optimal execution strategy in the presence of permanent price impact and fixed transaction cost

Abstract

We study a single risky financial asset model subject to price impact and transaction cost over an infinite horizon. An investor needs to execute a long position in the asset affecting the price of the asset and possibly incurring in fixed transaction cost. The objective is to maximize the discounted revenue obtained by this transaction. This problem is formulated first as an impulse control problem and we characterize the value function using the viscosity solutions framework. We also analyze the case where there is no transaction cost and how this formulation relates with a singular control problem. A viscosity solution characterization is provided in this case as well. We also establish a connection between both formulations with zero fixed transaction cost. Numerical examples with different types of price impact conclude the discussion.

Keywords: Price impact, impulse control, singular control, dynamic programming, viscosity solutions

1 Introduction

An important problem for stock traders is to unwind large block orders of shares. Market microstructure literature has shown (e.g. (Chan and Lakonishok, 1995; Holthausen et al., 1990)), both theoretically and empirically, that large trades move the price of risky securities either for informational or liquidity reasons. Several papers addressed this issue and formulated a hedging and arbitrage pricing theory for large investors under competitive markets. For example, in (Cvitanić and Ma, 1996) a forward-backward SDE is defined, with the price process being the forward component and the wealth process of the investor’s portfolio being the backward component. In both cases, the drift and volatility coefficients depend upon the price of the stocks, the wealth of the portfolio and the portfolio itself. (Frey, 1998) describes the discounted stock price using a reaction function that depends on the position of the large trader. In (Bank and Baum, 2004; Çetin et al., 2004) the authors, independently, described the price impact by assuming a given family of continuous semi-martingales indexed by the number of shares held ((Bank and Baum, 2004)) and by the number of shares traded ((Çetin et al., 2004)).

The optimal execution problem has been studied in (Bertsimas and Lo, 1998; Almgren and Chriss, 2000) in a discrete-time framework. In both cases the dynamics of the price processes are arithmetic random walks affected by the trading strategy. In (Bertsimas and Lo, 1998) the impact is proportional to the amount of shares traded. In (Almgren and Chriss, 2000) the change in the price is twofold, a temporary impact caused by temporary imbalances in supply/demand dynamics and a permanent impact in the equilibrium or unperturbed price process due to the trading itself. Also, this work takes into account the variance of the strategy with a mean-variance optimization procedure. Later on, nonlinear price impact functions were introduced in (Almgren, 2003). These ideas were adopted by more recent works under a continuous time framework. (Schied et al., 2010) propose the problem within a regular control setting. The authors consider expected-utility maximization for CARA utility functions, that is, for exponential utility functions. The dynamics of the price and the market impact function are fairly general. (Schied and Schöneborn, 2009) is the only reference that considers an infinite horizon model based on the original model in (Almgren and Chriss, 2000). Finally, (He and Mamaysky, 2005) consider only permanent price impact but they allow continuous and discrete trading (singular control setting) with a geometric Brownian motion as price process.

On the other hand, it is also well established that transaction costs in asset markets are an important factor in determining the trading behavior of market participants. Typically, two types of transaction costs are considered in the context of optimal consumption and portfolio optimization: proportional transaction costs ((Davis and Norman, 1990; Øksendal and Sulem, 2002)) using singular type controls and fixed transaction costs ((Korn, 1998; Øksendal and Sulem, 2002)) using impulse type controls. The market impact effect can be significantly reduced by splitting the order into smaller orders but this will increase the transaction cost effect. Thus, the question is to find optimal times and allocations for each individual placement such that the expected revenue after trading is maximized. (Ly Vath et al., 2007) include both permanent market price impact and fixed transaction cost and assume that the unperturbed price process is a geometric Brownian motion process. This reference only accepts discrete trading (impulse control setting) and uses the theory of (discontinuous) viscosity solutions to characterize the value function. Finally, (Subramanian and Jarrow, 2001) propose a slightly different model which does not include any fixed transaction cost but includes an execution lag associated with size of the discrete trades. It is important to remark that all papers referenced above assume a terminal date at which the investor must liquidate her position.

In this paper we study an infinite horizon price impact model that includes fixed transaction cost under the setting of impulse control, similar to (Ly Vath et al., 2007). We describe a general underlying price process and a general permanent market impact. With help of some classic results for optimal stopping problems and the discontinuous viscosity solutions theory for nonlinear partial differential equations, developed in references such as (Crandall et al., 1992; Ishii and Lions, 1990; Ishii, 1993; Fleming and Soner, 2006), we obtain a fully characterization of the value function when the price process satisfies some technical condition. Most of the processes used in financial studies satisfy this condition. This characterization is not complete when the fixed transaction cost is zero. By analyzing the HJB equation obtained in the previous case, we formulate a singular control model to include this case. For this new formulation we are able to complete the characterization. We are able to show that both formulations agree in the value function even though the formulations are completely different, when we choose the appropriate market impact functions. Finally, we describe the value function and the optimal strategy explicitly for an important special case.

The structure of the paper is as follows: The general impulse control model, growth condition and boundary properties of the value function which are useful for the characterization of the function are exposed in Section 2. This section characterizes the value function of the problem as a viscosity solution of the Hamilton-Jacobi-Bellman equation and shows uniqueness when the fixed transaction cost is strictly positive and the price process satisfies certain conditions. Section 3 proposes a singular control model to tackle the case when the transaction cost is zero. Here a viscosity solution characterization and uniqueness result are proved as well under the same conditions. We present a special case where the value function of the impulse control model coincides with the value function of the singular control model and obtain the value function explicitly for this case. Section 4 shows that, in fact, these two formulation produce the same value function even though they consider different types of control. Section 5 presents numerical results for different underlying price processes with both formulations. Finally, we state some conclusions and future work.

2 Impulse control model

Let be a probability space which satisfies the usual conditions and be a one-dimensional Brownian motion adapted to the filtration. We consider a continuous time process adapted to the filtration denoting the price of a risky asset . The unperturbed price dynamics, when the investor makes no action, are given by:

| (2.1) |

where and satisfy regular conditions such that there is a unique strong solution of this SDE (i.e. Lipschitz continuity). We are mainly interested in price processes that are always non-negative, thus we assume that is absorbed as soon as it reaches 0 and that the initial price is non-negative.

Now, the number of shares in the asset held by the investor at time is denoted by and it is up to the investor to decide how to unwind the shares. Different models and formulations will define the admissible strategies for the investor. At the beginning the investor has number of shares and we only allow strategies such that for all . Since the investor’s interest is to execute the position, we don’t allow to buy shares, that is is a non-increasing process. Hence, we can see that (with interior ) is the state space of the problem. The goal of the investor is to maximize the expected discounted profit obtained by selling the shares. Given we define , the value function, as such maximum (or supremum), taken over all admissible trading strategies such that . We call the discount factor and the transaction cost. Note that we can always do nothing, in which case the expected revenue is 0. Therefore for all .

