A ”Joint+marginal” approach to parametric polynomial optimization

Abstract.

Given a compact parameter set , we consider polynomial optimization problems ) on whose description depends on the parameter . We assume that one can compute all moments of some probability measure on , absolutely continuous with respect to the Lebesgue measure (e.g. is a box or a simplex and is uniformly distributed). We then provide a hierarchy of semidefinite relaxations whose associated sequence of optimal solutions converges to the moment vector of a probability measure that encodes all information about all global optimal solutions of , as . In particular, one may approximate as closely as desired any polynomial functional of the optimal solutions, like e.g. their -mean. In addition, using this knowledge on moments, the measurable function of the -th coordinate of optimal solutions, can be estimated, e.g. by maximum entropy methods. Also, for a boolean variable , one may approximate as closely as desired its persistency , i.e. the probability that in an optimal solution , the coordinate takes the value . At last but not least, from an optimal solution of the dual semidefinite relaxations, one provides a sequence of polynomial (resp. piecewise polynomial) lower approximations with (resp. almost uniform) convergence to the optimal value function.

Key words and phrases:

Parametric and polynomial optimization; semidefinite relaxations1991 Mathematics Subject Classification:

65 D15, 65 K05, 46 N10, 90 C221. Introduction

Roughly speaking, given a set parameters and an optimization problem whose description depends on (call it ), parametric optimization is concerned with the behavior and properties of the optimal value as well as primal (and possibly dual) optimal solutions of , when varies in . This a quite challenging problem and in general one may obtain information locally around some nominal value of the parameter. There is a vast and rich literature on the topic and for a detailed treatment, the interested reader is referred to e.g. Bonnans and Shapiro [4] and the many references therein. Sometimes, in the context of optimization with data uncertainty, some probability distribution on the parameter set is available and in this context one is also interested in e.g. the distribution of the optimal value, optimal solutions, all viewed as random variables. In particular, for discrete optimization problems where cost coefficients are random variables with joint distribution , some bounds on the expected optimal value have been obtained. More recently Natarajan et al. [17] extended the earlier work in [3] to even provide a convex optimization problem for computing the so-called persistency values111Given a optimization problem and a distribution on , the persistency value of the variable is at an optimal solution . of (discrete) variables, for a particular distribution in a certain set of distributions. However, this convex formulation requires knowledge of the convex hull of a discrete set and approximations are needed. The approach is nicely illustrated on a discrete choice problem and a stochastic knapsack problem. For more details on persistency in discrete optimization, the interested reader is referred to [17] and the references therein.

In the context of polynomial equations whose coefficients

are themselves polynomials of some parameter , some specific ”parametric”

methods exist. For instance, one may compute symbolically once and for all, what is called a comprehensive Gröbner basis,

i.e., a fixed basis that is a Gröbner basis for all ; see Weispfenning [25] and more recently Rostalski [19] for more details.

Then when needed, one may compute the solutions

for a specific value of the parameter , e.g. by the eigenvalue method of Möller and Stetter [16, 22]. However, one still needs to

apply the latter method for each value of the prameter . A similar two-step approach is also proposed for homotopy

(instead of Gröbner bases) methods in [19].

The purpose of this paper is to show that in one restricts to the case of polynomial parametric optimization then all information about the optimal value and optimal solutions can be obtained, or at least, approximated as closely as desired.

Contribution

We here restrict our attention to parametric polynomial optimization, that is, when

is described by polynomial equality and inequality constraints

on both the parameter vector and the optimization variables . Moreover, the set

is restricted to be a compact basic semi-algebraic set of , and preferably a set

sufficiently simple so that one may obtain the

moments of some probability measure on , absolutely continuous with respect to the Lebesgue

measure. For instance if

is a simple set (like a simplex, a box) one may choose to be the probability measure uniformly distributed on ; typical candidates are polyhedra. Or sometimes, in the context of optimization with data uncertainty,

is already specified. We also suppose that

has a unique optimal solution for almost all values of the parameter .

In this specific context we are going to show

that one may get insightful information on the set of all global optimal

solutions of , via what we call a ”Joint+marginal” approach. Our contribution is as follows:

(a) Call (resp. ) the optimal value (resp. the set of optimal solutions) of for the value of the parameter. We first define an infinite-dimensional optimization problem whose optimal value is exactly . Any optimal solution of is a probability measure on with marginal on . It turns out that encodes all information on the optimal solutions , . Whence the name ”Joint+marginal” as is a joint distribution of and , and is the marginal of on .

(b) Next, we provide a hierarchy of semidefinite relaxations of with associated sequence of optimal values , in the spirit of the hierarchy defined in [13]. An optimal solution of the -th semidefinite relaxation is a sequence indexed in the monomial basis of the subspace of polynomials of degree at most . If for almost all , has a unique global optimal solution , then as , converges pointwise to the sequence of moments of defined in (a). In particular, one obtains the distribution of the optimal solution , and therefore, one may approximate as closely as desired any polynomial functional of the solution , like e.g. the -mean or variance of .

In addition, if the optimization variable is boolean then one may approximate as closely as desired its persistency (i.e., the probability that in an optimal solution ), as well as a a necessary and sufficient condition for this persistency to be .

