On the density of the sum of two independent Student t-random vectors

Abstract

In this paper, we find an expression for the density of the sum of two independent dimensional Student random vectors and with arbitrary degrees of freedom. As a byproduct we also obtain an expression for the density of the sum , where is normal and is an independent Student vector. In both cases the density is given as an infinite series

where is a sequence of probability densities on and is a sequence of positive numbers of sum , i.e. the distribution of a non-negative integer-valued random variable , which turns out to be infinitely divisible for and When and the degrees of freedom of the Student variables are equal, we recover an old result of Ruben.

1 Introduction

The Student distributions plays an important role in statistics for the analysis of normal samples. One of the major properties of these distributions is their heavy-tail behaviour; the same behaviour is shown by the famous family of stable distributions. The Student t-distributions show the advantage of having an explicit expression, what allows for example to write down explicitly their likelihood function [4]; this is not the case for the stable distributions, except some well-known particular cases.

However, except in the Gaussian and Cauchy case, the Student t-distributions show the drawback of not being stable by convolution. Thus the study of their behavior by convolution is of high interest. This study has been first addressed in [15] and more recently in [17, 6], but concerns only the case where the degrees of freedom is an odd integer. The study of Student t-processes has recently given rise to a series of studies [8, 7, 11].

The dimensional Student density with degrees of freedom is

In the following, we provide an expression for the density of the sum

where and are variate independent distributed random variables with respective degrees of freedom and . When and this equals an expression found by Ruben, cf. [14, formula 3.4]. As a byproduct, we also obtain an expression for the density of

where is standard Gaussian. Moreover, we extend this result to the case of with . In all cases, our expression is an infinite convex combination of a sequence of variate densities, which we describe next.

Let us introduce the family of densities

| (1) |

with We remark that is the variate Gaussian density with zero mean and covariance matrix for , by [9, Th. 2.9], is the density of where is a Gaussian vector with identity covariance matrix and is uniformly distributed on the unit sphere of and independent of

Let us also introduce the family of densities

| (2) |

where We note that, with the same notation as above, is the density of where follows a multivariate Student t-distribution with degrees of freedom

At last, we recall that a discrete random variable follows a negative binomial distribution with parameters and (denoted as ) if

distributions with non-integer parameter are also known as Pólya distributions.

2 Results

The distribution of the sum of two independent Student vectors

can be deduced by subordination from the distribution of where is Gaussian : if denotes the inverse Gamma measure with scale parameter and shape parameter

and if denotes the variate Gaussian semi-group of normal densities

then the Student density can be obtained as the mixture

Therefore, we begin by finding an expression for the density of .

2.1 The sum of a Gaussian and a Student vector

Our first result states as follows.

Theorem 1.

The density of can be written

| (3) |

where the densities are defined in (1), are positive coefficients that sum to and given by

| (4) |

and is defined as

| (5) |

Proposition 2.

The same result as in Theorem 1 holds for replacing by and by

Note that and have the same distributions as and respectively, so that we only need to consider the case in the above Proposition.

2.2 The sum of two Student vectors

Starting from the distribution (3) we obtain the following

Theorem 3.

The distribution of where and are independent distributed with respective degrees of freedom and can be written as the infinite convex combination

| (6) |

where are the probability densities given by (2) and are positive coefficients that sum to defined by

| (7) |

Note that (7) shows that as is to be expected.

Remark 1.

The Fourier transform of the Student density in the case is

| (8) |

with

where is the MacDonald function.

We claim that

| (9) |

In fact, from (8), we get

which is (9) because

Theorem 3 can be expressed for as

hence by (9)

and finally by (7), for

with

In terms of the Macdonald function, this equation can be written

We have not been able to find this expression in the literature.

Still another interpretation of formula (6) for is to rewrite it as

which shows that has a holomorphic extension to the open set which is the region between the two branches of the equilateral hyperbola

Remark 2.

In [14], Ruben shows that in the dimensional case, the density of the convolution can be written as a mixture of scaled Student t-distributions with degrees of freedom, i.e. as

for some probability density on . This representation differs from (6) which is a discrete mixture of the densities (2). In the same paper, Ruben obtains several expressions for the density in the case Ruben’s formula (3.4) coincides with formula (6) in the special case

3 Properties of the mixing distributions

3.1 Stochastic interpretation

Since, as a consequence of (4), the coefficients are positive, and since they sum to 1 (see Theorem 7), a stochastic interpretation of Theorem 1 is as follows:

where, given has the conditional density (1) and is a discrete random variable with

| (10) |

We deduce the following

Proposition 4.

