A vastly extended and updated version of this paper will appear as a book:

Credit Models and the Crisis: A journey into CDOs, Copulas,

Correlations and Dynamic Models, Wiley, Chichester, 2010

—

Credit Models and the Crisis, or:

How I learned to stop worrying and love the CDOs

Abstract

We follow a long path for Credit Derivatives and Collateralized Debt Obligations (CDOs) in particular, from the introduction of the Gaussian copula model and the related implied correlations to the introduction of arbitrage-free dynamic loss models capable of calibrating all the tranches for all the maturities at the same time. En passant, we also illustrate the implied copula, a method that can consistently account for CDOs with different attachment and detachment points but not for different maturities. The discussion is abundantly supported by market examples through history. The dangers and critics we present to the use of the Gaussian copula and of implied correlation had all been published by us, among others, in 2006, showing that the quantitative community was aware of the model limitations before the crisis. We also explain why the Gaussian copula model is still used in its base correlation formulation, although under some possible extensions such as random recovery. Overall we conclude that the modeling effort in this area of the derivatives market is unfinished, partly for the lack of an operationally attractive single-name consistent dynamic loss model, and partly because of the diminished investment in this research area.

JEL classification code: C15, C31, C46, C61, G12, G13.

AMS classification codes: 60J75, 62E20, 91B30, 91B70, 91B82

Keywords: Credit Crisis, Credit Derivatives, Gaussian Copula Model, Implied Correlation, Base Correlation, Compound Correlation, Implied Copula, Dynamic Loss Model, GPL Model, Arbitrage Free Models, Collateralized Debt Obligations, DJi-Traxx and CDX Tranches, CDO Tranche Calibration.

Preface

Part 1: Randomized by foolishness

This is a paper that has been written very rapidly in order to respond to a perceived need of clarity in the quantitative world. The paper subtitle, “How I learned to stop worrying and love the CDOs” is obviously ironic in referring to the hysteria that has often characterized accounts of modeling and mathematical finance in part of the press and the media, and the demonization of part of the market products related to the crisis, such as CDOs and derivatives more generally. Let us be clear and avoid any misunderstanding: The crisis is very real, it has caused suffering to many individuals, families and companies. However, it does not help looking for a scapegoat without looking at the whole picture with a critical eye. Accounts that try and convince the public that the whole crisis is due mainly to modeling and to sophisticated and obscure products being traded are necessarily partial, and to partly righting this perceptive bias this paper is devoted.

Indeed, the public opinion has been bombarded with so many cliches on derivatives, modeling and quantitative analysis that we feel a paper offering a little clarity is needed. And while we are aware that this sounds a little Don Quixotesque, we hope this paper will help changing the situation. In trying to do so, we need to balance carefully the perspectives of different readerships. We would like our paper to be attractive to a relatively general industry and academic public without disappointing the scientific and technically minded specialists, and at the same time we do not want our paper to be a best-seller type of publication full of bashing and negatively provocative ideas and very little actual technical content. All of this while keeping windmills at large111The Ingenious Hidalgo Don Quixote of La Mancha, 1605 and 1615.. Hence we will be walking the razor’s hedge here, in trying to maintain the balance between a popular account and scientific discourse.

We are not alone in our attempt to bring clarity222See primarily Shreve, S. (2008), Don’t Blame the Quants, Forbes Commentary, but also, for example, Donnelly, C., and Embrechts, P. (2009), The devil is in the tails: actuarial mathematics and the subprime mortgage crisis, accepted for publication in the ASTIN Bulletin. Giorgio Szego (2009), the Crash Sonata in D Major (to appear in the Journal of Risk Management in Financial Institutions), gives a much broader overview of the crisis with some critical insight that is helpful in clarifying the more common misconceptions. This paper however does so in an extensive technical way, showing past and present research that is quite relevant in disproving a number of mis-conceptions on the role of mathematics and quantitative analysis in relation with the crisis. This paper takes an extensive technical path, starting with static copulas and ending up with dynamic loss models. Even though our paper is short, we follow a long path for Credit Derivatives and multi-name credit derivatives in particular, focusing on Collateralized Debt Obligations (CDOs). What are CDOs? To describe the simplest possible CDO, say a synthetic CDO on the corporate market, we can proceed as follows.

We are given a portfolio of names, say 125 names for example. The names may default, generating losses to investors exposed to those names. In a CDO tranche there are two parties, a protection buyer and a protection seller. A tranche is a portion of the loss of the portfolio between two percentages. For example, the 3-6% tranche focuses on the losses between 3% (attachment point) and 6% (detachment point). Roughly speaking, the protection seller agrees to pay to the buyer all notional default losses (minus the recoveries) in the portfolio whenever they occur due to one or more defaults of the entities, within 3% and 6% of the total pool loss. In exchange for this, the buyer pays the seller a periodic fee on the notional given by the portion of the tranche that is still “alive” in each relevant period.

In a sense, CDOs look like contracts selling (or buying) insurance on portions of the loss of a portfolio. The valuation problem is trying and determining the fair price of this insurance.

The crucial observation here is that “tranching” is a non-linear operation. When computing the price (mark to market) of a tranche at a point in time, one has to take the expectation of the future tranche losses under the pricing measure. Since the tranche is a nonlinear function of the loss, the expectation will depend on all moments of the loss and not just on the expected loss. If we look at the single names in the portfolio, the loss distribution of the portfolio is characterized by the marginal distributions of the single names defaults and by the dependency among different names’ defaults. Dependency is commonly called, with an abuse of language, “correlation”. This is an abuse of language because correlation is a complete description of dependence for jointly Gaussian random variables, but more generally it is not. The complete description is either the whole multivariate distribution or the so-called “copula function”, that is the multivariate distribution once the marginal distributions have been standardized to uniform distributions.

The dependence of the tranche on “correlation” is crucial. What the market does is assuming a Gaussian Copula connecting the defaults of the 125 names. This copula is parametrized by a matrix with 7750 entries of pairwise correlation parameters. However, when looking at a tranche these 7750 parameters are assumed to be all equal to each other. So one has a unique parameter. This is such a drastic simplification that we need to make sure it is noticed:

Then one chooses the tranches that are liquid on the market for standardized portfolios, for which the market price is known as these tranches are quoted. The unique correlation parameter is then reverse-engineered to reproduce the price of the liquid tranche under examination. This is called implied correlation, and once obtained it is used to value related products. The problem is that whenever the tranche is changed, this implied correlation changes as well. Therefore, if at a given time the 3-6% tranche for a five year maturity has a given implied correlation, the 6-9% tranche for the same maturity will have a different one. It follows that the two tranches on the same pool are priced with two models having different and inconsistent loss distributions, corresponding to the two different correlation values that have been implied.

This may sound negative, but as a matter of fact the situation is even worse. We will explain in detail that there are two possible implied correlation paradigms: compound correlation and base correlation. The second one is the one that is prevailing in the market. However, base correlation is inconsistent even at single tranche level, in that it prices the 3-6% tranche by decomposing it into the 0-3% tranche and 0-6% tranche and using two different correlations (and hence distributions) for those. Therefore base correlation is inconsistent already at single tranche level. And this inconsistency shows up occasionally in negative losses (i.e. in defaulted names resurrecting).

This is admittedly enough to spark a debate. Even before modeling enters the picture, some famous market protagonists have labeled the objects of modeling, i.e. derivatives, as responsible for a lot of troubles. Warren Buffett, in a very interesting 2003 report wrote: “[…] Charlie and I are of one mind in how we feel about derivatives and the trading activities that go with them: We view them as time bombs, both for the parties that deal in them and the economic system. […] In our view […] derivatives are financial weapons of mass destruction, carrying dangers that, while now latent, are potentially lethal. […] The range of derivatives contracts is limited only by the imagination of man (or sometimes, so it seems, madmen).”333February, 21 2003, “Berkshire Hathaway Inc. Annual Report 2002”,

www.berkshirehathaway.com/2002ar/2002ar.pdf.

While when hearing about products such as Constant Proportion Debt Obligations (CPDOs) or CDO squared one may sympathize with Mr. Buffett, this overgeneralization might be a little excessive. Derivatives, when used properly, can be quite useful. For example, swap contracts on several asset classes (interest rates, foreign exchange, oil and other commodities) and related options allow entities to trade risks and buy protection against adverse market moves. Without derivatives, companies could not protect themselves against adverse future movements of the prices of oil, exchange rates, interest rates etc. This is not to say that derivatives cannot be abused. They certainly can, and we invite the interested readers to reason on the case of CPDOs444See for example Torresetti and Pallavicini (2007), “Stressing Rating Criteria Allowing for Default Clustering: the CPDO case“, and the Fitch Ratings report “First Generation CPDO: Case Study on Performance and Ratings”, published before the crisis in April 2007, stating “[…] Fitch is of the opinion that the past 10 years by no means marked a high investment grade stress in the range of ’AAA’ or ’AA’.”

as an example, and to read the whole report by Mr Buffett.

When moving beyond the products and entering the modeling issues, one may still find popular accounts resorting to quite colorful expressions such as “the formula that killed Wall Street”. Indeed, if one looks at popular accounts such as Salmon (2009)555Recipe for disaster: the Formula that killed Wall Street. Wired Magazine, 17.03., or Jones (2009)666Jones, S. (2009). Of couples and copulas: the formula that felled Wall St. April 24 2009, Financial Times. just to make two examples, one may end up with the impression that the quantitative finance (“quant”) community has been incredibly naive in accepting the Gaussian Copula and implied correlation without questioning it, possibly leading to what Mr Buffet calls “mark to myth” in his above–mentioned report, especially when applying the calibrated correlation to other non-quoted “bespoke tranches”. In fact both articles have been written on the Gaussian copula, a static model that is little more than a static multivariate distribution which is used in credit derivatives (and in particular CDOs) valuation and risk management. Can this simple static model have fooled everyone in believing it was an accurate representation of a quite dynamic reality, and further cause the downfall of Wall Street banks? While Salmon (2009) correctly reports that some of the deficiencies of the model have been known for a while, Jones (2009) in the Financial Times wonders why no-one seemed to have noticed the model’s weaknesses. The crisis is considered to have been heavily affected by mathematical models, with the accent on “mathematical”.

This is in line with more general criticism of anything quantitative appearing in the news. As an example, the news article “McCormick Bad Dollars Derive From Deficits Model Beating Quants”,777By Oliver Biggadike, November, 24 2009, Bloomberg. more focused on the currency markets, informs us that “[…] focus on the economic reasons for currency moves is gaining more traction after years when traders and investors relied on mathematical models of quantitative analysis.” Then it continues with “These tools worked during times of global growth and declining volatility earlier this decade, yet failed to signal danger before the financial crisis sparked the biggest currency swings in more than 15 years. McCormick, using macroeconomic and quantitative analyses, detected growing stresses in the global economy before the meltdown.” The reader, by looking at this, may understand that on one side “mathematical models of quantitative analysis” (a sentence that sounds quite redundant) fail in times of crises, whereas “macroeconomic and quantitative analyses” helped predicting some aspects of the crisis. One is left to wonder what is the different use of “quantitative” between “mathematical models of quantitative analysis” and “macroeconomic and quantitative analyses”. It is as though mathematics had all of a sudden become a bad word. Of course the article aims at saying that macroeconomic analysis and fundamentals are of increasing importance and should be taken more into account, although in our opinion it does not distinguish clearly valuation from prediction, but some of the sentences used to highlight this idea are quite symptomatic of the attitude we described above towards modeling and mathematics.

