Continuous time Ehrenfest process in term structure modelling

Abstract

In this paper, a finite-state mean-reverting model for the short-rate, based on the continuous time Ehrenfest process, will be examined. Two explicit pricing formulae for zero-coupon bonds will be derived in the general and the special symmetric cases. Its limiting relationship to the Vasicek model will be examined with some numerical results.

Keywords: ehrenfest model, interest rate derivatives, short-rate, term structure, vasicek model, zero-coupon bond

Classification: Primary 91G30

Secondary 60J28; 91G20; 33C52

1 Introduction

One of the fundamental approaches to term structure modelling is based on the specification of the short-term interest rate – the short-rate. Vasicek [20] first introduced a mean-reverting short-rate model with Gaussian distribution and derived a closed-form representation for the zero-coupon bond (ZCB) price. Since then, a variety of short-rate models have become established, each having its advantages and disadvantages.

Albeit the earliest, Vasicek’s model is still very popular among practitioners owing to its analytical tractability with regard to ZCB prices and European options thereof. Unfortunately, the model has some shortcomings. The most prominent of these is the possibility for the interest rates to become negative – a fact relating to all models with Gaussian distribution. Even though the probability of negative rates is rather small, not only is the realism of the model questionable, but also problems may appear while valuing ZCBs with a long time to maturity and a low interest rate level.

The idea of using both the discrete and the continuous time versions of the Ehrenfest process in finance is well-known. The discrete time approach was used, for example , by Okunev and Tippett [14] in modelling accumulated cashflows, by Takahashi [19] in exploring changes in stock prices and exchange rates for currencies, and by Buehlmann [5] in modelling interest rates. With regard to the modelling of interest rates, it seems that the discrete time approach leads in general only to a recursively computable term structure. Sumita, Gotoh and Jin [17] studied the passage times and the historical maximum of the Ornstein-Uhlenbeck process via an approximation by means of a special case of the continuous time Ehrenfest process.

This paper proposes a finite-state mean-reverting model for the short-rate related to the continuous time Ehrenfest process. By choosing arbitrary lower and upper bounds for the rate, the respective short-rate process can be seen as a suitably linearly transformed birth-and-death process on . By choosing the lower bound as non-negative, the problem of negative interest rates can be avoided. Furthermore, the model allows an explicit evaluation of ZCB prices. In this way, the model aims at realism and analytical tractability.

The main outcome of the paper is the derivation of pricing formulae for ZCBs in the general and the special symmetric cases of the model. In both cases the arbitrage-free ZCB price at time and maturity is given as follows:

where is a constant, and and can be expressed in terms of the hypergeometric functions of a matrix argument given in Section 2 (see also [7]). In the general case the model is governed by five parameters – a valuable fact considering the fitting of the model to the market data. The special case provides four parameters and is characterized by the symmetry of the underlying distribution with respect to the mean-reverting value. The advantage here is that we have more tractable expressions of and from the computational point of view. Moreover, a suitably transformed symmetric case of the model yields the Vasicek model in the limit as tends to infinity.

The paper is organized as follows: the following section gives a short review of the special functions we shall encounter throughout this paper. Section three deals with the Ehrenfest process in continuous time. The main results are given in section four, where the Ehrenfest short-rate model is defined and the ZCB pricing formulae are derived. The fifth section gives an overview of the Vasicek model and its limiting relationship to the Ehrenfest short-rate model. Section six illustrates the advantages of the Ehrenfest short-rate model.

This paper comprises part of my Ph.D. project at the Technische Universität Dortmund. I am deeply indebted to Professor Michael Voit for his patience and for being a wonderful research mentor.

2 Special functions and orthogonal polynomials

Throughout this paper we will make use of some well-known facts concerning the Krawtchouk polynomials (see [10], [18] and [21]) and functions (see [7]), as well as some of their practical implications. In the interests of clarity we give in this section an overview of these special functions.

Hypergeometric functions of matrix argument

2.1 Definition.

-

(a)

A partition is an -tuple of non-negative integers such that

-

(b)

For a partition the generalized Pochhammer symbol is defined by

where denotes the usual Pochhammer symbol.

