USLV: Unspanned Stochastic Local Volatility Model ††thanks: Opinions expressed in this paper are those of the authors, and do not necessarily reflect the view of JPMorgan Chase and Numerix.

Abstract

We propose a new framework for modeling stochastic local volatility, with potential applications to modeling derivatives on interest rates, commodities, credit, equity, FX etc., as well as hybrid derivatives. Our model extends the linearity-generating unspanned volatility term structure model by Carr et al. (2011) by adding a local volatility layer to it. We outline efficient numerical schemes for pricing derivatives in this framework for a particular four-factor specification (two “curve” factors plus two “volatility” factors). We show that the dynamics of such a system can be approximated by a Markov chain on a two-dimensional space , where coordinates and are given by direct (Kroneker) products of values of pairs of curve and volatility factors, respectively. The resulting Markov chain dynamics on such partly “folded” state space enables fast pricing by the standard backward induction. Using a nonparametric specification of the Markov chain generator, one can accurately match arbitrary sets of vanilla option quotes with different strikes and maturities. Furthermore, we consider an alternative formulation of the model in terms of an implied time change process. The latter is specified nonparametrically, again enabling accurate calibration to arbitrary sets of vanilla option quotes.

1 Introduction

1.1 Motivation

The present work is motivated by the desire to have a unified modeling methodology and shared implementation for derivatives pricing with a dynamic volatility smile for various asset classes, including interest rates (IR), commodities, equities, credit, foreign exchange (FX) etc., as well as for modeling hybrid derivatives such as equity-IR or equity-commodities hybrids. We present one possible approach, which extends a recently proposed class of stochastic volatility models.

1.2 Related Previous Work

Gabaix, (2007) proposed a new class of asset price models, the so-called linearity-generating processes (LGP). Such processes are defined by the condition that the current prices of basic instruments (stock, bonds, futures, swaps etc.) are linear in a driving Markov process . This stands in sharp contrast to popular affine models where, e.g., a zero-coupon bond price is an exponentially-affine function of a Markov driver .

On the theoretical side, the LGP processes appear very attractive. Indeed, typical ways we model basic instruments are drastically different between, say, IR and equity models111Both are taken to be examples of term-structure models vs. spot-models. Instead of IR and equity, we could, e.g. compare commodities and FX.. In the equity world, basic instruments (equities) are linear in stochastic factors (usually taken to be equity prices themselves for purposes of modeling derivatives), and volatility is stochastic (SV) and unspanned (USV, see below for the definition of this term).

In the IR world, the mathematics are almost the same for the HJM-type models that model the entire yield curve. As the yield curve is in one-to-one correspondence with bond prices, it can be viewed as an “observable” basic instrument that again is linear in factors, and typically gives rise to USV.

But such linearity of HJM-like models has a high price, namely that the number of state variables needed for the Markovian dynamics turns out to be too high for use in a lattice-based setting in most cases of practical interest. Therefore, even with Markovian specifications, HJM-like models are typically employed within a Monte Carlo setup rather than on a lattice. On the other hand, an attempt to reduce the curve modeling to a short-rate modeling, as is done in affine models, leads to a nonlinear relation between bond prices and the factors, which produces undesirable side effects, such as a dependence of the instantaneous forward curve on the short-rate volatility.222This is the cost one has to pay for non-linearity. Clearly, nothing similar ever occurs in spot models: today’s stock price is obviously independent of the current volatility or current value of the volatility factor . Mathematically, this can be formulated as the statement that for spot stochastic volatility models (such as e.g. the Heston model), the pricing function of basic instruments (stocks) is an identity , see also Table 1 in Sect. 2.

This problem is resolved in the LGP approach. By putting both equity and bonds on equal footing in terms of making them both linear functionals of the factors (and doing it in a different way from HJM), the LGP-based models play a role of “grand unification models,” similar in a conceptual sense to “grand unification theories” (GUT) in physics. No proliferation of the number of Markov drivers occurs in LGP-type models as we move from one class of basic instruments (stocks) to other class (bonds).

Also on the practical side, linearity has profound consequences for tractability of asset pricing modeling within the LGP framework. In particular, if a zero-coupon bond price is linear in , then so will be prices of a coupon bond or a swap. As a result, the swaption pricing, e.g. can be done in a semi-analytical form without additional approximations, such as those used by the Libor Market Models (LMM). It is also very helpful in calibration, as will be discussed in more detail below.

