measures and the properties of contract prices.

For buying American options, the buyer faces a two-stage optimal stopping problem, in which the purchase date is first selected, followed by an option exercise date. We find that the delayed purchase premium for an American option has a direct connection with its early exercise premium (Carr et al., 1992). In the case of buying perpetual American Puts under a defaultable stock model, we give explicit solutions for the option prices, the buyer’s value function, as well as the optimal purchase and exercise thresholds.

In incomplete markets, there are many candidate risk-neutral pricing measures that will yield no-arbitrage prices. Some well-known examples include the minimal martingale measure (Föllmer and Schweizer, 1990), the minimal entropy martingale measure (Fujiwara and Miyahara, 2003; Fritelli, 2000), and the -optimal martingale measure (Hobson, 2004). In most practical models of incomplete markets, the various pricing measures are parameterized through the market price of risk of some nontraded factor. For the derivative purchase problem, it is then important to understand the dependence of prices on market price of risk, as well as the evolution of market price of risk over time. Two representative setups we will discuss below include (i) equity models subject to default risk and (ii) stochastic volatility models with volatility driven by a second stochastic factor. In models of type (i), we will be concerned with market price of default risk; in models of type (ii) with market price of volatility risk.

To our knowledge, the purchase timing problem considered herein is new in the mathematical finance literature. As explained above, it links together the extensive body of research on representations of equivalent martingale measures in incomplete markets and the continuous-time optimal stopping models. We also draw upon results comparing option prices under different pricing measures, such as Romano and Touzi (1997); Henderson et al. (2005). Some existing work similar in flavor to ours includes study of optimal static-dynamic hedges (Leung and Sircar, 2009) and quasi-static hedging (Allen and Padovani, 2002). Finally, in a recent series of papers, Peskir and Samee (2008) and Peskir et al. (2009) proposed a new financial engineering contract termed British options. In those works the classical complete Black-Scholes market is considered and the payoff upon exercise can be viewed as the undiscounted price of the claim under the “contract” (and non-martingale) measure .

The rest of the paper is organized as follows. In Section 2, we setup our mathematical model and the main structural results. In Section 3, we consider optimal timing of purchases for derivatives written on defaultable stocks, while in Section 4 we consider buying options on stocks with stochastic volatility. Finally, Section 5 concludes and points out related problems where our analysis can also be applied.

2 Problem Overview

In the background, we fix an investment horizon with a finite terminal time , which is chosen to coincide with the expiration date of all securities in our model. We assume a probability space equipped with a filtration , which satisfies the usual conditions of right continuity and completeness.

The financial market consists of one risky asset and the riskless money market account with a constant interest rate . For the purpose of presenting the main ideas in this section, we work with a general incomplete market, where the price process is a càdlàg, locally bounded -semimartingale. Our detailed analysis of the problem will be conducted under two specific market models, namely, (i) a defaultable stock model where is a geometric Brownian motion up to an exogenous default time (in Section 3), and (ii) a diffusion stochastic volatility model (in Section 4). We assume that all market participants have access to the same information, encoded in . It is possible, though beyond the scope of this paper, to introduce price discrepancies due to incomplete information via filtration enlargement/shrinkage (see e.g. Guo et al. (2009) and El Karoui et al. (2010)).

Let us consider a buyer of a European-style option written on underlying with some payoff function at expiration date . As is standard in no-arbitrage pricing theory, the market price of a derivative is computed according to some pricing measure, or equivalent martingale measure (EMM), , which does not lead to arbitrage opportunities. Therefore, we consider the trading price process for the option , denoted by , as given by

| (1) |

The buyer may view the market as a representative agent (the seller), who sells option at the ask price for . Depending on the setup, this option may or may not be liquidly traded. Unless the market is complete, there exists more than one no-arbitrage pricing measure. Hence, we assume that the buyer computes her own mark-to-model price of the option under another pricing measure , namely,

| (2) |

In many parametric market models, the pricing measure is directly linked to the risk premia assigned to the underlying sources of risk. This provides a natural explanation to the difference in pricing measures and derivative prices between the buyer and the market (or among market participants in general).

2.1 The Buyer’s Optimal Stopping Problem

The buyer has the opportunity to purchase the European option at the market price at or before its expiration date. The set of admissible purchase times, denoted by , consists of all stopping times with respect to taking values in . The buyer’s objective is to determine the optimal stopping time that maximizes the spread between her subjective price and the market price . At time , she faces the optimal stopping problem:

| (3) |

where . The quantity is interpreted as the optimal spread between the model price and the market ask price and can be used for statistical arbitrage algorithms. Namely, various profit opportunities can be ranked according to their spreads since other things being equal, larger is more likely to generate trading profit (in a generic case where true model is unknown).

Since is itself a trivial stopping time and , it follows from (3) that and . Hence, can be viewed as an American spread option. Since at time the option expires and all market participants realize the same payoff, the choice means the buyer never buys the option. For instance, when the market price is consistently higher than the buyer’s price, i.e., for , we have and (see also Remark 3.1).

By substituting (2) into (3), along with repeated conditioning, we simplify to

| (4) |

where

| (5) |

Therefore, in order to determine the buyer’s optimal purchase time for , one can equivalently solve the cost minimization problem represented by in (5). In other words, the buyer selects the optimal purchase time that minimizes the expected discounted market price under her pricing measure . If there were no market for the option , then the investor’s cost would be . By optimally purchasing from the market, the investor’s reduced cost is . Therefore, one can view as the benefit of market access to the buyer.

In addition, we observe the following put-call parity in terms of the optimal purchase strategies.

Proposition 2.1.

The buyer’s optimal strategies for buying a European Call and for buying a European Put, with the same underlying, strike and maturity, are identical.

Proof.

Let and , respectively, be the market prices of a European Put and European Call on with the same strike and maturity. Applying the well-known model-free Put-Call parity and the fact that is a -martingale, we obtain

| (6) |

Since the last two terms do not depend on the choice of , it follows that

∎

Our aim for the remainder of the paper is to characterize the optimal acquisition time corresponding to the optimal stopping problem in (5) in terms of and . An important question is under what conditions it is optimal to immediately buy the option from the market, or conversely never purchase it. Moreover, we want to examine the market factors, in particular the option payoff shape, that influence the investor to buy the option earlier or later.

