Critical comparison of several order-book models for stock-market fluctuations

Abstract

Far-from-equilibrium models of interacting particles in one dimension are used as a basis for modelling the stock-market fluctuations. Particle types and their positions are interpreted as buy and sel orders placed on a price axis in the order book. We revisit some modifications of well-known models, starting with the Bak-Paczuski-Shubik model. We look at the four decades old Stigler model and investigate its variants. One of them is the simplified version of the Genoa artificial market. The list of studied models is completed by the models of Maslov and Daniels et al. Generically, in all cases we compare the return distribution, absolute return autocorrelation and the value of the Hurst exponent. It turns out that none of the models reproduces satisfactorily all the empirical data, but the most promising candidates for further development are the Genoa artificial market and the Maslov model with moderate order evaporation.

pacs:

89.65.-s Social and economic systems and 05.40.-a Fluctuation phenomena, random processes, noise, and Brownian motion and 02.50.-r Probability theory, stochastic processes, and statistics1 Introduction

The order book is the central notion in the stock market. People willing to buy or sell express their desire in well-specified orders and the authority of the stock exchange logs all the orders in a list, where they wait until they are either satisfied (executed) or cancelled. The visible part of the stock market dynamics, i. e. the complex movement of the price, is rooted in the detailed and mostly invisible processes happening within the order book. Anyone who wants to study seriously the stock market fluctuations, must pay attention to the dynamics of the order book.

There are several reasons why physicists may and should embark on such study. First, the discipline of Econophysics is now established and accepted with decent respect within the Physics community an_ar_pi_88 ; ma_sta_99 ; bou_pot_00 ; schweitzer_02 . But even if the study of economic phenomena by the tools of physics were a bare empty bubble (which is not!, the author believes) to be broken into pieces, the study of the order book itself may remain one of the shards of value. (Another one may be the Minority Game cha_zha_97 .) Indeed, the second motivation to spend some effort here is that the order book is a genuinely one-dimensional non-equilibrium system with complex dynamics. It abounds with rich phenomena and poses a serious intellectual challenge, which may provoke development of new tools in one-dimensional non-equilibrium physics.

The most simplified view of an order book may be the following. The orders are immobile particles of two kinds, (for asks, i. e. orders to sell), and (for bids, i. e. orders to buy), residing on a line of price (or logarithm of price, if more convenient). All bids are always on the left of all asks. The actual price lies somewhere between (and included) the highest bid and the lowest ask. The interval between the two is the spread and it is one of the key quantities observed in the order book. Besides these limit orders, waiting for the future in the order book, also market orders arrive, which buy or sell immediately at any price available in the market. Thus, the market orders provide liquidity.

As we already said, the tip of the order-book iceberg is the price. All order-book models must be confronted with what is known about the price fluctuations. These stylised facts are now very well established ma_sta_95 ; li_ci_me_pe_sta_97 ; go_me_am_sta_98 ; ple_gop_am_mey_sta_99 . To quote here only those which we shall be faced later, the price movements are generically characterised by a power-law tail in return distribution, with exponent , power-law autocorrelation of volatility, with exponent ranging between to , anomalous Hurst exponent , measured either directly in the so-called Hurst plot, or as a by-product of another essential feature of the price fluctuations, which is the scaling. It must be noted, though, that the scaling holds satisfactorily only for not too long time separations. At larger times, the gradual crossover to Gaussian shape of return distribution is observed. This feature is well reproduced in multifractal stochastic models (from many works in this direction see e. g. va_au_98 ; bac_del_muz_01 ; eis_ker_04 ; liu_dim_lux_07 ). However, we must state from the beginning, that explanation of multifractality and other subtle features of the stock-market fluctuations bou_mat_pot_01 ; lil_mik_far_05 , goes beyond the scope of this paper.

Let us mention at least some of the special features found empirically in order books. The literature is indeed very ample bia_hil_spa_95 ; mas_mil_01 ; cha_sti_01 ; cha_sti_03 ; gab_gop_ple_sta_03 ; ple_gop_gab_sta_04 ; ple_gop_sta_05 ; rosenow_02 ; web_ros_03 ; web_ros_04 ; bou_mez_pot_02 ; pot_bou_02 ; bou_gef_pot_wya_03 ; bou_koc_pot_04 ; wya_bou_koc_pot_vet_06 ; zov_far_02 ; lil_far_man_02 ; lil_far_man_03 ; far_gil_lil_mik_sen_03 ; far_pat_zov_03 ; pon_lil_man_06 ; far_zam_06 ; far_ger_lil_mik_06 ; lillo_06 ; sca_kai_kir_hub_ted_06 ; far_lil_04 . The first thing we may ask is the average order book profile, i. e. the average number of orders existing in given moment at given distance form the current price. It was found that it has sharp maximum very close to, but away from, the price cha_sti_01 ; bou_mez_pot_02 ; pot_bou_02 . The decrease at large distances seems to be a power law with exponent bou_mez_pot_02 ; pot_bou_02 , but the form of the increase between the price and the peak is not so clear.

Related information is contained in the price impact function, which says how much the price moves when an order of a specific volume arrives. In first approximation, we consider the virtual impact function, obtained by simple integration of the order book profile from the current price to the new, shifted price. Beyond the maximum, the profile decreases and therefore the virtual impact is a convex function mas_mil_01 ; cha_sti_01 ; web_ros_03 . The striking surprise in the empirical study of order books is, that the actual price impact is much smaller, and moreover, it is a concave, rather than convex, function of volume web_ros_03 . The form of the price impact was studied intensively gab_gop_ple_sta_03 ; lil_far_man_02 ; lil_far_man_03 ; far_gil_lil_mik_sen_03 ; far_pat_zov_03 ; pon_lil_man_06 ; far_zam_06 ; far_ger_lil_mik_06 , yet a controversy persist, whether it can be better fitted on a square root (a qualitative theoretical argument for this fit can be found in zhang_99 ), a power with exponent or on a logarithm.

The incoming orders have various volumes and it turns out that they are power-law distributed mas_mil_01 . For the market orders, the exponent is , while for the limit orders it has higher value . The limit orders are deposited at various distances from the current price and also here the distribution follows a power law bou_mez_pot_02 ; pot_bou_02 ; zov_far_02 ; lillo_06 , although the value of the exponent reported differs rather widely ( to ) from one study to another. The limit orders are eventually either satisfied or cancelled. The time they spend within the order book is again power-law distributed cha_sti_01 ; cha_sti_03 ; lo_mac_zha_02 with exponent for cancellations and for satisfactions.

There were attempts to explain some of the properties of price fluctuations as direct consequences of the empirically found statistics of order books. In Refs. gab_gop_ple_sta_03 ; gab_gop_ple_sta_03a the power-law tail in return distribution is related to the specific square-root form of the impact function combined with power-law distribution of order volumes. On the other hand, Ref. far_gil_lil_mik_sen_03 shows that the distribution of returns copies the distribution of first gap (the distance between best and second best order - where “best” means “lowest” for asks and “highest” for bids). It was also found that the width of the spread is distributed as power law, with exponent ple_gop_sta_05 , which is essentially the same value as the exponent for the distribution of returns. The discussion remained somewhat open, ple_gop_gab_sta_04 ; far_lil_04 , but we believe that the properties of the price fluctuations cannot be deduced entirely from the statistics of the order book. For example the difference between the virtual and actual price impact suggests that the order book reacts quickly to incoming orders and reorganises itself accordingly. Therefore, without detailed dynamical information on the movements deep inside the book we cannot hope for explanation of the dynamics of the price.

