Shrinkage and spectral filtering of correlation matrices:

a comparison via the Kullback-Leibler distance

††thanks: Presented at the Workshop “Random Matrix Theory: From Fundamental Physics To Application”, Krakow, Poland, May 3 -5, 2007.

Abstract

The problem of filtering information from large correlation matrices is of great importance in many applications. We have recently proposed the use of the Kullback-Leibler distance to measure the performance of filtering algorithms in recovering the underlying correlation matrix when the variables are described by a multivariate Gaussian distribution. Here we use the Kullback-Leibler distance to investigate the performance of filtering methods based on Random Matrix Theory and on the shrinkage technique. We also present some results on the application of the Kullback-Leibler distance to multivariate data which are non Gaussian distributed.

02.50.Sk, 05.45.Tp, 05.40.Ca, 02.10.Yn, 89.65.Gh

1 Introduction

In many applications the monitoring of the dynamics of the system provides multivariate time series and often the number of monitored variables is very high. Examples include gene expression level measurement in microarray experiments brown , fMRI experiments Eguiluz , analysis of economic or financial data such as firm growth rates or stock price returns Laloux1999 ; Plerou1999 ; Mantegna1999 . A common way to investigate the interaction between the variables of the system is through the cross correlation matrix. As any statistical estimator, the sample correlation matrix is unavoidably affected by the statistical uncertainty due to the finite size of the sample. This problem becomes extremely important when the number of investigated variables is comparable with the number of records of each variable. To cope with the problem of the statistical uncertainty of the sample correlation matrix one needs to introduce filtering methods able to remove from the correlation matrix at least part of the noise. Many techniques have been proposed in the literature in order to filter out information from the correlation matrix. However, unless one knows in advance the model describing the system dynamics, it is difficult to asses the goodness of the filtering procedures. Recently Tumminello2007 we have proposed the use of the Kullback-Leibler (KL) distance as a method of assessing the performance of correlation matrix filtering procedures. There are several reasons why we believe KL distance is a good performance estimator. The main reason is that we proved Tumminello2007 that for Gaussian distributed variables the expected values of the KL distance are independent from the underlying model. This fact allowed us to devise a method to asses the performance of the filtering method in recovering the underlying model without having any knowledge on the model itself.

In this paper we consider filtering procedures based on Random Matrix Theory (RMT), hierarchical clustering and shrinkage and we use the KL distance to evaluate their performance. We consider both artificial and real data samples. Finally we present an extension of the KL distance to an important class on non-Gaussian distribution, specifically the multivariate Student’s t-distribution.

2 Kullback-Leibler distance for Gaussian variables

The KL distance (see for instance Kullback ; Cover ) or mutual entropy is a measure of the distance between two probability densities, say and , which is defined as , where indicates the expectation value with respect to the probability density . The KL distance is asymmetric since the expectation value is evaluated according to the distribution .

Here we consider the KL distance between multivariate probability distributions and we indicate with the dimension of the space spanned by the variables. Let us consider first the case of multivariate Gaussian variables. Without loss of generality we assume that the variables have zero mean and unit variance. In this case, the Gaussian multivariate probability density function is completely defined by the correlation matrix of the system. Given two different probability density functions and , we have

| (1) |

where indicates the determinant of .

From now on we indicate

simply with .

Consider the Pearson sample correlation matrix obtained from the observation of the variables each for records. The sample correlation matrix is different from the true correlation matrix of the system. The Pearson estimator of the correlation matrix has the advantage that sample covariance matrices of finite variance variables belong to the ensemble of Wishart random matrices and many statistical properties of Wishart matrices are known Mardia . Since different realizations of the process give rise to different sample correlation matrices, a KL distance having one or two sample correlation matrices as arguments is a function of one or two random matrices. We investigated the statistical properties of KL distance involving sample correlation matrices of multivariate Gaussian random variables in Ref. Tumminello2007 .

Let and be two sample correlation matrices obtained from two independent realizations of the system both of length . By making use of the theory of Wishart matrices Mardia we obtain Tumminello2007 that

| (2) | |||

| (3) | |||

| (4) |

where

is the usual Gamma function and is the derivative of .

We also obtained Tumminello2007 the asymptotic expectation value of the standard deviation of by using the Bartlett statistics Bartlett54 . Specifically if , and we infer that the standard deviation of is .

