Adaptive LASSO-type estimation for ergodic diffusion processes

Abstract

The LASSO is a widely used statistical methodology for simultaneous estimation and variable selection. In the last years, many authors analyzed this technique from a theoretical and applied point of view. We introduce and study the adaptive LASSO problem for discretely observed ergodic diffusion processes. We prove oracle properties also deriving the asymptotic distribution of the LASSO estimator. Our theoretical framework is based on the random field approach and it applied to more general families of regular statistical experiments in the sense of Ibragimov-Hasminskii (1981). Furthermore, we perform a simulation and real data analysis to provide some evidence on the applicability of this method.

Key words: discretely observed diffusion processes, model selection, oracle properties, random fields, stochastic differential equations.

1 Introduction

The least absolute shrinkage and selection operator (LASSO) is a useful and well studied approach to the problem of model selection and its major advantage is the simultaneous execution of both parameter estimation and variable selection (see Tibshirani, 1996; Knight and Fu, 2000, Efron et al., 2004). This is realized by the fact that the dimension of the parameter space does not change (while it does with the information criteria approach, e.g. in AIC, BIC, etc), because the LASSO method only sets some parameters to zero to eliminate them from the model. The LASSO method usually consists in the minimization of an norm under norm constraints on the parameters. Thus it usually implies least squares or maximum likelihood approach plus constraints. The important property stating that the correct parameters are set to zero by LASSO method under the true data generating model, is called oracle property (Fan and Li, 2001). As shown by Zou (2006), since the classical LASSO estimator uses the same amount of shrinkage for each parameters, the resulting model selection could be inconsistent. To overcome this drawback, it is possible to consider an adaptive amount of shrinkage for each parameters (Zou, 2006).

Originally, the LASSO procedure was introduced for linear regression problems, but, in the recent years, this approach has been applied to time series analysis by several authors mainly in the case of autoregressive models. For example, just to mention a few, Wang et al. (2007) consider the problem of shrinkage estimation of regressive and autoregressive coefficients, while Nardi and Rinaldo (2008) consider penalized order selection in an AR() model. The VAR case was considered in Hsu et al. (2007). Very recently Caner (2009) studied the LASSO method for general GMM estimator also in the case of time series and Knight (2008) extended the LASSO approach to nearly singular designs.

In this paper we consider the LASSO approach for discretely observed diffusion processes. In this case, the likelihood function is not usually known in closed form, moreover most models used in application are not necessarily linear. In this paper, instead of working on a single approximation of the likelihood, we study the problem in terms of random fields (see Yoshida, 2005) which encompasses all widely used methods in the literature of inference for discretely sampled diffusion processes. Although we do not explicitly state the results in this form, the proofs in this paper, based on the properties of random fields, are immediately extensible to regular statistical experiments in the sense of Ibragimov-Hasmkinskii (1981), i.e. they apply to i.i.d. as well as regressive and autoregressive models.

For diffusion processes, the LASSO method requires some additional care because the rate of convergence of the parameters in the drift and the diffusion coefficient are different. We point out that, the usual model selection strategy based on AIC (see Uchida and Yoshida, 2005) usually depends on the properties of the estimators but also on the method used to approximate the likelihood. Indeed, AIC requires the calculation of the likelihood (see Iacus, 2008). On the contrary, the present LASSO approach depends solely on the properties of the estimator and so the problem of likelihood approximation is not particularly compelling.

It is worth to mention that, model selection for continuous time diffusion processes was considered earlier in Uchida and Yoshida (2001) by means of information criteria.

The paper is organized as follows. Section 2 introduced the model and the regularity assumptions and states the problem of LASSO estimation for discretely sampled diffusion processes. Section 3 proves consistency and oracle properties of the LASSO estimator. Section 4 contains a Monte Carlo analysis and one application to real financial data. Proofs are collected in Section 5. Tables and figures at the end of the manuscript.