2 Existing models

There is no space here for an exhaustive review of the order-book modelling, not to speak of other types of stock-market models. We select here only a few models we shall build upon in the later sections and quote only a part of the literature. We apologise for unavoidable omissions, not due to underestimation of the work of others, but dictated by reasonable brevity of this study.

2.1 Stigler

To our best knowledge, the first numerical model of the order book and the first computer simulation ever in economics was the work of Stigler stigler_64 . The model is strikingly simple. There are only limit orders of unit volume and they are supplied randomly into the book within a fixed allowed interval of price. If the new order is e. g. a bid and there is an ask at lower price, then the bid is matched with the lowest ask and both of them are removed. If the bid falls lower than the lowest ask, it is stored in the book and waits there.

From this example we understand, why the order-book models are often called “zero-intelligence” models. Indeed, there is no space for strategic choice of the agents and the people may be very well replaced by random number generators. It is interesting to note that experiments with human versus machine trading were performed god_sun_93 , which found as much efficiency in “zero-intelligence” machines as in “rational” people (graduate students of business).

2.2 Bak, Paczuski, and Shubik

Another model, very simple to formulate but difficult to solve, was introduced by Bak, Paczuski, and Shubik (BPS) ba_pa_shu_97 . On a line representing the price axis, two kinds of particles are placed. The first kind, denoted (ask), corresponds to sell orders, while the second, (bid), corresponds to buy orders. The position of the particle is the price at which the order is to be satisfied. A trade can occur only when two particles of opposite type meet. If that happens, the orders are satisfied and the particles are removed from the system. This can be described as annihilation reaction . It is evident that all particles must lie on the left with respect to all particles. The particles diffuse freely and in order to keep their concentration constant on average, new orders are inserted from the left ( type) and from the right ( type). The whole picture of this order-book model is therefore identical to the two-species diffusion-annihilation process. The changes in the price are mapped on the movement of the reaction front.

Many analytical results are known for this model. Most importantly, the Hurst exponent can be calculated exactly krapivsky_95 ; bar_how_car_96 ; eli_ko_98 ; ta_tia_99 and the result is . This value is well below the empirically established value .

Several modifications of the bare reaction-diffusion process were introduced ba_pa_shu_97 to remedy some of the shortcomings of the model. The simplest one is to postulate a drift of articles towards the current price. This feature mimics the fact that in real order books the orders are placed close to the current price. It also suppresses the rather unnatural assumption of free diffusion of orders. However, the measured Hurst exponent remains to be as before.

More important modification consists in a kind of “urn” process. The new orders are placed close to already existing ones, thus mimicking certain level of “copying” or “herding” mechanism, which is surely present in the real-world price dynamics. In this case the Hurst exponent is higher and in fact very close to the random walk value, .

The diffusion constant of the orders can also be coupled to the past volatility, introducing a positive feedback effect. This way the Hurst exponent can be enhanced up to the level consistent with the empirical value. In this case, scaling was observed in the distribution of returns with Hurst exponent .

2.3 Genoa market model

The diffusion of orders contradicts reality. Indeed, orders can be placed into the order book, and later either cancelled or satisfied, but change in price is very uncommon. It is therefore wise to return back to Stigler’s immobile orders but to make his model more realistic.

Rather involved modification of the Stigler model appeared much later under the name of Genoa artificial market rab_cin_foc_mar_01 ; cin_foc_mar_rab_03 ; rab_cin_05 ; rab_cin_foc_mar_05 ; rab_cin_dos_foc_mar_05 ; cin_foc_pon_rab_sca_06 . The model contains many ingredients and is therefore very plastic.

Again, there are only limit orders and the liquidity is assured by non-empty intersection of intervals, where the bids and asks, respectively, are deposited. In practical implementation, the probability of order placement was Gaussian, with the centre shifted slightly above the current price for asks and slightly below for the bids. The width of the Gaussians was also related to the past volatility, thus introducing a feedback. Note that essentially the same feedback was introduced already in the BPS model. The price of the contract was calculated according to demand-offer balance. There was also a herding of agents in play, in the spirit of the Cont-Bouchaud model co_bou_97 . The main result to interest us here was the power-law tail of the return distribution, with very realistic value of the exponent. However, it was not at all clear which of the many ingredients of the model is responsible for the appearance of the power-law tail.

2.4 Maslov model

To appreciate the crucial role of the market orders, Maslov introduced a model maslov_99 , in which the bids are deposited always on the left and asks on the right from the current price. The limit orders never meet each other. The execution of the orders is mediated by the market orders, annihilating the highest bid or lowest ask, depending on the type of the market order.

The Maslov model has several appealing features. Especially, the return distribution characterised by exponent seems to be close to the empirically found power law. The scaling in return distribution is clearly seen as well as the volatility clustering manifested by power-law decay of the autocorrelation of absolute returns. However, the Hurst exponent is as in the BPS model, which is bad news. Maslov model was treated analytically in a kind of mean-field approximation slanina_01 . Unfortunately, the exponent found there disagrees with the simulations. Later, the reason for this difference was identified in the assumption of uniform density of orders on either of the sides of the price. Taking the density zero at the current price and linearly increasing on both the ask and bid side, the exponent becomes , in agreement with the numerics maslov_private .

2.5 Models with uniform deposition

The Maslov model is still very idealised. The most important difference from real situation is the absence of cancellations. In real order books the orders can be scratched, if their owners think that they waited too long for their patience. The group of Farmer and others introduced several variants of models with cancellation (“evaporation”) of orders smi_far_gil_kri_02 ; dan_far_ior_smi_02 ; dan_far_gil_ior_smi_03 ; ior_dan_far_gil_kri_smi_03 . Another fundamental feature which makes these models different from the Maslov model is that the orders are deposited uniformly within their allowed range, i. e. bids from the current price downwards up to a prescribed lower bound and equivalently for the asks.

The order book profile, price impact and many related properties were studied very thoroughly and their dependence on the rates of thee processes involved was clarified. An important step forward was the analytical study performed in smi_far_gil_kri_02 . Two complementary “mean-field” approaches were applied, achieving quite good agreement with the simulations. The first approach calculates the average density of orders as a continuous function, neglecting the fluctuations. The other approach represents the state of the order book by intervals between individual orders, assuming that at most one order can be present on one site (a kind of exclusion principle). The approximation consists in neglecting the correlations between the lengths of the intervals.

This line of research was recently pushed forward in and important paper by Mike and Farmer mik_far_07 . A scheme, which was given very fitting name “empirical model” was proposed, which incorporates several basic empirical facts on the order flow dynamics, namely the distribution of distances, from the best price, where the orders are placed; the long memory in the signs of the orders; the cancellation probability, depending on the position of the order. Including there empirical ingredients into the Farmer model, an excellent agreement with other empirical findings was observed, including the return and spread distributions. The importance of that work, at least from our point of view, consists in observation that the most tangible feature of the price fluctuation, the return distribution, is in fact a secondary manifestation of more basic and yet unexplained features. These are the features which enter the model of mik_far_07 as empirical input.

In our work, we address a less ambitious but more fundamental question. What will be the fluctuation properties of these models without assuming anything special about order flow? We shall see that in many aspects the answer is disappointing in the sense that the results are often far from reality. This means that the inputs of mik_far_07 are essential. On the other hand, we can hardly be satisfied until we detect the causes behind the empirical ingredients of mik_far_07 .

2.6 Other approaches

A rather phenomenological model was simulated in bou_mez_pot_02 . The profile of the order book was successfully explained assuming power-law distribution of placement distances from the current price.