In this formulation we assume that the investor can only trade discretely over the time horizon. This is modeled with the impulse control , where the random variable is the number of trades, are stopping times with respect to the filtration such that that represent the times of the investor’s trades, and are real-valued -measurable random variables that represent the number of shares sold at the intervention times. Note that any control policy fully determines . Given any strategy , the dynamics of are given by

| (2.2) | ||||

| (2.3) |

We consider price impact functions such that the price goes down when the investor sells shares. Also, the greater the volume of the trade, the grater the impact in the price process. Thus, we let be the post-trade price when the investor trades shares of the asset at a pre-trade price of . We assume that is smooth, non-increasing in , and non-decreasing in such that for all . These conditions imply that for . Furthermore, we will also assume that for all

| (2.4) |

This assumption says that the impact in the price of trading twice at the same moment in time is the same as trading the total number of shares once. This assumption will prevent any price manipulation from the investor. Two possible choices for are:

where . A linear impact like has the drawback that the post-trade price can be negative. Given a price impact and an admissible strategy , the price dynamics are given by:

| (2.5) | ||||

| (2.6) |

When , then we apply the impact twice, therefore

If more that two actions are taken at the same time, we apply the impact accordingly. Now, given the value function has the form:

| (2.7) |

As usual, we assume that on .

2.1 Hamilton-Jacobi-Bellman equation

In order to characterize the value function we will use the dynamic programming approach. This principle has been proved for several frameworks and types of control. Some of the references that prove it in a fairly general context are (Ishikawa, 2004; Ma and Yong, 1999). We have that the following Dynamic Programming Principle (DPP) holds: For all we have

| (2.8) |

where is any stopping time. Let’s define the impulse transaction function as

for all and . This corresponds to the change in the state variables when a trade of shares has taken place. We define the intervention operator as

for any measurable function . Also, let’s define the infinitesimal generator operator associated with the price process when no trading is done, that is

for any function . The HJB equation that follows from the DPP is then ((Øksendal and Sulem, 2005))

| (2.9) |

We call the continuation region to

and the trade region to

2.2 Growth Condition

We will define a particular optimal stopping problem and use some of the results in (Dayanik and Karatzas, 2003) to establish an upper bound on the value function and therefore a growth condition. Consider the case where there is no price impact, that is, for all . We define

| (2.10) |

where follows the unperturbed price process. It is clear that . When there is no price impact, the investor would need to trade only one time.

Proposition 2.1.

For all

| (2.11) |

where the supremum is taken over all stopping times with respect to the filtration .

Proof.

Since is an admissible strategy for any stopping time , then . Now, let the set of admissible strategies with at most interventions. The proof will continue by induction in to show that for all

| (2.12) |

Clearly (2.12) is true for . Let . Note that , therefore, conditioning on we have

where the last inequality follows from the fact that the process is a supermartingale ((Øksendal and Reikvam, 1998)). This proves (2.12). By Lemma 7.1 in (Øksendal and Sulem, 2005), the left hand side of (2.12) converges to as and the proof is complete. ∎

From the previous result we have the bound

| (2.13) |

where the supremum is taken over all stopping times with respect to the filtration . Following section 5 in (Dayanik and Karatzas, 2003), let and be the unique, up to multiplication by a positive constant, strictly increasing and strictly decreasing (respectively) solutions of the ordinary differential equation and such that and as . For any , let

| (2.14) |

Then is finite in if and only if is finite for all . Furthermore, when is finite we also have that for some

| (2.15) |

and

| (2.16) |

We will assume that is finite.

2.3 Boundary Condition

Since the investor is not allowed to purchase shares of the asset we have that for all . Also, the price process gets absorbed at 0, therefore on . If we assume that is finite then by (2.15) we have that as for all , that is, is continuous on . Now we distinguish two cases:

-

1.

0 is an absorbing boundary for the price process . This means that for any , . A simple example is the arithmetic Brownian motion. Since the process is stopped at 0, we must have that for all

Also, (Dayanik and Karatzas, 2003) shows that in this case is continuous at whenever U is finite. Therefore the boundary conditions for the value function are

(2.17) -

2.

0 is a natural boundary for the price process . This means that for any , . For example the geometric Brownian motion. In this case we can have different situations in as goes to 0 depending on the price process. In particular, we can have the situation where is discontinuous on the set .

2.4 Viscosity solution

We now are going to prove that the value function is a viscosity solution of the HJB equation (2.9) and find the appropriate conditions that make this value function unique. The appropriate notion of solution of the HJB equation (2.9) is the notion of discontinuous viscosity solution since we cannot know a priori if the value function is continuous in . We must first state some definitions.

Definition 2.2.

Let be an extended real-valued function on some open set .

-

(i)

The upper semi-continuous envelope of is

-

(ii)

The lower semi-continuous envelope of is

Note that is the smallest upper semi-continuous function which is greater than or equal to , and similarly for . Now we define discontinuous viscosity solutions.

Definition 2.3.

Given an equation of the form

| (2.18) |

a locally bounded function on is a:

- (i)

- (ii)

- (iii)

We are now ready for the following theorem:

Proof.

By the bounds given in the section 2.2, it is clear that is locally bounded. Now we show the viscosity solution property.

Subsolution property: Let and such that is a maximizer of on with . Now suppose that there exists and such that

| (2.19) |

for all such that . Let be a sequence in such that and

By the dynamic programming principle (2.8), for all there exist an admissible control such that for any stopping time we have that

| (2.20) |

where is the process controlled by for . Now consider the stopping time

where is the first intervation time of the impulse control . By (2.20) we have that

| (2.21) | ||||

| (2.22) |

Now, by Dynkin’s formula and (2.19) we have

Since and , by (2.22)

for all . Letting go to infinity we have that

which implies that

Combining the above with (2.21) when we let we get

Since this is true for all small enough, then sending to 0 we have

If we show that , then we would have proved that if , then and therefore

Appendix A contains the proof of this last fact.

Supersolution property: Let and such that is a minimizer of on with . By definition of and we have that on and therefore . Let be a sequence in such that and

Now, since is lower semi-continuous and is continuous we have

Hence . Now suppose that there exists and such that

| (2.23) |

for all such that . Fix large enough such that and consider the process for with no intervention such that . Let

Now, by Dynkin’s formula and (2.23) we have

On the other hand, and using the dynamic programming principle (2.8) we have

Notice that since a.s by a.s continuity of the processes , then by the above two inequalities and taking , we have that

contradicting the fact that . This establishes the supersolution property. ∎

2.5 Uniqueness

Let be defined as before and let’s assume that the function defined in (2.13) is finite. Also assume that the transaction cost . Then, we want to prove that is the unique viscosity solution of the equation (2.9) that is bounded by . We will need an additional assumption about the function : For all

| (2.24) |

Following the ideas in (Crandall et al., 1992; Ishii, 1993) let be an upper semi-continuous (usc) viscosity subsolution of the HJB equation (2.9) and be a lower semi-continuous (lsc) viscosity supersolution of the same equation in , such that they are bounded by and

| (2.25) |

Define

for all . Then is still lsc and clearly by definition of . Now,

Therefore is supersolution of (2.9). Now, by the growth condition of and and equations (2.15) and (2.24) we get

| (2.26) |

We will show now that

| (2.27) |

It is sufficient to show that for all since the result is obtained by letting . Suppose that there exists such that . Since is usc, by (2.26) and (2.25) there exist such that . Let be the one with minimum norm over all possible maximizers of . For , define