-

(c)

For a partition the normalized Schur function of index is defined by

-

(d)

The hypergeometric function of matrix argument is defined as a real-analytic function on the space of Hermitian matrices with eigenvalues and is given by the series

(1) where, for and and none of the numbers is a non-negative integer.

We will be particularly concerned with the function, which is also known as the confluent hypergeometric function of matrix argument. From Theorem 4.1 in [7] we know that it converges absolutely for all An important result, that will be crucial later on, is given without proof in the following remark (see [7], p. 25).

2.2 Remark.

Let denote the standard simplex in defined by

| (2) |

Then for the following equation holds:

| (3) |

In order to compute the function numerically we truncate the series (1) by as follows:

| (4) |

Koev and Edelman [11] provide an effective algorithm for computing the function. For the complexity of their algorithm is linear in and subexponential in which is acceptable if we consider the fast convergence of the power series (4).

Krawtchouk polynomials

For given and the Krawtchouk polynomials are the orthogonal polynomials that relate to the binomial distribution and the probability mass function at the points They can be defined in two different, but equivalent ways.

2.3 Definition.

Definition 2.3 leads to the following basic well-known properties:

2.4 Lemma.

-

Symmetry:

(7) for all .

-

for all .

-

-

Generating function:

(8) for all

-

Recurrence relation:

(9) for all

-

Orthogonality relation:

(10) where

(11) for all

-

For

(12) Note that

3 Original Ehrenfest model

The original Ehrenfest model describes the heat exchange between two isolated bodies, each of arbitrary temperature. The temperatures are symbolized by the number of fluctuating balls in two urns with a total of balls. For details of the continuous and discrete time versions of the model we refer to [2], [10], [12] and [16].

In this section we shall discuss the continuous time Ehrenfest process. Primarily, its representation as a sum of independent simple processes will allow us to show the main result of this paper which comes up in the next section. Furthermore, we examine the transition semigroup of the Ehrenfest process and explore some of its basic properties.

Ehrenfest process

Let balls, initially distributed between urns I and II, fluctuate independently in continuous time between the two urns. We fix a fluctuation parameter and independent Poisson processes with intensity Let be a Markov chain with the state space and transition probability matrix

| (13) |

Then, the subordinated Markov chain describes the state of the -th ball at time where or when the -th ball is in urn I or II respectively. Hence,

| (14) |

is a Markov process with the state space denoting the number of balls in urn I at time We call the (continuous time) Ehrenfest process. A discrete time version of (14) with arbitrary and was studied by Kraft and Schaefer [12].

3.1 Remark.

-

(a)

A special case of (14) with first suggested by Siegert [16] and also studied by Bingham [2], where the transitions become “deterministic” in the sense of switching between the states 0 and 1, will be important for us later on in Section 4. (Its discrete time analogue leads to the original Ehrenfest chain).

-

(b)

Karlin and McGregor [10] provided an alternative but equivalent definition of (14) as a birth-and-death process with the state space . Here, the time intervals between events are independently exponentially distributed with intensity and for the birth and death rates are and respectively, where and are given as above. It can be verified that in the setting at hand

Before computing the transition semigroup of we need the following result:

3.2 Lemma.

The transition semigroup of is given by

| (15) |

where and

Proof.

Since is a Markov chain subordinated by a Poisson process with index the associated transition semigroup can be written as (see [3], p.333)

| (16) |

We can avoid the computation of by writing where is a stochastic matrix with is the identity matrix, and Then, (16) becomes

Since for all we can easily compute the above series, which completes the proof. ∎

3.3 Remark.

Analogue to the proof above, we see that a variation of and in (15) can be equivalently described as a suitable modification of and . Thus, the distribution of depends only on the two parameters and or, equivalently, and .

3.4 Theorem.

(Properties of the Ehrenfest process) Let be the Ehrenfest process given by (14).

-

The transition probabilities are given by

(17) where and are the Krawtchouk polynomials as given in Definition 2.3 .

-

The conditional mean and variance of are given by

(18) -

The stationary distribution is the limiting distribution, and it is given by the binomial distribution on with parameter

Proof.