In fact, the crucial role of the evaporation of orders was first noticed in the work of Challet and Stinchcombe cha_sti_01 . The new limit orders were deposited close to the price, with standard deviation which was linearly coupled with the width of the spread. The evaporation caused a clearly visible crossover from Hurst exponent at short time distances to the random-walk value at larger times. This class of models was investigated in depth subsequently cha_sti_03 ; cha_sti_02 ; stinchcombe_06 . In a related development, a version of asymmetric exclusion model ha_zha_95 was adapted as an order-book model wil_sch_cha_02 . The two crucial ingredients are the (biased) diffusion of particles (orders), returning somewhat back to the BPS model, and the exclusion principle, allowing at most one order at one site. It also forbids “skipping” of particles, so each order represents an obstacle for the diffusion of others. Price is represented by the particle of a special type. Mapping to the exactly soluble asymmetric exclusion model gives the precise value of the Hurst exponent , nicely coinciding with reality. One must remember, though, that the price for this result is the unrealistic assumption of diffusing orders. Moreover, even if we accepted the view that removal and immediate placement of an order not far from the original position may be effectively described as diffusion, why then the particles are not allowed to overtake each other? We consider that feature very far from reality.

Let us only list some other works we consider relevant for order-book modelling osborne_65 ; kul_ker_01 ; fra_mar_mat_01 ; mat_fra_01a ; far_josh_00 ; challet_06 . Schematic models, like the Interacting Gaps model mu_sla_sol_03 ; svo_sla_07 , may also bring some, however limited, insight. Despite continuing effort of many groups performing empirical analyses as well as theoretical studies, the true dynamics of the order book is far from being fully understood. On one side, the trading in the stock market is much more intricate than mere play of limit and market orders. There are many more types of them, sometimes rather complicated. At the same time, it becomes more and more evident that assuming “zero-intelligence” players misses some substantial processes under way in the stock market. Strategic thinking cannot be avoided without essential loss. This brings us close to our last remark. All the models mentioned in this section are appropriate only to those markets, which operate without an official market maker. In presence of a market maker, the orders do not interact individually, but in smaller or larger chunks. One is tempted to devise a “zero-intelligence” model with a market maker, but there is perhaps a wiser path to follow. We have in mind a combination of order-book models with Minority Game. The latter represents an antipole to “zero-intelligence” order-book models and amalgamating the two opposites may prove fruitful.

In this work we shall not go thus far. Our aim is rather to clarify the dark places in the ensemble of existing order-book models. Performing new simulations for several of these models in parallel, we hope to shed some light on the the usefulness and the limitations of them.

3 New simulations

Here we present our new results of numerical simulations of the models sketched above. Some of the data aim at improving the results already present in the literature, but mostly we try to clarify aspects not studied before. We also used the same methodology in analysing the simulations for all models, in order to make comparable statements for each of the models under scrutiny.

3.1 Bak-Paczuski-Shubik model

The first model to study is the Bak-Paczuski-Shubik (BPS) model. As we already explained, we have two types of diffusing particles, called and . There are particles of each type, i. e. total particles placed at the segment of length . The particles can occupy integer positions from the set . In one update step we choose one particle and change its position as (there is no bias, so both signs of the change have the same probability), on condition that the new position stays within the allowed interval, . We use the convention that the time advances by in one step. If the new site was empty or there was already another particle of the same type at the new position, nothing more happens an the update is completed. We set and , On the other hand, if the new site is occupied by a particle of opposite type, say, particle , so that , then the two particles annihilate. To keep the number pf particles constant, we immediately supply two new particles at opposite edges of the allowed segment. E. g. if was type and was type , the update is , and , .

The annihilation corresponds to an elementary transaction. The price set in this deal is just the position where the annihilation took place, . If the transaction did not occur, the price stays unchanged, . This completes the definition of the variant of the BPS model simulated here.

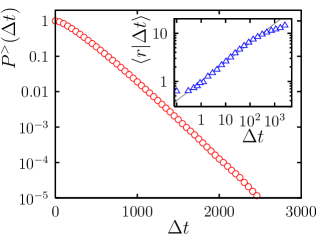

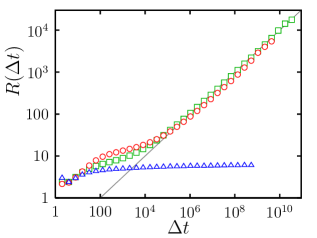

In Fig. 1 we can see how the typical configuration of orders evolves in time. There are rather long periods where the price does not change, but the positions of orders are mixed substantially. We shall first look at these waiting times between consecutive trades. In Fig. 2 we can see the (cumulative) probability distribution of them. It is evident that the distribution is exponential, or very close to it, so we can consider the sequence of trade times at least approximately as Poisson point process.

The most desired quantity is the one-trade return distribution. If is the time of -th trade, we define and in Fig. 3 we plot the distribution of the absolute returns in stationary state, for several sizes and particle numbers . We find that the distribution collapses onto a single curve when we rescale the data by the factor

| (1) |

We then find

| (2) |

and the scaling function decays faster than an exponential. The fit of the type seems to be fairly satisfactory. Evidently, this distribution is very far from the fat tails observed empirically. It is also interesting to see how the one-trade return depends on the waiting time before the trade. We measure the conditional average of the return

| (3) |

and find (see the inset in Fig. 2) that it increases slowly as a power law .

Diffusion of the price is quantified by the Hurst plot. Usually we calculate the quantity

| (4) |

where the average is taken over interval while the average extends over all times. The time-dependent normalisation in the denominator of (4) accounts for temporal variations of the volatility.

However, especially in BPS model the measure (4) is inconvenient as it does not cover properly the time scales below the typical waiting time. We use instead a simplified and also frequently used quantity

| (5) |

Both (4) and (5) are expected to share the same asymptotic behaviour for , i. e. with Hurst exponent .

The results for BPS model are shown in Fig. 4. We can appreciate there how difficult it is to actually observe the value predicted by the theory. Relatively long “short-time” regime seen in Fig. 4 is characterised by , which corresponds to ballistic, rather than diffusive, movement of the price. In this regime, the time scale is shorter than the average inter-event time, so there is typically at most one transaction. The transaction times follow approximately the Poisson point process, so the probability that one transaction occur during time is, for short times, proportional to . Assuming that the price change, if it occurs, has certain typical size, the scale of the average price change should be also proportional to . Hence the ballistic behaviour seen in the Hurst plot. Note, however, that this argument needs some refinement, because, as we have seen in Fig. 2, longer waiting times imply larger price jumps afterwards. Nevertheless, we believe that the general line of the argument is true.

The behaviour changes when becomes comparable to the average inter-event time. The most often encountered result is represented by triangles in Fig. 4. At scales larger than the average inter-event time the quantity saturates, yielding . It is easy to understand why it must be so. If the density of particles is large enough, the configuration of the order book can be described by average concentrations and of particles and , respectively. The variable measures the position on the price axis. It is easy to find that neglecting the fluctuations in the order density the solution of the BPS model trivialises into , . So, in absence of fluctuations the price is pinned in the exact middle of the allowed interval. This is just the saturation regime .

To see the theoretically predicted Hurst exponent we must find a time window between the ballistic and pinned regime. This is often very narrow, if it exists at all, as testified in Fig. 4 by the data for and . Only for large enough size with small enough density of orders the fluctuation regime is observable. (Note that in the finite-size analysis the number of orders must scale as with the length of the allowed interval.) In Fig. 4 we can see an example for , where such time window is visible.

