Distribution of the time at which the deviation of a Brownian motion is maximum before its first-passage time

Abstract

We calculate analytically the probability density of the time at which a continuous-time Brownian motion (with and without drift) attains its maximum before passing through the origin for the first time. We also compute the joint probability density of the maximum and . In the driftless case, we find that has power-law tails: for large and for small . In presence of a drift towards the origin, decays exponentially for large . The results from numerical simulations are in excellent agreement with our analytical predictions.

Keywords: Brownian motion, first-passage problems, extreme value problems

Introduction

In this paper, we derive the probability distribution of a random variable associated with a Brownian motion, namely the time at which a Brownian motion attains its maximum value before it crosses the origin for the first time. This random variable appears quite naturally in different problems such as in queueing theory and in the evolution of stock prices in finance.

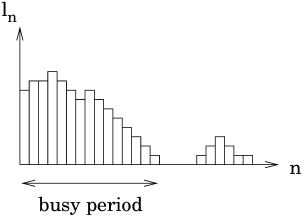

Let us first consider, for example, a single-server discrete-time queueing process, modelled as a simple random walk [1, 2] via:

where is the length of the queue at time and ’s are independent and identically distributed random variables each taking values with probability (signifying the arrival of a new customer), with probability (indicating the departure of an already served customer) or with probability . In the queueing language, this is referred to as the Geo/Geo/1 queue [2].

Given , one calls busy period the period at the end of which the queue becomes empty for the first time (see Fig. 1): during such a period, the server always has some customers to serve. It is then natural to enquire about the time at which the queue is at its longest during the busy period. In the random walk model where the queue length is the position of the walker at time step , this amounts to investigating the time at which the position of the walker (initially positive) is farthest from the origin before it crosses the origin for the first time.

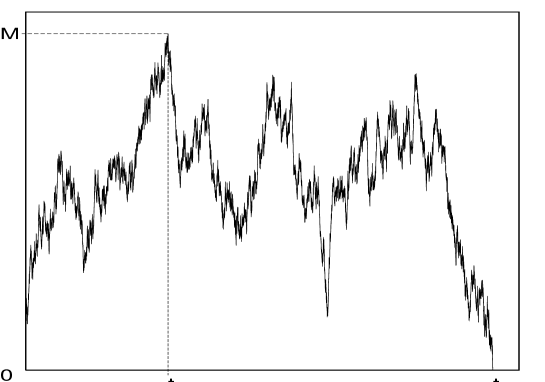

Another area where the same variable appears quite naturally is in the evolution of stock prices in finance. The evolution of a stock price with time is often modelled by the exponential of a random walk [3, 4]. Starting from its initial value the price evolves with time stochastically. A natural question for an agent holding this stock is: what is the suitable time for selling this stock? If the stock price goes below a threshold, say , it is too risky to wait any longer. Thus an agent can wait at most up to the time at which the ratio crosses the level from above. Within this time, the ratio will achieve its maximum at some intermediate time which is clearly the best time to sell the stock. Assuming that the random variable performs a random walk starting from its initial value , one then wants to calculate the probability distribution of the time at which the random walk is farthest from the origin till its first-passage time through the origin, i.e., till the time at which , i.e., indicating the first-passage through the origin.

In this paper, we will consider a further simplified case, namely a continuous-time Brownian motion as opposed to the discrete-time random walk in the above two problems. For a continuous-time Brownian motion we calculate explicitly, using path-integral methods, the probability density of the time at which a Brownian motion (starting from ) is farthest from the origin before it crosses the origin for the first time. Algorithmically speaking, for each sample of the Brownian motion starting at we stop when it crosses the origin for the first time say at time and locate the time at which the Brownian motion achieves its maximum value. Note that both (the first-passage time) and varies from one sample to another. We repeat it many times and then construct a histogram of the ’s which gives its probability density function . Even though the discrete-time problem is more relevant, we expect the continuous-time result to provide the right asymptotics for the discrete problem. As we will see below, the continuous-time problem, though still non-trivial, is easier to handle analytically.

Note that for a Brownian motion or a Brownian bridge over a fixed time interval , the probability density of the time at which the process attains its maximum is well known [5]. For example, for a zero-drift Brownian motion over starting at the origin, the probability density where for [5]. On the other hand, for a Brownian bridge over the fixed interval and starting at the origin, the probability density of is uniform, for [5]. In contrast, in our case, the Brownian motion is not over a fixed time interval, but rather over a variable time interval where the upper edge is the first-passage time which itself is a random variable [6] and hence varies from sample to sample.