Ad The proof here is similar to that in [2]. First, we compute the moment-generating function of given In the following we suppress the dependence of on when it is clear from the context. From Lemma 3.2 we have

Since are independent for all we obtain from (14) the moment-generating function of given as follows:

Applying and of Lemma 2.4, we obtain

Applying (8) once again, we get

Equating coefficients of completes the proof of the claim.

Ad Combining (17) with results and of Lemma 2.4, we obtain

| (20) | |||||

where for as given in (12), which implies (18). Moreover,

where is given by (12). A straightforward computation of

4 Ehrenfest short-rate model

In this section we introduce a finite-state mean-reverting short-rate model associated with the continuous time Ehrenfest process (14) and give its basic properties. As a main result, we exploit the algebraic-combinatorial roots of the Ehrenfest process and derive explicit pricing formulae for ZCBs in the general and the special cases of the process, both of which have their advantages.

Definition and properties

Let be an interval on the real line. We decompose it into equal pieces of length and consider the process

| (21) |

as a short-rate process with state space where is the Ehrenfest process given by (14) with . Considering Remark 3.1 , we notice that can be seen as an affine linearly transformed birth-and-death process on In the case at hand, can be interpreted as the state space discretization parameter. Clearly, also depends on . We will suppress this dependence when it is clear from the context. Bearing in mind Remark 3.3, we denote this short-rate model as model.

From Theorem 3.4 we immediately obtain the conditional mean and variance of given as follows:

| (22) | |||||

| (23) | |||||

where We also obtain the mean reversion of

| (24) | |||||

| (25) |

Thus, we have a total of five parameters, and to fit the model to the market data. Here, governs the skewness of the underlying distribution, and have an impact on its kurtosis, and influences the speed of reversion to the mean reverting value

Zero-coupon bond

We assume that an equivalent martingale measure (or risk-neutral measure) exists (see [13], Prop. 4.2), and that the underlying probability measure is this equivalent martingale measure. Let be the natural filtration of Then, the arbitrage-free ZCB price at time with a face value of 1 monetary unit and maturity at is given by (see [4], p. 51)

| (26) |

In the following we also omit explicitly writing out the dependence of on when it is clear from the context.

The calculation of (26) within the model with arbitrary is inspired by the proof of Theorem 3.1 in [6]. There, Delbaen and Shirakawa represent the transition probabilities of the underlying short-rate process as a weighted series of the Jacobi polynomials. Using orthogonality relations of the Jacobi polynomials, they obtain a pricing formula for ZCBs in the associated model. However, this formula is only semi-explicit, since it contains multiple integrals that have to be calculated iteratively. We will avoid this problem by representing such integrals in terms of functions.

4.1 Theorem (ZCB price in model).

Proof.

Let be the state of at time Bearing in mind that is a Markov process, and using the definitions (14) and (21), we get from (26)

| (29) | |||||

where for The last equality holds because of the independence of for all In the following we omit writing out the dependence on particular and set

| (30) |

Using (30), we rewrite (29) as follows:

| (31) |

From the power series representation of the exponential function, we obtain

where The last equality follows from

and the dominated convergence theorem.

For the given and we have

where Using the symmetry relation (7), we write the transition probabilities given in Theorem 3.4 as follows:

where Analogue to the calculation of the expected value (20) in the proof of Theorem 3.4, we obtain

where is defined by (12) and Iteratively, we get

Hence, (4) becomes

In order to evaluate the multiple integrals above, we tranform the integration domain to the standard simplex defined by (2) via the following mapping:

| (34) |

Using (4), we rewrite (34) as follows:

where and denotes the standard inner product. Applying (3) with we express the integrals in (4) as functions as follows:

| (36) |

for all setting If we combine (31) and (4) with (36) and the fact that the theorem follows. ∎

Now we consider the model with . On the one hand, we lose one of the fitting parameters, although, the model is still well suited to model the term structure, and it yields the famous Vasicek model in the limit (see Section 5). On the other hand, we obtain a more tractable pricing formula for ZCBs, where, in contrast to the general case, no multiple sums need calculation, which improves the computational speed.

The calculation of the arbitrage-free ZCB price (26) in this setting is very intuitive and requires no knowledge of the transition probabilities of since the only stochastic parameters are the arrival times of the underlying Poisson process.