The difficulty to observe the desired regime in BPS model contrasts with the way the exponent was derived analytically krapivsky_95 ; bar_how_car_96 . In these works the two reactants occupy initially the positive and negative half-lines, respectively. Then, they are let to diffuse and react. Annihilated particles are not replaced. Therefore, the reaction front spreads out indefinitely and we can observe a well defined long-time regime characterised by the exponent . (There is also a logarithmic factor there, but we neglect it in this discussion.) On the contrary, in BPS the long-time regime has always .

3.2 Stigler model and its free variant

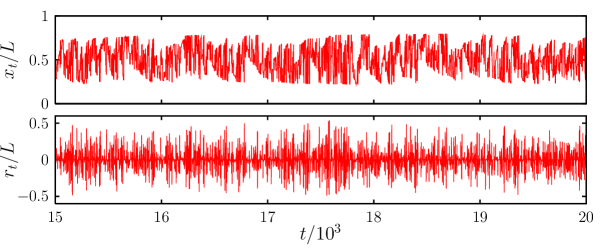

In Stigler model, we have again the allowed price range , where the orders can be placed. There can be at most orders total. If, at time , there is still the order deposited at time , it is removed. Then, we deposit a new order. We decide whether it will be a bid or an ask (with equal probability) and choose randomly, with uniform distribution, its position within the allowed price range. A transaction may follow. If the new order is e. g. a bid placed at position and the lowest ask is at position , then the new price is set to and both the new bid at and the old lowest ask at are removed. If , the price does not change, and the new bid stays in the order book. (Symmetrically it holds for depositing an ask.)

In Fig. 5 we show an example of the typical time sequence of price and one-step returns . Qualitatively, we can guess that the fluctuations are far from Gaussian, i. e. returns will not obey the normal distribution. Indeed, we can see in Fig. 6 that for several decades the distribution falls off slowly as a power with small exponent, and then it is sharply cut off. Indeed, the cutoff comes from the natural bound .

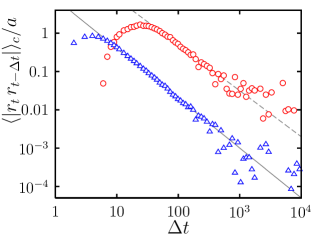

In the time series in Fig. 5 we can also glimpse the volatility clustering. To measure it quantitatively, we plot in Fig. 7 the autocorrelation of absolute returns

| (6) |

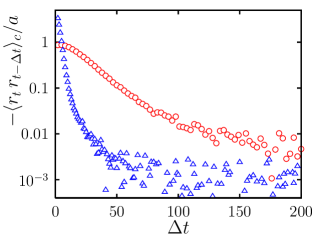

It decays as a power, but with rather large exponent, . On the other hand, the returns themselves are only short-time negatively correlated with exponential decay, as can be seen in Fig. 8.

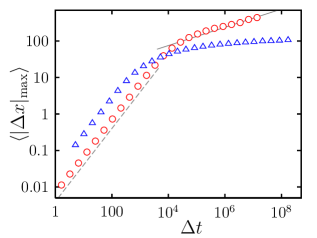

These findings show that Stigler model is not a very good candidate model for explaining the empirical facts. However, it may well serve as a starting point for successful construction of better models. The first limitation we must remove is the fixed range of prices from to . A severe consequence of this limitation is the saturation seen in the Hurst plot (Fig. 13). In long time regime, the Hurst exponent is obviously . To cure this problem we introduce a “free” variant of the Stigler model. It may be also considered as a precursor of the Genoa market model, to be studied in the next section.

The price axis is now extended to all integer numbers. Of course, the position on this axis must be now interpreted as logarithm of price, rather than price itself. Nonetheless, for brevity we shall speak of “price” also in this case. The orders are again deposited randomly within an allowed range, but now the range depends on the actual position of the price . We introduce two integer parameters, the width of the allowed interval and the shift of the interval’s centre with respect to the current price. Denote the order issued at time . If it is a bid, it is deposited uniformly within the range , while for an ask the range is . Of course, in order to have any transactions at all, we must have . As with the Stigler model, the orders older than steps are removed.

In spite of the change in the deposition rules, the basic features of the free Stigler model remain very similar to those of the original variant. In Fig. 6 we can see that the return distribution exhibits slow power-law decay with a sharp cutoff at large returns. The exponent is larger than in the Stigler model, but still remains very much below the empirical value . The autocorrelation of absolute returns (see Fig. 7) decays as a similar power law . In addition, a peak in the autocorrelation function, merely visible in Stigler model, becomes quite pronounced here and is shifted to larger times, about . This indicates some quasi-periodic pattern in the time series of the volatility, related probably to a typical waiting time between subsequent trades. Indeed, we found that the waiting times are exponentially distributed, and for the parameters of Fig. 7 the average waiting time is about . As for the autocorrelation of returns, it decays exponentially again, albeit more slowly, as shown in Fig. 8.

The main difference observed, compared to the original Stigler model, is shown in the Hurst plot, Fig. 13. At shorter times, there is a tendency to saturation, as in the Stigler model, but at larger times the purely diffusive regime with prevails. We can attribute these results the following interpretation. The orders present in the order book form a “bunch” located somewhere around the current price. Orders too far from the price are usually cancelled after their lifetime (equal to ) expires. Hence the localisation around the price. Now, while in the Stigler model the bunch of orders is imprisoned between and , in the free Stigler model the bunch can wander around, following the price changes. The value shows that the movements of the bunch as a whole can be described as an ordinary random walk.

3.3 Genoa market model

Both in original and free Stigler model, the agents behind the scene have truly zero intelligence. At most, they look at the price in this instant and place orders at some distance from it, but the distance is not affected neither by the present nor the past sequence of prices. However, it is reasonable to expect that the agents react to the fluctuations observed in the past. The simplest feedback mechanism may be that the distance to place an order is proportional to the volatility measured during some time period in the past. This idea was already applied in one of the variants of the BPS model ba_pa_shu_97 and lies in the basis of the Genoa artificial market rab_cin_foc_mar_01 . What we shall call “Genoa market model” from now on, is in fact very reduced version of the complex simulation scheme of Ref. rab_cin_foc_mar_01 . We believe, however, that we retain the most significant ingredients.

We must first define a convenient measure of instantaneous volatility. Averaging absolute price changes with an exponentially decaying kernel

| (7) |

turns out to be a good choice. We use the value throughout the simulations. The orders will be placed on integer positions within an interval determined by the width and the shift from actual price, as in the free Stigler model, but now these two parameters are time-dependent. Their ratio will be held constant and both will expand as the volatility will grow. So, the prescription will be

| (8) |

and the constants and , besides the maximum number of orders (i. e. maximum lifetime of an order) constitute the parameters of the model. In order that we have any transactions at all, we impose the bound .

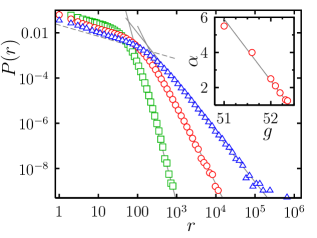

The feedback mechanism we apply makes significant difference in all aspects of the model. Let us look first at the return distribution. In Fig. 9 we can see how it changes when we tune the parameter . Generically, a power-law tail develops, with an exponent strongly depending on . The larger , the smaller the exponent, until for some critical value it approaches the limit . beyond that point, the average returns, i. e. also the stationary value of the average volatility diverges. This may be regarded as a kind of phase transition. It is also worth nothing that for low returns there is an interval where another power law holds, with . This is the remainder of the behaviour characteristic for the free Stigler model, the parent of the Genoa stock market.

