Koszykowa 75, PL-00-662 Warsaw, Poland 22institutetext: ETH Zurich, Switzerland, and Swiss Finance Institute, Switzerland

Dedicated to Werner Ebeling on the occasion of his 75th birthday

The Lehman Brothers Effect and Bankruptcy Cascades

Abstract

Inspired by the bankruptcy of Lehman Brothers and its consequences on the global financial system, we develop a simple model in which the Lehman default event is quantified as having an almost immediate effect in worsening the credit worthiness of all financial institutions in the economic network. In our stylized description, all properties of a given firm are captured by its effective credit rating, which follows a simple dynamics of co-evolution with the credit ratings of the other firms in our economic network. The dynamics resembles the evolution of Potts spin-glass with external global field corresponding to a panic effect in the economy. The existence of a global phase transition, between paramagnetic and ferromagnetic phases, explains the large susceptibility of the system to negative shocks. We show that bailing out the first few defaulting firms does not solve the problem, but does have the effect of alleviating considerably the global shock, as measured by the fraction of firms that are not defaulting as a consequence. This beneficial effect is the counterpart of the large vulnerability of the system of coupled firms, which are both the direct consequences of the collective self-organized endogenous behaviors of the credit ratings of the firms in our economic network.

pacs:

89.65.GhEconomics; econophysics, financial markets, business and management1 Introduction

The largest financial crisis since the great depression started in 2007 with an initially well-defined epicenter focused on mortgage backed securities (MBS). It has since been cascading into a global economic recession, whose increasing severity and uncertain duration has led and is continuing to lead to massive losses and damage for billions of people. This crisis has brought to the attention of everyone the concept that risk can be endogenous and can cascade as a growing avalanche through the financial and economic system. This is the opposite of the assumption held previously by many regulators, credit agencies and bankers that risks can be managed by using models essentially focusing on the risk of each single institution, and by combining them using assumptions of inter-dependencies calibrated in good times. The unveiled systemic nature of financial risks makes now clear the need for global approaches including economic and financial networks and modeling the collective behaviors that results from the coupling between institutions, firms, financial products and so on.

During the development of the crisis in 2008, a succession of problems unfolded, the most prominent ones being associated with names such as Bear Stearns, Fannie, Freddie, AIG, Washington Mutual, and Wachovia. Except for the famous bankruptcy of Lehman Brothers Holding Inc., all the other “too-big-to-fail” financial institutions and insurance companies were bailed out, while thousands of smaller banks have been left alone to undergo bankruptcy.

We propose here a minimalist framework to account for the observed cascade of defaults, which incorporates the impact of changes of beliefs in credit worthiness of a given firm, resulting from the change of credit worthiness of other institutions in the same economic network. In this way, we are able to account for the cascade phenomenon, and explain how small changes can lead to dramatic consequences, all the more so, the more coupled is the economic network and the larger is the number of firms. Our framework allows us to also analyze the so-called “Lehman Brothers” effect, i.e., the crash on the stock market and the subsequent panic among financial institutions, following its filling for bankruptcy on 15 September 2008. We account for this aftermath by introducing a global field influencing every firm by enlarging the probability of rating downgrade, which embodies the psychological impact of the destruction of trust among institutions, which suddenly realized that, after all, the US Treasury and the Federal Reserve might not bail them out. The abrupt drop in confidence led to a drop in credit supply and to the major recession. Finally, we investigate, within our set-up, the effect of a simple bail-out policy consisting of accepting to rescue a certain number of defaulting firms. We find that this rescue policy is the most efficient when the economy is functioning at its most vulnerable state of critical coupling between its constituting firms.

Many models have been proposed to investigate the effects of credit contagion on the default probability of individual firms. Motivated by the accounting scandals at Enron, Worldcom and Tyco, Giesecke Giesecke04 developed a structural model of correlated multi-firm default, in which investors update their belief on the liabilities of remaining firms after each firm default, which leads to contagious jumps in credit spreads of business partners. Eisenberg and Noe created a model of contagion in a network of liabilities EisenbergNoe . When an agent cannot fulfill its obligation, it defaults and the loss propagates along the network. Propagation of this distress can trigger off another defaults by contagion. Battiston et al. Battistonetal07 studied a simple model of a production network in which firms are linked by supply-customer relationships involving extension of trade-credit. They recover some stylized facts of industrial demography and the correlation, over time and across firms, of output, growth and bankruptcies. Delli Gatti et al. Delligattietal studied the properties of a credit-network economy characterized by credit relationship connecting downstream and upstream firm through trade credit and firms and banks through bank credit. They included a change in the network topology over time due to an endogenous process of partner selection in an imperfect information decisional context, which leads to an interplay between network evolution and business fluctuations and bankruptcy propagation. The bankruptcy of one entity can bring about the bankruptcy of one or more other agents possibly leading to avalanches of bankruptcies. Azizpour et al. Azizpour developed a self-excited model of correlated event timing to estimate the price of correlated corporate default risk. Sakata et al. Sakata06 introduced an infectious default and recovery model of a large set of firms coupled through credit-debit contracts and determined the default probability of defaults. Ikeda et al. Ikeda07 have developed an agent-based simulation of chain bankruptcy, in which a decrease of revenue by the loss of accounts payable is modeled by an interaction term, and bankruptcy is defined as a capital deficit. Lorentz et al. Lorenzetal09 have introduced a general framework for models of cascade and contagion processes on networks using the concept of the fragility of a firm, including the bundle model, the voter model, and models of epidemic spreading as special cases. Ormerod and Colbaugh Ormerod-Colbaugh developed a model of heterogeneous agents interacting in an network evolving according to the formation of alliances based on the decisions of self-interested fitness optimizers. In the presence of external negative shocks, they find that increasing the number of connections causes an increase in the average fitness of agents, and at the same time makes the system as whole more vulnerable to catastrophic failure/extinction events on an near-global scale. Schafer et al. Schaferretal07 set up a structural model of credit risk for correlated portfolios containing many credit contracts exposed to risk factors which undergo jump-diffusion processes and derive the full loss distribution of the credit portfolios. Neu and Kühn Neu-Kuhn2004 generalized existing structural models for credit risk in terms of credit contagion with feedbacks, using the analogy to a lattice gas model from physics. Already for moderate micro-economic dependencies, they find that, for stronger mutually supportive relationship between the firms, collective phenomena such as bursts and avalanches of defaults can be observed in their model. Hatchett and Kühn Hatchett-Kuehn studied the model of Neu-Kuhn2004 and found it to be solvable for the loss distributions of large loan portfolios with fat tails. Anand and Kühn AnandKuhn07 extend these analyzes by studying the functional correlation approach to operational risk and discover the coexistence of operational and nonoperational phases, such that their credit risk systems are susceptible to discontinuous phase transitions from the operational to nonoperational phase via catastrophic breakdown. Their model is also relevant to understand the cascades of unprecedented losses suffered in August 6, 2007, by a number of high-profile and highly successful quantitative long/short equity hedge funds Khandani-Lo .

