Quantum Model of Bertrand Duopoly

Abstract

We present the quantum model of Bertrand duopoly and study the entanglement

behavior on the profit functions of the firms. Using the concept of optimal

response of each firm to the price of the opponent, we found only one Nash

equilibirum point for maximally entangled initial state. The very presence

of quantum entanglement in the initial state gives payoffs higher to the

firms than the classical payoffs at the Nash equilibrium. As a result the

dilemma like situation in the classical game is resolved.

PACS: 03.65.Ta; 03.65.-w; 03.67.Lx

Keywords: Quantum Bertrand duopoly; profit functions, Nash equilibria.

In economics, oligopoly refers to a market condition in which sellers are so few that action of each seller has a measurable impact on the price and other market factors [1]. If the number of firms competing on a commodity in the market is just two, the oligopoly is termed as duopoly. The competitive behavior of firms in oligopoly makes it suitable to be analyzed by using the techniques of game theory. Cournot and Bertrand models are the two oldest and famous oligopoly models [2, 3]. In Cournot model of oligopoly firms put certain amount of homogeneous product simultaneously in the market and each firm tries to maximize its payoff by assuming that the opponent firms will keep their outputs constant. Later on Stackelberg introduced a modified form of Cournot oligopoly in which the oligopolistic firms supply their products in the market one after the other instead of their simultaneous moves. In Stackelberg duopoly the firm that moves first is called leader and the other firm is the follower [4]. In Bertrand model the oligopolistic firms compete on price of the commodity, that is, each firm tries to maximize its payoff by assuming that the opponent firms will not change the prices of their products. The output and price are related by the demand curve so the firms choose one of them to compete on leaving the other free. For a homogeneous product, if firms choose to compete on price rather than output, the firms reach a state of Nash equilibrium at which they charge a price equal to marginal cost. This result is usually termed as Bertrand paradox, because practically it takes many firms to ensure prices equal to marginal cost. One way to avoid this situation is to allow the firms to sell differentiated products [1].

For the last one decade quantum game theorists are attempting to study classical games in the domain of quantum mechanics [-]. Various quantum protocols have been introduced in this regard and interesting results have been obtained [15-25]. The first quantization scheme was presented by Meyer [15] in which he quantized a simple penny flip game and showed that a quantum player can always win against a classical player by utilizing quantum superposition.

In this letter, we extend the classical Bertrand duopoly with differentiated products to quantum domain by using the quantization scheme proposed by Marinatto and Weber [17]. Our results show that the classical game becomes a subgame of the quantum version. We found that entanglement in the initial state of the game makes the players better off. Before presenting the calculation of quantization scheme, we first review the classical model of the game.

Consider two firms A and B producing their products at a constant marginal cost such that , where is a constant. Let and be the prices chosen by each firm for their products, respectively. The quantities and that each firm sells is given by the following key assumption of the classical Bertrand duopoly model

| (1) |

where the parameter shows the amount of one firm’s product substituted for the other firm’s product. It can be seen from Eq. (1) that more quantity of the product is sold by the firm which has low price compare to the price chosen by his opponent. The profit function of the two firms are given by

| (2) |

In Bertrand duopoly the firms are allowed to change the quantity of their product to be put in the market and compete only in price. A firm changes the price of its product by assuming that the opponent will keep its price constant. Suppose that firm B has chosen as the price of his product, the optimal response of firm A to is obtained by maximizing its profit function with respect to its own product’s price, that is, , this leads to

| (3) |

Firm B response to a fixed price of firm A is obtained in a similar way and is given by

| (4) |

Solution of Eqs.(3 and 4) lead to the following optimal price level that defines the Nash equilibrium of the game

| (5) |

The profit functions of the firms at the Nash equilibrium become

| (6) |

From Eq. (6), we see that both firms can be made better off if they choose higher prices, that is, the Nash equilibrium is Pareto inefficient.