The most important property of the expectation values given in Eq.s (2-4) is that they are independent of , i.e. they are independent of the specific true correlation matrix. This fact implies that (i) the KL distance is a good measure of the statistical uncertainty of correlation matrix which is due to the finite length of data series and (ii) the expected value of the KL distance is known also when the underlying model hypothesized to describe the system is unknown.

3 Comparison of filtering procedures

The KL distance can be used to quantify and compare the performance of different filtering procedures of correlation matrices Tumminello2007 . A good filtering procedure should have two important properties: (i) being able to remove the “right” amount of noise from the data in order to recover the signal and (ii) produce filtered matrices which are stable when one makes different observations of the same system. These two requirements are often in competition one with the other. In real cases one does not know the true correlation matrix, therefore it seems impossible to know whether a filtering procedure is removing the right amount of noise. However the above mentioned property of the expected value of the KL distance of being independent from the model correlation matrix can be used to estimate the goodness of the filtering procedure. The proposed procedure to evaluate the performance of a filtering procedure is the following.

Suppose we are given with a data sample and we have our favorite filtering procedure. We propose to generate bootstrap replicas () of the data. We then compute the sample correlation matrix and apply the filtering procedure obtaining the filtered matrix to each replica . In order to measure the stability of the filtering procedure, we consider the average of over the replicas of the quantity . An optimal filtering procedure should be perfectly stable (i.e. ) because from each realization the filtering recovers the model matrix. In order to measure the filtered information we consider the average of over the replicas. This quantity measures the information present in the sample correlation matrix that has been discarded by the filtering procedure. We have seen above that for Gaussian variables the KL distance is different from zero and independent from the model (see Eq. 3). Therefore if our filtering procedure is recovering the true underlying model we should expect that is equal to the right hand side of Eq. 3. We have thus an optimal value for both the stability and the information expected from an optimal filtering and these values are independent from the underlying model. We will represent the result of the analysis with a plane where the axis is related to the stability and the axis is related to the information . In this plane the optimal point, labeled , has coordinate and equal to the right hand side of Eq. 3. A filtering procedure will be considered good if the corresponding point in the stability-information plane is close to .

There are many different filtering procedures. A widespread procedure is based on random matrix theory Metha90 . If the variables are independent and with finite variance then in the limit , with a fixed ratio , the eigenvalues of the Pearson sample correlation matrix is bounded from above by the value where for correlation matrices. In some practical cases, such as for example in finance, one finds that the largest eigenvalue of the empirical correlation matrix is definitely inconsistent with RMT. In these cases, the null hypothesis is modified so that correlations can be explained in terms of a one factor model and Laloux1999 . The filtering procedure considered here works as follows Potters2005 . One diagonalizes the correlation matrix and replaces the all eigenvalues smaller than in the diagonal matrix with their average value. Then one retransforms the modified diagonal matrix in the standard basis obtaining a matrix of elements . Finally, the filtered correlation matrix is the matrix of elements .

In this paper we also consider hierarchical clustering based filtering procedures Anderberg . Hierarchical clustering methods allow to hierarchically organize the elements in a rooted tree or dendrogram. The whole information about the rooted tree can be stored in a matrix that can be considered as the output of the filtering procedure Anderberg . In a recent paper we have shown that this filtered matrix is a proper correlation matrix at least when all of its elements are non negative numbers epl . Here we consider two widespread hierarchical clustering techniques, specifically the Single Linkage Cluster Analysis (SLCA) and the Average Linkage Cluster Analysis (ALCA) Anderberg . For more details about these techniques see Refs Tumminello2007 ; epl . Finally, we also consider a shrinkage filtering procedure haff ; Ledoit03 in which we construct a filtered matrix as

| (5) |

where and is a target matrix. As commonly done in financial literature, we choose the target matrix as a matrix with and for . We estimate the performance of the shrinkage procedure for different values of . It is also interesting to note that there exist analytical methods to obtain the optimal value according to a cost function based on standard quadratic (or Frobenius) norm Schafer . In the figures we also show the point (labeled ) corresponding to the value .