The organization of the paper is as follows. Section 2 describes the model, with the definition of the key variable, the “effective credit rating grade” (ECRG), its dynamics, and how we take into account the interdependencies between firms through the changes of their ECRGs. Section 3 presents the main results of how a global crisis occurs in our model, and the relevance of a phase transition in the presence of the “panic” effect. Section 4 examines the sensitivity of the paths of defaulting economies as a function of the average coupling strength between firms, the panic field and the initial probabilities of ECRG changes. Section 5 presents some results on the impact of a simple rescue policy consisting in preventing the first few defaults to occur. Section 6 concludes.

2 Description of the model

Our model is adapted from Sieczka and Hołyst Sieczka , who introduced a stylized model of financial contagion among interacting companies.

2.1 Definition of the key variable: “effective credit rating grade” (ECRG)

Since we wish to focus on the possible contagion and cascade of defaults among the firms in a network, we abstract from the multidimensional complexity of all the variables impacting a firm’s financial health. We propose to capture the solvability of a given firm by a single variable that we refer to as the “effective credit rating grade” (ECRG). In our simulations, we will consider a rather small number of effective credit rating grades, that is, we assume that the ’s take discrete values: , with . When , investors (who are international to the networked economy) consider agent to be a safe investment. As the grade decreases, the risk perception of the investors on agent ’s future profitability (and viability) increases. In other words, investors are more skeptical of agent and hence less likely to lend to agent in the future. For , agent has defaulted on at least one of its obligations to the lenders. This defaulted state is assumed to be an absorbing state in that, once an agent has defaulted in the economy, it remains so for the remainder of time. The effective credit rating grade associated with each firm provide an integrated, low dimensional and effective indicator of the investors’ subjective perception of the creditworthiness of firm . We conjecture that the effective credit rating grade can be obtained as the end result of a Mori-Zwanzig projection technique applied to a full behavioral model, after integrating over all degrees of freedom except these effective ratings degrees of freedom, similarly to the approach of Neu and Kuhn on market risks KuhnNeu08 .

The term “effective credit rating grade” derives obviously from the standard credit rating which is provided by credit rating agencies such as Fitch Ratings, Moody’s Investors Service or Standard & Poor’s in the U.S. Indeed, it is well-known that there is a strong correlation between credit quality and default remoteness: the higher the rating, the lower the probability of default, and the lower ratings always correspond to higher default ratios BrandBahar2001 . With default as our target, our model can also be thought of as a description of the world of financial instruments and their interactions. Thus, our model can also be taken as a description of a network of various financial instruments, including collateral debt obligations and structured asset-backed security, which formed the substrate on which the 2007 crisis developed. Note that the choice of the discrete values, , with , for is motivated by the principal grades (AAA, AA, A, BBB, BB, B, CCC) used by rating agencies. We associate deterministically the eighth lowest level to the state of default. This corresponds to a stylized representation of the well-known abrupt increase of default rates as credit rating deteriorates. For instance, for the period from 1981 to 1999, Standard & Poor’s reported a probability of default per year for AAA-rated firms, compared with a value of per year for B-rated firms and a value of for CCC-rated firms BrandBahar2001 . In the same vein, the probability of a default over a 15 year period is for AAA-rated firms, compared with for B-rated firms and of for CCC-rated firms.

Our aim is to account for the many complexities associated with the default hazard of each firm by focusing on the dynamics of a single variable for each firm. Then, the question arises as whether the dynamics of the standard credit ratings are faithful indicators of the evolution of firm default hazards. The answer is probably negative, in view of the wave of defaults that started in 2007 and accelerated in 2008, in which many financial instruments, special vehicles as well as major insurance companies and investment banks that were rated AAA turned out to default.

This is the principal reason for our proposal to think of each , as not being the official published credit rating grade but, as an “effective credit rating grade”, which can be interpreted in several ways. It could be the real internal credit worthiness, that credit agencies should strive to uncover. Another way to think about the effective credit rating grade is that it is the rating that the rating agency has produced internally but not yet published due to their well documented conflict of interest leading to patently misleading published ratings. Indeed, it is now well-recognized that the rating grade provided by rating agencies are imperfect, as shown by the development of the financial crisis since 2007: (i) credit rating agencies do not downgrade companies promptly enough; (ii) credit rating agencies have made significant errors of judgment in rating structured products, particularly in assigning AAA ratings to structured debt, which in a large number of cases has subsequently been downgraded or defaulted. The “effective credit rating grade” of a given firm can be also interpreted as quantifying the risk perception of the market concerning that firm.

2.2 Dynamical evolution of the ’s, for in a network of firms

We consider a network of firms operating in a common economic environment. We assume that the dynamics of the financial health of firms can be captured by that of their effective credit rating grades (ECRG) ’s. We assume the simple discrete correlated random walk with constraints,

| (1) |

where is a stochastic variable taking only three possible values .

This means that the ECRG of a given firm can change by no more than one level over one time step, i.e., .

Since a value of the ECRG of a firm equal to corresponds to the maximum possible level, if , then can only either remain at the same level or decrease by . This means that the one–time-step ECRG change of a firm can only take values or if . This corresponds to a “reflecting” condition of the discrete correlated random walk (1).