(c) Finally, let be the vector . Then as , and for every , the sequence converges to for the measurable function . In other words, the sequence is the moment sequence of the measure on . And so, the -th coordinate function of optimal solutions of , , can be estimated, e.g. by maximum entropy methods. Of course, the latter estimation is not pointwise but it still provides useful information on optimal solutions, e.g. the shape of the function , especially if the function is continuous, as illustrated on some simple examples. For instance, for parametric polynomial equations, one may use this estimation of as an initial point for Newton’s method for any given value of the parameter .

Finally, the computational complexity of the above methodology is roughly the same as the moment approach described in [13] for an optimization problem with variables since we consider the joint distribution of the variables and the parameters . Hence, the approach is particularly interesting when the number of parameters is small, say or . In addition, in the latter case the max-entropy estimation has been shown to be very efficient in several examples in the literature; see e.g. [5, 23, 24]. However, in view of the present status of SDP solvers, if no sparsity or symmetry is taken into account as proposed in e.g. [14], the approach is limited to small to medium size polynomial optimization problems.

But this computational price may not seem that high in view of the ambitious goal of the approach. After all, keep in mind that by applying the moment approach to a single -variables problem, one obtains information on global optimal solutions of an -variables problem that depends on parameters, that is, one approximates functions of variables!

2. A related linear program

Let denote the ring of polynomials in the variables , and the variables , whereas denotes its subspace of polynomials of degree at most . Let denote the subset of polynomials that are sums of squares (in short s.o.s.). For a real symmetric matrix the notation stands for is positive semidefinite.

The parametric optimization problem

Let be a compact set, called the parameter set, and let , , be continuous. For each , fixed, consider the following optimization problem:

| (2.1) |

where the functions are defined via:

Next, let be the set:

| (2.2) |

and for each , let

| (2.3) |

The interpretation is as follows: is a set of parameters and for each instance of the parameter, one wishes to compute an optimal decision vector that solves problem (2.1). Let be a Borel probability measure on , with a positive density with respect to the Lebesgue measure on . For instance choose for the probability measure

uniformly distributed on . Sometimes, e.g. in the context of optimization with data uncertainty, is already specified.

We will use (or more precisely, its moments) to

get information on the distribution of

optimal solutions of , viewed as random vectors.

In the rest of the paper we assume that for every , the set in (2.3) is nonempty.

2.1. A related infinite-dimensional linear program

Let be the set of finite Borel measures on , and consider the following infinite-dimensional linear program :

| (2.4) |

where denotes the marginal of on , that is, is a probability measure on defined by

Notice that for any feasible solution of . Indeed, as is a probability measure and one has .

Recall that for two Borel spaces , the graph of a set-valued mapping is the set

If is measurable then any measurable function with for every , is called a (measurable) selector.

Lemma 2.1.

Let both and in (2.2) be compact. Then the set-valued mapping is Borel-measurable. In addition:

(a) The mapping is measurable.

(b) There exists a measurable selector such that for every .

Proof.

As and are both compact, the set valued mapping is compact-valued. Moreover, the graph of is by definition the set , which is a Borel subset of . Hence, by [11, Proposition D.4], is a measurable function from to the space of nonempty compact subsets of , topologized by the Hausdorff metric. Next, since is continuous for every , (a) and (b) follows from e.g. [11, Proposition D.5]. ∎

Theorem 2.2.

Let both and in (2.2) be compact and assume that for every , the set in (2.3) is nonempty. Let be the optimization problem (2.4) and let , . Then:

(a) and has an optimal solution.

(b) For every optimal solution of , and for almost all , there is a probability measure on such that:

| (2.5) |

(c) Assume that for almost , the set of minimizers of is the singleton for some . Then there is a measurable mapping such that

| (2.6) |

and for every , and :

| (2.7) |

Proof.

(a) As is compact then so is for every . Next, as for every and is continuous, the set is nonempty for every . Let be any feasible solution of and so by definition, its marginal on is just . Since , one has for all and all . So, for all and therefore

which proves that .

On the other hand, recall that . Consider the set-valued mapping . As is continuous and is compact, then is compact-valued. In addition, as is continuous, by [11, D6] (or [20]) there exists a measurable selector (and so ). Therefore, for every , let be the Dirac probability measure with support on the singleton , and let be the probability measure on defined by:

(The measure is well-defined because is measurable.) Then is feasible for and

which shows that is an optimal solution of and .

(b) Let be an arbitrary optimal solution of , hence supported on . Therefore, as is contained in the cartesian product , the probability measure can be disintegrated as

where for all , is a probability measure on . (The object is called a stochastic kernel; see e.g. [8, p. 88–89] or [11, D8].) Hence from (a),

Therefore, using on ,

which implies for almost all .

(c) Let be the measurable mapping of Lemma 2.1(b). As and then necessarily for every . Next, let be an optimal solution of , and let , . Then

the desired result. ∎

An optimal solution of encodes all information on the optimal solutions of . For instance, let be a given Borel set of . Then from Theorem 2.2,

with as in Theorem 2.2(b).

Consequently, if one knows an optimal solution of then one may evaluate functionals on the solutions of , . That is, assuming that for almost all , problem has a unique optimal solution , and given a measurable mapping , one may evaluate the functional

For instance, with one obtains the mean vector of optimal solutions , .

Corollary 2.3.

Proof.

2.2. Duality

Consider the following infinite-dimensional linear program :

| (2.9) |

Then is a dual of .

Lemma 2.4.

Proof.

