Fractality feature in oil price fluctuations

Abstract

The scaling properties of oil price fluctuations are described as a non-stationary stochastic process realized by a time series of finite length. An original model is used to extract the scaling exponent of the fluctuation functions within a non-stationary process formulation. It is shown that, when returns are measured over intervals less than 10 days, the Probability Density Functions (PDFs) exhibit self-similarity and monoscaling, in contrast to the multifractal behavior of the PDFs at macro-scales (typically larger than one month). We find that the time evolution of the distributions are well fitted by a Lévy distribution law at micro-scales. The relevance of a Lévy distribution is made plausible by a simple model of nonlinear transfer.

pacs:

02.50.-r,02.50.Ey,64.60.alI introduction

Many natural or man-made phenomena, such as turbulence flows, fluctuations in finance (stock market), seismic recording, internet traffic, climate change, etc., are characterized by randomness or stochasticity Fris ; bisk ; Kolm1 ; noroz ; mant ; mant1 ; bouch ; abra ; farah ; ken ; keil ; vere ; voig ; bufe ; saic ; kosc ; barb ; frae . Analysis of non-stationary stochastic processes referring to quantities which fluctuate widely and are uncertain has been a problem of fundamental interest for a long time. Over the past two decades, oil price has increased very sharply, rising from $25 per barrel in January 1986 to a peak of close to $ 122 per barrel in the last week of July 2008. The effects of oil price fluctuations on the world economy are undeniable and particularly evident from the international reports. Oil price data as a time series exhibit complex patterns and seemingly appear to be a chaotic system. Indeed, the behavior of oil price fluctuations can be efficiently modelled by the Ising model which was proposed for stock-price fluctuations pler and by the the cascade model developed based on fractal concepts which was used for hydrodynamics and magnetohydrodynamic turbulence ghas ; muzy ; mom . Here, we employ the latter technique to characterize the statistical properties of the oil-price time series, which sensitively distinguish between self-similarity and multi-fractality in a time series. The model is based on two-point increments of oil price, yielding a comprehensive and scale-dependent characterization of the statistical properties of the system via an associated Probability Density Function(PDF). It is necessary to stress that the data series is represented by a finite number of records which do not constitute a stationary process. The effect of non-stationarity on the detrended fluctuation analysis has been investigated in Ref. hu . To eliminate the effect of sinusoidal trend, we apply the Fourier Detrended Fluctuation Analysis (F-DFA). After the elimination of the trend we use the Multifractal Detrended Fluctuation Analysis (MF-DFA) to analysis the data set. The MF-DFA methods are the modified version of detrended fluctuation analysis (DFA) to detect multifractal properties of time series. The detrended fluctuation analysis (DFA) method introduced by Peng et al. peng has became a widely-used technique for the determination of (multi)fractal scaling properties and the detection of long-range correlations in noisy, non-stationary time series hu ; peng . It has successfully been applied to diverse fields such as DNA sequences buld ; buld1 , heart rate dynamics ken ; ken1 , neuron spiking bles , human gait haus , long-time weather records kosc ; ivan , cloud structure ivan1 , geology mala , ethnology alad , economical time series mant ; liu , solid state physics kant , sunspot time series sadegh , and cosmic microwave background radiation keil ; vere .

We propose a method for generating a stationary process analysis out of a non-stationary process. The fact is that stationary stochastic systems often show scaling in a statistical sense, coincident with non-Gaussian leptokurtic (heavy- tailed) statistics. Importantly, identification of the associated scaling exponents implies the ability to interpret and estimate the behavior of the fluctuations as well as the detection of long-range correlations. A self-similar Brownian walk with Gaussian PDFs, which has scaling exponent , is a good example of the process where shows uncorrelation on all temporal scales. We try to determine the scaling properties of the PDFs that are leptokurtic at micro-scales. The scaling exponents can be determined through the scaling behavior of the moments, usually characterized by computing structure functions. It is said that the fluctuations are self-similar (monofractal) if scaling exponents of the moments exhibit a linear power-law dependence. In contrast a nonlinear dependence infers to multifractal scaling, which is caused by intermittent small-scale structures of oil price fluctuations. A similar feature has been found in physical systems for example, in velocity and magnetic fields of the solar wind kian ; kian1 ; gold as well as in magnetohydrodynamic turbulence studied via direct numerical simulations mom . Finally, distributed price changes are characterized by a stable Lévy distribution in the central part of the distribution.