Let

Clearly . Then, this inequality reads . Since and and are bounded above in that region, this implies that and (along a subsequence) as . We also find that , and . By theorem 3.2 in (Crandall et al., 1992), for all , there exist symmetric matrices and such that , and

Since is a subsolution of (2.9) and is a supersolution, we have

and

Now, if we show that for infinitely many ’s we have that

| (2.28) |

and since it is always true that

we have that by following the classical comparison proof in (Crandall et al., 1992). Suppose then, that there exists such that (2.28) is not true for all , then for

Since is a supersolution, we must have that

Since is usc, there exist such that . Then

Extracting a subsequence if necessary, we assume that as . First, consider , then by taking in the inequality above we get . This is a contradiction since . Now assume that . From the above inequalities we have that

for any . Since , let and taking in the above inequality we get that

This is a contradiction since was chosen with minimum norm among maximizers of and . Therefore (2.28) must hold for infinitely many ’s and (2.27) holds. As usual continuity in and uniqueness of follow from the fact that is a viscosity solution of (2.9).

We have just proved the following theorem:

Theorem 2.5.

Assume condition and that the transaction cost . If is a viscosity solution of equation (2.9) that is bounded by and satisfies the same boundary conditions as , then . Furthermore, is continuous in .

Remark 2.6.

Condition (2.24) is satisfied by Itô processes like Brownian Motion, Geometric Brownian Motion, Ornstein-Uhlenbeck and Cox-Ingersoll-Ross.

3 No transaction cost

From the proof of the above uniqueness result, we can see that the result depends on the fact that . Let’s start by pointing out that in this case the intervention operator becomes

| (3.1) |

for any measurable function . This implies in particular that any measurable function is a viscosity subsolution of (2.9). On the other hand, for the value function. Then we have that

Assume now that . Since is a maximum for , then for all :

Recall that is non-increasing in , so we define

| (3.2) |

for all . Hence, we get the following condition for :

| (3.3) |

This suggests that if we assume no fixed transaction cost we should look at a different HJB equation, that is

| (3.4) |

On the other hand, condition (2.4) implies that it is always better to split the orders into smaller orders. Indeed, given and

since is non-increasing in .

3.1 Singular control

In fact, the equation (3.4) is the associated equation of the following control problem ((Øksendal and Sulem, 2005)): In this case our admissible controls are of the singular type, that is

where , is an adapted, continuous non-decreasing and non-negative process. The price process in this case follows the dynamics

where (see (3.2)) is a non-negative smooth function that accounts for the price impact. In order to guarantee the existence and uniqueness of the process , we need to also assume that is a Lipschitz function ((Protter, 2004)). Now, the form of the value function changes to

| (3.5) |

for all . In this case the appropriate form of the DPP is

| (3.6) |

for any stopping time . As before, we can define the continuation region as

and the trade region as

Typically, singular controls are allowed to be càdlàg instead of continuous. We decide to restrict our controls for two reasons: (1) Under the absence of fixed transaction cost, the investor will divide the orders into very small pieces as shown above. (2) When the singular control is discontinuous the stochastic integral may not be properly defined (see (Protter, 2004)).

3.2 Viscosity solution

Although we only consider continuous strategies, the value function is still a viscosity solution of equation (3.4) (which definition is similar to 2.3).

Proof.

Since we can approach finite variation functions by simple functions, by proposition 2.1 we have that

| (3.7) |

Therefore, is locally bounded.

Subsolution property: Let and such that is a maximizer of on with . Now suppose that there exists and such that

| (3.8) |

for all such that . Let be a sequence in such that and

Given any stopping time , by (3.6), for all there exists an admissible control such that

where is the process controlled by for starting at . Since , using Dynkin’s formula for semimartingales ((Protter, 2004)) we have that

Consider again the stopping time

then by (3.8)

Taking we obtain a contradiction since the integral inside the expectation is bounded away from 0 for any admissible control by the a.s continuity of the process . Hence at least one of the inequalities in (3.8) is not possible and this establishes the subsolution property.

Supersolution property: Let and such that is a minimizer of on with . Let be a sequence in such that and

First, suppose that there exists and such that

| (3.9) |

for all such that . Fix large enough such that and consider the process for with no intervation, i.e. , such that . Let

Now, by Dynkin’s formula for semimartingales and (3.9) we have

As before, from here we can draw a contradiction with by the a.s. continuity if the process . Now, take and consider the process with control process and for given . Using (3.6) we can show that

By Dynkin’s formula again,

Letting , we have

Therefore, for all we have

Since is continuous, letting we get

as desired. This establishes the supersolution property. ∎

3.3 Uniqueness

Recall that with the impulse formulation we do not have uniqueness in absence of transaction cost. This is not the case with the singular control formulation.

Theorem 3.2.

Proof.

The proof follows the same strategy as in the impulse control case. Let be an upper semi-continuous (usc) viscosity subsolution of the HJB equation (3.4) and be a lower semi-continuous (lsc) viscosity supersolution of the same equation in , such that they are bounded by and condition (2.25) holds. Define

for all and as in (2.15). Recall that is non-negative and is an increasing function, then (2.15) implies that

Also , where is the identity operator. Therefore is a strict supersolution of (3.4) in . Following the same lines and definitions as in the previous proof we have

and

where . Since and , for large enough . We need to show now that for infinitely many ’s we have that

| (3.10) |

Suppose then, that there exists such that (3.10) is not true for all , then for

Since is a supersolution, we must have that

Hence,

Since goes to 0 as goes to , we get the contradiction . Therefore (3.10) must hold for infinitely many ’s and the comparison result holds. Everything follows now as before. ∎

3.4 Optimal strategy for a special case

Previous sections characterize the value function of our problem in different formulations. We will calculate now the explicit solution of the value function and describe the optimal strategy in a particular case. Let us come back to the impulse control case. Since we are allowed to do multiple trades at the same time, we are going to explore this strategy. Assumption (2.4) guarantees that the price impact does not change by splitting the trades, but the profit obtained by doing so could be greater. Let’s define the following function

| (3.11) |

This is the best that we can do when we do many trades at the same time. It is clear that this is not attainable with any impulse control. Since is non-increasing on and positive, we have for all

| (3.12) |

Therefore, for all

where the last inequality follows from (3.12). Hence and therefore by (3.1). On the other hand, the function satisfies (3.3) with equality. Indeed, by the condition (2.4) we have that for any , and

and taking we obtain

Now, since is smooth we find

If we had also that , then would solve both equations (2.9) and (3.4) and .

Now, (Subramanian and Jarrow, 2001) considers impact functions of the form , where is nonincreasing. In our case, by condition (2.4), must satisfy and therefore we end up with the following price impact functions and :

| (3.13) | ||||

| (3.14) | ||||

| (3.15) |

with . This function was proposed also in (He and Mamaysky, 2005) and (Ly Vath et al., 2007). Let’s consider this price impact function for the moment. In this case we have the following:

Theorem 3.3.

if and only if .

Proof.