The sum is distributed as where

-

1.

vector is uniformly distributed on the unit sphere in

-

2.

vector is Gaussian with identity covariance matrix,

-

3.

random variable defined by (10) follows a compound negative binomial distribution where the parameter is Gamma distributed with scale parameter and shape parameter (in short ) so has the density

An analogous result in the case of the sum of two Student t-vectors is as follows: is distributed as a random variable such that, given has the conditional density given by (2) and is a discrete random variable defined by

| (11) |

We deduce the following

Proposition 5.

The sum is distributed as where

-

1.

vector is uniformly distributed on the sphere in

-

2.

random vector is Student t-distributed with degrees of freedom

-

3.

random variable defined by (11) follows a compound negative binomial distribution where the parameter follows a Beta distribution with parameters and

3.2 Hausdorff moment sequence

A sequence is called a Hausdorff moment sequence if it has the form

for some positive measure It is called normalized if The following result holds:

Theorem 6.

Both sequences and are Hausdorff moment sequences for and

3.3 Mean and Variance

The first and second order moments of these distributions can be easily computed as a consequence of the fact that they are compound distributions.

Theorem 7.

The distribution (10) of verifies

In the case of the sum of Student t- variables, we have

Theorem 8.

The distribution (11) of verifies

3.4 Asymptotic behaviors

3.4.1 fixed value of

Let us now study the asymptotic behavior of the distribution (3) for large value of the degrees of freedom note that the two next theorems can be checked directly by looking at the stochastic representation of as given in Proposition 4, but their proofs are instructive by themselves.

Theorem 9.

For a fixed value of the parameter

We note that this result is a consequence of the fact that since has covariance matrix the random variable has the same distribution as as

3.4.2 covariance matrix of fixed

Let us now look at the asymptotic behavior of these coefficients for large values of but for a fixed value of the covariance matrix of since has covariance matrix let us consider

| (12) |

where has covariance matrix and has covariance matrix . Define

so that

| (13) |

Theorem 10.

The coefficients in (13) behave for large as

As a consequence, the density of converges to a Gaussian density with covariance matrix , as expected.

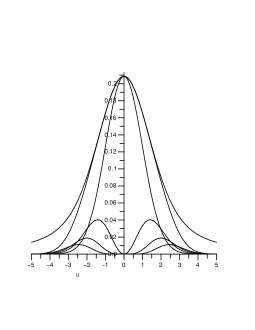

In Fig.1 are shown the succesive terms of the approximation of the density of in the one-dimensional case (): the upper curve is the density the second one is the approximation of by the sum of the four first terms in (3), and the four lower curves are the successive terms of this sum for and The first term (Gaussian density) fits around but the tail is underestimated; the other terms contribute to correct this underestimation, each adding, as increases, a smaller contribution farther from the origin.

4 Proofs

4.1 Proof of Theorem 1

Using a result by Keilson and Steutel [12], a stochastic representation for the random variable is

where is variate standard normal, is Gamma distributed and denotes equality in distribution. The density of reads thus

| (14) |

Since with , we deduce

where the interchange of the sum and the integral is justified by the Lebesgue monotone convergence theorem. Since, using [10, 4.642],

which is equal to the function as defined by (1) is a probability density and the result follows. Using the Kummer function

| (15) |

cf. [10, p.1085], the integral in the expression of can be written

| (16) |

4.2 Proof of Proposition 2

We have

with so that and

but so that the result holds.

4.3 Proof of Theorem 3

Let us define so that and consider the th term in the convex combination (3)

putting and subordinating with the inverse Gamma distribution yields

By the change of variable this is equal to

and, since the latter integral is a Gamma integral, to

The latter integral can be identified as Euler’s integral representation of a hypergeometric function [3, Th. 2.2.1 p.65]

so that, using Pfaff’s formula [3, 2.2.6 p.68]

we deduce

Replacing the hypergeometric function by its series, we deduce

where the density is defined by (2) and the coefficient is equal to

using the identity twice. Writing and we deduce

Now the density of is the sum over of these terms and reads

We perform the change of variable to obtain

The inner sum can be written

where we have used the identity

By the Chu-Vandermonde identity [3, p.70]

and using the identities and we deduce

where we have used the change of summation index and where the trinomial [2] coefficient is

Writing and and replacing the resulting Beta function by its integral representation we obtain

and since the generating function of the trinomial coefficient is

we finally obtain

which is the desired result.

4.4 Proof of Theorem 6

In the case of the coefficients we can factorize

where

This expression shows that the sequence is also a Hausdorff moment sequence (not normalized) and hence is a Hausdorff moment sequence for as product of two such sequences. It is not normalized since In fact, is trivially a Hausdorff moment sequence when and for we have

It is a general fact that is a Hausdorff moment sequence when see [5, formula (26)] and if then is not even a Hamburger moment sequence since the Hankel determinant

This shows that the density (3) is an infinite convex combination of the densities (1) and the discrete probability is infinitely divisible for since the sequence is completely monotonic, which is the same as being a Hausdorff moment sequence.