We assume that, when a firm or a financial product defaults, it does not recover and remains at the default state . This corresponds to remaining equal to for all subsequent time steps and this is an “absorbing” condition for the discrete correlated random walk (1). Because we are describing a short time span of just a few years in our simulations, we do not include a firm entry process. Neglecting the creation of new banks seems to be a reasonable assumption when thinking of the economy of banks during the financial crisis.

2.3 Interdependencies between firms in the changes of their effective credit rating grades

There is rich literature on networks of firms, including credit and corporate ownership networks, as well as production, trade, supply chain and innovation networks (see e.g. SchweitzerScience09 ; SchweitzerACS09 and references therein). These links between firms are concrete and quantifiable through cash flows or control structures (such as voting rights). But, many of these links, forming complex networks of creditor/obligor relationships, revolving credit agreements and so on, are largely unmapped Lo08 . This supports considering another type of networks, a network of more intangible but nonetheless essential relationships of how the credit rating grades of different firms interact. This idea is also suggested by the cases of the Asian crises of 1997 and the more recent subprime crisis of 2007-2008.

Consider first the case of the Asian crises in 1997 and the remarkable fact emphasized by Krugman Krugman_depressioneconomics08 that the traditional measures of vulnerability did not forecast the crisis. One possible explanation is that the problem was off the government’s balance sheet, and not part of the governments’ visible liabilities until after the fact. The crisis developed as a self-fulfilling generated downward spiral of asset deflation and disintermediation. Post-mortem analyses have generally concluded that the key ingredient was that many of the Asian countries at that time had either pegged their currency to the dollar or operated in a narrow exchange rate band. In addition, asset price bubbles were growing in these countries, catalyzed by an influx of foreign funds. With deteriorating economic conditions, these economies became ripe for speculative attacks and bank runs. The sequence of events was one of speculative attacks on the currency pegs in Thailand and Malaysia followed by flight of capital away from these and surrounding economies, a process sometimes referred to as twin-crisis Goldsteintwincrises05 .

This all looks clear in hindsight, but the notion of ripeness to speculative attacks and bank runs is a matter of debate. For instance, no bank, however sound its capital and liability structure, can survive a bank run, by construction. Krugman Krugman_depressioneconomics08 emphasizes another important effect, what we could call a “virtual” network effect: while the real economic and financial links between the strongest Asian tigers (South Korea and Hong-Kong) and the others were weak on a relative GDP measure, foreign investors lumped them in their mental framework as part of the same “Asian” portfolio. Starting in Malaysia in July 1997, the contagion of the crisis to the other Asian countries was actually strongly amplified by the misperception by foreign investors that these different economies (Thailand, Malaysia, South Korea, Hong Kong…) were strongly linked. According to this mental framing Ariely09 , the problem of Thailand was not just a one-country happenance due to a localized over-indebtness, but it was thought that this was the problem of the whole economic Asian zone. While the vulnerability of South Korea and Hong Kong has been disputed, the incorrect geographical emphasis made the links become self-created by the western investors and banks pulling out from all these countries simultaneously in a process analogously to a bank run (see the argument developed in some details in Krugman_depressioneconomics08 ).

The causes of the financial and economic crisis initiated by the subprime crisis starting in 2007 are multiple and intertwined. The following elements have been documented and argued to be important contributors: (i) Real-estate loans and MBS (morgage backed securities) as fraction of bank assets, leading to feedback loops in leverage and ultimately in fragility; (ii) Managers’ greed and poor corporate governance problems; (iii) Deregulation and lack of oversight; (iv) Bad quantitative risk models in banks (Basel II); (v) Lowering of lending standards; (vi) Securitization of finance; (vii) Leverage; (viii) Rating agency failures; (ix) Under-estimating aggregate risks; (x) Growth of over-capacity; (xi) the agenda of several successive US administration to promote accession to house ownership to the middle-class and poor; (xii) Government sponsored entities such as Freddy Mac and Fanny Mae with unfair access to liquidity and mispriced returns due to the implicit Government put option. There is an enormous contemporary literature, which is growing everyday and which analyzes these different factors and suggests new solutions and new designs.

However, Sornette and Woodard argued recently SorWood10 that these elements were part of and contributed to a more global process, dubbed “the illusion of the perpetual money machine,” that developed over the last twenty years. During its development, the shadow banking (with a capital value peak of $2.2 trillions in early 2007) constituted a large network of inter-dependencies between financial instruments and between investment houses including banks, that became apparent only after the crisis started to unfold Krugman_depressioneconomics08 . This shadow banking system included such financial instruments as the auction rate preferred securities, asset-backed commercial paper, structured investment vehicles, tender option bonds and variable rate demand notes. These different instruments are indeed interacting directly through their overlapping collaterals and underlying assets, and indirectly through their impacts onto investment portfolios, through the joint impact of economic and/or financial shocks and, very importantly through the psychological contagion of investors.

These elements motivate us in modeling the direct as well as indirect couplings between firms through the effective credit rating grade changes ’s. This provides us with a coarse-grained description that has the advantage of lumping together many coupled mechanisms. Following the theory of multinomial choice McFadden74 ; McFadden78 , we formulate the conditional probability for the ECRG change of a given firm under the form

| (2) |

where is the Kronecker delta and ensures a proper normalization. Here, the on the left side of is realized at time , while the conditioning variables on the right side of are realized at time . Expression (2) gives the dependence of the probability that the ECRG change of a firm takes a value , or , given the previous ECRG changes at , and given the ECRG level at time . The probability of a rating change does not depend on a rating history. It is an assumption that agrees with a behavior of the Merton model in which a value of a firm’s asset evolves as a geometric Brownian motion and rating classes can be translated into thresholds of the firm’s asset value.

This Ising-like expression (2) is also motivated by the demonstration that finite-size long-range Ising model turns out to be an adequate model for the description of homogeneous credit portfolios and the computation of credit risk when default correlations between the borrowers are included MolinsVives . This probability (2) is controlled by two contributions.

