The price of bond and European option on bond without credit risk.

Classical look and its quantum extension.

Abstract

In this paper we compare two classical one-factor diffusion models which are used to model the term structure of interest rates. One of them is based on the Wiener-Bachelier process while the second one is based on the Ornstein-Uhlenbeck process. We show essential differences between the prices of European call options on a zero-coupon bond in these models.

PACS numbers: 02.50.-r, 03.67.-a

Keywords: Stochastic processes, Merton model, Vasicek model, Wieiener-Bachelier process, Ornstein-Uhlenbeck process

Introduction

The bond market forms a very important segment of financial markets. However, modelling of it is difficult because the bond prices depend on both the present situation of the market and the time to maturity. The prices of bonds are expressed in terms of various interest rates and yields, so understanding bonds pricing is equivalent to understanding interest rate behaviour. The term structure of interest rates is defined as the dependence between interest rates and maturities. We propose two models:

1) the Merton model based on the Wiener-Bachelier process,

2) the Vasicek model based on the quantum Ornstein-Uhlenbeck process.*1)*1)*1)In the quantum

game theory Ornstein-Uhlenbeck process has the interpretation of non-unitary tactics resulting in a new strategy. These strategies are the Hilbert’s spaces vectors. Quantum strategies create unique opportunities for making profits during intervals shorter than the

characteristic thresholds for the Brown particle, see [1, 2].

In the above models we find the formula for the zero-coupon bond price and we price

the option on this bond. In the first section we propose general zero-coupon bond pricing model

and we give some information about forward contracts with the help of which we price options on zero-coupon bonds. Then, we discuss the Merton model while in the third one we discuss the Vasicek model. Finally, we compare both models.

We assume that the market is effective without an opportunity of arbitrage and the face value of any bond equals one. Let be the price of the zero-coupon bond at some date with the time to maturity . Let denotes the discount rate called zero-coupon rate or spot rate for date in continuous capitalisation [3]. Then is related to the continuously compounded zero-coupon rate by

| (1) |

hence

| (2) |

We call the function the discount function and

the transformation the yield curve.

The short-term interest rate is given by the formula

We introduce few notions which are connected with the derivatives. First, we consider options on the zero-coupon bonds. Let us consider European options. We must clearly distinguish between the call option and the put option. The time of maturity of the option is denoted by . Let denotes the time price of an European call option on the zero-coupon bond, which gives a payment of at time , where , with the exercise price of . Similarly, let denotes the price of the corresponding put option. The prices of these options at maturity are equal to and *2)*2)*2) always denotes the price of the zero-coupon bond at the time with the time to maturity .. The prices of European call and put option on the zero-coupon bonds fulfil the put-call parity relation [4]

| (3) |

As the result, we can restrict ourself to pricing of European call options.

Another derivatives are forward contracts on the zero-coupon bonds. If the underlying variable is the price of the zero-coupon bond, the essential part by the pricing of the forward contracts plays the present prices of the zero-coupon bonds only. If there is no arbitrage, the time value of the forward contract on the zero-coupon bond, with the delivery date and the delivery price , is given by the formula [4]

| (4) |

is the maturity date of the underlying bond. For forwards contracted upon at time , the delivery price is set so that the value of the forward at time is zero (). This value of is called the forward price . Solving (4) we obtain that

| (5) |

1 The pricing in affine models

We assume that for considered market model, there is a risk-neutral probability measure (or equivalent martingale measure) and a one-dimensional Wiener process under measure . If the risk-neutral probability measure exists, then there is also the -forward martingale measure and then is the Wiener process under measure . If there exists a spot martingale measure, then the market is arbitrage free. Part of the market characteristic fulfils the short rate under the risk-neutral probability measure (i.e. the spot martingale measure). The model in which this rate is represented by the process , that fulfils the stochastic equation

| (6) |

where and , we call the affine model. Let us consider that and , where are constant. We know that the discount price of the zero-coupon bond is given by the formula [5]

| (7) |

With the help of this assumption, we can calculate the formula for the discount price of the zero-coupon bond, see [6]. This price can be written as a function of time and the current short rate .