The statistical properties of the functionals (such as the area, the maximum etc.) of a Brownian motion or its variants (such as a bridge, excursion, meander etc.) over a fixed time interval have many applications in physics, graph theory, computer science and they have been studied extensively (for recent reviews on Brownian functionals see [7, 8]). In particular, the area under a Brownian excursion or meander has found many recent applications in problems as diverse as fluctuating interfaces [9], graph enumeration [10], lengths of internal paths in rooted planar trees [8, 11] or cost functions in data storage via the “linear probing with hashing” algorithm [8, 12]. Similarly, the statistical properties of functionals of Brownian motion restricted up to its first-passage time (usually referred to as ‘first-passage functionals’) also have various applications, and have appeared recently in many different contexts [1, 15, 16], including the computation of the time period of oscillation of an undamped particle in a random potential [14] and the determination of the distribution of the lifetime of a comet in the solar system [8, 13]. The probability density of the area swept by an initially positive Brownian motion till its first-passage time was computed exactly in [15], with an application to queuing theory. In this paper, our focus is on the random variable which, though not quite a functional in the strict sense, is an important random variable associated with such a Brownian motion restricted up to its first-passage time.

In [15], the authors also computed directly the probability density of the maximum of a Brownian motion (starting at ) before its first-passage time through the origin, via a “backward” Fokker-Planck method and showed that it has a power law behavior where . In this paper, we extend this work using a path decomposition method that allows us to obtain the joint probability density of the maximum and the time at which the maximum occurs before the first-passage time. By integrating over , we then get the ‘marginal’ , i.e. the probability density of . We calculate explicitly both for a driftless and drifted Brownian motion. We also compare the results of numerical simulations to our analytical predictions and find excellent agreement.

1 Driftless Case

We consider a continuous-time Brownian motion evolving via , where is a white noise with and . We start by recalling the quick derivation of given in [15]:

Let be the probability that a Brownian particle starting from exits the interval for the first time through , i.e., the probability that the maximum before the first-passage time is less than or equal to . Writing for the distribution function of a Brownian displacement in the time interval , we have:

| (1) |

Expanding for small values of , and using the fact that in the absence of drift the mean value of is , one finds that satisfies:

| (2) |

whose solution is:

| (3) |

As mentioned in its definition, it can easily be seen that also corresponds to the probability that the maximum before the first-passage time is less than or equal to ; therefore, differentiating Eq. 3 with respect to gives the probability density of :

| (4) |

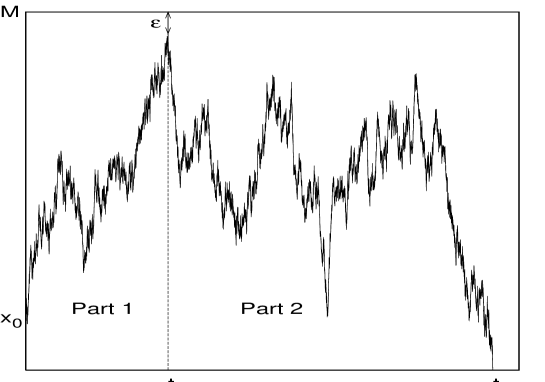

To compute the joint probability density we proceed as follows. We first assume that the maximum occurs at and then we split the Brownian path into two parts (before/after , as shown in Fig. 3) and determine the weights of a path’s left-hand side and right-hand side separately. Note that due to the Markovian property of the Brownain path, once the position of the walker is specified at , the weights of the left and the right parts become completely independent and the total weight is just proportional to the product of the weights of the two separate parts. For the left part, we have a process that propagates from at to at without crossing the level in (since is the maximum) and the level (the origin). For the right part, the process propagates from the value at to at where without crossing the level and the level in between. We need to be careful, however, because, as pointed out in [9], a Brownian walker that crosses a given level once crosses it infinitely many times immediately after the first crossing. It is therefore impossible to enforce the constraint and simultaneously forcing the motion to stay below before or after (for a lattice walk, one does not have this problem since the lattice constant provides a natural cut-off). Following the method used in [9], we introduce a cut-off by imposing and consider all paths having a maximum less than or equal to and passing through at . We compute their weight and then let go to eventually.

On the right side of : we have to determine the weight of a path that starts at and exits for the first time the interval through . This is given by Eq. 3:

| (5) |

On the left side of : we use a path integral treatment with the Feynman-Kac formula (as in [9]) giving the weight of a path in terms of the propagator , where with a square well having infinite barriers at and and for (the infinite barriers at , enforce the condition that the path can penetrate neither at nor at ). The normalized eigenfunctions of labelled by the integer are with the associated eigenvalues . The eigenfunction vanishes at both ends and of the box. The propagator can be easily evaluated in this eigenbasis, and one gets:

| (6) |

In the limit when , we get to leading order

| (7) |

Taking the product of Eqs. 5 and 7, we get the total weight of the path, to leading order in small ,

| (8) |

The proportionality constant is set by using the normalization constant:

It is easy to show that the proportionality constant . Thus, in the limit , we finally obtain

| (9) |

As a first check, let us show that , thus recovering the marginal of the maximum in Eq. 4. Integrating over , we get

| (10) |

where the last identity can be found (and derived easily) in [17].