For a topological space denote by the space of bounded continuous functions on . Let be the vector space of finite signed Borel measures on (and so is its positive cone). Let be defined by for all , with adjoint mapping defined as

Put (2.4) in the framework of infinite-dimensional linear programs on vector spaces, as described in e.g. [1]. That is:

with dual:

One first proves that and then .

By [1, Theor. 3.10], to get , it suffices to prove that the set is closed for the respective weak topologies and . Therefore consider a converging sequence with . The sequence is uniformly bounded because

But by the Banach-Alaoglu Theorem (see e.g. [2]), the bounded closed sets of are compact in the weak topology. And so for some and some subsequence . Next, observe that for arbitrary,

where we have used that . Hence combining the above with , we obtain . Similarly, because . Hence is closed and the desired result follows.

We next prove that . Given fixed arbitrary, there is a function such that on and . By compactness of and the Stone-Weierstrass theorem, there is such that . Hence the polynomial is feasible with value , and as was arbitrary, the result follows. ∎

As next shown, optimal or nearly optimal solutions of provide us with polynomial lower approximations of the optimal value function that converges to in the norm. Moreover, one may also obtain a piecewise polynomial approximation that converges to almost uniformly. (Recall that a sequence of measurable functions on a measure space converges to almost uniformly if and only if for every , there is a set such that and uniformly on .)

Corollary 2.5.

Proof.

By Lemma 2.4, we already know that and so

Next by feasibility of in (2.9)

Hence (2.10) follows from on .

Next, with fixed, the sequence is obviously monotone non decreasing and bounded above by , hence with a limit . Therefore has the pointwise limit . Also, by the Montone convegence theorem, . This latter fact combined with (2.10) and yields

which in turn implies that for almost all . Therefore for almost all . And so, by Egoroff’s Theorem [2, Theor. 2.5.5], almost uniformly. ∎

3. A hierarchy of semidefinite relaxations

In general, solving the infinite-dimensional problem and getting an optimal solution is impossible. One possibility is to use numerical discretization schemes on a box containing ; see for instance [12]. But in the present context of parametric optimization, if one selects finitely many grid points , one is implicitly considering solving (or rather approximating) for finitely many points in a grid of , which we want to avoid. To avoid this numerical discretization scheme we will use specific features of when its data (resp. ) is a polynomial (resp. a compact basic semi-algebraic set).

Therefore in this section we are now considering a polynomial parametric optimization problem, a special case of (2.1) as we assume the following:

-

•

and , for every .

-

•

is compact and is a compact basic semi-algebraic set.

Hence the set in (2.2) is a compact basic semi-algebraic set. We also assume that there is a probability measure on , absolutely continuous with respect to the Lebesgue measure, whose moments , , are available. As already mentioned, if is a simple set (like e.g. a simplex or a box) then one may choose to be the probability measure uniformly distributed on , for which all moments can be computed easily. Sometimes, in the context of optimization with data uncertainty, the probability measure is already specified and in this case we assume that its moments , , are available.

3.1. Notation and preliminaries

Let with . With a sequence , , indexed in the canonical basis of , let be the linear mapping:

Moment matrix

The moment matrix associated with a sequence , has its rows and columns indexed in the canonical basis , and with entries.

for every and every .

Localizing matrix

Let be the polynomial . The localizing matrix associated with and a sequence , has its rows and columns indexed in the canonical basis , and with entries.

for every and every .

A sequence has a representing finite Borel measure supported on if there exists a finite Borel measure such that

The next important result states a necssary and sufficient condition when is compact and its defining polynomials satisfy some condition.

Assumption 3.1.

Let be a given family of polynomials. There is some such that the quadratic polynomial can be written

for some s.o.s. polynomials .

Theorem 3.2.

Let and let satisfy Assumption 3.1. A sequence has a representing measure on if and only if:

Theorem 3.2 is a direct consequence of Putinar’s Positivstellensatz [18] and [21]. Of course, when Assumption 3.1 holds then is compact. On the other hand, if is compact and one knows a bound for on then its suffices to add the redundant quadratic constraint to the definition of , and Assumption 3.1 holds.

3.2. Semidefinite relaxations

To compute (or at least, approximate) the optimal value of problem in (2.4), we now provide a hierarchy of semidefinite relaxations in the spirit of those defined in [13].

Let be as in (2.2), and let be the compact semi-algebraic set defined by:

| (3.1) |

for some polynomials ; let for every . Next, let with

be the moments of a probability measure on , absolutely continuous with respect to the Lebesgue measure, and let . For , consider the following semidefinite relaxations:

| (3.2) |

Theorem 3.3.

Let be as (2.2) and (3.1) respectively, and let satisfy Assumption 3.1. Assume that for every the set is nonempty, and for almost all , is attained at a unique optimal solution . Consider the semidefinite relaxations (3.2). Then:

(a) as .

The proof is postponed to Section 4.

Remark 3.4.

Observe that if for some index in the hierarchy (and hence for all ), then the set is empty for all in some Borel set of with . Conversely, one may prove that if is empty for all in some Borel set of with , then necessarily for all sufficiently large. In other words, the hierarchy of semidefinite relaxations (3.2) may also provide a certificate of emptyness of for some Borel set of with positive Lebesgue measure.

3.3. The dual semidefinite relaxations

The dual of the semidefinite relaxtion (3.2) reads:

| (3.5) |

Observe that (3.5) is a strenghtening of (2.9) as one restricts to polynomials of degree at most and the nonnegativity of in (2.9) is replaced with a stronger requirement in (3.5). Therefore for every .

