Liquidity Crisis, Granularity of the Order Book and Price Fluctuations

Abstract

We introduce a microscopic model for the dynamics of the order book to study how the lack of liquidity influences price fluctuations. We use the average density of the stored orders (granularity ) as a proxy for liquidity. This leads to a Price Impact Surface which depends on both volume and . The dependence on the volume (averaged over the granularity) of the Price Impact Surface is found to be a concave power law function with . Instead the dependence on the granularity is with , showing a divergence of price fluctuations in the limit . Moreover, even in intermediate situations of finite liquidity, this effect can be very large and it is a natural candidate for understanding the origin of large price fluctuations.

1 Introduction

One of the basic assumptions of the Arbitrage Pricing Theory, which is a standard tool of Financial Engineering, is the perfect liquidity of a market [1, 2, 3].

This assumption implies that a market is always able to absorb incoming orders without

producing a significant movement in the price.

However in the last ten years a great amount of studies demonstrates that finite liquidity effects play a crucial role in order to understand the features of a modern market [4, 6, 7, 8, 9, 10].

From these studies liquidity appears more important in fixing the price response of a market than the order volume or the flow of information which are canonically assumed in Economics as the main ingredients to explain price movements [11, 12, 13].

The problem of finite liquidity have been highlighted by detailed studies of real order books [14, 15, 16].

In order to explain the empirical features of order books, several analytical and numerical models

have been introduced [17].

A very important class of models for the order book are the so called zero-intelligence models which are characterized by random order deposition mechanisms [18, 19].

In this paper we introduce and discuss a zero-intelligence model of order book to investigate the relation between finite liquidity and price fluctuations.

Zero-intelligence model are in general simple and workable but still able to

reproduce the main properties of real order books.

In order to quantify the liquidity of a given configuration of the order book

we measure it via the average density of the stored orders in the book which

we call granularity.

The analysis of the system response to a granularity fluctuation

can be properly addressed in the framework of a really elementary dynamics

for order placement which differs from the coarse-grained approach used in [19, 20, 21].

We find that the impact of an order, which depends both on its volume and on the granularity of the configuration of the book, is a concave function of the volume.

This reproduces the empirical observations and represents an important test for the model itself.

Our main result is that the price response to an incoming order is inversely proportional to the granularity.

This means that granularity and the associated finite liquidity represent fundamental elements in the price response, which becomes divergent in the limit of vanishing granularity.

From these results it is clear that a realistic modelling of a financial market requires the inclusion of finite liquidity.

The paper is organized in the following way:

in section 2 we describe how an order book works and we introduce the problem of finite liquidity;

in section 3 we define our model and point out similarities and differences with respect to other order book models;

in section 4 we give the criteria to set the model parameters according to empirical data;

in section 5 we introduce granularity as an operational measure of liquidity;

in section 6 we introduce the Market Impact Surface and we study its dependence on both the volume and the granularity;

in section 7 we draw the conclusions and outline the possible extensions of our model.

2 Order book and the role of liquidity

The elementary mechanism of price formation is a double auction where traders

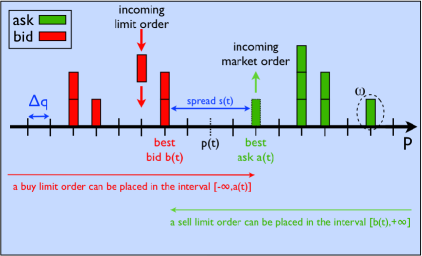

submit orders to buy or sell. The complete list of all orders is called the ’order book’. In Fig. 1 we give a schematic representation of an order book.

There are two classes of orders: market orders and limit orders.

Market orders correspond to the intention of immediately purchase or sale at the best price

(quote) available at that time.

The limit ones instead are not immediately executed since they are offers to buy or sell at a certain quote which is

not necessary the best one. If we consider a sell limit order this means that its quote is higher than (or equal to) the best bid which is the order of buying with the highest price. On the other hand

a buy limit order implies that its price is lower than (or equal to) the best ask which is the order of selling with the lowest price.

The non-zero difference between and is defined as the spread .

The prices of placement of orders (called ’quotes’) are not continuous but quantized in unit of ticks

whose size is an important parameter of an order book.