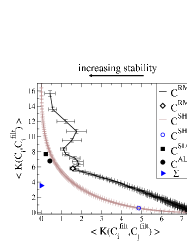

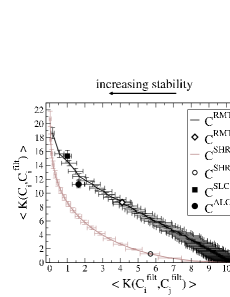

In fig. 1 we show the KL distance in the plane stability-information for these filtering procedures applied to artificial data generated according to two different models. The left panel shows the result for a block diagonal model with blocks, whereas the right panel shows the result for a hierarchical model. This is a Hierarchically Nested Factor Model (HNFM) with factors and it has been introduced in Ref. epl . In both panels we show the points corresponding to the RMT, SLCA, and ALCA filtering procedures. We also show the points corresponding to filtering procedures in which an a priori fixed number of eigenvalues is retained and the remaining ones are set equal to their average. We also show the points corresponding to the shrinkage filtering procedure of Eq. 5 for different values of . As expected when one includes more and more eigenvalues in the filtering procedure the amount of discarded information decreases and the filtered matrix becomes less and less stable. Interestingly in the block diagonal model a clear kink is observed close to the point corresponding to the filtering procedure where eigenvalues are included. The point corresponding to the kink is also the closest to the optimal point and close to the point corresponding to the RMT filtering procedure outlined above. This result shows that for simple block diagonal models RMT and KL procedures gives consistent results. For the hierarchical model we observe no kink when one varies the number of eigenvalues retained by the filtering procedure. This fact indicates that filtering procedures based on spectral analysis may have problems in filtering correlation matrices with a complex structure. Moreover, the number of eigenvalues retained by the RMT filtering procedure is not equal to the number of factors of the HNFM. In the case of the hierarchical model the structure of eigenvalues and eigenvectors is definitely more complicated than the one observed for a block diagonal model. Such a structure is better recovered in the filtering by hierarchical clustering techniques according to the right panel of fig. 1. Finally, the shrinkage method is capable to achieve a very good compromise between stability and information. From this analysis it is possible to extract an optimal value of minimizing the distance from the point labeled with . It should be noted that this value in general does not coincide with the value obtained with the standard method by minimizing the Frobenius norm Schafer .

We now consider an application to a real system. We investigate the daily returns of highly capitalized stocks traded at the NYSE in the period 2001-2003 (). In Fig. 2 we show the performance of different filtering procedures in the plane stability-information. First of all it is worth noting that no kink is observed when one varies the number of eigenvalues retained. This indicates that the block diagonal matrix is far from being a faithful representation of financial correlation matrices. RMT, SLCA and ALCA have different properties in terms of stability and information Tumminello2007 . SLCA is the most stable even if it is the least informative, whereas RMT is the least stable but the most informative. ALCA has intermediate properties both with respect to stability and to information. As for the models the shrinkage seems to outperform the other filtering techniques, even if in this case a quantitative prediction of the optimal value of is more difficult due to the non-Gaussianity of financial returns. This point will be discussed in the next section.

4 A first extension to non-Gaussian variables

The results obtained so far are valid for multivariate Gaussian variables. However in many real systems the random variables of interest are non-Gaussian, and have often the property that the tails of the distribution are significantly fatter than in the Gaussian case. A paradigmatic example is financial price return discussed above. In this section we present some numerical results obtained for a specific class of non-Gaussian variables. A non-Gaussian multivariate distribution useful in describing financial returns is the multivariate Student’s t-distribution Bouchaud .

The multivariate distribution is

| (6) |

The parameter describes the tail behavior of the marginal distribution of any since . A process distributed as Eq. 6 can be obtained by setting , where the s are multivariate Gaussian variables with correlation matrix and is a suitably distributed random variable.

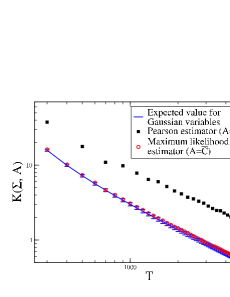

In order to check whether the results on the KL distance for Gaussian distributions described above also hold for Student’s t-distributions we have generated samples of records of a multivariate Student’s t-distribution of variables. The correlation matrix of the underlying Gaussian variables is the HNFM described in Ref. epl and this model is the same as the one used in Ref. Tumminello2007 and in the right panel of Fig. 1. We made this choice in order to have a correlation matrix with a non trivial structure. By using Eq. 1 we then compute the KL distance between the model correlation matrix and a sample correlation matrix obtained with the Pearson estimator. We compare this value with the expected value of of Eq. 2 and we find that these values are significantly different.Specifically, the value of Eq. 1, obtained by using the sample Pearson correlation matrix, is larger than the expected value given by Eq. 2 (see Fig. 3). At first sight this seems to indicate that the results on the KL distance for Gaussian distributions cannot be applied to non-Gaussian variables. However it is known Bouchaud that the Pearson estimator of the correlation matrix is not the maximum likelihood estimator when the variables are non-Gaussian. In the case of the Student’s t-distribution of Eq. 6 there exists a recursive equation for the maximum likelihood estimator which is Bouchaud