Another article that brings mathematics and mathematicians (provided that is what one means by “math wizards”) into the picture for the blaming is Lohr (2009), in “Wall Street’s Math Wizards Forgot a Few Variables”, appeared in the New York Times of September 12. Also, Turner888Turner, J.A. (2009). The Turner Review. March 2009. Financial Services Authority, UK.

www.fsa.gov.uk/pubs/other/turner_review.pdf. (2009) has a section entitled “Misplaced reliance on sophisticated maths”.

This overall hostility and blaming attitude towards mathematics and mathematicians, whether in the industry or in academia, is the reason why we feel it is important to point out the following: the notion that even more mathematically oriented quants have not been aware of the Gaussian Copula model limitations is simply false, as we are going to show, and you may quote us on this. The quant and academic communities have produced and witnessed a large body of research questioning the copula assumption. This is well documented: there is even a book999Lipton, A. and Rennie, A. (Editors), Credit Correlation - Life After Copulas, World Scientific, 2007. based on a one-day conference hosted by Merrill Lynch in London in 2006, well before the crisis, and called “Credit Correlation: Life after Copulas”. This conference had been organized by practitioners. The “Life after Copulas” book contains several attempts to go beyond the Gaussian Copula and implied correlation, most of which come from practitioners (and a few by academics). But that book is only a tip of the iceberg. There are several publications that appeared pre-crisis and that questioned the Gaussian Copula and implied correlation. For example, we warned against the dangers implicit in the use of implied correlation in our report “Implied Correlation: A paradigm to be handled with care”, that we posted in SSRN in 2006, again well before the crisis.

Still, it seems that this is little appreciated by some market participants, commentators, journalists, critics, politicians, and academics. There are still a number of people out there who think that a formula killed Wall Street.

This paper brings a little clarity by telling a true story of pre-crisis warnings and also of pre-crisis attempts to remedy the drawbacks of implied correlation. We do not document the whole body of research that has addressed the limits of base correlation and of the Gaussian Copula, but rather take a particular path inside this body, based on our past research, that we also update to see what our models tell us in-crisis.

To put our paper in a nutshell, we can say that it starts from the payoffs of CDOs, explaining how to write them and how they work. We then move to the introduction of the inconsistent Gaussian Copula model and the related implied correlations, both compound and base, moving then to the GPL model: an arbitrage-free dynamic loss model capable of consistently calibrating all the tranches across attachments and detachments for all the maturities at the same time. En passant, we also illustrate the Implied Copula, a method that can consistently account for CDOs with different attachment and detachment points but not for different maturities, and the Expected Tranche Loss (ETL) surface, a model independent approach to CDO prices interpolation.

We will see that, already pre-crisis, both the Implied Copula and the dynamic loss model imply modes far down the right tail of the loss distribution. This means that there are default probability clusters corresponding to joint default of a large number of entities (sectors) of the economy.

The discussion is abundantly supported by market examples through history. We cannot stress enough that the dangers and critics we present to the use of the Gaussian Copula and of implied correlation, and the modes in the tail of the loss distribution obtained with consistent models, had all been published by us, among others, in 2006, well before the crisis.

Despite these warnings, the Gaussian Copula model is still used in its base correlation formulation, although under some possible extensions such as random recovery. The reasons for this are complex. First the difficulty of all the loss models, improving the consistency issues, in accounting for single name data and to allow for single name sensitivities. This is due to the fact that if we model the loss of the pool directly as an aggregate object, without taking into account single defaults, then the model sensitivities to single name credit information are not in the picture. In other terms, while the aggregate loss is modeled so as to calibrate satisfactorily indices and tranches, the model does not see the single name defaults but just the loss dynamics as an aggregate object. Therefore partial hedges with respect to single names are not possible. As these issues are crucial in many situations, the market practice remains with base correlation. Furthermore, even the few models achieving single name consistency have not been developed and tested enough to become operational on a trading floor or in a large risk management platform. Indeed, a fully operational model with realistic run times and numerical stability across a large range of possible market inputs would be more than a prototype with some satisfactory properties that has been run in some “off-line” studies. Also, when one model has been coded in the libraries of a financial institution, changing the model implies a long path involving a number of issues that have little to do with modeling and more to do with IT problems, integration with other systems, and the likes. Therefore, unless a new model appears to be really promising and extremely convincing in all its aspects, there is reluctance in adopting it on the trading floor or on risk management systems.

Overall we conclude that the modeling effort in this area of the derivatives market is unfinished, partly for the lack of an operationally attractive single-name consistent dynamic loss model, and partly because of the diminished investment in this research area, but the fact that the modeling effort is unfinished does not mean that the quant community has been unaware of model limitations, as we abundantly document, and, although our narrative ends with an open finale, we still think it is an entertaining true story.

Part 2: How I learned to stop worrying and love the CDOs

We cannot close this preface without going back to the large picture, and ask the more general question: is the crisis due to poor modeling?

As we have seen, the market has been using simplistic approaches for credit derivatives, but it has also been trying to move beyond those. However, we should also mention that CDOs are divided into two categories: Cash and Synthetics. Cash CDOs involve hundreds or even thousands of names and have complex path-dependent payouts (“waterfalls”). Even so, Cash CDOs are typically valued by resorting to single homogeneous default-rate scenarios or very primitive assumptions, and very little research and literature is available on them. Hence these are complex products with sophisticated and path-dependent payouts that are often valued with extremely simplistic models. Synthetic CDOs are the ones we described in this preface and that will be addressed in this paper. They have more simple and standardized payouts than the cash CDOs but are typically valued with more sophisticated models, given the larger standardization and the ease in finding market quotes for their prices. Synthetic CDOs on corporates are epitomized by the quoted tranches of the standard pools DJ-iTraxx (Europe) and CDX (USA). However, CDOs, especially Cash, are available on other asset classes, such as loans (CLO), residential mortgage portfolios (RMBS), commercial mortgages portfolios (CMBS), and on and on. For many of these CDOs, and especially RMBS, quite related to the asset class that triggered the crisis, the problem is in the data rather than in the models. Bespoke corporate pools have no data from which to infer default “correlation” and dubious mapping methods are used. At times data for valuation in mortgages CDOs (RMBS and CDO of RMBS)

are dubious and can be distorted by fraud101010See for example the FBI Mortgage fraud report, 2007,

www.fbi.gov/publications/fraud/mortgagefraud07.htm..

At times it is not even clear what is in the portfolio: the authors have visioned offering circulars of a RMBS on a huge portfolio of residential mortgages where more than the of properties in the portfolio were declared to be of unknown type. What inputs can we give to the models if we do not even know the kind of residential property that functions as underlying of the derivative?

All this is before modeling. Models obey a simple rule that is popularly summarized by the acronym GIGO (Garbage In Garbage Out). As Charles Babbage (1791- 1871) famously put it:

On two occasions I have been asked [by members of Parliament], “Pray, Mr. Babbage, if you put into the machine wrong figures, will the right answers come out?” I am not able rightly to apprehend the kind of confusion of ideas that could provoke such a question.

So, in the end, is the crisis due to models inadequacy? Is the crisis due to quantitative analysts and academics pride and unawareness of models limitations?

We show in this paper that quants have been aware of the limitations and of extreme risks before the crisis. Lack of data or fraud-corrupted data, the fragility in the “originate to distribute” system, liquidity and reserves policies, regulators lack of uniformity, excessive leverage and concentration in real estate investment, poor liquidity risk management techniques, accounting rules and excessive reliance on credit rating agencies are often factors not to be underestimated. This crisis is a quite complex event that defies witch-hunts, folklore and superstition. Methodology certainly needs to be improved but blaming just the models for the crisis appears, in our opinion, to be the result of a very limited point of view.

London, Milan, Madrid, Pavia and Venice, December 1, 2009.

Damiano Brigo, Andrea Pallavicini and Roberto Torresetti.

Acknowledgments

We are grateful to Tom Bielecki for several interesting discussions and helpful correspondence. We are also grateful to Andrea Prampolini for helpful interaction on recovery modeling and other issues on the credit derivatives market. Frederic Vrins corresponded with us on the early versions, helping with a number of issues.

Damiano wishes to express gratitude to co-authors, colleagues and friends who contributed to his insight in the last years, including Aurelien Alfonsi, Agostino Capponi, Naoufel El-Bachir, Massimo Morini, and the Fitch Solutions London team including Imane Bakkar, Johan Beumee, Kyriakos Chourdakis, Antonio Dalessandro, Madeleine Golding, Vasileios Papatheodorou, Ed Parcell, Mirela Predescu, Karl Rodolfo, Daniel Schiemert, Gareth Stoyle, Rutang Thanawalla, Fares Triki, Weike Wu. This paper (and the related book) preparation has also been intersecting Damiano’s wedding, so that he is especially grateful to Valeria for her patience, the wonderful wedding and the Patagonia honeymoon, and to both families for constant support and affection in difficult times.

Andrea is grateful to his colleagues and friends for their helpful contributions and patience.

Roberto thanks Luis Manuel García Muñoz and Seivane Navia Soledad for helpful suggestions and support with analysis and insight.

1 Introduction:

credit modeling pre- and in-crisis

This paper aims at showing the limits of popular models or pseudo-models (mostly quoting mechanisms with modeling semblance) that in the past years have been extensively used to mark to market and risk manage multi-name credit derivatives. We present a compendium of results we first published before the crisis, back in 2006, pointing out the dangers in the modeling paradigms used at the time in the market, and showing how the situation has even worsened subsequently by analyzing more recent data. We also point out that the current paradigm had been heavily criticized before the crisis, referring to our and other authors works addressing the main limitations of the current market paradigm well before popular accounts such as Salmon (2009) appeared.

Problems of the current paradigm include

-

•

Unrealistic Gaussian copula assumption and flattening of 7750 pairwise dependence parameters into one.

-

•

Lack of consistency of the implied correlation market models with more than one tranche quote at the time

-

•

Occasional impossibility of calibration even of single tranches, or possibility to obtain negative expected tranched losses violating the arbitrage free constraints.

-

•

Lack of an implied loss distribution consistent with market CDO tranche quotes for a single maturity.

-

•

Lack of a loss distribution dynamics consistent with CDO tranche quotes on several maturities;

In this respect we will introduce examples of models published before the crisis that partly remedy the above deficiencies. All the discussion is supported by examples based on market data, pre- and in- crisis. In addressing these issues we adopt the following path through the different methodologies.

Bottom-up models

A common way to introduce dependence in credit derivatives modeling is by means of copula functions. A typically Gaussian copula is postulated on the exponential random variables triggering defaults of the pool names according to first jumps of Poisson processes. In general, if one tries to model dependence by specifying dependence across single default times, one is in the so called “bottom-up” framework, and the copula approach is typically within this framework. Such procedure cannot be extended in a simple way to a fully dynamical model in general. We cannot do justice to the huge copula literature in credit derivatives here. We only mention that there have been attempts to go beyond the Gaussian copula introduced in the CDO world by Li (2000) and leading to the implied (base and compound) correlation framework, some important limits of which have been pointed out in Torresetti et al. (2006b). Li et al (2005) also proposed a mixture approach in connection with CDO squared. For results on sensitivities computed with the Gaussian copula models see for example Meng and Sengupta (2008).

An alternative to copulas in the bottom up context is to insert dependence among the default intensities of single names, see for example the paper by Chapovsky, Rennie and Tavares (2006). Joshi and Stacey (2006) resort to modeling business time to create default correlation in otherwise independent single names defaults, resorting to an “intensity gamma” framework. Similarly but in a firm value inspired context, Baxter (2006) introduces Levy firm value processes in a bottom up framework for CDO calibration. Lopatin (2008) introduces a bottom up framework effective in the CDO context as well, having single name default intensities being deterministic functions of time and of the pool default counting process, then focusing on hedge ratios and analyzing the framework from a numerical performances point of view, showing this model to be interesting even if lacking explicit modeling of single names credit spread volatilities.