-

1.

The term describes a mimetic or contagion effect, as well as a persistence mechanism: the larger the number of firms which have seen their grading updated upward (respectively unchanged or downward), the more new firms will have their grading updated upward (respectively unchanged or downward) in the next time step.

The strength of the influence of firm on firm and vice-versa (as we assume for simplicity symmetric couplings) is quantified by the symmetric interaction matrix . The elements can take zero, negative, or positive values. For , the two firms do not influence each other through the contagion effect. A positive corresponds to two dependent firms in the same industry branch, such that an improving (respectively worsening) condition in one of them tends to improve (respectively worsen) the situation of the other firm. In contrast, a negative may describe anti-correlations, such that one firm might profit at the expanse of the other one. As there is clear evidence of a strong bias toward positive correlations among firms, we assume that the ’s are normally distributed with a positive mean and standard deviation :

(3) -

2.

The term embodies the sentiment of panic, which was triggered when Lehman Brothers Holding Inc., a global financial-services firm, declared bankruptcy on 15 September 2008. The field is equal to zero until the first bankruptcy occurs in the network of firms, after which it remains fixed to : after the first bankruptcy occurs in our network, all credit rating grades are biased towards deteriorating, where is the strength of this bias. Formally,

(4) which is equal to when at least one firm defaulted (), otherwise the field is equal to . The field models a global shock which appears after the default of a first company. The “panic” field captures the psychological impact of the destruction of trust among institutions. Its structural impact is reasonable in the interpretation of the “effective credit rating grade” of a given firm as quantifying the risk perception of the market concerning that firm. The activation of describes the contagion effect of the increased risk perception. The activation of can also be justified as describing a genuine loss of real internal credit worthiness following a shock on one of the firms, due to the inter-connected liabilities in the bank balance sheets.

Finally, the panic term in equation (2) is either (if there is at least one bankrupted firm) or (if there is none). It could be argued to be more realistic to make the panic term depending on the number of bankrupted firms. Our simplifying framework consists in considering only the systemically important institutions such as Bear Stearns, Fannie, Freddie, AIG, Washington Mutual, Wachovia and so on, which are considered consensually to be “too-big-to-fail” financial institutions and insurance companies. Just one of them going to bankruptcy is arguably sufficient to trigger the Lehman Brothers type of panics that we model here.

Our goal is to study what is the effect on the global firm network of the change in psychological attitude of investors following the first bankruptcy.

3 Global crisis as a phase transition in the presence of the “panic effect”

3.1 Description of the numerical simulation procedure

We simulated a system of firms. The standard deviation of the coupling coefficients defined by (3) is set to . We fix the average value of the coupling coefficients and the value of the “panic field.”

-

1.

We generate a given realization of a randomly initialized matrix ;

-

2.

The initial sets of and are generated from uniform distributions (with exclusion of );

- 3.

-

4.

We repeat the previous step times in total, so as to update the rating of firms, which defines one complete time step;

-

5.

We then go back to steps 3 and 4 and iterate them times, which corresponds to a total lifetime of time steps;

-

6.

We count the number of defaults () that have occurred over these time steps;

-

7.

The whole procedure starting from step 1 to step 6 is repeated 1000 times to generate 1000 different realizations over which we can average over the random realizations of the matrix and over the initial values of and .

In the following, we analyze different properties of the systems of firms as a function of and .

3.2 Critical point and susceptibility

3.2.1 Absence of the global “panic” field ()

In the absence of the panic field (), the dynamics of the ’s defined by model (2) with the updating rules described in subsection 3.1 is nothing but the implementation of the Glauber algorithm Glauber63 applied to the Potts model for a fully connected Potts model with random couplings with strictly positive average . For such a system, it is known SherringtonKirkpatrick ; GabayToulouse ; Nishimori that, in the limit , a phase transition separates a (so-called paramagnetic) phase at where the ’s on the average occupy all three states in equal numbers, from a (so-called ferromagnetic) phase at where one state of the ’s dominates over the remaining two. If we define and as the relative numbers of ’s in states and respectively, we can describe the system using the pair . The system in the paramagnetic phase is characterized by . In case of a ferromagnetic phase, three equi-probable pairs with , are possible and the system selects one of them randomly according to the influence of initial conditions and its noisy dynamics. This is the phenomenon of “spontaneous symmetry breaking”, defined as the situation in which the solution selected by the dynamics has a lower symmetry than its equation. The concept of spontaneous symmetry breaking has many important applications in many fields of science Aravind ; Consoli ; Drugowich ; Goldenfeld92 ; Sivardiere1 ; Sivardiere2 ; Weinberg , with deep implications that span the creation of the universe, the fundamental interactions in physics, the emergence of particle masses to the emergence of stock market speculation Sornettespec2000 . When the average coupling strength is equal to the critical value , the system is at its critical point at which its susceptibility diverges for (and grows as a positive power of for finite ). The numerical value of in the limit is a well-defined function of Nishimori .

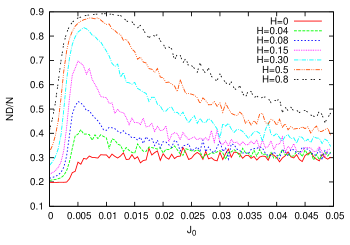

For , we thus expect each ECRG to follow a kind of correlated unbiased random walk for . In contrast, for , the spontaneous symmetry breaking of the average of the ’s translates into a non-zero bias. With probability , this bias is positive, tending to push the credit ratings upwards. With probability , the bias is negative, pushing the firms inexorably towards the default state . And with probability , the bias is neutral, keeping the credit rating in its position. Figure 1 presents the average cumulative number of defaults observed in our simulations over time steps, averaged over 1000 realizations, as a function of for different field amplitudes . For , we observe that the fraction of firms that have defaulted in the time span of time steps jumps from to as passes through a critical value . This is the signature of the bias just mentioned above associated with the spontaneous symmetry breaking occurring above the critical point at .

