On Practical Algorithms for Entropy Estimation and the Improved Sample Complexity of Compressed Counting

Ping Li

Department of Statistical Science

Faculty of Computing and Information Science

Cornell University

Ithaca, NY 14853

pingli@cornell.edu

Abstract

The long-standing problem of Shannon entropy estimation in data streams (assuming the strict Turnstile model) is now an easy task by using the technique proposed in this paper. Essentially speaking, in order to estimate the Shannon entropy with a guaranteed -additive accuracy, it suffices to estimate the th frequency moment, where , with a guaranteed -multiplicative accuracy, where . Previous studies have shown that has to be extremely small (e.g., or even much smaller). In other words, the sample complexity for entropy estimation is , where is the coefficient essentially determined by the variance of the estimator of frequency moments. In this paper, the proposed algorithm achieves and hence is a practical technique with complexity (which is essentially if we consider ). We provide the (small) complexity bound constants numerically (for ) and analytically (for small ).

Prior well-known algorithms based on symmetric stable random projections could only achieve , meaning that the sample complexity would be , which will be extremely large. For example, if and , then .

Compressed Counting (CC)[27], based on maximally skewed stable random projections, was recently proposed for estimating the th frequency moment of data streams. [27] proposed algorithms for CC based on the geometric mean and harmonic mean estimators. It was proved that the geometric mean estimator could achieve , leading to an algorithm, which unfortunately could still be impractical. In this paper, we prove that the harmonic mean estimator for CC also could only achieve .

The proposed new estimator for CC has a simple clean form: , where ’s are the projected data and is the sample size. We prove that its variance achieves , leading to a practical algorithm with complexity . In other words, if , the new algorithm improves the prior algorithms based the symmetric stable random projections roughly by a factor of ; and it improves the geometric/harmonic mean algorithms for CC roughly by a factor of .

Our extensive experiments (in the Appendix) verify that, using the proposed algorithm, samples could provide accurate estimates of the Shannon entropy. The proposed algorithm is also numerically very stable, even for as small as .

1 Introduction

The problem of “scaling up for high dimensional data and high speed data streams” is among the “ten challenging problems in data mining research”[39]. This paper is devoted to estimating entropy of data streams. Mining data streams[20, 4, 1, 32] in (e.g.,) 100 TB scale databases has become an important area of research, e.g., [10, 1], as network data can easily reach that scale[39]. Search engines are a typical source of data streams[4].

Consider the Turnstile stream model[32]. The input stream , arriving sequentially describes the underlying signal , meaning

(1)

where the increment can be either positive (insertion) or negative (deletion). Restricting results in the strict-Turnstile model, which suffices for describing almost all natural phenomena[32].

This study focuses on the relaxed strict-Turnstile model and studies efficient algorithms for estimating the th frequency moment of data streams

(2)

We are particularly interested in the case of , which is very important for estimating Shannon entropy.

The relaxed strict-Turnstile model only requires at the time one cares about (e.g., the end of streams); and hence it is considerably more flexible than the strict-Turnstile model.

1.1 Entropy, Moments, and Estimation Complexity

A very useful (e.g., in Web and networks[12, 25, 40, 30] and neural comptutations[33]) summary statistic is the Shannon entropy

(3)

Various generalizations of the Shannon entropy have been proposed. The Rényi entropy[34], denoted by , and the Tsallis entropy[19, 36], denoted by , are respectively defined as

(4)

(5)

As , both Rényi entropy and Tsallis entropy converge to Shannon entropy:

. Thus, both Rényi entropy and Tsallis entropy can be computed from the th frequency moment; and one can approximate Shannon entropy from either or by letting . Several studies[40, 18, 17]) used this idea to approximate Shannon entropy, all of which relied critically on efficient algorithms for estimating the th frequency moments (2) near . In fact, one can numerically verify that the values proposed in [18, 17] are extremely close to 1, for example, [18, Alg. 1] or [17] are quite likely.111

In [18, Alg. 1], , , where is the number of streaming updates. If we let , , , then . If we let , , then .

[17, Sec. 4.2.2 and 5.2] provides some improvements, to allow larger . If and , then . If and , then .

From the definition of the Rényi and Tsallis entropies, it is clear that, in order to achieve a -additive guarantee for the Shannon entropy, it suffices to estimate the th frequency moment with an guarantee (for sufficiently small ). For example, suppose an estimator guarantees (with high probability) that , then the estimated Rényi entropy, denoted by would satisfy , assuming is sufficiently small.

Another perspective is from the estimation variances. From the definitions of the Rényi and Tsallis entropies, it is clear that we need estimators of the frequency moments with variances proportional to in order to cancel the term . The estimation variance, of course, is also closely related to the sample complexity.

Suppose we have an unbiased estimator of whose variance is , where is the sample size. Then the sample complexity is essentially , using the standard argument popular in the theory literature, e.g., [23]. The space complexity (in terms of bits) will be .

The drawback of this argument is that it does not fully specify the constants.

