Fluctuation-dissipation theory of input-output interindustrial relations

Abstract

In this study, the fluctuation-dissipation theory is invoked to shed light on input-output interindustrial relations at a macroscopic level by its application to IIP (indices of industrial production) data for Japan. Statistical noise arising from finiteness of the time series data is carefully removed by making use of the random matrix theory in an eigenvalue analysis of the correlation matrix; as a result, two dominant eigenmodes are detected. Our previous study successfully used these two modes to demonstrate the existence of intrinsic business cycles. Here a correlation matrix constructed from the two modes describes genuine interindustrial correlations in a statistically meaningful way. Further it enables us to quantitatively discuss the relationship between shipments of final demand goods and production of intermediate goods in a linear response framework. We also investigate distinctive external stimuli for the Japanese economy exerted by the current global economic crisis. These stimuli are derived from residuals of moving average fluctuations of the IIP remaining after subtracting the long-period components arising from inherent business cycles. The observation reveals that the fluctuation-dissipation theory is applicable to an economic system that is supposed to be far from physical equilibrium.

pacs:

05.40.-a, 87.23.Ge, 89.65.Gh, 89.75.FbI Introduction

Both the business cycle and the interindustrial relationship are long-standing basic issues in the field of macroeconomics, and they have been addressed by a number of economists. Recently, we analyzed (bc, ) business cycles in Japan using indices of industrial production (IIP), an economic indicator that measures current conditions of production activities throughout the nation on a monthly basis. Careful noise elimination enabled us to extract business cycles with periods of 40 and 60 months that were hidden behind complicated stochastic behaviors of the indices.

In this accompanying paper, we focus our attention on interindustrial relationship by analyzing IIP data in a framework of the linear response theory; the fluctuation-dissipation theory plays a vital role in the analysis of IIP data. We also discuss the difference between moving average fluctuations in the original data and long-period components arising from inherent business cycles. The residuals may be interpretable as a sign of external stimuli to the economic system. The recent worldwide recession offers us a good opportunity to conduct this study, because it delivered an unprecedented shock to the economic system of Japan.

The interindustrial relations of an economy are conventionally represented by a matrix in which each column lists the monetary value of an industry’s inputs and each row lists the value of the industry’s outputs, including final demand for consumption. Such a matrix, called the input-output table, was developed by Leontief (Leontief1936, ; Leontief1986, ). This table thus measures how many goods of one industrial sector are used as inputs for production of goods by other industrial sectors and also the extent to which internal production activities are influenced by change in final demand. Leontief’s input-output analysis can be regarded as a simplified model of Walras’s general equilibrium theory (Walras1954, ) to implement real economic data for carrying out an empirical analysis of such economic interactions. Currently, the basic input-output table is constructed every 5 years according to the System of National Accounts (SNA) by the Ministry of Internal Affairs and Communications in Japan.

It should be noted that the input-output table describes yearly averaged interindustrial relations. Although such a poor time resolution of the table may be tolerable for budgeting of the government on an annual basis, various day-to-day issues faced by practitioners require them to react promptly. We thus need a more elaborate methodology that enables investigation of the input-output interindustrial relationship with a much higher time resolution.

Econophysics (MS2000, ; BP2003, ; AY2007, ; AFIIS2010, ) is a newly emerging discipline in which physical ideas and methodologies are applied for understanding a wide variety of complex phenomena in economics. We adopt this approach to address the above-mentioned issues in macroeconomics. That is, we pay maximum attention to real data while drawing any conclusions. Of course it is important to remember that real data are possibly contaminated with various kinds of noise. The random matrix theory (RMT), combined with principal component analysis, has been used successfully to extract genuine correlations between different stocks hidden behind complicated noisy market behavior (laloux1999ndf, ; plerou1999uan, ; plerou2002rma, ; utsugi2004rmt, ; kim2005sag, ; KD2007, ; PhysRevE.76.046116, ; SZ2009, ). Recently, dynamical correlations in time series data of stock prices have been analyzed by combining Fourier analysis with the RMT (nakayamai2009rmt, ).

In this study, we further develop the noise elimination method initiated in previous studies. The null hypothesis that has been adopted thus far for extracting true mutual correlations corresponds to shuffling time series data in a completely random manner. Although we should distinguish between mutual correlations and autocorrelations, both these correlations are destroyed at the same time by the completely random shuffling. To solve this problem, rotational random shuffling of data in the time direction is introduced as an alternative null hypothesis; such randomization preserves autocorrelations involved in the original data. The new null hypothesis thus elucidates the concept of noise elimination for mutual correlations.

