22institutetext: Sayantan Ghosh, The Insitute of Mathematical Sciences, C.I.T. Campus, Taramani, Chennai 600 113, India.333sayantan@imsc.res.in

33institutetext: P. Manimaran, Center for Mathematical Sciences, C R Rao Advanced Institute of Mathematics, Statistics and Computer Science, HCU campus, Hyderabad 500 046, India.444rpmanimaran@gmail.com

44institutetext: Dilip P. Ahalpara, The Insitute for Plasma Research, Bhat, Gandhinagar, 382 428, India.555dilip@ipr.res.in

Statistical Properties of Fluctuations: A Method to Check Market Behavior

Abstract

We analyze the Bombay stock exchange (BSE) price index over the period of last 12 years. Keeping in mind the large fluctuations in last few years, we carefully find out the transient, non-statistical and locally structured variations. For that purpose, we make use of Daubechies wavelet and characterize the fractal behavior of the returns using a recently developed wavelet based fluctuation analysis method. the returns show a fat-tail distribution as also weak non-statistical behavior. We have also carried out continuous wavelet as well as Fourier power spectral analysis to characterize the periodic nature and correlation properties of the time series.

1 Introduction

Financial markets are known to show different behavior at different time scales and under different socio-economic conditions. The random behavior of fluctuations in the smaller time scales and the manifestation of structured behavior at intermediate and long time scales have been well studied plerou -mandel . Many of the stock markets have shown large scale fluctuations during the past three years. Here we concentrate on the behavior of the fluctuation of the Bombay stock exchange (BSE) high price values in daily trading. The point that makes the analysis of the BSE price index interesting is the fact that it has a significant fluctuations on a shorter time scale while growing tremendously over a longer time period. The statistical properties of the fluctuations and the behavior of the returns of such a growing market are of particular interest. Wavelet transform daub -ram based multi-resolution analysis mani1 ; mani3 has been successfully used earlier to analyze time series from various areas drozdz -mani4 .

In this work, we analyze the BSE high price index value using both continuous and discrete wavelet transform and multifractal detrended fluctuation analysis (MF-DFA) khu -mohaved . We use the continuous wavelet transform (CWT) to analyze the behavior of the time series at different frequencies and extract the periodic nature of the series if existent. The discrete wavelet transform based method is used to find the multifractal nature of the time series. For the purpose of comparison, the MF-DFA method is used for characterization of the time series. It has been observed in mani2 that BSE returns showed a Gaussian random behavior and certain non-statistical features.

The present work is organized as follows. Section 2 contains a brief description and applications of the continuous and discreet wavelet transforms. The discrete wavelet based method mani4 to analyze fluctuations is reviewed in section 3. In section 4, the data is analyzed through the wavelet based method, MF-DFA and Fourier analysis. We conclude in section 5 with results and a brief discussion.

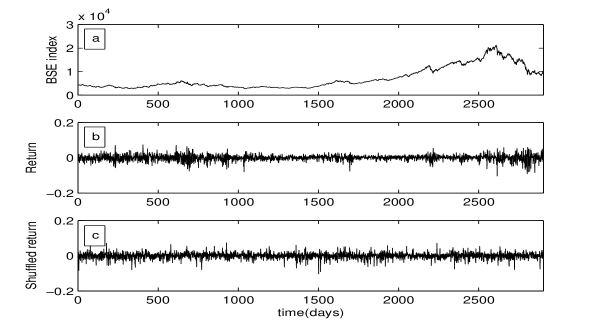

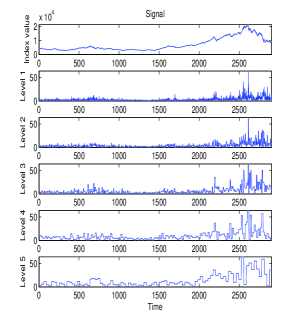

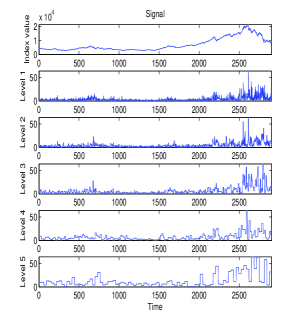

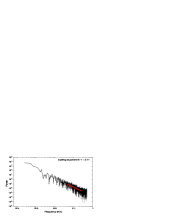

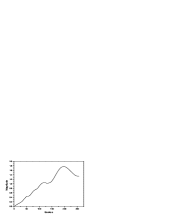

The BSE index yahoo dates from July 01, 1997 to March 31, 2009. The data spans over 2903 points and is shown in Fig.1(a). As is evident from the data, the first half does not show much activity but the second half shows significant variations. Fig.1(b) depicts the logarithmic returns calculated from (6) and Fig.1(c) depicts the shuffled returns, which reveals some differences with the returns.