In a summary, in order to provide a (e.g., 0.1) additive approximation of the Shannon entropy, one should use samples for estimating the th frequency moments. This bound initially appears disappointing, because, if for example, , , , then it requires samples, which is very likely impractical. Well-known algorithms based on symmetric stable random projections[21, 26] indeed exhibit .

1.2 Some Applications of Shannon Entropy

1.2.1 Real-Time Network Anomaly Detection

Network traffic is a typical example of high-rate data streams. An effective and reliable measurement of network traffic in real-time is crucial for anomaly detection and network diagnosis; and one such measurement metric is Shannon entropy[12, 24, 38, 7, 25, 40]. The Turnstile data stream model (1) is naturally suitable for describing network traffic, especially when the goal is to characterize the statistical distribution of the traffic. In its empirical form, a statistical distribution is described by histograms, , to . It is possible that (IPV6) if one is interested in measuring the traffic streams of unique source or destination.

The Distributed Denial of Service (DDoS) attack is a representative example of network anomalies. A DDoS attack attempts to make computers unavailable to intended users, either by forcing users to reset the computers or by exhausting the resources of service-hosting sites. For example, hackers may maliciously saturate the victim machines by sending many external communication requests. DDoS attacks typically target sites such as banks, credit card payment gateways, or military sites.

A DDoS attack changes the statistical distribution of network traffic. Therefore, a common practice to detect an attack is to monitor the network traffic using certain summary statistics. Since Shannon entropy is a well-suited for characterizing a distribution, a popular detection method is to measure the time-history of entropy and alarm anomalies when the entropy becomes abnormal[12, 25].

Entropy measurements do not have to be “perfect” for detecting attacks. It is however crucial that the algorithm should be computationally efficient at low memory cost, because the traffic data generated by large high-speed networks are enormous and transient (e.g., 1 Gbits/second). Algorithms should be real-time and one-pass, as the traffic data will not be stored[4]. Many algorithms have been proposed for “sampling” the traffic data and estimating entropy over data streams[25, 40, 6, 16, 3, 8, 18, 17],

1.2.2 Entropy of Query Logs in Web Search

The recent work[30] was devoted to estimating the Shannon entropy of MSN search logs, to help answer some basic problems in Web search, such as, how big is the web?

The search logs can be viewed as data streams, and [30] analyzed several “snapshots” of a sample of MSN search logs. The sample used in [30] contained 10 million Query, URL,IP triples; each triple corresponded to a click from a particular IP address on a particular URL for a particular query. [30] drew their important conclusions on this (hopefully) representative sample. Alternatively, one could apply data stream algorithms such as CC on the whole history of MSN (or other search engines).

1.2.3 Entropy in Neural Computations

A workshop in NIPS’03 was devoted to entropy estimation, owing to the wide-spread use of Shannon entropy in Neural Computations[33]. (http://www.menem.com/~ilya/pages/NIPS03) For example, one application of entropy is to study the underlying structure of spike trains.

1.3 Previous Algorithms for Estimating Frequency Moments

The problem of approximating has been very heavily studied in theoretical computer science and databases, since the pioneering work of [2], which studied , 2, and . [11, 21, 26] provided improved algorithms for . [22] provided algorithms for to achieve the lower bounds proved by

[35, 5, 37]. [14] suggested using even more space to trade for some speedup in the processing time.

Note that the first moment (i.e., the sum), , can be computed easily with a simple counter[31, 13, 2]. This important property was recently captured by the method of Compressed Counting (CC)[27], which was based on the maximally-skewed stable random projections.

[27] provided two algorithms, based on the geometric mean and harmonic mean,222

The geometric mean and harmonic mean algorithms could be empirically improved using another algorithm based on numerical optimizations[28], which is very difficult for precise theoretical analysis (variances and bounds).

and proved some important theoretical results:

•

The geometric mean algorithm has the variance proportional to in the neighborhood of , where . This is the first algorithm that captured the intuition that, in the neighborhood of , the moment estimation algorithms should work better and better as , in a continuous fashion.

Our comments: The geometric mean algorithm, unfortunately, did not provide an adequate mechanism for entropy estimation. As previously discussed, this methods leads to an entropy estimation algorithm with complexity , which is actually quite intuitive from the definitions of the Tsallis entropy and Rényi entropy. Both entropies contain the terms, meaning that the variance will blow up as , which can not be canceled by . Note that [27] did not show the variance of the harmonic mean algorithm is also proportional to ; this paper will provide the proof.

•

For fixed , as , the sample complexity bound of the geometric mean algorithm is with all constants specified. This result was a major improvement over the well-known bound[37, 21, 26]. Note that the assumption of fixing and letting is needed for theoretical convenience in order to derive bounds with no unspecified constants. This study will continue to use this assumption.

Our comments: When , the moment estimation problem is trivial and only requires one simple counter. Therefore, even intuitively, can not possibly be the true complexity bound.

