Langevin process reflected at a partially elastic boundary I

Abstract

Consider a Langevin process, that is an integrated Brownian motion, constrained to stay in by a partially elastic boundary at 0. If the elasticity coefficient of the boundary is greater than or equal to , bounces will not accumulate in a finite time when the process starts from the origin with strictly positive velocity. We will show that there exists then a unique entrance law from the boundary with zero velocity, despite the immediate accumulation of bounces. This result of uniqueness is in sharp contrast with the literature on deterministic second order reflection. Our approach uses certain properties of real-valued random walks and a notion of spatial stationarity which may be of independent interest.

keywords:

[class=AMS]keywords:

1 Introduction

In 1905, Einstein has been the first one to develop the theory of Brownian motion, providing an explanation of the erratic trajectories of particles observed by Brown eighty years earlier. He considered time scales no smaller than a “relaxation time”, so that he could suppose the independence of the displacements of the particles, and proposed a statistical physics approach, working on the probability density of the particle, rather than its paths. He obtained that this density should satisfy the heat equation, leading to the now usual Brownian motion model.

Three years later, Langevin proposed his own approach. The particles should simply satisfy the usual equation of motion, stating that their acceleration, multiplied by their mass, should be equal to the external forces applied to them. The randomness is only hidden in these forces, which can be decomposed into a deterministic friction term and a stochastic term, which we would now call white noise. This leads to the Langevin equation, which is historically the first example of a stochastic equation. Its solution yields essentially the same behavior as Brownian motion on large time scales. But on smaller time scales (smaller than the relaxation time), a Langevin process is fundamentally different from a Brownian motion, since its paths are , and is a more accurate model for real particles.

Today, a well-known and well studied object is the reflected Brownian motion, used to describe the trajectories of particles constrained to stay in a domain, and in many other applications. However, there has been only few studies of the reflected Langevin processes yet, and this paper proposes such a study. For the sake of simplicity, we consider only the simplest Langevin process. The space is one dimensional, the only external force is a white noise,111that is, we consider no friction force. The relaxation time is then infinite. and the particle has mass one. Then, if is the initial position of the particle and its initial velocity, its path is simply given by

where is the standard Brownian motion driving the motion. We call this process (free) Langevin process, or integrated Brownian motion. A consequent study can be found in Lachal [14].

Further, suppose this particle is constrained to stay in by a barrier at 0, in such a way that when the particle hits the barrier with incoming velocity , it will instantly bounce back with velocity , where is a parameter called elasticity coefficient or velocity restitution coefficient. When we say the reflection is perfectly elastic, when it is said totally inelastic. The modeling of this barrier naturally involves second order reflection, which can be expressed, for the Langevin process, by the following second order stochastic differential equation:

| where | is the standard Brownian motion driving the motion, standard | |||

| meaning that it starts from and has variance at time . | ||||

| is the initial or starting condition. |

The model and these equations will be further discussed in the preliminaries. The second order reflection for a particle submitted to a deterministic force already reveals a formidable complexity. See the paper of Ballard [1] for relatively recent results, and also those of Bressan in 1960 [6], Percivale in 1985 [16], Schatzman in 1998 [17] for further reference. In particular, an analytic force implies the existence of a unique solution, but this may fail even with a force. The main aim of this work is to show that our stochastic model is nicer, in the sense that there is always a unique solution to (RLP), in the weak sense. The particular case of an inelastic reflection has already been treated in Bertoin [3] (see also [2] and [12]) – though in slightly less general settings, as the possibility of a nonzero term was not considered.

Our first observation is that when the starting position is , then Equations (RLP) have a unique maximal solution killed when hitting . We shall see in Preliminaries that this hitting time is infinite if and only if the coefficient is no less than the critical value . In the sequel we restrict the study to that case and investigate what happens when the starting condition is . It may seem an easy question but once again an analogy with the deterministic equations enlightens the difficulty of the problem.

We will prove the existence of a unique law of a solution to (RLP), that is, of a unique reflected Langevin process started from . Its law is obtained as the weak limit of the law of the reflected Langevin process starting from 0 with a nonzero velocity , when goes to 0. We also express directly the law of the reflected Langevin process started from , and translated at some random time.

These results may seem similar to those obtained in the inelastic case in [3]. However, the behavior of the reflected process is very different when the elasticity coefficient is nonzero, and so is the whole study. In a forthcoming paper, we will also investigate the subcritical case . In that case too, we will prove the existence of a unique reflected Langevin process, but once again, the qualitative behavior of the reflected process being fairly different, we will have to use other specific techniques.

The guiding line in this article is to focus on the velocities of the process at the bouncing times, and we start with the crucial observation that the sequence of their logarithms forms a random walk. We first prove a convergence result for this random walk (Corollary 2). Then we translate it to a convergence result for the reflected process itself (Lemma 3), through which we can prove our main results (Theorem 1 and 2).