The price of a stock can be conventionally defined as the mid-price and it can change only if a limit order falls inside the spread or if a market order matches all the orders placed at the best quote.

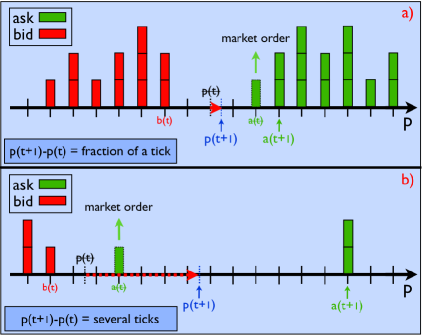

It is clear that the specific configuration of an order book it is a very important

aspect for price movements. A thick book full of orders can absorb the arrival of new orders

without giving rise to large jumps of the price. On the contrary if the book is sparse, even a small

incoming order could trigger a large price variation.

In order to clarify this problem we can consider an order book in the configuration of panel a in Fig. 2.

This situation corresponds to a very liquid market in which the order book can absorb several orders without

large price variations even if they are relatively large. This regime corresponds to the assumptions of the standard financial picture where an order can be immediately executed, its impact is marginal and the market is nearly efficient.

Instead if a liquidity crisis occurs, the configuration of the order book changes dramatically and the situation is like the one represented in panel b in Fig. 2. The orders stored are few, the average distance between them is large and the flow of market orders cannot be easily and immediately absorbed by the system and by consequence

even a small order can produce a large price variation.

Hence a lack of liquidity can dramatically amplify the response of the system.

3 Definition of the model

The purpose of this paper is to study the price response function in presence of liquidity crisis and to

appropriately address this problem we are going to introduce a model with a suitable

microscopic dynamics. Our model can be defined as a ’zero-intelligence’ model as the ones introduced in [19, 20].

It should be noted that the specific questions that we consider cannot be addressed by the dynamics of Refs. [19, 20].

In fact in [19, 20] the deposition is modelled in term of a flow of orders driven by a Poisson process. The orders arrive at each quote at a certain fixed rate so that the deposition interval and the number of orders per unit of time are infinite but the orders per unit price interval are finite. The motivation of the authors of [19, 20] is that in such a way the order book can be never depleted and some finite size effects, due to a finite deposition interval, are avoided.

On the other hand in our model it is preferred an elementary microscopic mechanism for order deposition.

The difference between these two mechanisms for order deposition is

the definition of the time unit.

In the present paper the time unit corresponds to the time (that is not fixed) between two following orders. Instead in Refs. [19, 20] the time unit corresponds to a physical and fixed amount of time (for example equal to some minutes) during which several actions are made

by investors. This permits a coarse-grained description in terms of average quantities, such as order flow.

For the specific implementation of our model we start by considering three mechanisms of deposition which will be compared with the empirical data.

We want to point out that only one of the three mechanisms gives rise to a realistic dynamics.

Certain elements are however common to the three mechanisms and we start by discussing them.

In our set-up, as in a real order book, an order can be placed at a quote that is an integer multiple (positive or negative) of the tick size . In this paper we do not investigate the effects of this parameter; therefore we set it equal to .

For the sake of simplicity we assume that all orders (limit and market) have the same volume . The fact that a market order has the same volume of a limit order is coherent with the observation that in more than of the cases a market order does not exceed the best limit order available [7].

In this model there is one mechanism for order creation, the limit orders deposition, and two for order annihilation, the arrival of market orders and the cancellation process of limit orders. The cancellation of a limit order occurs when the order has been stored in the book for time steps without being executed, where is a parameter to be fixed111We know that this assumption, reasonable for the present study,

is far to be realistic from the moment that

analysis of real order books have shown that the lifetime of a limit order increases monotonically with its distance from the mid-price [15, 21].

The balancing of the three mechanisms of creation/annihilation fixes the properties of the steady state that is reached very quickly (about steps if ranges between and ).

Two limit orders can be also removed from the order book when the spread is zero, that is when an incoming limit order is placed at the opposite best quote. However, these events are very unlikely ( of the number of the market orders) and their effect is negligible.