Theorem 1.1.

In an affine model, in which the short rate is described by (6),

the time price of the zero-coupon with the time to maturity and face value is equal to

| (8) |

The functions fulfil the following system of ordinary differential equations:

for and .

Proof.

The proof is based on the Feynman-Kac theorem, see (5.8) in Appendix. From theorem (5.8) follows that , given by the formula (8), fulfils the partial differential equation

The relevant derivatives are

After substituting these formulas into (5.8), we obtain

After gathering terms involving , we obtain

The last equation must be fulfilled for arbitrary , so the expressions in the brackets must be identically . Hence, we find equations which the function and must fulfil. Because , so and hence . We see that the function (8) fulfils the Feynman-Kac equation.

Let us observe that, if we have the function from the above formula, we can calculate the function from the formula*3)*3)*3)If , so . Let us take into consideration that .

| (9) |

If we want to determine the price of the bond, we have to find the solution of the differential equation given by the formula

Now, let us observe that for . Above all, from the continuity of , the conditions and follow that in the vicinity of . From this, grows up in the vicinity of , that is for small . As if for certain , there is a point from the Intermediate Value Theorem [7], such that . From the Rolle theorem [7], we obtain , so there must exist such that . If we substitute to the differential equation fulfilled by , we obtain the equality for . Let us consider constant function . It fulfils the same differential equation, so . Furthermore, , that means that both functions fulfil the same initial-value problem. From the uniqueness of solution we obtain that and , that is, , which is impossible because does not fulfil the quadratic equation which is satisfied by . We obtain contradiction, so for . It means that the function is strictly decreasing.

In the further parts of our paper we will use the formula for the volatility of the process under -forward martingale measure. It looks the same as for measure . From the Feynman-Kac theorem, it is given by the formula

and in our specific situation . Using the formula (8), we obtain

| (10) |

Let denotes the relative drift of the process under measure .

2 The Merton model

The first dynamic, affine and continuous time model of the term structure of the interest rate was described by Merton [8]. The short rate follows a generalised Brownian motion under the spot martingale measure:

where and are constant. We begin by finding the price of the zero-coupon bond and then we calculate the price of the option. We see that the price of the bond in this model is given by the formula (see (8))

where the function fulfils the simple ordinary differential equation with So, and the function is given by the formula (see (9))

therefore

| (11) |

In order to price the option, we use the theorem (5.7), see Appendix. The price of an European call option on the zero-coupon bond with the expiration date , the exercise price , and maturing at the time is given by, see (14) in Appendix,

| (12) |

From (5) we know that the forward price fulfils the formula:

hence, in particular . The forward price is a martingale under the -forward martingale measure, what means that the drift rate equals under this probability measure. Simultaneously, this process is a quotient of the prices of two zero coupon bonds. In the diffusion equations for and , the relative volatilities of the bond are equal to and respectively, so that

By an application of the Itô lemma, see Appendix (5.3), for functions of multiple stochastic processes and because of that, the drift of the process equals under the -forward martingale measure, we obtain

This means that, follows a geometric Brownian motion, see Appendix (5.4), with . Hence, the random variable is normally distributed and

| (13) |

what result from (5.5), see Appendix. Moreover,

Let us consider the function and a random variable . From the formula (12) and with the help of that , we obtain

From the equation (13) we have that is independent of and is -measurable, because the process is a martingale. Hence, we can use the lemma (5.2)*4)*4)*4)Let us observe that , so that is bounded, because ., see Appendix. By the using the lemma (5.6), see Appendix, we can calculate the expected value [ !]

If we substitute to the above equation , we obtain

and finally

where

3 The Vasicek Model

In the paper [9] Vasicek proposed a mean-reverting version of the Ornstein-Uhlenbeck process for the short term rate. Specifically, under the risk-neutral measure , is given by

where and are positive constants. The parameter denotes long-term level of the short rate, because the rate pull towards a long-term level of , determines the speed of adjustment, and is the average deviation of the rate of return.