Theorem 3.5.

Let be as (2.2) and (3.1) respectively, and let satisfy Assumption 3.1. Assume that for every the set is nonempty, and consider the semidefinite relaxations (3.5). Then:

(a) as .

(b) Let be a nearly optimal solution of (3.5), e.g. such that . Then and

| (3.6) |

Moreover if one defines

then almost uniformly on .

Proof.

Recall that by Lemma 2.4, . Moreover let be a maximizing sequence of (2.9) as in Corollary 2.5 with value , and let for every so that on . By Theorem 3.2, there exist s.o.s. polynomials such that . Letting be the maximum degree of and , , it follows that is a feasible solution of (3.5) with . Hence and the result (a) follows because , and the sequence is monotone. Then (b) follows from Corollary 2.5.

∎

Hence Theorem 3.5 provides a lower polynomial approximation of the optimal value function . Its degree is bounded by , the order of the moments of taken into account in the semidefinite relaxation (3.5). Moreover one may even define a piecewise polynomial lower approximation that converges almost uniformly to on .

Functionals of the optimal solutions

Theorem 3.3 provides a mean of approximating any polynomial functional on the optimal solutions of , . Indeed,

Corollary 3.6.

Let be as (2.2) and (3.1) respectively, and let satisfy Assumption 3.1. Assume that for every the set is nonempty, and for almost all , is attained at a unique optimal solution . Let ,

and let be a nearly optimal solution of the semidefinite relaxations (3.2).

Then, for sufficiently large,

3.4. Persistence for Boolean variables

One interesting and potentially useful application is in Boolean optimization. Indeed suppose that for some subset , the variables , , are boolean, that is, the definition of in (2.2) includes the constraints , for every .

Then for instance, one might be interested to determine whether in an optimal solution of , and for some index , one has (or ) for almost all values of the parameter . In [3, 17] the probability that is is called the persistency of the boolean variable

Corollary 3.7.

Let be as in (2.2) and (3.1) respectively. Let satisfy (3.1). Assume that for every the set is nonempty. Let be a nearly optimal solution of the semidefinite relaxations (3.2). Then for fixed.

(a) for almost all , only if .

(b) for almost all , only if .

Assume that for almost all , is attained at a unique optimal solution . Then , and so:

(c) for almost all , if and only if .

(d) for almost all , if and only if .

Proof.

(a) The only if part. Let . From the proof of Theorem 3.3, there is a subsequence such that

where is an optimal solution of . Hence, by Theorem 2.2(b), can be disintegrated into where is a probability measure on for every . Therefore,

and as the subsequence was arbitrary, the whole sequence converges to , the desired result. The proof of (b) being exactly the same is omitted.

Next, if for every , is attained at a singleton, by Theorem 3.3(b),

from which (c) and (d) follow. ∎

3.5. Estimating the density

By Corollary 3.6, one may approximate any polynomial functional of the optimal solutions, like for instance the mean, variance, etc .. (with respect to the probability measure ). However, one may also wish to approximate (in some sense) the ”curve” , that is, the surface described by the -th coordinate of the optimal solution when varies in .

So let be the measurable mapping in Theorem 3.3 and suppose that one knows some lower bound vector , where:

Then for every , the measurable function defined by

| (3.7) |

is nonnegative and integrable with respect to .

Hence for every , one may consider as a Borel measure on with unknown density with respect to , but with known moments . Indeed, using (3.4),

| (3.8) | |||||

where for every ,

with being an optimal (or nearly optimal) solution of the semidefinite relaxation (3.2).

Hence we are now faced with a density estimation problem, that is: Given the sequence of moments , , of the unknown nonnegative measurable function on , ”estimate” . One possibility is the so-called maximum entropy approach, briefly described in the next section.

Maximum-entropy estimation

We briefly describe the maximum entropy estimation technique in the univariate case. The multivariate case generalizes easily. Let 222 denote the Banach space of integrable functions on the interval of the real line, equipped with the norm . be a nonnegative function only known via the first moments of its associated measure on . (In the context of previous section, the function to estimate is in (3.7) from the sequence in (3.8) of its (multivariate) moments.)

From that partial knowledge one wishes (a) to provide an estimate of such that the first moments of the measure match those of , and (b) analyze the asymptotic behavior of when . This problem has important applications in various areas of physics, engineering, and signal processing in particular.

An elegant methodology is to search for in a (finitely) parametrized family of functions, and optimize over the unknown parameters via a suitable criterion. For instance, one may wish to select an estimate that maximizes some appropriate entropy. Several choices of entropy functional are possible as long as one obtains a convex optimization problem in the finitely many coefficients ’s. For more details the interested reader is referred to e.g. Borwein and Lewis [6, 7] and the many references therein.

We here choose the Boltzmann-Shannon entropy :

| (3.9) |

a strictly concave functional. Therefore, the problem reduces to:

| (3.10) |

The structure of this infinite-dimensional convex optimization problem permits to search for an optimal solution of the form:

| (3.11) |

and so is an optimal solution of the finite-dimensional unconstrained convex problem

Notice that the above function is just the Legendre-Fenchel transform of the convex function .