To summarize, the class of LGP-like models identified by Gabaix is a new interesting class that may develop into a viable competitor to both affine models, which are currently one of the main workhorses for derivatives modeling in credit, commodities, rates and other asset classes, and also HJM-type models. Yet this approach is in its infancy compared to the well-studied class of affine models.

In 2011, Carr, Gabaix and Wu (CGW) proposed a LGP-type stochastic volatility term structure model (Carr et al., (2011)). CGW, in particular, emphasize the point that stochastic volatility generated in LGP-type models is unspanned in the sense of the definition of Colin-Dufresne & Goldstein, (2002), who coined the original term “unspanned volatility”333Following Colin-Dufresne & Goldstein, (2002), the volatility is called unspanned if bond prices do not depend on the stochastic volatility driver.. The CGW model offers a number of attractive features. Most importantly, it is a low-dimension Markov model with unspanned stochastic volatility (USV), and an orthogonal set of model parameters with a separate calibration to the term structure and option volatilities.

The CGW model is a pure stochastic volatility model, as volatility is modeled as a superposition of CIR processes. To make it more practical, it would be very useful to add a local volatility layer to the model. Our extension of the CGW model amounts to introduction of such a local volatility factor, along with efficient numerical methods for calibration and pricing. To differentiate our framework from CGW, in what follows we will refer to it as the unspanned stochastic local volatility (USLV) model.

2 Overview of Our Framework

By construction, USLV preserves the linearity and USV properties of the CGW approach. Another property inherited from the CGW model is that USLV is formulated directly in the physical measure (see below) rather than in the risk-neutral measure , which makes it easier, e.g., to combine the historical and pricing data for model estimation, if desired.

The main theoretical construction that USLV adds to the CGW model is a local volatility layer. The resulting mixed stochastic/local volatility dynamics has a few important implications.

First, adding a local volatility layer enables nearly perfect matching of an arbitrary number of European vanilla option quotes with different strikes and maturities.444Note that while this property of USLV is shared by local stochastic volatility models as well, the key point here is that now we have an additional risk factor (volatility) to acknowledge, model and hedge. Such an extension is clearly desirable in order to apply this approach for pricing of both vanilla and exotic derivatives, especially if vanilla options are used to hedge the exotics.

Second, the presence of a local volatility layer alongside a stochastic volatility part induces a decomposition of the option volatility into spanned and unspanned parts, rather than being of a pure unspanned type as in the CGW model. One could expect that such decomposition of volatility should translate into a decomposition of an option’s vega into a delta-vega and a “genuine vega” part.

Because of the way our model is calibrated, it enables traders to incorporate their view on the relative weights of the spanned and unspanned parts in the option’s vegas.555Technically, this is done by giving the end user the ability to input his/her own set of speed factors (SF), see below. By viewing a trader’s inputs as a prior model that does not necessarily match observed options, our model finds a minimal adjustment (“tweak”) to the trader’s prior model in order to reinforce an accurate match of the option quotes.

In contrast, the volatility in local volatility models would be 100% spanned. In local volatility models, matching vanilla pricing would fix the volatility surface for all strikes and maturities, and would not leave any flexibility for the model to match prices of more exotic options. The inclusion of stochastic volatility allows one to simultaneously have more realistic forward smile dynamics and additional parameters to match exotics’ prices (if available). The ability of USLV to incorporate a possible trader’s view is what sets it apart from both pure local volatility models and pure SV models of the CGW type.

On the implementation side, USLV concentrates on the most important low-dimensional specifications for practicality, e.g., two factors for the term structure (with curve factors in general), and one or two factors for stochastic volatility (with volatility factors in general). In particular, for a (2+2)-factor case, we show how to approximate the dynamics of the driving factors by a two-dimensional Markov chain on a space constructed by folding (see below) of the original four-dimensional state space. This enables fast pricing by standard backward induction on the chain.