Further, we borrow the concept of the fluctuation-dissipation theory (Landau1980, ) from physics to elucidate the interindustrial relationship and the response of an economic system to external stimuli. The theory establishes a direct relationship between the fluctuation properties of a system in equilibrium and its linear response properties. We assume that the validity of the fluctuation-dissipation theory in physical systems is also true for such an exotic system as described by the IIP. Very recently, dynamics of the macroeconomy has been studied in the linear response theory by taking an explicit account of heterogeneity of microeconomic agents (HA2008, ).

The present paper is organized as follows. In Sec. II, we first provide a brief review of the noise elimination from the IIP using the RMT. A new null hypothesis based on rotational random shuffling is introduced in Sec. III. Section IV presents construction of a genuine correlation matrix for the IIP by consideration of only those dominant modes that are approved to be statistically meaningful by the RMT. We present development of a fluctuation-dissipation theory for input-output interindustrial relations in Sec. V. Then, in Sec. VI, we quantitatively discuss relationship between shipments of final demand goods and production of intermediate goods. In Sec. VII, we elucidate response of the industrial activities to external stimuli by subtracting long-period components arising from inherent business cycles from moving average fluctuations in the original data. Section VIII concludes this paper.

II Application of Random Matrix Theory to IIP

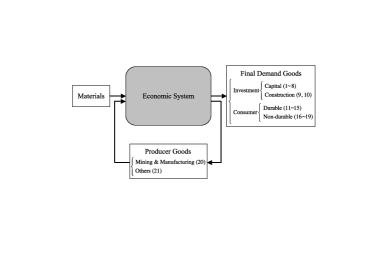

In Japan, the IIP are announced monthly by the Ministry of Economy, Trade and Industry (iip, ). For this study, we will choose seasonally adjusted data instead of original data. Two classification schemes of the IIP are available: indices classified by industry and indices classified by use of goods. We adopt the latter classification scheme because we are interested in input-output interindustrial relations here, which are measured by correlations between shipments of final demand goods and production of intermediate goods in the IIP data. The concept is illustrated in Fig. 1. We emphasize that the inner loop of production existing in the economic system may give rise to a nonlinear feedback mechanism to complicate the dynamics of the system; outputs are reused by the system as inputs for its production activities. Table 1 lists the categories 111See reference (bc, ) for details on the classification. of goods along with weights assigned to each of them for computing the average IIP. These weights are proportional to value added produced in the corresponding categories, and their total sum amounts to 10,000. Unfortunately, the resolution of the IIP data for the producer goods is quite poor, which are just categorized as Mining & Manufacturing and Others.

| Final Demand Goods (4935.4) | ||

| Investment Goods (2352.5) | ||

| Capital Goods (1662.1) | 1 | Manufacturing Equipment (530.7) |

| 2 | Electricity (148.1) | |

| 3 | Communication and Broadcasting (48.8) | |

| 4 | Agriculture (31.0) | |

| 5 | Construction (129.6) | |

| 6 | Transport (381.3) | |

| 7 | Offices (175.4) | |

| 8 | Other Capital Goods (217.2) | |

| Construction Goods (690.4) | 9 | Construction (568.1) |

| 10 | Engineering (122.3) | |

| Consumer Goods (2582.9) | ||

| Durable Consumer | 11 | House Work (62.3) |

| Goods (1267.9) | 12 | Heating/Cooling Equipment (62.5) |

| 13 | Furniture & Furnishings (43.4) | |

| 14 | Education & Amusement (246.5) | |

| 15 | Motor Vehicles (853.2) | |

| Nondurable | 16 | House Work (649.7) |

| Consumer Goods (1315.0) | 17 | Education & Amusement (105.2) |

| 18 | Clothing & Footwear (92.2) | |

| 19 | Food & Beverage (467.9) | |

| Producer Goods (5064.6) | ||

| 20 | Mining & Manufacturing (4601.7) | |

| 21 | Others (462.9) | |

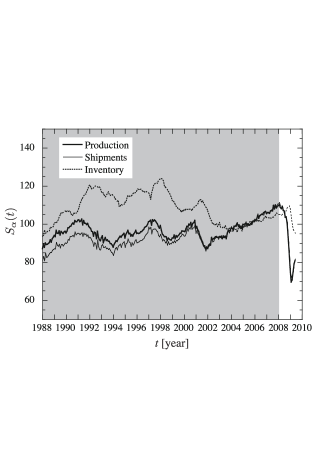

Figure 2 shows temporal change of the averaged IIP data for production, shipments, and inventory during the period of January 1988 to June 2009. The ongoing global recession is traced back to the subprime mortgage crisis in the U.S., which became apparent in 2007. The economic shock has affected Japan without exception, leading to a dramatic drop in the production activities of the country, as shown in the figure.