2 The LASSO problem for diffusion models

In the first part of this Section, we introduce the model on which makes inference and some basic notations. Let be a -dimensional diffusion process solution of the following stochastic differential equation

| (2.1) |

where , , , , , and is a standard Brownian motion in . We assume that the functions and are known up to the parameters and . We denote by the parametric vector and with its unknown true value. For a matrix , we denote by and by the inverse of . Let . The sample path of is observed only at equidistant discrete times , such that for (with and ). We denote by our random sample with values in .

The asymptotic scheme adopted in this paper is the following: , and as . This asymptotic framework is called rapidly increasing design and the condition means that shrinks to zero slowly. We need some assumptions on the regularity of the process:

-

There exists a constant such that

-

.

-

The process is ergodic for every with invariant probability measure .

-

For all and for all , .

-

For every , the coefficients and are five times differentiable with respect to and the derivatives are bounded by a polynomial function in , uniformly in .

-

The coefficients and and all their partial derivatives respect to up to order 2 are three times differentiable with respect to for all in the state space. All derivatives with respect to are bounded by a polynomial function in , uniformly in .

-

If the coefficients and for all (-almost surely), then and .

Hereafter, we assume that the conditions hold. Let be the positive definite and invertible Fisher information matrix at given by

where

Moreover, we consider the matrix

where and are respectively the indentity matrix of order and .

In order to introduce the LASSO problem, we consider a random field admitting the first and second derivatives with respect to ; we denote by the vector of the first derivatives and by the Hessian matrix. Furthermore, we assume that the following conditions hold:

-

for each , we have that

(2.2) -

for each , let be a consistent estimator of given by

such that

(2.3)

An example of random field (contrast function) satisfying the assumptions is given by the quasi-likelihood function obtained by means the Euler approximation (see Kessler, 1997, Yoshida, 2005), that is

| (2.4) |

where , and . Then the unpenalized estimator

satisfies the assumption . For other examples, the reader can consult Bibby amd Sorensen, (1995), Kessler and Sorensen (1999), Nicolau (2002) and Aït-Sahalia (2008).

The classical adaptive LASSO objective function, in this case, should be given by

| (2.5) |

where and assume real positive values representing an adaptive amount of the shrinkage for each elements of and . Nevertheless, following the same approach of Wang and Leng (2007), we observe that by means of a Taylor expansion of at , one has immediately that

Therefore, we use the following objective function

| (2.6) |

instead of (2.5), and the LASSO-type estimator is defined as

| (2.7) |

The function is a penalized quadratic form and it has the advantage to provide an unified theoretical framework. Indeed, the objective function (2.5) allows us to perform correctly the LASSO procedure only if is strictly convex and this fact restricts the choice of the possible contrast functions for the model (2.1). Then, the function (2.6) overcomes this criticality. We also point out that has two constraints, because the drift and diffusion parameters and are well separated with different rates of convergence.

3 Oracle properties

As observed by Fan and Li (2001), a good procedure should have the oracle properties, that is:

-

•

identifies the right subset model;

-

•

has the optimal estimation rate and converge to a Gaussian random variable where is the covariance matrix of the true subset model.

The aim of this Section is to prove that LASSO-type estimator has a good behavior in the oracle sense.

As shown by Zou (2006) the classical LASSO estimation cannot be as efficient as the oracle and the selection results could be inconsistent, whereas its adaptive version has the oracle properties. Without loss of generality, we assume that the true model, indicated by , has parameters and equal to zero for and , while and for and . To study the asymptotic properties of the LASSO-type estimator , we consider the following conditions:

-

.

and where and

-

.

and where and

The assumption says us that the maximal tuning coefficient for the parameter and , with and , tends to zero faster than and respectively and then implies that , . Analogously, we observe that means that that the minimal tuning coefficient for the parameter and , with and , tends to infinite faster than and .

Theorem 1.

Under the conditions and , one has that

For the sake of simplicity, we denote by the vector corresponding to the nonzero parameters, where and , while is the vector corresponding to the zero parameters where and . Therefore, and .

Theorem 2.

Under the conditions and , we have that

| (3.1) |

From Theorem 1, we can conclude that the estimator is consistent. Furthemore, Theorem 2 says us that all the estimates of the zero parameters are correctly set equal to zero with probability tending to 1. In other words, the model selection procedure is consistent and the true subset model is correctly indentified with probability tending to 1.