Going back to bottom-up models in the context of CDOs, Albanese et al. (2006) introduce a bottom-up approach based on structural models ideas that can be made consistent with several inputs both under the historical and pricing measures and that manages to calibrate CDO tranches.

Compound correlation

Building on Torresetti et al (2006b), in the context of bottom-up models, we start with the net present value (NPV) of synthetic Collateralized Debt Obligations (CDO) tranches on pools of corporate credit references in its original layout: the compound correlation framework.

We highlight two of the major weaknesses of the compound correlation:

-

•

Lack of robustness of the compound correlation framework in view of the non-invertibility of mainly the 10-year-maturity DJi-Traxx and CDX tranches and more recently the non-invertibility of mainly the 10-year-maturity DJi-Traxx and CDX tranches.

-

•

Flattening information on 7750 pairwise correlation parameters into a single one for each tranche.

-

•

More importantly from a practical standpoint, we highlight the typical non smooth behaviour of the compound correlation and the resulting difficulties in pricing bespoke CDO tranches.

Base correlation

We then introduce the next step the industry took, see for example McGinty and Ahluwalia (2004), namely the introduction of base correlation, as a solution to both problems given the fact that:

-

•

the resulting map is much smoother, thus facilitating the pricing of bespoke tranche spreads from liquid index tranches;

-

•

until early 2008 the heterogeneous pool one-factor Gaussian copula base correlation has been consistently invertible from index market tranche spreads

Nevertheless we expose what are some of the known remaining weaknesses of the base correlation framework:

-

•

Depending on the interpolation technique being used, tranche spreads could be not arbitrage free. In fact for senior tranches it may well be that the expected tranche loss plotted versus time is initially decreasing.

-

•

The impossibility of inverting correlation for senior AAA and super senior tranches.

-

•

Inconsistency at single tranche valuation level, as two components of the same trade are valued with models having two different parameter values;

-

•

Last but not least, flattening information on 7750 pairwise correlation parameters into a single one for each equity tranche trade.

As an explanation to the first weakness we point to the fact related to the third one, namely that this arises because the NPV of each tranche is obtained computing the expected tranche loss and outstanding notional under two different distributions (the distribution corresponding to the attachment base correlation and the one corresponding to the detachment base correlation) so that base correlation is an inconsistent notion already at single tranche level.

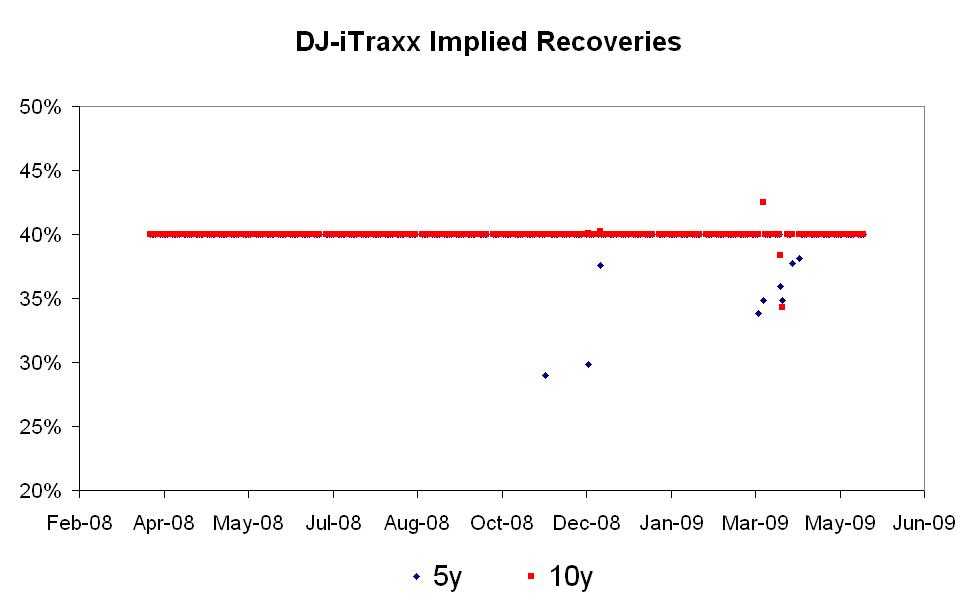

As an explanation to the second weakness we point to the fact that the deterministic recovery assumption, whilst being computationally very convenient, does not allow to capture the more recent market conditions. This has been addressed in the implied correlation framework by Amraoui and Hitier (2008) and Krekel (2008). However, even with this update, base correlation remains exposed to the remaining three weaknesses.

Base correlation, with updates and variants, remains to this day the main pricing method for synthetic corporate CDOs, regardless of the body of research criticizing it we hint at above and below.

Implied copula

We next summarize the concept of Implied Copula (introduced by Hull and White (2006) as “Perfect Copula”) as a non-parametric model, to deduce from a set of market CDO spreads, spanning the entire capital structure, the shape of the risk-neutral pool loss distribution. The general use of flexible systemic factors has been later generalized and vastly improved by Rosen and Saunders (2009), who also discuss the dynamic implications of the systemic factor framework. Factors and dynamics are also discussed in Inglis et al. (2008), while Eberlein, Frey and von Hammerstein (2008) generalize the original factor model by Vasicek (1987, 1991) and also propose a dynamic Markov chain model for CDO tranche pricing.

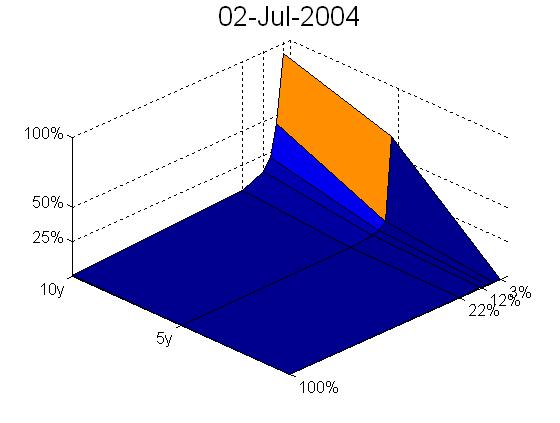

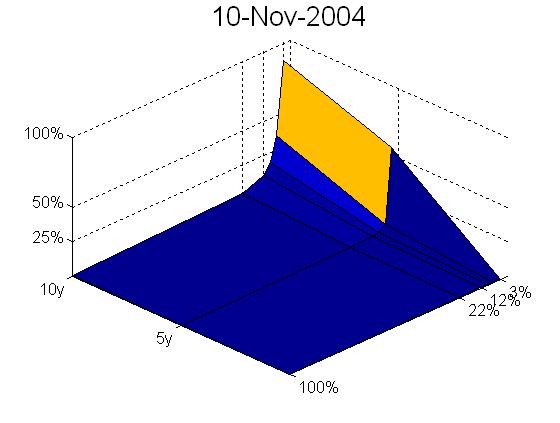

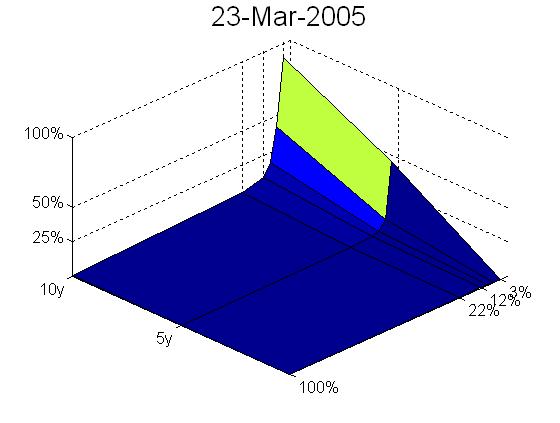

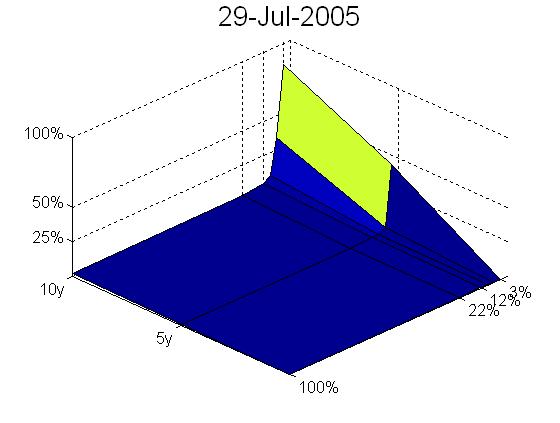

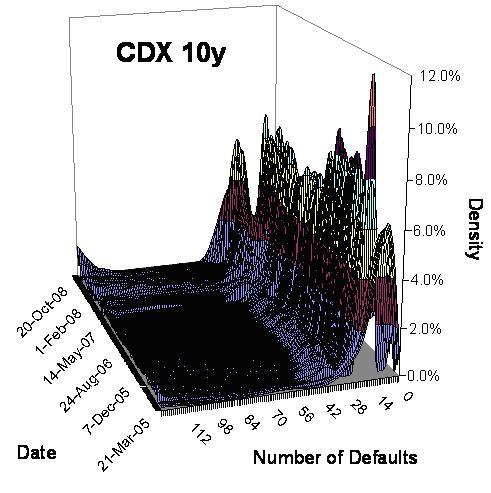

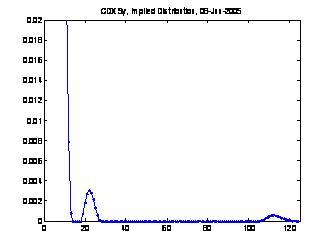

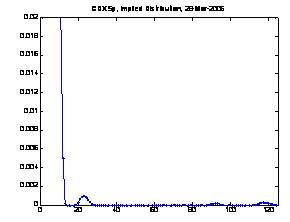

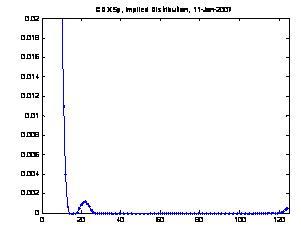

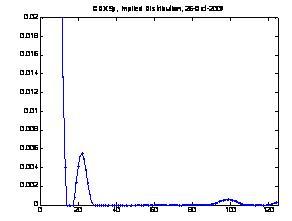

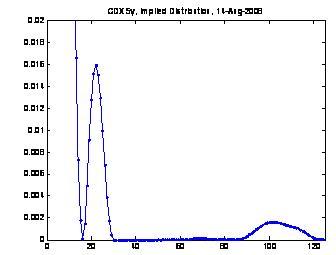

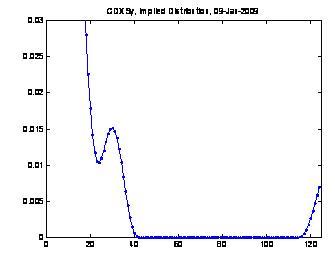

Our calibration results based on the implied copula, already seen in Torresetti et al (2006c), point out that a consistent loss distribution across tranches for a single maturity features modes in the tail of the loss distribution. These probability masses on the far right tail imply default possibilities for large clusters (possibly sectors) of names of the economy. These results had been published originally in 2006 on SSRN.com. We will report such features here and we will find the same features again following a completely different approach below.