To quantize the game, we consider that the game space of each firm is a two dimensional Hilbert space of basis vector and , that is, the game consists of two qubits, one for each firm. The composite Hilbert space of the game is a four dimensional space which is formed as a tensor product of the individual Hilbert spaces of the firms, that is, , where and are the Hilbert spaces of firms A and B, respectively. To manipulate their respective qubits each firm can have only two strategies and . Where is the identity operator and and is the inversion operator also called Pauli spin flip operator. If and stand for the probabilities of and that firm A applies and , , are the probabilities that firm B applies, then the final state of the game is given by [17]

| (7) | |||||

In Eq. (7) is the initial density matrix with initial state , which is given by

| (8) |

where and represents the degree of entanglement of the initial state. In Eq. (8) the first qubit corresponds to firm A and the second qubit corresponds to firm B. The moves (prices) of the firms and the probabilities , of using the operators can be related as follows,

| (9) |

where the prices and and the probabilities , . By using Eqs. (7 - 9), the nonzero elements of the final density matrix are obtained as

| (10) |

The payoffs of the firms can be found by the following trace operations

| (11) |

where and are payoffs operators of the firms, which we define these as

| (12) |

where , and . By using Eqs. (10 - 12), the payoffs of the firms are obtained as

One can easily see from Eq. (LABEL:E13) that the classical payoffs can be reproduced by setting in Eq. (LABEL:E13).

We proceed similar to the classical Bertrand duopoly to find the response of each firm to the price chosen by the opponent firm. For firm B’s price , the optimal response of firm A is obtained by maximizing its own payoff (Eq. (LABEL:E13)) with respect to . Similarly, the reaction function of firm B to a known is obtained. These reaction functions can be written as

The results of Eq. (LABEL:E14) reduce to the classical results given in Eqs. (3 and 4) for the initially unentangled state, that leads to the classical Nash equilibrium. This shows that the classical game is a subgame of the quantum game.

Now, we discuss the behavior of entanglement in the initial state on the game dynamics. It can be seen from Eq. (LABEL:E14) that the optimal responses of the firms to a fixed price of the opponent firm, for a maximally entangled state, are given by

| (15) |

Solving these equations, we can obtain the optimal price levels and the corresponding payoffs of each firm. In this case the following four points are obtained

| (16) |

where the numbers in the parentheses correspond to the respective points (the symbols correspond to points and respectively). To verify which point (points) defines the Nash equilibrium of the game, we use the second partial derivative condition. That is, for Nash equilibrium, the strategy (point) must be the global maximum of the payoff function, that is, and the payoff function at the point must be higher than the payoff function at the boundary points. It can easily be verified that this condition is satisfied only at point . Hence point defines the Nash equilibrium of the game. The payoffs of the firms at the Nash equilibrium become

| (17) | |||||

The new parameters introduced in Eqs. (16 and 17) are defined as , . The payoffs of the firms at the Nash equilibrium must be real and positive for the entire range of substitution parameter . This condition for marginal cost is satisfied when . The firms’ payoffs at the other three points become

| (18) |

where .

|

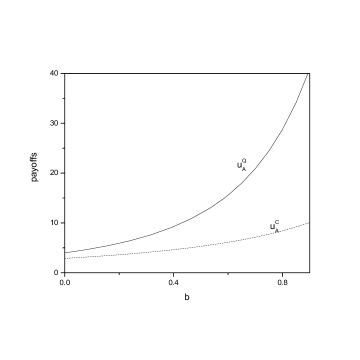

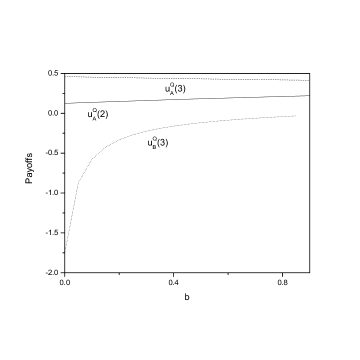

We present a quantization scheme for the Bertrand duopoly with differentiated products. To analyze the effect of quantum entanglement on the game dynamics, we plot the payoffs of the firms at the classical and quantum Nash equilibria against the substitution parameter in figure (). The values of parameters and are chosen to be and , respectively. The solid line () represents quantum mechanical payoffs and the dotted line () represents the classical payoffs of the firms. It is clear from the figure that quantum payoffs of the firms are higher than the classical payoffs for the entire range of substitution parameter . The maximum entanglement in the initial state of the game makes the firms better off. In figure (2), we plot the payoffs of the firms (Eq. 18) against the substitution parameter at the other three points which are not the Nash equilibria.