The paper is structured as follows. In Section II we describe our data set. The MF-DFA method is briefly presented in Section III and shown that the scaling exponent determined via the MF-DFA method are identical to those obtained by the standard multifractal formalism based on PDF analysis. In Section IV we employ a recently developed technique kian ; kian1 ; mom that sensitively distinguishes between self-similarity and multifractality in times series. By analyzing the temporal evolution of price dynamics, we demonstrate the strongly the non-Gaussian behavior of the returns of oil price and scale-dependent behavior of the PDFs. Also we explain the Hurst exponents analysis. The micro-scale PDFs resemble leptokurtic Lévy distribution which will be discussed in Section V. Finally, in Section VI we will summarize all results discussed throughout this paper.

II The data

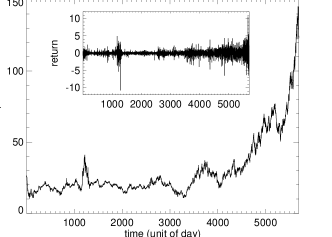

Over a twelve-year period, on average, the price of oil has increased from $25 per barrel in January 1986 to a peak of close to $ 122 per barrel in the last week of July 2008 . Oil price as recorded in international markets sit offer us an almost unique possibility to gain information on the stochastic dynamics state in a very large scale range, say 1 day up to 200 days. Our database consists of about 5695 daily price values which seem to provide a set of data points which will be sufficient to obtain the scaling properties the system. Fig.1 presents the daily fluctuations in oil price in the period 1986-2008. It is evident from the figure that the fluctuations do not constitute a stationary process, for instance one can show that the variance of the signal in some window does not remain stable upon increasing the window size. Let us introduce the increments (or returns) defined by, . The resulting series for is shown in the inset graph of Fig.1.

It is straightforward to show, by measuring the average and the variance of in a moving window, that is stationary. Upon initiating the analysis of the distribution of oil price returns, the mean, standard deviation, skewness, and kurtosis of the return series are calculated (see Table 1). It is easy to show that the skewness of a Gaussian function is zero so that the negative value of skewness, , is a hallmark of departure of the PDFs from the Gaussian distribution (such as a leptokurtic distribution), which confirms the existence of intermittency in the fluctuations. On the other hand the large value of kurtosis, , with respect to Gaussian kurtosis , show that the tails of the return distribution are fatter than the Gaussian ones.

| Mean | Standard Deviation | Skewness | Kurtosis |

| 0.0124274 | 0.729173 | -0.606749 | 9.55225 |

III The MF-DFA analysis

The MF-DFA method is a modified version of detrended fluctuation analysis to detect multifractal properties of a time series. Omitting unnecessary details, a brief summary of the method for calculating MF-DFA based on fractal concepts can be formulated in five steps. We take the price series with the size of and follow the steps as follow:

step 1: Determine the ” profile”

| (1) |

where is the mean of the series. Subtraction of the mean is not compulsory, since it would be eliminated by the detrending later in the third step.

step 2: Divide the profile into nonoverlapping segments of equal lengths . Since the length of the series is often not a multiple of the considered time scale , a short part at the end of the profile may remain. In order not to disregard this part of the series , the same procedure is repeated starting from the opposite end.

step 3: Calculate the local trend for each of the segments by a least-square fit of the series. Then determine the variance

| (2) |

for each segment , and

| (3) |

for . Here we use the linear fitting polynomial in segment .

step 4: Average over all segments to obtain the -th order fluctuation function, defined as:

| (4) |

where, in general, the index variable can take any real value except zero. We repeat steps 2, 3 and 4 on several timescales . It is apparent that will increase with increasing .

step 5: Determine the scaling behavior of the fluctuation functions by analyzing log-log plots of versus .