3.2.2 Effect of the global “panic” field ()

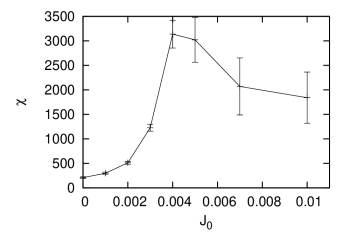

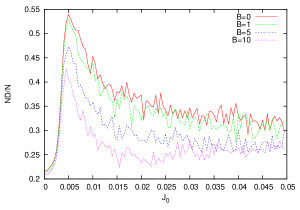

For , the number of defaults develops a maximum for in the vicinity of the critical point and the value of the maximum is higher for higher values of the panic field . This peak is due to the phenomenon mentioned above that the neighborhood of the critical point is associated with an increased susceptibility of the system to external perturbations. In the present context, the susceptibility (or we should rather say the vulnerability to panic) can be defined as

| (5) |

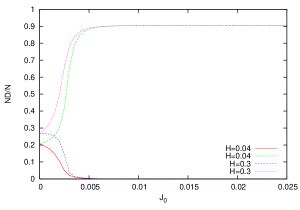

A numerical estimation of the susceptibility for the system of nodes and different is presented in Fig. 2. A maximum of near the critical point is clearly visible. The peak is expected to diverge as the system size goes to infinity.

3.2.3 Critical susceptibility and non-monotonous nonlinear amplification of negative shocks

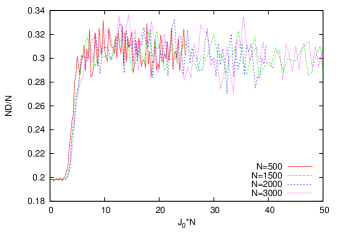

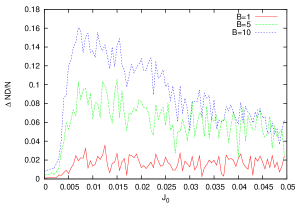

The interplay between the panic field and the collective phenomenon of defaults is well illustrated by comparing Figure 3 and Figure 4. Figure 3 for shows that the number of defaults scaled by the size of the economy is independent of . In other words, for all values of the average coupling strength , the number of defaults is simply proportional to the size of the economy all along the nonlinear path as a function of . This result illustrates that the severity of the crisis which, in an economy where firms are coupled to each other, does not remain localized to a few firms but scales with the size of the economy.

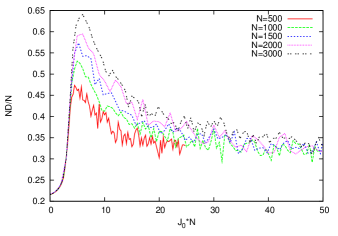

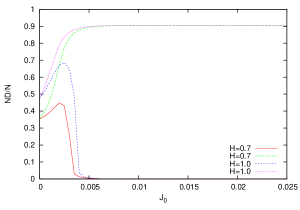

Figure 4 shows that, in the presence of the panic field , the simple scaling of Figure 3 does not hold anymore. It is replaced by a strong nonlinear amplification of the number of defaults with the size of the economy: the scaled variable grows with growing at the peak occurring close at the critical point . Far away from the critical point, one can observe again a good collapse of the curves for different economy sizes. Thus, the nonlinear amplification as a function of system size is specifically associated with the behavior of the susceptibility which tends to diverge at as the system size increases.

Figures 1-4 carry two vivid messages.

-

•

Even in the absence of panic (), as the strength of the interactions between firms increases, represented by a rising , the severity of the crisis quantified by the fraction of firms defaulting on their obligations exhibits an abrupt nonlinear jump around a critical value .

-

•

In the presence of the panic field (), the situation worsens considerably, with nonlinear and non-monotonous responses as a function of the average coupling strength . The observed maximum susceptibility to a panic effect is associated with a very strong dependence on the size of the system: as shown in Figure 4, the larger the number of interacting firms and of coupled financial instruments in the economy, the much larger is the amplitude of the crisis as measured by the fraction of default.

Students of collective phenomena will not be surprised by these strong nonlinearities that emerge endogenously from the interactions between the firms and might even take advantage of the existence of precursors associated with the approach to the critical point (see chapter 10 on “Transitions, bifurcations and precursors” of SornetteCritbook06 ). In other words, while the severity of the crisis is many times amplified in the presence of a panic field in a neighborhood of the critical point, making them akin to so-called predictable “dragon-king” SornetteDragon09 , the good news is that such behavior can be anticipated Sornettepredic2002 ; Scheffer-Nature09 . The analysis presented by Sornette and Woodard SorWood10 supports this claim, based on the realization that the fundamental cause of the unfolding financial and economic crisis stems from the accumulation of five bubbles and their interplay and mutual reinforcement. In this vein, one of us and his group at ETH Zurich has started the “financial bubble experiment” to test systematically and rigorously the hypothesis that financial crises can be diagnosed in advance FCO-FBE . The present model provides a possible supporting mechanism.

4 Sensitivity study of the paths of defaulting economies

The evolution of firms depends on the initial condition of the economy, represented by the set of and values at the initial time. In the simulations whose results have been presented in Figures 1-4, we used initial conditions for which the states and the non-zero rating level are equally populated. Defining and as the probabilities for and respectively at time , this corresponds to .

We now study how the evolution of the economy depends on different initial conditions for and .

4.1 Evolution of the ECRG changes by homogenized equations

First, we study the evolution of the ECRG change via their probabilities. The evolution of the probability of the different states , in absence of default, can be described by the following equations Sieczka

| (6) |

| (7) |

where . Of course, the probability that the ECRG change is at time is simply . These equations (6-7) are obtained by using a representative firm approach, known in mathematics as an homogenization procedure, and in physics as a mean-field approximation.