We define the price as the mid-price where and are the quotes of the best ask and of the best bid.

In our model we completely neglect the daily closures of the market and therefore the strong price variations during the night.

The typical length of a run is time steps ( if a larger sample is needed) which corresponds to a real sample of about years, estimating about operations per day.

3.1 Order deposition

Now we are going to discuss three possible cases for order deposition which we will test with respect to empirical data in order to select the most appropriate mechanism. Due to the symmetry of the order book, the probability that an order is a sell or a buy one is always the same.

3.1.1 Case 1

Once the nature (buy or sell) is determined, the order can be a market one with probability and a limit one with probability , with . Limit orders will be placed in the interval or depending on their nature (sell or buy respectively). The probability distribution within these intervals is considered uniform and is a free parameter to be fixed. Hence the deposition interval is independent on the spread size.

3.1.2 Case 2

The order can be a market one with probability and a limit one with probability with as in case . A limit order will be placed in the interval or with with a uniform distribution, being the spread. In this case the length of the deposition interval depends on the spread size through a sort of auto-regressive process. This implies that the probability that a limit order produces a price variation (i.e. an order is placed inside the spread) is time-independent and approximately equal to . We anticipate that this second case will turn out to be the more realistic one with respect to the empirical data.

3.1.3 Case 3

The third case is inspired by the mechanism proposed in [21]. First a number in the interval is extracted. If the order is a limit order otherwise it is a market one. If the order is a sell limit order its quote is . On the contrary if the order is a buy one its quote is . In such a way the probability of being a market or a limit order is not set a priori.

We have previously mentioned that our choice for order deposition produces a finite number of orders stored in the order book and a finite depth. This causes a finite size effect: the order book is subject to complete depletion with a cut off in those quantities linked with the book depth. However the probability of a complete depletion goes very quickly to when the cancellation parameter is increased (this probability is less than for ).

Moreover we note that the uniform deposition mechanisms used in this paper cannot reproduce in a realistic way all the empirical features of the order book; nevertheless this assumption has been made with the aim to define a minimal model still able to reproduce the main properties of the order book. Besides, the main goal of this work is the evaluation the effects of the granularity in price fluctuations, which depends on the static realization of the profile.

4 Calibration of parameters and preliminary results

In this section we check the properties of the models we have introduced with respect to the empirical data. This analysis will also allow us to decide how to calibrate the parameters.

The empirical results of Ref. [7] indicate that a realistic value for is approximately . In case the probability of being a market or a limit order is not fixed a priori. Nevertheless in this case we find that the fraction of market orders tends to a realistic value (about ) when grows, and becomes substantially independent on when the probability of emptying the order book turns to be negligible (i.e. ). This feature does not seem to depend crucially on the parameter .

We now have to fix the remaining parameters.

Two quantities that can be calibrated on empirical data are the average spread and the average number of stored orders . The parameters of the model which rule these quantities are

, (case ) and (case and ).

Since it is not always possible to a find a configuration of all parameters able to

reproduces these two quantities in a realistic way, we give priority to those sets of parameters that produce a reasonable average number of orders.

All three cases exhibit a realistic accumulation of orders (i.e. orders per side) for ranging from to . This clarifies the role of in driving the average number of orders in the steady state. In case we choose and in case , in such a way the order book has approximately the same depth in both cases. For these two cases we applied the previous criterion of priority in order to have a realistic average number of orders.

Case appears to be very interesting because it exists a range of parameters for which we can reproduce both a realistic average spread and average number of orders. For instance for , we obtain an average number of orders per side of about and ticks. In Table 1 we report a summary of the results for the tested parameters. We have only reported some selected results and a more detailed and systematic analysis will be given in a future survey [27].

| Case 1 | Case 2 | Case 3 | |

| / | |||

| 200 | / | 100 | |

| / | or | / | |

| General | Realistic case | ||

| remarks | |||

| for , |

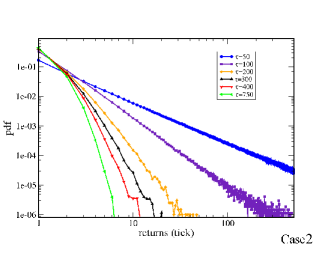

It is worth noticing that the auto-regressive case is also interesting with respect to the Stylized Facts. In fact only in this case we can observe some volatility clustering in the price increments (returns). All cases exhibit a return probability density function which decades as a power law (see Fig. 3) but only in the second case the exponent of the tail is compatible with the empirical observations (). For instance in case we find for and for .