Here we highlight the persistence of the modes (bumps) in the right tail of the implied loss distribution

-

•

Through time, via historical calibrations

-

•

Through regions, comparing the results of the historical calibration to the DJi-Traxx and the CDX

-

•

Through maturities, comparing the results of the calibration to different maturities

The Implied Copula can calibrate consistently across the capital structure but not across maturities, as it is a model that is inherently static. The next step thus consists in introducing a dynamic loss model. This moves us into the so called top-down framework (although dynamic approaches are also possible in the bottom-up context, as we have seen in part of the above references). But before analyzing the top-down framework in detail, we make a quick diversion for a model-independent approach to CDO tranches pricing and interpolation.

Expected Tranche Loss (ETL) Surface

Expected tranche losses (ETL) for different detachment points and maturities can be viewed as the basic bricks on which synthetic CDO formulas components are built with linear operations (but under some non-linear constraints). We explain in detail how the payoffs of credit indices and tranches are valued in terms of expected tranched losses (ETL). This methodology, first illustrated pre-crisis in Torresetti et al. (2006a), reminds of Walker’s (2006) earlier work and of the formal analysis of the properties of expected tranche loss in connection with no arbitrage in Livesey and Schlögl (2006).

ETL are natural quantities to imply from market data. No-arbitrage constraints on ETL s as attachment points and maturities change are introduced briefly. As an alternative to the inconsistent notion of implied correlation illustrated earlier, we consider the ETL surface, built directly from market quotes given minimal interpolation assumptions. We check that the kind of interpolation does not interfere excessively with the results. Instruments bid/asks enter our analysis, contrary to Walker s (2006) earlier work on the ETL implied surface. By doing so we find less violations of the no-arbitrage conditions.

We also mention some further references appeared later and dealing with evolutions of this technique: Parcell and Wood (2007), again pre-crisis, consider carefully the impact of different kinds of interpolation, whereas Garcia and Goossens (2007) compare ETL between the Gaussian copula and Lévy models.

In general the ETL implied surface can be used to value tranches with nonstandard attachments and maturities as an alternative to implied correlation. However, deriving hedge ratios as well as extrapolation may prove difficult. Also, ETL is not really a model but rather a model-independent stripping algorithm, although the particular choice of interpolation may be viewed as a modeling choice. Eventually ETL is not helpful for pricing more advanced derivatives such as tranche options or cancelable tranches. This is because ETL does not specify an explicit dynamics for the loss of the pool. To that we turn now, by looking at the top-down dynamic loss models.

Top (down) framework

One could give up completely single name default modeling and focus on the pool loss and default counting processes, thus considering a dynamical model at the aggregate loss level, associated to the loss itself or to some suitably defined loss rates. This is the “top-down” approach, see for example Bennani (2005, 2006), Giesecke, Goldberg and Ding (2005), Schönbucher (2005), Di Graziano and Rogers (2005), Brigo, Pallavicini and Torresetti (2006a,b), Errais, Giesecke and Goldberg (2006), Lopatin and Misirpashaev (2007), Ding, Giesecke and Tomecek (2009) among others.

The first joint calibration results of a dynamic loss model across indices, tranches attachments and maturities, available in Brigo, Pallavicini and Torresetti (2006a), show that even a relatively simple loss dynamics, like a capped generalized Poisson process, suffices to account for the loss distribution dynamical features embedded in market quotes.

This work also confirms the implied-copula findings of Torresetti et al (2006c), showing that the loss distribution tail features a structured multi-modal behaviour implying non negligible default probabilities for large fractions of the pool of credit references, showing the potential for high losses implied by CDO quotes before the beginning of the crisis. Cont and Minca (2008) use a non-parametric algorithm for the calibration of top models, constructing a risk neutral default intensity process for the portfolio underlying the CDO, looking for the risk neutral loss process “closest” to a prior loss process using relative entropy techniques. See also Cont and Savescu (2008).

However, in general to justify the “down” in “top-down” one needs to show that from the aggregate loss model one can recover a posteriori consistency with single-name default processes when they are not modeled explicitly. Errais, Giesecke and Goldberg (2006) advocate the use of random thinning techniques for their approach, see also Halperin and Tomecek (2008), who delve into more practical issues related to random thinning of general loss models, and Giesecke, Goldberg and Ding (2005) who compare the thinning based edges of the top down model with the copula-based ones. Bielecki, Crepey and Jeanblanc (2008) build semi-static hedging examples and consider cases where the portfolio loss process may not be a sufficient statistics.

Still, it is not often clear for specific models whether a fully consistent single-name default formulation is possible given an aggregate model as the starting point. There is a special “bottom-up” approach that can lead to a distinct and rich loss dynamics. This approach is based on the common Poisson shock (CPS) framework, reviewed in Lindskog et al. (2003). This approach allows for more than one defaulting name in small time intervals, contrary to some of the above-mentioned “top-down” approaches. In the “bottom-up” language, one sees that this approach leads to a Marshall-Olkin copula linking the first jump (default) times of single names. In the “top-down” language, this model looks very similar to the Generalized Poisson Loss model in Brigo et al (2006a) when one does not cap the number of defaults. The problem of the CPS framework is that it allows for repeated defaults, which is clearly wrong as one name could default more than once.

In the credit derivatives literature the CPS framework has been used for example in Elouerkhaoui (2006), see also references therein. Balakrishna (2006) introduces a semi-analytical approach allowing again for more than one default in small time intervals and hints at its relationship with the CPS framework, showing also some interesting calibration results. Balakrishna (2007) then generalizes this earlier paper to include delayed default dependence and contagion.

Generalized Poisson (Cluster) Loss model

Brigo et al (2007) address the repeated default issue in CPS by controlling the clusters default dynamics to avoid repetitions. They calibrate the obtained model satisfactorily to CDO quotes across attachments and maturities, but the combinatorics for a non-homogeneous version of the model are forbidding, and the resulting GPCL approach is hard to use successfully in practice when taking into account single names. Still, in the context of the present paper, the GPL and GPCL models will be useful in showing how a loss distribution dynamics consistent with CDO market quotes should evolve.

In this paper we summarize the Generalized Poisson Loss model, leaving aside the GPCL model. As explained above, GPL is a dynamical models for the loss, able to reprice all tranches and all maturities at the same time. We employ here a variant that models directly the loss rather than the default counting process plus recovery. The loss is modeled as the sum of independent Poisson processes, each associated with the default of a different number of entities, and capped at the pool size to avoid infinite defaults. The intuition of these driving Poisson processes is that of defaults of sectors, although the sectors amplitudes vary in our formulation of the model pre- and in-crisis. In the new model implementation in-crisis for this paper we fix the amplitude of the loss triggered by each cluster of defaults a priori, without calibrating it as we were doing in our earlier GPL work. This makes the calibration more transparent and the calibrated intensities of the sectors defaults easier to interpret. We point out, however, that the precise default of sectors is made rigorous only in GPCL.

We highlight how the GPL model is able to reproduce the tail multimodal feature that the Implied Copula proved to be indispensable to reprice accurately the market spreads of CDO tranches on a single maturity. We also refer to the later related results of Longstaff and Rajan (2007), that point in the same direction but adding a principal component analysis on a panel of CDS spread changes, with some more comments on the economic interpretation of the default clusters being sectors. An econometric investigation of cluster defaults starting from the Poisson framework is in Duan (2009).

Remark 1.1.

We draw the reader’s attention to the default history, pointing to default clusters being concentrated in a relatively short time period (a few months) like the thrifts in the early 90s at the height of the loan and deposit crisis, airliners after 2001, autos and financials more recently. In particular, from the 7th September 2008 to the 8th October 2008, a time window of one month, we witnessed seven credit events occurring to major financial entities: Fannie Mae, Freddie Mac, Lehman Brothers, Washington Mutual, Landsbanki, Glitnir, Kaupthing. Fannie Mae and Freedie Mac conservatorships were announced on the same date (September 7, 2008) and the appointment of a “receivership committee” for the three icelandic banks (Landsbanki, Glitnir, Kauping) was announced between the 7th and the 8th of October.

Remark 1.2.

Standard and Poors issued a request for comments related to changes in the rating criteria of corporate CDO111111see “Request for Comment: Update to Global Methodologies and Assumptions for Corporate Cash Flow CDO and Synthetic CDO Ratings” , 18-Mar-09, Standard & Poor s.. Thus far agencies have been adopting a multifactor Gaussian Copula approach to simulate the portfolio loss in the objective measure. S&P proposed changing the criteria so that tranches rated ’AAA’ should be able to withstand the default of the largest single industry in the asset pool with zero recoveries. We believe this goes in the direction of modelling the loss in the risk neutral measure via GPL like processes, given that this implies admitting as a stressed but plausible scenario the possibility that a cluster defaults in the objective measure. See also Torresetti and Pallavicini (2007) for the specific case of Constant Proportion Debt Obligations (CPDO).

We finally comment more generally on the dynamical aggregate models and on their difficulties to lead to single name hedge ratios when trying to avoid complex combinatorics. The framework remains thus incomplete to this day, because obtaining jointly tractable dynamics and consistent single name hedges, that can be realistically applied in a trading floor, remains a problem. We provided some references for the latest research in this field above. We highlight, though, that even a simple dynamical model like our GPL or the single-maturity implied copula is enough to appreciate that the market quotes were implying the presence of large default clusters with non-negligible probabilities well in advance of the credit crisis, as we documented in 2006 and early 2007.

Paper structure

Section 2 introduces the index and CDO tranche payouts we will be analyzing in this paper, explaining also the definition of tranche spread and upfront quotes. Section 3 introduces the Gaussian copula model, in its different formulations concerning homogeneity and finiteness, and then illustrates the notions of implied correlation from CDO tranche quotes. The two paradigms of base correlation and compound correlation are explained in detail. Existence and uniqueness of implied correlation are discussed on a number of market examples, highlighting the pros and cons of compound and base correlations, and the limitations inherent in these concepts. The section ends with a summary of issues with implied correlations, pointing out the danger for arbitrage when negative expected tranche losses surface, and the lack of consistency across capital structure and maturity. The first inconsistency is then addressed in Section 4, with the implied copula, illustrated with a number of studies throughout a long period, both pre- and in- crisis, whereas both inconsistencies are addressed in Section 6, where our full-fledged GPL dynamic loss model is illustrated pre-crisis. In Section 6 we explore en passant a model-free extraction of expected loss information from CDO quotes that can be occasionally helpful in interpolating or checking arbitrage constraints. All these paradigms are then analyzed in crisis in Section 7, while the final discussion, including the reasons why implied correlation is still used despite all its important shortcomings, are given in Section 8. In Particular, the need for hedge ratios with respect to single names, random recovery modeling and speed of calibration remain issues that are hard to address jointly outside the base correlation framework.

2 Market quotes

For single names our reference products will be credit default swaps (CDS).

The most liquid multi-name credit instruments available in the market are instead credit indices and CDO tranches (e.g. DJi-TRAXX, CDX). We discuss them in the following.

The procedure for selecting the standardized pool of names is the same for the two indices. Every six months a new series is rolled at the end of a polling process managed by MarkIt where a selected list of dealers contributes the ranking of the most liquid CDS. All credit references that are not investment grade are discarded. Each surviving credit reference underlying the CDS is assigned to a sector. Each sector is contributing a predetermined number of credit references to the final pool of names. The rankings of the various dealers for the investment grade names are put together to rank the most liquid credit references within each sector.

The index is given by a pool of names , typically , each with notional so that the total pool has unitary notional. The index default leg consists of protection payments corresponding to the defaulted names of the pool. Each time one or more names default the corresponding loss increment is paid to the protection buyer, until final maturity arrives or until all the names in the pool have defaulted.