2.2 -Optimal Concatenation of Pricing Measures

The minimum cost can be alternatively viewed as the risk-neutral price of the option under some special measure. To this end, we first denote the density processes associated with and (with respect to ) by

| (7) |

where the expectations are taken under the historical measure . Next, we consider a probability measure that is identical to up to the -stopping time and then coincides with over . Precisely, is defined through its -density process, , as

| (8) |

It is straightforward to check that is a strictly positive -martingale and that is again an EMM. The expression in (8) is referred to as the concatenation of the density processes and (or equivalently, the concatenation of the EMMs and ); see, for example, Delbaen (2006), and Riedel (2009). We denote by the collection of EMMs generated by concatenating the EMMs and , parameterized by a stopping time .

Proposition 2.2.

The minimum cost can be expressed as

| (9) |

Proof.

According to Proposition 2.2, the purchase timing flexibility allows the buyer to expand the space of pricing measures from her single pricing measure to the collection of measures that is linked to the market measure through concatenation. Note that all these candidate pricing measures coincide with the market measure after time . In particular, the choice of or corresponds to pricing under or , respectively. By choosing the purchase time, the buyer is in effect choosing the optimal time to adopt the market pricing measure. Related models of timing the adoption of market model risk in the context of irreversible investment have been considered in the real options literature; see Alvarez and Stenbacka (2004).

2.3 Delayed Purchase Premium

From the optimal stopping problem in (9), we observe the inequality . This implies that the timing option necessarily reduces the buyer’s valuation of the claim from to at any . In order to quantify this benefit of optimally waiting to purchase the option from the market, we define the buyer’s delayed purchase premium as

| (10) |

where is current cost of the option given in (see (1)) and is the minimized cost (see (5)).

Recall that the optimal stopping time in (5) corresponds to the first time the value process equals the reward process (Karatzas and Shreve, 1998, Appendix D). Using (9) and (10) we obtain

| (11) | ||||

As a result, the buyer will purchase the option from the market as soon as the delayed purchase premium diminishes to zero.

Let be the density process between the equivalent measures and . We can re-express the minimal purchase cost as

Let be the discounted market price. Applying the integration-by-parts formula (Protter, 2003, p. 83) to the semimartingale , we obtain

| (12) |

where is the covariation process of and . Since both and are -local martingales and assuming enough integrability, this implies that

| (13) |

Thus, we see that the bracket , which we call the drift function, plays a crucial role in determining the delayed purchase premium and, in view of (11), the optimal purchase time. This observation will be key to our Theorems 3.2 and 4.2 below that explicitly derive and analyze in specific Markovian models. Expression (13) can also be interpreted as the covariation process between the buyer’s state price deflator and the market price .

Remark 2.3.

The British options studied in Peskir and Samee (2008); Peskir et al. (2009) have payoffs of the related form , where the expectation is taken under a non-martingale “contract” probability measure . Working under the Black-Scholes model, Peskir and Samee also derive an expression similar to the drift function (see e.g. (3.18) in Peskir and Samee (2008)). They also characterize the early-exercise premium representation and the corresponding exercise boundary via a nonlinear integral equation using the methods of Peskir and Shiryaev (2006).

2.4 Buying American Options

The optimal timing of derivative purchase can be extended to the case of American options. Suppose the investor is considering to buy a finite-maturity American option, with payoff at any exercise time . At time , the buyer’s price and the market price are respectively given by

| (14) |

The buyer’s objective is to maximize the spread between his own price and the market quote:

| (15) |

Since is itself a stopping time and , this implies that . Hence, any candidate stopping time with is suboptimal, being dominated by . It follows that at purchase time , which means the buyer will hold on to the American option for a positive amount of time after purchase, rather than exercise it immediately. However, it is still possible that , so that the buyer may purchase the option even when the market price reflects a zero exercise premium.

In contrast to its European counterpart, the optimal timing problem (15) with American options is more difficult since it involves optimal multiple stopping, namely, the optimal purchase followed by the optimal exercise. Due to the optimal stopping problems nested inside the expectation in (15), the simplification (5) does not apply.

On the other hand, the American option price process is a -supermartingale and can be decomposed into the European option price plus the early exercise premium:

| (16) |

See, for example, Kramkov (1996) in a general incomplete market and El Karoui and Quenez (1995) in models with Brownian motions. Note that is a -martingale, and is a positive -adapted decreasing process with .

To measure the value of optimal timing to purchase an American option, we define the delayed purchase premium by

| (17) |

where the second equality follows from (12) and (16). In contrast to the delayed purchase premium for European options in (13), the delayed purchase premium depends on the early exercise premia difference in addition to the stochastic bracket between the European option market price and the density process . In terms of , the optimal purchase time is given by In particular, when the option is not purchased since according to (17).

Under a defaultable equity model, we will provide an explicit solution to the problem of buying perpetual American puts, as well as analysis on the finite-maturity American puts in Section 3.3.

3 Buying Options on a Defaultable Stock

In this section, we study the option purchase problem under a one-factor reduced-form defaultable stock model. Under the historical measure , the defaultable stock price evolves according to

| (18) |

with constant drift and volatility . Here, is a standard Brownian motion under , and is the intensity process for the single jump process under . Specifically, we define

and is a positive -adapted process. At , the stock price immediately drops to zero and remains there permanently, i.e. for a.e. , . We denote the filtration and assume it satisfies the usual conditions of right continuity and completeness. The compensated -martingale associated with is given by . Herein, we will consider Markovian local intensity of the form , for some bounded positive function . To summarize, follows a geometric Brownian motion until the default time , with a local default intensity . Similar equity models have been considered e.g. in Linetsky (2006), and date back to Merton (1976).