It should be noted that while in this paper we concentrate on modeling term-structure dynamics (e.g., of futures, swap rates or credit spreads) with potential applications to “term structure asset classes,” such as IR, commodities or credit, the same approach can be used for modeling spot prices, which would be a proper setting for “spot asset classes,” such as equities or FX. Moreover, due to a symmetric treatment of “term-structure assets” and “spot assets” in the present framework, this approach is readily available for modeling hybrid derivative products (e.g., equity-IR or equity-commodity hybrids) using the same implementation. Changes from one asset class to another would amount to a proper reparametrization and reinterpretation of the Markov generator matrices while leaving the computational algorithm intact.666In principle, this could produce a generic pricing engine, similar in a sense to Monte Carlo (MC). Indeed, the latter method is a “universal” method of derivatives pricing in the sense that in this framework, we only need to implement dynamic equations and payoff functions for a particular model-product combination in order to use a generic MC engine. Likewise, our Markov chain framework is “universal” in the same sense (within a class of all diffusive local stochastic volatility models in up to (2+2) dimensions). The only difference here is that while in MC we typically start with continuous space dynamics, which is then discretized for simulation through discretization of processes (e.g., Brownian motions) driving the dynamics, the dynamics in our approach are fundamentally defined in terms of discretized state variables. Furthermore, in the continuous limit, different parametrizations of the stochastic volatility generator in our Markov chain model give rise to a rich class of (2+2)-factor models, including stochastic local volatility with jumps. Note that in this paper we primarily concentrate on specifications whose continuous limit is a two-dimensional diffusion with a two-dimensional diffusive stochastic local volatility. This case is covered in detail below in Sect. 6. However, in Sect. 7, we will present an alternative formulation that can give rise to jumps in both the underlying and stochastic volatility. Our approach is thus quite flexible in its ability to accommodate different specifications of the dynamics, including a four-factor stochastic local volatility model with jumps.

2.1 USLV vs. HJM vs. Affine Models

Our initial interest in using LGP-type models for modeling stochastic volatility was inspired by the observation that LGP-type models (and, by extension, USLV-like models) seem to combine the best features of both HJM-type models and affine models, while avoiding their disadvantages. Indeed, like the HJM-type models, the stochastic volatility is unspanned in USLV. Unlike the HJM-types, the model is Markov in dimension rather than , as in HJM-type models. Conversely, both affine models and USLV have the same number of state variables (). However, in USLV, volatility is always (partly) unspanned, while in affine models, volatility in general will be spanned unless some special constraints are imposed on parameters, which might be restrictive for calibration purposes. (See also Table 1 below.)

The above reasoning suggests that if we manage to generalize the pure stochastic volatility model of CGW to a stochastic local volatility model (i.e., to make a USLV out of CGW), and do it in a numerically efficient way, and if the resulting model demonstrates good parameters and hedges stability etc., then such a model can be considered a viable candidate for use in practice. This paper outlines the theoretical framework for USLV, leaving numerical experiments for future work.

A few more words of caution are in order here. Our outline of the USLV is generic and is not tied yet to any specific asset class. Each asset class makes its own demands on a model. For example, the ability to reproduce the Samuelson effect and asset cointegration are very important for commodities, alongside the ability to handle seasonality in asset levels and volatilities for certain commodities, such as gas or power. It has yet to be seen how (or whether) the USLV framework can accommodate such specific requirements. A discussion of this matter is planned for the second stage of the present theoretical work.

A brief summary of different model classes is presented in Table 1, where we compare the behavior of equity stochastic volatility models such as the Heston model, HJM-type, affine-type and LGP/CGW/USLV-type. The third column shows the functional form of conditional expectations arising in calculation of prices of elementary instruments.

| Model | USV | D | |||

| Equity | Yes | ||||

| IR HJM | Yes | ||||

| IR Affine | No | ||||

| CGW/USLV | Yes |

3 The Carr-Gabaix-Wu Model

In this section, we provide a brief overview of the CGW model of Carr et al., (2011). The CWG model is then used as the first step in our setting. Simultaneously, in this section we set our notation, on which we largely follow Carr et al., (2011).

3.1 State-Price Processes and Martingale Pricing

The famous fundamental theorem of asset pricing (Harrison & Pliska, (1981)) states that if the economy is arbitrage free, then there exists (under certain technical conditions such as positivity and time consistence) a strictly positive process called the state space deflator, such that the deflated gain process associated with any admissible trading strategy is a martingale under the measure . In particular, for a contingent payoff at time , its value at time is given by the following -conditional expectation:

| (1) |

The ratio is sometimes referred to as the stochastic discount factor or the pricing kernel. The -measure SDE for reads

where is a vector of risk factors and measures the market prices of risk for these factors. The formal solution to this SDE takes a multiplicative form

where stands for the stochastic exponential martingale operator. The latter defines the Radon-Nikodým derivative that transforms the physical measure to the risk-neutral measure such that, under , the contingent claim valuation reads

| (2) |

3.2 One-Factor Case

Our starting point is a version of one-factor LGP dynamics suggested in Bekker & Bouwman, (2009). It differs from Carr et al., (2011) by i) parametrization, and ii) derivation and interpretation of the main result of the LGP approach (see Eq.(9) below). The two formulations can, however, be mapped onto one another by a proper re-parametrization.

