Time series technical analysis via new fast estimation methods: a preliminary study in mathematical finance

Abstract

: New fast estimation methods stemming from control theory lead to a fresh look at time series, which bears some resemblance to “technical analysis”. The results are applied to a typical object of financial engineering, namely the forecast of foreign exchange rates, via a “model-free” setting, i.e., via repeated identifications of low order linear difference equations on sliding short time windows. Several convincing computer simulations, including the prediction of the position and of the volatility with respect to the forecasted trendline, are provided. -transform and differential algebra are the main mathematical tools.

keywords:

Time series, identification, estimation, trends, noises, model-free forecasting, mathematical finance, technical analysis, heteroscedasticity, volatility, foreign exchange rates, linear difference equations, -transform, algebra.1 Introduction

1.1 Motivations

Recent advances in estimation and identification (see, e.g., Fliess & Sira-Ramírez (2003, 2004); Fliess, Join & Sira-Ramírez (2004); Fliess & Sira-Ramírez (2008); Fliess, Join & Sira-Ramírez (2008) and the references therein) stemming from mathematical control theory may be summarized by the two following facts:

-

•

Their algebraic nature permits to derive exact non-asymptotic formulae for obtaining the unknown quantities in real time.

-

•

There is no need to know the statistical properties of the corrupting noises.

Those techniques have already been applied in many concrete situations, including signal processing (see the references in Fliess (2008)). Their recent and successful extension to discrete-time linear control systems Fliess, Fuchshumer, Schöberl, Schlacher & Sira-Ramírez (2008) has prompted us to study their relevance to financial time series.

Remark 1.1

Remark 1.2

The title of this communication is due to its obvious connection with some aspects of technical analysis, or charting (see, e.g., Aronson (2007); Béchu, Bertrand & Nebenzahl (2008); Kaufman (2005); Kirkpatrick & Dahlquist (2006); Murphy (1999) and the references therein), which is widely used among traders and financial professionals.111Technical analysis is often severely criticized in the academic world and among the practitioners of mathematical finance (see, e.g., Paulos (2003)).

1.2 Linear difference equations

Consider the univariate time series : is not regarded here as a stochastic process like in the familiar ARMA and ARIMA models but is supposed to satisfy “approximatively” a linear difference equation

| (1) |

where . Introduce as in digital signal processing the additive decomposition

| (2) |

where

- •

-

•

the additive “noise” is the mismatch between the real data and the trendline.

Thus

| (3) |

where

| (4) |

We only assume that the “ergodic mean” of is , i.e.,

| (5) |

It means that, , the moving average

| (6) |

is close to if is large enough. It follows from Eq. (4) that also satisfies the properties (5) and (6). Most of the stochastic processes, like finite linear combinations of i.i.d. zero-mean processes, which are associated to time series modeling, do satisfy almost surely such a weak assumption. Our analysis

-

•

does not make any difference between non-stationary and stationary time series,

-

•

does not need the often tedious and cumbersome trend and seasonality decomposition (our trendlines include the seasonalities, if they exist).

1.3 A model-free setting

It should be clear that

-

•

a concrete time series cannot be “well” approximated in general by a solution of a “parsimonious” Eq. (1), i.e., a linear difference equation of low order;

-

•

the use of large order linear difference equations, or of nonlinear ones, might lead to a formidable computational burden for their identifications without any clear-cut forecasting benefit.

We adopt therefore the quite promising viewpoint of Fliess & Join (2008) where the control of “complex” systems is achieved without trying a global identification but thanks to elementary models which are only valid during a short time interval and are continuously updated.333See the numerous examples and the references in Fliess & Join (2008) for concrete illustrations. We utilize here low order difference equations.444Compare with Markovsky, Willems, van Huffel, de Moor & Pintelon (2005). Then the window size for the moving average (6) does not need to be “large”.

1.4 Content

Sect. 2, which considers the identifiability of unknown parameters, extends to the discrete-time case a result in Fliess (2008). The convincing computer simulations in Sect. 3 are based on the exchange rates between US Dollars and €uros. Besides forecasting the trendline, we predict

-

•

the position of the future rate w.r.t. the forecasted trendline,

-

•

the standard deviation w.r.t. the forecasted trendline.

Those results might lead to a new understanding of volatility and risk management.555See Taleb (1997) for a critical appraisal of the existing literature on this subject, which is of utmost importance in financial engineering. (Extreme) risks are discussed in Bouchaud & Potters (1997); Dacorogna, Gençay, Müller, Olsen & Pictet (2001); Mandelbrot & Hudson (2004); Sornette (2003) from quite different perspectives. It is the trendline which would exhibit abrupt changes in our setting (compare with the probabilistic standpoint; see, e.g., Wilmott (2006) and the references therein). Our estimation techniques permit an efficient change-point detection Mboup, Join & Fliess (2008), which needs to be extended, if possible, to some kind of forecasting. Sect. 4 concludes with a short discussion on the notion of trend.

2 Parameter identification

2.1 Rational generating functions

Consider again Eq. (1). The -transform of satisfies (see, e.g., Doetsch (1967); Jury (1964))

| (7) |

It shows that , which is called the generating function of , is a rational function of , i.e., :

| (8) |

where

Hence

Proposition 2.1

, , satisfies a linear difference equation (1) if, and only if, its generating function is a rational function.

It is obvious that the knowledge of and permits to determine the initial conditions .

Remark 2.2

Consider the inhomogeneous linear difference equation

where , . Then the -transform of is again rational. It is equivalent saying that , , still satisfies a homogeneous difference equation.