To begin our analysis, we define the set of equivalent martingale measures (EMMs) and study the price dynamics of options written on . Following the standard procedure in the literature (see, among others, Jarrow et al. (2005) and Bellamy and Jeanblanc (2000)), an EMM is defined through the Radon-Nikodym density , where

is a product of the Doléans-Dade exponentials

| (19) | ||||

| (20) |

Here, is a strictly positive bounded -predictable process which acts as a scaling factor for the default intensity, and is another bounded process found from the equation

| (21) |

The process is commonly referred to as the market price of risk and as the default risk premium. The condition (21), which is common in jump-diffusion models (see Bellamy and Jeanblanc (2000) and references therein), ensures that the discounted stock price is a martingale under . Indeed, by Girsanov Theorem, the evolution of under any EMM is given by

| (22) |

where is a -Brownian motion, and is a -martingale. Therefore, the default intensity under is and the discounted stock price is a -martingale.

According to (21), the set of the risk-neutral pricing measures can be viewed as being parameterized by the default risk premium only. Herein, we will consider Markovian default risk premium of the form for some bounded positive function . This makes the entire model Markov with state space and the risk-neutral price under any of an European option with terminal payoff can be written as

| (23) |

where is a deterministic function which depends on the choice of . The discounted option price is a -martingale and satisfies the SDE

| (24) |

Moreover, by standard Feynman-Kac arguments, the option price function solves the inhomogenous linear PDE problem:

| (25) |

where is the default intensity under , and is the second order differential operator defined by

| (26) |

The dynamics of will play a crucial role in the option buyer’s optimal stopping problem which we discuss next. Let us point out that as long as there are no liquid contracts for hedging the default time, such as credit default swaps, the option market remains incomplete. Thus, in this setup we can assume that all vanilla Calls/Puts are liquid, and their market prices can be used to calibrate the market measure .

3.1 The Buyer’s Optimal Purchase Timing

Denote and to be the market and the buyer’s pricing measures, respectively. The option prices under and are denoted by and , and are different due to different default risk premia and assigned by the market and the buyer.

At time , the buyer maximizes profit by solving the optimal stopping problem:

| (27) | ||||

where is the default time of under . The second equality follows from the fact that stays at zero past and . When the stock defaults, we have since all price discrepancies between the buyer and the market are eliminated. As a result, on the event , the timing option has no value, and the buyer will not purchase the derivative. This is also consistent with practice because most derivatives stop trading after the underlying defaults.

By applying repeated conditioning to (27), we obtain , where

| (28) | ||||

Note that in the case of default, so it follows from (11) that a.s. The possibility of default implies two scenarios: (i) in the event , the buyer purchases the option prior to default, and (ii) in the event of default, i.e. , the optimal timing problem is over and no purchase takes place. The buyer’s optimal timing is characterized by the buy region and the delay region , namely,

| (29) | ||||

| (30) |

Furthermore, the variational inequality associated with is

| (31) |

for , with terminal condition , for . Note that the market price acts as the obstacle term in the variational inequality. Moreover, the default rates and essentially act as state-dependent discount rates for the equations defining and respectively. Consequently, standard numerical tools for pricing of European/American-style options can be used to solve (25) and (31). Similar variational inequalities also arise in pricing American options under jump-diffusion models; see, for example, Pham (1997) and Oksendal and Sulem (2005).

Remark 3.1.

If the market price always dominates the buyer’s price, i.e., , then we can infer from (27) that and , which implies (see (3)). We can also verify this by substituting into the variational inequality (31) and using the PDE (25). For instance, this price dominance can occur for American Puts when the market default intensity dominates the buyer’s, i.e. ; see Proposition 5.1 of Pham (1997).

We now use (13) to derive the drift function for the defaultable equity model and characterize the respective delayed purchase premium (see (10)).

Theorem 3.2.

Define the function

| (32) |

If for all , then it is optimal to never purchase the option, i.e. and . If for all , then it is optimal to purchase the option immediately, i.e. is optimal for , and .

Proof.

Recall that and are the market prices of risk for the market and the buyer. It follows from the Girsanov Theorem that

where is a -Brownian motion, and is a -Brownian motion. This implies that

and the Radon-Nikodym derivative associated with the equivalent measures and is given by

| (33) |

where the processes and are defined by and . Since default risk premia are bounded, is a true -martingale and satisfies the SDE

| (34) |

where is a -martingale. Using Ito’s formula, the dynamics of under are

| (35) |

Since , and are all -martingales, the drift of is the last term. Therefore, the condition (resp. ) implies that is a -supermartingale (resp -submartingale), and the result follows.

Finally, applying SDE (35) yields the buyer’s delayed purchase premium as

| (36) |

which gives the conclusions of the Theorem in terms of . ∎

The drift function is related to the gamma or convexity of the option price . Indeed, if for each , is convex in , i.e. its gamma , then

whereby the drift function takes the same sign as the difference in premiums, i.e. . Hence, the optimal purchase rule is simplified to a direct comparison of risk premia. In summary,

Corollary 3.3.

Suppose the option price function is convex for each . If (resp. ) , then (resp. ).

As an application of Theorem 3.2 and Corollary 3.3, we discuss an example with European Calls and Puts. Here, we assume . Then, the market Call and Put prices with strike are respectively given by

| (37) | ||||

| (38) |

where and are the Black-Scholes pricing formulas for the Call and the Put. Both options are convex in and, applying Theorem 2.1 and (32) to (37) and (38), admit the same drift function

| (39) |

where is the standard Gaussian cdf and is as in the classical Black-Scholes formula. By Corollary 3.3, if for all , then it is never optimal to purchase the Call or the Put, whereas if for all , then it is optimal to purchase them immediately.

Theorem 3.2 implies that to have a non-trivial purchase strategy, the expression must change signs on . For instance, if , then the purchase strategy is trivial unless can be both positive and negative. In other words, there must exist times and stock levels, such that the buyer’s default intensity is less than the market’s, and other times and stock levels such that the buyer’s default intensity is larger than the market’s. The location of the level set is then crucial for determining the optimal purchase boundary for the buyer.