The preliminaries start with an informal discussion about the model, and an insight into the qualitative behavior of the reflected process. Then starts the rigorous mathematical study, where we show in particular the phase transition at the critical value . We end the preliminary section with defining a notion of spatial stationarity, in an abstract context, and giving an abstract convergence result using this notion (Lemma 2), which will be proved in the Appendix. Section 3 starts with the statement of our two theorems, both relying on Lemma 3. Section 3.1 uses renewal theory and Lemma 2 to construct a spatially stationary process and reduce the proof of Lemma 3 to that of Lemma 5. Section 3.2 handles this proof in the supercritical case, thanks to an explicit construction222These two constructions in particular may be of independent interest. of the spatially stationary random walk. However this construction does not hold in the critical case, and Section 3.3 completes then the proof, thanks to a disintegration formula22footnotemark: 2 for the spatially stationary random walk.

2 Preliminaries

2.1 Informal discussion on the model

First order reflected Brownian motion

We start with a few words about the first order reflected Brownian motion, that is the common reflected Brownian motion. In this model the path is driven by a standard Brownian motion . The reflected path started from is requested to be a process evolving in solution of the following equation:

where models the push of the barrier. The process starts from 0 and is requested to be nondecreasing, continuous, and increasing only when the particle is at the barrier, in the sense . Its solution is simply given pathwise by a so-called Skorohod reflection:

We stress that the non-reflected process has continuous but non-derivable paths, and that, at a given time, the law of the future of this process just depends on its current position. For these reasons, first order reflection is the most natural way to model a barrier.

Second order reflected Langevin process

On the contrary, a Langevin process has a well-defined velocity, and its behavior in the future depends both of its position and its velocity at present. Therefore first order reflection does not make much sense. Second order reflection, as described in the introduction, is the most natural model to consider, leading to (RLP). In this model, the push of the barrier has a direct effect only on the velocity of the particle. This push necessarily involves a discontinuous part, each jump modeling a bounce, which is happening when the particle is at 0 with nonzero incoming velocity. This yields the sum in the equation, indexed by the bouncing times. The only restrictive assumption we make about this term is that the velocity restitution coefficient be a constant parameter.

But the barrier push may also include, in full generality, a continuous component. We should take into account a continuous process (possibly degenerate), that increases only when the particle is at . In the cases when and the external force is non-positive, the only second order reflected process starting from initial condition is the process staying at 0. We then have . This example should be enough to illustrate the importance of the term (which was not considered in [3, 12]).

The existing works on second order reflection reveal that it is a much more complex equation than first order reflection. In the general case there is no uniqueness result and no simple expression of any solution. Consequently, a pathwise approach has a priori no chance to succeed.

Second order reflection and transience hypothesis

At any instant such that , there is locally no bounce (or only one bounce), and there is local pathwise existence and uniqueness of a solution to (RLP). Therefore, for a starting condition , Equations (RLP) yield a unique strong maximal solution stopped when hitting . The whole difficulty of second order reflection is concentrated near the point , where the process is not necessarily constant, and where an infinite number of bounces occur on a finite time interval.

Now, suppose that the following “transience hypothesis” holds: whenever the process is not at , the maximal solution is defined for all positive times (without hitting ). Then the only obstruction to the existence of a unique solution is the starting condition . Observe, now, that in our model, a solution to (RLP) cannot stay locally at 0, as a Brownian motion is almost surely not monotone on any interval. Therefore a solution has to take off instantly, and will never be again in 0 with zero velocity. Obviously, in that case must be equal to 0.

Now, if is a solution to (RLP) starting from and is small, then the process is a solution to (RLP) starting from the random position , which is near to . This may suggest to study the convergence of the law of the solution starting from , when goes to . And indeed, we will prove that these laws have a unique limit, which is the law of a solution starting from . But while a major part of this discussion was relevant for any second order reflection, we stress that this particular result of convergence to the solution starting from is specific to our stochastic model. Some deterministic forces may lead to unexpected behaviors, which we illustrate with two counterexamples.

Consider the easiest counterexample to uniqueness, when the force is a negative constant , and the elasticity coefficient is larger than one. We can write explicitly all the solutions starting from . They are given by the trajectory constantly staying on the barrier, and by the trajectories , for , , defined by

It is easily seen that the solutions can all be approached by the solution starting from an initial condition close to, but different from, , while this is not the case for the other solutions, which stay in a certain amount of time. Therefore not only the solution starting from does not converge to a unique limit trajectory when goes to , but also the limit trajectories do not yield all the solutions starting from . However, we should say that this counterexample is called “pathological” by physicists, since the elasticity coefficient is larger than one.

A physically more realistic counterexample is given by Ballard in [1], Section 5.3, for . A close look to it reveals that there are actually not only two solutions starting from , as indicated by the author, but an infinite number of them, each one leaving instantly. In addition, any of these solutions can be approached by the solution starting from an initial condition close to .

The perfectly elastic reflected Langevin process

Finally, let us observe that the special case is straightforward for our model: whatever the initial condition, the reflected Langevin process has the same law as the absolute value of a non-reflected Langevin process. In addition we can use previous works to understand better the reflected process.

Suppose the starting position be 0 and starting velocity be nonzero. Introduce and for the sequence of the successive bouncing times, and for the sequence of the velocities of the process at these bouncing times. The results of McKean [15] show that the sequence is a homogeneous Markov chain with explicit transition probabilities. Lachal furthers this study in [13] by giving explicit formulas for the law of for a fixed .