Since some of the entries, such as and , are missing before January 1988, we use the data (iip, ) for the 240 months from January 1988 to December 2007. Further, this chosen period for the study excludes the abnormal behavior of the IIP data due to The Great Recession. We denote the IIP data for goods as , where and for production (value added), shipments, and inventory, respectively. Similarly, denotes the 21 categories of goods, and with month and ; and correspond to 1/1988 and 12/2007, respectively. The logarithmic growth rate is defined as

| (1) |

where runs from 1 to . Then, it is normalized as

| (2) |

where denotes average over time and is the standard deviation of over time. Definition (2) ensures that the set has an average of zero and a standard deviation of one.

Figure 3 shows an overview of how the volatility of the standardized IIP data behaves on a time-goods plane. Unfortunately, the visualization does not allow for detecting any correlations involved in the IIP data. One may even doubt whether useful information on interindustrial relations truly exists in the data.

To answer the obvious question that would arise here, we begin with calculating the equal-time correlation matrix of according to

| (3) |

whose diagonal elements are unity by definition of the normalized growth rate . Since () runs from 1 to 3 and () runs from 1 to 21, the matrix has () components. We denote the eigenvalues and the corresponding eigenvectors of the correlation matrix as and , respectively:

| (4) |

where the eigenvalues are sorted in descending order of their values and the norm of eigenvectors is set to unity.

On the basis of the eigenvectors thus obtained, the normalized growth rate can be decomposed into

| (5) |

The correlation matrix is also decomposable in terms of the eigenvalues and eigenvectors as

| (6) |

The eigenvalues satisfy the following trace constraint:

| (7) |

By substituting Eq. (5) into Eq. (3) and comparing it with Eq. (6), we find that

| (8) |

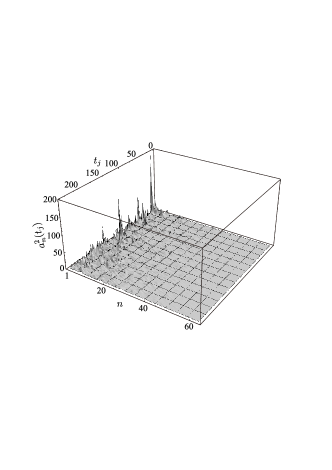

The eigenvalue of each eigenmode thus represents the strength of fluctuations associated with the mode. Figure 4 shows the temporal variation of , which is in sharp contrast to the results shown in Fig. 3. The transformation of the base for describing the IIP data reveals that very few degrees of freedom actually are responsible for the complicated behavior of the IIP.

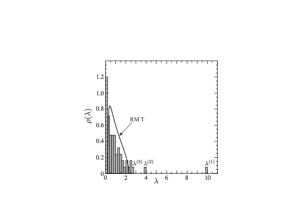

Thanks to the RMT, we are able to quantify how many eigenmodes should be considered. Probability distribution function for the eigenvalues () of the correlation matrix is shown in Fig. 5. It is compared with the corresponding result (sengupta1999dsv, ) of the RMT in the limit of infinite dimensions:

| (9) |

where and the upper and lower bounds for are given as

| (10) |

We see that the largest and the second largest eigenvalues, designated as and , are well separated from the eigenvalue distribution predicted by the RMT, whereas the third largest eigenvalue is adjacent to the continuum. Therefore, only 2 eigenmodes out of a total of 63 are of statistical significance according to the RMT.

Readers may be curious about the present construction of a correlation matrix by mixing up data for production, shipments, and inventory, because these are very different species of data at first glance. Thus far, physicists have applied the RMT mainly to analyses of stock data having similar characteristics. In this sense our approach is quite radical. However, production, shipments, and inventory form a trinity in the economic theory for business cycles, so that those variables should be treated on an equal footing. Using the two dominant eigenmodes, in fact, we were successful in proving the existence of intrinsic business cycles (bc, ).

In passing, we note that one may favor the growth rate itself defined by

| (11) |

for the present analysis over the logarithmic growth rate (1). If the relative change in is small, we need not distinguish between Eqs. (1) and (11) numerically. To confirm that the results obtained here are insensitive to the choice of stochastic variables, we repeated the same calculation by using Eq. (11) and found no appreciable difference between the two calculations for the dominant eigenvalues and their associated eigenvectors. For instance, the first three largest eigenvalues 9.95, 3.83, and 2.77 as shown in Fig. 5 are replaced with 9.96, 3.73, and 2.78, respectively.

III Rotational Random Shuffling

There are two major sources of noise in the IIP data. One of them, corresponding to thermal noise in physical systems, arises from elimination of a large number of degrees of freedom from our scope as hidden variables. This highlights the stochastic nature of the IIP and has a strong influence on autocorrelation of all goods. The other source of noise originates from the finite length of time series data. Such statistical noise hinders the detection of correlations among different goods in the IIP data. If one could have data of infinite length, statistical noise would disappear in the mutual correlations and only thermal noise would remain. These two types of noise should be distinguished conceptually. The RMT is an effective tool for eliminating statistical noise from raw data to extract genuine mutual correlations.