Assume that a state variable is driven by the following SDE under measure :

| (3) |

where is the standard Brownian motion and the short rate is an affine function of :

| (4) |

where is a detrended state variable with being the growth rate of , and and are two constants777Note that we can set without any loss of generality. However, we prefer to keep it in the formulae for correct dimensionality, i.e. has the dimensionality of divided by that of ..

The -measure SDE for the state price deflator reads

| (5) |

The representation of stochastic dynamics given in Eq.(3) and Eq.(5) is convenient as both the real world (measure ) and risk-neutral (measure ) dynamics can be directly read from these equations provided we know functions and . Indeed, by the Girsanov theorem, the combination is a -martingale, so that the -measure drift of is the short rate . This means that the state variable can be interpreted economically as a risky (tradable or non-tradable) asset, or be related to aggregate market returns, see Bekker & Bouwman, (2009).

Using Eq.(5) and the fact that is a martingale under measure (which is easy to verify using Itó’s lemma and Eq.(3) and Eq.(5)), we compute the conditional time- expectation of as follows888All conditional expectations in this paper refer to measure unless specifically stated otherwise.:

This produces the following result for the time- zero-coupon bond price

| (7) |

Differentiating this relation with respect to , we transform it into a differential equation:

| (8) |

whose solution reads (Bekker & Bouwman, (2009))

| (9) |

Note that this expression does not depend on specification of functions and in Eq.(3), and the shape of the yield curve at time is driven by the current value of . This is different from affine models where the bond price is represented as a conditional expectation of a non-linear functional of future values of the state variables.