Now, suppose on the contrary that the initial condition is . Then the reflected process has an infinite number of bounces just after the initial time. The works of McKean and Lachal still describe the bouncing times and velocities at these instants, now thanks to two sequences. The first one corresponding to the successive bounds happening after time 1, the second one to the successive bounds happening before time 1, counted backwardly.

In a fairly similar manner, in the general case , we are led to consider a single sequence but indexed by . To do this, the first bounce for which the velocity is greater than 1 will be chosen as the reference, in the sense that this bounce will have index 0.

Remark 1.

Wong also studies in [19, 20] the passage times to zero for a certain stationary process, which is obtained from the Langevin process by an exponential change of scale in both time and space. The passage times to zero of this stationary process are closely related to a certain stationary random walk that we will introduce later on. However, this process shall not be confused with the “stationary Langevin process” introduced in [12]. The two processes do not seem to be directly related.

2.2 The model, preliminary study

Notations

We use the notation for the set of nonnegative real numbers , and for the set of positive real numbers . Introduce and . Our working space is , the space of càdlàg trajectories , which satisfy

This space is endowed with the algebra generated by the coordinate maps and with the topology induced by the following injection:

where is the space of càdlàg trajectories on , equipped with Skorohod topology. We denote by the canonical process and by its natural filtration, satisfying the usual conditions of right continuity and completeness. Besides, by a slight abuse of notation, when we define a probability measure , we also write for the expectation under this probability measure. When is a measurable functional and an event, we also write for the quantity .

For any , the second order reflection of the Langevin process with starting position and starting velocity leads to Equations (RLP), which we recall here:

where is the standard Brownian motion driving the motion and is requested to be a continuous nondecreasing process starting from and increasing only when . A solution is the quadruplet . For any , there is a unique solution to Equations killed at the first hitting time of for the process . We write for the law of , which is a strong Markov process, and whose first coordinate will be called the killed reflected Langevin process. We will almost exclusively consider the case when the starting position is , and write for (with ).

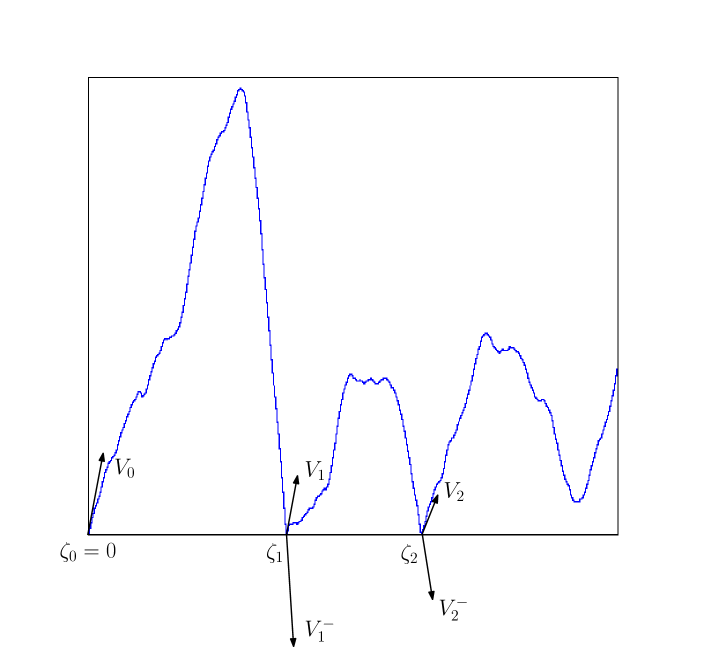

Write and for the sequence of successive hitting times of zero, and call an arch a part of the path included between two consecutive hitting times of zero. Figure 1 below shows two complete arches and the beginning of a third one. Write also , and for the speed of the process just before this -th bounce, and for the speed of the process just after this -th bounce, respectively, so that we have .

Please note that the event that for some , we have , has probability 0. We call time of accumulation of bounces the time . It coincides almost surely with the hitting time of . Next, we will study the sequence and see whether time is infinite, as in the perfectly elastic case.

A phase transition

Lemma 1.

-

1.

The law of under is given by

(2.1) -

2.

Under , the sequence is i.i.d. The common law of its marginals, also independent of , is that of under .

-

3.

In particular, the sequence is a random walk. The density of its step distribution under does not depend on and is given by:

(2.2) In particular has finite variance and expectation

-

4.

We have, when ,

(2.3) where

Proof.

The three first points are essentially results given by McKean [15] or direct consequences of these. The last point is similar to a result of Goldman for the law of the process with zero starting velocity and nonzero starting position [8], and follows from (2.1) by standard integral calculus.

For the convenience of the reader, we explain the second point. It follows from the observation that the variable (resp. ) is equal to the duration of the th arch renormalized to start with speed one (resp. to the absolute value of the speed of the process just before its return time to zero, for this renormalized arch). More precisely:

Recall that, conditionally on , the process is independent of and has the same law as under , thus is independent of has the same law as under . It follows that the variable is independent of and has the same law as under (conditionally on , but this conditioning can simply be removed). The statement follows. ∎

From this Lemma we deduce the phase transition phenomena:

Corollary 1.