We can look at this behaviour from another aspect when we directly

calculate the time average

. Its dependence

on is shown in Fig. 10. This plot requires

some explanation. The actual implementation of the algorithm prevents

the average volatility from diverging. Instead, it reaches a

relatively large value above . So, all points beyond this level

should be considered as effectively infinite. Moreover, in

Fig. 10 we can see a sign of bistability, or

hysteresis, which is at first sight a signature of a first-order phase

transition. However, a more careful analysis with varying shows

that the presence of an apparent hysteresis curve is

misleading. Actually, it is a subtle finite-size effect and the

phase transition is continuous (i. e. second order).

We can see that the transition points found independently in Figs. 9 and 10 are consistent, so it is indeed a single transition with two aspects. In fact, the coincidence between Figs. 9 and 10 means equality of time and “ensemble” averages, i. e. ergodicity of the model dynamics.

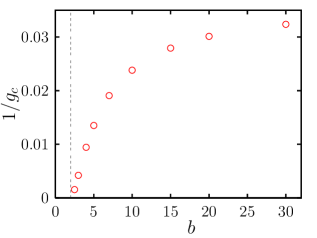

In Fig. 11 we show a phase diagram of the model, indicating the dependence of the critical point on the parameter . When approaches its lower limit equal to (note that there are no trades for ), the critical value diverges. It comes as no big surprise, because trades became more rare when and therefore the volatility diminishes. This allows the feedback measured by to be stronger without divergence in the realised average volatility. The phase diagram depends on the maximum number of orders , but we found that the dependence is very weak and never changes the qualitative look of the phase diagram. The reason for this is that for large the actual number of orders present in the system is maintained mainly by the annihilation by other orders and the fraction of orders which live long enough to be discarded at the end of their lifetime is very small. In other words, the average number of orders in the system grows extremely slowly with .

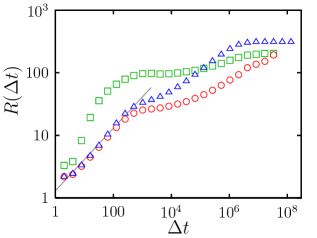

To complete the study of the Genoa market model, we show in Fig. 12 the autocorrelations and in Fig. 13 the Hurst plot. Contrary to both the Stigler model and its free variant, the autocorrelation of absolute returns decays as a clear exponential, although the characteristic time is extremely long. As for the Hurst exponent, is is equal to , in accord with the behaviour of the free Stigler model. In both Genoa and free Stigler models the long-time behaviour of is dominated by the diffusion of the bunch of orders as a whole. What makes difference between the two is the dynamics within the bunch, but this is not visible in the Hurst plot. Note also that for the parameters used in Fig. 13 the regime with starts at times . At such time scale the autocorrelations are already damped out, regardless the power-law decay in free Stigler or the slow exponential decay in Genoa models (compare Figs. 7 and 12).

3.4 Maslov model

So far, the models investigated did not distinguish between limit orders and market orders. The distinction was only implicit. All bids placed below the lowest ask acted effectively as limit orders, as well as the asks placed above the highest bid. In the model of Maslov maslov_99 the orders of unit volume were issued at each step, being limit orders or market orders with equal probability . The limit orders were placed at close vicinity of the current price. Here we add also the feature of order evaporation, as in cha_sti_01 . Each order present in the book will have the same probability of being cancelled (evaporated). Therefore, we do not take into account the age of the order, as we did in various variants of the Stigler model.

We tune the speed of the evaporation by a parameter . For simpler terminology, we shall call it evaporation probability. Actually, the probabilities of deposition, satisfaction and evaporation event in one step of the evolution, at time , will be defined as, respectively,

| (9) |

where is the actual number of orders in the book. The parameter controls the number of orders in the book and again, to simplify the terminology, it will be called average number of orders, although the actual value of the average number of orders is slightly different (due to the effect of fluctuations). If the evaporation probability is zero, the parameter becomes irrelevant for the dynamics. Note that the three probabilities (9) change in time, as the total number of orders fluctuates.

The orders are placed at integer positions denoting the (logarithm of the) price. Let be the price at time and , actual number of asks and bids, respectively, with the total number of orders .

In case deposition is selected to happen, according to probabilities (9), we add an ask () or a bid () with equal probability. The position of the new order is , for the ask and sign for the bid. The price remains unchanged, because no transaction occurred.

The execution, or satisfaction, of an order happens always when a market order is issued, and there is a limit order to match it. Again, sell and buy side are equivalent, so they are selected with equal probability . Suppose a sell order is issued and there is at least one bid, , and is the position of the highest bid. Then, the new price is , we update and remove the order at from the book. Symmetrically it holds for the buy order.

When the evaporation of an order is about to happen, we select any of the existing orders with uniform probability and remove it from the system. Note that removals of a bid and an ask are not equiprobable, as we evaporate a bid with probability and an ask with probability .

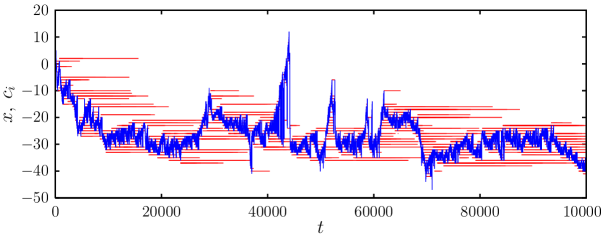

We can see in Fig. 14 the space-time diagram of a typical evolution of the order book. The price “sows” new orders along its fluctuating path, which are either satisfied, as the price returns next to its original position, or they vanish by evaporation. Longer price jumps occur when the density of orders is low. Conversely, the price becomes temporarily pinned, when it enters a region with large density of orders.

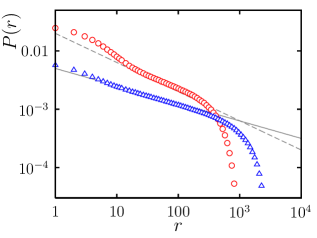

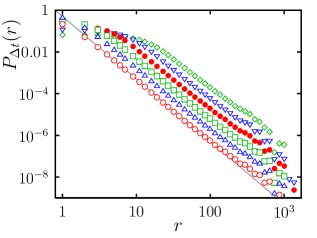

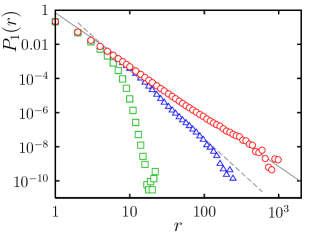

Let us first revisit the results for the original Maslov model without evaporation (). In Fig. 15 we show the distribution of returns at several time lags

| (10) |

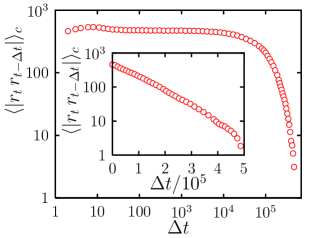

We can see clearly the power-law tail , observed first in maslov_99 . The results can be also rescaled to fall onto a single curve, as shown in Fig. 16. The dependence of the scaling factor on the time lag is shown in the inset of Fig. 16 and we can clearly see the power-law dependence . Hence we deduce the Hurst exponent of the price fluctuation process . The same value of the Hurst exponent is confirmed independently by drawing the Hurst plot, Fig. 20.