2.2 Parameter identifiability

2.2.1 Generalities

Let

be the field generated over the field of rational numbers by , which are considered as unknown parameters and therefore in our algebraic setting as independent indeterminates Fliess & Sira-Ramírez (2003); Fliess, Join & Sira-Ramírez (2004); Fliess & Sira-Ramírez (2008). Write the algebraic closure of (see, e.g., Lang (2002); Chambert-Loir (2005)). Then , i.e., is a rational function over . Moreover is a differential field (see, e.g., Chambert-Loir (2005)) with respect to the derivation . Its subfield of constants is the algebraically closed field .

Introduce the square Wronskian matrix of order Chambert-Loir (2005) where its -row, , is

| (9) |

It follows from Eq. (7) that the rank of is if, and only if, does not satisfy a linear difference relation of order strictly less than . Hence

Theorem 2.3

If does not satisfy a linear difference equation of order strictly less than , then the parameters

are linearly identifiable.666It means following the terminology of Fliess & Sira-Ramírez (2003, 2008) that are uniquely determined by a system of linear equations, the coefficients of which depend on and , .

2.2.2 Identifiability of the dynamics

For identifying the dynamics, i.e., , without having to determine the initial conditions consider the Wronskian matrix , where its -row, , is

It is obtained by taking the -dependent entries in the last rows of type (9), i.e., in disregarding the entries depending on . The rank of is again . Hence

Corollary 2.4

are linearly identifiable.

2.2.3 Identifiability of the numerator

Assume now that the dynamics is known but not the numerator in Eq. (8). We obtain from the first rows (9). Hence

Corollary 2.5

are linearly identifiable.

2.3 Some hints on the computer implementation

We proceed as in Fliess & Sira-Ramírez (2003, 2008) and in Fliess, Fuchshumer, Schöberl, Schlacher & Sira-Ramírez (2008). The unknown linearly identifiable parameters are solutions of a matrix linear equation, the coefficients of which depend on . Let us emphasize that we substitute to its filtered value thanks to a discrete-time version of Mboup, Join & Fliess (2009).777See, e.g., Gençay, Selçuk & Hafner (2002) for an excellent presentation of various filtering techniques in economics and finance.