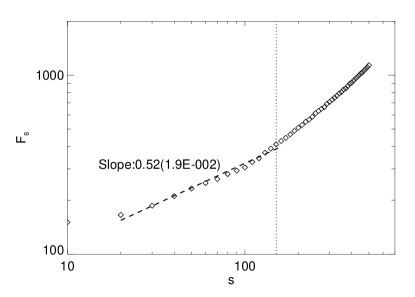

A power law relation between and indicates the presence of scaling: . In general, the exponent may depend on . For stationary time series such as fGn (fractional Gaussian noise), in Eq. (1), will be a fBm (fractional Brownian motion) signal, so, sadegh1 . As a result, the fluctuation function shows a scaling behavior, , which is identical to the well-known Hurst exponent . The Hurst exponent is called the scaling exponent or correlation exponent, and represents the correlation properties of the signal. If , there is no correlation and the signal is an uncorrelated signal, if , the signal is anticorrelated, if , there is positive correlation in the signal. We obtain the following estimate for the Hurst exponent, as we can see in Fig. (2). Since it is concluded that oil price returns show persistence, i.e, a certain correlation among consecutive increments. For the empirical data deviate from the initial scaling behavior, as we can see in Fig. (2). This indicates that oil price tends to loose its memory after a period of the order of 200 days or less.

IV Statistical self-similarity

A set of time series is obtained for each value of nonoverlapping time lag . The return of the stochastic variable is said to be self-similar with parameter , if for any

| (5) |

The relation (5) is interpreted as an equality in law (EL), that is the two sides of the equation have the same statistical properties. For the associated cumulative probability distribution, it follows that

| (6) |

for any real . This implies for the probability density

| (7) |

introducing the master PDF with . According to Eq. (7), there is a family of PDFs that can be collapsed to a single curve , if is independent of . This is known as monoscaling in contrast to multifractal scaling observed, e.g., for oil price returns at macro-scales.