However, the noise reduction method based on the RMT heavily depends on the following assumption: stochastic variables would be totally independent if correlations between different variables were switched off. Such a null hypothesis simultaneously excludes both autocorrelations and mutual correlations. In the case of daily change in Japanese stock prices that were available (nakayamai2009rmt, ) to us, we found no detectable autocorrelations in the corresponding variables; therefore, the RMT functions ideally. In contrast, the IIP data have significant autocorrelations as shown in Fig. 6, where the autocorrelation function of the normalized growth rate is defined as

| (12) |

By definition, , and if there are no autocorrelations, for . We observe that both production () and shipments () have nontrivial values of autocorrelations at month, whereas there is no clear evidence for autocorrelations for inventory () in the same time interval; the values averaged over 21 goods are , , and . Beyond the one-month time lag, however, we find no appreciable autocorrelations for any of these three categories.

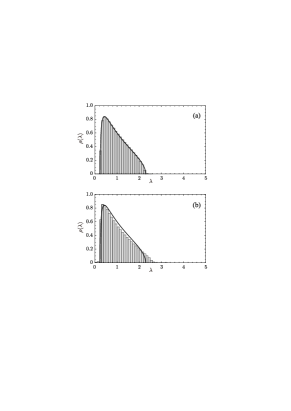

To formulate the null hypothesis of the RMT using actual data, one may shuffle the IIP data completely in the time direction. In fact, the eigenvalue distribution of the resulting correlation matrix reduces to that of the RMT as demonstrated in panel (a) of Fig. 7, where a total of samples were generated. Departure from the RMT owing to finiteness of the data size is almost negligible even for such small-scale data as the IIP. This randomization process inevitably destroys both autocorrelations and mutual correlations. From a methodological point of view, it is favorable to deal with these two types of correlations separately.

We instead propose to shuffle the data rotationally in the time direction, imposing the following periodic boundary condition on each of the time series:

| (13) |

where is a (pseudo-)random integer and is different for each and . This randomization destroys only the mutual correlations involved in the data, with the autocorrelations left as they are; therefore, it provides us with a null hypothesis more appropriate than that of the RMT.

Panel (b) of Fig. 7 shows the result in rotational shuffling with the same number of samples as that in the complete shuffling. We find that the existence of autocorrelations alone leads to departure from the RMT. The third largest eigenvalue becomes even closer to the upper limit, , of the eigenvalues obtained on the basis of the alternative null hypothesis, where the error is estimated at 95% confidence level. This result reinforces neglect of the third eigenmode by the RMT.

Thus, this new method for data shuffling conceptually clarifies noise elimination for the correlation matrix, although the difference in the eigenvalue distribution from that of the RMT is practically not very dramatic. In addition, we note that the rotational shuffling of the stock price data in Japan reproduces the RMT result quite well, as is expected from the fact that no appreciable autocorrelations are observed there.

IV Genuine Correlation Matrix

In the current system of IIP data, the above careful arguments permit us to adopt

| (14) |

as a genuine correlation matrix, which consists of just the first and second eigenvector components in the spectral representation (6) of plus the diagonal terms, thereby ensuring that all the diagonal components are 1. We note that self-correlations of stochastic variables always exist even if they are merely noise. The components of are explicitly written as

| (15) |

The eigenvectors and , associated with and , are shown in panels (a) and (b) of Fig. 8, respectively. These two eigenvectors have characteristic features that distinguish them from each other. The eigenvector represents an economic mode in which production and shipments of all goods expand (shrink) synchronously with decreasing (increasing) inventory of producer goods. This corresponds to the market mode obtained for the largest eigenvalue in the stock market analyses (laloux1999ndf, ; plerou1999uan, ), and may be referred to as the “aggregate demand” mode according to Keynes’ principle of effective demand: both shipments and production in all the sectors are moved jointly by aggregate demand (Keynes1936, ). On the other hand, the eigenvector is a mode that apparently represents dynamics of inventory, i.e., accumulation or clearance of inventory, for most goods, including producer goods. We further find positive correlation between production enhancement and inventory accumulation for most goods. This finding indicates that production has a kind of inertia in its response to change of demands.