2 The Proposed Algorithm

We consider the relaxed strict-Turnstile model (1). Conceptually, we multiply the data stream vector by a random projection matrix . The resultant vector is only of length . More specifically, the entries of the projected vector are

’s are random variables generated from the following (non-standard) skewed stable distribution[41]:

(6)

where (i.i.d.) and (i.i.d.), an exponential distribution with mean 1. We use this formulation to avoid numerical problems and simplify the analysis.

Of course, in data stream computations, the matrix is never fully materialized. The standard procedure in data stream computations is to generate entries of on-demand[21]. In other words, whenever an stream element arrives, one updates entries of as

The proposed algorithm is defined as follows:

(7)

The following Theorem proves that this new estimator is (asymptotically) unbiased with the variance proportional to . Note that as .

In this paper, we only consider . This is because the maximally-skewed stable distributions have good theoretical properties when [27]; for example, all negative moments exist; see Lemma 2.

2.1 Review Maximally-Skewed Stable Random Projections and Estimators

The standard procedure for sampling from skewed stable distributions is based on the Chambers-Mallows-Stuck method[9]. To generate a sample from , i.e., -stable, maximally-skewed (), with unit scale, one first generates an exponential random variable with mean 1, , and a uniform random variable , then,

(10)

where when and when .

Note that as . For convenience (and avoiding numerical problems), we will use

In this study, we will only consider , i.e, . After simplification, we obtain

Therefore, CC boils down to estimating from i.i.d. stable samples. [27] provided two statistical estimators, the geometric mean and harmonic mean estimators, which are derived based on the following basic moment formula.

Assume , to , are i.i.d. samples from . After simplifying the corresponding expression in [27], we obtain

(12)

which is unbiased and has asymptotic variance

(13)

As , the asymptotic variance approaches zero at the rate of only , which is not adequate.

2.1.2 The Harmonic Mean Estimator

(14)

which is asymptotically unbiased and has variance

(15)

[27] only graphically showed that the harmonic mean estimator is noticeably better than the geometric mean estimator. We prove the following Lemma, which says the variance of the harmonic mean is also proportional to . Thus, the harmonic mean estimator is not adequate for entropy estimation either.

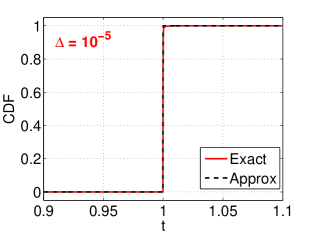

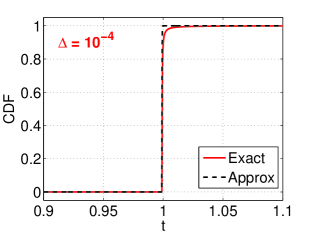

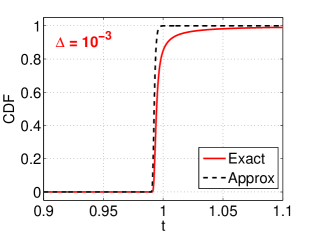

Note that approaches zero as . Thus, one might be wondering if we replace by , the errors may be quite small. This conjecture is verified in Figure 1.

Figure 1: We plot the CDF curves as derived in Lemma 4, for , , and . As , the exact CDF (solid curves) is very close to the approximate CDF (dashed curves), which we obtain by replacing the exact function in Lemma 4 with the limit .

2.3 The Intuition Behind the Proposed Algorithm

Basically, we derive the proposed estimator by “guessing.” We first derive a maximum likelihood estimator (MLE) for a slightly different distribution based on the intuition from Lemma 4 and Figure 1. Then we verify that this MLE is actually a very good estimator (in terms of both the variances and tail bounds) for the stable distribution we care about.

Here, we consider a random variable whose cumulative distribution function (CDF) is

(17)

It is indeed a CDF because it is an increasing function of , , and .

Similar to stable random projections, we are interested in estimating from i.i.d. samples , to . Statistics theory tells us that the maximum likelihood estimator (MLE) has the (asymptotic) optimality. Because the distribution function of is known, we can actually compute the MLE in this case.

Theorem 2

Suppose , to , are i.i.d. samples from a distribution whose CDF is given by (17). Let , where . Then the maximum likelihood estimator of is given by

Compared with the proposed estimator in (7), the MLE solution has the addition term of . Note that, while both and approach 1, considerably slower than , because

For example, when , , ; when , , .

Therefore, while may be considered negligible, it may be preferable to keep . In fact, when proving that the proposed estimator is (asymptotically) unbiased (see Appendix A), we do need the term.

is asymptotically unbiased with variance proportional to . Using the standard argument, we know that the sample complexity bound must be . We are, however, very interested in the precise complexity bounds, not just the orders.

Normally, we would like to present the tail bounds as, e.g., , which immediately leads to the statement that:

With probability at least , it suffices to use to guarantee .

Ideally, we hope will be as small as possible. In fact, in order to achieve a -additive algorithm for entropy estimation, we need (where or even much smaller). Therefore, we really need . In this sense, it is no longer appropriate to treat as a “constant.”