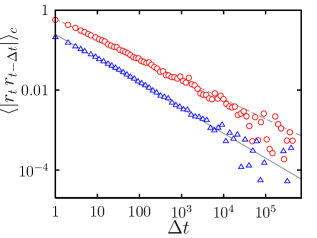

The volatility clustering, measured by the autocorrelation of absolute returns, is shown in Fig. 17. The autocorrelations decay as a power law, similarly as in the Stigler model, but now the exponent is significantly lower, , which makes the behaviour much more similar to empirical price sequences.

Now we investigate the effect of finite evaporation probability, . In the distribution of one-step returns, Fig. 18, it leads to deformation of the original power-law dependence. At very small values of , we observe an effective increase of the power-law exponent, to values and even more. This would sound fine, as this is just the value reported in empirical studies. However, a cutoff starts developing as well and when we increase further, the cutoff prevails and the power-law regime vanishes completely. Since the evaporation destroys the power law, it is not surprising that the scaling also breaks down. In Fig. 19 we can see that no scaling can be seen, because at each time lag the shape of the graph is different.

While the return distribution changes substantially, the absolute return autocorrelation remains nearly the same. The decay follows again a power law, but the exponent is somewhat larger, . The long-time correlations are caused by the immobile orders who sit within the book until the price finds its path back to them. Evaporation removes some of the orders, thus eroding the correlations. Quantitatively it results in suppression of the correlation function.

Finally, we look at the Hurst plot, Fig. 20. As mentioned already in cha_sti_01 , evaporation of orders induces the crossover to purely diffusive behaviour, at large times. Interestingly, when we compare the quantity at equal time difference for different values of we can see that larger evaporation probability actually suppresses the diffusion. The Hurst exponent remains universal, but the diffusion constant is lower for larger . The possible explanation is that the evaporation events go at the expense of satisfaction events. Therefore, there are less trades per unit of time, hence the slower diffusion of the price.

We studied also another modification of the Maslov model, where the evaporation of orders was implemented in the sense of Stigler model. Instead of removing an arbitrarily chosen order with fixed probability, we track the age of the orders and remove them if the age exceeds certain fixed lifetime. We did not observe much difference compared to the variant with usual evaporation. The Hurst plot looks much like that of Fig. 20, showing clear crossover from the short time to long-time behaviour. Absolute returns autocorrelation decays as a power with similar (slightly larger) exponent. Somewhat larger difference can be seen in the return distribution. The finite lifetime of the orders leads to decrease in the exponent of the power-law part, while the evaporation causes its increase. Qualitatively, the cutoff at larger returns seems more severe than in the case of evaporation, although quantitative comparison is hardly possible. To sum up, we consider the variant with finite lifetime farther from the reality than the variant with simple evaporation.

3.5 Uniform Deposition Model

In Maslov model, the new orders are placed locally, at distance from the actual price. It could be possible to fix another limit for the maximum distance, and indeed, in the original work maslov_99 this number was . There is little, if any, effect of the precise value of this parameter. The important thing is that the orders are never placed farther than certain predefined limit.

In reality, however, the distribution of distances at which the orders are placed is rather broad and decays as a power law bou_mez_pot_02 . The mechanism responsible for this power law is probably related to the optimisation of investments performed by agents working at widely dispersed time horizons lillo_06 . Actually it is reasonable to expect that the distribution of time horizons and (related to it) distribution of distances is maintained by equilibration, so that all agents expect just the same average gain, irrespectively of the time horizon on which they act. This idea would certainly deserve better formalisation.

Instead of taking the empirical distribution of placements as granted without deeper theoretical understanding, we prefer to compare the localised deposition in Maslov model with a complementary strategy applied in the set of models investigated by Daniels, Farmer and others smi_far_gil_kri_02 ; dan_far_ior_smi_02 ; dan_far_gil_ior_smi_03 ; ior_dan_far_gil_kri_smi_03 . Instead of keeping short distance from the price, the orders are deposited with equal probability at arbitrary distance. In this work, we adopt one of the variants studied in smi_far_gil_kri_02 and within this paper we shall call it Uniform Deposition Model (UDM).

In fact, the only difference with respect to the Maslov model with evaporation, defined in Sec. 3.4 is that we limit the price to a segment of length and orders are deposited uniformly on this segment. So, the orders and price can assume integer position from the set . As in the Maslov model, there are three classes of events, deposition, order satisfaction, and evaporation. Their probabilities are defined by the same formulae (9) as in the Maslov model. When an order is to be deposited, we first look where is the price . Then, select randomly a point from the set and deposit an order there. If the order becomes an ask, if it is a bid. (We forbid depositing exactly at the price position.) Although the probabilities (9) look the same as in the Maslov model, we should note that there is a big difference in the typical values of the evaporation probability . In Maslov model the orders are clustered around the price and the evaporation is somehow a complement or correction to the natural satisfaction of the limit orders by incoming market orders. So, is typically a small number compared to . On the contrary, in UDM the evaporation is essential, because orders are deposited in the whole allowed segment and ought to be removed also from areas where the price rarely wanders. Therefore, is comparable to, although smaller than, one. Very often, the simulations were performed in the regime where was much smaller than .

To see a typical situation, we plot in Fig. 21 the space-time chart of orders and price. We can see how the price “crawls” through a see of orders and the configuration of the orders changes substantially also very far from the price and without being affected by its movement. Of course, this is to be expected due to uniform deposition rule. On the other hand, this is certainly not a realistic feature.

We found fairly interesting, although absolutely unrealistic, the distribution of one-step returns, as shown in Figs. 22 and 23. The tail is characterised by power-law decay and the exponent, close to the fraction , seems to be universal, irrespectively of the parameters and . The value of the exponent is far below the empirical value, but the very fact of universal behaviour in such reaction-deposition model calls for explanation. We do not have any yet.

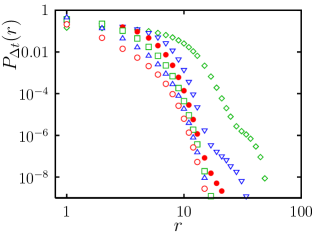

While the power law in the return distribution indicates some scale-free behaviour at single time, we find no sign of scaling when we compare the returns at different time scales. We can see that in Fig. 24. At longer lags the power-law tail vanishes and the distribution becomes uniform. This means that after long enough time the price can jump arbitrarily from one position to another within nearly all the allowed range, except the vicinity of the extremal points. In fact, the same behaviour was observed also for long enough time lags in the Stigler model. Certainly, the origin of such behaviour is the very existence of the limited price range, both in UDM and the Stigler model.

Let us look on the volatility clustering now. In Fig. 25 we show the autocorrelation of absolute returns. the decay is rather slow, i. e. slower than exponential, but at the same time it is faster than a power law. This behaviour is special to the Uniform Deposition Model.

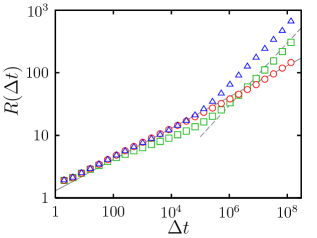

Finally, in Fig. 26 we show the Hurst plot. Again, there is close similarity to the Stigler model in the sense that there is no long-time diffusive regime but saturation is observed instead. Only in the very short initial transient we observe ordinary diffusion-like behaviour characterised by . It is unclear from our simulations whether there is an intermediate time window in which a non-trivial Hurst exponent (like the notorious ) would be observed.