4.2 Theorem (ZCB price in model).

Proof.

Let be the state of at time Analogue to the derivation of the expresion (31) in the proof of Theorem 4.1, we obtain

| (40) |

where

| (41) |

In order to evaluate , we count the number of jumps in the underlying Poisson process within the time interval and, denoting the jump times by and setting we split the integral on the right-hand side of (41), obtaining

At this point, we have to distinguish between even and odd numbers of jumps, since switches between 0 and 1 a.s. according to its transition probability matrix (13). Thus, conditional on the Markov chain stays in 1 after an even jump, whereas it stays in 0 after an odd jump. This consideration yields

Furthermore, from the order statistics property of the Poisson process (see, for example, [9], pp. 101-102), we know that the joint density of the arrival times of in conditional on is given by

| (42) |

Hence, for we obtain

| (43) | |||||

Analogue to the proof of Theorem 4.1, we consider the mapping given in (34) and integrate (43) by substitution, which yields

| (44) | |||||

where and denotes the standard inner product. Applying the relation (36), we rewrite (44) as follows:

| (45) | |||||

In similar fashion, we obtain

| (46) | |||||

If we combine (45) and (46) with (40), the theorem follows. ∎

Practical implementation

From Theorems 4.1 and 4.2, the ZCB prices can be computed approximately by truncating the series in the according formulae. We also use the truncated function defined by (4) as an approximation for the function.

In the setting of Theorem 4.2, we truncate the series (4.2) and (4.2), obtaining

| (48) | |||||

The choice of the truncation parameters and is left to the practitioner and should be made in the way of maintaining a balance between the accuracy of the results and the computational speed. Some numerical examples, which provide numerical accuracy and computational speed for the formulae (47) and (48), will be given at the end of the next section. In the following we omit explicitly writing out the dependence on and when it is clear from the context.

5 Connection to the Vasicek model

The Vasicek model [20] is one of the most popular short-rate models. Closed-form expressions of ZCB prices and European options thereof make the model highly appealing to practitioners. However, it also has some shortcomings.

In this section we give a short description of the Vasicek model. We point out its advantages and disadvantages. Here we follow paragraph 3.2.1 of [4]. We provide a convergence result, which shows that after a linear rescaling the model converges weakly to the Vasicek model. We show the convergence of the respective ZCB prices and provide some numerical examples.

Vasicek model

The formulation of the Vasicek model under the risk-neutral measure is

| (49) |

where are positive constants, and is the standard Wiener process on the probability space with the natural filtration Integration of the equation (49) yields for

| (50) |

Thus, conditional on is normally distributed with mean and variance

| (51) | |||||

| (52) |

Hence, the short-rate process tends to the mean-reverting value for The drawbacks of the model are the possible negativity of the interest rates, implied by the Gaussian distribution, and the fact that it is driven by only three parameters, which makes the calibration an ill-posed problem and yields often poor results.

The price at time of a ZCB with maturity at conditional on is given by

| (53) |

where

Convergence results

It is well known that the Ehrenfest process converges weakly to the Ornstein-Uhlenbeck process (see, for instance, [9], pp. 168-173, or [17]). The following theorem shows that the model also converges weakly to the Vasicek model.

5.1 Theorem.

Proof.

The proof follows analogue to [9], pp. 168-173, when we compute the conditional moments of ∎

5.2 Remark.

Karlin and McGregor show in a rigorous way (see [10], pp. 371-373), that the transition probability function (17) of the Ehrenfest process converges locally uniformly to the transition probability function of the Ornstein-Uhlenbeck process as which sharpens the above result after a linear transformation of the underlying processes.

A direct consequence of Theorem 5.1 is the convergence of the respective ZCB prices.

5.3 Corollary.

Proof.