To complete our program, we derive the asymptotic distribution of . Hence, we indicate by the submatrix of at point , that is

and introduce the following rate of convergence matrix

The next result establishes that the estimator is efficient as well as the oracle estimator.

Theorem 3 (Oracle property).

Under the conditions , and , we have that

| (3.2) |

Clearly, the theoretical and practical implications of our method rely to the specification of the tuning parameter and . As observed in Wang and Leng (2007), these values could be obtained by means of some model selection criteria like generalized cross-validation, Akaike information criteria or Bayes information criteria. Unfortunately, this solution is computationally heavy and then impracticable. Therefore, the tuning parameters should be chosen as is Zou (2006) in the following way

| (3.3) |

where and are the unpenalized estimator of and respectively, and usually taken unitary. The asymptotic results hold under the additional conditions

4 Performance of the LASSO method for small sample size

In this section we perform a small Monte Carlo analysis to check whether the LASSO method is able to select a specified model also in small samples. We also apply the method to a benchmark data set often used in the literature of model selection. The asymptotic framework of this paper is not completely realized in the next two applications, but nevertheless we test what happens outside the theoretical framework.

In both cases, we do not pretend to give extensive analysis of the method, because the previous theorems already prove the asymptotic validity of the LASSO approach for diffusion processes. Instead, we just want to show some evidence on simulated and real data to give the feeling of the applicability of the method.

4.1 A simulation experiment

We reproduce the experimental design in Uchida and Yoshida (2005). Therefore, we consider a diffusion process solution of the following stochastic differential equation

We simulate 1000 trajectories of this process using the second Milstein scheme, i.e. the data are simulated according to

with , and (resp. and ) are the first and second partial derivative in of the drift (resp. diffusion) coefficients (see, Milstein, 1978). This scheme has weak second-order convergence and guarantees good numerical stability. Data are simulated at high frequency and resampled at lower frequency for a total of observations. The simulations are done using the sde package (see Iacus, 2008) for the R statistical environment. So we estimate via LASSO the following five dimensional parametric model

and the true model is . The LASSO estimator is obtained plugging in the objective function , the quasi-likelihood estimator and the Hessian matrix obtained by the function particularized for the present model . For the penalization term we use in (3.3).