The probabilistic representation (36) allows us to analyze the optimal purchase time via the premium . Indeed, from (36) it is clear that if then the buyer should postpone her purchase since positive infinitesimal “rent” can be derived by taking for sufficiently small in (36). Hence, for every in the buy region , we must have . For instance, for a Call option we must have and the market must be underestimating the default intensity in the buy region. Furthermore, when the Call is near expiry and , then and hence by continuity of until , and being bounded, for small enough. Conversely, if , then near expiry and it follows that the critical stock price separating the buy and delay regions satisfies in the limit .

Furthermore, if for all , then the corresponding delayed purchase premia satisfy . As a result, it is always optimal to purchase the derivative associated with before that associated with . We illustrate this observation through the following example.

Example 3.4.

(Call vs Bull Spread) Let us compare the buyer’s optimal purchase timing between two bullish positions: a Call and a bull spread (also known as capped Call). First, we assume constant default intensities and for the buyer and the market. The market price of the Call with strike is as in (37), and its drift function is given by (39). The market price of the bull spread with strikes , , is given by . The corresponding drift function is , but it is not immediately clear from what the buyer’s optimal strategy is.

Nevertheless, when , we have by (39), and therefore . We can apply the observations above to conclude that the delayed purchase premium of the bull spread must dominate that of the Call, i.e. . As a result, the optimal purchase time for the bull spread is always later than the Call purchase time. In fact in this case, the buyer will buy the Call immediately, but may delay to buy the bull spread. By similar arguments, when , it follows that , and the buyer will never purchase the Call but may buy the bull spread prior to expiration.

3.2 Numerical Examples

In the cases where the purchase timing problem is nontrivial, we must revert to numerical methods. Optimal stopping problems on finite horizon generally do not admit closed-form solutions, but have been extensively investigated in the literature. The defaultable equity model above is one-dimensional in space and the most straightforward algorithm is to solve the respective variational inequality. Note that we have three possible formulations, namely solving for the profit spread , the minimal purchase cost or the delayed purchase premium . The variational inequality for was given in (31) and applying (25) and (31) it follows that the variational inequality for is

| (40) |

Both formulations yield the same exercise boundary. In the examples below, we employed the standard implicit PSOR algorithm to solve for over a uniform grid (typically of size ) on (see Ch. 9 of Wilmott et al. (1995)). This method has the advantage that a simple adjustment allows to compute as well, and therefore derive all the quantities of interest. Standard Dirichlet/von Neumann boundary conditions were applied on the -boundaries of the grid.

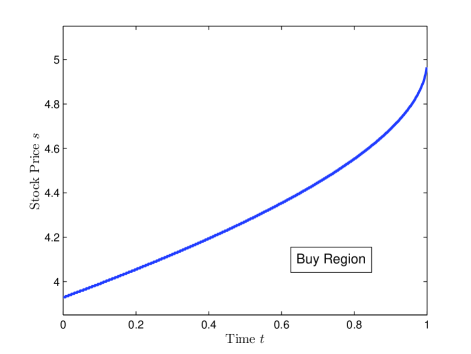

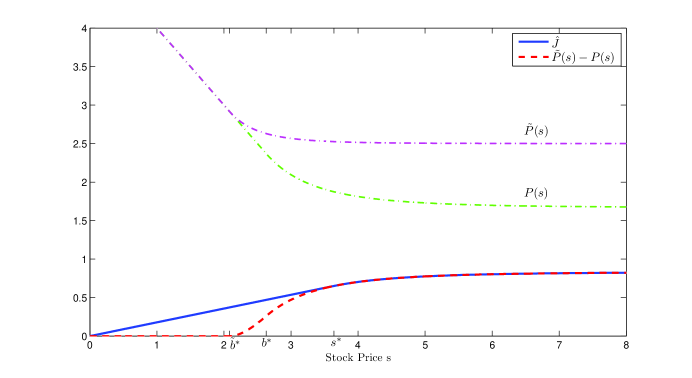

Figure 1 illustrates the optimal purchase boundary that represents the critical stock value at which the buyer should buy a European Put. The buyer will buy as soon as reaches from above, but if default arrives first then will jump across to zero and no purchase will be made. In that example, for large and for small . As explained above, by Put-Call parity, the purchase boundary of the corresponding Call is the same. At maturity the purchase boundary converges to , due to the fact that .

Recall that the buyer’s total profit is

which decomposes into the current difference in valuations plus the delayed purchase premium , see (10). For instance with the parameters of Figure 1 and initial stock price , the defaultable Put has market price and investor’s valuation of , so that a model-based profit of can be booked by buying this Put immediately. In addition, we find that so that another 1.3 cents (or over of the above spread) can be gained by timing this purchase optimally. The overall profit is therefore given by . Observe that the maximum profit of over 7 cents is realized around but in those cases it is optimal to lock it in immediately and . The total gain from optimal timing of the derivative purchase can be represented as

and shows the profit obtained compared to the trivial strategies of and .

|

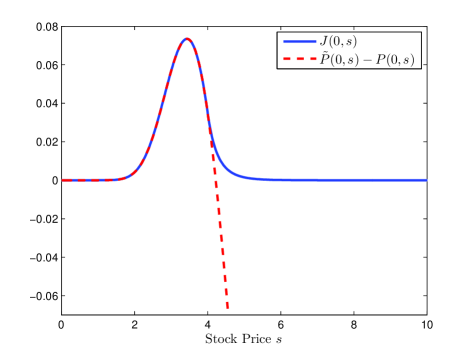

In Figure 2, we consider a digital Call option with constant default intensities and which implies that the corresponding digital option prices are given by the classical Black-Scholes formulas with discount rates and respectively. The resulting drift function is then

where is the standard Gaussian density. has horizontal asymptotes and and, moreover, changes sign. As a result, the purchase boundary , shown in Figure 2 (left) is non-trivial. Interestingly, this boundary is not monotone in and moreover switches from being out-of-the-money for large to in-the-money close to maturity. Similar non-monotonicity of is documented for British options, see Figure 5 in Peskir and Samee (2008). The difference in prices also exhibits a sign-change (right panel of Figure 2).

|

Remark 3.5.