Accordingly, we project out raw fluctuations of onto the first and second eigenmodes; that is, only the first two terms are retained and the remaining terms are regarded as just noise in expansion (5):

| (16) |

This process extracts statistically meaningful information on mutual correlations among as has been already discussed in Secs. II and III. Collaboration of these two modes results in inherent business cycles with periods of 40 and 60 months throughout the economy. The cycles are accounted for by time lags in information flow between demand of goods by consumers and decision making of firms on production (bc, ); inventory fills this information gap. If we singled out the most dominant mode alone in Eq. (5), all would oscillate without phase difference. As will be shown later, each goods possesses its own characteristics in the phase relations among production, shipments, and inventory.

Temporal change of the two principal factors and is plotted in panel (a) of Fig. 9. Since the functional behavior of these variables is very noisy, we take their simple moving average defined as

| (17) |

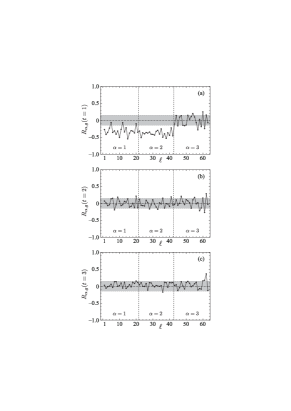

where is a characteristic time scale for smoothing. This process eliminates “thermal” noise present in the original data. Actually, the moving average was taken with ; the results for and are shown in panel (b) of Fig. 9. We see that the moving-average operation significantly reduces the level of noise present in . It is noteworthy that Fig. 9 indicates the existence of some mechanical relationship between and . This finding is ascertained more quantitatively from Fig. 10, in which the correlation coefficient between and ,

| (18) |

is plotted as a function of time lag . A correlation as large as 0.7 is detected between the two dominant modes around months. Detailed study of the underlying dynamics in the economic system is in progress and will be reported elsewhere.

V Fluctuation-Dissipation Theory

The fluctuation-dissipation theory plays a central role in nonequilibrium statistical mechanics because this theory establishes a general relation between fluctuation properties of a physical system in equilibrium and response properties of the system to small external perturbations. We assume that the theory still is applicable to the economic system under study here. This assumption provides us with a framework to derive input-output interindustrial relations in the system. Its validity in view of how the system responded to the recent economic crisis will be discussed later .

Let us denote our variable as , whose index runs from 1 to 63. We assume that obeys dynamics governed by a Hamiltonian , where is a set of “hidden” variables in the system, which encompass all variables in the current economics. These numerous variables interact with each other in a nonlinear chaotic way and hence, the temporal change of appears stochastic in the same way as that of a Brownian particle. The existence of underlying dynamics in the IIP (bc, ), as demonstrated in Figs. 9 and 10, strongly supports this idea borrowed from mechanics of motion.

Actually, however, the economy of a nation is quite open now; therefore, it could potentially be subjected to perturbations such as disasters, political issues, and trade issues. We thus add external forces to the system; then, the total Hamiltonian becomes

| (19) |

This extra term represents external perturbations to the equation of motion for :

| (20) | ||||

| (21) |

where is the momentum conjugate to . Therefore, directly affects at time , the effect of which then extends to other ’s through direct and indirect interactions among them.

For simplicity, let us assume that is constant in time. Thus, the perturbation set induces a static shift of the equilibrium positions of the variables , which otherwise move stochastically around the origin . If the perturbation is weak, the shift thus induced can be expressed by the following linear response relation:

| (22) |

where the ensemble average denoted by has replaced the time average. The coefficients are the result of the interactions, and they are called “magnetic susceptibility” while describing the physics of magnetic materials.

Once such a set of susceptibilities is available, we can quantify the response of the economic system to external perturbations. For instance, suppose that the government adopts an economic policy to increase the shipment of one of the final demand goods by with a stimulus . The resulting changes in production, shipments, and inventory of goods are given as

| (23) |

Since is not an observable quantity, it should be appropriate to eliminate appearing in Eq. (23) and express ripple effects on the economy in terms of as

| (24) |

In Sec. VI, we demonstrate that Eq. (24) can provide quantitative information on input-output interindustrial relations in Japan. Further, one may make reverse use of the linear response relation (22) to distinguish and detect external perturbation from observed economic changes in ; this is discussed in Sec. VII.

Now, the remaining problem is how to calculate . To this end, we invoke the concept of the fluctuation-dissipation (FD) theorem in statistical physics. If we assume that the stochastic process of is characterized by Gibbs’ ensemble, then the probability density function (PDF) for is given as

| (25) |

where the hidden variables have been integrated out and is the inverse “temperature” of the economic system. For a weak perturbation, Eq. (25) is expanded to the first order of as

| (26) |

where

| (27) |

is the PDF in the absence of . Equation (26) enables us to calculate the induced change in by as

| (28) |

where denotes the ensemble average without perturbation. Comparison of Eqs. (22) and (28) gives one of the outcomes of the FD theorem:

| (29) |

where denotes a correlation matrix in the absence of external perturbations.