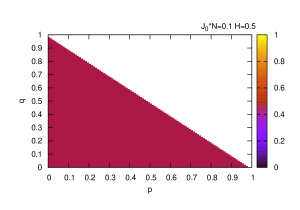

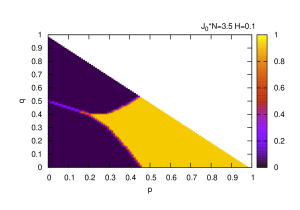

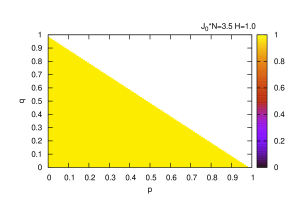

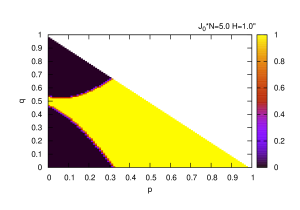

Starting with an initial condition , the equations (6-7) were iterated to obtain an asymptotic value at long times. The results are presented in Fig. 5. The initial state is represented by a point on a plane, while the final state is visualized by a specific color. It can be seen that the effect of initial initial conditions is different for different parameters and .

In a paramagnetic phase (, ), all initial conditions lead to the same final state, which is biased by the field . A ferromagnetic phase (, ) breaks into two final states of a complete ordering which depends on the initial condition. In the illustrated case, the symmetry is broken by the field and, as a consequence, the state is favored. In the ferromagnetic phase with a strong field (, ), the symmetry is completely broken and all initial conditions lead to . For higher interaction strength (, ), the system is back to a two-state competition with state preferred more often, due to the effect of the field. In the cases (, ) and (, ), the bottom dark regions correspond to states ordered along the neutral axis with zero average magnetization. This rating status quo could result from economic stagnation with no firm default but no improvement in credit ratings.

A mean field approach for an infinite range model provides the exact solution. However, applying a mean field approach to our model constitutes an approximation for two reasons. First, we assume in equations (6-7) that the field H is nonzero from the beginning of the iteration which is not true in the simulations where the field appears after the first default happens. Second, the simulations run over a finite time, so that the asymptotic state can only be an approximation. Results of the iteration presented in Fig. 5 play an illustrative role and show areas of initial conditions that lead to common asymptotic solution.

4.2 Sensitivity of defaults on initial conditions

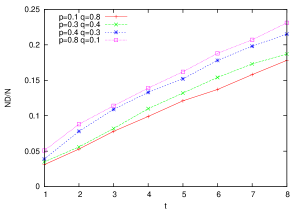

Is the development of a financial crisis through a cascade of default ineluctable? What is the role of the initial conditions and of random shocks during its development? We can address these questions by using our model and study the impact of different values of the probabilities of the initial ECRG changes and for various and .

In the paramagnetic phase (), the initial values have only a small effect on the number of defaults and a small difference between them leads to negligible consequences as shown in Figure 6. This figure presents the evolution of for four different starting points in the paramagnetic phase with zero panic field (. In both cases, the number of defaults grows linearly in time with similar rate.

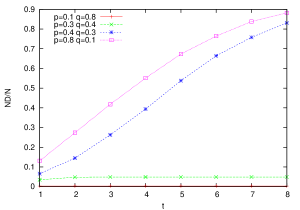

In contrast, for corresponding to the ferromagnetic phase with , initial conditions play a strong role in determining the subsequence evolution. Fig. 7 illustrates the typical situation in which two very different scenarios develop for the cumulative number of defaults for systems starting with different initial conditions. The upper curves in Fig. 7 favors . This slight breaking of symmetry in the initial probability condition is sufficient to accelerate tremendously the rate of default, compared to the situation shown in Figure 6. In the case corresponding to a small bias towards the ECRG change , the cooperative ferromagnetic phase has the effect of actually quenching the crisis, i.e., making it less severe with a rapid saturation to a total number of defaults more than half that obtained for the same initial conditions in the paramagnetic phase shown in Figure 6.

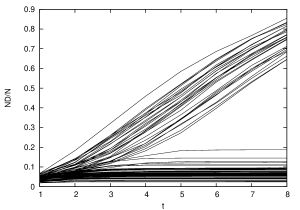

Figures 8 and 9 illustrate further the drastically increased sensitivity to different initial conditions, as the average coupling strength crosses the critical region , in the presence of a non-zero panic field . As shown in these Figures, different starting points may lead to opposite default scenarios, seen as a pair of two branches. As the panic field increases to rather large values, an interesting effect is visualized in Fig. 9: in the absence of bias in the initial conditions (), the number of defaults is maximum close to the critical point while going to zero for large ’s. In contrast, when a bias is present () in favor of , the number of defaults increases rapidly to an almost complete collapse of the economy as the coupling strength increases.

4.3 Direct impact of the phenomenon of “spontaneous symmetry breaking”

These effects described in the previous subsection are in essence all the children of the “spontaneous symmetry breaking” occurring for mentioned in subsection 3.2.1, amplified by two additional symmetry breaking in the initial conditions and in the presence of the panic field. To make the point clearer, Figure 10 shows the time evolution of an ensemble of 100 realizations of an economy with the same parameters , with symmetric initial conditions . We can observe that about 40% of the economies bifurcate to a large number of defaults while the other 60% exhibit a much milder crisis. Nothing but the phenomenon of spontaneous symmetry breaking differentiates these different realizations. The conclusion is that, for systems functioning close to and above a critical point, a large variability can be observed with, under the same conditions, either a very severe or a very mild crisis unfolding. The later would not doubt be hailed as the success of better regulations or better policy or risk management, while this huge difference is inherent to the dynamics of systems driven by collective effects.

The pattern of time evolutions shown in figure 10 can be interpreted from the diagrams of figure 5, specifically the cases (, ) and (, ) in which the dark regions correspond to states ordered along the positive or the neutral axis. In such regimes, the number of up-going trajectories leading to a large occurrence of firm defaults is about 40% of all trajectories. This 40% fraction consists of a fraction of 33% of trajectories associated with the negative ordered phase and of a number of trajectories that run first in the paramagnetic phase until they become ordered in the neutral phase. Since the paramagnetic phase allows stochastic movements of firm rating to , a number of firms are subjected to this effect.