In all the examples above, both the purchase delay region and the buy region were connected. This occurred because was monotone in , which implies from (36) that there is a simple curve separating and . In more complicated settings may be changing signs several times which would lead to multiple purchase boundaries and disconnected and/or regions.

3.3 Buying American Options

Continuing our discussion in Section 2.4, let us study the optimal timing to buy American options under the defaultable equity model (22). To provide an example with closed-form solutions, we first analyze the purchase timing of a perpetual American Put with strike . Assuming the market default intensity to be a constant , standard calculations (Karatzas and Shreve, 1998, Ch. 2.7) yield the market price and corresponding optimal exercise threshold

| (41) |

where

| (42) |

Further assuming that the buyer also has a constant default intensity under , we may replace with in (41)-(42) to obtain the buyer’s value and exercise threshold .

The perpetual American option buyer’s optimal stopping problem is

Note that (resp. ) is increasing and (resp. ) is decreasing with respect to (resp. ) (see Figure 3 (left)). If , then we have and for all . In this case, there is no value in optimally timing the purchase. Henceforth, we will focus on the case with .

The payoff function is increasing in but is neither convex nor concave. Nevertheless, the buyer’s optimal stopping problem admits a closed-form solution.

Proposition 3.6.

Assume . The value of the timing option is

| (43) |

with the constant given by

| (44) |

where is the optimal purchase threshold uniquely determined from the algebraic equation with

| (45) |

Moreover, the thresholds are ordered by the inequality .

Proof.

Let be the conjectured solution in (43), which is simply the smallest concave majorant of the payoff function (see right panel of Figure 3). To this end, the constants and are chosen to satisfy the continuous-fit and smooth-fit conditions: and , which simplify to (44) and (45). Furthermore, exists and is unique and finite because the function in (45) is strictly increasing for , and satisfies and .

By direct substitution and computation, we verify that satisfies the variational inequality

| (46) |

for , with boundary condition . This implies that is a (bounded) -supermartingale. Hence, for any stopping time ,

| (47) |

Maximizing over , we get . On the other hand, (47) is an equality for the admissible stopping time , which yields . ∎

Proposition 3.6 is illustrated in Figure 3. We observe that the value is linear in in the continuation region and increasing concave in in the exercise region . It also admits the constant upper bound . If the initial stock price , then the buyer will wait till the stock price hits the upper level to buy the perpetual American put before exercising it at a lower level .

For perpetual American Calls written on in (22), the timing problem is not well-defined. Indeed, the discounted price process is a martingale under and , so it follows from Jensen’s inequality that is a submartingale under and . Therefore, the optimal policy for either the market or the buyer is to hold on to the Call forever.

Next, we turn our attention to the case of buying a finite-maturity American Put. Denote by and , respectively, the market price and the buyer’s price for the same American Put with payoff . The classical early exercise premium decomposition gives that

| (48) |

and similarly for . The representation (17) then implies that

| (49) |

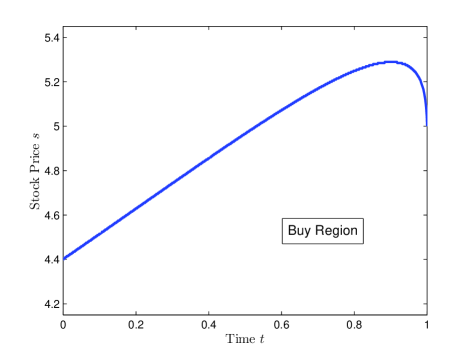

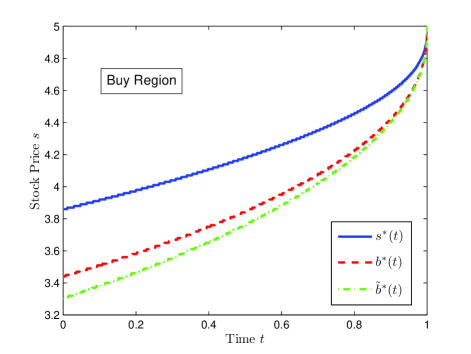

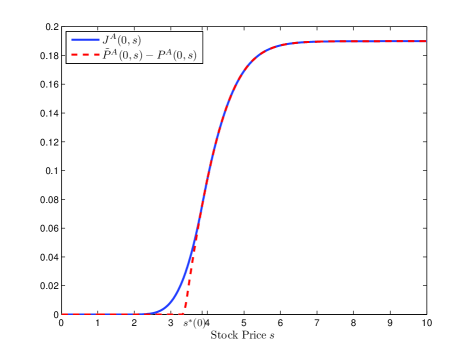

When and are constant, then the optimal strategy is to exercise the underlying American Put as soon as the stock reaches (from above) the exercise boundary , (see Proposition 2.2 of Pham (1997)). As a result, and the delayed purchase premium depends on the different probabilities under and that stays in the respective exercise regions. Note that the stock price may spend some time in the exercise regions before the buyer decides to purchase the option.

In Figure 4, we illustrate the optimal purchase boundary. In this example, the default intensities are constant, and so the underlying optimal exercise problems for and are essentially identical to the classical American Put under the Black-Scholes model with discount rate (resp. ). The corresponding Put exercise boundaries, denoted and , are shown in Figure 4. Since , we have and for all . The buy region in Figure 4 is above the purchase boundary denoted by , so that American Put is purchased on an up-tick. Intuitively, deep in-the-money the Put should be exercised under both EMMs, so that and no profit spread is available. Conversely, out-of-the-money is positive and concave in (Figure 4 right) and in the spirit of Corollary 3.3 it is optimal to purchase the American Put immediately. As a result, lies slightly in-the-money, and for it is possible that , i.e. the Put is purchased after its original exercise date under either EMM.