3 Example: Forecasting 5 days ahead the $ - € exchange rates

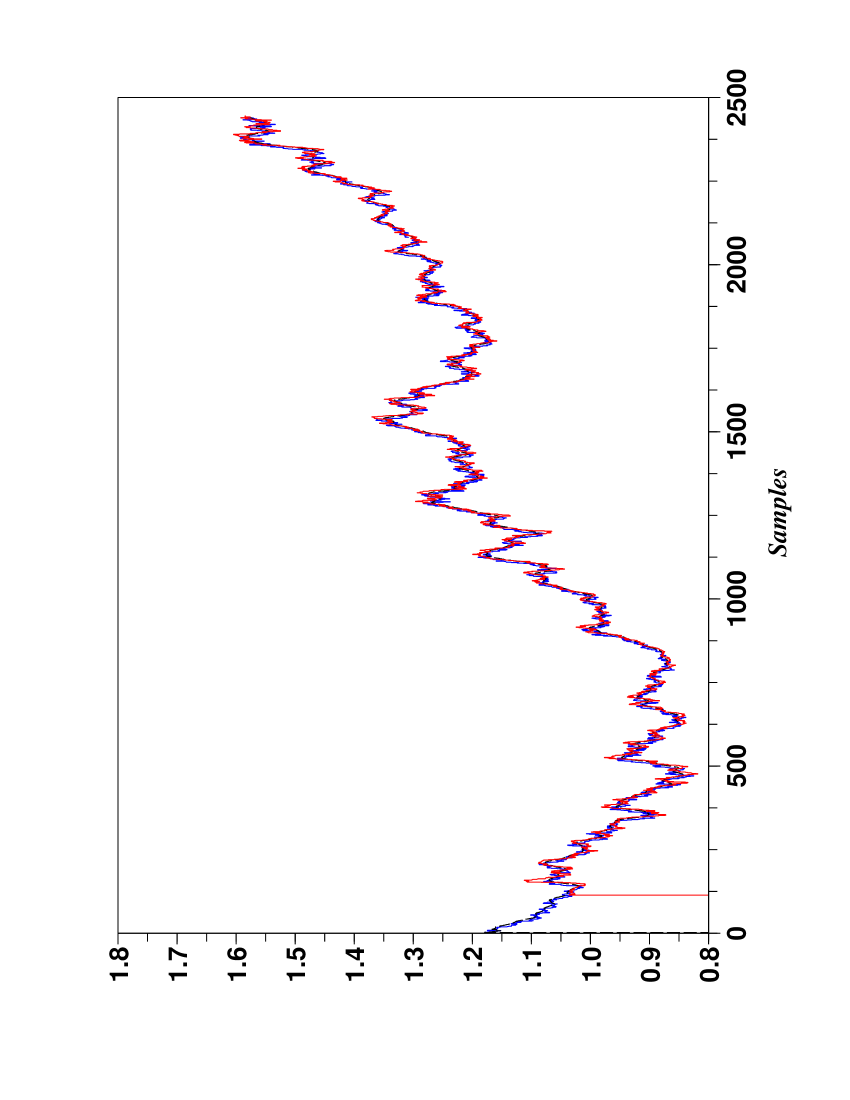

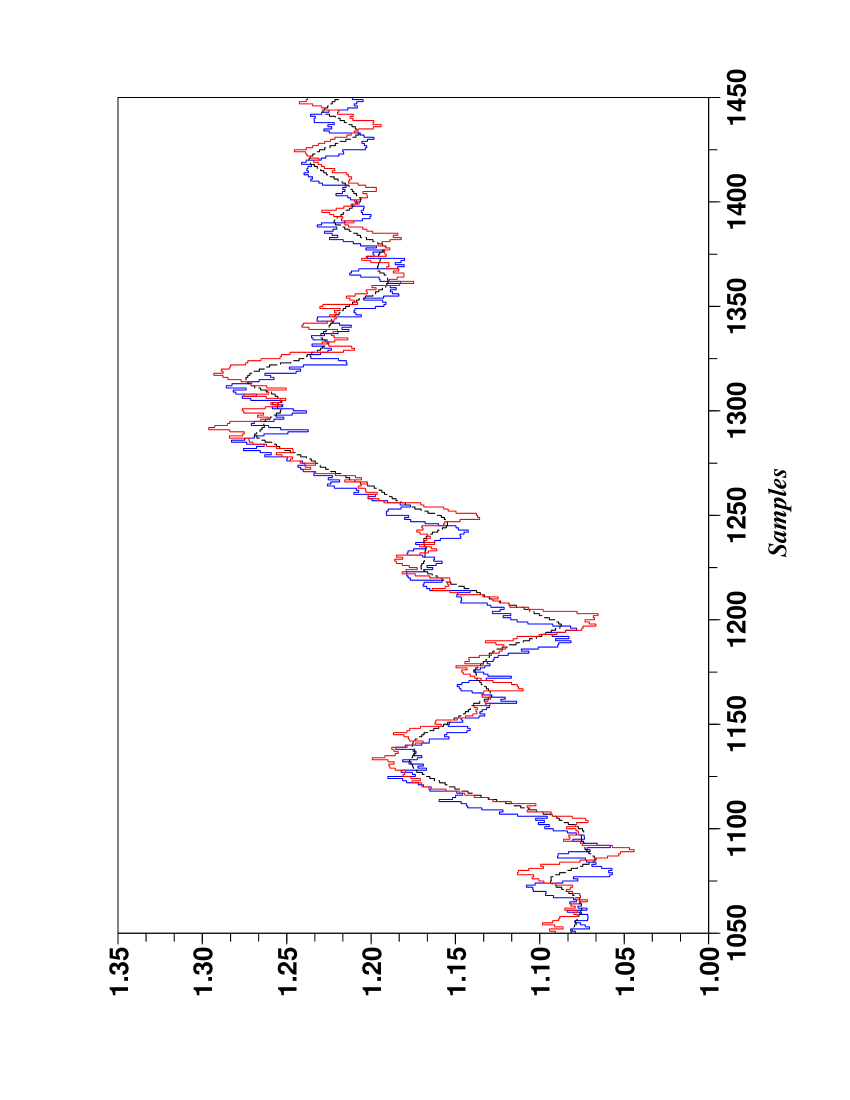

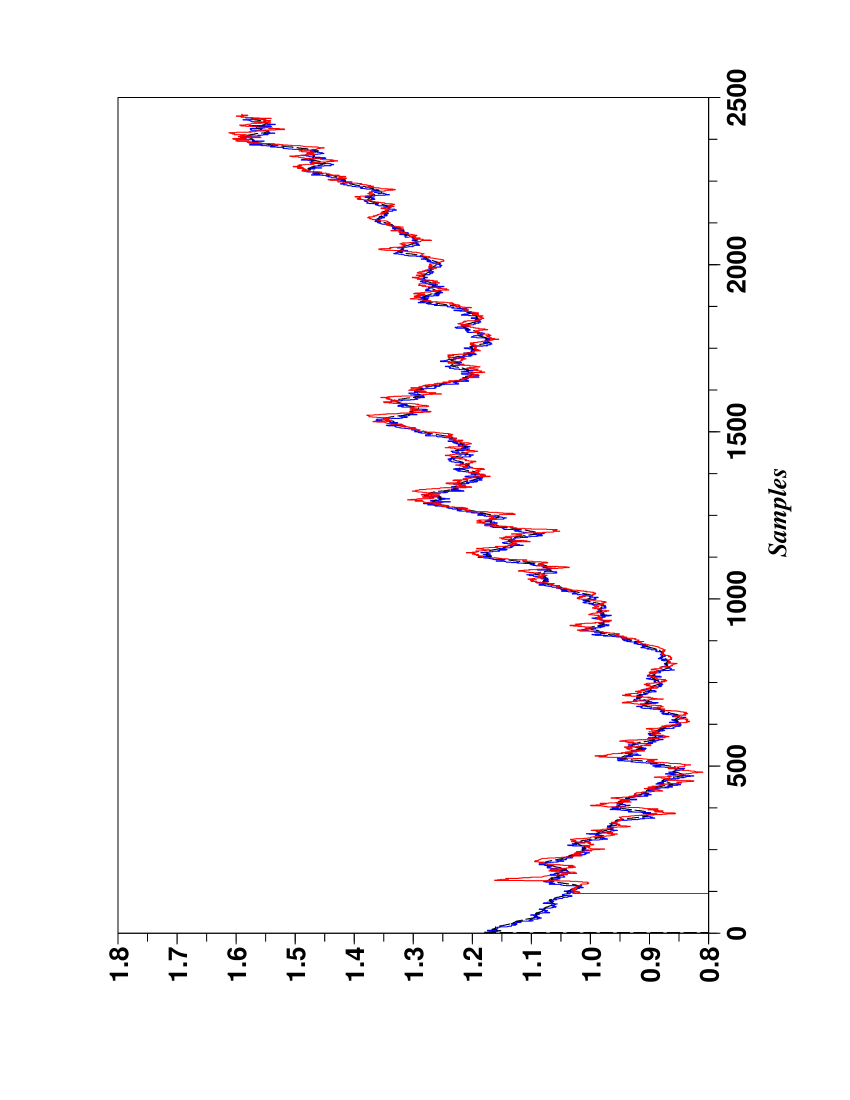

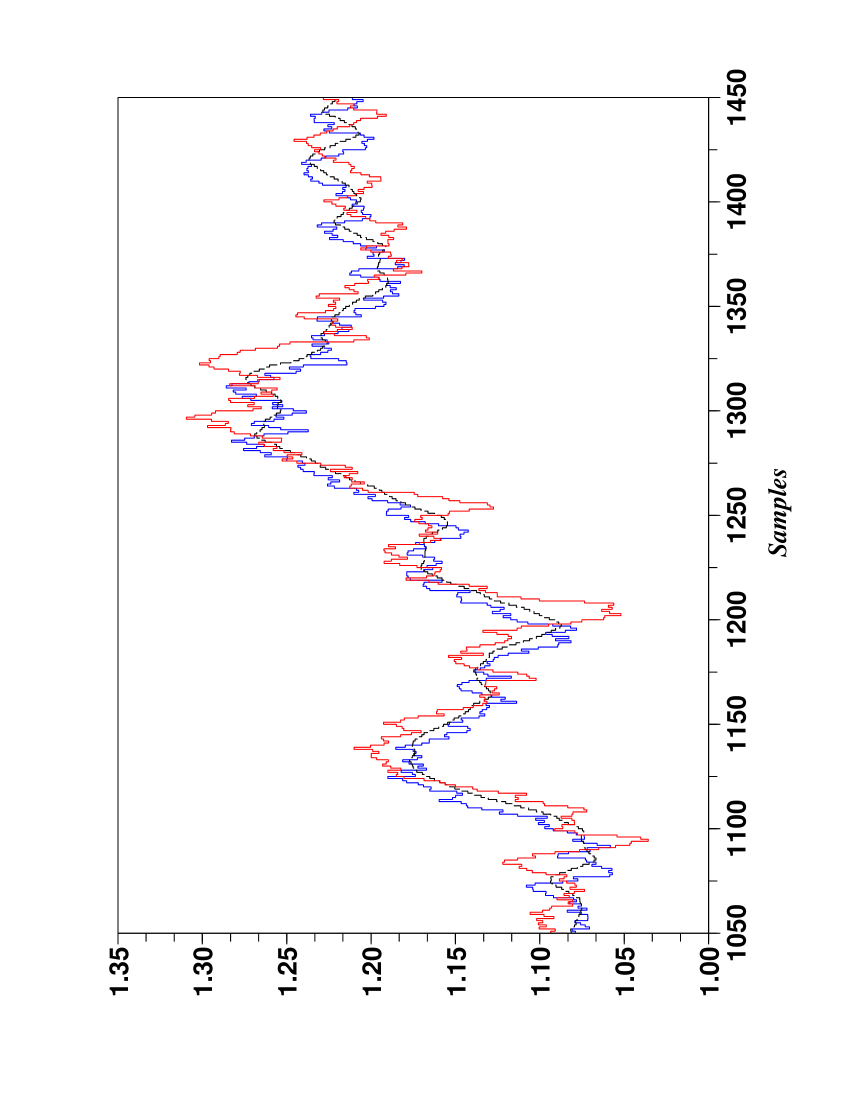

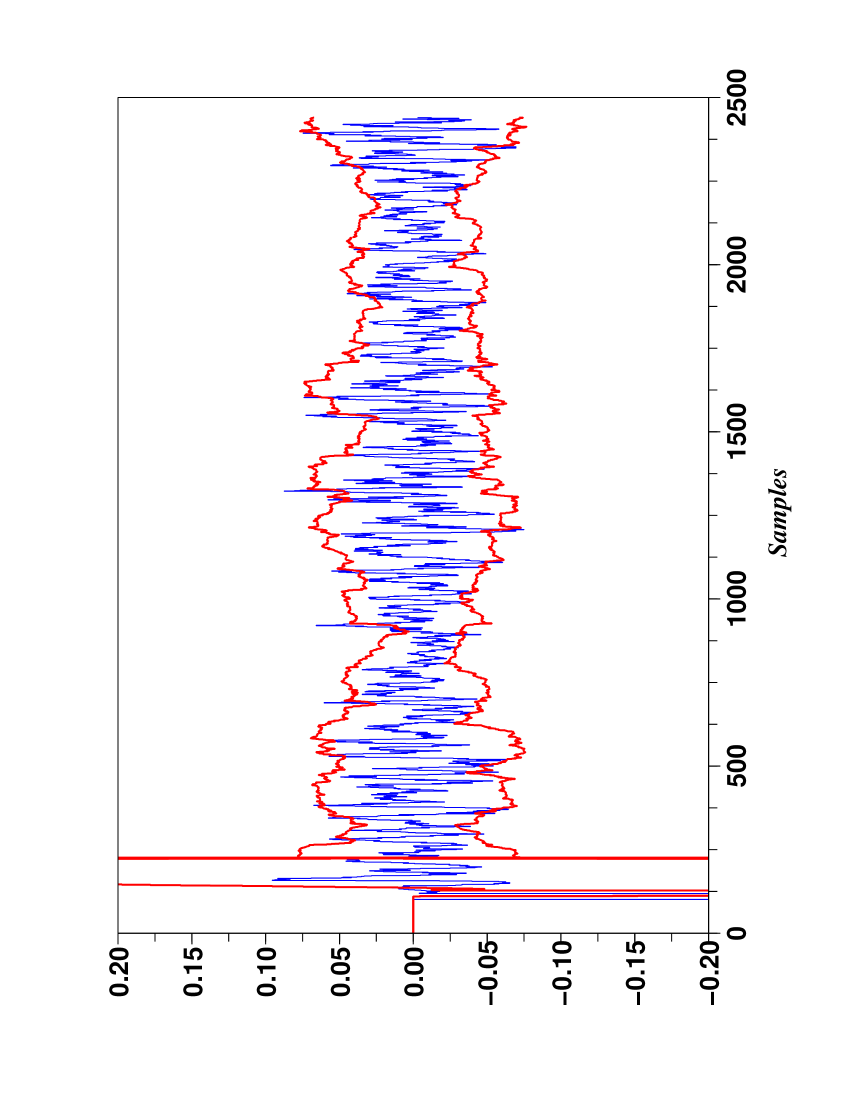

We are utilizing data from the European Central Bank, depicted by the blue lines in the Figures 1 and 2, which summarize the last daily exchange rates between the US Dollars and the €uros.888The authors are perfectly aware that only computations dealing with high frequency data might be of practical value. This type of results will be presented elsewhere.