5 Impact of rescue policy

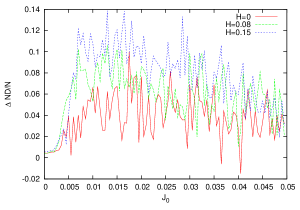

Until now, our model has implemented the negative psychological effect of defaults occurring in the economy via a “panic” field, which tends to enhance the downgrading of firms and the probability of default. We have shown that the negative sentiment, modeled by the panic field which appears when the first default happens, has the effect of destabilizing the economy and of increasing significantly the number of defaults. As discussed in the introduction, the inspiration of our model and subsequent analysis was the occurrence of Lehman Brothers bankruptcy and the controversial decision by the US Treasury and the Federal Reserve to let Lehman Brothers fail. Our model provides a simple playground to test what would be the effect of a policy bailing out defaulting firms in the hope of regaining stability.

We thus implemented a rescue policy in our simulations by resetting the first firms that default when their rating reach with an effective credit rating grade (ECRG) randomly chosen between and and with ECRG changes randomly set between and with the same probabilities. Because the rescue occurs before the information that can spread within the network, it corresponds to a bail-out action just before an agent defaults.

Fig. 11 shows that the bailing out policy can significantly reduce the scale of collective bankruptcies, however it cannot prevent them. Again, the impact of the rescue policy is strongest close to the critical point where is the economy is the most susceptible to shocks, either negative or positive. The impact of the rescue policy is quantified in Figures 12 and 13, which presents the dependence as a function of of the fraction of firms that avoid bankruptcy as a consequence of the policy to bail out the first first defaulting firms. For a fixed moderate panic field , Figure 13 shows that just bailing out one firm reduces by about 2% the relative number of defaulting firms. While seemingly not much, for our economy of 1000 firms, this amounts to save endogenously about 20 firms by the spill-over effect of the collective interactions in the network of firms at the cost of just bailing out one firm. Bailing out the first 10 defaulting firms lead to a maximum salvation of 16% of the firms in the economy (or 160 out of the 1000). While the (gain / cost) ratio ) for is smaller than the (gain / cost) ratio ) for , the effect remains significant.

Figure 13 shows that the impact of the rescue policy is stronger for larger panic fields, as would be hoped for.

6 Conclusions

Johnson SimonJohnson summarizes the three main events that triggered the severe global phase of the crisis as follows: “On the weekend of September 13-14, 2008, the U.S. government declined to bailout Lehman. The firm subsequently failed, i.e., did not open for business on Monday, September 15. Creditors suffered major losses, and these had a particularly negative effect on the markets given that through the end of the previous week the Federal Reserve had been encouraging people to continue to do business with Lehman… On Tuesday, September 16, the government agreed to provide an emergency loan to the major insurance company, AIG. This loan was structured so as to become the company’s most senior debt and, in this fashion, implied losses for AIG’s previously senior creditors; the value of their investments in this AAA bastion of capitalism dropped 40% overnight… By Wednesday, September 17, it was clear that the world’s financial markets - not just the US markets, but particularly US money market funds - were in cardiac arrest. The Secretary of the Treasury immediately approached Congress for an emergency budgetary appropriation of $700bn (about 5% of GDP), to be used to buy up distressed assets and thus relieve pressure on the financial system…”

Inspired by these events, we have developed a simple model of the “Lehman Brothers effect” in which the Lehman default event is quantified as having an almost immediate effect in worsening the credit worthiness of all financial institutions in the economic network. This effect embodies (i) the direct consequences of the Lehman default on its creditors as well as (ii) the psychological impact of the realization that the US Treasury and Federal Reserve was ready to let fail a major financial institution so that no one felt protected anymore and (iii) the valuation effect that the worthiness of financial derivatives was much less than previously estimated, leading to a global realization that the problem was much more severe that imagined before. We have offered a stylized description in which all properties of a given firm can be captured by its effective credit rating. We have specified simple dynamics of co-evolution of the effective credit ratings of coupled firms, that show the existence of a global phase transition around which the susceptibility of the system is strongly enhanced. In this context, we show that bailing out the first few defaulting firms does not solve the problem, but does alleviate considerably the global shock, as measured by the fraction of firms that are not defaulting as a consequence. We quantify a more than ten-fold effect: bailing out the first (respectively the first ten) defaulting firm(s) saves 20 (respectively 160) more firms in an economy of 1000 firms. This amplification effect is the direct consequence of the collective linkage between the firm credit ratings in our economic network which is organized endogenously.

An idea to generalize the model would be to introduce heterogeneity in size of the firms and in their economic connections in order to make them more realistic. That could be done by introducing a different, non symmetric interaction matrix in which one node would have a greater impact on its partners than the opposite. We leave this issue for a further studies.

Acknowledgements

The authors acknowledge helpful discussions and exchanges with H. Gersbach, Y. Malevergne, M. Marsili and R. Woodard. All remaining errors are ours. PS and JAH were supported by European COST Action MP0801 (Physics of Competition and Conflicts) and by the Polish Ministry of Science and Education, Grant No 578/N-COST/2009/0. DS acknowledges financial support from the ETH Competence Center “Coping with Crises in Complex Socio-Economic Systems” (CCSS) through ETH Research Grant CH1-01-08-2 and from ETH Zurich Foundation.

References

- (1) K. Anand, R. Kühn, Physical Review E 75, 016111 (2007)

- (2) P. K. Aravind, American Journal of Physics 55, 437-439 (1987)

- (3) D. Ariely, Predictably Irrational: The Hidden Forces That Shape Our Decisions. (HarperCollins, 2008)

- (4) S. Azizpour, K. Giesecke, Premia for correlated default risks. (http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1126462) (2008)

- (5) S. Battiston, D. Delli Gatti, M. Gallegati, B. Greenwald, J. E. Stiglitz, Journal of Economic Dynamics and Control 31, 2061-2084 (2007)

- (6) L. Brand, R. Bahar, Ratings Performance 2000 (Default, Transition, Recovery, and Spreads). Special Report, Standard & Poor’s, January 2001.