5 Operational estimator of the granularity

Given a certain configuration of the order book we want to define a way to measure the liquidity of it. In fact our objective is a detailed study of the relation between finite liquidity and price fluctuations.

We would like to describe the effect that the order book may not be compact but characterized by orders separated by voids.

In order to perform this analysis we are going to introduce a function which we call granularity.

We propose a definition for granularity which is related to the inverse of the size of the average void between two adjacent quotes (gaps). At each time the spread sets a characteristic length which can be used as unit of measurement for these gaps.

However we are also interested in measuring the granularity of the order book in a region far from the best quotes since the two sides of the order book usually have a depth much larger than . Therefore we define a partitioning of size of one side of the order book and we perform the following average

| (1) |

where is the number of intervals of length defined by the partition (we require in order to calculate ) and is the volume of orders in an interval of length . From the definition of we observe that is approximately the range of the order book and consequently the granularity results equal to the average linear density of orders

| (2) |

where . For the sake of simplicity we now drop the temporal dependence of and the brackets of the average. We note that the definition of granularity given in Eq. (2) does not measure the real average size of the voids because more than one order can be stored at the same quote. Therefore can be seen as the equivalent gap between two adjacent quotes in an hypothetical system where each quote can store only one order. We also observe that in the limit of a continuous order book, the price variation produced by an order of volume would be

| (3) |

where is the density of the stored orders. If we approximate with its average value we find the following scaling relation for and

| (4) |

In this framework a liquidity crisis occurs when , on the contrary the market is very liquid if . In fact when is very large a great amount of orders can be executed without producing a significant price variation.

The granularity defined by Eq. (2) has the dimension of a . In order to obtain an absolute parameter for liquidity, we define the dimensionless liquidity as . As we have seen in section 3 at this stage we are not interested in the effect of the tick size on the model so we have set it equal to . Consequently the dimensional and the dimensionless liquidity numerically coincide. Furthermore we want to point out that the definition of given by Eq. (2) is not directly related to a specific disposition in the order book but it gives only an average information about the void size.

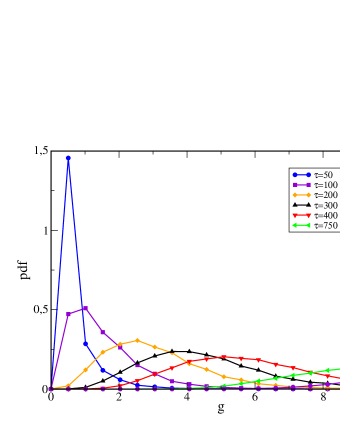

In Fig. 4 we show the histogram of for the model labelled as ’case ’.

The probability to observe a liquidity crisis, as expected, vanishes when because of the large amount of orders stored in the order book. However, this probability cannot be neglected for values of ranging from to that we have previously recognized as the realistic ones.

It is important to note that in this paper we give a different definition of granularity with respect to the definition of Ref. [20]. In fact in that paper the authors define two dimensionless parameters to describe the discreteness of the system: the first, named granularity, is the dimensionless order size, the second one is the dimensionless tick size. In a certain sense both aspects are included in our definition of granularity and combined in a single parameter. These different choices are motivated by different purposes, while the authors of [20] gives the priority to the parameters that describe the order flows, differently we are going to focus our attention on how the discreteness influences the response function of the system.

6 Price Impact Surface

In this section we restrict our analysis to the ’case ’ mechanism for order deposition and all the results reported here correspond to and . In order to analyze the average response of the system to an external perturbation (i.e. the volume of an incoming market order) after a certain time lag , we introduce the Price Impact Function defined as

| (5) |

One can consider two interesting limits of Eq. (5), the asymptotic limit () and the instantaneous limit (). In this paper we restrict our investigation to the second case because the persistent effects on the market cannot be fully explained by a zero-intelligence model which neglects all the time-correlated structures of the order deposition (see[8, 9, 10, 28, 29]).