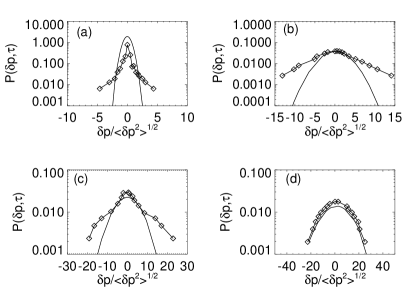

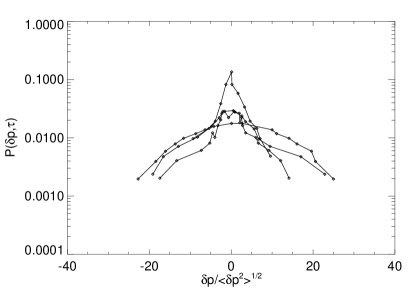

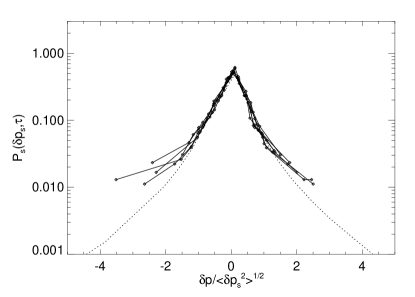

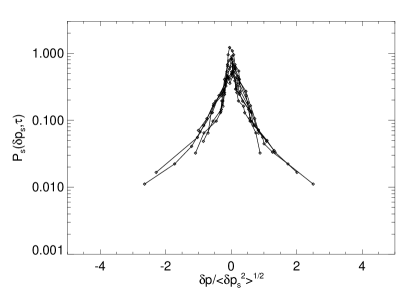

To characterize quantitatively the observed stochastic process, we measure the PDF of the price fluctuations for ranging from 1 to 200 days. The number of data in each set decreases from the maximum value of 5695 to the minimum value of 5495 . In Fig.(3) we show the four selected PDFs (normalized with the variance ) for , , , and from the top ( left side) to the bottom (right side) respectively. The distributions lose their leptokurtic shape, as increases. Due to the lack in correlation among distant fluctuations, the associated distributions become approximately Gaussian at macro-scale. The scaling behavior of the distribution at coarser time scales has two different regimes. At micro-scales (typically shorter than 10 days), correlations between successive price changes are dominant. This may be due to several reasons, such as oil pipe line damage, weather changes, or local variations in the internal (US) oil availability. Interestingly, the PDFs at the micro-scales have the same leptokurtic shape, exhibit monoscaling, and do not change fundamentally, and resemble closely Lévy distributions, see Fig. (4). On the other hand, at macro-scale (typically larger than one month) permanent crisis in the Middle East and north African govern the price drift and corresponding to a Gaussian regime. This is coincide with a multifractal feature, as we can see in Fig. (5). However the micro-and macro time scales regimes can be led to a linear and nonlinear scaling-dependence respectively.

First, let us consider the scaling as defined by the structure functions. The generalized structure function of order are simply defined as

| (8) |

The analysis which follows is also valid for the moments; however, structure functions are typically calculated for a data series. The arguments do not apply to structure functions of odd order, which not only may have negative coefficients, but could in fact even change the sign of the scaling range. The proof will, however, remain valid for odd orders if the structure functions are defined with the absolute value of the returns. Using the relation (7) we obtain

| (9) |

where the linear function refer to the statistical self-similarity, monoscaling case. On the contrary, in some cases, one may observe multifractality scaling, in the sense that a nonlinear dependence is observed on where is a convex function of and . This deviation from strict self-similarity over all time scale , also termed multifractal scaling, is caused by the intermittent micro-scale structure of turbulence.

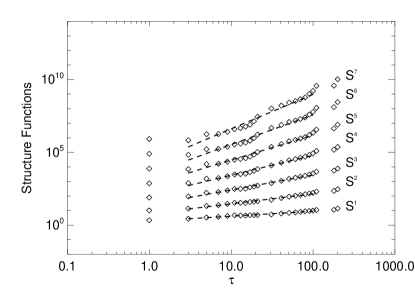

To test if the above-mentioned interesting observations in oil

price are a phenomenon related to inherent properties of stochastic

processes, structure functions for different , given by

Eq. (8), are computed. A difficulty that can arise in the

experimental determination of the is that for a finite

length times series, the integral Eq. (8) is not sampled

over the range , rather the outlying measured values of

determine the limit, . Fig. (6) shows some

selected , according to Eq. (8). The slope of

the curve gives scaling exponent which can be obtained by

fitting a straight line to a log-log plot in the interval . Because of increasing of the statistical errors at the

higher orders, such a fitting becomes rather arbitrary. In Fig.

(7) we report the scaling exponents extracted from the

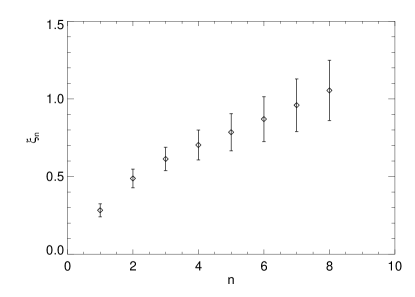

structure functions. The behavior of against shows

that scaling exponents have nonlinear behavior at all scales , say,

they are different from the usual linear law.