The time of accumulation of bounces is:

finite almost surely if ,

infinite almost surely if .

We thus call the critical elasticity coefficient. We call the case the supercritical regime, the case the subcritical regime, the case the critical regime.

Proof.

We may express as the series:

For , the law of large numbers tells that the sequence converges to a.s. On the other hand, it follows from (2.3) that the expectation of is finite333This result was also stressed by McKean in [15]. Thus, for any fixed there are a.s. only a finite number of such that is larger than . We deduce an a. s. exponential decay for the variables . A fortiori is a. s. finite.

Take now . For , the random walk has a positive drift and is transient. Thus the sequence is diverging to . As is independent of and has a fixed distribution, we deduce that is infinite. For , the step distribution has zero expectation and finite variance, thus the random walk is recurrent (from the central limit theorem). Then the sequence is recurrent, but it is still not converging to zero, which is enough to conclude in the same way that is infinite. ∎

From now, we will restrict the study to the supercritical and critical regimes, or , when the transience hypothesis holds.

2.3 Spatial stationarity

After these first results on the Langevin process, we give the abstract context for a notion of spatial stationarity and an important lemma that we will need later.

Write for the set of sequences indexed by with values in , where is a topological space with an isolated point . For now, just consider this space as playing an accessory role that will be clarified later. The set is endowed with the usual product topology. An element of will be written alternatively , or .

For any real number we write for the hitting time of by the first coordinate, that is

Under all the measures that we will consider on we will have

and as a consequence will have values in -almost surely. Write for the subset of consisting in sequences for which . Define a spatial translation operator on , by:

| (2.4) |

Observe that the range of is always , and that the restriction of to is the identity. This definition immediately yields a notion of spatial stationarity for probability laws on :

Definition 1.

We say that a probability on is spatially stationary if for any .

We also write

An element of shall be thought of as a sequence indexed by . We write for the projection of defined by:

If is a probability law on , we write for the image probability law on by this projection. Finally the notation simply denotes the weak convergence for probability laws on the topological space . The following lemma formulates how convergence results on can imply a convergence result to a spatially stationary probability measure on .

Lemma 2.

Let be a family of probability laws on . We suppose that there is a probability law on such that:

| (2.5) |

Then there exists a unique spatially stationary probability law on such that . Moreover, we have

The proof of this technical lemma is based on the Kolmogorov existence theorem. We postpone it to the appendix.

3 Entering with zero velocity

Recall that we are in the critical or supercritical regime, . Write for the sequence of the logarithms of the (outgoing) velocity at the successive bounces, defined by . From Lemma 1, under , it is a random walk with step distribution given by (2.2) and drift

In the supercritical case the drift is strictly positive, while in the critical case the step distribution has zero drift and finite variance.

We introduce the (strictly) ascending ladder height process associated to the random walk , that is the random walk with positive jumps defined by and , where and . In both cases (positive drift, or null drift and finite variance), it is known (see Theorem 3.4 in Spitzer [18]) that the expectation of the step distribution of , that is belongs to The probability law

| (3.1) |

is known in renewal theory as the stationary law of the overshoot (see also Part 3.1).

We now state our main theorems. The first one is a convergence result for the probability laws when , while the second one states the weak existence and uniqueness of solutions to Equations (RLP) with initial condition .

Theorem 1.

The family of probability measures on has a weak limit when , which we denote by . More precisely, write for the instant of the first bounce with speed greater than , that is Then the law satisfies the following conditions:

Theorem 2.

Consider a process of law . Then the jumps of on any finite interval are summable and the process defined by

is a Brownian motion. As a consequence the quadruplet is a solution to with initial condition .

For any solution to with initial condition , the law of is , and almost surely.

Let us introduce a slightly larger working space,

We mention that can be seen as a subspace of , by removing time 0 from the trajectories. This inclusion is strict: an element of is a trajectory (indexed by ) which does not necessarily have a limit at . Both theorems will actually follow from the following lemma, which can be seen as a weak version of Theorem 1, and whose proof is reported to later.

Lemma 3.

There exists a law on such that:

We have for any , -almost surely.

conditions and are satisfied

For any , the joint law of and under converges weakly, when goes to 0, to that under .

Proof of Theorem 1 and Corollary 2.

Consider, under , the canonical process . From conditions and the Markov property, we deduce that is a strong Markov process with values in and transitions that of the reflected Langevin process.

It follows that for any , there exists a Brownian motion independent of and such that, for ,

The Brownian motions are linked by for . We introduce . For any , we have

Therefore is a Brownian motion. It follows that is a Brownian motion. Write for its limit when tends to 1. Now, define the process by

It is easy to check that is a Brownian motion and satisfies for . Hence, for ,

| (3.2) |

The increments of are equal to the sum of two terms, on the one side the increments of , and on the other side, the jumps, which are happening at the bouncing times. Besides, conditions imply . That is, the value of at a bouncing time is going to 0 when this time goes to 0. It follows . Therefore we also have . Consequently, by setting , we define a process in . We call its law . Now, take again System (3.2) and let go to 0. First, we obtain that the sum of the jumps happening just after the initial time (or in a finite time interval) is finite. Then we deduce that under , is a solution to with starting condition .