An optimal solution can be calculated by applying first-order methods, in which case the gradient of the function

is provided by:

If one applies second-order methods, e.g. Newton’s method, then computing the Hessian at current iterate , reduces to computing

In such simple cases like a box (or in the multivariate case) such quantities can be approximated quite accurately via cubature formula as described in e.g. [9]. In particular, several cubature formula behave very well for exponentials of polynomials as shown in e.g. Bender et al. [5]. An alternative with no cubature formula is also proposed in [15].

One has the following convergence result which follows directly from [6, Theor. 1.7 and p. 259].

Proposition 3.8.

Hence, the max-entropy estimate we obtain is not a pointwise estimate of , and so, at some points of the max-entropy density and the density to estimate may differ significantly. However, for sufficiently large , both curves of and are close to each other. In our context, recall that is for instance , and so in general, for fixed , is close to and might be chosen for the -coordinate of an initial point , input of a local minimization algorithm to find the global minimizer .

3.6. Illustrative examples

In this section we provide some simple illustrative examples. To show the potential of the approach we have voluntarily chosen very simple examples for which one knows the solutions exactly so as to compare the results we obtain with the exact optimal value and optimal solutions. The semidefinite relaxations (3.2) were implemented by using the software package Gloptipoly [10]. The max-entropy estimate of was computed by using Newton’s method, where at each iterate :

Example 1.

For illustration purpose, consider the toy example where ,

Hence for each value of the parameter , the unique optimal solution is . And so in Theorem 3.3(b), .

Let be the probability measure uniformly distributed on . Therefore,

Solving (3.2) with , that is, with moments up to order , one obtains the optimal value . Solving (3.2) with , one obtains the optimal value and the moment sequence

Observe that

Using a max-entropy approach to approximate the density on , with the first moments , , we find that the optimal function in (3.11) is obtained with

Both curves of and are displayed in Figure 1. Observe that with only moments, the max-entropy solution approximates relatively well, even if it differs significantly at some points. Indeed, the shape of resembles very much that of .

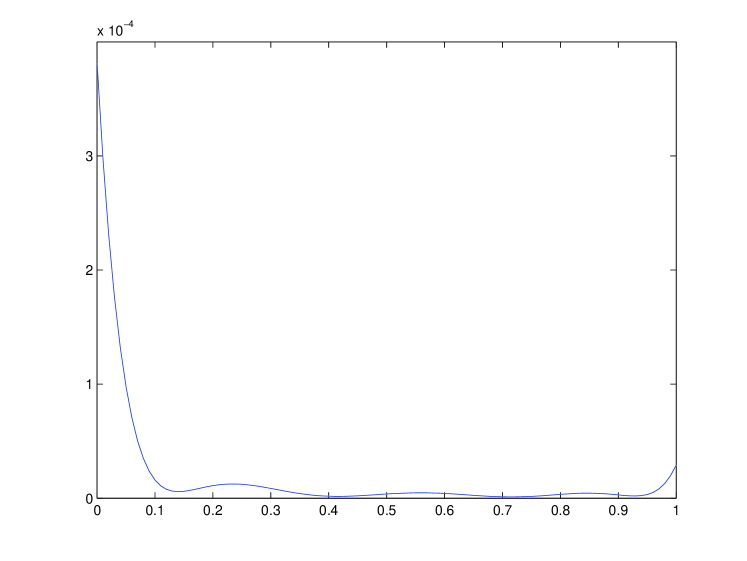

Finally, from an optimal solution of (3.5) one obtains for , the degree- univariate polynomial

and Figure 2 displays the curve on . One observes that and the maximum difference is about close to and much less for , a good precision with only moments.