If then and therefore for . By the uniqueness result for optimal stopping problems (see Theorem 3.1 in (Øksendal and Reikvam, 1998))

that is . Suppose that

for . This means that for . Therefore and satisfies the HJB equation (3.4) with . Also, satisfies the growth condition and has the same boundary conditions as by (2.13). By Theorem 3.2, we have that . To prove the second equality we will do induction in the number of trades. Note that the function in attains its maximum at . Then,

Now, let . Hence,

On the other hand, by induction hypothesis we have

Combining both inequalities above we have

Again, by Lemma 7.1 in (Øksendal and Sulem, 2005), the left hand side converges to as . Clearly the other inequality holds and the proof is complete. ∎

Example

Consider the case where the price process is a geometric Brownian motion. This is the only process that is considered in the papers (Subramanian and Jarrow, 2001; He and Mamaysky, 2005; Ly Vath et al., 2007). The unperturbed price process is

with . It is easy to see that the value function is finite if and only if . In this case the function takes the form

where , therefore condition (2.24) holds. Now, the condition (2.13) reads

This implies that . We can see that in this case the value function is not attainable with any impulse control, but we can approach it by trading smaller and smaller orders. We will show now how we can approach with singular (in fact regular) controls. Let and consider the strategy , that is, selling shares at a constant speed until the investor executes the position. Then,

and

by using Fubini’s theorem since the integrand is positive. Taking this expression converges to .

4 Connection between both formulation

Theorem 3.3 shows that for a special case, i.e., the value function of two different problems are the same. We are going to show that this is not a coincidence. Let us start with some notation: Given and we denote:

and

Lemma 4.1.

For all we have

Proof.

It is clear that is an upper bound. Let , then there is and such that

For any we have that

∎

Theorem 4.2.

Proof.

First, consider the case when there is no impact in the price. Then and by proposition 2.1 , where . Since is viscosity solution of

Then is solution of (3.4).

Assume now that there is price impact. We know that satisfies the equation

Supersolution property: Let and such that is a minimizer of on with . Hence, . Now, let such that . Thus,

Since , then . This implies that is a maximum for , therefore

Subsolution property: Let and such that is a maximizer of on with . Without loss of generality we can assume that is a strict local maximum, that is, there exists such that is maximum of over . Let be a sequence in such that and

Recall that is continuous and is the unique viscosity solution of

| (4.1) |

for all . Let be a maximum of over and let be a limit point of as . For all and all we have that

By lemma 4.1, taking along the sequence such that , we have that for all

Taking we obtain that

and therefore since is a strict local maximum. Thus, as . Let , since , then for a fix large enough and for small enough . Hence

The above shows that is a local maximum of over where , and as . Since is subsolution of (4.1), we can consider two cases:

-

•

There exists a sequence such that . Taking along the sequence we have that

and is subsolution.

-

•

For all small enough . This implies that there exists such that

(4.2) Let be a limit point of as . We claim that : Suppose , then for small enough such that

where the second inequality follows from (2.4) and the definition of . Now, since is strictly decreasing in (otherwise condition (2.4) cannot hold) we can choose small such that and we get a contradiction.

∎

5 Computational Examples

We are going to present different choices of price processes. Throughout this section we will consider the price impact function:

In the following examples, analytical solutions for do not seem easy to find, so we used an implicit numerical scheme following chapter 6 in (Kushner and Dupuis, 1992). In particular, we used the Gauss-Seidel iteration method for approximation in the value space. Additionally, for the impulse control case we followed the iterative procedure described in (Øksendal and Sulem, 2005).