The solution of Eq.(3) in the zero volatility limit reads

| (12) |

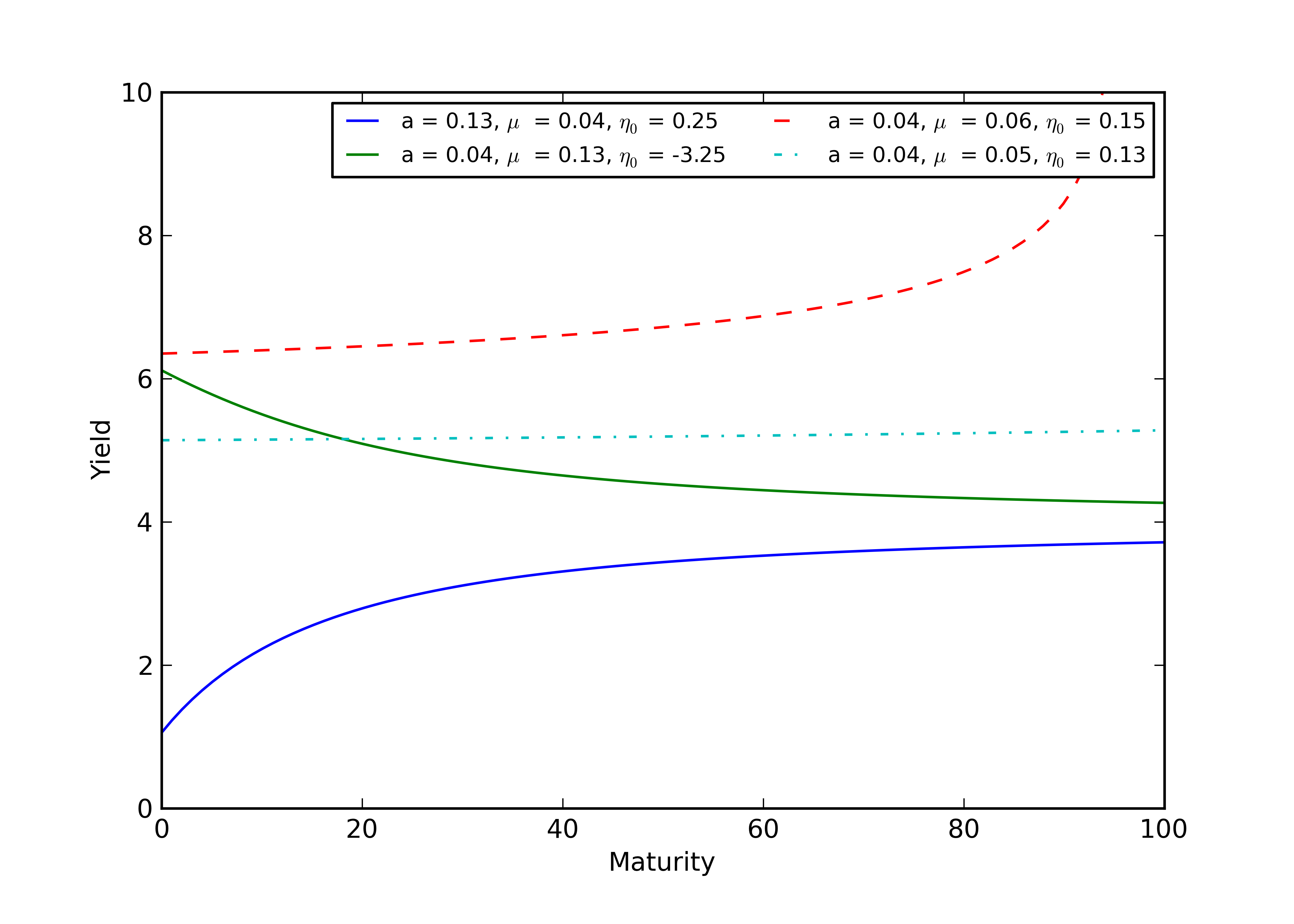

In what follows, we concentrate on the case which corresponds to the scenario where the detrended asset reaches a constant level as . In addition, we assume that , so that which produces an increasing and concave yield curve, while negative values of produce inverted yield curves, see Fig. 1.

In this scenario, the short rate approaches as . If satisfies a more restrictive constraint , then the short rate stays positive (or equivalently ) for all . Therefore, we assume a slightly more general constraint on by introducing another parameter that lies in the interval :

| (13) |

For such choice of , Eq.(12) with produces a concave and monotonically increasing yield curve, while the short rate and state process are bounded at all times as follows:

| (14) |

where the low and upper boundaries for (respectively, upper and lower boundaries for ) are attained by setting or , respectively. One sees that parameter can be used to control how much the short rate can go negative. If we set , the short rate is non-negative at all times , but as we will see shortly such choice for may not necessarily be optimal in the present framework.

Now we return to Eq.(3) with non-vanishing volatility, and consider the following ansatz for :

| (15) |

which is obtained by replacing a constant in Eq.(12) by a stochastic process restricted to the strip . Such a process with a given initial value can be constructed as follows:

| (16) |

where is a non-negative martingale under measure that starts at and satisfies the following SDE:

| (17) |

where is a local volatility function that will be specified later. The initial value is expressed in terms of as follows:

| (18) |

Substituting Eq.(16) into Eq.(15), we obtain

| (19) |

where

| (20) |

Eq.(19) defines as a fractional-linear function999This function is also known as a Möbius transformation in complex analysis. of the martingale process determined by Eq.(17). Clearly, the process defined by Eq.(19) is bounded, as it should be as long as it is related by a linear equation Eq.(9) to the bond price which is bounded101010One can notice here a certain conceptual similarity between the LGP and Markov functional models on the one hand, and a difference with the affine models on the other hand. For the latter, the driving SDE has affine drift and diffusion coefficients, while the function (see Table 1) is nonlinear (nonaffine). For the LGP-type models, e.g. the CGW model, the situation is reversed: the state equation is now nonaffine but the pricing equation is affine.. By taking the limits and , one obtains bounds for :

| (21) |

which coincides with Eq.(14). Note that Carr et al., (2011) obtain a fractional-linear expression for as a function of that is similar to our Eq.(19), however their choice of time-dependent coefficients is different.

Using Ito’s lemma, we find that defined by Eq.(19) satisfies Eq.(3) provided we choose the following specification for functions and (which we express here as functions of rather than ):

| (22) |

Note that volatility vanishes in both limits or which correspond to boundaries in the -space given by Eq.(21). Finally, the solution of Eq.(5) reads

| (23) |

where we normalize to enforce the constraint . Therefore, the state price deflator is a linear functional of the Markov driver . Linearity of this expression is exactly the reason we do not have any convexity corrections in Eq.(9). For any nonlinear functional a resulting expression for would depend on volatility of . Such behavior is intentionally avoided in the present framework. Further note that using Eq.(23), Eq.(19) can be re-written as follows:

| (24) |

Therefore, for contingent payoffs that are linear in , the conditional expectation in Eq.(1) reduces to the expectation of a linear functional of 111111In addition, Eq.(24) shows self-consistency of our approach: while we know from Eq.(3) and Eq.(5) that the product is a martingale, Eq.(24) shows that this product is proportional to an affine function of a martingale , which is a martingale.. This property of the model can be used, in particular, in order to reduce the swaption pricing to a single option on a future value , see Carr et al., (2011) for more details.