Similarly to the Merton model, at the first we calculate the formula for the zero-coupon bond price. From the theorem 1.1 we know that

but in the described model we have

Hence,

From (9) we obtain that

If we substitute and to the formula (8), we obtain analogous formula for the bond price to the Merton model, see (11).

We calculate the formula for the call option price similar to the Merton model. Let us use the basic formula

With the help of the Itô lemma (5.3) and because of that the drift of process equals under the -forward martingale measure, we obtain the diffusion equation for the forward price:

Therefore, the process of forward prices is a geometric Brownian motion with . The random variable has the Gaussian distribution. Similarly, we obtain the formulas:

Our further reasoning is the same like in the Merton model. Let the function and the random variable . We obtain the formula

With the help of independence of and -measurability of , we can use the lemma (5.2). Then, if we use the lemma (5.6), we calculate that the expected value equals

If we substitute to the above equation we obtain

and finally

where

4 Final remarks

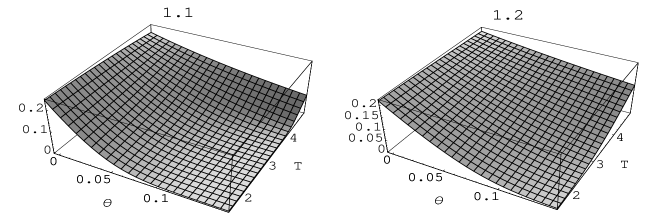

The Fig. 1 shows the prices of European call options on the zero-coupon bonds with the expiration date years, the face value and the real values of the market parameters based on the Merton model and the Vasicek model.

In the above figures, we consider the European call option on the zero-coupon bond with the exercise price , time to maturity years and the face value .

As it follows from the general affine model pricing, see (6), we can compare this two models under the assumption that . The results are qualitatively different. Let us notice that, the price of the option described by Vasicek is higher than the price described by Merton and faster drawn towards to , where is the expected price of the option with fixed expiration date , because the market is effective without an opportunity of arbitrage. Let us observe that, both models give equal prices for the long interest rate .

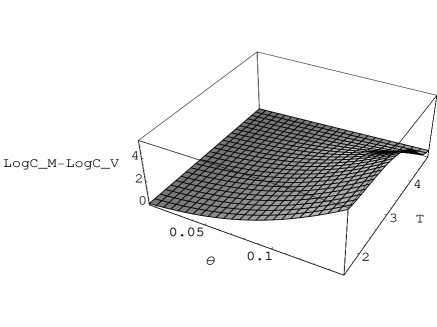

The difference between the logarithmic price of the European call option described by the Ornstein-Uhlenbeck process and the logarithmic price of the call option described by the Wiener-Bachelier process is illustrated in the Fig. 2.

The difference between these logarithmic prices increases with the growth of and fades away in the limit of the expiration date () of the zero-coupon bond. One of the inappropriate properties of the Merton model is the constant drift of the short rate. With the constant positive drift the short rate is expected to increase in the future. But this is not realistic. Many empirical studies show that, the interest rates exhibit mean reversion, in the sense that, if an interest rate is high by historical standards, it typically will be falling in the near future (analogically if the current interest rate is low).

In paper [2] we considered the prices of options on company’s stock supported by Wiener-Bachelier model and Ornstein-Uhlenbeck model and we interpreted the Ornstein-Uhlenbeck process in terms of quantum market games theory as a non-unitary thermal tactic. We compared the probability density functions of both distributions and showed that the Ornstein-Uhlenbeck process would give the true reflection of the market in time scale where the approximation by a Wiener-Bachelier process is not valid, but such that market expectations and the asymptotic equilibrium state have not been changed. We called this time interval mezzo-scale. The differences between a classical look and the pricing which is supported by the quantum model; they are visible for very liquid financial instruments. The quantum game theory takes advantage the Ornstein-Uhlenbeck process for the financial modelling. Quantum strategies create unique opportunities for making profits during intervals shorter than characteristic thresholds for an effective market (Brownian motion). The additional possibilities offered by quantum strategies can lead to more successful outcomes than purely classical ones, see [14].

5 Appendix

In this section we introduce definitions and theorems (without proofs) which are used in our paper. They can be find in [3],[4],[10],[11],[12].