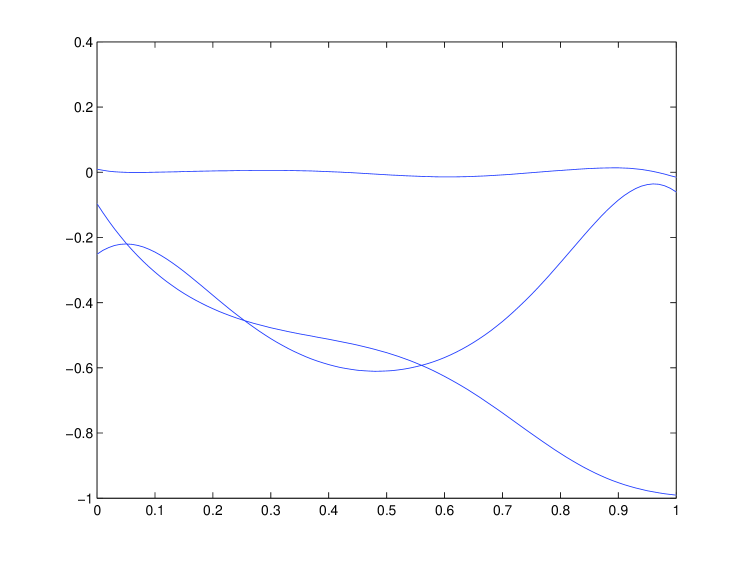

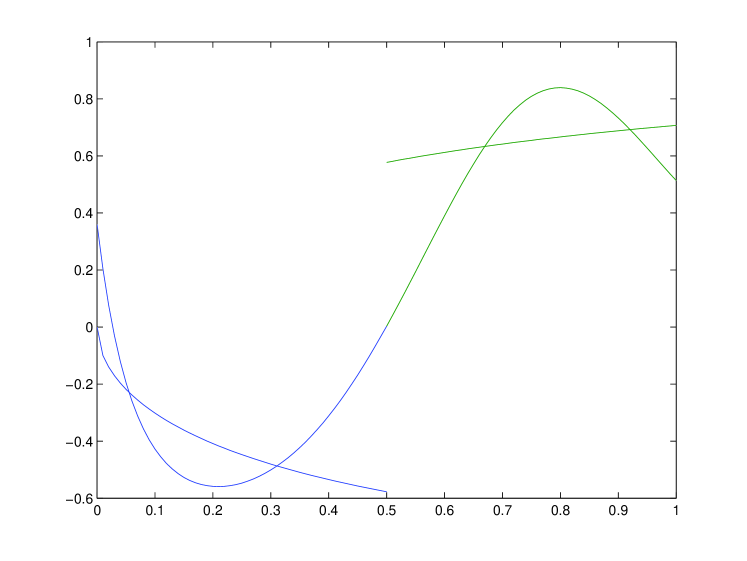

Example 2.

Again with , let

For each value of the parameter , the unique optimal solution satisfies

with optimal value

So in Theorem 3.3(b),

and with being the probability measure uniformly distributed on ,

Solving (3.2) with , that is, with moments up to order , one obtains with . Solving (3.2) with , one obtains with , and the moment sequence , :

and

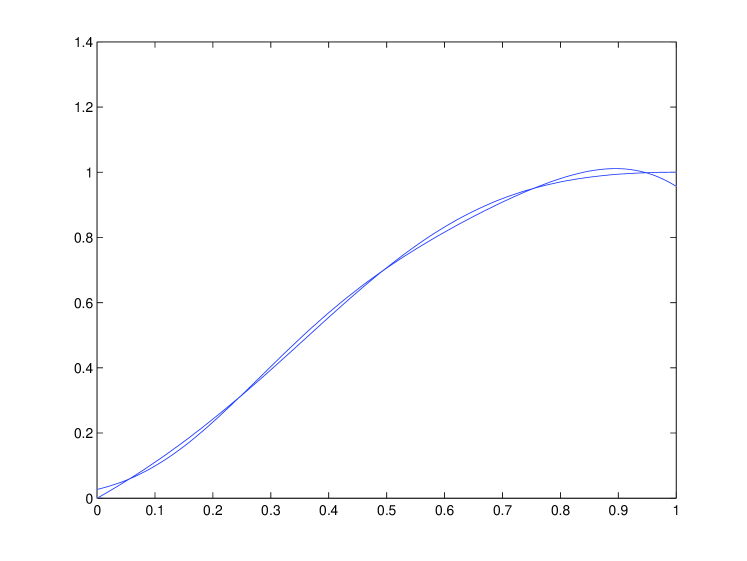

Using a max-entropy approach to approximate the density on , with the first moments , , we find that the optimal function in (3.11) is obtained with

and we find that

In Figure 3 are displayed the two functions and , and one observes a very good concordance.

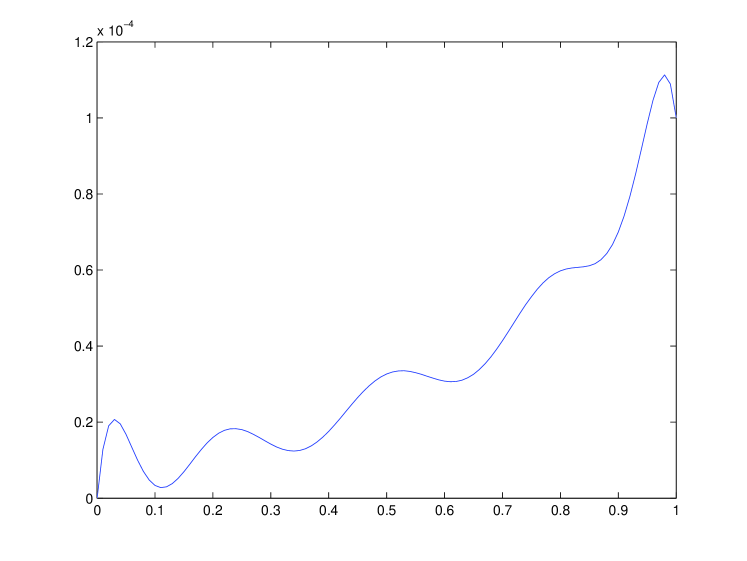

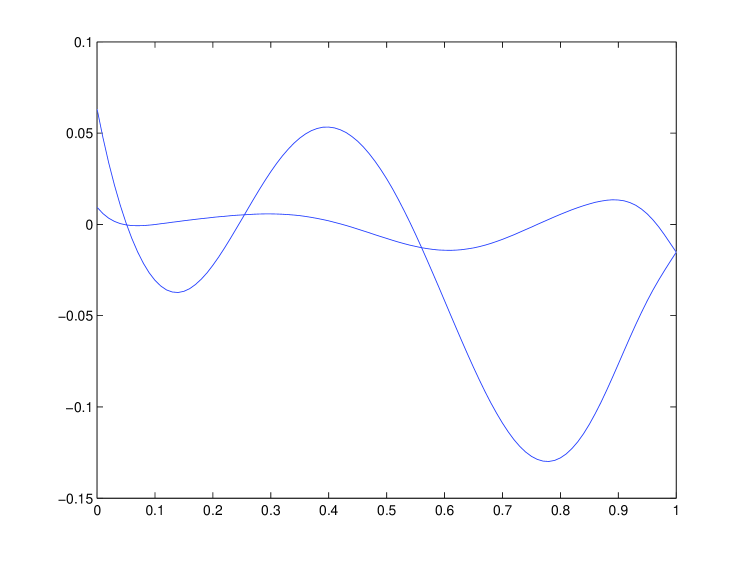

Finally, from an optimal solution of (3.5) one obtains for , the degree- univariate polynomial

and Figure 4 displays the curve on . One observes that and the maximum difference is about , a good precision with only moments.