- (7) M. Consoli, P.M. Stevenson, International Journal of Modern Physics A 15, 133-157 (2000)

- (8) D. Delli Gatti, M. Gallegati, B. Greenwald, A. Russo, J. E. Stiglitz, Financially constrained fluctuations in an evolving network economy, NBER Working Paper No. 14112 (http://www.nber.org/papers/w14112.pdf) (2008)

- (9) J. R. Drugowich de Felicio, O. Hipolito, American Journal of Physics 53, 690-693 (1985)

- (10) L. Eisenberg, T. H. Noe, Management Science 47, 236-249 (2001)

- (11) M. Gabay, and G. Toulouse, Phys. Rev. Lett. 47, 201-204 (1981)

- (12) K. Giesecke, Journal of Banking & Finance 28, 1521-1545 (2004)

- (13) R. J. Glauber, Journal of Mathematical Physics 4, 294-307 (1963)

- (14) N. Goldenfeld, Lectures on Phase Transitions and the Renormalization Group, Advanced Book Program, (Addison-Wesley, Reading, MA 1992)

- (15) I., Goldstein, The Economic Journal 115, 368-390 (2005).

- (16) J. P. L. Hatchett, R. Kühn, Credit contagion and credit risk. (http://arXiv.org/abs/physics/0609164 (2006)

- (17) Y. Ikeda, Y. Fujiwara, W. Souma, H. Aoyama, H. Iyetomi, Agent Simulation of Chain Bankruptcy. (http://arxiv.org/abs/0709.4355) (2007)

- (18) S. Johnson, The Economic Crisis and the Crisis in Economics user-pic. (http://tpmcafe.talkingpointsmemo.com/2009/01/06/the_economic_crisis_and_the_crisis_in_economics/) (2009)

- (19) A. Khandani, A. W. Lo, What Happened to the Quants in August 2007? (http://ssrn.com/abstract=1015987) (2008)

- (20) P. Krugman, The Return of Depression Economics and the Crisis of 2008, (Allen Lane 2008)

- (21) R. Kühn and P. Neu P., J. Phys. A: Math. Theor. 41, 324015 (2008).

- (22) A. W. Lo, Hedge Funds: An Analytic Perspective, (Princeton University Press, Princeton, New Jersay 2008)

- (23) J. Lorenz, S. Battiston, F. Schweitzer, European Physical Journal B 71, 441-460 (2009).

- (24) D. McFadden, “Conditional Logit Analysis and Qualitative Choice behavior.” In Paul Zarembka (ed.), Frontiers in Econometrics, (New York: Academic Press 1974)

- (25) D. McFadden,,“Modelling the Choice of Residential Location,” in A. Karlqvist et al. (eds.), Spatial Interaction Theory and Planning Models. (New York: North-Holland Publishing Co. 1978)

- (26) J. Molins, and R. Vives, Long range Ising model for credit risk modeling. AIP Conference Proceedings (Institute of Physics), 779, 156-161. (http://arxiv.org/abs/cond-mat/0401378) (2005)

- (27) P. Neu, R. Kühn, Physica A 342, 639-655 (2004)

- (28) H. Nishimori, Statistical Physics of Spin Glasses and Information Processing. (Oxford University Press, New York 2001)

- (29) P. Ormerod, R. Colbaugh, Cascades of Failure and Extinction in Evolving Complex Systems, (http://arxiv.org/abs/nlin/0606014) (2006)

- (30) A. Sakata, M. Hisakado, S. Mori, Infectious Default Model with Recovery and Continuous Limit. (http://arXiv.org/abs/physics/0610275) (2006)

- (31) R. Schafer, M. Sjolin, A. Sundin, M. Wolanski, T. Guhr, Physica A 383, 533-569 (2007).

- (32) M. Scheffer, J. Bascompte, W.A. Brock, V. Brovkin, S.R. Carpenter, V. Dakos, H. Held, E. H. van Nes, M. Rietkerk, G. Sugihara, Nature 461, 53-59 (2009).

- (33) F. Schweitzer, G. Fagiolo, D. Sornette, F. Vega-Redondo, A. Vespignani, D. R. White, Science 325, 422-424 (2009).

- (34) F. Schweitzer, G. Fagiolo, D. Sornette, F. Vega-Redondo, D.R. White, Advances in Complex Systems 12, 407-422 (2009).

- (35) D. Sherrington and S. Kirkpatrick, Phys. Rev. Lett. 35, 1792-1796 (1975).

- (36) J. Sivardiere, American Journal of Physics 51, 1016-1018 (1983).

- (37) J. Sivardiere, American Journal of Physics 65, 567-568 (1997).

- (38) P. Sieczka, J. A. Hołyst, European Physical Journal B 71, 461-465 (2009).

- (39) D. Sornette, Physica A 284, 355-375 (2000)

- (40) D. Sornette, Predictability of catastrophic events: material rupture, earthquakes, turbulence, financial crashes and human birth, Proceedings of the National Academy of Sciences USA, 99 SUPP1, 2522-2529 (2002)

- (41) D. Sornette, Critical Phenomena in Natural Sciences, (Chaos, Fractals, Self-organization and Disorder: Concepts and Tools), 2nd ed., (Springer Series in Synergetics, Heidelberg 2006)

- (42) D. Sornette, 2009. International Journal of Terraspace Science and Engineering 2(1), (2009) 1-18. (http://ssrn.com/abstract=1470006).

- (43) D. Sornette, M. Fedorovsky, S. Riemann, H. Woodard, R. Woodard, W.-X. Zhou, (The Financial Crisis Observatory), 2009. The Financial Bubble Experiment: advanced diagnostics and forecasts of bubble terminations, (http://arxiv.org/abs/0911.0454).

- (44) D. Sornette, R. Woodard, Financial Bubbles, Real Estate bubbles, Derivative Bubbles, and the Financial and Economic Crisis. to appear in the Proceedings of APFA7 (Applications of Physics in Financial Analysis), “New Approaches to the Analysis of Large-Scale Business and Economic Data,” Misako Takayasu, Tsutomu Watanabe and Hideki Takayasu, eds., Springer (http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1407608) (2010)

- (45) S. Weinberg, The Quantum Theory of Fields, (Cambridge University Press, Cambridge 1995-1996)