Now we are going to consider also

the dependence of on the granularity .

In this way we have to deal with a Price Impact Surface rather than a Price Impact Function and we can

analyze how the price response of the system depends both on the order volume and on the granularity .

Hence we define the Price Impact Surface as

| (6) |

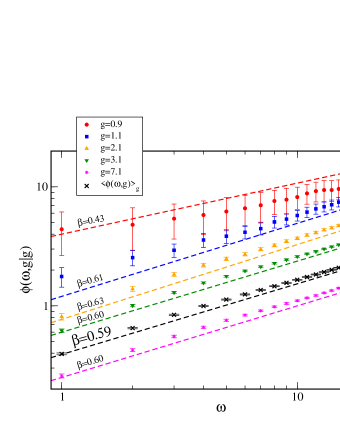

Before investigating the dependence of the price response surface on we should verify the well-known empirical property that (i.e. the standard Price Impact Function defined as in Eq. (5)) is a concave function with respect to the order volume . This is a manifestation of the fact that the order book is far from being in a linear regime. While the agreement on the concavity is almost universal, different functional form of the Impact Function have been given: the authors of [15] propose , instead other authors propose with exponent ([32]) and ([8, 31]). In Fig. 5 we find that the surface averaged on (black crosses) is concave and follows a power law

| (7) |

6.1 Price Impact Surface in the direction of

Now we consider the Price Impact Surface as a function of for fixed values of . We see from Fig. 5 that its behavior is a power law where the exponent and the amplitude depend on

| (8) |

This function is highly concave for small value of and grows for increasing values of . However we notice that the dependence of the amplitude on is far stronger than the one of . This implies, as expected, that the Impact Surface produces smaller variation of price in the limit of large , even if the exponent is larger.

It is worth noticing that the observed scaling behavior for is different from the one predicted by the zero order approximation made in Eq. 4. This is due to the peculiar shape of the order book profile whose maximum is peaked far from the best quote.

The results of Fig. 5 are qualitatively similar to those of Fig. 6 of Ref. [20] even if the different definitions of granularity do not permit a detailed comparison of the two models.

6.2 Price Impact Surface in the direction of

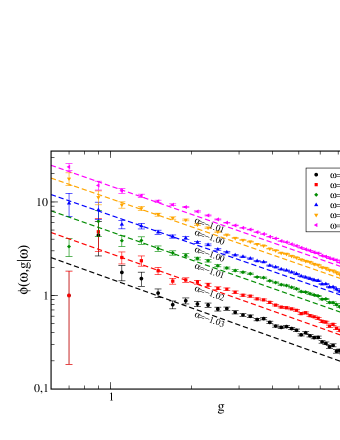

Now we analyze the price variation as a function of the granularity for a fixed volume of the incoming market order. We find that the -dependence of the surface is well represented by a power law

| (9) |

In this case the exponent is negative and it appears to be nearly independent on (see Fig. 6). In fact we find that its value is (within the error bars) for all values of . Consequently when the granularity vanishes the response of the system diverges. We can now quantitatively analyze how this limit is approached for finite

(but large) values of . For example if we consider an order of size ,

the average price variation induced when is about ten times greater than the one observed when .

Therefore we have found that the amplification induced by the discreteness of the system is approximately proportional to the equivalent gap measured by as predicted by the zero order approximation of section 5.

However we want to stress that for small values of some deviations from the scaling behavior seem to be observed. This fact suggests that, when vanishes, the deviation of

the density from the average density measured by , is significant.

Further investigation of this aspect will be considered in future works.

The fact that the exponent of the power law in the direction of does not seem to exhibit a significant dependence on may suggest a possible factorization of the price impact surface, as we are going to verify in the next section.