In exchange for loss increase payments, a periodic premium with rate is paid from the protection buyer to the protection seller, until final maturity . This premium is computed on a notional that decreases each time a name in the pool defaults, and decreases of an amount corresponding to the notional of that name (without taking out the recovery).

We denote with the portfolio cumulated loss and with the number of defaulted names up to time divided by . Since at each default part of the defaulted notional is recovered, we have . The discounted payoff of the two legs of the index is given as follows:

where is the discount factor (often assumed to be deterministic) between times and and is the year fraction. In the second equation the actual outstanding notional in each period would be an average over , but we replaced it with the value of the outstanding notional at for simplicity.

The market quotes the values of that, for different maturities, balances the two legs. Assuming deterministic default-free interest rates, if one has a model for the loss and the number of defaults one may impose that the loss and number of defaults in the model, when plugged inside the two legs, lead to the same risk neutral expectation (and thus price)

| (1) |

Synthetic CDO with maturity are contracts involving a protection buyer, a protection seller and an underlying pool of names. They are obtained by “tranching” the loss of the pool between the points and , with .

An alternative expression that is useful is

| (2) |

Once enough names have defaulted and the loss has reached , the count starts. Each time the loss increases the corresponding loss change re-scaled by the tranche thickness is paid to the protection buyer, until maturity arrives or until the total pool loss exceeds , in which case the payments stop.

The discounted default leg payoff can then be written as

Again, one should not be confused by the integral, the loss changes with discrete jumps. Analogously, also the total loss and the tranche outstanding notional change with discrete jumps.

As usual, in exchange for the protection payments, a premium rate , fixed at time , is paid periodically, say at times . Part of the premium can be paid at time as an upfront . The rate is paid on the “survived” average tranche notional. If we further assume payments are made on the notional remaining at each payment date , rather than on the average in , the premium leg can be written as

When pricing CDO tranches, one is interested in the premium rate that sets to zero the risk neutral price of the tranche. The tranche value is computed taking the (risk-neutral) expectation (in ) of the discounted payoff consisting on the difference between the default and premium legs above. Assuming deterministic default-free interest rates we obtain

| (3) |

The above expression can be easily recast in terms of the upfront premium for tranches that are quoted in terms of upfront fees.

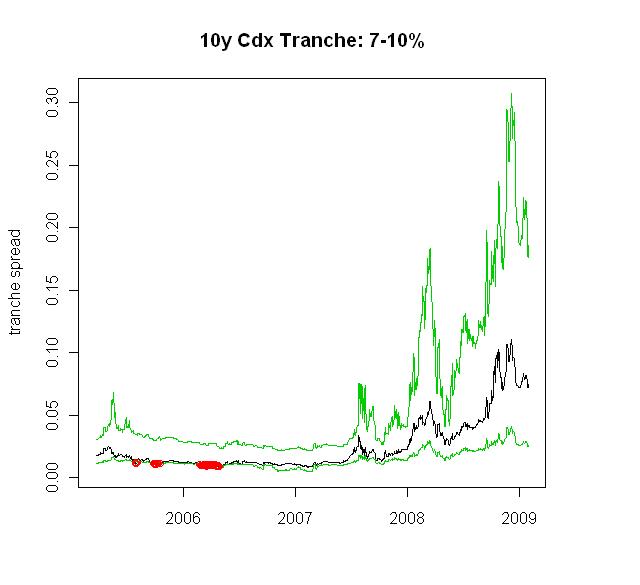

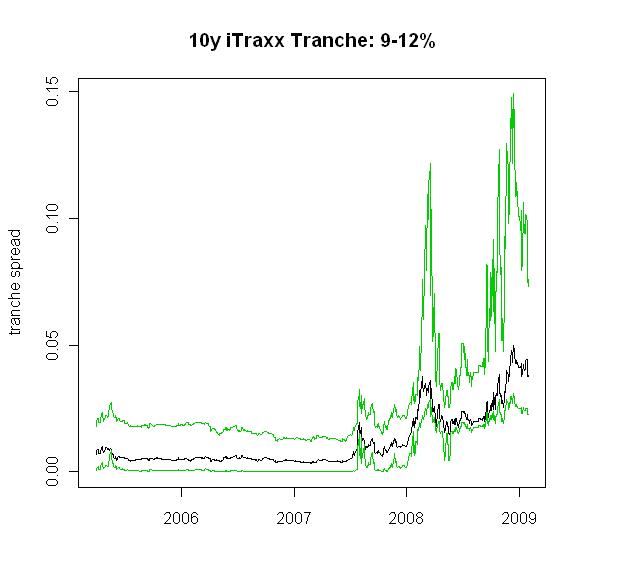

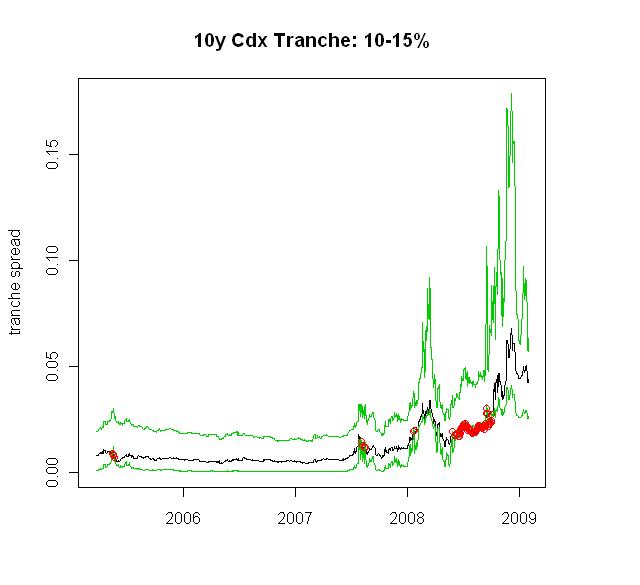

The tranches that are quoted on the market refer to standardized pools, standardized attachment-detachment points and standardized maturities. The standardized attachment and detachment are slightly different for the CDX.NA.IG and the DJi-Traxx Europe Main121212The attachment of the CDX tranches are slightly higher reflecting the average higher perceived riskiness (as measured for example by the CDS spread or balancesheet ratios) of the liquid investment grade north american names..

| DJi-Traxx Europe Main | CDX.NA.IG |

|---|---|

| 0-3% | 0-3% |

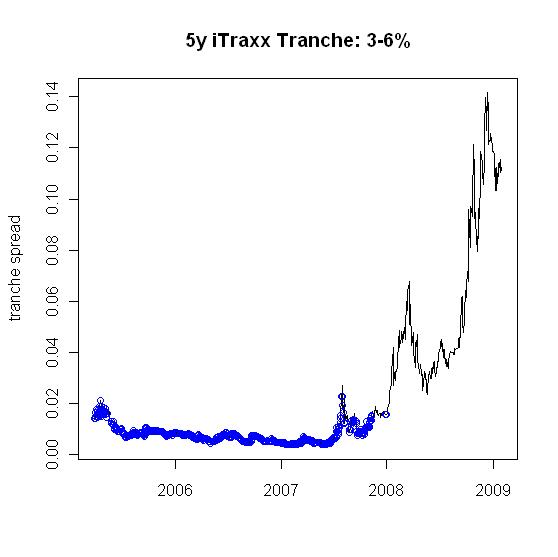

| 3-6% | 3-7% |

| 6-9% | 7-10% |

| 9-12% | 10-15% |

| 12-22% | 15-30% |

| 22-100% | 30-100% |

For the DJi-Traxx and CDX pools, the equity tranche is quoted by means of the fair , while assuming131313The reason for the equity tranche to be quoting as upfront is to reduce the counterparty credit risk the protection seller is facing. . All other tranches are generally quoted by means of the fair running spread , assuming no upfront fee (. Following the recent market turmoil also the 3-6% and the 3-7% have been quoting in terms of an upfront amount and a running given the exceptional riskiness priced by the market also for mezzanine tranches.

3 Gaussian copula model

The Gaussian Copula model is a possible way to model dependence of random variables and, in our case, of default times. As the default event of a credit reference is a random binary variable, the correlation between default events is not an intuitive object to handle. We need to focus our attention rather on default times. We denote by the default time of name in a pool of names. Default times of different names need to be connected. The copula formalism allows to do this in the most general way.

Indeed, if is the default probability of name by time , we know that the random variable is a uniform random variable. Copulas are multivariate distributions on uniform random variables. If we call a multivariate uniform distribution, and is a multivariate uniform with distribution , then a possible multivariate distribution of the default times with marginals is

where for simplicity we are assuming the s to be strictly invertible. Clearly, since the variables are connected through a multivariate distribution , we have a dependence structure on the default times.

The Gaussian copula enters the picture when we assume that

where the are standard Gaussian random variables and is a given multivariate Gaussian random variable with a given correlation matrix. is the cumulative distribution function of the one-dimensional standard Gaussian. In the Gaussian Copula model the default times are therefore linked via normally distributed latent factors .

A particular structure is assumed for the default probabilities . The default probabilities of single names are supposed to be related to hazard rates . In other terms . We define .

We also anticipate that the correlation matrix characterizing the Gaussian copula is often taken with all off-diagonal entries equal to each other according to a common value in corporate synthetic CDO valuation applications. This is always the case in particular when defining implied correlations.

(spread) or (upfront) would be provided by the market and a correlation number characterizing a Gaussian copula with a correlation matrix where all entries are equal to (in this case we will say the correlation matrix to be “flat to ”) would be implied from the market quote. Indeed, Formula (3) defined the market quotes in terms of expectations of the tranced loss ; in turn, the loss to be tranched at a given time is defined in terms of single default times as

| (4) |

where the are multivariate Gaussians with correlation matrix flat to and are the recovery rates associated to each name.

The correlation parameter is therefore affecting the tranche price since it is a key statistical parameter contributing to the tranched loss distribution whose expectation will be used in matching the market quote. Implied correlation aims at finding the value of consistent with a given tranche quote when every other model parameter (the s, the s) has been fixed.

We next illustrate the two main types of implied correlation one may obtain from market CDO tranche spreads:

-

1.

Compound correlation is more consistent at single tranche level but for some market CDO tranche spreads cannot be implied or more than one correlation can be implied.

-

2.

Base correlation is less consistent but more flexible and can be implied for a much wider set of CDO tranche market spreads. Furthermore, base correlation is more easily interpolated and leads to the possibility to price non-standard detachments. Even so, Base correlation may lead to negative expected tranche losses, thus violating basic no-arbitrage conditions. We illustrate these features with numerical examples.

We will first introduce the general One-Factor Gaussian Copula model. Then we will introduce the Finite Pool (where is finite) Homogeneous ( and ) One-Factor Gaussian Copula model. We will show how the loss probabilities formulas can be computed in this case.

Remark 3.1.

In this work we stay with the homogeneous version, since this is enough to highlight some of the key flaws of implied correlation, leaving to the full book of Brigo, Pallavicini and Torresetti (2010) the detailed derivation of the formulas for the heterogeneous and large pool versions. It is to be said that in practice, due to the necessity of computing hedge rations with respect to single names, the heterogeneous version is used, even if spread dispersion across names, leading possibly to very different s, complicates matters.

3.1 One-factor Gaussian copula model

A One-factor copula structure is a special case of the Gaussian copula above where

with standard independent Gaussian variables. is a systemic factor affecting default times of all names. is a idiosyncratic factor affecting just the -th name.

This parameterization would lead to a correlation between Gaussian factors and given by . However, consistently with the flat correlation assumption and the homogeneity assumption all pairwise correlation parameters collapse to a single common value, i.e. for all .