These bounds appear to be too complicated to gain insightful information. People may be even wondering about numerical stability of the infinite sums.

First of all, we notice that when (i.e., ), we can compute the tail bounds exactly, as presented in Lemma 5.

Lemma 5

When , i.e., ,

(23)

(24)

Proof: When (), we have , , , and . The conclusions follow easily.

Next, we re-formulate the tail bounds to facilitate numerical evaluations. Our numerical results show that, when is small, and , for . Thus, we indeed have an algorithm for entropy estimation with complexity .

The tail bounds (19) and (21) contain , which can be written as

Thus, for numerical reasons, we can rewrite (19) and (21) as

The infinite series always converge provided and . In fact, because the bounds hold for any (not necessarily the optimal values, and ), we know and if using (e.g.,) . In other words, and , as desired. We state this as a Lemma.

Therefore, to estimate within a factor, it suffices to let the sample size , using the proposed estimator .

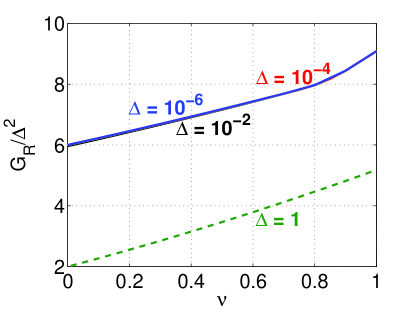

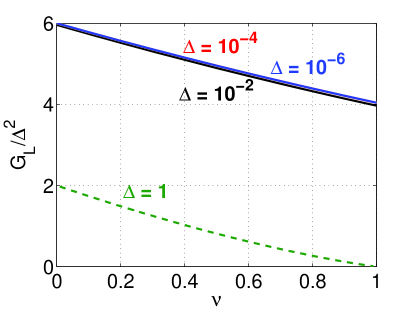

Figure 2 presents the values in terms of and for and , , , together with the closed-form expressions for as obtained in Lemma 5. The values are pleasantly small. Thus, at least numerically, we can say, for example, when is small,

In other words, with a probability at least , using the proposed estimator, one can achieve by using samples. And we know the constant 9 could be replaced by 6 if is small.

Figure 2: Numerical values of and in the tail bounds (19) and (21), for , , and , together with the closed-form expressions for as obtained in Lemma 5. Because and , we present the results in terms of and . Note that as , both and approach , as proved in Lemma 7. Also, note that the curves for , , and largely overlap.

Whenever possible, analytical expressions are always more desirable. In fact, when , we can actually obtain the analytical expressions for and .

In the previous (unpublished) work[29], we proposed the sample minimum estimator, which allowed us to prove a much improved sample complexity bound than that in [27]. Interestingly, the proposed estimator in this paper actually converges to the sample minimum estimator, denoted by ,

(26)

This fact is quite intuitive. As , the smallest one of ’s is amplified the most by . This is analogous to the well-know fact that, the norm approaches the norm (which is the maximum element of the vector), as .

In [29], we proved the following (closed-form) sample complexity bound for :

Basically, in terms of , Theorem 4 is applicable when is large () and is small. A simulation study in [29] demonstrated that the bound in Theorem 4 can be very sharp.

5 Conclusion

Real-world data are often dynamic and can be modeled as data streams. Measuring summary statistics of data streams such as the Shannon entropy has become an important task in many applications, for example, detecting anomaly events in large-scale networks. One line of active research is to approximate the Shannon entropy using the th frequency moments of the stream with very close to 1 (e.g., or even much smaller).

Efficiently approximating the th frequency moments of data streams has been very heavily studied in theoretical computer science and databases. When , it is well-known that efficient -space algorithms exist, for example, symmetric stable random projections[21, 26], which however are impractical for estimating Shannon entropy using extremely close to 1. Recently, [27] provided an algorithm to achieve the bound in the neighborhood of , based on the idea of maximally-skewed stable random projections (also called Compressed Counting (CC)). The algorithms provided in [27], however, are still impractical.

In this paper, we provide a truly practical algorithm for entropy estimation. We prove that its variance is proportional to whereas previous algorithms for CC developed in [27] have variances proportional only to . This new algorithm leads to an algorithm for entropy estimation to achieve -additive accuracy, while previous algorithms must use samples [21, 26], or samples [27]. Note that because is so small, it is no longer appropriate to treat it as “constant.”

We also analyze the precise sample complexity bound of the proposed new estimator, both numerically (for general ) and analytically (for small ), to demonstrate that the sample complexity bound of the new estimator is free of large constants. This further confirms that our proposed new estimator is practical.

Recall . We will basically proceed by using the “delta” method popular in statistics. We need to be a bit careful here as is small. Just to make sure the resultant higher-order terms are indeed negligible, we carry out the algebra.