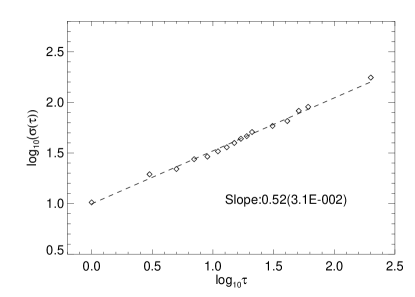

To apply the rescaling procedure given by Eq. (7) the exponent is extracted from the underlying data by a independent technique, kian ; mom . The standard deviation which is defined by the root of the second-order structure function, and has the minimum of statistical error, exhibits power-law behavior with respect to the increment distance, as depicted in Fig. (8).

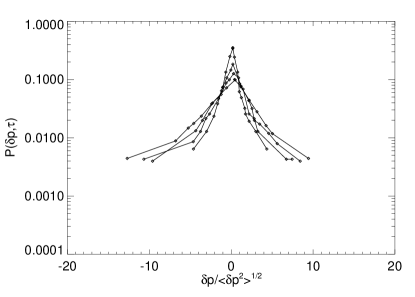

A linear least-square fit is carried out to obtain . The characteristic exponent deduced in this way is which is in good agreement with the value of obtained in Section. (III). Fig. (9) and Fig. (10) show the rescaled sets of PDFs on the micro- and macro-scales respectively. Evidently the PDFs at micro-scales are self-similar and collapse with weak scattering on the master PDF, , when using the characteristic exponents given above. The corresponding increment distances are all shorter than 10 days. We may model this PDFs by a Lévy distribution, which thus turns out to be a successful fit to the distribution of oil price fluctuations. On the other hand, at macro-scale the PDFs do not show a self-similar behavior and rather constitute a multicascade process. This occurs at scales larger than the one month. Because of the resulting multifractal scaling of the PDFs it is evident that they can not collapse onto a single curve, see Fig. (10).

V Lévy distribution model

Lévy-stable laws are a rich class of probability distributions that comprise fat tails and have many intriguing mathematical properties. They have been proposed as models for many types of physical and economic systems. There are several reasons for using Lévy-stable laws to describe complex systems. First of all, in some cases there are solid theoretical reasons for expecting a non-Gaussian Lévy stable model, which can be a good fitting to experimental and numerical results. The second reason is the Generalized Central Limit Theorem which states that the only possible non-trivial limit of normalized sums of independent identically distributed terms is Lévy-stable. (Recall that the classical Central Limit Theorem states that the limit of normalized sums of independent identically distributed terms with finite variance is Gaussian.) The third argument for modeling with Lévy-stable distributions is empirical; many large data sets exhibit fat tails (or heavy tails); for a review see jani ; silv . Such data sets were described by a Casting model based on the log normal ansatz (in terms of the variance of the Gaussian distribution). To confirm that model it is convenient to summarize the basic features of the Lévy stable distribution.

A Lévy process is a time-dependent or position-dependent process that at an infinitesimal interval has the Lévy distribution of the process variable. The characteristic function of the Lévy process is

| (10) |

where can be a characteristic time or space scale. If the Lévy collapses to the Gaussian distribution. If the Lévy becomes a Cauchy distribution. The original Lévy process is given by its inverse Fourier transform, i.e.

| (11) |

and the symmetric Lévy distribution becomes

| (12) |

where the increment is ; here, , and is a scale factor. The maximum event probability leads to

| (13) |

The exponent of the best fits is constant at the micro-scales range and amounts approximately to which is . Natural phenomena also investigated where similar findings have been reported include, for example, financial systems e.g. the Tehran price stock market, where noroz , and also physical systems such as the solar wind, where hnat . From Fig. (9) we conclude that a central section of Lévy distributions describe very well the dynamics of the PDFs of oil price fluctuations at micro-scales. One can see that the rescaled PDFs are definitely non-Gaussian.