5.1 Impulse control with positive fixed transaction cost

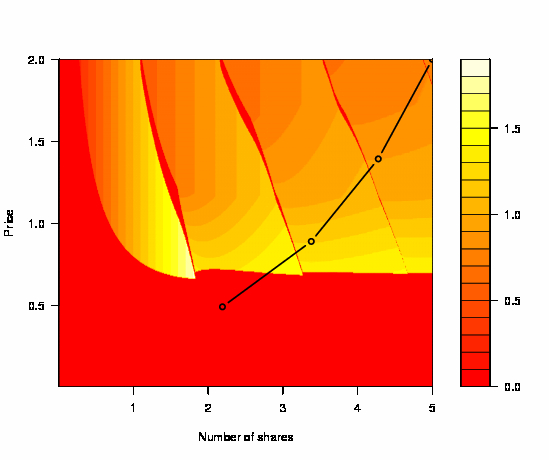

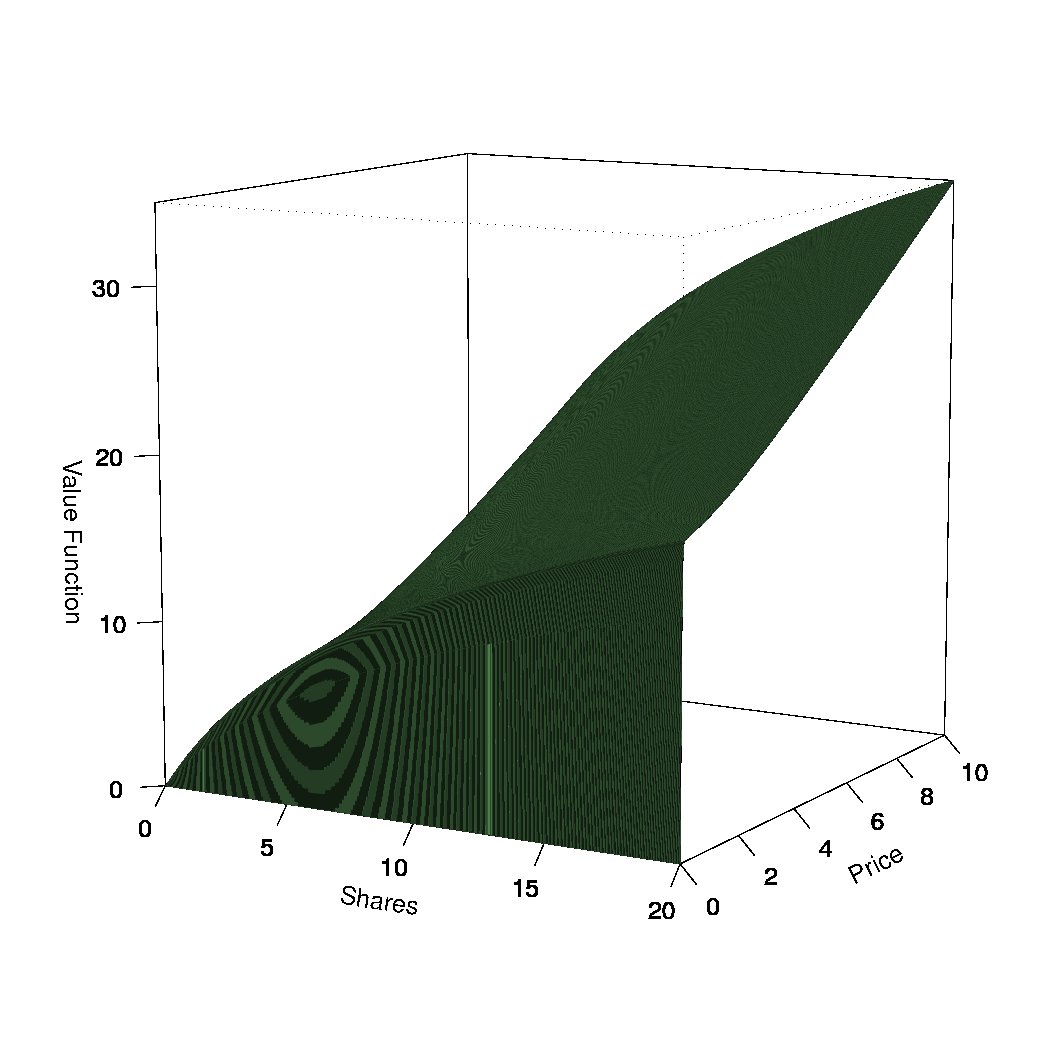

Consider the price process following a geometric Brownian motion with so that the value function is finite. Figure 1 shows the contour plot of the optimal number of shares the investor need to trade. The figure also shows the optimal strategy when the investor starts with 5 shares at a price of 2. At time 0, the investor needs to trade three times until the state variable enters the continuation region (i.e. when the optimal number of shares is 0).When is smaller, the number of trades at time 0 increases and the continuation region shrinks. When we obtain the situation described in theorem 3.3.

5.2 Singular control

Consider the case when the price process follows an arithmetic Brownian motion. Then the price dynamics are

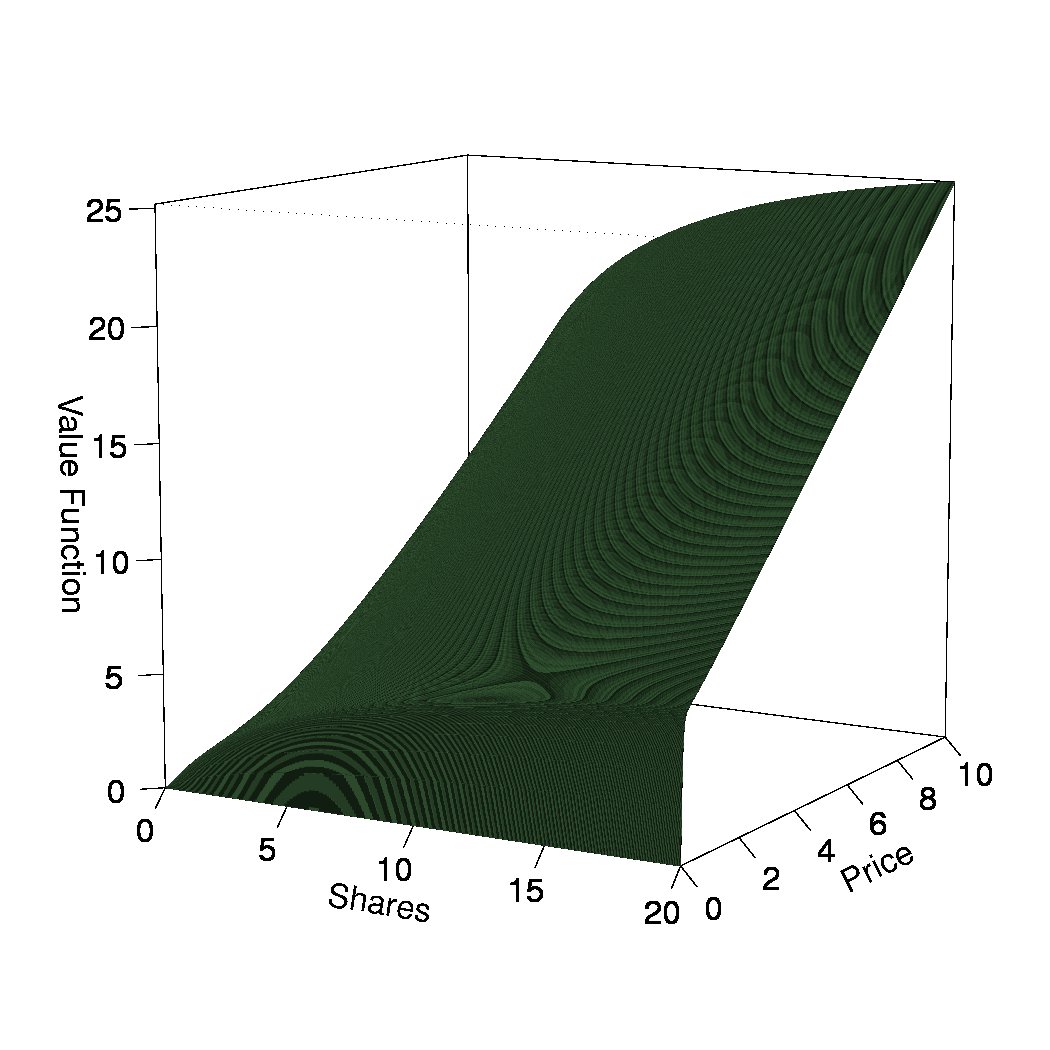

with . In this case the value function is always finite, regardless of , due to the exponential decay of the discount factor. Since 0 is an absorbing boundary for this process the boundary conditions are given by (2.17). Figure 2(a) shows the value function obtained by the scheme.