We have derived and in Theorem 3. The task of this Lemma is to show that, as ,

To proceed with the proof, we first assume that, as , we have

which can be later verified. With this assumption, we can expand :

Setting the first derivative to zero,

we obtain

which verifies that is indeed on the order of . Therefore,

Thus, we have proved that as . A similar procedure can also prove .

Appendix G Experiments

This section demonstrates that the proposed estimator in (7) for Compressed Counting (CC) is a truly practical algorithm, while the previously proposed geometric mean algorithm[27] for CC is inadequate for entropy estimation. We also demonstrate that algorithms based on symmetric stable random projections [21, 27] are not suitable for entropy estimation.

G.1 Data

Since the estimation accuracy is what we are interested in, we can simply use static data instead of real data streams. This is because the projected data vector is the same at the end of the stream (i.e., time ), regardless whether it is computed at once (i.e., static) or incrementally (i.e., dynamic).

Eight English words are selected from a chunk of Web crawl data. The words are selected fairly randomly, although we make sure they cover a whole range of data sparsity, from function words (e.g., “A”), to common words (e.g., “FRIDAY”) to rare words (e.g., “TWIST”). Thus, as summarized in Table 1, our data set consists of 8 vectors and the entries are the numbers of word occurrences in each document.

Table 1: The data set consists of 8 English words selected from a corpus of Web pages, forming 8 vectors whose values are the word occurrences. The table lists their fractions of non-zeros (sparsity) and the Shannon entropies ().

Word

Sparsity

Entropy

TWIST

0.004

5.4873

FRIDAY

0.034

7.0487

FUN

0.047

7.6519

BUSINESS

0.126

8.3995

NAME

0.144

8.5162

HAVE

0.267

8.9782

THIS

0.423

9.3893

A

0.596

9.5463

G.2 Estimating Frequency Moments

We estimate the th frequency moments , for , 0.1, …, , using the proposed new estimator and the geometric mean estimator , as well as the geometric mean estimator for symmetric stable random projections proposed in [26]. Recall

We find is numerically very stable, if we express it as

where , the first moment, can be computed exactly. Using Matlab (the 32-bit version), we find no numerical problems with even for very small (e.g., ; see Figure 3).

However, we could not find a numerically very stable implementation of the geometric mean estimator , when . We tried a variety of ways (including the tricks in implementing ) to implement and the Gamma functions (e.g., using “gammaln” instead of “gamma” in Matlab). Fortunately, we believe is sufficiently small for comparing the two estimators.

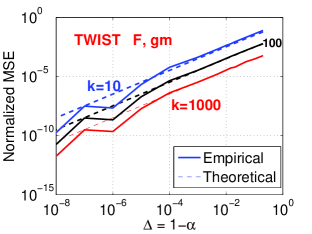

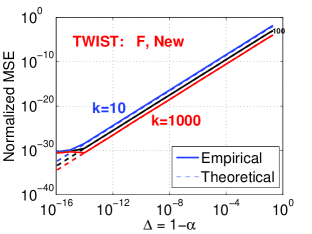

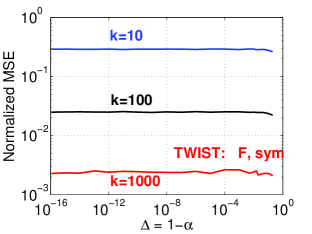

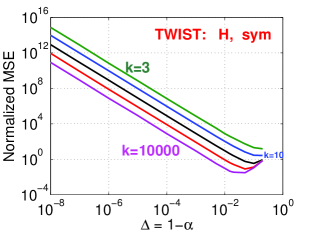

Figure 3: Normalized MSEs for estimating the th frequency moments using the geometric mean estimator (left panel) and the proposed new estimator (middle panel) for CC, together with the geometric mean estimator (right panel) for symmetric stable random projections. For and , we also plot their theoretical variances (dashed curves), which largely overlap the empirical MSEs whenever the algorithms are numerically stable. The proposed new estimator is numerically very stable even when . In comparison, is not stable if . We present results at the sample sizes , 100, and 1000.

We experiment with three values: 10, 100, and 1000; and we present the estimation errors in terms of the normalized mean square errors (MSE, normalized by the square of the true values). As decreases, the MSEs for the symmetric stable random projections (in the right panel of Figure 3) are roughly flat, verifying that algorithms based on symmetric stable random projections do not capture the fact that the first moment () should be a trivial problem.

Using Compressed Counting (CC), the geometric mean estimator, (in the left panel of Figure 3), and proposed new estimator, (in the middle panel), clearly exhibit the desired property that the MSEs decrease as decreases. Of course, as expected, , has a much faster rate of decreasing than ; the latter is also numerically much less stable when .