VI Summary

In this paper, we have presented a statistical analysis of oil price in the United States for the period of 1986 to 2008. We have applied a generic MF-DFA method to extract scaling exponent of the fluctuation functions, in particular, relying on the second order which was used in the rescaling procedure. However, the simple scaling properties that we have found via an analysis of the PDFs, allow us to detect mono(multi) fractality feature over all time scales. The presence of intermittency in oil price fluctuations is manifested by the leptokurtic nature of the PDFs which show increased probability of large fluctuations compared to that of the Gaussian distribution. Fluctuations on the macro temporal scales, day, converge toward a Gaussian distribution and are an uncorrelated signal. The reason may be due to unstable conditions in the Middle East or OPEC’s decisions oil production. The critical macro scale which was obtained is different for some financial and physical systems; see for example in Refs. noroz ; ken . We have also obtained a good collapse onto a single curve for , according to the rescaling procedure (7). The proximity of the PDFs to Lévy distributions is made plausible by a simple model mimicking nonlinear spectral transfer.

References

- (1) U. Frisch, Turbulence, (Cambridge University Press, Cambridge,1995).

- (2) D. Biskamp, Magnetohydrodynamic Turbulence, (Cambridge University Press, Cambridge, 2003).

- (3) A. N. Kolmogrov , J. Fluid. Mech . 13, 82 (1962).

- (4) P. Norouzzadeh and G.R. Jafari, Physica A 356, 609 (2005).

- (5) R.Mantegna and H.E. Stanley, An Introduction to Econophysics, (Cambridge University Press, Cambridge, 2000).

- (6) R.Mantegna and H.E. Stanley, Nuture, 376, 46 (1995).

- (7) J.-P. Bouchaud and M. Potters, Theory of Financial Risks, (Cambridge University Press, Cambridge, 2000).

- (8) Abraham C.-L. Chian, Erico L. Rempel, and Colin Rogers, Chaos, Solitons and Fractals 29, 1194 (2006).

- (9) F. Farahpour, Z. Eskandari, A. Bahraminasab, G.R. Jafari, F. Ghasemi, Muhammad Sahimi, and M. Reza Rahimi Tabar, Physica A 385, 601 (2007).

- (10) Ken Kiyono, Zbigniew R. Struzik, and Yoshiharu Yamamoto, Phys.Rev.Lett 96, 068701 (2006).

- (11) V.I. Keilis-Borok and A.A. Soloviev, Nonlinear Dynamics of the Lithosphere and Earthquake Prediction, (Springer, New York, 2003).

- (12) D. Vere-Jones, Math. Geol 9, 407 (1977).

- (13) B. Voight, Nature 332, 125 (1988); Science 243, 200 (1989)

- (14) C.G. Bufe and D.J. Varnes, J. Geophys. Res. 98, 9871 (1993).

- (15) A. Saichev and D. Sornette, Tectonophysics 431, 7 (2007).

- (16) E. Koscielny-Bunde, A. Bunde, S. Havlin, H.E. Roman, Y. Goldreich, and H.-J. Schellnhuber, Phys. Rev. Lett. 81 729 (1998).

- (17) S.M. Barbosa, M.J. Fernandes, and M.E. Silva, Physica A 371, 725 (2006)

- (18) K. Fraedrich, U. Luksch, and R. Blender, Phys. Rev. E 70,037301 (2004).

- (19) V. Plerou, P. Gopikrishnan, X. Gabaix, and H. E. Stanley, Phys. Rev. E 66, 027104 (2002).

- (20) S. Ghashghaie, W. Breymann, J. Peinke, P. Talkner, and Y. Dodge, Nature (London) 381, 767 (1996).

- (21) J. F. Muzy, J. Delour, and E. Bacry, Eur. Phys. J. B 17, 537 (2000).

- (22) M. Momeni and W.-C. Müller, Phys. Rev. E 77, 056401 (2008).

- (23) K. Hu, P.Ch. Ivanov, Z. Chen, P. Carpena, and H.E. Stanley, Phys. Rev. E. 64, 011114 (2001).

- (24) C.K. Peng, S.V. Buldyrev, S. Havlin, M. Simons, H.E. Stanley, and A.L. Goldberger, Phys. Rev. E 49, 1685 (1994); S.M. Ossadnik, S.B. Buldyrev, A.L. Goldberger, S. Havlin, R.N. Mantegna, C.K. Peng, M. Simons, and H.E. Stanley, Biophys. J. 67, 64 (1994).