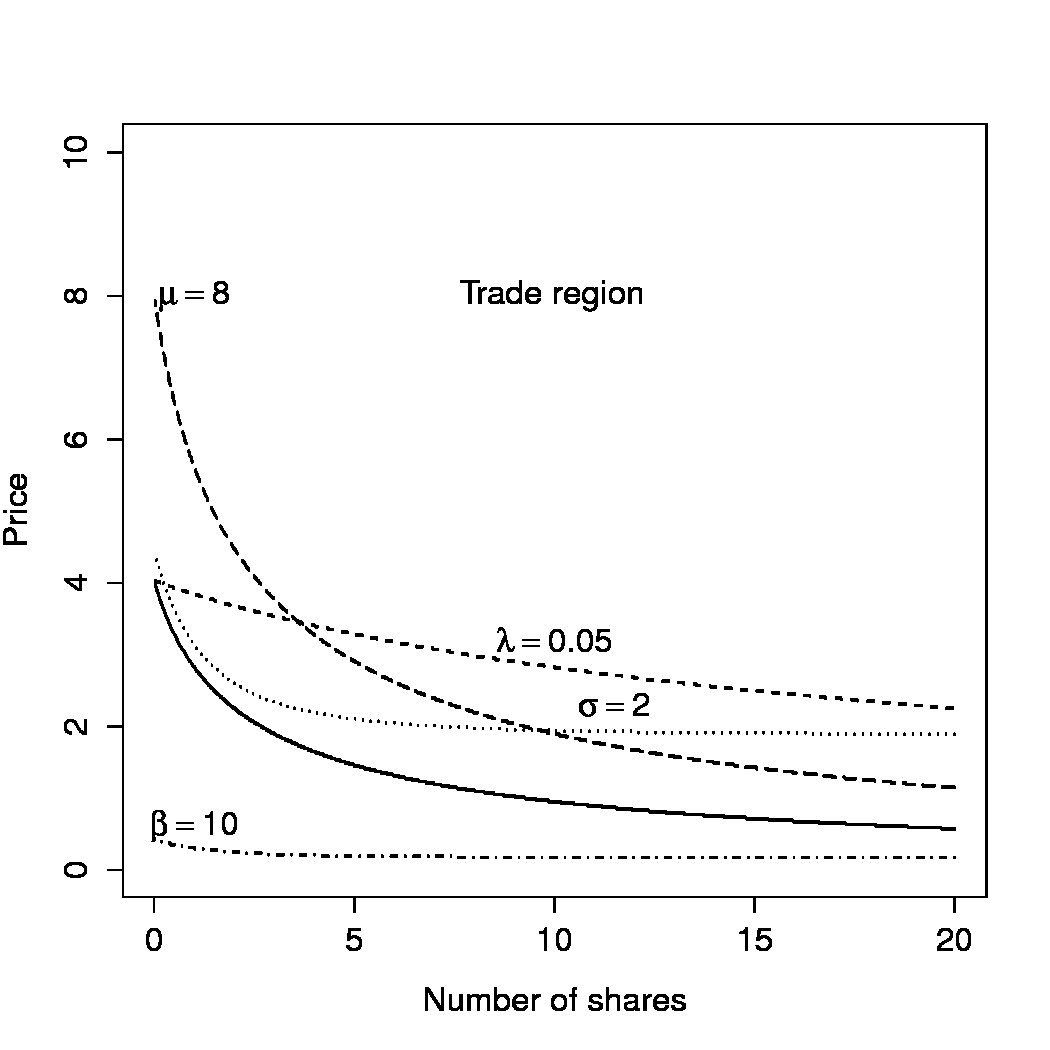

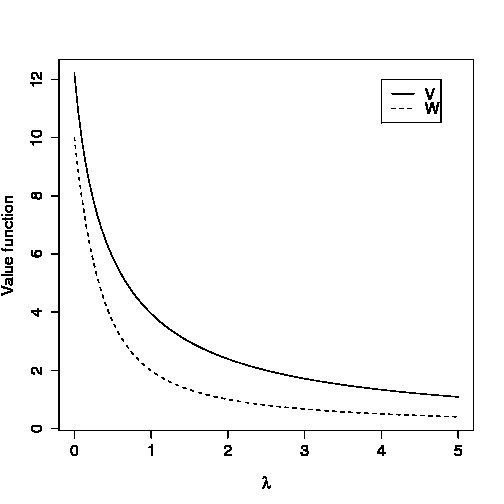

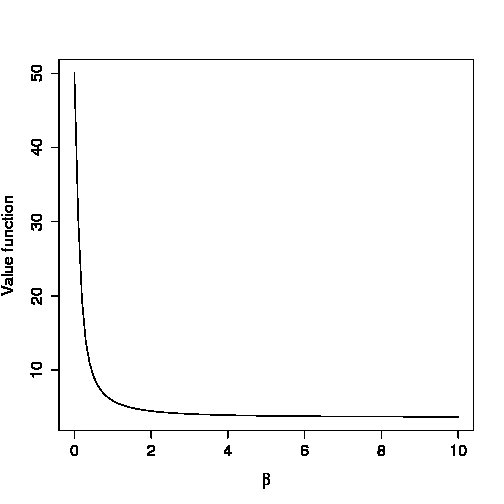

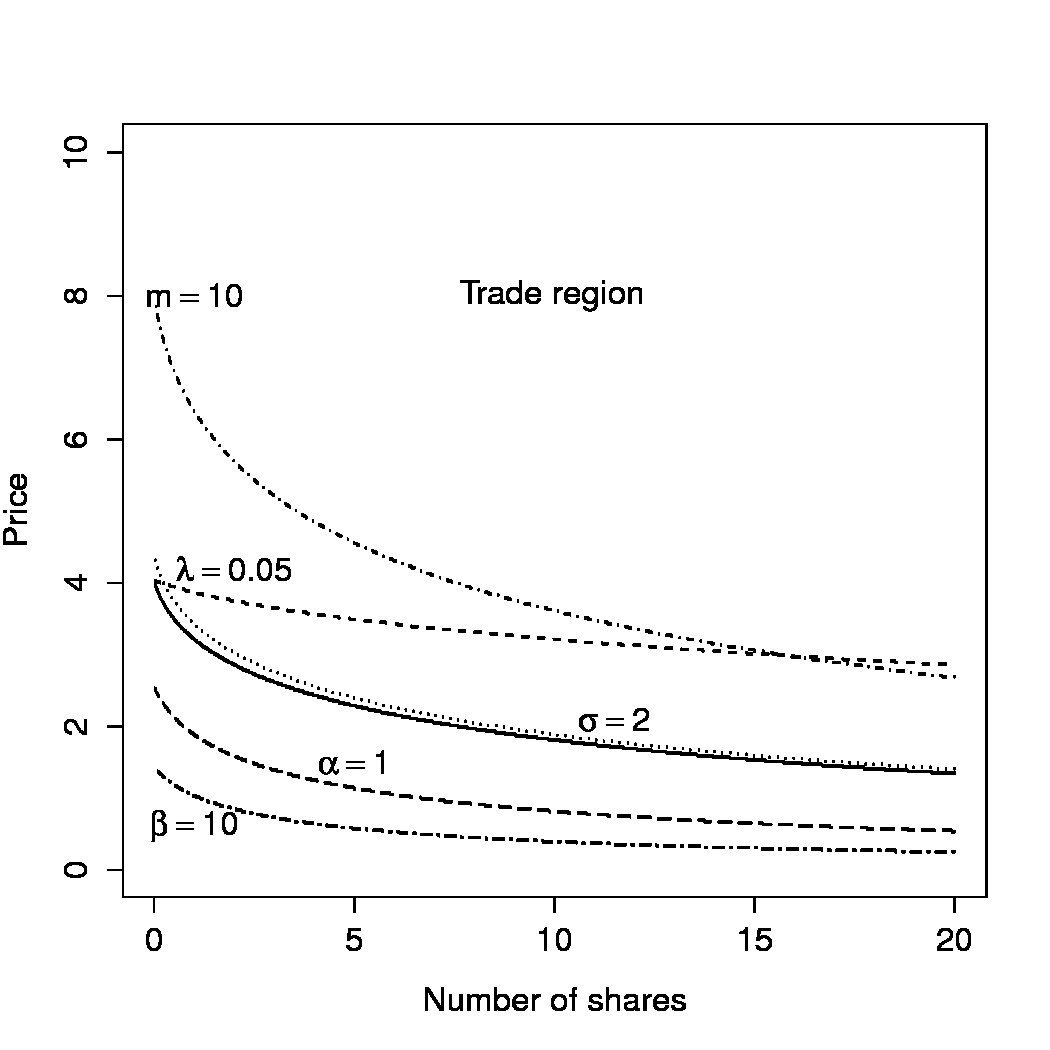

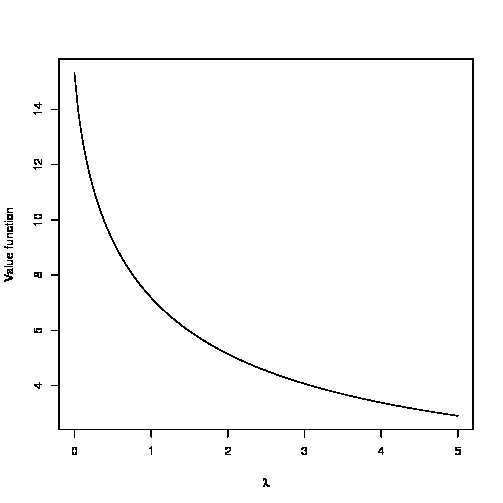

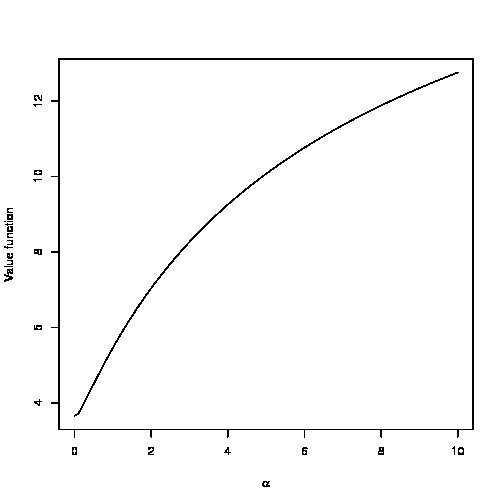

First note that the conditions of Theorem 3.3 are not satisfied, that is , and therefore , as shown in figure 2(b). Thus, in this case the optimal strategy would be to trade very fast in the trading region until the state variable hit the free boundary. The figure also shows how the different parameters affect the continuation/trade regions. Now, let’s see how the change in the parameters of the model affect the value function . Figure 3(a) shows that the value function is very sensitive to changes in the parameter for small values but not so much for large values. This behavior is common to both processes GBM (described by theorem 3.3) and BM. This means that the bigger the investor (i.e. the larger the price impact) the less sensitive to small changes in the value of . Clearly the value function decreases as the impact increases.

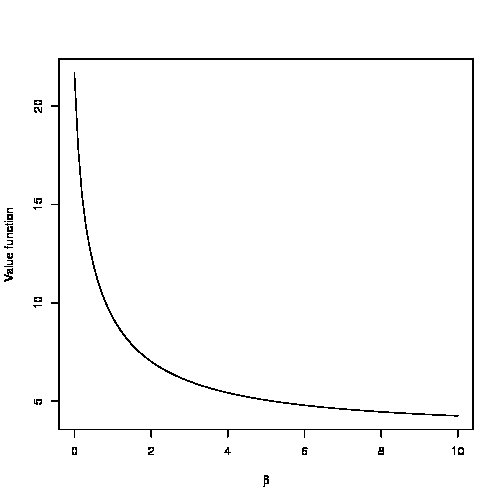

If , the value function would not be finite for any , so small values of yield a very large value of . As increases the effect in is diminishing. Also, the investor has to act greedily and therefore the trade region approaches to and approaches to .

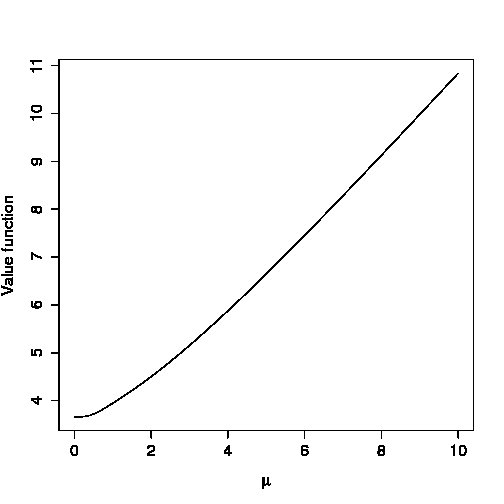

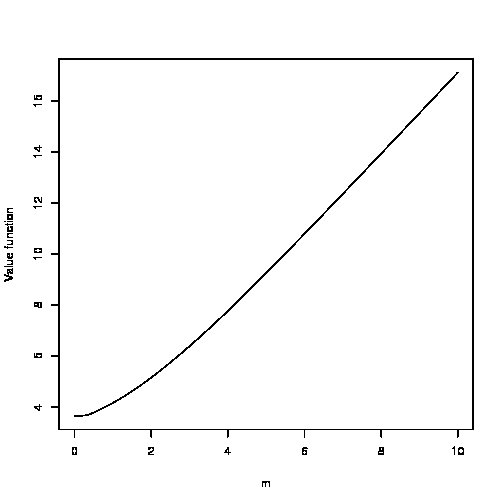