G.3 Estimating Shannon Entropies

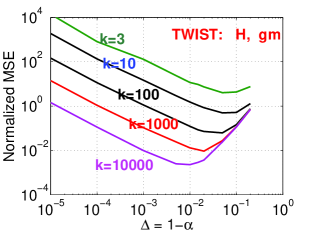

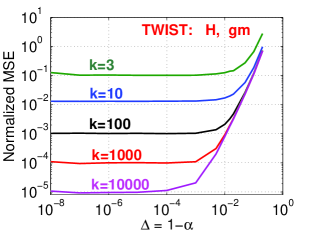

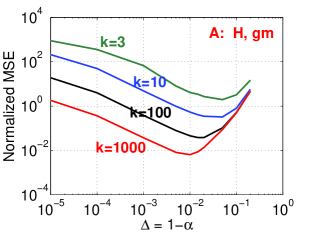

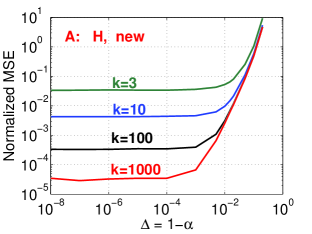

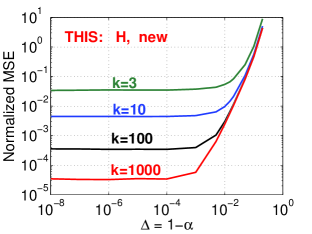

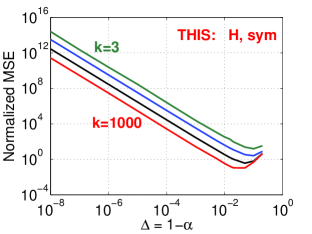

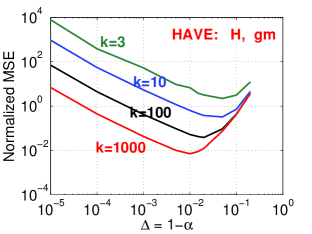

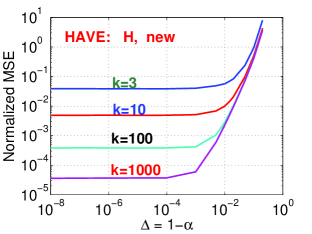

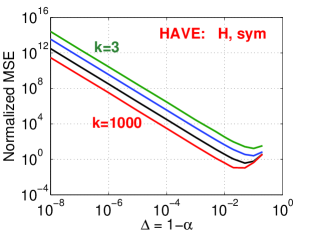

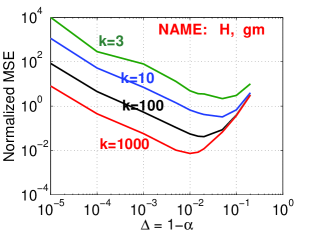

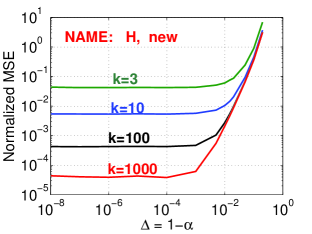

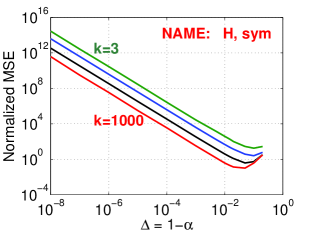

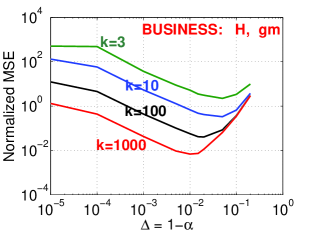

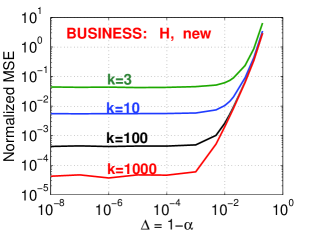

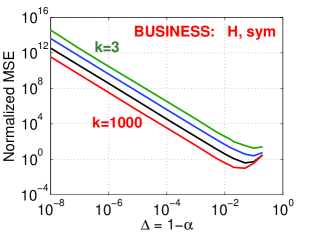

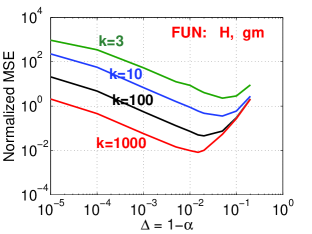

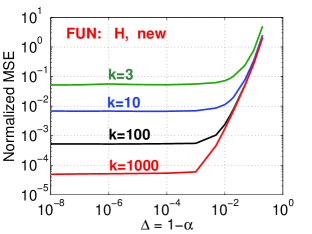

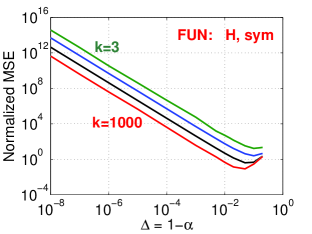

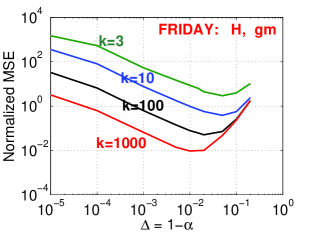

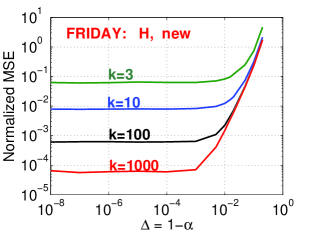

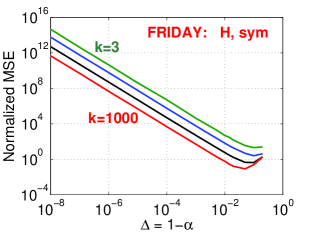

After we have estimated the frequency moments, we use them to estimate the Shannon entropies using Tsallis entropies. For the data vector “TWIST”, we present results at sample sizes , and 10000. For all other vectors, we do not experiment with . Figure 4 and Figure 5 present the normalized MSEs.

Using CC and the proposed estimator (middle panels), only samples already produces fairly accurate estimates. In fact, for some vectors (such as “A”), even may provide reasonable estimates. We believe the performance of the new estimator is remarkable. Another nice property is that the estimation errors (MSEs) become stable after (e.g.,) (or ).

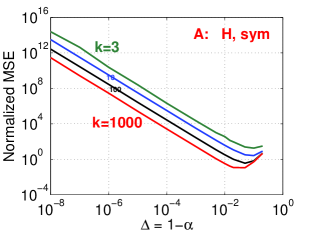

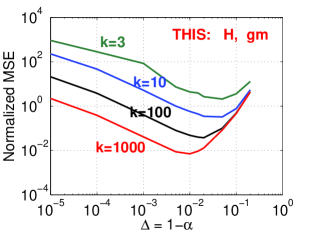

In comparisons, the performance of the geometric mean estimator (left panels) for CC is not satisfactory. This is because its variance only decreases only at the rate of , not .

Also clearly, using symmetric stable random projections (right panels) would not provide good estimates of the Shannon entropy (unless the sample size is extremely large () and one could carefully choose a good to exploit the bias-variance trade-off).

Figure 4: Normalized MSEs for estimating Shannon entropies using (left panels) and (middle panels) for CC, and the geometric mean estimator for symmetric stable random projections (right panels).