6.3 Factorization of the Price Surface Impact

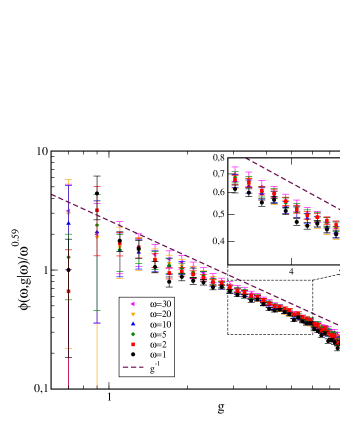

In Ref. [15] the authors observe that the empirical impact function admits the following factorization

| (10) |

Similarly we verify whether the Impact Surface Function could be expressed in the following way

| (11) |

To check if the factorization of Eq. (11) is correct we have to verify if it exists a function of such that the impact surface divided by this function turns out to be independent on . This is equivalent to say that we would like to observe a complete collapse into a unique curve

by rescaling with this function the surface .

The simplest choice for this scaling function is the average impact function . We report the rescaled functions for different values of in Fig. 7 and we observe a nearly perfect collapse for within error bars.

In principle we cannot obtain a perfect factorization because of the dependence of the exponent on .

Nevertheless we observe that this dependence is very weak, especially for when

. In fact in Fig. 7 one can appreciate

some discrepancies only for .

We can conclude that the factorization proposed in Eq. (11) approximately holds at least for small values of . We also expect that can be factorized with respect to its variables, instead the situation may be very complicated for the function since depend on time. We will consider these points in future investigations.

7 Conclusions

In this paper we have introduced a model of order book to study the generalized Price Impact Function (Price Impact Surface) and its dependence not only on order volume but also on granularity.

We find that the granularity operates as a strong amplifier of price variations

when a liquidity crisis takes place.

In particular the dependence of the Price Impact Surface on the granularity is a power law

with exponent nearly equal to . This result implies that the system response to an incoming order

diverges in the limit of vanishing granularity.

It would be interesting to compare the Price Impact Surface found in the model with the empirical one.

Furthermore agent-based models for financial markets usually do not take into account the problem of finite liquidity.

In fact a common way to model the price movements in an agent based model is through the Walras’ mechanism in which the price adjustments are proportional to the excess demand i.e. .

The coefficient and the excess demand are generally assumed to be independent on granularity.

If, in first approximation, one interprets the Market Impact Function as the quantity the price movements are proportional to in the Walras’ mechanism, then the previous coefficient must depends on granularity.

Moreover we have observed that the Price Impact Surface can be factorized and we can try to identify the excess demand with and with .

Consequently we aim at introducing this dependence on in the workable agent based model we have introduced in previous papers [23, 24, 25, 26].

In this framework we expect that even small unbalances of the market can produce large price adjustments if a liquidity crisis is present. Therefore the role of the amplification introduced by could be one of the explanation of the breaking of the cause-effect relation and so that small perturbations can produce large fluctuations.

Acknowledgments

We are grateful to Doyne Farmer, Gabriele La Spada, Marcello Mezzedimi and the anonymous referee for interesting discussions and suggestions.

References

- [1] M. Goodfriend and R. G. King. The New Neoclassical Synthesis. NBER Macroeconomics Annual, 1997.

- [2] J. Hasbrouck. Empirical Market Microstructure. Oxford University Press, 2007.

- [3] L. Harris. Trading and Exchanges. Oxford University Press, 2003.

- [4] F. Lillo and J. D. Farmer. The key role of liquidity fluctuations in determining large price changes. Fluctuation and Noise Letters, 5(2):209–216, 2005.

- [5] A. Joulin, A. Lefevre, D. Grunberg, and J.-P. Bouchaud. Stock price jumps: news and volume play a minor role. [physics.soc-ph] arXiv:0803.1769v1, 2008.

- [6] P. Weber and B. Rosenow. Large stock price changes: volume and liquidity. Quant. Fin., 6(1):7–14, 2006.

- [7] J. D. Farmer, L. Gillemot, F. Lillo, S. Mike, and A. Sen. What really causes large price changes?. Quant. Fin., 4(4):383–397, 2004.

- [8] J. D. Farmer, A. Gerig, F. Lillo, and S. Mike. Market efficiency and the long-memory of supply and demand: Is price impact variable and permanent or fixed and temporary. Quant. Fin., 6(2):107–112, 2006s.

- [9] J.-P. Bouchaud, J. Kockelkoren, and M. Potters. Random walks, liquidity molasses and critical response in financial markets. Quant. Fin., 6(2):115–123, April 2004.