Assuming deterministic and possibly distinct recovery rate upon default we are able to simulate the pool loss at any time starting from the simulation of the Gaussian variables s starting from equation (4). Thus we are able to simulate the NPV of the premium and default leg of any tranche.

The heterogeneous Gaussian Copula model assumes possibly different recovery rates and probabilities of default . The large pool assumption basically assumes homogeneity of both the recovery rates and probabilities of default and also assumes an infinite number of credit references leading to a substantial increase in the numerical efficienty of the pricing formulas.

In the following, as already mentioned, we stay with the homogeneous version thus assuming identical and for all credit references in the pool.

Calculating the NPV of a derivative instrument via simulations can be necessary but may lead to intensive numerical effort. Introducing the assumption of homogeneity it turns out that the Gaussian Copula model yields a semi-analytical formula to calculate the distribution of the pool loss.

Assume we know the realization of the systemic factor . In this case, conditional on , the default events of the pool of credit references are independent. The default by time conditional on the realization of the systemic factor of each single credit reference in the pool is a Bernoulli random variable with the same event probability of default

The number of defaulted entities in the pool by time conditional on the realization of the systemic factor is the sum of Bernoulli variables and thus is binomially distributed.

| (5) |

where we point out that the s are the same for all s, since we are dealing with an homogeneous pool assumption.

We can now integrate the expression in (5) to get the unconditional probability of defaults occurring to the standardized pool of credit references before time , leading to

| (6) |

By computing the integral in (6) for we obtain the unconditional distribution of the pool loss rate that we need in order to compute the theoretical tranche spread (or upfront ) in equation (3).

The integral in equation (6) does not allow for a closed form solution whereas all other quantities can be analytically calculated. Hence the name semi-analytical (analytical up to the calculation of the integral) for the finite-pool homogeneous one-factor Gaussian copula model formula for theoretical tranche spread in (3).

3.2 Compound correlation

Compound correlation is a first paradigm for implying credit default dependence from liquid market data. This approach consists in linking defaults across single names through a Gaussian copula where all the correlation parameters are collapsed to one.

Given this correlation parameter and given the desired declination of the One-Factor Gaussian Copula we can compute the loss distribution on a given set of dates. Thus we can compute the expectations contained in (3), and with them the fair tranche spread.

A key step that will allow us to distinguish compound from base correlation is the decomposition of the tranche loss according to Equation (2). Since the default leg and premium leg (in particular the DV01) defining (3) are linear in the tranced loss , by Equation (2) this results to be linear in base tranched losses and .

Now one key step is that when we evaluate the expected through (2), we can use two different copula correlations for the two pieces (correlation ) and (correlation ). As a consequence, the final formula reads

| (7) |

A similar decomposition holds for the DV01, that is a linear combination of such objects.

Consider the DJi-Traxx tranches for example, to clarify the procedure. For a given maturity in 3y, 5y, 7y, 10y, consider the market quotes

To obtain the implied correlation one proceeds as follows.

First solve in for the equity tranche

Then in moving on one has two choices: retain from the earlier tranche calibration and solve

in (base correlation) or solve

in a new (compound correlation). The next step will be again similar, and we iterate, until we reach the end of the capital structure.

| Tranche | Running | Upfront |

|---|---|---|

| 0-3% | 500 bps | 49% |

| 3-6% | 360 bps | 0% |

| 6-9% | 82 bps | 0% |

| 9-12% | 46 bps | 0% |

| 12-22% | 31 bps | 0% |

Compound correlation is more consistent at the level of single tranche, since we value the whole payoff of the tranche premium and default legs with one single copula (model) with parameter .

Base correlation is inconsistent at the level of single tranche: we value different parts of the same payoff with different models, i.e. part of the payoff (involving ) is valued with a copula in , while a different part (involving ) of the same payoff is valued with a copula in .

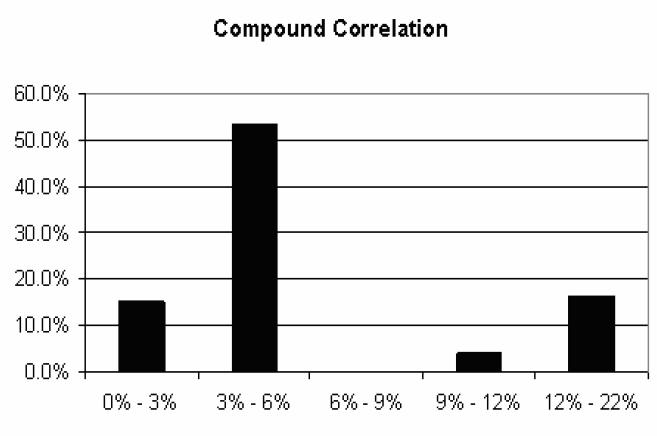

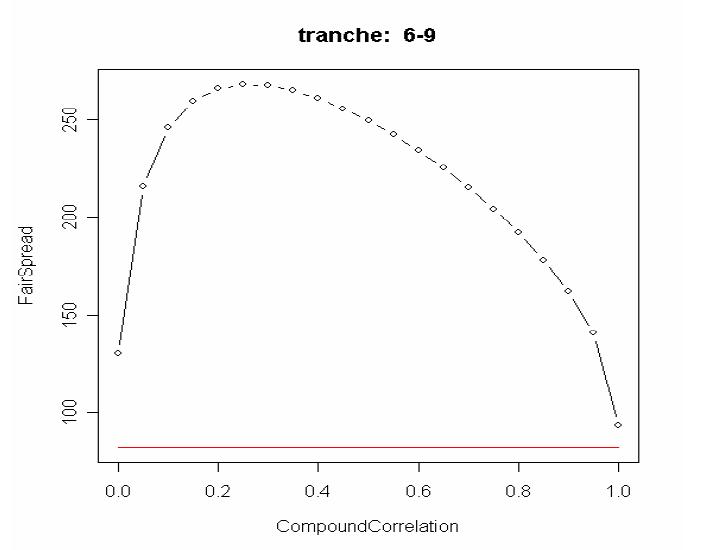

We will focus on implications for base correlation later on, and deal now with compound correlation. The market data we take as inputs are detailed in Table 2. In Figure 1 we present the compound correlation smile we imply from this set of market data. We notice that there is no bar corresponding to the 6-9% tranche: from the market spread of the tranche we cannot imply a compound correlation. We see in the following how this problem is not atypical.

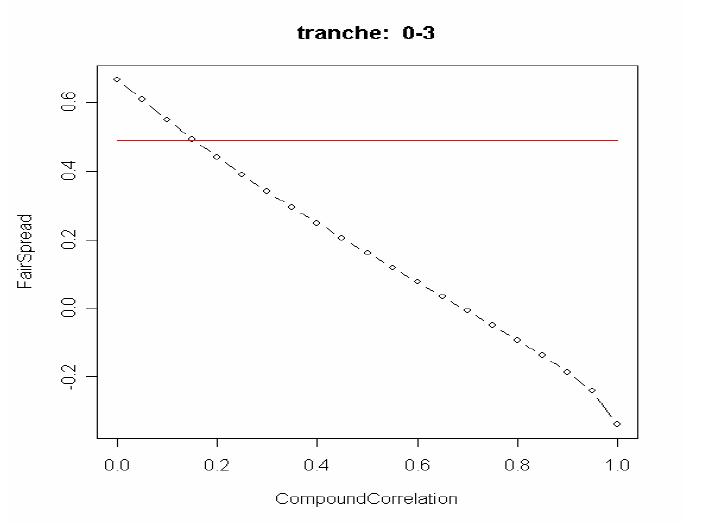

We have just seen that on a particular date we cannot imply a compound correlation from the market spread of the 6-9% tranche. To see why this is the case we investigate further this date plotting in Figure 2 the fair market spread as a function of the compound correlation: the equity tranche is quoted upfront (0.49 means ) and all other tranches are quoted in number of running basis points (360 means per annum). The red flat line is the level of the market spread.

Further, we notice that:

-

1.

for certain tranches, from the unique market spread we can imply more than one compound correlation, although this does not happen in our example of Figure 2 where the flat red line crosses the dotted black line at most in one point;

-

2.

given a market spread we are not always guaranteed we can imply a compound correlation, as we see for example in the 6-9% tranche of Figure 2 (there is no intersection between the flat red line and the dotted black line).

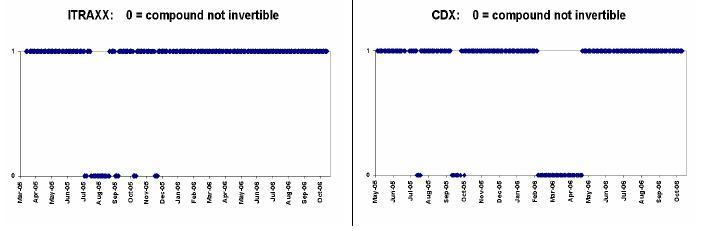

We have seen that on 3rd-aug-2005 we cannot imply a compound correlation for the 6-9% tranche. In Figure 3, taken from Torresetti et al. (2006b), we see how this problem is not limited to a sporadic set of dates but is rather affecting clusters of dates. From March 2005 to November 2006, the sample on which the analysis in Torresetti et al. (2006b) is based, the non invertibility of the compound correlation concerned for DJi-Traxx the 10 year 6-9% tranche, and for CDX the 10 year 7-10% tranche and, marginally, the 10 year 10-15%.

3.3 Base correlation

Here we will illustrate base correlation and we will see how compound correlation problems are overcome but at the expense of introducing a deeper inconsistency.