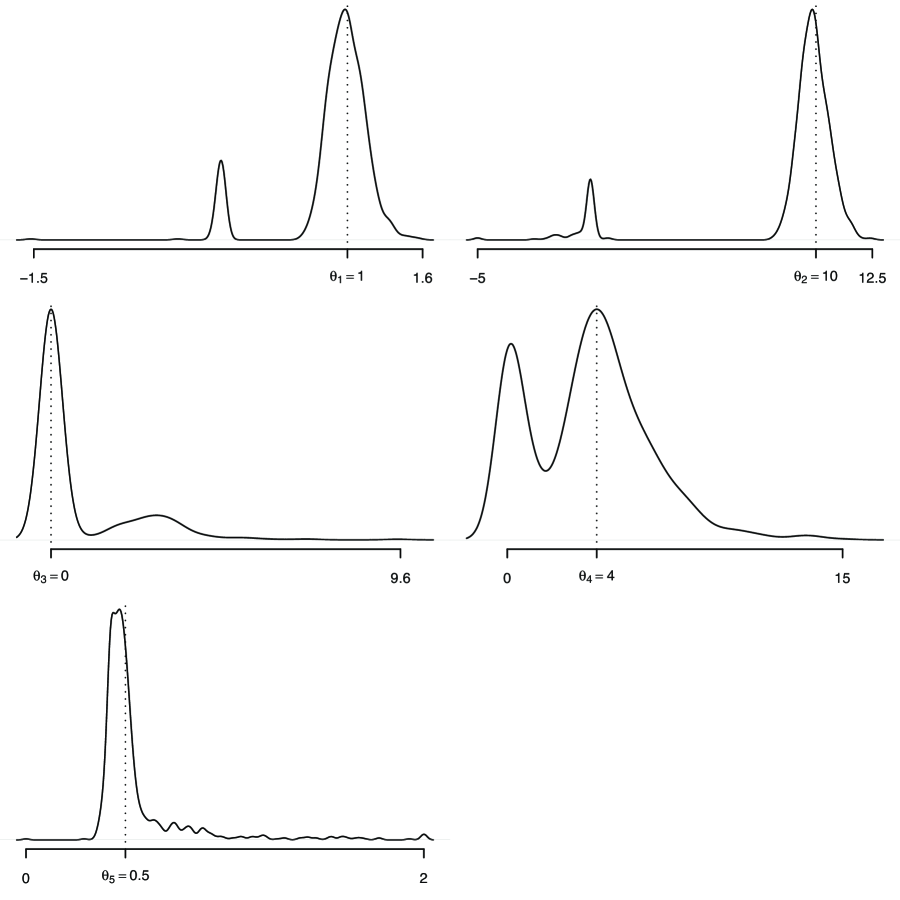

Figure 1 about here

Figure 1 reports the density estimation of the estimates of the parameters , against their theoretical true value. These distributions are obtained using the estimates obtained from the 1000 Monte Carlo replications. Figure 1 indicates that all parameters are correctly estimated most of the times and, in particular, the parameter is often estimated as zero.

4.2 An example of use in the problem of identification of the term structure of interest rates

In this section we reanalyze the U.S. Interest Rates monthly data from 06/1964 to 12/1989 for a total of 307 observations. These data have been analyzed by many author including Nowman (1997), Aït-Sahalia (1996), Yu and Phillips (2001) just to mention a few references. We do not pretend to give the definitive answer on the subject, but just to analyze the effect of the model selection via the LASSO in a real application. The data used for this application were taken from the R package Ecdat by Croissant (2006). The different authors all try to fit a version of the so called CKLS model (from Chan et al., 1992) which is the solution of the following stochastic differential equation

This model encompass several other models depending on the number of non-null parameters as Table 1 shows. This makes clear why the model selection on the CKLS model is quite appealing.

Table 1 about here

Our application of the LASSO method is reported in Table 2 along with the results from Yu and Phillips (2001) just for comparison.

Table 2 about here

Although we have proven that asymptotically the LASSO provides consistent estimates with the oracle properties, for finite sample size this is not always the case as mentioned by several authors. In this application, we estimate the parameters using quasi-likelihood method (QMLE in the table) in the first stage, then set the penalties as in (3.3) and run the LASSO optimization. We estimate the CKLS parameters via the LASSO using mild penalties (i.e. in (3.3)) and strong penalties (i.e. ). Very strong penalties suggest that the model does not contain the term and in both cases, the LASSO estimation suggest , therefore a model quite close to Cox, Ingersoll and Ross (1980). Being a shrinkage estimator, the LASSO estimates have very low standard error compared to the other cases. As said, this application has been done to show the applicability of the LASSO method and we do not pretend to draw in depth conclusions from this empirical evidence which is out of our competence.

5 Proofs

Proof of Theorem 1.

Following Fan and Li (2001), the existence of a consistent local minimizer is implied by that fact that for an arbitrarily small , there exists a sufficiently large constant , such that

| (5.1) |

with . After some calculations, we obtain that

Now, it is clear that from the condition , one has that . Furthermore, being , is uniformly larger than and

where is the minum eigenvalue of . We observe that

and then is bounded and linearly dependent on . Therefore, for sufficiently large, dominates with arbitrarily large probability. This implies (5.1) and the proof is completed by noticing that is striclty convex which implies that the local minimum is the global one. ∎

Proof of Theorem 2.

For

where is the -th row of . The first term of the previous expression is , while . Since Theorem 1, is a minimizer of , then necessarely, (see Proof of Theorem 2, Wang and Leng, 2007). Similarly for the estimators of the coefficients , we have that

and by means the same arguments we get that . ∎

Proof of Theorem 3.2.

Before starting the proof, it is necessary to introduce the following notations. Let

-

•

be the matrix with elements , ,

-

•

be the matrix with elements , , ,

-

•

be the matrix with elements , ,

-

•

be the matrix with elements , ,

-

•

be the matrix with elements , , ,

-

•

be the matrix with elements , ,

where

with

-

•

, where ,

-

•

, where ,

-

•

, where ,

and

with

-

•

, where ,

-

•

, where ,

-

•

, where .