3.1 Forecasting the trendline

In order to forecast the exchange rate days ahead we apply the rules sketched in Sect. 2.3 and we utilize a linear difference equation (1) of order (the filtered values of the exchange rates are given by the black lines in the Figures 1, 2). Fig. 3 provides the estimated values of the coefficients of the difference equation. The results on the forecasted values of the exchange rates are depicted by the red lines in the Figures 1 and 2, which should be viewed as a predicted trendline.

3.2 Above or under the predicted trendline?

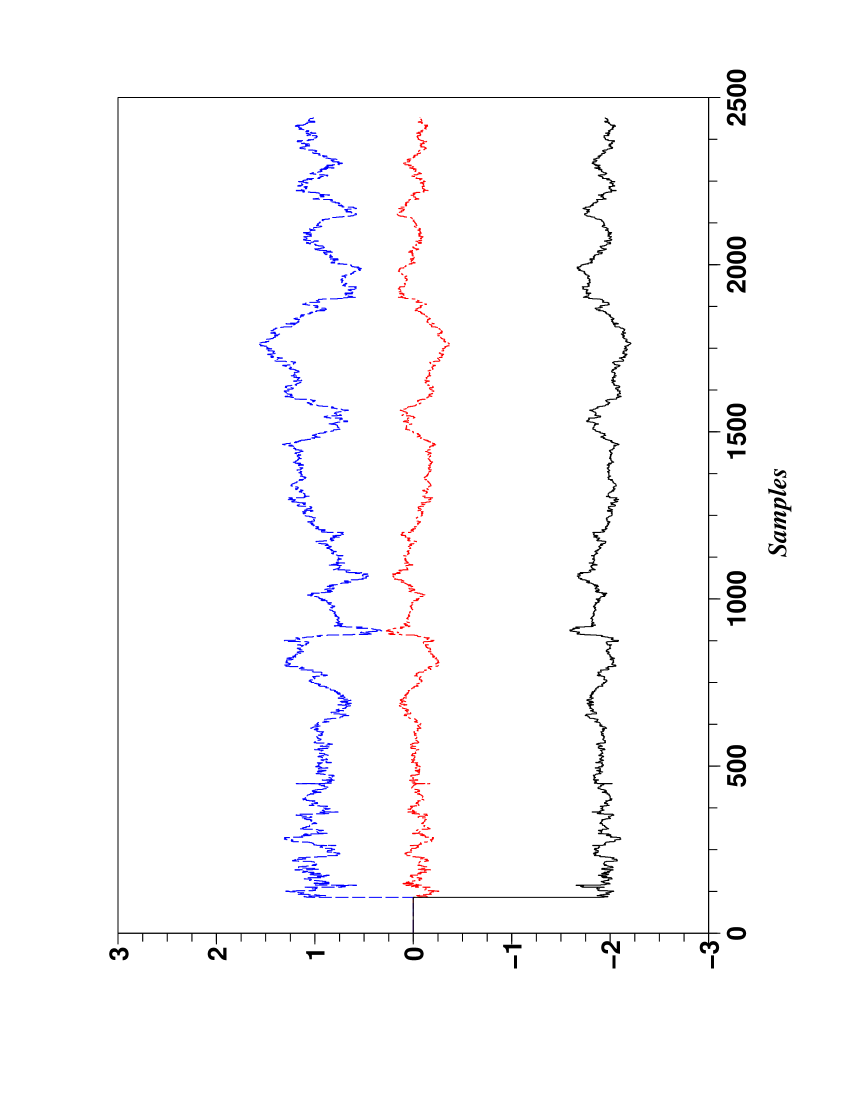

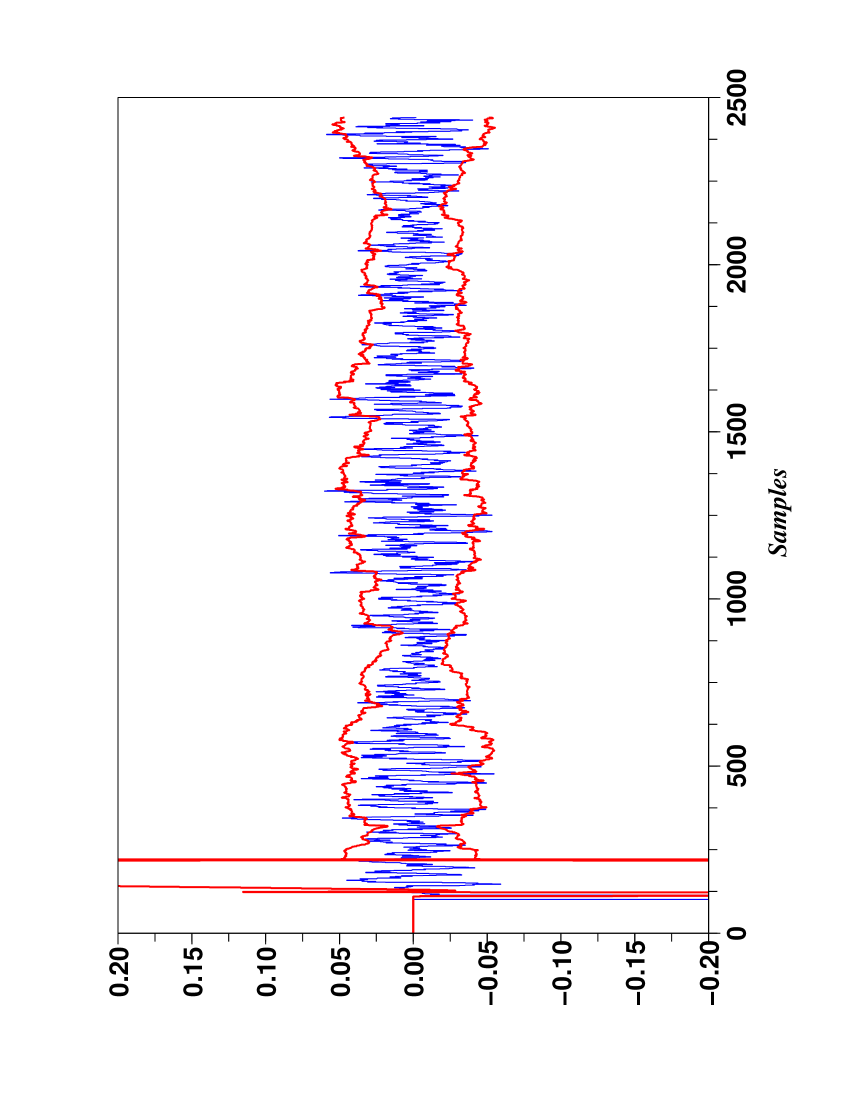

Consider again the “error” in Eq. (2) and its moving average in Eq. (6). Forecasting as in Sect. 3.1 tells us an expected position with respect to the forecasted trendline. The blue line of Fig. 4 displays the result for the window size . The meaning of the indicators and is clear.