Definition 5.1.

Let be an integrable random variable on a probability space , and let be a -field contained in . Then the conditional expectation value of , for given , is defined to be a random variable such that:

-

•

is -measurable,

-

•

for any

Lemma 5.2.

If is -field and is a Borel and bounded function, is a random variable which is independent of , and is -measurable and , then

Theorem 5.3 (Itô lemma).

-

(i)

Let be a real-valued process with dynamics

where are real-valued processes, and is a one-dimensional standard Brownian motion. Then, for any function which is two times continuously differentiable in and continuously differentiable at , the process defined by is an Itô process with dynamics

-

(ii)

Let be a one-dimensional standard Brownian motion, , and be two-dimensional stochastic processes with dynamics:

Then, for any function which is two times continuously differentiable in and and continuously differentiable at , the process is an Itô process with dynamics

Definition 5.4.

A stochastic process is said to be the geometric Brownian motion if it is a solution of the stochastic differential equation

where are deterministic functions of time. The initial value for process is assumed to be positive, .

The function is the growing rate (drift) and is a volatility rate of the process .

Theorem 5.5.

Let be the geometric Brownian motion with , then for any the following conditions are fulfilled:

-

(i)

,

-

(ii)

a random variable has a normal distribution,

-

(iii)

if is a volatility rate of the process , then

Lemma 5.6.

If and , then for any constant

Theorem 5.7.

Let be the expiration date and the exercise price of the European option, and be the price of the underlying assets at the expiration date, then the price of the option at the time is equal to

| (14) |

The basic tool for pricing the financial models is the Feynman-Kac theorem. We assume that is a diffusion process with dynamics given by the stochastic differential equation

| (15) |

Moreover, we assume that a process () describes the short interest rate and the risk-neutral probability measure exists.

Let us consider a security with a single payment of and the expiration date . Let denotes the price of the security at the moment . It is proved that

| (16) |

Theorem 5.8 (Feynman-Kac theorem).

The function defined by

satisfies the partial differential equation

| (17) |

together with the terminal condition . The process describes the price of the considered security. The process is a diffusion process under and with the drift

| (18) |

and the volatility rate

| (19) |

References

- [1] E. W. Piotrowski and J. Sładkowski, Quantum diffusion of prices and profits, Physica A 345 (2005), 185.

- [2] E. W. Piotrowski, M. Schroeder, A. Zambrzycka, Quantum extension of European option pricing based on the Ornstein-Uhlenbeck process, Physica A 368 (2006), 176–182.

- [3] C. Munk, Fixed Income Analysis: Securities, Pricing and Risk Management, Lecture Notes, University of Southern Denmark, 2005; http://www.sam.sdu.dk/cmu/.

- [4] J. Hull, Options, Futures, and Other Derivative Securities, Prentice-Hall International Inc., Fifth Edition. 2003

- [5] R. J. Elliott, P. E. Kopp, Mathematics of Financial Markets, Springer-Verlag New York Inc., 1999.

- [6] D. Duffine, Dynamic Asset Pricing Theory, Princeton University Press, Third Edition. 2001.

- [7] W. R. Wade, An Introduction to Analysis, Prentice-Hall Inc. NJ., Second Edition. 2000.

- [8] R. C. Merton, Theory of rational option pricing, Bell Journal of Economics and Management Science 4 (1973), 141–183.

- [9] O. Vasicek, An equilibrium characterisation of the term structure, Journal of Financial Economics 5 (1977), 177–188.

- [10] P. Protter, Stochastic Integration and Differential Equations, A New Approach, Springer-Verlag, 1990.

- [11] Z. Schuss, Theory and Applications of Stochastic Differential Equations, John Wiley & Sons Inc., 1980.

- [12] Z. Brzesniak, T. Zastawniak, Basic Stochastic Process, Springer-Verlag, 1999.

- [13] R. Rebonato, Interest Rate Option Model, John Wiley & Sons, 1996.

- [14] E. W. Piotrowski, J. Sładkowski, Quantum Games in Finance, Quantitative Finance 4 (2004), 61.