From Theorem 2 follows that the estimator globally minimizes of the following objective function

Hence, the following normal equations hold

| (5.2) |

| (5.3) |

where and are respectively and vectors with -th and -th component given by and . From (5.2), by simple calculations, we have that

being by condition . Furthermore, by inverting the block matrix , we obtain that

where and then

By condition and the properties of the conditional multivariate Gaussian distribution, we derive that

and

Thus converges to . Similarly, from (5.3) we obtain that

with . Therefore, converges to . This concludes the proof. ∎

References

- [1] [] Aït-Sahalia, Y. (1996) Testing continuous-time models of the spot interest rate, Rev. Financial Stud., 9(2), 385–426.

- [2]

- [3] [] Aït-Sahalia, Y. (2008) Closed-form likelihood expansions for multivariate diffusions, Annals of Statistics, 36, 906-937.

- [4]

- [5] [] Bibby, B.M., Sorensen, M. (1995) Martingale observed diffusion estimation functions for discretely observed processes, Bernoulli, 1, 17-39.

- [6]

- [7] [] Brennan, M.J., Schwartz, E. (1980) Analyzing convertible securities, J. Financial Quant. Anal., 15(4), 907–929

- [8]

- [9] [] Caner, M. (2009) LASSO-type GMM estimator, Econometric Theory, 25, 270–290.

- [10]

- [11] [] Chan, K.C., Karolyi, G.A., Longstaff, F.A., Sanders, A.B. (1992) An empirical investigation of alternative models of the short-term interest rate, J. Finance, 47, 1209–1227.

- [12]

- [13] [] Cox, J.C., Ingersoll, J.E., Ross, S.A. (1980) An analysis of variable rate loan contracts, J. Finance, 35(2), 389–403.

- [14]

- [15] [] Cox, J.C., Ingersoll, J.E., Ross, S.A. (1985) A theory of the term structure of interest rates, Econometrica, 53, 385–408.

- [16]

- [17] [] Croissant, Y. (2006) Ecdat: Data sets for econometrics, R package version 0.1-5. Available at www.r-project.org.

- [18]

- [19] [] Dothan, U.L. (1978), On the term structure of interest rates, J. Financial Econ., 6, 59–69.

- [20]

- [21] [] Efron, B., Hastie, T., Johnstone, I., Tibshirani, R. (2004) Least angle regression, The Annals of Statistics, 32, 407–489.

- [22]

- [23] [] Fan, J., Li, R. (2001) Varaible selection via nonconcave peanlized likelihood and its Oracle properties, J. Amer. Stat. Assoc., 96(456), 1348-1360.

- [24]

- [25] [] Iacus, S.M. (2008) Simulation and Inference for Stochastic Differential Equations, Springer, New York.

- [26]

- [27] [] Ibragimov, I.A., Hasminskii, R.Z. (1981) Statistical Estimation: Asymptotic Theory, Springer, Berlin.

- [28]

- [29] [] Kessler, M. (1997) Estimation of an ergodic diffusion from discrete observations, Scandinavian Journal of Statistics, 24, 211-229.

- [30] Kessler, M., Sorensen, M. (1999) Estimating equations based on eigenfunctions for a discretely observed diffusion process, Bernoulli, 5, 299-314.

- [31]

- [32] [] Knight, K. (2008) Shrinkage estimation for nearly singular designs, Econometric Theory, 24, 323–337.

- [33]

- [34] [] Knight, K., Fu, W. (2000) Asymptotics for lasso-type estimators, Annals of Statistics, 28, 1536–1378.

- [35]

- [36] [] Merton, R.C. (1973) Theory of rational option pricing, Bell J. Econ. Manage. Sci., 4 (1), 141–183.

- [37]

- [38] [] Milstein, G.N. (1978) A method of second-order accuracy integration of stochastic differential equations, Theory Probab. Appl., 23, 396–401.