In summary, we defined a law on satisfying conditions and , and thus and almost surely. Besides, the joint law of and under converges weakly to that under . In order to deduce the convergence of to , we just need to control what happens on . More precisely, it is enough to control the velocity . Let us call the supremum of on . It will be enough to prove that when is small, the variable is small with high probability, uniformly on small, in the following sense:

Start from the basic observation , where is the underlying Brownian motion. It follows

for a well-chosen , independent of . Now, by writing the right side in the form , and using , a.s., we get that the following inequality

is satisfied for small enough. Choose , smaller than , such that the inequality is satisfied. Then, from the convergence of the law of under to that under , we get that for smaller than some , we have

Now it is clear that the inequality stays satisfied for , which ends the proof. The law converges weakly to , and Theorem 1 is proved.

Finally, we should prove the uniqueness in Theorem 2. Consider any solution to with starting condition . As discussed in the preliminaries, almost surely, and we have for any positive . If the first coordinate were not coming back to zero at small times, then there wouldn’t be any jumps for at small times, thus would behave like a Langevin process. But this is not possible as the Langevin process starting from zero with zero velocity does come back at zero at arbitrary small times. As a consequence, the process necessarily satisfies condition . Now, the process converges in law to , thus the law of is an accumulation point of the family when . It must coincide with . ∎

The rest of the section is devoted to the proof of Lemma 3. It can be sketched as follows. First, using renewal theory, we get, for any fixed , the convergence of the law of the process to a law that can be described in a simple way. Then Lemma 2 allows, in a certain sense, to include negative times in this convergence result. The last step will be to prove that converges in law to a finite valued random variable.

3.1 Convergence of shifted processes

We recall the notation for the (outgoing) velocity at the -th bounce and for its logarithm, for . We also write for the translated velocity path starting at the -th bounce and renormalized so as to start with speed one. That is, is defined by

| (3.3) |

The process is independent of and has law . The knowledge of the process , or , is equivalent to the knowledge of the sequence , or even just . But it is more convenient to first prove convergence results about (translations of) the sequence , then deduce results about , which we do.

We work with and we define moreover, for , so that the sequence lays in , in the settings of Section 2.3. We call its law on (or ), under . We also use the other notations of Section 2.3, such as , which we will simply write , or the spatial translation operator , defined by (2.4). We now aim at establishing convergence results for the probabilities .

First, observe that under and for , is measurable with respect to , and thus is entirely determined by , which follows the law . In other words, there is a deterministic functional such that and is the law on induced by the law for . Write now for the law on induced by the law for , where the measure is the stationary law of the overshoot we introduced earlier, defined by (3.1).

Lemma 4.

For any real number , we have

Proof.

Consider the ascending ladder height process defined at the beginning of Section 3. It is a random walk with positive jumps and finite expectation. It is nonarithmetic in the sense that its jumping law is not included in for any (nonarithmeticity is trivial for laws with densities). Renewal theory for random walks with positive jumps (see for example [10], p.62, or [7], p.355) gives the following result: the law of the overshoot over a level , that is , converges to when goes to infinity. This result is transmitted directly to the random walk , simply because it has the same overshoot: . Under , we have . Hence, when goes to , the law of the variable under , or, equivalently, that of under , converges to .

Now, the usual Markov and scaling invariance properties show that for any , , under , is independent of and has the same law as under . This altogether establishes the convergence of to . ∎

Applying Lemma 2, we immediately deduce:

Corollary 2.

For any real number , we have

| (3.4) |

where is the unique spatially stationary probability measure on such that

Remark 2.

Call , resp. , the projection of , resp. , on the first coordinate. Call the spatial translation operator induced on the first coordinate (defined by ). Then is the law of the random walk with starting position distributed according to . Moreover, we have , and is spatially stationary. Similar arguments show that is the unique spatially stationary measure such that . We call it the law of the spatially stationary random walk.

We now want to deduce Lemma 3 from Corollary 2. To this end, we have to understand how to reconstruct from . We start by working under , for some . We introduce an important variable, , the instant of the first bounce with speed greater than for the process .

Observe that the definition (3.3) of induces that the length of the first arch of , that is , is equal to times the length of the -th arch of . We may also express as a functional of by setting

| (3.5) |

where is defined by

| (3.6) |

with the convention . Now, the process is given as the following functional of :

Now, let us work under . It is natural to keep the definition of given by Formula (3.5). Please note however that the sum defining now contains an infinite number of nonzero terms.

Lemma 5.

1) -almost surely, the time is finite for any , and goes to 0 when goes to ,

2) The law of under converges to that under when .

The proof of Lemma 5 is postponed to the next subsections. Taking Lemma 5 for granted, we may proceed to the proof of Lemma 3.

Proof of Lemma 3.

The first part of Lemma 5 enables us to define a process on by

This construction is coherent. We call its law on .

Under , the instant is the instant of the first bounce with speed greater than . It is positive and converges a.s. to 0 when goes to 0. Besides, the law of is equal to , because by spatial stationarity, . Now, take and in the formula above. It follows that under , the law of is , and that conditionally on , the process has law . We leave to the reader the verification that it is also independent of . Hence the law satisfies conditions and .