- [10] J.-P. Bouchaud, J. D. Farmer, and F. Lillo. How Markets Slowly Digest Changes in Supply and Demand. Elsevier: Academic Press, 2008.

- [11] M. Gallegati and L. Pietronero. Why financial markets are unstable? submitted to The Economists’ Voice, 2008.

- [12] J.-P. Bouchaud . Economics needs a scientific revolution. Nature, 455(1185):176–190, 2008.

- [13] M. Marsili. Eroding market stability by proliferation of financial instruments. Available at SSRN: http://ssrn.com/abstract=1305174, 2008.

- [14] J.-P. Bouchaud, M. Mezard, and M. Potters. Statistical properties of stock order books: empirical results and models. Quant. Fin., 2:251–256, 2002.

- [15] M. Potters and J.-P. Bouchaud. More statistical properties of order books and price impact. Physica A, 324(1.2):133–140, 2003.

- [16] M. Wyart, J.-P. Bouchaud, J. Kockelkoren, M. Potters, and M. Vettorazzo. Relation between bid-ask spread, impact and volatility in order-driven markets. Quant. Fin., 8(1):41–57, 2008.

- [17] F. Slanina. Critical comparison of several order-book models for stock-market fluctuations. Eur. Phys. J. B, 61:225–240, 2008.

- [18] D. Challet and R. Stinchcombe. Non-constant rates and overdiffusive prices in simple models of limit order markets. Quant. Fin., 3:155–162, 2003.

- [19] M. G. Daniels, J. D. Farmer, L. Gillemot, G. Iori, and E. Smith. Quantitative model of price diffusion and market friction based on trading as a mechanistic random process. Phys. Rev. Lett., 90(10):108102, March 2003.

- [20] E. Smith, J. D. Farmer, L. Gillemot, and S. Krishnamurthy. Statistical theory of the continuous double auction. Quant. Fin., 3(6):481–514, 2003.

- [21] S. Mike and J. D. Farmer. An empirical behavioral model of liquidity and volatility. J Economic Dynamics and Control, 32(1):200–234, 2008.

- [22] J.D. Farmer, P. Patelli, and I.I. Zovko. The predictive power of zero intelligence in financial market. PNAS, 102:2254–2259, 2005.

- [23] V. Alfi, L. Pietronero, and A. Zaccaria. Minimal agent based model for the origin and self-organization of stylized facts in financial markets. EPL, 86:58003, 2009.

- [24] V. Alfi, M. Cristelli, L. Pietronero, and A. Zaccaria. Minimal agent based model for financial markets I: origin and self-organization of stylized facts. Eur. Phys. J. B, 67:385–397, 2009.

- [25] V. Alfi, M. Cristelli, L. Pietronero, and A. Zaccaria. Minimal agent based model for financial markets II: statistical properties of the linear and multiplicative dynamics. Eur. Phys. J. B, 67:399–417, 2009.

- [26] V. Alfi, M. Cristelli, L. Pietronero, and A. Zaccaria. Mechanisms of self-organization and finite size effects in a minimal agents based model. J. Stat., P03016 , 2009.

- [27] V. Alfi, M. Cristelli, L. Pietronero, and A. Zaccaria. preprint.

- [28] J.-P. Bouchaud, Y. Gefen, M. Potters, and M. Wyart. Fluctuations and response in financial markets: the subtle nature of random price changes. Quant. Fin., 4:176–190, 2004.

- [29] F. Lillo, S. Mike, and J. D. Farmer. Theory for long memory in supply and demand. Phys. Rev. E, 71:066122, 2005.

- [30] F. Lillo, J. D. Farmer, and R. N. Mantegna. Single curve collapse of price impact function for the New York Stock Exchange. arXiv:cond-mat/0207428, 2002.

- [31] J. D. Farmer and F. Lillo. On the origin of power law tails in price fluctuations. Quant. Fin., 4(1):7–11, 2004.

- [32] V. Plerou, P. Gopikrishnan, X. Gabaix, and H. E. Stanley. Quantifiying stock-price response to demand fluctuations. Phys. Rev. E, 324(1-2):66, 2002.