2 Continuous wavelet analysis through Morlet wavelet

Continuous Wavelet Transform (see farge and torrence for an excellent introduction to the topic) has been used in recent times to analyze financial time series to study self-organized criticality bartolozzi_1 ; bartolozzi_2 , correlations struzik ; awc , commodity prices connor to name a few. Recently, in dilip , an effort towards the characterization of cyclic behavior in the financial markets has been made through the multi resolution analysis of wavelet transforms. Here, the CWT of the BSE data has been carried using the Morlet wavelet given by morlet ,

| (1) |

where is a localized time index, for zero mean and localization in both time and frequency space (admissibility conditions for a wavelet) farge . The Morlet wavelet has a Fourier wavelength torrence given by

| (2) |

which means that here, the scale and the Fourier wavelength are approximately equal. The wavelet coefficients are calculated torrence by the convolution of a discrete sequence with scaled and translated ,

| (3) |

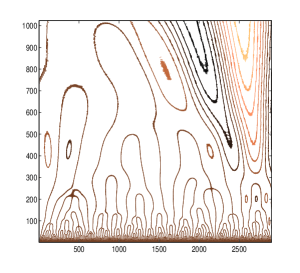

where is the scale. The wavelet coefficients for the BSE data has been given in a scalogram in Fig.2(a) as a function of scale and time. The periodicity of the coefficients over the scales is calculated as

| (4) |

and it is given in Fig.2(b).

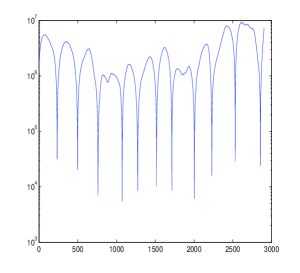

To analyze the periodicity of the data at different frequencies,

| (5) |

where is the frequency; we have shown the at different scales in Fig.3.

One observes significant fluctuations at different scales in the second half of the data.It is evident that the fluctuations have a self similar character. We depict the fluctuations at smaller scale as also the dominant periodic variations at different scales and one does not see significant transient fluctuations in the variations.

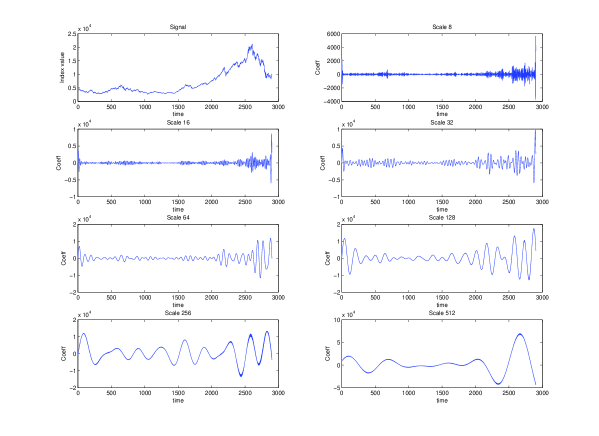

The extracted fluctuations at different levels through DWT are shown in Fig.4(a) and Fig.4(b). Having seen the periodic behavior of the data, and having extracted the fluctuations through DWT, in the next section, we discuss the wavelet based method for analysis of fluctuations to identify their fractal behavior.

3 Discrete wavelet based method for characterizing multifractal behavior

We have observed earlier the self-similar nature of the fluctuations in the wavelet domain. In the following we describe the procedure of the wavelet based method.