The second part of the lemma proves that for any fixed , the joint law of and under converges to that under , as laws on . ∎

Finally, all we have to do is to prove Lemma 5. By scaling, it suffices to show that is finite a.s. to prove the first part. We also can suppose for the second part. Finally, note that under , we have almost surely and hence .

This proof will be based on a more explicit description of the spatially stationary measures and . We must distinguish between the critical and supercritical cases.

3.2 Proof of Lemma 5 in the supercritical case

Throughout this section we suppose that . Therefore the drift is strictly positive. We propose a construction of based on the introduction of a temporally stationary measure on . If one just considers the first coordinate, this is a construction of the law of the spatially stationary random walk , using the temporally stationary random walk.

First, let us define this temporally stationary random walk. Introduce , law of the random walk indexed by , where and is i.i.d with common law that of the generic step. Then write for the law of under , and set

This -finite measure is (temporally) stationary, in the sense that for any , the sequences and have the same law under . This term “law" has to be understood in a generalized sense, that is in settings where we allow the laws to be not only probability measures but more generally -finite measures. We call this generalized process of law the (temporally) stationary random walk.

Now start again the same construction, but with adding the second coordinate. We first recall that under and for , is measurable with respect to ; we have , where is a deterministic functional. For , consider for the law of , where , (recall that denotes the velocity of the particle after the th bounce), and the sequence is given by .

It should be clear that the laws , , are compatible. Kolmogorov’s existence theorem entails the existence of , the law on under which has law for any . Then we just define by

Again, this is a -finite (temporally) stationary measure. Besides, the law of the first coordinate under is .

Now, consider the event , for and . It should be clear that its measure under is independent of and . The following lemma gives its value and states a link between and , as well as between and (recall Remark 2 after Corollary 2 for the introduction of the law of the spatially stationary random walk, ).

Lemma 6.

Suppose .

1) We have

2) We have and .

Proof.

Recall that is strictly positive and finite. We still write for the (strictly) ascending ladder height process of the sequence . Its drift is also strictly positive and finite. A result of Woodroofe [21] and Gut [9] states that, for any , we have

| (3.7) |

The calculation below follows:

where we used a symmetry property in the third line. As we can condition the infinite measure on the event to get the probability measure

We leave to the reader the simple verification that this measure on is spatially stationary in the sense of Definition 1 and is projected on the measure on . Thus it must coincide with , by Corollary 2. ∎

We may now prove the first part of Lemma 5.

Proof of Lemma 5.1).

Recall that we need to prove the -a.s. finiteness of the sum .

We start by proving that it is finite -almost surely, for a fixed . Under , the sequence is i.i.d with law that of under . Using the Borel-Cantelli lemma and estimate (2.3), we get that there are -a.s. only a finite number of such that is bigger than . On the other hand, the sequence under is a simple random walk, with an almost sure linear decay. Hence, the sum is finite -a.s. It follows that it is also finite -almost surely (by integration) and -almost surely (by conditioning on a nontrivial event). ∎

For Lemma 5.2), we need to prove the weak convergence of the law of under to that under , when . We start by introducing another notation,

It is clear that under , as well as under , we have almost surely and We also have a uniform convergence result: the law of the time under converges in probability to 0 when goes to , uniformly on , in the following sense:

| (3.8) |

Indeed, for any given and , we may choose such that Now, take . If , then , and there is nothing to prove. We suppose From a scaling property, for any , we have

Besides, under , we have and thus Hence, we have

where the next to last line is a disintegration formula for at time (recall that the law of under is ). Now, for small enough, and uniformly on , we get . The uniform convergence result is proved.

We are ready to tackle the proof of Lemma 5.2).

Proof of Lemma 5.2).

It is enough to prove the convergence of the expectation to for any continuous functional and any .

But Corollary 2 induces the convergence of the law of under to that under . It follows that goes to when goes to 0. This term in turn converges to when goes to . As for any , it follows

| (3.9) |

We finish this subsection with a corollary of Lemma 6.

Corollary 3.

Under , conditionally on , the sequence has the law of the random walk starting from and conditioned to stay positive at times .

Proof.

Under and conditionally on , the sequence has the law of the random walk starting from . The event , which is also equal to the event , has a positive and finite probability when . The expression of given in Lemma 6 directly implies the corollary. ∎

3.3 Proof of Lemma 5 in the critical case

In the critical case, we certainly can define and as before, but under these measures the time is almost surely equal to . Lemma 6 thus fails, and so does the previous construction of and .

However, an analogue of Corollary 3 will stay true and induce another construction of the law of the spatially stationary random walk . We will then use it to prove again the almost sure finiteness of , and Lemma 5 will follow from the same arguments as before. Throughout this subsection we assume .

3.3.1 The spatially stationary random walk in the critical case.

In order to formulate the analogue of Corollary 3, we need to define the “random walk conditioned to stay positive” for a random walk with null drift, for which the event of staying positive for all positive times has probability 0. This is done in [4]. We recall it here briefly.