- [39]

- [40] [] Nardi, Y., Rinaldo, A. (2008) Autoregressive processes modeling via the Lasso procedure, available at http://arxiv.org/pdf/0805.1179.

- [41]

- [42] [] Nicolau, J. (2002) A new technique for simulating the likelihood of stochastic differential equations, Econometrics Journal, 5, 91-103.

- [43]

- [44] [] Nowman, K. (1997) Gaussian estimation of single-factor continuous time models of the term structure of interest rates, Journal of Finance, 52, 1695–1703.

- [45]

- [46] [] Hsu, N.-J., Hung, H.-L., Chang, Y.-M. (2008) Subset selection for vector autoregressive processes using the Lasso, Computational Statistics & Data Analysis, 52, 3645–3657.

- [47]

- [48] [] Tibshirani, R. (1996) Regression shrinkage and selection via the Lasso, J. Roy. Statist. Soc. Ser. B, 58, 267–288.

- [49]

- [50] [] Uchida, M., Yoshida, N. (2001) Information Criteria in Model Selection for Mixing Processes, Statistical Inference for Stochastic Processes, 4, 73–98.

- [51]

- [52] [] Uchida, M., Yoshida, N. (2005) AIC for ergodic diffusion processes from discrete observations, preprint MHF 2005-12, March 2005, Faculty of Mathematics, Kyushu University, Fukuoka, Japan.

- [53]

- [54] [] Vasicek, O. (1977) An equilibrium characterization of the term structure, J. Financial Econ., 5, 177–188.

- [55]

- [56] [] Wang, H., Leng, C. (2007) Unified LASSO estimation by Least Squares Approximation, J. Amer. Stat. Assoc., 102(479), 1039-1048.

- [57]

- [58] [] Wang, H., Li, G., Tsai, C.-L. (2007) Regression coefficient and autoregressive order shrinkage and selection via the Lasso, J.R. Statist. Soc. Series B, 169(1), 63-78.

- [59]

- [60] [] Yoshida, N. (2005) Polynomial type large deviation inequality and its applications, to appear in Ann. Inst. Stat. Mat.

- [61]

- [62] [] Yu, J., Phillips, P.C.B. (2001) Gaussian estimation of continuous time models of the short term interest rate, Cowles Foundation Discussion Paper, n. 1309. Available at cowles.econ.yale.edu/P/cd/d13a/d1309.pdf

- [63]

- [64] [] Zou, H. (2006) The adaptive LASSO and its Oracle properties, J. Amer. Stat. Assoc., 101(476), 1418-1429.

- [65]

| Reference | Model | |||

|---|---|---|---|---|

| Merton (1973) | 0 | 0 | ||

| Vasicek (1977) | 0 | |||

| Cox, Ingersoll and Ross (1985) | ||||

| Dothan (1978) | 0 | 0 | 1 | |

| Geometric Brownian Motion | 0 | 1 | ||

| Brennan and Schwartz (1980) | 1 | |||

| Cox, Ingersoll and Ross (1980) | 0 | 0 | ||

| Constant Elasticity Variance | 0 | |||

| CKLS (1992) |

| Model | Estimation Method | ||||

|---|---|---|---|---|---|

| Vasicek | MLE | 4.1889 | -0.6072 | 0.8096 | – |

| CKLS | Nowman | 2.4272 | -0.3277 | 0.1741 | 1.3610 |

| CKLS | Exact Gaussian | 2.0069 | -0.3330 | 0.1741 | 1.3610 |

| (0.5216) | (0.0677) | ||||

| CKLS | QMLE | 2.0822 | -0.2756 | 0.1322 | 1.4392 |

| (0.9635) | (0.1895) | (0.0253) | (0.1018) | ||

| CKLS | QMLE + LASSO | 1.5435 | -0.1687 | 0.1306 | 1.4452 |

| with mild penalization | (0.6813) | (0.1340) | (0.0179) | (0.0720) | |

| CKLS | QMLE + LASSO | 0.5412 | 0.0001 | 0.1178 | 1.4944 |

| with strong penalization | (0.2076) | (0.0054) | (0.0179) | (0.0720) |