Table 1 compares for various window sizes the signs of the predicted values of , which tells us if one should expect to be above or under the trendline, with the true positions of with respect to the trendline. The results are expressed via percentages.

| Window’s size | Percentage |

|---|---|

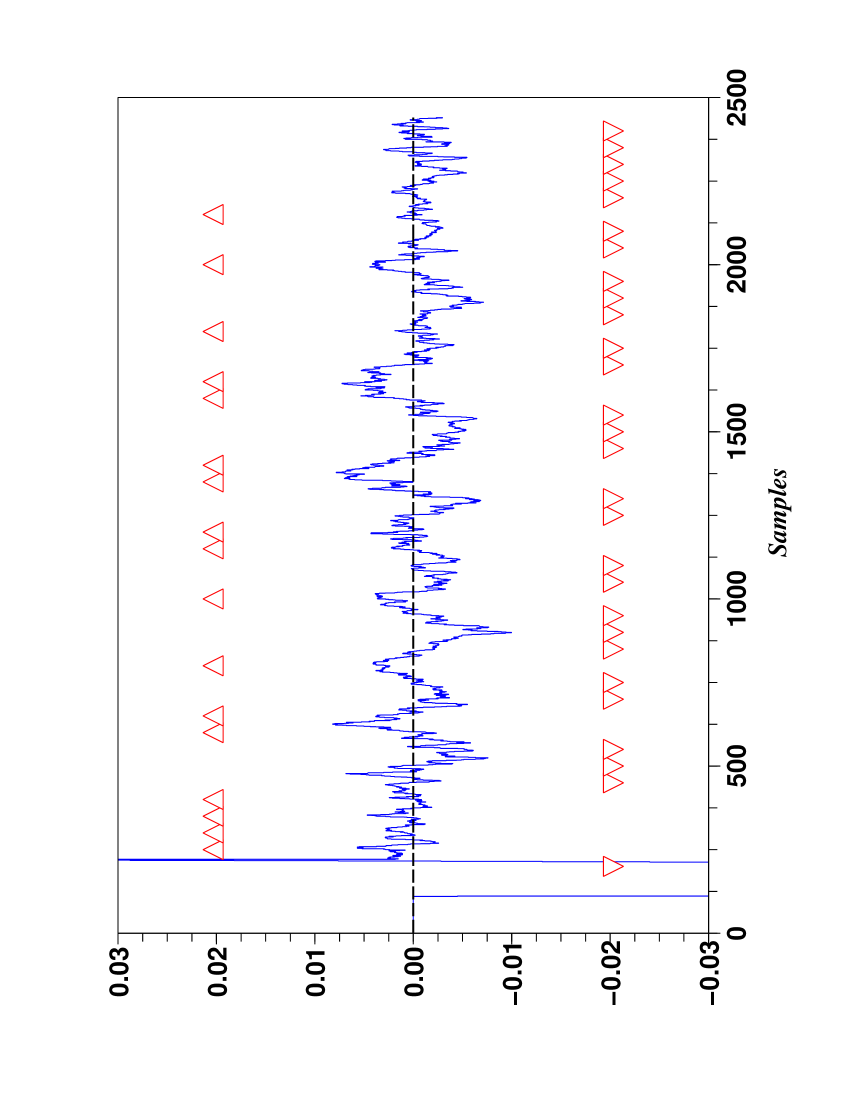

3.3 Predicted volatility w.r.t. the trendline

Introduce the moving standard deviation

and forecast it as in Sect. 3.2. The results, which are displayed for a window size in Table 2 and Fig. 5 via the familiar confidence intervals,999There is of course no need for the underlying statistics to be Gaussian. Lack of space prevents us from exhibiting forecasts of quantities like skewness and kurtosis, which would be obtained by similar calculations. This will be done in some future publications. confirm the time-dependence of the variance, i.e., the heteroscedasticity.