Write as usual for the law of the random walk starting from position . If you write for the strictly descending ladder height process (defined in the exact similar way as the strictly ascending ladder height process, and also equal to the opposite of the strictly ascending ladder height process of ) , the renewal function is defined by

In particular is non-decreasing, right-continuous, and we have and for . The renewal function is invariant for the random walk killed as it enters the negative half-line. It enables us to define the process conditioned on never entering , thanks to a usual transform, in the sense of Doob. That is, the law of this process starting from , written , is defined by

| (3.10) |

for any functional of the first steps. For any and , we also write for the law of the random walk starting from and conditioned on never entering , defined in the exact same way, by

| (3.11) |

for any functional of the first steps. The only other thing we will need to know about is the following sub-additive inequality, which is a consequence of a Markov property:

| (3.12) |

Recall that is the drift of the strictly ascending ladder height process and write for the transition densities of the random walk. The following proposition gives a disintegration description of the spatially stationary random walk, which is very similar to that of the spatially stationary Lévy process introduced by Bertoin and Savov in [5].

Proposition 1.

The measure

is a probability law.

The law of is determined by:

Under , has the law .

Conditionally on and , the processes and are independent, the law of is , that of is .

The measure is nothing else than the stationary joint law of the overshoot and the undershoot. The proof of this proposition will last until the end of the subsection. As a preliminary, we introduce a crucial though rather simple lemma.

Lemma 7.

For any , we have:

| (3.13) | |||||

| (3.14) |

Proof.

By expressing the event as the limit of the events we get

The first term of the sum is equal to because the function is invariant for the random walk killed when hitting . The second term is positive and bounded from above by which goes to 0 when goes to . This proves equation (3.13). Then (3.14) is straightforward: Indeed, for functional of the first steps, we have:

∎

Now, recall that the invariance property of yields that, for any , we have

Define by for any real number . Thus for , and coincide, but for they certainly don’t. This enables us to define, for any , the law of the random walk starting from and conditioned on never entering at times , by the formula:

| (3.15) |

for any functional This definition is of course consistent with our previous notations. The following generalization of Lemma 7 and its corollary are consequences of straightforward calculations, that we leave to the interested reader

Lemma 8.

For any , any , we have

| (3.16) | |||||

| (3.17) |

Corollary 4.

Write (resp. ) for the first (resp. second) marginal of . These measures on are given for , by

Moreover,

where we have written for , as well as for

This corollary should make the introduction of the measure in the proposition more transparent. Indeed, it gives us two alternative ways of defining the measure . First, take distributed according to and, conditionally on , take of law and independent and of law (in the sense defined just before). Second, take distributed according to and, conditionally on , take of law conditioned on having a first jump no smaller than , and independent and of law .

Proof of the proposition.

We need to prove three things, the fact that is a probability measure (that is, has mass one), the fact that is spatially stationary, and the equality . We start with the spatial stationarity. Fix . We should prove that and have the same law under .

We introduce the notation for the instant of the last passage under level for the process . Besides, observe that is also equal to the instant of the last passage under level for the process . Suppose that we proved that has the same law as the process under . Then, conditionally on , it is clear that the process is independent of and follows the law . Besides, for a process under , conditionally on , the process is independent from and follows the law . This altogether proves that the process follows the law . Finally, from a Markov property, it is clear that given , the process is independent of and follows the law , thus the law of is .

Therefore, the only thing we still need to prove is the following duality property444This property also finds its analogue in [5], in their Theorem 2.: the variable has the same law as the variable for a process of law . Fix and a positive continuous functional. We should prove the following equality:

The case is particular and follows from this calculation:

In the case , we write , the usual duality property for random walks stating

We are ready to calculate

where is equal to

Now the two facts that has mass one and that both follow from the equality

for (recall that is the strictly ascending ladder height process). Fix some . We already know from (3.16) that , thus we should prove

| (3.18) |

This will be a consequence from another duality argument. Write for the instant when hits its minimum on times . Write (so that ). Then under and under are in duality. Indeed, fix and a positive continuous functional. Write also . Then,

This duality property implies in particular (3.18). ∎

3.3.2 Finiteness of in the critical case.

The only thing we actually need from the last subsection is the fact that under (or, equivalently, under ), the sequence is a random walk conditioned to stay positive, with some initial law. The paper [11] gives very precise results about the behavior of this random walk conditioned to stay positive, and we deduce in particular the following rough bounds that are sufficient for our purposes:

Lemma 9.

For any , we have

| (3.19) |

when -a.s.

We now work under and we recall that is then given by

We write for the duration of the arch of index . We need to transfer the results about the behavior of to results about the behavior of . This is made possible by the following lemma:

Lemma 10.

1) Under and conditionally on a realization , the variables are mutually independent, and the law of is that of under .

2) If for some real number , then

| (3.20) |

Proof.

The result of the first part is easy for , and we get the result for by spatial stationarity.

The -almost sure finiteness of follows straightforwardly. Write

and, for , write for the event

The lemma states that the probability of is bounded above by a constant times . Hence only a finite number of occur, almost surely. This together with (3.19) gives that the are summable, almost surely. This shows the -almost sure finiteness of and concludes the proof.