| (7) |

Fig. 3 compares the KL distance of Eq. 1 between the model correlation matrix and the two estimators, specifically the Pearson estimator and the maximum likelihood estimator of Eq. 7. The figure shows that, while is not described by Eq. 1, the KL distance using the maximum likelihood estimator is well described by Eq. 1. This result suggests that in some cases one can extend the results obtained for Gaussian variables to non-Gaussian variables provided that the maximum likelihood estimator and not the Pearson estimator is used in the computation of the KL distance. An analytical extension of the KL distance to non-Gaussian distributions is presented in Ref. Biroli of this issue. One of the obtained results confirms the conclusion drawn in this section about the Maximum Likelihood Estimator of Student correlation matrices.

5 Conclusions

We have considered the application of KL distance to the measurement of the performance of correlation matrix filtering procedures in giving reliable and stable estimates of the underlying correlation matrix. Our analysis suggests that the optimal number of eigenvalues to be retained in filtering correlation matrices by mean of spectral procedures is close to the number of eigenvalues indicated by RMT. Our investigation of models also indicates that spectral filtering procedures are slightly more efficient in filtering “separable” systems, like those described by block diagonal models, than hierarchical clustering filtering procedures, whereas the latter work better for systems with a clear hierarchical structure of correlations. We have also shown that the shrinkage approach is very efficient in filtering a sample correlation matrix, although the estimate of the optimal shrinkage intensity in terms of the Frobenius norm is far from being optimal in terms of the KL distance. Finally, we have suggested a possible extension of our method to non-Gaussian variables.

Acknowledgments We thank Jean-Philippe Bouchaud for very useful discussions and for sending us Ref. Biroli before publication. We acknowledge partial support from MIUR research project “Dinamica di altissima frequenza nei mercati finanziari” and NEST-DYSONET 12911 EU project.

References

- (1) O. Alter, P. O. Brown and D. Botstein, Proc. Nat. Acad. Sci. USA 97, 10101 (2000).

- (2) V.M. Eguiluz, et al. Phys. Rev. Lett. 94, 018102 (2005).

- (3) L. Laloux, P. Cizeau, J.-P. Bouchaud, and M. Potters, Phys. Rev. Lett. 83, 1467-1470 (1999).

- (4) V. Plerou, P. Gopikrishnan, B. Rosenow, L. A. N. Amaral, and H. E. Stanley, Phys. Rev. Lett. 83, 1471-1474 (1999).

- (5) R. N. Mantegna, Eur. Phys. J. B 11, 193-197 (1999).

- (6) M. Tumminello, F. Lillo, and R.N. Mantegna, Phys. Rev. E 76 031123 (2007).

- (7) S. Kullback and R. A. Leibler, Ann. Math. Statist. 22, 79-86 (1951).

- (8) T. M. Cover and J. A. Thomas, in Elements of Information Theory (Wiley Interscience, New York, 1991).

- (9) K. V. Mardia, J. T. Kent, and J. M. Bibby in Multivariate Analysis, (Academic Press, San Diego, CA, 1979).

- (10) M. S. Bartlett, J. Roy. Statist. Soc. B, 16, 296-298 (1954).

- (11) M.L. Metha, Random Matrices (Academic Press, New York, 1990).

- (12) M. Potters, J.-P. Bouchaud and L. Laloux, Acta Phys. Pol. B 36 (9), 2767-2784 (2005).

- (13) M. R. Anderberg, in Cluster Analysis for Applications (Academic Press, New York, 1973).

- (14) M. Tumminello, F. Lillo and R. N. Mantegna, Europhys. Lett. 78, 30006 (2007).

- (15) L.R. Haff, Ann. Statist. 8 586 (1980).

- (16) O. Ledoit and M. Wolf, J. Mult. Analysis 88, 365 (2004).

- (17) J. Schäfer and K. Stimmer, Stat. Appl. Gen. Mol. Biol. 4 (2005).

- (18) J.-P. Bouchaud and M. Potters, Theory of Financial Risk and Derivative Pricing, (Cambridge University Press, 2003).

- (19) G. Biroli, J.-P. Bouchaud, and M. Potters, The Student ensemble of correlation matrices: eigenvalue spectrum and Kullback-Leibler entropy, this volume.