Finally, from Eq. 9 an integration over (note that varies from to ) yields the desired marginal :

| (11) | |||||

The sum in Eq. 11 can be expressed in terms of a known special function and we get

| (12) |

where is the fourth of Jacobi’s Theta functions ([19]). Subsequently one can obtain the large and small asymptotics of from the exact expression in Eq. 12.

Large- asymptote:

We first consider the case when . Changing variables in Eq. 11 through and letting gives for :

| (13) |

Small- asymptote:

In the opposite limit , we start from Eq. 9 and first take a Laplace transform:

where the sum of the series can be found in [17]. Letting become much larger than and , we obtain:

which, after the Laplace inversion ([18]) yields:

| (14) |

Integrating over gives for :

| (15) |

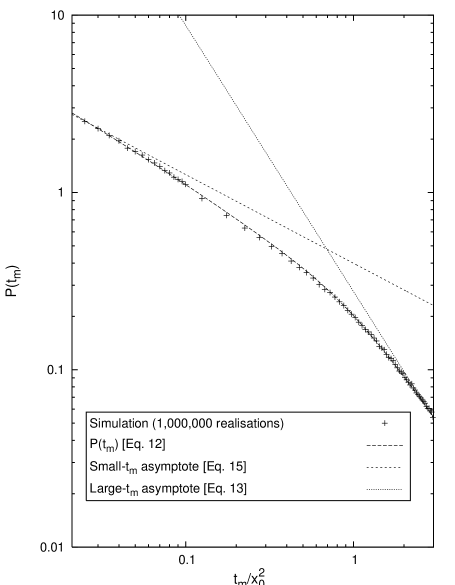

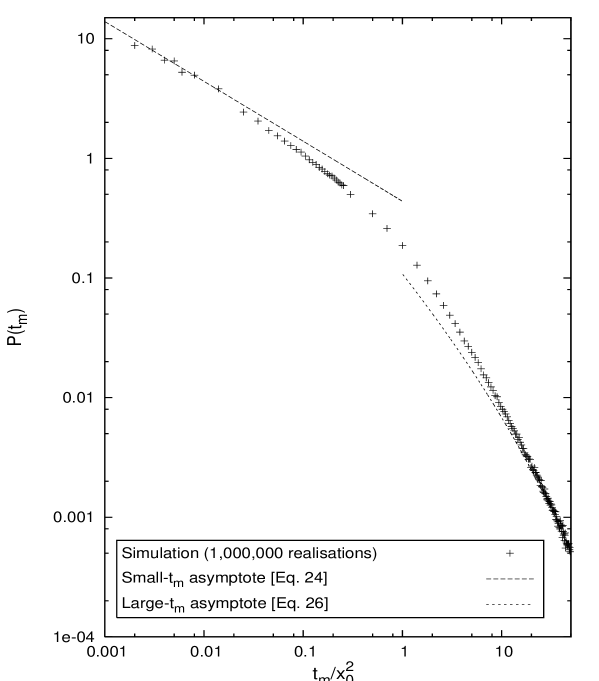

Thus, has power law behavior at both large and small tails. For large , the probability density falls off as , whereas for small it diverges as . The exact analytical form of and its asymptotes from Eqs. 12, 13, 15 are plotted (using Mathematica) in Fig. 4 together with the points obtained from the numerical simulation (with 1,000,000 realisations). They are in good agreement with each other.

2 In the Presence of a Negative Drift

We now consider a Brownian motion in the presence of a drift . For , it is clear that the walker will excape to with a nonzero probability. This means that with a finite probability . Therefore this case is not much of interest in the present context. Instead, we focus here on the opposite case where the drift is towards the origin, i.e., . The Langevin equation describing the motion becomes:

where is the Gaussian white noise with and . We use the same strategy as in the driftless case, i.e., splitting the motion into two independant parts (before and after ) and introducing a small cut-off .

On the right-hand side: Letting, as in the driftless case, be the probability that a Brownian particle starting from exits the interval for the first time through , we have as before:

| (16) |

In the presence of a drift, the mean value of is no longer and one can easily show that the analogue of Eq. 2 now reads:

| (17) |

The solution is:

| (18) |

and so we have:

| (19) |

As in the driftless case, the probability density of can be obtained by differentiation of Eq. 18 with respect to , as was done in [15]:

| (20) |

where we have added the subscript “d” to indicate that the density corresponds to the drifted case.