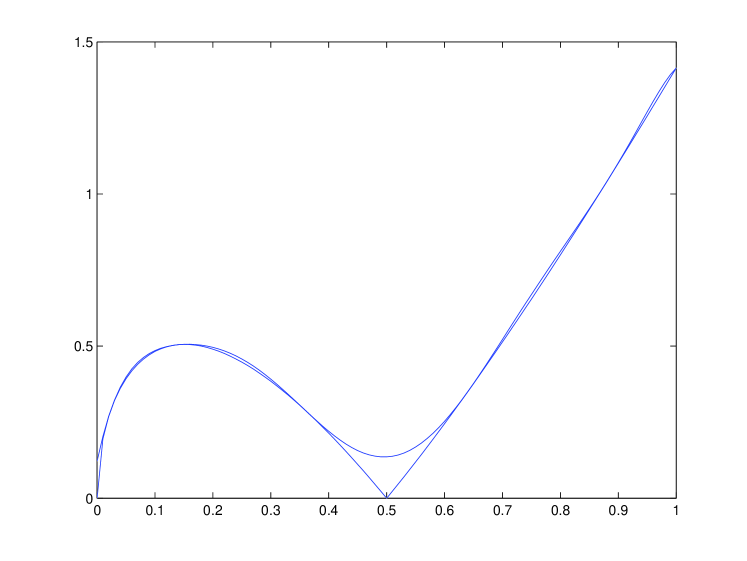

Example 3.

In this example one has , , and

That is, for each the set is the intersection of two ellipsoids. It is easy to chack that for all , . With the max-entropy estimate for is obtained with

whereas the max-entropy estimate for is obtained with

Figure 5 displays the curves of and , as well as the constraint . Observe that on which means that for almost all , at an optimal solution , the constraint is saturated. Figure 6 displays the curves of and .

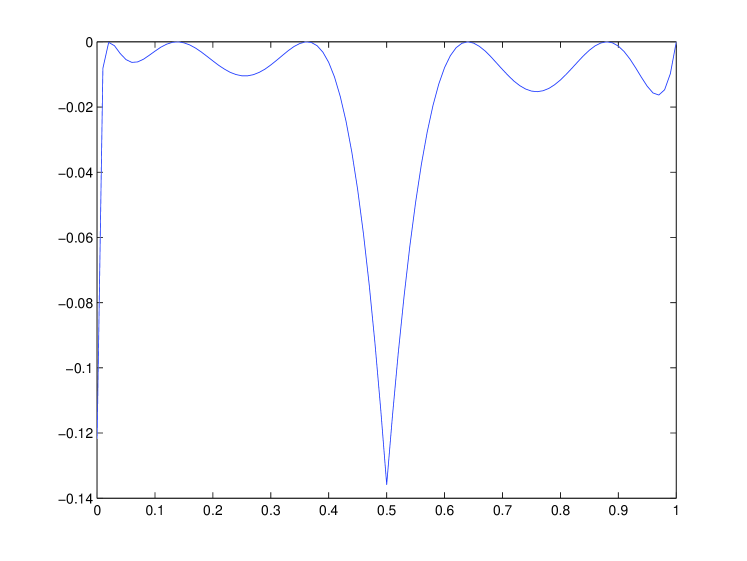

Example 4.

This time , , and

That is, for each the set is the intersection of two ellipses, and

With the max-entropy estimate for is obtained with

In Figure 7 are displayed the curves and , whereas in Figure 8 is displayed the curve . One may see that is a good lower approximation of even with only 8 moments.

On the other hand, in Figure 9 is displayed versus where the latter is on and on . Here we see that the discontinuity of is difficult to approximate ”pointwise” with few moments, and despite a very good precision on the five first moments. Indeed:

We end up this section with the case where the density to estimate is a step function which would be the case in an optimization problem with boolean variables (e.g. the variable takes values in ).

Example 5.

Assume that with a single parameter , the density to estimate is the step function.

The max-entropy estimate in (3.11) with moments is obtained with

and we have

In particular, the persistency of the variable , is very well approximated (up to precision) by , with only moments.

Of course, in this case and with only 5 moments, the density is not a good pointwise approximation of the step function ; however its ”shape” reveals the two steps of value separated by a step of value . A better pointwise approximation would require more moments.

4. Appendix

Proof of Theorem 3.3.

We already know that for all . We also need to prove that for sufficiently large . Let be the quadratic module generated by the polynomials that define , i.e.,

In addition, let be the set of elements which have a representation for some s.o.s. family with and for all .

Let be fixed. As is compact, there exists such that on , for all and , with . Therefore, under Assumption 3.1(ii), the polynomial belongs to ; see Putinar [18]. But there is even some such that for every . Of course we also have for every , whenever . Therefore, let us take . For every feasible solution of one has

This follows from , and , which implies

for some with .