Making use of Eq. (29), we can rewrite the relation (24) of economic ripple effects caused by the increase in shipments of final demand goods as

| (30) |

This is just one example of possible interindustrial relations derived from the present formulation. What we should emphasize here is that Eq. (30) has a rather general form in the framework of linear response.

For instance, we do not need to determine the temperature of the economic system for . Even the assumption of Gibbs’ ensemble, e.g., as given in Eqs. (25) and (27), may be too restrictive, because the assumption (26) about the PDF is sufficient to derive Eq. (30). We also recall Onsager’s regression hypothesis onsager1931a ; onsager1931b , on which the fluctuation-dissipation theorem relies. Once one accepts the hypothesis, one can readily derive Eq. (30). According to him, the response of a system in equilibrium to an external field shares an identical law with its response to a spontaneous fluctuation. In other words, the regression of spontaneous fluctuations at equilibrium takes place in the same way as the relaxation of non-equilibrium disturbances does. Let us suppose that the non-equilibrium disturbances and are linearly related through

| (31) |

Accordingly, the spontaneous fluctuations and satisfy the same relation as Eq. (31):

| (32) |

The ensemble average of Eq. (32) multiplied by on both hand sides determines the proportionality coefficient as

| (33) |

We thus see that Eq. (30) is directly derivable from Onsager’s hypothesis.

We note that the correlation matrix appearing in Eqs. (29) and (30) should be measured for a system not subject to any perturbations. However, the genuine correlation matrix determined by Eq. (15) is possibly contaminated with various kinds of external economic shocks. While such forces may easily affect the stochastic motion of each , it is legitimate to assume that their influence on the correlations among ’s are much weaker; otherwise, the external factors would have to work coherently to change “springs” connecting pairs of ’s. This consideration justifies the replacement of in Eq. (30) with .

VI Interindustrial Relations

We are now in a position to quantitatively estimate the strength of the interindustrial relations by making use of the genuine correlation matrix through Eq. (30). In particular, we focus on ripple effects on production of intermediate goods that are triggered by applying an external stimulus to consumption of final demand goods:

| (34) |

| (35) |

with .

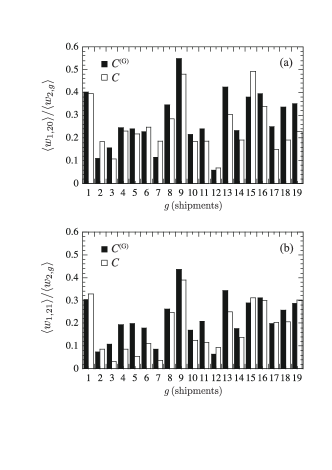

The results for production of intermediate goods for Mining & Manufacturing () are shown in the upper panel of Fig. 11, in which those obtained with the original correlation matrix are also added for comparison. This figure shows an increase in the logarithmic growth rate of production of intermediate goods that is predicted from unit increment of the logarithmic growth rate of shipments of each of the final demand goods. As expected, increase in shipments of final demand goods with large weights, as represented by Manufacturing Equipment (), Construction (), Motor Vehicles (), House Work (), and Food & Beverage (), certainly causes large ripple effects on the production of intermediate goods. If the original correlation matrix is replaced with the genuine one, then the relative importance of species of final goods is interchanged between Construction and Motor Vehicles. This is understandable because sales of cars are sometimes promoted just for inventory adjustment, having no effect on the growth of production of intermediate goods. We also note that the original correlation matrix significantly underestimates the effects of Furniture & Furnishing () and Nondurable Consumer Goods (). It is noteworthy that Furniture & Furnishing and Clothing & Footwear, having much smaller weights than the major final demand goods, have comparable contributions; some feedback mechanism must be working through the inner loop in the economic system.

The lower panel in Fig. 11 shows the corresponding results for production of intermediate goods for Others (), whose weight is one order of magnitude smaller than that of Mining & Manufacturing. The important species of final demand goods are common in both categories of intermediate goods. In contrast, the original correlation matrix significantly underestimates the effects of different final demand goods such as those given by to .