W.l.o.g. let We denote by the space of the real-valued functions on that are right continuous and have left-hand limits (RCLL). From [1] (see p. 123), we know that a metric exists that makes a Polish space, i.e. a metric, separable and complete space. Clearly, and both lie in . With Theorem 5.1, it follows that in

Consider a linear operator on defined by

Clearly, is a continuous operator on Then, the operator defined by

is a continuous operator on Let and Then, Theorem 5.1 in [1] yields Since is uniformly integrable, it follows from Theorem 5.4 in [1] that

which completes the proof. ∎

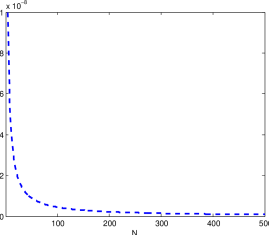

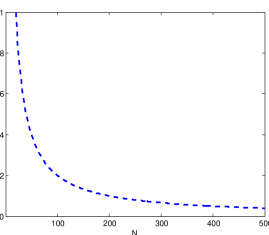

Figure 1 illustrates the convergence result of Corollary 5.3. All computations were made on an INTEL Core2Duo 2400MHz machine. We consider two scenarios: in case we have a favourable set of parameters for the ZCB valuation; in case we choose an unrealistic high of 20% for the interest rate market volatility and a time to maturity of 10 years. Within the Vasicek model the valuation is done according to the pricing formula (53). The approximative values of the ZCB prices in the model are computed according to Corallary 5.3 via (48) with and In both cases we observe fast convergence of the respective prices.

6 Discussion

In this section we discuss the advantages of the model with respect to the positivity of the interest rates. We use the case study of a ZCB valuation, showing that the model can still be used when the Vasicek model reaches its limits.

The main shortcoming of all models with Gaussian distribution, including the Vasicek model, is the positive probability of the interest rates becoming negative. Although this probability is rather small, some problems may appear while valuing ZCBs with long residual maturity. For instance, Rogers [15] illustrates how an attempt to keep the probability of negative interest rates negligible by choosing suitable parameters of the Vasicek model in the limiting case leads to an exponential growth in of the ZCB prices. Conversely, the model allows the choice of the lower and upper bounds and for the interest rate, and excludes the possibility of negative as well as unrealistically high positive interest rates.

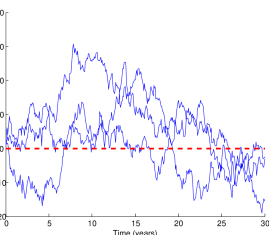

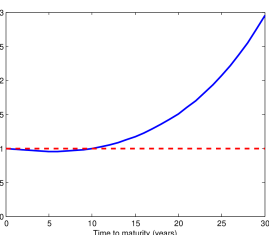

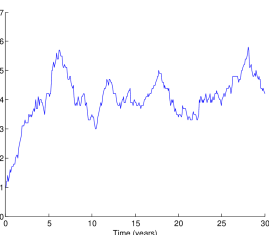

Times of financial crisis are often accompanied by interest rates near , as we see at present. The following example of pricing ZCBs in a respective scenario illustrates the advantage of the model over the Vasicek model. First, we assume the Vasicek model given according to (49) with and Figure 2 shows three sample paths of the underlying process over a period of 30 years simulated according to (50). We see that every path of the simulated process spends some time below the zero mark. Figure 2 demonstrates the weakness of the model in the case at hand, as we observe that the ZCB prices are not monotone falling in the time to maturity and even exceed the upper bound of 1 monetary unit, which is contradictory to no-arbitrage principles.

Now we consider the model in a similar hypothetical setting. We set the lower and upper bounds at and , and the state space discretization parameter We choose and in that we have with (24) a mean-reverting value of as in the case above. Here, we set as well. Figure 3 demonstrates a possible trajectory of the short-rate process over 30 years, simulated on the basis of the underlying distribution. In Figure 3 we see the strictly monotone decreasing character of the respective ZCB prices as a function of the time to maturity, which is highly plausible.

7 Conclusions

This paper has explored a finite-state mean-reverting short-rate model based on the Ehrenfest process. The respective short-rate process can be seen as an affine linearly transformed birth-and-death process on The model provides a certain degree of analytical tractability, since it allows explicit pricing of ZCBs and solves the problem of negative interest rates characteristic of Gaussian models. The pricing formulae for ZCBs have been derived for both the general case and the special case, in which the underlying distribution is symmetric with respect to the mean-reverting value. The key to both approaches has turned out to be the representation of the underlying Ehrenfest process as a sum of independent binary processes, which has been possible only in continuous time. We also used the hypergeometric functions of a matrix argument and the Krawtchouk polynomials. The special case benefits also from a more tractable pricing formula for ZCBs.