In particular, , which proves that , and so for

all sufficiently large .

From what precedes, and with arbitrary, let and be such that

| (4.1) |

Let , and let be a nearly optimal solution of with value

| (4.2) |

Fix . Notice that from (4.1), for every , one has

Therefore, for all ,

| (4.3) |

where with

Complete each vector with zeros to make it an infinite bounded sequence in , indexed in the canonical basis of . In view of (4.3),

| (4.4) |

and for all .

Hence, let be the new sequence defined by

and in , consider the sequence , as .

Obviously, the sequence is in the unit ball of , and so, by the Banach-Alaoglu theorem (see e.g. Ash [2]), there exists , and a subsequence , such that as , for the weak topology of . In particular, pointwise convergence holds, that is,

Next, define

The pointwise convergence implies the pointwise convergence , i.e.,

| (4.5) |

Next, let be fixed. From the pointwise convergence (4.5) we deduce that

Similarly

As was arbitrary, we obtain

| (4.6) |

which by Theorem 3.2 implies that is the sequence of moments of some finite measure with support contained in . Moreover, the pointwise convergence (4.5) also implies that

| (4.7) |

As measures on compacts sets are determinate, (4.7) implies that the marginal of on is the probability measure , and so is feasible for . Finally, combining the pointwise convergence (4.5) with (4.2) yields

which in turn yields that is an optimal solution of . And so as . As the sequence is monotone this yields the desired result (a).

References

- [1] E.J Anderson and P. Nash, Linear Programming in Infinite-Dimensional Spaces, John Wiley & Sons, Chichester (1987).

- [2] R. Ash, Real Analysis and Probability, Academic Press, San Diego (1972).

- [3] D. Bertsimas, K. Natarajan, and Chung-Piaw Teo,Persistence in discrete optimization under data uncertainty, Math. Prog. Ser. B 108 (2005), 251–274.

- [4] J. F. Bonnans and A. Shapiro. Perturbation Analysis of Optimization Problems, Springer, New York, 2000.

- [5] C.M. Bender, L. R. Mead, and N. Papanicolaou, Maximum entropy summation of divergent perturbation series, J. Math. Phys. 28 (1987), 1016-1018.

- [6] J. Borwein and A.S. Lewis, On the convergence of moment problems, Trans. Am. Math. Soc. 325 (1991), 249–271.

- [7] J. Borwein and A.S. Lewis, Convergence of best entropy estimates, SIAM J. Optim. 1 (1991), 191–205.

- [8] E.G Dynkin and A.A. Yushkevich, Controlled Markov Processes, Springer-Verlag, New York (1979).

- [9] W. Gautschi, Numerical Analysis: An Introduction, Birkhäuser, Boston (1997).

-

[10]

D. Henrion, J. B. Lasserre and J. Lofberg, GloptiPoly 3: moments, optimization and semidefinite

programming, Optim. Methods and Softw., to appear.

http://www.laas.fr/henrion/software/gloptipoly3/ - [11] O. Hernández-Lerma and J. B. Lasserre, Discrete-Time Markov Control Processes: Basic Optimality Criteria, Springer-Verlag, New York (1996).

- [12] O. Hernández-Lerma and J.B. Lasserre, Approximation schemes for infinite linear programs, SIAM J. Optim. 8 (1998), 973–988.

- [13] J.B. Lasserre, Global optimization with polynomials and the problem of moments, SIAM J. Optim. 11 (2001), 796–817.

- [14] J.B. Lasserre, Convergent SDP-relaxations in polynomial optimization with sparsity, SIAM J. Optim. 17 (2006), 822–843.

- [15] J.B. Lasserre, Semidefinite programming for gradient and Hessian computation in maximum entropy estimation, Proceedings 48th IEEE CDC Conference, New-Orleans (2007), pp. 3060–3064.

- [16] H.M. Möller and H.J. Stetter, Multivariate polynomial equations with multiple zeros solved by matrix eigenproblems, Num. Math. 70 (1995), 311–329.

- [17] K. Natarajan, Miao Song and Chung-Piaw Teo, Persistency and its applications in choice modelling, Mang. Sci. 55 (2009), 453–469.

- [18] M. Putinar, Positive polynomials on compact semi-algebraic sets, Indiana Univ. Math. J. 42 (1993), 969–984.

- [19] P. Rostalski, Algebraic Moments: Real root finding and related topics, PhD Thesis, Automatic Control Laboratory, ETH Zurich, Switzerland, May 2009.

- [20] M. Schäl, Conditions for optimality and for the limit of -stage optimal policies to be optimal, Z. Wahrs. verw. Gerb. 32 (1975), 179–196.

- [21] M. Schweighofer, Optimization of polynomials on compact semialgebraic sets, SIAM J. Optim. 15 (2005), 805–825.

- [22] H.J. Stetter, Numerical Polynomial Algebra, SIAM, Philadelphia (2004).

- [23] A. Tagliani, Entropy estimate of probability densities having assigned moments: Hausdorff case, Appl. Math. Lett. 15 (2002), 309–314.

- [24] A. Tagliani, Entropy estimate of probability densities having assigned moments: Stieltjes case, Appl. Math. Comput. 130 (2002), 201–211.

- [25] V. Weispfenning, Comprehensive Gröbner bases, J. Symb. Comp. 14 (1992), 1–29.