Note that as , the detrended process with defined by Eq.(19) converges to the following equilibrium value:

| (25) |

irrespective of the behavior of the process . In other words, stochasticity dies off in the one-factor LGP model, while the onset of this asymptotic regime is attained at times where approaches unity:

| (26) |

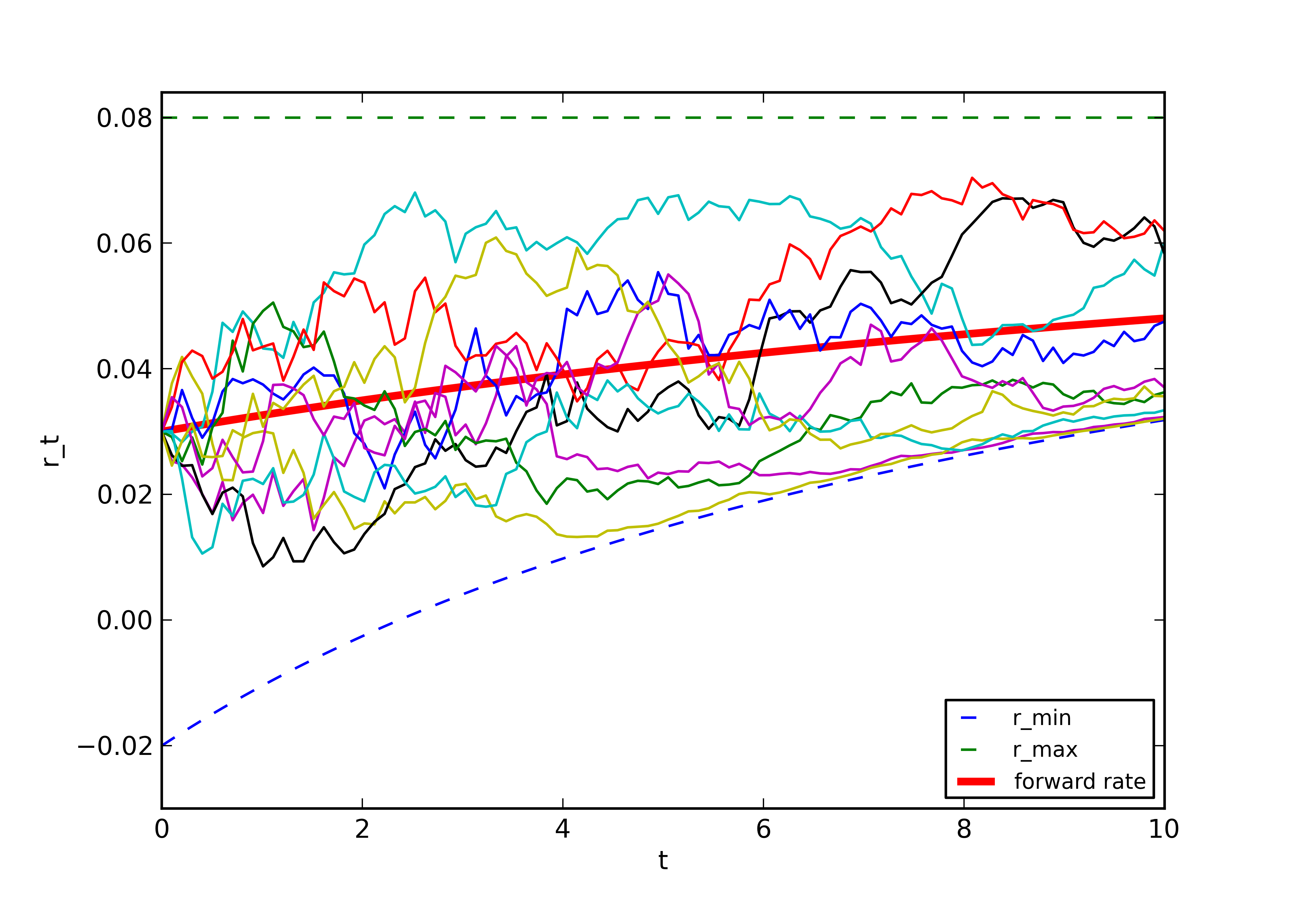

The resulting asymptotic extinction of volatility of the process as appears to be a theoretical limitation of a one-factor LGP framework. This behavior is illustrated in Fig. 2 where we show a few paths of a simulated short rate process. As will be shown in the next section, a two-factor formulation allows one to build dynamics where stochasticity does not die off as . Another limitation of the one-factor formulation is that it is only able to produce monotonic (increasing or decreasing) yield curves. In order to get a humped-shaped yield curve, one needs at least a two factor specification.