| Confidence intervals | Prediction | Real |

|---|---|---|

| mean-std,mean+std | ||

| mean-std,mean+std | ||

| mean-std,mean+std |

3.4 Forcasting 10 days ahead

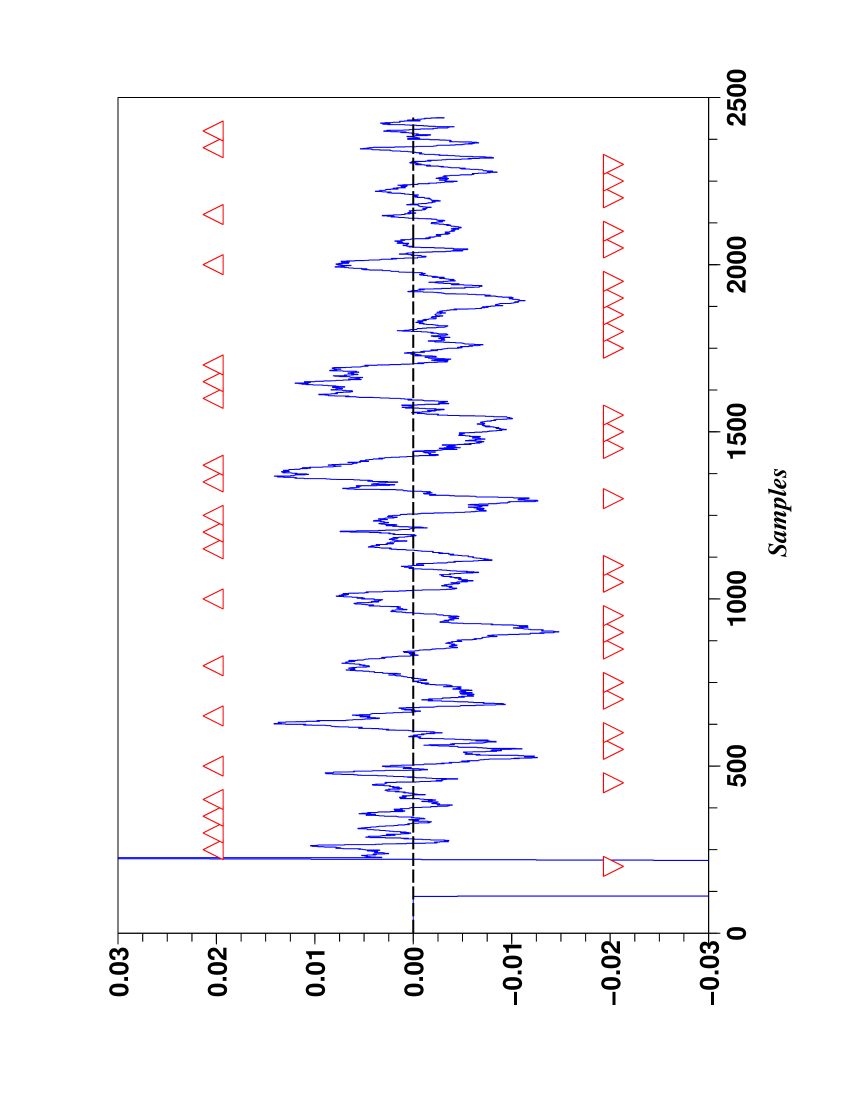

Figures 6, 7, 8, 9 display the same type of results as in Sections 3.1, 3.2, 3.3 via similar computations for a forecasting days ahead. The quality of the computer simulations only slightly deteriorates.

4 Conclusion

The existence of trends, which is

- •

-

•

quite foreign, to the best of our knowledge, to the academic mathematical finance, where the paradigm of random walks is prevalent (see, e.g., Wilmott (2006)),

is fundamental in our approach. A theoretical justification will appear soon Fliess & Join (2009).111111The existence of trends does not necessarily contradict a random character (see Fliess & Join (2009) for details). We hope it will lead to a sound foundation of technical analysis,121212See also Dacorogna, Gençay, Müller, Olsen & Pictet (2001) for a most exciting study which employs high frequency data. There are also other types of attempts to put technical analysis on a firm basis (see, e.g., Lo, Mamaysky & Wang (2000)). See Blanchet-Scalliet, Diop, Gibson, Talay & Tanré (2007) for a comparison between technical analysis and model-based approaches with parametric uncertainties. which will bring as a byproduct easily implementable real-time computer programs.131313Our technics already lead to such computer programs in automatic control and in signal processing.

Acknowledgement. The authors wish to thank G. Daval-Leclercq (Société Générale - Corporate & Investment Banking) for helpful discussions and comments.

References

- (1)

- Aronson (2007) Aronson D. (2007). Evidence-Based Technical Analysis. Wiley.

- Béchu, Bertrand & Nebenzahl (2008) Béchu T., Bertrand E., Nebenzahl J. (2008). L’analyse technique (6e éd.). Economica.

- Blanchet-Scalliet, Diop, Gibson, Talay & Tanré (2007) Blanchet-Scalliet C., Diop A., Gibson R., Talay D., Tanré E. (2007). Technical analysis compared to mathematical models based methods under parameters mis-specification. J. Banking Finance, 31, 1351–1373.

- Bouchaud & Potters (1997) Bouchaud J.-P., Potters M. (1997). Théorie des risques financiers. Eyrolles. English translation (2000): Theory of Financial Risks. Cambridge University Press.

- Box, Jenkins & Reinsel (1994) Box G.E.P., Jenkins G.M., Reinsel, G. (1994). Time Series Analysis: Forecasting and Control (3rd ed.). Prentice Hall.