In this example, since , the European Put would be purchased immediately and by Corollary 3.3. In contrast, the American Put’s delayed purchase premium is positive when (Figure 4 right), the purchase is delayed and the profit spread is larger .

|

4 Buying Options Under Stochastic Volatility

In this section, we study the problem of optimally buying an option under stochastic volatility. Under the historical measure we consider a Markovian stochastic volatility model, where the underlying stock price and stochastic process solve the SDEs:

| (50) | ||||

| (51) |

In (50)-(51), and are two independent standard Brownian motions defined on , where is taken to be the augmented -algebra generated by . The growth rate and the positive volatility coefficient are driven by the non-traded stochastic factor . We model the correlation between and through the coefficient and set .

Assumption 4.1.

(1) The volatility function is Lipschitz, -differentiable, and bounded above and below away from zero. (2) the functions and are bounded Lipschitz on , with . (3) is Lipschitz on .

The stochastic volatility model in (50)-(51) as well as Assumption 4.1 are adopted from the more general setups in Romano and Touzi (1997) and Fouque et al. (2000).

Let be a bounded -progressively measurable process. Then, we can define an equivalent martingale measure by

| (52) |

where is the bounded Sharpe ratio of . By Girsanov’s change of measure, the dynamics of and under are given by

| (53) | ||||

| (54) |

where

| (55) |

are independent -Brownian motions. Therefore, the process parametrizes the set of pricing measures, and is typically called the volatility risk premium. In particular, when the risk premium is , the associated measure is the well-known minimal martingale measure (MMM) (see Föllmer and Schweizer (1990)). The intuitive effect of is to modify the drift of as observed in (54). Therefore, for options with positive dependence on volatility (such as those with convex payoffs and , see Romano and Touzi (1997)), larger risk premium reduces the drift of and hence is expected to decrease the option price. To this end, Henderson et al. (2005) have analyzed the ordering of option prices by risk premium under a stochastic volatility model (see also Henderson and Hobson (2003) for jump-diffusions). The price ordering will also play a role in the buyer’s optimal purchase decision.

4.1 The Buyer’s Optimal Purchase Timing

For our analysis, we consider Markovian risk premia for the buyer and the market. Specifically, we let and , for bounded continuous functions and , which correspond to the buyer’s measures and the market measure respectively. The option in question has a payoff at expiration date . The nontradability of makes it impossible to completely replicate the option payoff by trading in and the money market account, so the market is incomplete. The buyer’s price and the market price are computed under their respective measures, namely,

| (56) | ||||

| (57) |

The buyer’s objective is to solve the optimal stopping problem

| (58) |

With this, the buyer’s delayed purchase premium is given by . The buyer’s optimal timing naturally depends on the option’s market price as well as the risk premia and . The next theorem expresses this dependence through the respective drift function , cf. Theorem 3.2.

Theorem 4.2.

Let

| (59) |

If for all , then it is optimal not to purchase the option, i.e. and . If for all , then it is optimal to purchase the option immediately, i.e. and .

Proof.

From (55), we observe that , and Therefore, the two equivalent pricing measures and are connected via the Radon-Nikodym derivative

where is the (bounded) volatility premium difference between the buyer and the market. Also, solves the SDE: Consequently, the process satisfies

| (60) |

Since , are -martingales and is positive by convention, the process is a -submartingale (resp. -supermartingale) if a.s. on (resp. ). Then, it is optimal to purchase immediately (resp. never purchase) since the expected discounted cost increases (resp. decreases) over time. Finally, due to (13), the delayed purchase premium admits the representation

| (61) |

∎

Remark 4.3.

Although our analysis focuses on options written on only, Theorem 4.2 also immediately applies for an option with payoff . Other elements of the model, such as to unbounded risk premia, can also be generalized as long as the martingale properties of the processes , and are preserved. We do not address the full generalization here.

Under the common assumption that is increasing, the drift function is again closely linked to the convexity of the option price, cf. Corollary 3.3.

Corollary 4.4.

Assume the option price is convex in for every and . If for all , then it is optimal to never purchase the option. If for all , then it is optimal to purchase immediately.

Proof.

When the option payoff is convex, such as the Call and the Put, then the option price is also convex (see Proposition 4.3 of Romano and Touzi (1997)), so Corollary 4.4 applies.

By inspecting the probabilistic representation (61), we deduce that if , then the buyer should postpone her purchase since an infinitesimal reward can be obtained by waiting for an infinitesimal moment. Hence, along the exercise boundary , , we must have . For options with convex payoffs as in Corollary 4.4, if and only if , so in the exercise region the buyer must overestimate the volatility risk premium relative to the market.

Corollary 4.5.

Assume the option’s payoff function is convex and . The buyer will not buy the option at if at that point.

Next, using Theorem 4.2 and Corollary 4.4, we can also compare the optimal purchase strategy between vanilla options and some exotic options.

Example 4.6.

(Call vs Bull Spread, cf. Example 3.4) Suppose . Since for Calls, it follows that the drift function of the Call with strike dominates that of the bull spread with strikes , . Therefore, by (11) and (61), the buyer will purchase the bull spread later than the Call. By Corollary 4.4 the buyer will purchase the Call now, but may delay to buy the bull spread. Conversely, when , the buyer will never purchase the Call but may buy the bull spread prior to expiration.

Example 4.7.

(Price Ordering by the -Optimal Measures) Intuitively, the option price should influence the buyer’s purchase timing. To illustrate this, we consider the price ordering via the -optimal measures studied by Henderson et al. (2005). We recall that -optimal measures arise from taking the probability measure that minimizes the -th moment of the Radon-Nikodym derivative between and , i.e. . Pricing under can also be interpreted as marginal indifference price of a risk-averse agent with a constant relative risk aversion (power) utility .

The respective market price of volatility risk is in general a complicated expression given as solution of a semi-linear PDE (see Hobson (2004)). However, in the case of a Heston stochastic volatility model, namely,

with constants and , Henderson et al. (2005) showed that is increasing. Therefore, assuming and with (the investor is more risk averse than the market), it follows that the market Call/Put price always exceeds the investor’s price and the buyer can never profit from buying from the market, so . Conversely, if then .