On the practical side, the effect of decaying stochasticity of in the one-factor formulation can be somewhat mitigated by a suitable choice of parameters. In particular, if the yield curve is not too steep, by taking , we can admit some negative short rates in the short term while guaranteeing that stays positive for longer maturities, as shown in Fig. 2 where can go negative for years. Such simple trick allows one to somewhat delay shrinkage of the support region of for larger time horizons. Therefore, we expect that the one-factor version of the model can still be used for monotonic yield curves with sufficiently short time horizons.

3.3 Extension to a Multi-Factor Case

The previous formulation treats a one-factor case . For an arbitrary number of factors , the state vector satisfies the following equation:

| (27) |

where is a -dimensional standard Brownian motion and the short rate is an affine function of :

| (28) |

where are detrended state variables with being the corresponding growth rates, and and are non-negative constants. The -measure SDE for the state price deflator reads

| (29) |

The solution to this equation generalizes Eq.(23):

| (30) |

where parameters and functions with are defined similarly to Eq.(20). Finally, the solution for the bond price in a -factor model generalizes Eq.(9) (Bekker & Bouwman, (2009)):

| (31) |

where . As can be seen from Eq.(31), only the factor with the smallest value of contributes to this expression in the limit . In our analysis below we set and assume that . Therefore, we interpret the second factor as a long term factor, while serves as a short-term factor that drives, jointly with , the short-term part of the yield curve. A two-factor specification gives rise to a richer set of yield curves than a one-factor one, including, in particular, humped curves or curves with sign-changing convexity which could not be obtained with a one-factor specification.

Another key difference of a multi-factor case from a one-factor one is that volatility does not necessarily die off in the long run. We can illustrate this for . Proceeding similarly to the one-factor case, we first solve the system Eq.(27) without noise, by setting . We obtain

| (32) |

where and are two constants that are determined by initial conditions. In what follows, we assume that and , as suggested by a numerical example below. For such a scenario, the following constraints on parameters and :

| (33) |

guarantee that Eq.(3.3) is well defined at all times. Additional constraints on parameters and arise if we enforce positivity of the short rate . We will omit details that can be reproduced using similar steps to the above one-factor case, and instead concentrate on showing that volatility in a two-factor (or, more generally, a multi-factor) LGP-type model does not in general die off in the long term.

To this end, we note that a solution of a full model with non-vanishing volatility can be obtained along similar lines to the previous case. More specifically, we should replace constants and in the deterministic solution Eq.(3.3) by judiciously chosen fractional-linear functions of a two-dimensional martingale process . The latter satisfies a two-factor generalization of Eq.(17), and has the initial value . On the other hand, assuming that and , the asymptotic behavior of the deterministic solution Eq.(3.3) as is as follows:

| (34) |

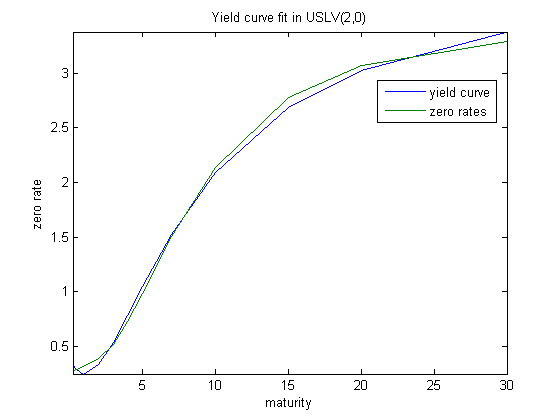

This suggests that volatility of factors does not necessarily get extinct in the long run, unlike the behavior observed in the one-factor case. An example of a calibrated yield curve is shown in Fig. 3.

4 The USLV Model

Until this point, our formalism has largely followed the CGW model by Carr et al., (2011) (albeit using the formulation of LGP dynamics proposed by Bekker & Bouwman, (2009)). Now it is time to part ways.

CGW investigate a parametric stochastic volatility (SV) specification of the dynamics of . In that specification, the stock volatility is obtained by a stochastic time change with an activity rate process given by a superposition of CIR processes.