We have seen that the Ehrenfest short-rate model is a good approximation to the Vasicek model under normal conditions and a better alternative to it in extreme cases, where the interest rates are low and the volatility is high, providing solely positive interest rates. A further advantage of the model is the availability of five fitting parameters in the general case.

Our conclusion is that especially the general case of the Ehrenfest short-rate model is an interesting enrichment in the field of term structure modelling, combining analytical tractability with the desired property of interest rates remaining positive.

Problems that remain open for the short-rate model that we have examined here are the derivation of an explicit pricing formula for European options on ZCBs, parameter estimates for the model under the objective measure, and an extension of the model according to the three urn Ehrenfest model (see. [10], pp. 363 - 368).

References

- [1] Billingsley, P. (1968). Convergence of Probability Measures. John Wiley, New York.

- [2] Bingham, N. H. (1991). Fluctuation theory for the Ehrenfest urn. Adv. Appl. Prob. 23, 598–611.

- [3] Brémaud, P. (1999). Markov Chains: Gibbs Fields, Monte Carlo Simulation, and Queues. Springer, New York.

- [4] Brigo, D. and Mercurio, F. (2005). Interest Rate Models - Theory and Practice. Springer, Berlin.

- [5] Buehlmann, H. (1994). Continuous and discrete models in finance, in particular for stochastic interest rates. Riv. Mat. Sci. Econom. Social. 17, 3–20.

- [6] Delbaen, F. and Shirakawa, H. (2002). An interest rate model with upper and lower bounds. Asia-Pacific Finan. Markets 9, 191–209.

- [7] Gross, K. I. and Richards, D. St. P. (1989). Total positivity, spherical series, and hypergeometric functions of matrix argument. J. Approx. Theory 59, no. 2, 224–246.

- [8] Karlin, S. and Taylor, H. M. (1975). A First Course in Stochastic Processes, 2nd edn. Academic Press, New York.

- [9] Karlin, S. and Taylor, H. M. (1981). A Second Course in Stochastic Processes. Academic Press, New York.

- [10] Karlin, S. and McGregor, J. (1965). Ehrenfest urn models. J. Appl. Prob. 2, 352–376.

- [11] Koev, P. and Edelman, A. (2006). The efficient evaluation of the hypergeometric function of a matrix argument. Math. Comput. 75, 833–846.

- [12] Kraft, O. and Schaefer, M. (1993). Mean passage times for tridiagonal transition matrices and a two-parameter Ehrenfest urn model. J. Appl. Prob. 30, 964–970.

- [13] Lakner, P. (2006). Martingale measures for a class of right-continuous processes. Math. Finance 3, no. 1, 43–53.

- [14] Okunev, J. and Tippett, M. (1990). Continuous-time stochastic calculus: A survey of applications in finance and accountancy. IMA J. Math. Appl. Bus. Ind. 2, no. 2, 157–171.

- [15] Rogers, L. C. G. (1995). Which Model for Term Structure of Interest Rates Should One Use? In M. Davis, D. Duffie, W. Fleming and S. Shreve (eds.), Mathematical Finance. IMA Vol. Math. Appl. Vol. 65. Springer, New York.

- [16] Siegert, A. J. F. (1949). On the approach to statistical equlibrium. Phys. Rev. 71, 1708–1714.

- [17] Sumita, U., Gotoh, J. and Jin, H. (2006). Numerical exploration of dynamic behavior of Ornstein-Uhlenbeck process via Ehrenfest process approximation. J. Oper. Res. Japan 49, 256–278.

- [18] Szegö, G. (1983). Orthogonal Polynomials. Amer. Math. Soc. Colloquium Publ. 23, AMS. Providence, RI.

- [19] Takahashi, H. (2004). Ehrenfest model with large jumps in finance. Physica D 189, no. 1-2, 61–69.

- [20] Vasicek, O. (1977). An equilibrium characterisation of the term structure. J. Financ. Econ. 5, 177–188.

- [21] Voit, M. (1996). Asymptotic distributions for the Ehrenfest urn and related random walks. J. Appl. Prob. 33, no. 3, 340–356.