4 Conclusions

It is not easy to make a synoptic comparison of the whole ensemble of models studied here. However, one easy conclusion can be drawn, that none of them reproduces satisfactorily the reality. Most importantly, the empirically observed Hurst exponent is not found anywhere. We can classify the diffusion behaviour into three main types. The first and most trivial one is dominated by the saturation, and happens always when the price is restricted by definition to an interval, like in the Stigler and Uniform Deposition models. The same holds also for the asymptotic regime of the BPS model, although in the latter the interesting things happen at the intermediate time scale, where . We do not exclude the possibility that also in UDM the intermediate times have , but we were not able to make any conclusive statement about that. The second type is characterised by asymptotic sub-diffusion, with . Strictly speaking this holds only for the Maslov model without evaporation. The third and most frequent type of behaviour can be described as ordinary diffusion () at long times. The initial transient regime may exhibit either , as in the Maslov model with evaporation or with fixed finite lifetime of orders, or it may instead show the tendency to saturation, as in the free Stigler model and Genoa artificial market model. It seems really difficult to design an order-book model where super-diffusive behaviour () would arise naturally, without being put in by hand. We cannot resist the temptation to compare this difficulty with the situation in stochastic modelling by continuous-time random walks scalas_05 . There also, the sub-diffusive behaviour can be found easily, but the super-diffusive one should be essentially forced.

The power-law tails in the return distribution seem to work slightly better. When we set apart the BPS model, where the tail decays even faster than exponentially, we can distinguish the models where the exponent in the power-law decay is far too low (), which comprises Stigler model, free Stigler model and UDM, from the models, where the exponent lies close, although not always precisely at the empirical value. The latter group contains the Genoa market model and the Maslov model with and without evaporation. The best chance for success when matched with the real data has the Genoa model, where the exponent can be tuned by variation of the model parameters. On the other hand, it is a priori unclear, why the parameter values should be this and not that. In the Maslov model proper, the exponent is universal, . Adding evaporation increases this value, so the agreement with the data can be again tuned, in this case by changing the evaporation speed. However, evaporation induces not only effective increase of the exponent, but also emergence of a cutoff. In fact, we think that the change in exponent is only an illusion brought about by combination of the power law and a weak cutoff. This contrasts with the Genoa model, where, below the phase transition, the power-law tails are genuine for all values of the parameter .

The very existence of the phase transition in the Genoa market model is a remarkable fact. It is intimately related to the dependence of the tail exponent on . When the exponent drops to the value the average return diverges and the transition occurs. One could speculate, how the picture would change if the feedback between volatility and order placement was defined differently. For example, the volatility can be defined through squares of returns, instead of absolute returns. This would also sound more natural, we think. We expect that in this case the transition would be related to the divergence of the second moment of the return distribution, i. e. it would be located at such parameter values which would imply the exponent . Otherwise, the picture would be most probably the same.

There is one feature, not so much important as such, but showing that the free Stigler model, Genoa stock market and Maslov model are members of the same family. If we look at the return distribution at small returns, we find that Genoa stock market and Maslov model (see Ref. maslov_99 ) exhibit another power-law regime, with very small exponent . Clearly it is the sign that deep within the bunch of orders surrounding the price the two models behave just like the free Stigler model, which shows the same power law in entire range of returns.

The return distribution in the Maslov model without evaporation has a very important and appealing feature. Its is the scaling property. The returns at different time lags scale with Hurst exponent equal to . Qualitatively it agrees with the empirically found scaling, but, unfortunately, quantitatively it is completely off. An important finding is that the evaporation of orders destroys the scaling, which is also absent in the UDM model. On the contrary, we also observed scaling in the Genoa market model, but not a perfect one. The difference between different lags is in the (not so much important, after all) low-return range, where the power-law tail is not yet developed.

When we want to compare the volatility clustering measured through the autocorrelation of absolute returns, we exclude the BPS model. Due to rather long waiting times, the measurement of the autocorrelation was impractical. In all remaining models, we found slow decay of the autocorrelations, but the functional form was not always a power. In fact, there are two exceptions. In the Genoa market model, the decay is exponential, although very slow. In UDM, the decay is faster than any power-law but slower than an exponential. A stretched exponential may be perhaps the candidate. In the remaining models, the power-law decay is observed. The difference lies in the exponent. While in the Stigler and free Stigler model, the exponent is above , in the Maslov model, both with and without evaporation, the value lies at or close to .

A crucial conclusion from the above is, that we cannot simply pick a model (“the best one”) from those studied here and apply it directly for a stock-market practice, e. g. for option pricing. All the models need some extensions or modifications to serve well as a realistic description. In this work we had no intent to amend the models by gluing together ad hoc parts with the only scope to get exponents right. We consider that counter-productive. If a simple, bare model is not satisfactory, one should look for another one, preferably as simple as the first one. That is why we strove to compare “bare” models here. To express our feeling, the models which passed the tests with highest scores were the Genoa market model and the Maslov model, with some (but not too much) evaporation of orders. We must also note that the empirical model of Ref. mik_far_07 reproduces the data for return distribution by far the best accuracy. At the same time, though, it makes use of several empirical inputs, rather than clear microscopic mechanisms, and therefore follows somewhat different modelling philosophy than ours. That is why we leave this model aside, without neglecting its merits and importance.

To sum up, we compared several order-book models of stock-market fluctuations. None of them is fully satisfactory yet. Calculating the return distribution, volatility autocorrelation and the Hurst plot, we were able to identify which of the models are promising candidates for future development. To tell the names, they are the Genoa market model and the Maslov model.

Acknowledgements.

This work was supported by the MŠMT of the Czech Republic, grant no. 1P04OCP10.001, and by the Research Program CTS MSM 0021620845.References

- (1) P. W. Anderson, K. J. Arrow, and D. Pines (eds.), The Economy as an Evolving Complex System (Addison Wesley, Reading, 1988).

- (2) R. N. Mantegna and H. E. Stanley, Introduction to Econophysics: Correlations and Complexity in Finance (Cambridge University Press, Cambridge, 1999).

- (3) J.-P. Bouchaud and M. Potters, Theory of Financial Risks (Cambridge University Press, Cambridge, 2000).

- (4) F. Schweitzer (editor), Modeling Complexity in Economic and Social Systems, (World Scientific, Singapore, 2002).

- (5) D. Challet and Y.-C. Zhang, Physica A 246, 407 (1997).

- (6) R. N. Mantegna and H. E. Stanley, Nature 376, 46 (1995).

- (7) Y. Liu, P. Cizeau, M. Meyer, C.-K. Peng, and H. E. Stanley, Physica A 245, 437 (1997).

- (8) P. Gopikrishnan, M. Meyer, L. A. N. Amaral, and H. E. Stanley, Eur. Phys. J. B 3, 139 (1998).

- (9) V. Plerou, P. Gopikrishnan, L. A. N. Amaral, M. Meyer, and H. E. Stanley, Phys. Rev. E 60, 6519 (1999).

- (10) N. Vandewalle and M. Ausloos, Eur. Phys. J. B 4, 257 (1998).

- (11) E. Bacry, J. Delour, and J. F. Muzy, Phys. Rev. E 64, 026103 (2001).

- (12) Z. Eisler and J. Kertész, Physica A 343, 603 (2004).

- (13) R. Liu, T. Di Matteo, T. Lux, arXiv:0704.1338 (2007).

- (14) J.-P. Bouchaud, A. Matacz, and M. Potters, Phys. Rev. Lett. 87, 228701 (2001).

- (15) F. Lillo, S. Mike, and J. D. Farmer, Phys. Rev. E 71, 066122 (2005).