From the financial (BSE stock index) time series , the scaled logarithmic returns is defined as,

| (6) |

here is the standard deviation of . The profile of the time series is obtained from the cumulative,

| (7) |

Next, apply the wavelet transform on the time series profile to extract the fluctuations from the trend. The trend is extracted by discarding the high-pass coefficients and reconstructing only with low-pass coefficients using inverse wavelet transform. The fluctuations are then extracted at each level by subtracting the trend from the original time series. This procedure is followed to extract fluctuations at different levels. Here the wavelet window size at each level of decomposition is considered as the scale . We have made use of Daubechies (Db) wavelets for the extraction of desired polynomial trend. Although the Daubechies wavelets extract the fluctuations effectively, its asymmetric nature and wrap around problem affects the precision of the values. We apply wavelet transform on the reverse profile, to extract a new set of fluctuations. These fluctuations are then reversed and averaged over the earlier obtained fluctuations.

Now the extracted fluctuations using wavelet transform are subdivided into non-overlapping segments where is the length of the fluctuations and is the scale. The order fluctuation function is then obtained by squaring and averaging the fluctuations over all segments:

| (8) |

Here ’’ is the order of moment. The above procedure is repeated for different scale sizes for different values of (except ). The power law scaling behavior is obtained from the fluctuation function,

| (9) |

in a logarithmic scale for each value of . If the order , direct evaluation leads to the divergence of the scaling exponent. In that case, logarithmic averaging has to be employed to find the fluctuation function:

| (10) |

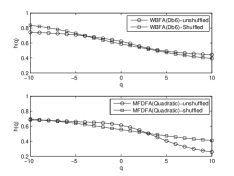

For the monofractal time series, values are independent of q and for the multi-fractal time series values are dependent on . , the Hurst scaling exponent is a measure of fractal nature such that varies . Here and reveal the anti-persistent and persistent nature of the time series, whereas is for random time series.

4 Data analysis and observations

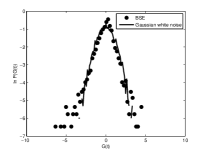

The wavelet based fluctuation analysis (WBFA) which is used here was carried on the time series profile obtained from the returns and shuffled returns. The analyzed time series using discrete wavelet based method with Db-6 wavelet reveals the presence of multifractal nature with long-range correlation behavior that is shown in Fig.5 (top panel). For the sake of comparison, MF-DFA method with quadratic polynomial fit is also used which complements the wavelet based method (see Fig.5 (bottom panel)). The Hurst scaling exponent reveals that the time series possesses persistent behavior, which is shown in Table 1. The semi-log plot of distribution of logarithmic returns of BSE index and the Gaussian white noise is shown in Fig. 5 for the BSE index. The fat tails for large fluctuations and sharper behavior near the origin for small fluctuations are clearly seen.

| X | ||||

|---|---|---|---|---|

| Hurst Scaling Exponent | 0.5486 | 0.5218 | 0.5590 | 0.5420 |

We have also analyzed the scaling behavior through Fourier power spectral analysis,

| (11) |

Here is the accumulated fluctuations after subtracting the mean . It is well known that, . For the BSE price index time series, the scaling exponent which reveals long range correlated behavior as shown in Fig. 6. The obtained scaling exponent can be compared with Hurst exponent by the relation . The wavelet based method and FFT are comparable.

5 Conclusion

We have analyzed BSE high price index values in daily trading. A detailed study reveals multifractal behavior and non statistical distribution of the returns. The distribution function of the returns also show fat-tail behavior. The analysis through the wavelet based method, MFDFA method and also Fourier power spectrum analysis reveal a persistent nature, as well as multifractal behavior of the BSE price index values. The multifractal nature of the time series may arise due to herding behavior, and other intrinsic non-linear character of the market and other control mechanism. We intend to study the fluctuations in different price indices in different countries for this time period. This may reveal the physical origin of the other time periods as also the multi fractal character.

6 Acknowlegement

PM, one of the authors would like to thank the Department of Science and Technology for their financial support (DST-CMS GoI Project No. SR/S4/MS:516/07 Dated 21.04.2008).

References

- (1) Plerou V et. al (2000), Physica A 279:443.

- (2) Bachelier L (1900) Ann. Sci. École Norm. Sup. 3:21.

- (3) Pareto V (1897) Cours d’Économie Politique Lausanne, Paris.

- (4) Lévy P (1937) Théorie de l’Addition des Variables Alé atoires, Gauthier-Villars, Paris.

- (5) Mandelbrot B B (1963) J. Bus. 36:394419.

- (6) Mantegna, R N, Stanley H E (2000), Introduction to Econophysics: Correlations and Complexity in Finance, Cambridge University Press, Cambridge.