For it is not optimal to wait at all, so , but as increases clearly the value function increases in an almost linear fashion.

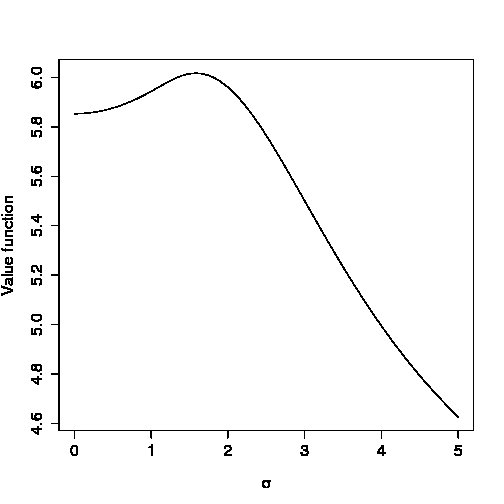

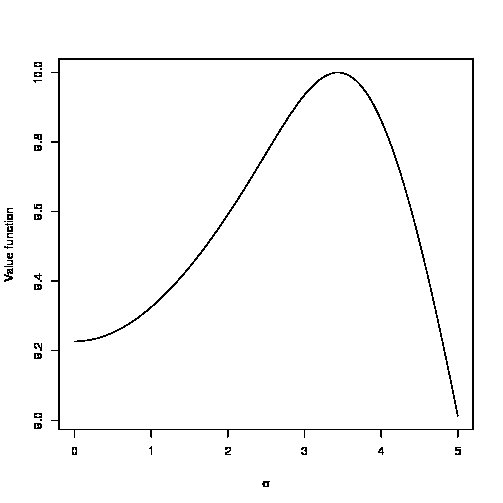

The effect of in the value function is probably the most interesting one. In figure 3(d) we see that it is beneficial for the investor to have some variance in the asset but not too much. An explanation for this is that when the variance increases it is more likely for the price process to enter the trading region. On the other hand, if the variance is too big, the process can hit 0 too fast. Clearly the variance of the revenue increases with , thus as part of future research it would be interesting to consider the risk aversion of the investor.

The second example is when the price follows the Ornstein–Uhlenbeck process. Then the price process becomes

with . As in the case of arithmetic Brownian motion, the boundary conditions are given by (2.17), since 0 is an absorbing boundary for this process. Figure 4 shows the value function and the continuation-trade region. Again, this case does not fit within Theorem 3.3, so the strategy is similar to the BM case. Also, the sensitivity of the function to the parameters is similar to the previous case. The only parameter that is exclusive to the mean-reverting process is the resilience factor . As we increase the value function increases (Figure 5(d)) and the continuation region grows (Figure 4(b)).