Figure 5: Normalized MSEs for estimating Shannon entropies using (left panels) and (middle panels) for CC, and the geometric mean estimator for symmetric stable random projections (right panels).

References

[1]

Charu C. Aggarwal, Jiawei Han, Jianyong Wang, and Philip S. Yu.

On demand classification of data streams.

In KDD, pages 503–508, Seattle, WA, 2004.

[2]

Noga Alon, Yossi Matias, and Mario Szegedy.

The space complexity of approximating the frequency moments.

In STOC, pages 20–29, Philadelphia, PA, 1996.

[3]

Khanh Do Ba Amit Chakrabarti and S. Muthukrishnan.

Estimating entropy and entropy norm on data streams.

Internet Mathematics, 3(1):63–78, 2006.

[4]

Brian Babcock, Shivnath Babu, Mayur Datar, Rajeev Motwani, and Jennifer Widom.

Models and issues in data stream systems.

In PODS, pages 1–16, Madison, WI, 2002.

[5]

Ziv Bar-Yossef, T. S. Jayram, Ravi Kumar, and D. Sivakumar.

An information statistics approach to data stream and communication

complexity.

In FOCS, pages 209–218, Vancouver, BC, Canada, 2002.

[6]

Lakshminath Bhuvanagiri and Sumit Ganguly.

Estimating entropy over data streams.

In ESA, pages 148–159, 2006.

[7]

Daniela Brauckhoff, Bernhard Tellenbach, Arno Wagner, Martin May, and Anukool

Lakhina.

Impact of packet sampling on anomaly detection metrics.

In IMC, pages 159–164, 2006.

[8]

Amit Chakrabarti, Graham Cormode, and Andrew McGregor.

A near-optimal algorithm for computing the entropy of a stream.

In SODA, pages 328–335, 2007.

[9]

John M. Chambers, C. L. Mallows, and B. W. Stuck.

A method for simulating stable random variables.

Journal of the American Statistical Association,

71(354):340–344, 1976.

[10]

Carlotta Domeniconi and Dimitrios Gunopulos.

Incremental support vector machine construction.

In ICDM, pages 589–592, San Jose, CA, 2001.

[11]

Joan Feigenbaum, Sampath Kannan, Martin Strauss, and Mahesh Viswanathan.

An approximate -difference algorithm for massive data streams.

In FOCS, pages 501–511, New York, 1999.

[12]

Laura Feinstein, Dan Schnackenberg, Ravindra Balupari, and Darrell Kindred.

Statistical approaches to DDoS attack detection and response.

In DARPA Information Survivability Conference and Exposition,

pages 303–314, 2003.

[13]

Philippe Flajolet.

Approximate counting: A detailed analysis.

BIT, 25(1):113–134, 1985.

[14]

Sumit Ganguly and Graham Cormode.