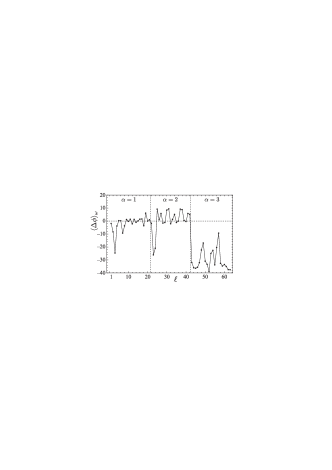

Presence of a correlation between two stochastic variables and does not indicate the existence of a mechanical connection between them. Actually, correlating and might be driven by a third variable ; then, there would be no causality relationship between and . To address this question, we provide detailed information on phase relations in the business cycles identified in the previous study bc . Table 2 lists phases of the cyclic motion of production, shipments, and inventory at and for each of the goods. We can see that shipments of final demand goods are ahead of or almost in phase with production of intermediate goods; the resolution limit (one month) is and for and , respectively. Electricity () and Communication & Broadcasting () are exceptions to this observation. The wave of production arrives first and then, that of shipments follows for Electricity; the production activity for Communication & Broadcasting behaves significantly out of phase with that averaged over goods. Since we have adopted a static approximation for the interindustrial relations, it may be more appropriate to average the phase relations over frequency. The results are shown in Fig. 12 and Table 3. The frequency-averaged phase relations in the cyclic behavior of the economic fluctuations thus support our postulate that production of intermediate goods is driven by increasing shipments of final demand goods with a few exceptions.

| Goods | P | S | I | P | S | I |

|---|---|---|---|---|---|---|

| Average | ||||||

| Final demand goods | Producer goods | ||

|---|---|---|---|

| P | () | ||

| S | () | ||

| I | () | ||

VII External Stimuli

Finally, we try to identify the presence of external stimuli hidden in real data by inversely using the linear response relationship (22). The recent global economic crisis certainly has delivered an extremely large shock to the economic system of Japan, as is clearly shown in Fig. 2. In our previous paper (bc, ), however, we demonstrated that the crisis has simply increased the level of fluctuations associated with the dominant modes that were determined from the data during the normal time, instead of destroying the industrial structure itself; this is also manifested here, as shown in Fig. 9. And the information on collective movement of the IIP that we could extract from the dominant modes remains intact even in such an abnormal situation. This result thus conforms to the idea of Onsager’s regression hypothesis, indicating the validity of the fluctuation-dissipation theory even in an economic system that is supposed to be far away from equilibrium.

Since approximation (15) has been adopted for the correlation matrix, we consider only two independent external fields that are coupled to the normal coordinates associated with the two dominant eigenmodes and , respectively. The total Hamiltonian (19) is therefore simplified to

| (36) |

The reduced external fields in Eq. (36) are derived from the original ones in Eq. (19) through

| (37) |

Then, Eq. (22) is projected onto the two-dimensional reduced state space as

| (38) |

where

| (39) |

and the reduced susceptibilities are defined as

| (40) |

The relative values of with reference to are calculated from as

| (41) |

This results shows that the two eigenmodes are almost decoupled from each other, which is understandable from the orthogonality (8) of the normal coordinates.

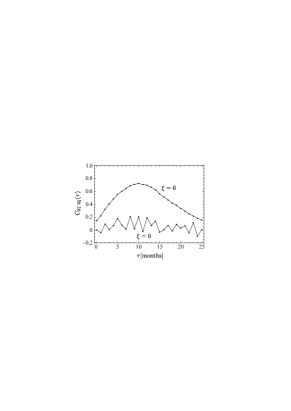

One can obtain using the inverse of Eq. (38) along with Eqs. (39) and (40), although it is not so straightforward. We first recall that in the right-hand side of Eq. (39) is the deviation of from the equilibrium value induced by external perturbation, and not fluctuations of directly observed in the real data. We then identify as residuals obtained by subtracting the long-period components arising from the inherent business cycles from moving average fluctuations of the IIP.

To extract , we first define the Fourier transform of the coefficients as

| (42) |

with the Fourier frequency and hence . The relevant long-period component is obtained by limiting the sum over only to (), (), (), and () or by summing all of the terms with periods larger than 2 years () in Eq. (42). The formula for is finally expanded as

| (43) |

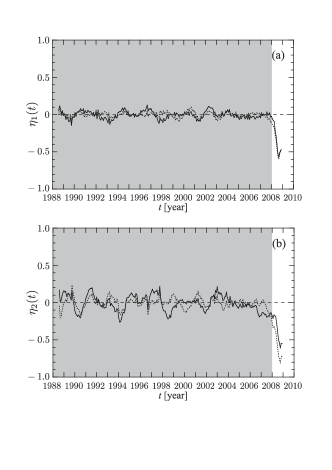

Figure 13, for which we arbitrarily set in Eq. (41), shows the external fields and thus derived from . Two computational schemes were adopted to evaluate the long-period components in the IIP data, and no appreciable difference was observed between the two results. Here, the economic system was assumed to respond instantaneously to the applied external fields without any time delay. Referring to Fig. 2, we clearly confirm that such a large external shock as manifested in causes the drastic drop in industrial activities in Japan. We also see that another large shock in , which leads to reduction in inventory, immediately accompanies the first shock. In contrast, the maximum fluctuation levels of and are 0.1 and 0.2, respectively, in the normal period (before the end of 2007).