- Chambert-Loir (2005) Chambert-Loir A. (2005). Algèbre corporelle. Édit. École Polytechnique. English translation (2005): A Field Guide to Algebra. Springer.

- Dacorogna, Gençay, Müller, Olsen & Pictet (2001) Dacorogna M.M., Gençay R., Müller U., Olsen R.B., Pictet O.V. (2001). An Introduction to High Frequency Finance. Academic Press.

- Doetsch (1967) Doetsch G. (1967). Funktionaltransformationen. In R. Sauer, L. Szabó (Eds): Mathematische Hilfsmittel des Ingenieurs, 1. Teil, pp. 232–484. Springer.

- Durlauf & Philips (1988) Durlauf S.N., Philips P.C.B. (1988). Trends versus random walks in time series analysis. Econometrica, 56, 1333–1354.

- Fliess (2008) Fliess M. (2008). Critique du rapport signal à bruit en communications numériques. ARIMA, to appear. Online http://hal.inria.fr/inria-00311719/en/.

- Fliess, Fuchshumer, Schöberl, Schlacher & Sira-Ramírez (2008) Fliess M., Fuchshumer S., Schöberl M., Schlacher K., Sira-Ramírez H. (2008). An introduction to algebraic discrete-time linear parametric identification with a concrete application. J. europ. syst. automat., 42, 211–232.

- Fliess & Join (2008) Fliess M., Join C. (2008). Commande sans modèle et commande à modèle restreint, e-STA, 5. Online http://hal.inria.fr/inria-00288107/en/.

- Fliess & Join (2009) Fliess M., Join C. (2009). A mathematical proof of the existence of trends in financial time series. Int. Conf. Systems Theory: Modelling, Analysis and Control. Fes, Marocco. Soon online http://hal.inria.fr/INRIA.

- Fliess, Join & Sira-Ramírez (2004) Fliess M., Join C., Sira-Ramírez H. (2004). Robust residual generation for linear fault diagnosis: an algebraic setting with examples. Int. J. Control, 77, 1223–1242.

- Fliess, Join & Sira-Ramírez (2008) Fliess M., Join C., Sira-Ramírez H. (2008). Non-linear estimation is easy. Int. J. Modelling Identification Control, 4, 12–27.

- Fliess & Sira-Ramírez (2003) Fliess M., Sira-Ramírez H. (2003). An algebraic framework for linear identification. ESAIM Control Optimiz. Calculus Variat., 9, 151–168.

- Fliess & Sira-Ramírez (2004) Fliess, M., Sira-Ramírez, H. (2004). Reconstructeurs d’état. C.R. Acad. Sci. Paris Ser. I, 338, 91–96.

- Fliess & Sira-Ramírez (2008) Fliess M., Sira-Ramírez H. (2008). Closed-loop parametric identification for continuous-time linear systems via new algebraic techniques. In H. Garnier, L. Wang (Eds): Identification of Continuous-time Models from Sampled Data, pp. 363–391, Springer.

- Gençay, Selçuk & Hafner (2002) Gençay R., Selçuk F., Whitcher B. (2002). An Introduction to Wavelets and Other Filtering Methods in Finance and Economics. Academic Press.

- Gouriéroux & Monfort (1995) Gouriéroux C., Monfort A. (1995). Séries temporelles et modèles dynamiques (2e éd.). Economica. English translation (1996): Time Series and Dynamic Models. Cambridge University Press.

- Hamilton (1994) Hamilton J.D. (1994). Time Series Analysis. Princeton University Press.

- Kaufman (2005) Kaufman P.J. (2005). New Trading Systems and Methods (4th ed.). Wiley.

- Jury (1964) Jury E.I. (1964). Theory and Application of the -Transform Method. Wiley.

- Kirkpatrick & Dahlquist (2006) Kirkpatrick C.D., Dahlquist J.R. (2006). Technical Analysis: The Complete Resource for Financial Market Technicians. FT Press.

- Lang (2002) Lang S. (2002). Algebra (3rd rev. ed.). Springer.

- Lo, Mamaysky & Wang (2000) Lo A.W., Mamaysky H., Wang J. (2000). Foundations of technical analysis: computational algorithms, statistical inference, and empirical implementation. J. Finance, 55, 1705-1765.

- Mandelbrot & Hudson (2004) Mandelbrot B.B., Hudson R.L. (2004). The (Mis) Behavior of Markets. Basic Books.

- Markovsky, Willems, van Huffel, de Moor & Pintelon (2005) Markovsky I., Willems J.C., van Huffel S., de Moor B., Pintelon R. (2005). Application of structured total least squares for system identification and model reduction. IEEE Trans. Automat. Control, 50, 1490-1500.

- Mboup, Join & Fliess (2008) Mboup M., Join C., Fliess M. (2008). A delay estimation approach to change-point detection. Proc. 16th Medit. Conf. Control Automation, Ajaccio. Online http://hal.inria.fr/inria-00179775/en/.

- Mboup, Join & Fliess (2009) Mboup M., Join C., Fliess M. (2009). Numerical differentiation with annihilators in noisy environment. Numer. Algor., DOI: 10.1007/s11075-008-9236-1.

- Murphy (1999) Murphy J.J. (1999). Technical Analysis of the Financial Markets (3rd rev. ed.). New York Institute of Finance.

- Paulos (2003) Paulos J.A. (2003). A Mathematician Plays the Stock Market. Basic Books.

- Sornette (2003) Sornette D. (2003). Why Stock Markets Crash: Critical Events in Complex Financial Systems. Princeton University Press.

- Taleb (1997) Taleb N. (1997). Dynamic Hedging. Wiley.

- Wilmott (2006) Wilmott P. (2006). Paul Wilmott on Quantitative Finance (2nd ed., 3 volumes). Wiley.