- (25) S.V. Buldyrev, A.L Goldberger, S. Havlin, R.N. Mantegna, M.E. Matsa, C.K. Peng, M. Simons, and H.E. Stanley, Phys. Rev. E 51,5084 (1995)

- (26) S.V. Buldyrev, N.V. Dokholyan, A.L. Goldberger, S. Havlin, C.K. Peng, H.E. Stanley, and G.M. Viswanathan, Physica A 249,430 (1998).

- (27) Ken Kiyono, Zbigniew R. Struzik, Naoko Aoyagi, Seiichiro Sakata, Junichiro Hayano, and Yoshiharu Yamamoto, Phys.Rev.Lett. 93,178103 (2004).

- (28) S. Blesic, S. Milosevic, D. Stratimirovic, and M. Ljubisavljevic, Physica A 268, 275 (1999).; S. Bahar, J.W. Kantelhardt, A. Neiman, H.A. Rego, D.F. Russell, L. Wilkens, A. Bunde,and F. Moss, Europhys. Lett. 56,454 (2001).

- (29) J.M. Hausdorff, S.L. Mitchell, R. Firtion, C.K. Peng, M.E. Cudkowicz, J.Y. Wei, and A.L. Goldberger, J. Appl. Physiology 82,262 (1997).

- (30) K. Ivanova and M. Ausloos, Physica A 274,349 (1999) ; P. Talkner and R.O. Weber, Phys. Rev. E 62,150 (2000).

- (31) K. Ivanova, M. Ausloos, E. Clothiaux, T.P. Ackerman, Europhys. Lett. 52, 40 (2000).

- (32) B.D Malamud, D.L. Turcotte, J. Stat. Plan. Infer. 80,173 (1999).

- (33) C.L. Alados, M.A. Huffman, Ethnology 106,105 (2000).

- (34) Y. Liu, P. Gopikrishnan, P. Cizeau, M. Meyer, C.K. Peng, and H.E. Stanley, Phys. Rev. E 60, 1390 (1999); N. Vandewalle, M. Ausloos, and P. Boveroux, Physica A 269,170 (1999).

- (35) J.W. Kantelhardt, R. Berkovits, S. Havlin, and A. Bunde, Physica A 266, 461 (1999); N. Vandewalle, M. Ausloos, M. Houssa, P.W. Mertens, and M. Heyns, Appl. Phys. Lett. 74,1579 (1999).

- (36) M. Sadegh Movahed, G.R. Jafari, F. Ghasemi, S. Rahvar, and M. Rahimi Tabar, J. Stat. Mech. P02003(2006).

- (37) K. Kiyani, S. C. Chapman and B. Hnat, Phys. Rev. E 74, 051122 (2006).

- (38) K. Kiyani, S. C. Chapman, B. Hnat and R. M. Nicol, Phys. Rev. Lett 98, 211101 (2007)

- (39) Nigel Goldenfeld, Phys. Rev. Lett. 96, 044503 (2006).

- (40) Data obtained from USA Energy Information Administration: http://tonto.eia.doe.gov/dnav/pet .

- (41) M. Sadegh Movahed, Evalds Hermanis, Physica A , doi:10.1016/j.physa.2007.10.007 (2007).

- (42) A. Janicki, and A. Weron , Simulation and Chaotic Behavior of a-Stable Stochastic Processes, (Marcel Dekker, New York, 1994).

- (43) S. D. Silva, R. Matsusita, I. Gleria, A. Figueiredo, and P. Rathie , Communications in Nonlinear Science and Numerical Simulation 10, 365 (2005).

- (44) B. Hnat, S. C. Chapman, G. Rowlands, N. W. Watkins, and W.M. Farrell, Geophys. Res. Lett. 29, 86 (2002).