Appendix A Proof of Lemma 2

The uniqueness stated in the lemma is immediate. Indeed, if and are two probability laws satisfying the conditions of Lemma 2, then we have for any real , leading to . The existence result is based on Kolmogorov’s existence theorem, as follows.

First, note that we have for any real numbers. Consider and satisfying the hypothesis (2.5). Our first observation is that is necessarily concentrated on , and enjoys already the following “positive translation invariance property”. Consider any . The equality immediately yields, letting go to 0 and using for each term the hypothesis (2.5), the equality

| (A.1) |

For real numbers, let be the law on , defined as the image of by the application

It follows from (A.1) that all the one-dimensional marginals of are equal to . More generally, all the laws defined in that way are compatible. Hence Kolmogorov’s theorem yields the existence of a law on such that the finite dimensional marginal of on is equal to , whatever .

Consider a variable on with law . Fix . For any , we have , and therefore is independent of . Hence is an element of – write it – such that the value of and the restriction of to is independent of . We define a variable on by setting

where the limit is taken pointwise. Call its law. We clearly have . Moreover the law is spatially stationary. Indeed, for any , we have

but the family has the same law as , so also has law . Finally, we should prove the following convergence result of laws on :

for any . Take any positive bounded continuous functional depending on a finite number of variables , with , so that . We suppose without loss of generality . Observe that under the probability or under , we have , and the events and coincide, almost surely. Observe also . Then,

where we get the second line because the functional does not depend on , and where we obtain the last line thanks to the translation . Besides, we have:

and also

This is enough to deduce

The law converges weakly to .

Acknowledgements

I would like to thank specially J. Bertoin, my supervisor during this work, and A. Lachal, who made a remarkable work of rereading, and suggested many corrections and improvements.

References

- [1] P. Ballard. The dynamics of discrete mechanical systems with perfect unilateral constraints. Arch. Rational Mech. Anal., 154:199–274, 2000.

- [2] J. Bertoin. Reflecting a Langevin process at an absorbing boundary. Ann. Probab., 35(6):2021–2037, 2007.

- [3] J. Bertoin. A second order SDE for the Langevin process reflected at a completely inelastic boundary. J. Eur. Math. Soc. (JEMS), 10(3):625–639, 2008.

- [4] J. Bertoin and R. A. Doney. On conditioning a random walk to stay nonnegative. Ann. Probab., 22(4):2152–2167, 1994.

- [5] J. Bertoin and M. Savov. Some applications of duality for Lévy processes in a half-line. Bull. Lond. Math. Soc., 43(1):97–110, 2011.

- [6] A. Bressan. Incompatibilità dei teoremi di esistenza e di unicità del moto per un tipo molto comune e regolare di sistemi meccanici. Ann. Scuola Norm. Sup. Pisa Serie III, 14:333–348, 1960.

- [7] W. Feller. An introduction to probability theory and its applications. Vol. II. Second edition. John Wiley & Sons Inc., New York, 1971.

- [8] M. Goldman. On the first passage of the integrated Wiener process. Ann. Mat. Statist., 42:2150–2155, 1971.

- [9] A. Gut. Renewal theory and ladder variables. In Probability and mathematical statistics, pages 25–39. Uppsala Univ., Uppsala, 1983.

- [10] A. Gut. Stopped random walks. Springer Series in Operations Research and Financial Engineering. Springer, New York, second edition, 2009. Limit theorems and applications.

- [11] B. M. Hambly, G. Kersting, and A. E. Kyprianou. Law of the iterated logarithm for oscillating random walks conditioned to stay non-negative. Stochastic Process. Appl., 108(2):327–343, 2003.

- [12] E. Jacob. Excursions of the integral of the Brownian motion. Ann. Inst. H. Poincaré Probab. Statist., 46(3):869–887, 2010.

- [13] A. Lachal. Les temps de passage successifs de l’intégrale du mouvement brownien. Ann. Inst. H. Poincaré Probab. Statist., 33(1):1–36, 1997.

- [14] A. Lachal. Application de la théorie des excursions à l’intégrale du mouvement brownien. In Séminaire de Probabilités XXXVII, volume 1832 of Lecture Notes in Math., pages 109–195. Springer, Berlin, 2003.

- [15] H. P. McKean, Jr. A winding problem for a resonator driven by a white noise. J. Math. Kyoto Univ., 2:227–235, 1963.

- [16] D. Percivale. Uniqueness in the elastic bounce problem. J. Differential Equations, 56(2):206–215, 1985.

- [17] M. Schatzman. Uniqueness and continuous dependence on data for one dimensional impact problems. Math. Comput. Modelling, 28:1–18, 1998.

- [18] F. Spitzer. A Tauberian theorem and its probability interpretation. Trans. Amer. Math. Soc., 94:150–169, 1960.

- [19] E. Wong. Some results concerning the zero-crossings of Gaussian noise. SIAM J. Appl. Math., 14:1246–1254, 1966.

- [20] E. Wong. The distribution of intervals between zeros for a stationary Gaussian process. SIAM J. Appl. Math., 18:67–73, 1970.

- [21] M. Woodroofe. A renewal theorem for curved boundaries and moments of first passage times. Ann. Probability, 4(1):67–80, 1976.