6 Conclusions

The main goal of this work was to characterize the value function of the optimal execution strategy in the presence of price impact and fixed transaction cost over an infinite horizon. We formulated the problem using two different stochastic control settings. In the impulse control formulation we showed that the value function is the unique continuous viscosity solution of the Hamilton-Jacobi-Bellman equation associated to the problem whenever the transaction cost is strictly positive. The second formulation ruled out any transaction cost and admitted continuous singular controls only. In this case we also proved continuity and uniqueness of the value function under the viscosity framework. The next step, part of future research, would be to find the regularity of the value function. Numerical results provided in this paper, at least for the second formulation, suggest that the function is more than just continuous and that its regularity is related with the regularity of the function defined in Section 2. Although any impulse control is a singular control, in general the expected revenue obtained when applying the same impulse control in both formulation is different. However, the value function may be the same. In fact, we were able to show that this is the case for a special type of price impact and provide the explicit solution. The question if this is true in general is still unanswered. This is particularly challenging since the subsolution property for the HJB equation (2.9), when there is no transaction cost, has no information at all. Try to find answers is part of future work. Another important conclusion is that the HJB equation for the regular control formulation, (LABEL:hjbreg) has not enough information to characterize the solution. From an economic viewpoint, it would be important to study the effect of the price impact in hedging strategies and how they are different to the strategies obtained in classical models, e.g. Delta-hedging in Black-Scholes setting. Include utility functions to account for risk aversion is another important extension of this work. Finally, the finite time horizon natural extension is currently in preparation.

Appendix A Proof of

Let be a locally bounded function on . Let be a sequence in such that and

Since is usc and is continuous, for each there exists such that

The sequence is bounded (since ) and therefore converges along a subsequence to . Hence

References

- Almgren (2003) R. Almgren. Optimal execution with nonlinear impact functions and trading-enhanced risk. Applied Mathematical Finance, 10(1):1–18, January 2003.

- Almgren and Chriss (2000) R. Almgren and N. Chriss. Optimal execution of portfolio transactions. Journal of Risk, 3:5–39, 2000.

- Bank and Baum (2004) P. Bank and D. Baum. Hedging and portfolio optimization in financial markets with a large trader. Math. Finance, 14(1):1–18, 2004.

- Bertsimas and Lo (1998) D. Bertsimas and A. W. Lo. Optimal control of execution costs. Journal of Financial Markets, 1(1):1–50, April 1998.

- Çetin et al. (2004) U. Çetin, R. Jarrow, and P. Protter. Liquidity risk and arbitrage pricing theory. Finance Stoch., 8(3):311–341, 2004.

- Chan and Lakonishok (1995) L.K.C. Chan and J. Lakonishok. The behavior of stock prices around institutional trades. Journal of Finance, 50(4), September 1995.

- Crandall et al. (1992) M. G. Crandall, H. Ishii, and P. L. Lions. User’s guide to viscosity solutions of second order partial differential equations. Bulletin of the American Mathematical Society, 27(12):1–67, July 1992.

- Cvitanić and Ma (1996) J. Cvitanić and J. Ma. Hedging options for a large investor and forward-backward SDE’s. Ann. Appl. Probab., 6(2):370–398, 1996.

- Davis and Norman (1990) M.H.A. Davis and A.R. Norman. Portfolio selection with transaction costs. Math. Oper. Res., 15(4):676–713, 1990.

- Dayanik and Karatzas (2003) S. Dayanik and I. Karatzas. On the optimal stopping problem for one-dimensional diffusions. Stochastic Processes and their Applications, 107(2):173–212, October 2003.

- Fleming and Soner (2006) W.H. Fleming and H.M. Soner. Controlled Markov Processes and Viscosity Solutions. Springer, second edition, 2006.

- Frey (1998) R. Frey. Perfect option hedging for a large trader. Finance and Stochastics, 2(2):115–141, 1998.

- He and Mamaysky (2005) H. He and H. Mamaysky. Dynamic trading policies with price impact. Journal of Economic Dynamics and Control, 29(5):891–930, 2005.

- Holthausen et al. (1990) R.W. Holthausen, R. Leftwich, and D. Mayers. Large-block transactions, the speed of response, and temporary and permanent stock-price effects. Journal of Financial Economics, 26(1):71–95, July 1990.

- Ishii and Lions (1990) H. Ishii and P. L. Lions. Viscosity solutions of fully nonlinear second-order elliptic partial differential equations. Journal of Differential Equations, 83(1):26 – 78, 1990.

- Ishii (1993) K. Ishii. Viscosity solutions of nonlinear second order elliptic pdes associated with impulse control problems. Funkcialaj Ekvacioj, 36:123–141, 1993.

- Ishikawa (2004) Y. Ishikawa. Optimal control problem associated with jump processes. Applied Mathematics and Optimization, 50(1):21–65, 2004.

- Korn (1998) R. Korn. Portfolio optimisation with strictly positive transaction costs and impulse control. Finance and Stochastics, 2(2):85–114, 1998.

- Kushner and Dupuis (1992) H. Kushner and P. Dupuis. Numerical methods for stochastic control problems in continuous time. Springer-Verlag, New York, 1992.

- Ly Vath et al. (2007) V. Ly Vath, M. Mnif, and H. Pham. A model of optimal portfolio selection under liquidity risk and price impact. Finance Stoch., 11(1):51–90, 2007.

- Ma and Yong (1999) Jin Ma and Jiongmin Yong. Dynamic programming for multidimensional stochastic control problems. Acta Mathematica Sinica, 15:485–506, 1999. ISSN 1439-8516.

- Øksendal and Reikvam (1998) B. Øksendal and K. Reikvam. Viscosity solutions of optimal stopping problems. Stochastics An International Journal of Probability and Stochastic Processes: formerly Stochastics and Stochastics Reports, 62(3):285– 301, 1998.

- Øksendal and Sulem (2002) B. Øksendal and A. Sulem. Optimal consumption and portfolio with both fixed and proportional transaction costs. SIAM Journal on Control and Optimization, 40(6):1765–1790, 2002.

- Øksendal and Sulem (2005) B. Øksendal and A. Sulem. Applied Stochastic Control of Jump Diffusions. Springer, 2005.

- Protter (2004) P. Protter. Stochastic Integration and Differential Equations. Springer-Verlag, Berlin, second edition, 2004.

- Schied and Schöneborn (2009) A. Schied and T. Schöneborn. Risk aversion and the dynamics of optimal liquidation strategies in illiquid markets. Finance Stoch., 13(2):181–204, 2009.

- Schied et al. (2010) A. Schied, T. Schöneborn, and M. Tehranchi. Optimal Basket Liquidation for CARA Investors is Deterministic. Applied Mathematical Finance, 17:471–489, 2010.

- Subramanian and Jarrow (2001) A. Subramanian and R. Jarrow. The liquidity discount. Mathematical Finance, 11(4):447–474, 2001.