On estimating frequency moments of data streams.

In APPROX-RANDOM, pages 479–493, Princeton, NJ, 2007.

[15]

Izrail S. Gradshteyn and Iosif M. Ryzhik.

Table of Integrals, Series, and Products.

Academic Press, New York, fifth edition, 1994.

[16]

Sudipto Guha, Andrew McGregor, and Suresh Venkatasubramanian.

Streaming and sublinear approximation of entropy and information

distances.

In SODA, pages 733 – 742, Miami, FL, 2006.

[17]

Nicholas J. A. Harvey, Jelani Nelson, and Krzysztof Onak.

Sketching and streaming entropy via approximation theory.

In FOCS, 2008.

[18]

Nicholas J. A. Harvey, Jelani Nelson, and Krzysztof Onak.

Streaming algorithms for estimating entropy.

In ITW, 2008.

[19]

M E. Havrda and F. Charvát.

Quantification methods of classification processes: Concept of

structural -entropy.

Kybernetika, 3:30–35, 1967.

[20]

Monika R. Henzinger, Prabhakar Raghavan, and Sridhar Rajagopalan.

Computing on Data Streams.

American Mathematical Society, Boston, MA, USA, 1999.

[21]

Piotr Indyk.

Stable distributions, pseudorandom generators, embeddings, and data

stream computation.

Journal of ACM, 53(3):307–323, 2006.

[22]

Piotr Indyk and David P. Woodruff.

Optimal approximations of the frequency moments of data streams.

In STOC, pages 202–208, Baltimore, MD, 2005.

[23]

N. Karmarkar, R. Karp, R. Lipton, L. Lovasz, and M. Luby.

A monte-carlo algorithm for estimating the permanent.

SIAM J. Comput., 22(2):284–293, 1993.

[24]

Anukool Lakhina, Mark Crovella, and Christophe Diot.

Mining anomalies using traffic feature distributions.

In SIGCOMM, pages 217–228, Philadelphia, PA, 2005.

[25]

Ashwin Lall, Vyas Sekar, Mitsunori Ogihara, Jun Xu, and Hui Zhang.

Data streaming algorithms for estimating entropy of network traffic.

In SIGMETRICS, pages 145–156, 2006.

[26]

Ping Li.

Estimators and tail bounds for dimension reduction in

() using stable random projections.

In SODA, pages 10 – 19, San Francisco, CA, 2008.

[27]

Ping Li.

Compressed counting.

In SODA, New York, NY, 2009.

[28]

Ping Li.

Improving compressed counting.

In UAI, Montreal, CA, 2009.

[29]

Ping Li.

On the sample complexity of compressed counting.

Technical report, Department of Statistical Science, Cornell

University (http://arxiv.org/PS_cache/arxiv/pdf/0910/0910.1403v1.pdf),

2009.

[30]

Qiaozhu Mei and Kenneth Church.

Entropy of search logs: How hard is search? with personalization?

with backoff?

In WSDM, pages 45 – 54, Palo Alto, CA, 2008.

[31]

Robert Morris.

Counting large numbers of events in small registers.

Commun. ACM, 21(10):840–842, 1978.

[32]

S. Muthukrishnan.

Data streams: Algorithms and applications.

Foundations and Trends in Theoretical Computer Science,

1:117–236, 2 2005.

[33]

Liam Paninski.

Estimation of entropy and mutual information.

Neural Comput., 15(6):1191–1253, 2003.

[34]

Alfred Rényi.

On measures of information and entropy.

In The 4th Berkeley Symposium on Mathematics, Statistics and

Probability 1960, pages 547–561, 1961.

[35]

Michael E. Saks and Xiaodong Sun.

Space lower bounds for distance approximation in the data stream

model.

In STOC, pages 360–369, Montreal, Quebec, Canada, 2002.

[36]

Constantino Tsallis.

Possible generalization of boltzmann-gibbs statistics.

Journal of Statistical Physics, 52:479–487, 1988.

[37]

David P. Woodruff.

Optimal space lower bounds for all frequency moments.

In SODA, pages 167–175, New Orleans, LA, 2004.

[38]

Kuai Xu, Zhi-Li Zhang, and Supratik Bhattacharyya.

Profiling internet backbone traffic: behavior models and

applications.

In SIGCOMM ’05: Proceedings of the 2005 conference on

Applications, technologies, architectures, and protocols for computer

communications, pages 169–180, 2005.

[39]

Qiang Yang and Xingdong Wu.

10 challeng problems in data mining research.

International Journal of Information Technology and Decision

Making, 5(4):597–604, 2006.

[40]

Haiquan Zhao, Ashwin Lall, Mitsunori Ogihara, Oliver Spatscheck, Jia Wang, and

Jun Xu.

A data streaming algorithm for estimating entropies of od flows.

In IMC, San Diego, CA, 2007.

[41]

Vladimir M. Zolotarev.

One-dimensional Stable Distributions.

American Mathematical Society, Providence, RI, 1986.