In general, one has to numerically solve the free boundary problem associated with , namely

| (62) |

where we have suppressed and is the elliptic differential operator given by

Equivalently, one can solve for the delayed purchase premium via

| (63) |

with terminal condition for . Compared to (62), the free boundary problem (63) has a source term but a zero obstacle. Standard methods imply that under our assumptions (resp. ) are the unique viscosity solutions of (62) and (63), and therefore the usual finite-difference methods can be applied to numerically solve (62) or (63) for the associated purchase boundary that represents the critical values of at which the option should be purchased.

We have discussed the buyer’s optimal timing problem under a stochastic volatility model. In the model (50)-(51), the process can also represent a generic non-traded stochastic factor, not necessarily for stochastic volatility. Depending on the context, one may modify the model parameters and assumptions, and therefore, the convexity of option prices may no longer play a crucial role as seen in this section. However, Theorem 4.2 and representation (61) still apply and can be used to infer the buyer’s optimal timing.

5 Further Applications

The optimal timing problem we have discussed here also arises in other financial applications.

5.1 Optimal Rolling for Long-Dated Options

In a common transaction, an investor issues a long-dated option in a bespoke over-the-counter contract. This long-dated option is not traded in the market; thus, to hedge the resulting short position the investor (the hedger) instead purchases the same option with shorter maturity. For instance, to hedge a -year Put position on , the investor might initially buy a -year LEAPS Put. At a later date , the investor then plans to roll-over her position into the 5-year Put, by simultaneously buying a Put expiring at and selling the Put expiring at . In this example, assuming that LEAPS contracts are trading up to 3 years out, if the roll takes place during year 3, then a single such roll-over is needed; for maturities over 6 years multiple rolls would be required.

Let be the market price of a Put with arbitrary maturity . Then the goal of the investor is to minimize the net cost at the roll date given by , for . The roll-over must take place between , when the option expiring at first becomes available, and when the short-dated option matures.

In a complete market with a unique pricing measure , the cost process is a -martingale, so any admissible rolling time will lead to the same expected cost under . However, if the market is incomplete and the investor prices with her own pricing measure , then the rolling problem at time is

The above rolling problem matches closely our purchase timing model (5). Proposition 2.1 implies that the rolling of Puts and Calls with the same strike and maturities yield identical optimal strategies. Furthermore, we can express the delayed rolling premium as

Hence, the rolling strategy depends on the difference between the drift functions . In both classes of models in Section 3 and Section 4, the resulting rolling boundary is typically nontrivial. Indeed, in contrast to Corollary 3.3 in the defaultable equity model, the drift function difference does not take constant sign even if is constant. In fact, the shape of looks like that of the short digital Call and therefore a similar non-monotone exercise boundary for is obtained as in Figure 2. Similarly, in the stochastic volatility case, changes signs for different depending on the parameters.

Remark 5.1.

The investor’s total expected discounted cost at time is . The first part is the cost of acquiring the -Put initially, but due to its independence of , it is irrelevant to the selection of the optimal rolling time. In practice, the investor may also control the expiration date and strike of the first Put, though we do not discuss this here.

5.2 Sequential Buying and Selling of Derivatives

Another form of statistical arbitrage we may consider involves sequential buying and selling of the same derivative. Namely, the investor aims to generate profit by first buying the option at price and then selling it at price , making decisions based on model measure . Given , this problem is equivalent to maximizing the sale price , i.e. (28) up to a sign-change. If the purchase date can also be optimally timed, the investor then has a two-stage timing problem,

| (64) |

While (64) is a two-stopping-time problem, it can be straightforwardly decomposed into sequential stopping. Indeed, defining (cf. (5))

we have for any

| (65) |

Hence, we can first numerically solve the standard optimal stopping problem for and then another one for .

Proposition 5.2.

The value function from (64) admits the delayed purchase premium representation

| (66) |

Proposition 5.2 implies that in Markovian models, the drift function is once again useful in analyzing the optimal purchase and liquidation decisions. For instance, in the defaultable equity model of Section 3 with the drift function defined in (32), we have . Therefore, if is of constant sign, then following the spirit of Theorem 3.2 either the option is never purchased (whenever ) or it is purchased immediately and held till maturity (whenever ). Similar conclusions can be made for the stochastic volatility setup in Section 4.

In other cases, the investor will buy and then sell the option during and the timing strategy involves both a buy region and a subsequent sell region. Numerical solutions in a parametric model can be straightforwardly obtained using the sequential representation of in (65). Finally, one can also consider more complex models of contract accumulation/liquidation following the methods of Henderson and Hobson (2008).

5.3 Other Extensions

The optimal timing problem can also be extended in a number of directions, such as when (i) the underlying admits other dynamics, e.g. jump diffusion; (ii) the buyer wants to purchase other financial instruments, e.g. foreign exchange, fixed income, or credit derivatives; and (iii) the option buyer observes ask prices from multiple sellers. In the last case, each seller prices the option under a different EMM , yielding a no-arbitrage price . To the buyer, the cost of the option is now the cheapest offer among the seller’s prices , which can be viewed as the no-arbitrage price for the option under a certain EMM , i.e., such that . Hence, we can reduce this multiple-seller problem to the single-seller case discussed in this paper.

Finally, another practical extension is to incorporate the buyer’s risk preferences in her timing problem. One common approach is to formulate the buyer’s problem in terms of utility maximization. The buyer’s valuation of the option can be derived from the concept of utility-indifference price (or certainty equivalent), and her purchase decision naturally depends on the dynamics of both the buyer’s utility-indifference price and the market price. In a similar spirit, the recent works by İlhan and Sircar (2005) and Leung and Sircar (2009) apply indifference pricing to study static-dynamic hedging that also involves purchasing derivatives from the market.

In the model presented, the buyer knows precisely the market pricing measure . In some situations, such as when options are not liquidly traded, there may be in fact ambiguity about how the market/sellers generate ask quotes. Consequently, it may be useful to introduce model uncertainty regarding . These extensions will be considered in future works.