On the left-hand side: We use the same path integral method as in the driftless case. The weight of a path is now proportional to:

| (21) |

The position of the Brownian particle at and is known, so we can substitute for in the first exponential factor on the right-hand side of Eq. 21.

The propagator for the drifted case will therefore be equal to that for the driftless case (given in Eq. 6) multiplied by the factor , and will be given by:

| (22) |

As in the driftless case, we multiply the weights of the left and right side of derived above (Eqs. 19 and 22), and take the limit to obtain:

| (23) |

where is the joint density for the driftless case given in Eq. (9). Once again, by integrating over , one can recover the marginal probability density of the maximum derived originally in [15]. On the other hand, integrating over gives the marginal . We were not able to derive a compact expression for as in the driftless case, though the asymptotes of can be derived explicitly as shown below.

Small- asymptote:

Large- asymptote:

To study the behaviour of when , we start from the following expression for :

| (25) |

The series in Eq. 25 is dominated by the first term () for large . Hence, retaining only the term and making a change of variable in the integral, we get:

For large , the most important contribution to the integral comes from the small regime. Expanding the and functions and keeping only the leading order term reduces the integral to:

Letting , we next use the saddle point method to obtain the leading term via minimizing the function and get:

| (26) |

Thus, as expected, the density has an exponential decay for large in presence of a negative drift. Figure 5 shows a plot of the asymptotes (Eq. 24 and 26) together with the data from numerical simulation (1,000,000 realisations with ).

3 Summary and Conclusion

In summary, we have obtained an exact expression for the probability density of the time at which a Brownian motion attains its maximum before passing through the origin for the first time, and studied the tails of this probability density both for the driftless and for the drifted Brownian motion. This was done by first computing the joint distribution of the maximum attained and the time at which it is attained. In the context of the queuing theory, the result that decreases monotically with increasing suggests that the beginning of a busy period is more likely to be the time at which a queue is at its longest.

It would be interesting to derive the explicit results, obtained here by the path integral method, from the general theory of filtrations in Brownian motion developed recently in [20, 21].

It would also be of interest to extend this calculation to the discrete-time random walk case which remains a real challenge.

References

References

- [1] Kearney M J 2004,J. Phys. A. Math. Gen. 37, 8421.

- [2] Asmussen S 2003, Applied Probability and Queues 2nd edn (New York: Springer).

- [3] Williams R J 2006, Introduction to the Mathematics of Finance (AMS).

- [4] Yor M 2000, Exponential Functionals of Brownian Motion and Related Topics (Berlin: Springer); see also Comtet A, Monthus C and Yor M 1998, J. Appl. Prob. 35, 255.

- [5] Feller W 1968, An Introduction to Probability Theory and its Applications (New York: Wiley).

- [6] Redner S 2001, A Guide to First-Passage Processes (Cambridge: Cambridge University Press).

- [7] Comtet A, Desbois J and Texier C 2005,J. Phys. A. Math. Gen. 38, R341.

- [8] For a short review on Brownian functionals and their applications see Majumdar S N 2005, Current Science, 89, 2075; also available at http://xxx.arXiv.org/cond-mat/0510064.

- [9] Majumdar S N and Comtet A 2005,J. Stat. Phys. 119, 777; 2004 Phys. Rev. Lett. 92, 225501.

- [10] For an extensive review on the area under Brownian motion and its variants, see Janson S 2007, Prob. Surveys 4, 80.

- [11] Takács L 1991, Adv. Appl. Prob. 23, 557; 1995, J. Appl. Prob. 32, 375.

- [12] Flajolet P, Poblete P and Viola A 1998, Algorithmica 22, 490.

- [13] Hammersley J M 1961, Proc. 4th Berkeley Symp. on Math. Stat. and Prob. vol. 3 (Berkeley: Univ. Cal. Press), pp. 17.

- [14] Dean D S and Majumdar S N 2001, J. Phys. A. Math. Gen. 34, L697.

- [15] Kearney M J and Majumdar S N 2005, J. Phys. A: Math. Gen. 38, 4097.

- [16] Kearney M J, Majumdar S N and Martin R.J. 2007, arXiv:0706.2038.

- [17] Gradshteyn I S and Ryzhik I M 2000, Table of Integrals, Series and Products 6th edn., (New York: Academic Press).

- [18] Bateman H 1954, Tables of Integral Transforms (McGraw-Hill).

- [19] Abramowitz M and Stegun I A 1973, Handbook of Mathematical Functions (Dover).

- [20] Mansuy R and Yor M 2006, Lecture Notes in Mathematics 1873 (Berlin: Springer Verlag).

- [21] Nikeghbali A and Yor M 2006, Ill. J. Math. 50, 791.