- (16) B. Biais, P. Hillion, and C. Spatt, The Journal of Finance 50, 1655 (1995).

- (17) S. Maslov and M. Mills, Physica A 299, 234 (2001).

- (18) D. Challet and R. Stinchcombe, Physica A 300, 285 (2001).

- (19) D. Challet and R. Stinchcombe, Physica A 324, 141 (2003).

- (20) X. Gabaix, P. Gopikrishnan, V. Plerou, and H. E. Stanley, Nature 423, 267 (2003).

- (21) V. Plerou, P. Gopikrishnan, X. Gabaix, and H. E. Stanley, Quant. Finance 4, C11 (2004).

- (22) V. Plerou, P. Gopikrishnan, and H. E. Stanley, Phys. Rev. E 71, 046131 (2005).

- (23) B. Rosenow, Int. J. Mod. Phys. C 13, 419 (2002).

- (24) P. Weber and B. Rosenow, Quant. Finance 5, 357 (2005).

- (25) P. Weber and B. Rosenow, Quant. Finance 6, 7 (2006).

- (26) J.-P. Bouchaud, M. Mézard, and M. Potters, Quantitative Finance 2, 251 (2002).

- (27) M. Potters and J.-P. Bouchaud, Physica A 324, 133 (2003).

- (28) J.-P. Bouchaud, Y. Gefen, M. Potters, and M. Wyart, Quant. Finance 4, 176 (2004).

- (29) J.-P. Bouchaud, J. Kockelkoren, and M. Potters, Quant. Finance 6, 115 (2006).

- (30) M. Wyart, J.-P. Bouchaud, J. Kockelkoren, M. Potters, and M. Vettorazzo, physics/0603084 (2006).

- (31) I. Zovko and J. D. Farmer, Quant. Finance 2, 387 (2002).

- (32) F. Lillo, J. D. Farmer, and R. N. Mantegna, cond-mat/0207428.

- (33) F. Lillo, J. D. Farmer, and R. N. Mantegna, Nature 421, 129 (2003).

- (34) J. D. Farmer, L. Gillemot, F. Lillo, S. Mike, and A. Sen, Quant. Finance 4, 383 (2004).

- (35) J. D. Farmer, P. Patelli, and I. I. Zovko, Proc. Natl. Acad. Sci. U.S.A. 102, 2254 (2005).

- (36) A. Ponzi, F. Lillo, and R. N. Mantegna, physics/0608032 (2006).

- (37) J. D. Farmer and N. Zamani, Eur. Phys. J. B 55, 189 (2007).

- (38) J. D. Farmer, A. Gerig, F. Lillo, and S. Mike, Quant. Finance 6, 107 (2006).

- (39) F. Lillo, Eur. Phys. J. B 55, 453 (2007).

- (40) E. Scalas, T. Kaizoji, M. Kirchler, J. Huber, and A. Tedeschi, Physica A 366, 463 (2006).

- (41) J. D. Farmer and F. Lillo, Quant. Finance 4, C7 (2004).

- (42) Y.-C. Zhang, Physica A 269, 30 (1999).

- (43) A. W. Lo, A. C. MacKinlay, and J. Zhang, Journal of Financial Economics 65, 31 (2002).

- (44) X. Gabaix, P. Gopikrishnan, V. Plerou, and H. E. Stanley, Physica A 324, 1 (2003).

- (45) G. J. Stigler, The Journal of Business 37, 117 (1964).

- (46) D. K. Gode and S. Sunder, The Journal of Political Economy 101, 119 (1993).

- (47) P. Bak, M. Paczuski, and M. Shubik, Physica A 246, 430 (1997).

- (48) P. L. Krapivsky, Phys. Rev. E 51, 4774 (1995).

- (49) G. T. Barkema, M. J. Howard, and J. L. Cardy, Phys. Rev. E 53, 2017 (1996).

- (50) D. Eliezer and I. I. Kogan, cond-mat/9808240.

- (51) L.-H. Tang and G.-S. Tian, Physica A 264, 543 (1999).

- (52) M. Raberto, S. Cincitti, S. M. Focardi, and M. Marchesi, Physica A 299, 319 (2001).

- (53) S. Cincotti, S. M. Focardi, M. Marchesi, and M. Raberto, Physica A 324, 227 (2003).

- (54) M. Raberto and S. Cincotti, Physica A 355, 34 (2005).

- (55) M. Raberto, S. Cincotti, S. M. Focardi, and M. Marchesi, Computational Economics 22, 255 (2003).

- (56) M. Raberto, S. Cincotti, C. Dose, S. M. Focardi, and M. Marchesi, in: Nonlinear Dynamics and Heterogeneous Interacting Agents, eds. T. Lux, S. Reitz, and E. Samanidou 305 (Springer, Berlin, 2005).

- (57) S. Cincotti, S. M. Focardi, L. Ponta, M. Raberto, and E. Scalas, in: The Complex Network of Economic Interactions, eds. A. Namatame, T. Kaizouji, and Y. Aruka, 239 (Springer, Berlin, 2006).

- (58) R. Cont and J.-P. Bouchaud, Macroeconomic Dynamics 4, 170 (2000).

- (59) S. Maslov, Physica A 278, 571 (2000).

- (60) F. Slanina, Phys. Rev. E 64, 0561136 (2001).

- (61) S. Maslov, private communication.

- (62) E. Smith, J. D. Farmer, L. Gillemot, and S. Krishnamurthy, Quant. Finance 3, 481 (2003).

- (63) M. G. Daniels, J. D. Farmer, G. Iori, E. Smith, cond-mat/0112422.

- (64) M. G. Daniels, J. D. Farmer, L. Gillemot, G. Iori, and E. Smith, Phys. Rev. Lett. 90, 108102 (2003).

- (65) G. Iori, M. G. Daniels, J. D. Farmer, L. Gillemot, S. Krishnamurthy, and E. Smith, Physica A 324, 146 (2003).

- (66) S. Mike and J. D. Farmer, Journal of Economic Dynamics and Control 32, 200 (2008).

- (67) D. Challet and R. Stinchcombe, cond-mat/0208025.

- (68) R. Stinchcombe, in: Econophysics and Sociophysics: Trends and Perspectives, ed. B. K. Chakrabarti, A. Chakraborti, and A. Chatterjee, pp. 35-63 (Wiley-VCH, Weinheim, 2006).

- (69) T. Halpin-Healy and Y.-C. Zhang, Phys. Rep. 254, 215 (1995).

- (70) R. D. Willmann, G. M. Schütz, and D. Challet, Physica A 316, 430 (2002).

- (71) M. F. M. Osborne, Econometrica 33, 88 (1965).

- (72) L. Kullmann and J. Kertész, Physica A 299, 234 (2001).

- (73) F. Franci, R. Marschinski, and L. Matassini, Physica A 294, 213 (2001).

- (74) L. Matassini and F. Franci, Physica A 289, 526 (2001).

- (75) J. D. Farmer and S. Joshi, Journal of Economic Behavior and Organization 49, 149 (2002).

- (76) D. Challet, physics/0608013 (2006).

- (77) L. Muchnik, F. Slanina, and S. Solomon, Physica A 330, 232 (2003).

- (78) A. Svorenčík and F. Slanina, Eur. Phys. J. B 57, 453 (2007).

- (79) E. Scalas, in: The Complex Network of Economic Interactions, eds. A. Namatame, T. Kaizouji, and Y. Aruka, 3 (Springer, Berlin, 2006).