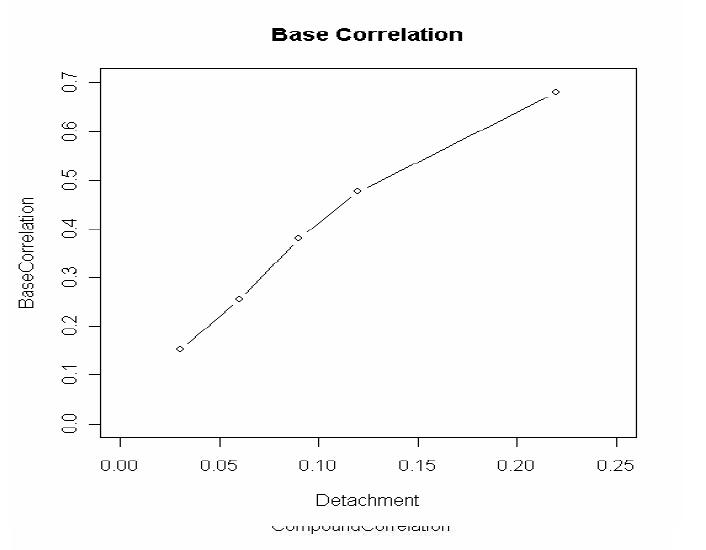

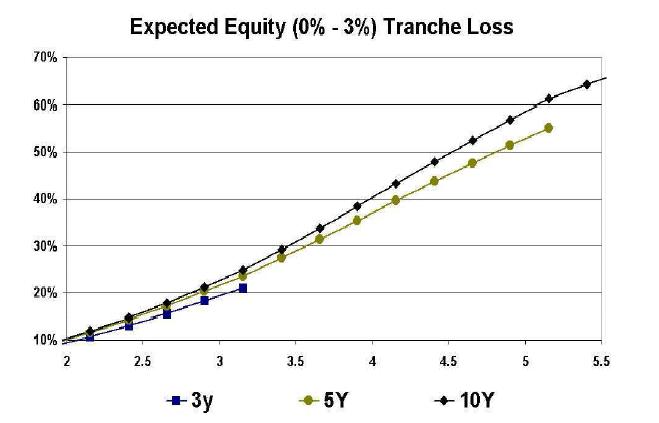

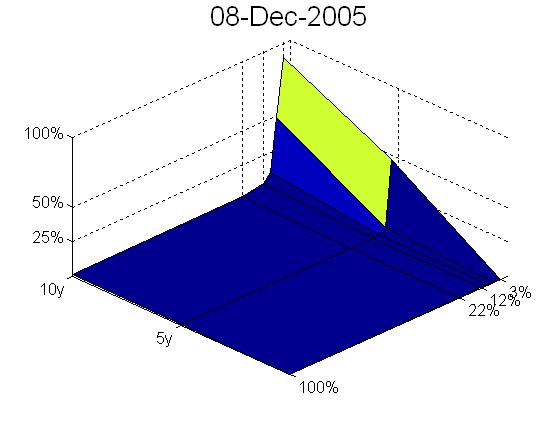

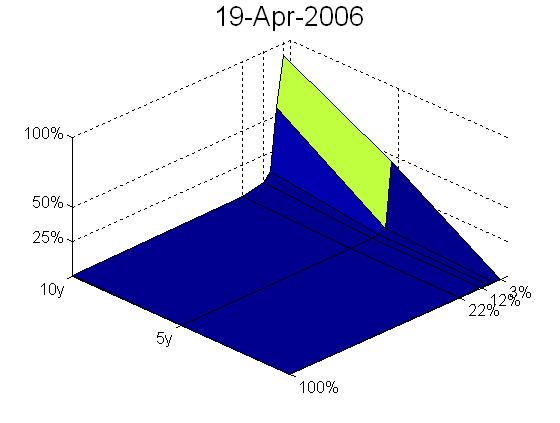

In Figure 4 we plot the Base Correlation calibrated to the market data in Table 2 and the Expected Equity Tranche Loss for the various detachment points as a function of time.

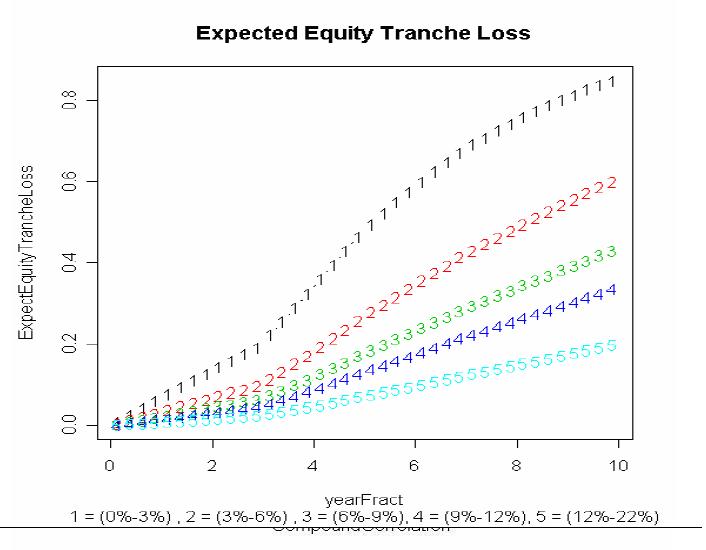

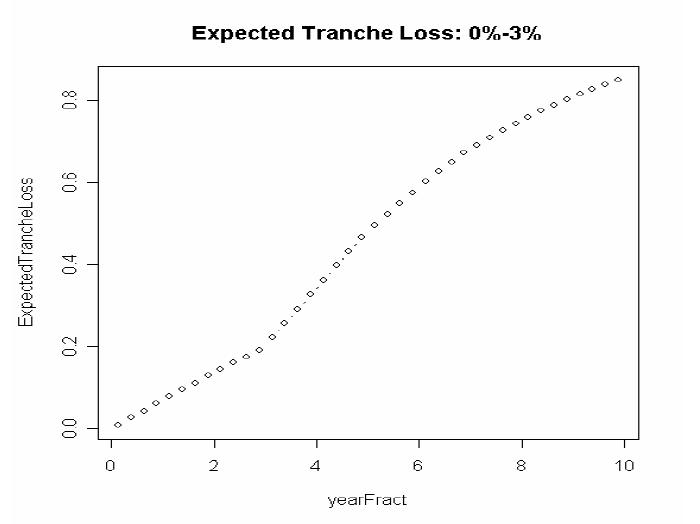

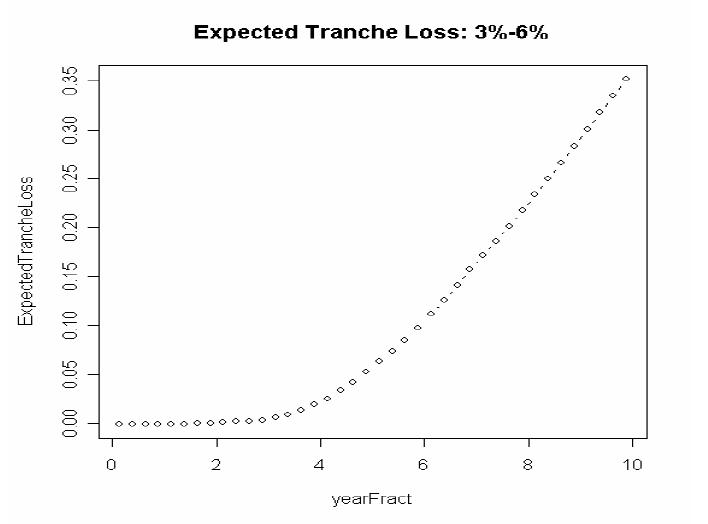

From these expectations, using equations (2), we can compute the Expected Tranche Loss , plotted in Figure 5 as a function of time.

From Figure 4 we note that the base correlation is a much smoother function of detachments than compound correlation. Also, to price a non-standard tranche, say a 4-15% tranche, we can interpolate the non-standard attachment 4% and detachment 15% whereas with the compound correlation we do not know exactly what to interpolate (since with compound correlation there is a unique correlation associated to each tranche, i.e. correlation is associated with two points rather than a single one).

As we can see from our examples, also the base correlation approach is not immune from inconsistencies. In fact in Figure 7 we note that already in 2005, taking the 6-9% tranche as an example, the expected tranche loss becomes initially slightly negative. This inconsistency arises from the different base correlations we use in Equation (2) to compute the two expected tranche loss terms in A and B.

3.4 Summary on implied correlation

Is base correlation a solution to the problems of compound correlation ?

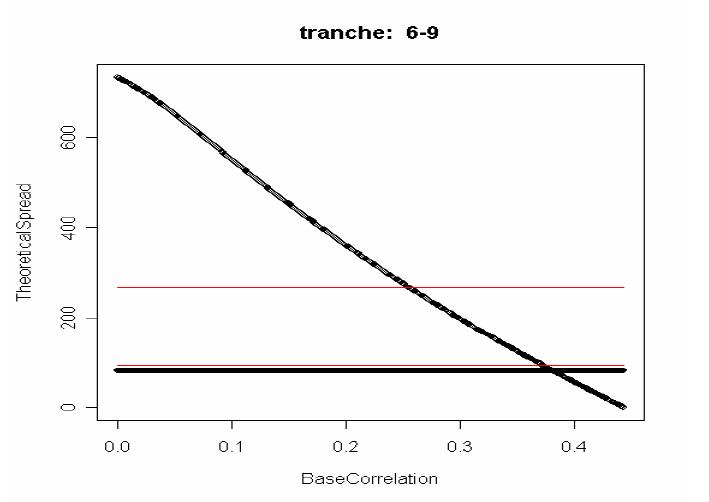

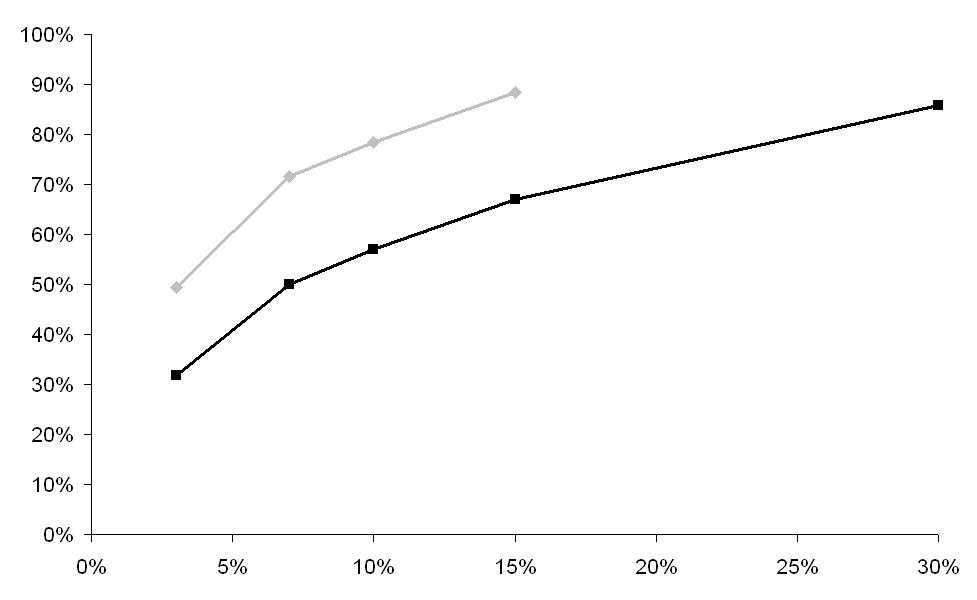

The answer is in the affirmative and this can be clearly seen for example in Figure 6 where we plot the fair tranche spread as a function of the base correlation on the detachment point for each tranche, given the base correlation on the attachment point set equal to the calibrated base in the left chart of Figure 4.

This gives us an idea of the range of the tranche spread we can calibrate using base correlation. These plots of Figure 6 can be compared with the plots in Figure 2, showing the fair tranche spread as a function of compound correlation. In Figure 6 the thick black line is flat at the level of the market spread for the tranche. The two thin red lines are the minimum and maximum spread we are able to obtain by varying compound correlation.

We note that for each tranche the fair spread is a monotonic function of the base correlation on the detachment point and also that the range of market spreads that can be attained by varying base correlation is much wider than the corresponding one for compound correlation. Consider for example the 6-9% tranche in Figure 2. The tranche spread that can be inverted in a compound correlation setting lies between 93 and 268 bps, whereas from Figure 6 the tranche spread that can be inverted in a base correlation setting lies in the wider range between 0 and 732 bps.