VIII Conclusion

This paper has described our attempt to utilize the fluctuation-dissipation theory for elucidating the nature of input-output correlations in the Japanese industry on the basis of IIP data. We were able to quantitatively estimate the strength of correlations between goods by using the genuine correlation matrix obtained in this study. We were also successful in extracting external stimuli over the last two decades. The noise reduction along with the RMT enabled us to detect economic signals hidden behind the complicated dynamics of the IIP. The strong coincidence between the sudden change in IIP data and the external shocks described here may prove that the present method is capable of predicting the input-output interindustrial relationship with a much higher time resolution than the annual resolution. We thus expect the results of this study to provide a new methodology for gaining deeper understanding of complex economic phenomena at a macroscopic level.

Acknowledgements.

The present study was supported in part by the Program for Promoting Methodological Innovation in Humanities and Social Sciences by Cross-Disciplinary Fusing of the Japan Society for the Promotion of Science and by the Ministry of Education, Science, Sports and Culture, Grants-in-Aid for Scientific Research (B), Nos. 20330060 (2008-10) and 22300080 (2010-12). We would also like to thank Hiroshi Yoshikawa for providing continual advice and encouragement.References

- (1) H. Iyetomi, Y. Nakayama, H. Yoshikawa, H. Aoyama, Y. Fujiwara, Y. Ikeda, and W. Souma, arXiv:0912.0857(2009)

- (2) W. Leontief, Rev. Econ. Statist. 18, 105 (1986)

- (3) W. Leontief, Input-Output Economics, 2nd ed. (Oxford University Press, New York, 1986)

- (4) L. Walras, Elements of Pure Economics (Allen and Unwin, London, 1954)

- (5) R. Mantegna and H. Stanley, An Introduction to Econophysics: Correlations and Complexity in Finance (Cambridge University Press, Cambridge, 2000)

- (6) J. Bouchaud and M. Potters, Theory of financial risks: from statistical physics to risk management, 2nd ed. (Cambridge University Press, Cambridge, 2003)

- (7) M. Aoki and H. Yoshikawa, Reconstructing Macroeconomics: A Perspective from Statistical Physics and Combinatorial Stochastic Processes (Cambridge University Press, New York, 2007)

- (8) H. Aoyama, Y. Fujiwara, Y. Ikeda, H. Iyetomi, and W. Souma, Econophysics and Companies: Statistical Life and Death in Complex Business Networks (Cambridge University Press, Cambridge, 2010)

- (9) L. Laloux, P. Cizeau, J. P. Bouchaud, and M. Potters, Phys. Rev. Lett. 83, 1467 (1999)

- (10) V. Plerou, P. Gopikrishnan, B. Rosenow, L. A. N. Amaral, and H. E. Stanley, Phys. Rev. Lett. 83, 1471 (1999)

- (11) V. Plerou, P. Gopikrishnan, B. Rosenow, L. A. N. Amaral, T. Guhr, and H. E. Stanley, Phys. Rev. E 65, 66126 (2002)

- (12) A. Utsugi, K. Ino, and M. Oshikawa, Phys. Rev. E 70, 26110 (2004)

- (13) D. H. Kim and H. Jeong, Phys. Rev. E 72, 46133 (2005)

- (14) V. Kulkarni and N. Deo, Europhys. J. B 60, 101 (2007)

- (15) R. K. Pan and S. Sinha, Phys. Rev. E 76, 046116 (2007)

- (16) J. Shen and B. Zheng, Europhys. Lett. 86, 48005 (2009)

- (17) Y. Nakayama and H. Iyetomi, Prog. Theor. Phys. Suppl. 179, 60 (2009)

- (18) L. D. Landau and E. M. Lifshitz, Statistical Physics, Part 1, 3rd ed. (Butterworth-Heinemann, Oxford, 1980)

- (19) R. J. Hawkins and M. Aoki, Economics: The Open-Access, Open-Assessment E-Journal 3 (2009), http://www.economics-ejournal.org/economics/journalarticles/2009-17

- (20) METI, Japan, “Indices of Industrial Production, Producer’s Shipments, Producer’s Inventory of Finished Goods, and Producer’s Inventory Ratio of Finished Goods,” http://www.meti.go.jp/english/statistics/tyo/iip /index.html (2010)

- (21) See reference (bc, ) for details on the classification.

- (22) A. M. Sengupta and P. P. Mitra, Phys. Rev. E 60, 3389 (1999)

- (23) J. M. Keynes, The General Theory of Employment, Interst and Money (Macmillan, London, 1936)

- (24) L. Onsager, Phys. Rev. 37, 405 (1931)

- (25) L. Onsager, Phys. Rev. 38, 2265 (1931)