Acknowledgements

We are grateful to Paul Glasserman, Matheus Grasselli and Vicky Henderson for useful conversations and suggestions, and Adi Dror for his assistance with the numerical implementation.

References

- Allen and Padovani (2002) Allen, S. and O. Padovani, 2002: Risk management using quasi static hedging. Economic Notes, 31 (2), 277–336.

- Alvarez and Stenbacka (2004) Alvarez, L. and R. Stenbacka, 2004: Optimal risk adoption: A real options approach. Economic Theory, 23, 123–148.

- Bellamy and Jeanblanc (2000) Bellamy, N. and M. Jeanblanc, 2000: Incompleteness of markets driven by a mixed diffusion. Finance and Stochastics, 4, 209–222.

- Carr et al. (1992) Carr, P., R. Jarrow, and R. Myneni, 1992: Alternative characterizations of American put options. Mathematical Finance, 2(2), 87–106.

- Delbaen (2006) Delbaen, F., 2006: The structure of stable sets and in particular of the set of risk neutral measures. In Lecture Notes in Mathematics, volume 1874. Springer Berlin / Heidelberg, 215-258.

- El Karoui et al. (2010) El Karoui, N., M. Jeanblanc, and Y. Jiao, 2010: What happens after a default: the conditional density approach. Stochastic processes and their applications, 120, 1011–1032.

- El Karoui and Quenez (1995) El Karoui, N. and M. Quenez, 1995: Dynamic programming and pricing of contingent claims in an incomplete market. SIAM Journal on Control and Optimization, 33, 29–66.

- Föllmer and Schweizer (1990) Föllmer, H. and M. Schweizer, 1990: Hedging of contingent claims under incomplete information. In Applied Stochastic Analysis, Stochastics Monographs, Davis, M. and Elliot, R., editors, volume 5. Gordon and Breach, London/New York, 389 - 414.

- Fouque et al. (2000) Fouque, J.-P., G. Papanicolaou, and R. Sircar, 2000: Derivatives in Financial Markets with Stochastic Volatility. Cambridge University Press.

- Fritelli (2000) Fritelli, M., 2000: The minimal entropy martingale measure and the valuation problem in incomplete markets. Math. Finance, 10, 39–52.

- Fujiwara and Miyahara (2003) Fujiwara, T. and Y. Miyahara, 2003: The minimal entropy martingale measures for geometric Lévy processes. Finance and Stochastics, 7(4), 509–531.

- Guo et al. (2009) Guo, X., R. Jarrow, and Y. Zeng, 2009: Credit risk models with incomplete information. Mathematics of Operations Research, 34(2), 320–332.

- Henderson and Hobson (2003) Henderson, V. and D. Hobson, 2003: Coupling and option price comparisons in a jump-diffusion model. Stochastics and Stochastics Reports, 75, 79–101.

- Henderson and Hobson (2008) Henderson, V. and D. Hobson, 2008: Optimal liquidation of derivative portfolios. Math. Finance. To appear.

- Henderson et al. (2005) Henderson, V., D. Hobson, S. Howison, and T.Kluge, 2005: A comparison of -optimal option prices in a stochastic volatility model with correlation. Review of Derivatives Research, 8, 5–25.

- Hobson (2004) Hobson, D., 2004: Stochastic volatility models, correlation, and the -optimal measure. Math. Finance, 14(4), 537–556.

- İlhan and Sircar (2005) İlhan, A. and R. Sircar, 2005: Optimal static-dynamic hedges for barrier options. Math. Finance, 16, 359–385.

- Jarrow et al. (2005) Jarrow, R. A., D. Lando, and F. Yu, 2005: Default risk and diversification: theory and empirical implications. Math. Finance, 15(1), 1–26.

- Karatzas and Shreve (1998) Karatzas, I. and S. Shreve, 1998: Methods of Mathematical Finance. Springer.

- Kramkov (1996) Kramkov, D., 1996: Optional decomposition of supermartingales and hedging contingent claims in incomplete security markets. Probability Theory and Related Fields, 105, 459–479.

- Leung and Sircar (2009) Leung, T. and R. Sircar, 2009: Exponential hedging with optimal stopping and application to ESO valuation. SIAM Journal of Control and Optimization, 48(3), 1422–1451.

- Linetsky (2006) Linetsky, V., 2006: Pricing equity derivatives subject to bankruptcy. Math. Finance, 16(2), 255–282.

- Merton (1976) Merton, R., 1976: Option pricing when underlying stock returns are discontinuous. Journal of Financial Economics, 3, 125–144.

- Oksendal and Sulem (2005) Oksendal, B. and A. Sulem, 2005: Applied Stochastic Control of Jump Diffusions. Springer.

- Peskir et al. (2009) Peskir, G., K. Glover, and F. Samee, 2009: The British Asian option. Sequential Anal. to appear.

- Peskir and Samee (2008) Peskir, G. and F. Samee, 2008: The British put option. Technical Report Research Report No. 1, Probab. Statist. Group Manchester.

- Peskir and Shiryaev (2006) Peskir, G. and A. N. Shiryaev, 2006: Optimal Stopping and Free-boundary problems. Birkhauser-Verlag, Lectures in Mathematics, ETH Zurich.

- Pham (1997) Pham, H., 1997: Optimal stopping, free boundary, and American option in a jump-diffusion model. Applied Mathematical and Optimization, 35, 145–164.

- Protter (2003) Protter, P., 2003: Stochastic integration and differential equations. Springer.

- Riedel (2009) Riedel, F., 2009: Optimal stopping with multiple priors. Econometrica, 77(3), 857 – 908.

- Romano and Touzi (1997) Romano, M. and N. Touzi, 1997: Contingent claims and market completeness in a stochastic volatility model. Math. Finance, 7(4), 399–410.

- Wilmott et al. (1995) Wilmott, P., S. Howison, and J. Dewynne, 1995: The Mathematics of Financial Derivatives. Cambridge University Press.