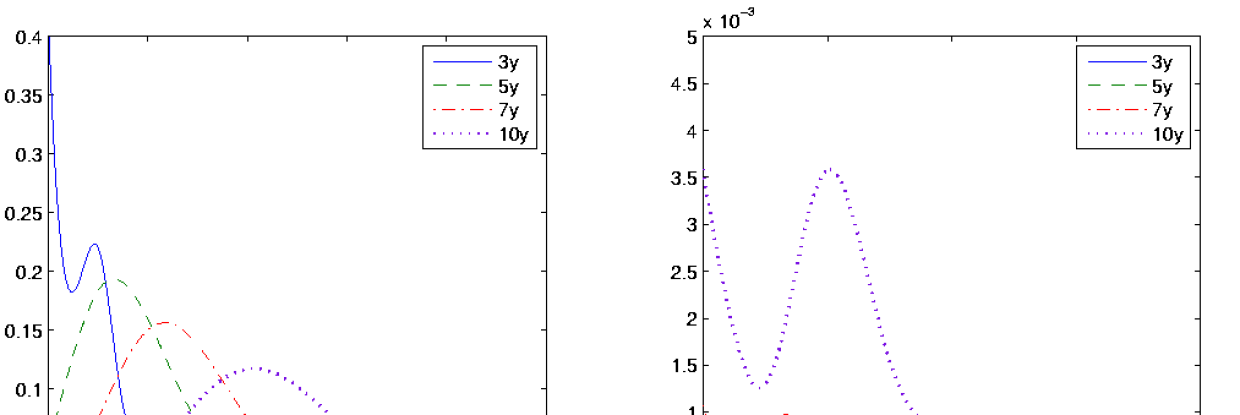

In Figure 6 we did not plot the market spread for all base correlations between 0 and 1 because beyond a certain point the fair tranche spread becomes negative. Recall once again that in Equation (2) we use two different correlation parameters for different parts of the same payoff: when these two correlations are very different from each other (the detachment correlation is much higher than the attachment one) the inconsistency of a negative expected tranche loss becomes more evident.

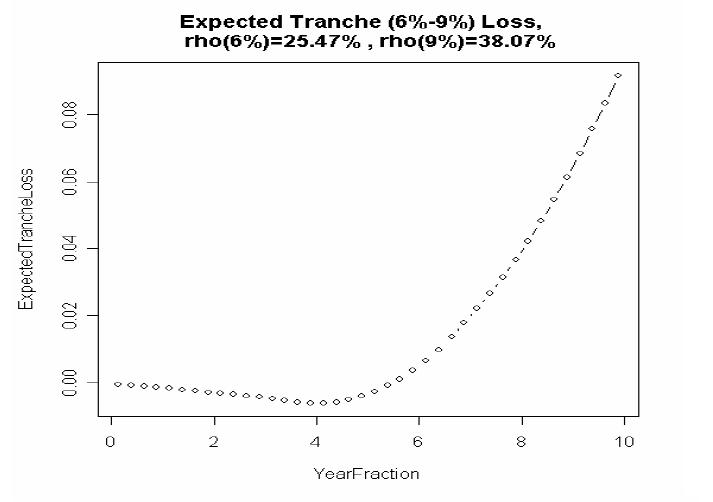

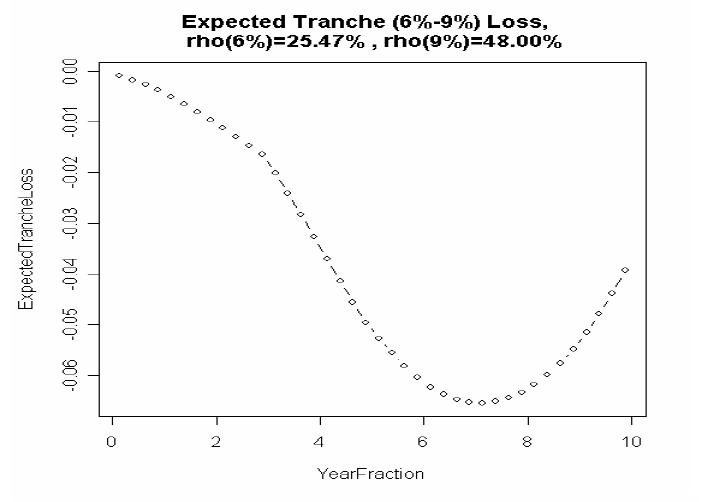

Consider for example the 6-9% tranche. In Figure 7 we plot in the abscissas the year fraction of the tranche payment dates and in the ordinates the Expected Tranche (6-9%) Loss. For both graphs in Figure 7 the tranche attachment correlation is the calibrated base on the detachment. The tranche detachment correlation is set to the calibrated base on the left hand graph and to an arbitrarily high level on the right hand graph.

We can see a markedly negative profile for the expected tranched loss, which clearly violates no arbitrage constraints. Indeed, the loss must be non-negative and non-decreasing in each paths through time, and tranching does not alter that. More simply, the tranched loss at a given point in time is a non-negative random variable, and its expected value needs to be non-negative itself. This does not happen in our example, in that the basic non-negativity constraint is violated. This is a strong drawback of the base correlation paradigm at a very basic level.

We have presented notions of implied correlation centered on the Gaussian copula. Alternative copula specifications are possible. Indeed, Hull and White (2004) show that on a particular date the “double-t copula” can consistently reproduce tranche spreads without skew in the correlation parameter. See the full book of Brigo, Pallavicini and Torresetti (2010) for more details on the double-t copula. This is unlikely to represent a solution to the lack of consistency in calibration, given both the low number of parameters in the model and a number of numerical issues with the procedure.

There are, overall, two major problems with the use of implied correlation as a parameter in a Gaussian copula model as we described it above, even if one is willing to accept the flattening of 7750 parameters into one: first, the model parameter changes every time we change tranche, implying very different and inconsistent loss distributions on the same pool. Second, there is a total lack of dynamics in the notion of copula. We address the first problem now, showing that the financial literature has been doing that well before the current crisis started in 2007. We will address the second problem in later sections.

4 Consistency across capital structure:

implied copula

In the implied copula approach, a factor copula structure is assumed, similarly to the One-Factor Gaussian Copula approach seen earlier. However, this time we do not model the copula explicitly, but we model default probabilities conditional on the systemic factor of the copula: the copula will then be “hidden” inside these conditional probabilities, that will be calibrated to the market. Hence the name “implied” copula. In illustrating the implied copula we will also assume a large pool homogeneous model, in that the default probabilities of single names will be taken all equal to each other and the pool of credit references is assumed to be comprised of an infinite number of credit references.

Let us consider, for simplicity, survival probabilities that are associated to a constant-in-time hazard rate. We know that if we have a constant-in-time (possibly random) hazard rate for name then the survival probability is

The implied copula approach postulates the following “scenario” distribution for the hazard rate conditional on the systemic factor :

This way the default probability for each single name is, conditional on the systemic factor ,

Compare with the Gaussian factor copula case:

Unconditionally, the implied copula yields the default probabilities

Conditional on , all default times are independent, have the same hazard rate and their hazard rates are given by the above scenarios.

By resorting to the infinite pool approximation, fully illustrated in the full book by Brigo, Pallavicini and Torresetti (2010), for the Gaussian factor copula in the LHP version, we have that the conditional default indicators are i.i.d. for all , so that their sample average as their number tends to infinity tends to the single common true mean:

when tends to .

Again, this way we avoid taking expectations, except the final one with respect to , since conditional on all randomness has been ruled out by the law of large numbers and both the default rate and the loss are completely determined.

We will assume, in line with the market convention, that the protection payment will be calculated on the average outstanding notional between any two protection premium payment dates. Conditional on the systemic factor realization the premium leg tranche value will be:

where and are the market mid upfront and running spread for the tranche A,B with maturity .

We will discretize the loss increments, entering the calculation of the discounted default leg payoff, on the same set of dates of the discounted premium leg payoff calculation: the protection premium payment dates. We will also assume that on average the loss increment arrives at the middle of each time interval .

where is a deterministic function of the probability of default conditional on the realization of the systemic factor , : we will expand more on this issue in the next section.

In case of the index the above definitions are still valid except for the DV01 which becomes:

We will call and the column vector that stacks respectively all discounted premium leg and default leg values conditional on the systemic factor states:

Then, we integrate against , simply summing over all possible hazard rate scenarios multiplying by the scenario probability, to obtain the tranche unconditional price. In matrix notation the receiver tranche value can be rewritten as

where is the column vector with the systemic factor probability distribution.

4.1 Recovery rate

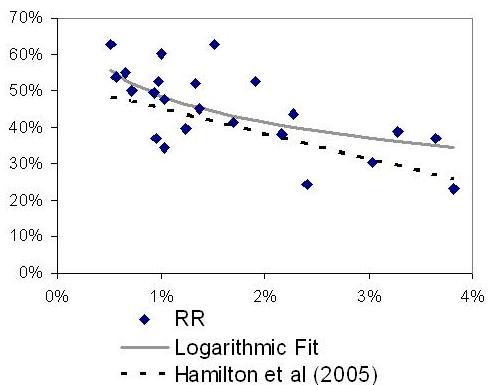

In this respect, we mention a relationship between default probabilities and recovery rates that may be necessary to fit the market correlation skew in periods of turmoil (e.g July 2005).

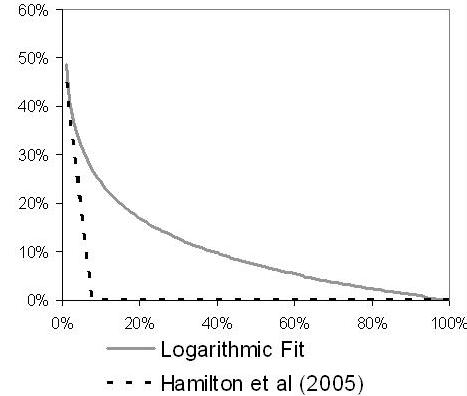

Following results of an empirical study by Hamilton et al (2005), Hull and White suggest to change recovery in each scenario by linking it to the conditional probability of default in that scenario:

This functional form will assign a recovery 0% to all default rate above 8%. Alternatively one could fit a logarithmic relationship between recovery rates and default rates:

Remark 4.1.

(Random recovery as a function of the systemic factor). The above formula makes the recovery a function of the intensity conditional on the systemic factor. This way recovery becomes a function of the systemic factor. An approach that makes recovery a function of the systemic factor in the inconsistent base correlation framework is in Amraoui and Hitier (2008).

The dots in the left panel of Figure 8 are the data points we have used to fit the parameter : Issuer Weighted All Rated Bond Default Rate and Issuer Weighted Recovery Rate Senior Unsecured from 1982 to 2004 taken from Moody’s.

From 1982 to 2004 the Issuer Weighted All Rated Bond Default Rate has been always below 3.82%. Therefore in the left panel of Figure 8 we cannot fully appreciate the different implication of the two functional forms when applied to the implied copula as we can do instead in the chart in the right panel.

4.2 Calibration of implied copula

When calibrating all the year DJ-iTraxx tranches we end up minimizing a constrained sum of squares. If we call NPV the matrix with all tranches (columns) discounted payoff for all possible states (rows)

then, calibration becomes simply

| (8) |

subject to:

Note that for the base correlation calibration the market tranches had to have consecutive adjacent attachment and detachment points spanning the whole capital structure; if that was not the case some base correlation interpolation assumption had to be introduced. With the Implied Copula this is not necessary in that the tranches to be calibrated need not span the whole capital structure or be adjacent.

In the implied copula framework, Hull and White (2006) calibrate the scenario probabilities while pre-assigning the hazard rate scenarios exogenously. The number of hazard rate scenarios can be seen empirically to be quite large, up to , in order to be able to fit market data with a good precision. In this case the above optimization has too many degrees of freedom which might result in a very good fit but quite an irregular scenario probability distribution. In order to cope with this problem Hull and White (2006) propose to add to the target function a quantity that penalizes changes in convexity in the patterns of the scenario probabilities plotted against the default probabilities associated to each scenario.

Torresetti et al. (2006c) propose a different approach with respect to Hull and White (2006) where there is no need to select a regularization coefficient. The main differences between the two approaches are summarized as follows.

-

•

Assign 125 possible states to the system factor . The hazard rates associated to each state are this time such that the pool default rate at maturity is equal to , where .

-

•

In our version perform a two stage optimization that will assure that all tranches are priced within the bid-ask spread without the need to choose a regularization coefficient.