- (7) Bouchaud J P, Potters M (2000) Theory of Financial Risk, Cambridge University Press, Cambridge.

- (8) Farmer J D (1999) Comput. Sci. Eng. 1:26.

- (9) Kondor I, Kértesz (eds.) (2000) Econophysics: An Emerging Science, Kluwer, Dordrecht.

- (10) Mantegna R N, (ed.) (1999) Proceedings of the International Workshop on Econophysics and Statistical Finance, Physica A (special issue) 269:1.

- (11) Bouchaud J P, Alström P, Lauritsen K B (eds.), (2000) Application of Physics in Financial Analysis, Int. J. Theor. Appl. Finance (special issue) 3.

- (12) Takayasu H (ed.) (2002), The Application of Econophysics: Proceedings of the Second Nikkei Econophysics Symposium,Springer.

- (13) Mandelbrot B B (1999),The Fractal Geometry of Nature Freeman, San Francisco.

- (14) Daubechies I (1992) Ten lectures on wavelets SIAM, Philadelphia.

- (15) Mallat S (1999) A Wavelet Tour of Signal Processing Academic Press.

- (16) Burrus C S, Gopinath R A, and Guo H (1998) Introduction to Wavelets and Wavelt Transforms Prentice Hall, New Jersey.

- (17) Manimaran P, Panigrahi P K, and Parikh J C (2005), Phys. Rev. E 72:046120.

- (18) Manimaran P, Lakshmi P A, Panigrahi P K (2006), J. Phys. A 39:L599.

- (19) Oświecimka P, Kwapién, Drozdz (2006) Phys. Rev. A. 74:016103.

- (20) Manimaran P, Panigrahi P K, and Parikh J C (2008) Physica A 387:5810.

- (21) Manimaran P, Panigrahi P K, and Parikh J C (2009) Physica A 388:2306.

- (22) Hu K, Ivanov P Ch, Chen Z, Carpena P, and Stanley H E (2001) Phys.Rev. E 64:11114.

- (23) Gopikrishnan et. al (1999) Phys. Rev. E 60:5305.

- (24) Plerou V et. al (1999) Phys. Rev. E 60:6519.

- (25) Chen Z, Ivanov P Ch., Hu K, and Stanley H E (2002) Phys. Rev. E 65:041107.

- (26) Matia K, Ashkenazy Y, and H. E. Stanley, (2003) Europhys. Lett. 61:422.

- (27) Hwa R C et. al(2005) Phys. Rev. E. 72:066308.

- (28) Ohashi K, Amaral L A N, Natelson B H, Yamamoto Y (2003) Phys. Rev. E. 68:065204.

- (29) Xu L et. al(2005) Phys. Rev. E. 71:051101.

- (30) Brodu N, eprint:nlin.CD/0511041.

- (31) Gu G F, Zhou W X (2006) Phys. Rev. E 74:061104.

- (32) Mohaved M S, Hermanis E (2008) Physica A 387:915.

- (33) obtained from http://in.finance.yahoo.com

- (34) Farge M, (1992) Annu. Rev. Fluid Mech. 24:395.

- (35) Stuzik Z R, (2001) Physica A 296:307.

- (36) Bartolozzi M et. al (2005) Physica A 350:451.

- (37) BartolozziM (2007) Eur. Phys. J. B 57:337.

- (38) Simonsen I, Hansen A, and Nes O -M, Phys. Rev. E 58 (1998) 2779.

- (39) Connor J and Rossiter R (2005), Studies in Nonlinear Dynamics and Econometrics 9:1.

- (40) Ahalpara D P et. al (2008) Pramana -J. Phys. 71:459.

- (41) Torrence C and Compo G P (1998) Bull. Amer. Meteorol. Soc. 79:61.

- (42) Goupillaud P, Grossman A, and Morlet J (1984) Geoexploration 23:85-102.

- (43) Hurst H E (1951) Trans. Am. Soc. Civ. Eng. 116:770.

- (44) Feder J(1988) Fractals Plenum Press, New York,

- (45) Arneodo A et. al (1988) Phys. Rev. Lett. 61:2284; Muzy J F et. al (1993) Phys. Rev. E 47:875.

- (46) Peng C K, et. al (1994) Phys. Rev. E 49:1685.

- (47) Kantelhardt J W, et. al (2003) Physica A 330:240.