|

In conclusion, we have used the Marinatto and Weber quantization scheme to find the quantum version of Bertrand duopoly with differentiated products. We have studied the entanglement behavior on the payoffs of the firms for a maximally entangled initial state. We found that for large values of substitution parameter both firms can achieve significantly higher payoffs as compared to the classical payoffs. Furthermore, for maximally entangled state the quantum payoffs are higher than the classical payoffs for the entire range of substitution parameter and is the best situation for both firms. Thus, the dilemma-like situation in the classical Bertrand duopoly game is resolved.

Acknowledgment

One of the authors (Salman Khan) is thankful to World Federation of

Scientists for partially supporting this work under the National Scholarship

Program for Pakistan

References

- [1] Gibbons R Game Theory for applied Economists Princeton Univ. Press Princeton, NJ, 1992: Bierman H.S, Fernandez L Game Theory with Economic Applications, 2nd Edition, Addison - Wesley, Reading MA 1998

- [2] Cournot A 1897 Researches into the Mathematical Principles of the Theory of Wealth, Macmillan Co., New York

- [3] Bertrand J, Savants J 1883 67 499

- [4] Stackelberg H von 1934 Marktform und Gleichgewicht (Julius Springer Vienna)

- [5] Flitney A.P, Ng J, Abbott D 2002 Physica A 314 35, doi:10.1016/S0378-4371(02)01084-1

- [6] Ramzan M et al 2008 J. Phys. A Math. Theor. 41 055307, doi:10.1088/1751-8113/41/5/055307

- [7] D’ Ariano G M 2002 Quantum Information and Computation 2 355

- [8] Flitney A.P, Abbott D 2002 Phys. Rev. 65 062318, doi:10.1103/PhysRevA.65.062318

- [9] Iqbal A, Cheo T, Abbott D 2008 Phys. Lett. A 372 6564, doi:10.1016/j.physleta.2008.09.026

- [10] Zhu X, Kaung L M 2008 Commun. Theor. Phys (china) 49 111

- [11] Ramzan M and Khan M K 2008 J. Phys. A: Math. Theor. 41 435302, doi:10.1088/1751-8113/41/43/435302

- [12] Ramzan M, Khan M.K 2009 J. Phys. A, Math. Theor. 42 025301, doi:10.1088/1751-8113/42/2/025301

- [13] Zhu X, Kaung L M 2007 J. Phys. A 40 7729, doi:10.1088/1751-8113/40/27/021

- [14] Salman Khan et al 2010 Int. J. Theor. Phys.49 31, doi:10.1007/s10773-009-0175-y

- [15] Meyer D A 1999 Phys. Rev. Lett. 82 1052, doi:10.1103/PhysRevLett.82.1052

- [16] Eisert J et al 1999 Phys. Rev. Lett. 83 3077, doi:10.1103/PhysRevLett.83.3077

- [17] Marinatto L and Weber T 2000 Phys. Lett. A 272 291, doi:10.1016/S0375-9601(00)00441-2

- [18] Li H, Du J, Massar S 2002 Phys. Lett. A 306 73, doi:10.1016/S0375-9601(02)01628-6

- [19] Lo C.F, Kiang D 2004 Phys. Lett. A 321 94, doi:10.1016/j.physleta.2003.12.013

- [20] Iqbal A and Abbott D 2009 arXiv:quant-ph/0909.3369

- [21] Iqbal A and Toor A H 2002 Phys. Rev. A 65 052328, doi:10.1103/PhysRevA.65.052328

- [22] Lo C.F, Kiang D 2003 Phys. Lett. 318 333, doi:10.1016/j.physleta.2003.09.047

- [23] Benjamin S.C, Hayden P.M 2001 Phy. Rev. A 64 030301, doi:10.1103/PhysRevA.64.030301

- [24] Lo C.F, Kiang D 2005 Phys. Lett. A 346 65, doi:10.1016/j.physleta.2005.07.055

-

[25]

Gan Qin et al 2005 J. Phys. A: Math. Gen. 38 4247,

doi:10.1088/0305-4470/38/19/013