In the case of the sequence we find

As before is a Hausdorff moment sequence for .

4.5 Proof of Theorem 7

Although the first result can be obtained by integrating (3) over we check it directly since the computation of the sum is instructive by itself. For any we have by the binomial series

| (19) |

so that, with ,

and we deduce

The expectation and variances are easily computed from the stochastic representation of the mean of a negative binomial variable being

since is Since moreover, the second order moment of a negative binomial is a straightforward computation gives

and

4.6 Proof of Theorem 8

The fact that the coefficients sum to is proved in the same way as in the Proof of Theorem 7; the expectation is computed accordingly as

with

The second order moment is similarly computed as

so that the variance reads

and the result follows after simplification.

4.7 Proof of Theorem 9

It is clearly enough to prove that since for . We have

hence

for some by the mean value theorem. For we therefore get

which tends to 0 for .

4.8 Proof of Theorem 10

The coefficients read

using change of variable Let us apply Laplace’s method [16, p.278]: if and then for large ,

Choosing and , an equivalent of the right-hand side integral reads

Thus an equivalent of the coefficients reads

which, by Stirling’s formula, is equivalent to

As a consequence, for large values of , the density of reads

with

4.9 Proof of Proposition 4

Conditionnally to a given value of the random variable follows the distribution ; let us check that the random variable follows a compound distribution where is : conditionnally to such a compound distribution reads

so that

by the change of variable this expression coincides with (4).

4.10 Proof of Proposition 5

Conditionnally to a value of the random variable follows the distribution we check that the random variable follows a where follows a Beta distribution with parameters and : conditionnally to this compound distribution reads

so that

which coincides with (7).

Acknowledgements

The work of the first author has been supported by grant 272-07-0321 from the Danish Research Council for Nature and Universe. CV thanks CB for his invitation to the University of Copenhagen in February 2009. The paper was finished during a stay of the first author as Guest Professor at University of Marne la Vallée in May 2009.

References

- [1] M. Abramowitz, I. Stegun, Handbook of Mathematical Functions: with formulas, Graphs, and Mathematical Tables, Dover Publications, 1965.

- [2] G. Andrews, Euler’s ’exemplum memorabile inductionis fallacis’ and Trinomial Coefficients, J. Amer. Math. Soc. 3, 653–669, 1990.

- [3] G. E. Andrews, R. Askey, and R. Roy, Special Functions, Cambridge University Press, Cambridge, UK, 1st ed., Feb. 1999.

- [4] V. E. Bening, V. Yu. Korolev, On an application of the Student distribution in the theory of probability and mathematical statistics, Theory Probab. Appl., Vol. 49, No. 3 (2005), 377–391.

- [5] C. Berg, On powers of Stieltjes moment sequences, II, J. Comput. Appl. Math., Vol. 199 (2007), 23–38.

- [6] C. Berg, C. Vignat, Linearization Coefficients of Bessel Polynomials and Properties of Student t-Distributions, Constructive Approximation, Vol. 27 (2008), 15–32.

- [7] C. Berg, C. Vignat, On some results of Cufaro Petroni about Student t-processes, J. Phys. A: Math. Theor. 41 (2008) 265004.

- [8] N. Cufaro Petroni, Mixtures in nonstable Lévy processes, J. Phys. A: Math. Theor. 40 (2007), 2227–2250.

- [9] K.-T. Fang, S. Kotz, K. W. Ng, Symmetric Multivariate and Related Distributions, Monographs on Statistics and Applied Probability, Chapman & Hall/CRC, 1989.

- [10] I. S. Gradshteyn, I. M. Ryzhik, Table of Integrals, Series, and Products, Seventh Edition, Academic Press, 2007.

- [11] C. C. Heyde, N. N. Leonenko, Student Processes, Adv. Appl. Prob. 37 (2005), 342–365.

- [12] J. Keilson, F.W. Steutel, Mixtures of Distributions, Moment Inequalities and Measures of Exponentiality and Normality, Annals of Probability, Volume 2, Issue 1, Feb. 1974, 112–130.

- [13] G. P. Nason, On the sum of and Gaussian random variables, Statistics and Probability Letters 76 (2006) 1280.

- [14] H. Ruben, On the distribution of the weighted difference of two independent Student variables. J. Roy. Statist. Soc. Ser. B, 22 (1960), 188–194.

- [15] G.A. Walker, J.G. Saw, The Distribution of Linear Combinations of -Variables. Journal of the American Statistical Association, Vol. 73, Issue 364, Dec. 1978, 876–878.

- [16] D.V. Widder, The Laplace Transform, Princeton University Press, 1946.

- [17] V. Witkovský, Exact distribution of positive linear combinations of inverted chi-square random variables with odd degrees of freedom. Statistics and Probability Letters 56 (2002), 45–50.