Our plan is different. We want to stick to simple one- or two-factor specifications of the stochastic volatility process, while concentrating on modeling a nonparametric local volatility layer in Eq.(17) in such a way that all observable option quotes would be exactly matched. Furthermore, our approach is necessarily numerical and is based on a Markov chain approximation to the dynamics of the martingale .

We will construct our model in two steps. In the first step, we develop a discretized nonparametric local volatility version of USLV that corresponds to a zero vol-of-vol limit of the full-blown model. Calibration to option quotes in this framework is achieved via a set of multiplicative adjustment factors acting on elements of the Markov generator (see below). We will refer to these adjustment factors as the one-dimensional (1D) Speed Factors (SFs). Calibration of such a one-dimensional USLV model amounts to computing a set of 1D SFs.

In the second step, we move on to a full-blown USLV model with a nonzero vol-of-vol by turning stochastic volatility on. In the present discrete-space framework, this amounts to making the Markov chain generator stochastic.

To retain a near-perfect calibration to a set of option quotes obtained in the first (1D) step, we introduce another set of speed factors which we will refer to as 2D speed factors (2D SFs). The 2D SFs are then calibrated from the previously computed 1D SFs using a version of the Markovian projection method implemented in an efficient manner using forward induction on the Markov chain. Once calibrated, the resulting 2D Markov chain can be utilized to set up efficient pricing schemes for derivatives based on backward-induction algorithms.

We note that the resulting discrete-space continuous-time dynamics on a Markov chain with a stochastic generator arising in our approach resembles the BSLP model developed for portfolio credit derivatives in Arnsdorf & Halperin, (2007). The two models are similar in that both use a two-step approach to calibration. In addition, both the definition and parametrization of our speed factors are similar to how analogously defined contagion factors are introduced and used in the BSLP model. The difference of the USLV model from the BSLP model is that while a discrete-space description is exact for credit,121212Provided some additional assumptions are made, such as a discrete spectrum of recovery values. it is used as an approximation to the dynamics of the underlying for USLV. Furthermore, while the BSLP model uses a non-linear death process as a model for a portfolio loss, in the present case we use a nonlinear quasi-birth-death (QBD) process as a discrete approximation to the dynamics of a two-dimensional Markov driver . Finally, we use a different method for an efficient computation of matrix exponentials arising in evaluation probabilities on Markov chains.

In what follows, we use the following compact notation for different flavors of our model. We denote one- and two-factor discretized local volatility models as USLV(1,0) and USLV(2,0), respectively. Versions with stochastic volatility are denoted as USLV(1,1), (2,1), or (2,2). We call a discretized process for a 1D process, while the joint process of and stochastic volatility is referred to as a 2D process.

4.1 USLV(1,0): One-Factor Local Volatility

We consider the following SDE describing a local volatility dynamics of a one-dimensional Markov driver under the -measure:

| (35) |

where is a Brownian motion and is a local volatility. Our objective is to discretize the dynamics corresponding to Eq.(35).

To this end, we first construct a nonuniform grid of possible values of the martingale with . Let be the number of points on the grid and be the nodes on the grid. Irregularity of the grid allows making it denser in interesting regions, and sparser in uninteresting ones. Clearly, the fact that our process is a martingale helps as our grid should not be too large: as time passes, the underlying stays around the current value in the sense of expectations.

Let the current state be and let be the th space interval on the grid. We construct the elements of the generator matrix following the adaptive Markov chain approximation of Cerrato et al., (2011). Adapting their formulae to our case of a zero-drift diffusion , we obtain the Markov chain generator

| (41) |

with elements

| (42) | ||||

where we defined a grid-valued set of speed factors (SFs)

| (43) |

Now we have a Markov generator parametrized by the pointwise set of speed factors in Eq.(43). Next we will show how the SFs in Eq.(43) are turned into tunable parameters and used for calibration to option quotes.

4.2 Parametrization of Speed Factors in USLV(1,0)

As it stands, the parametrization in Eq.(41) is very general. The number of free parameters per a given time slice is , typically far exceeding the number of observed option quotes available for calibration for cases of practical interest.131313Typical values of that we have in mind for practical implementation are around 20 to 100; see also Cerrato et al., (2011).

To achieve an exact match between the number of free parameters in our model and the number of available option quotes, we consider the following parametrization of our 1D speed factors Eq.(43). Our approach here is similar to how contagion factors are used in the BSLP model of Arnsdorf & Halperin, (2007).

We assume that as a function of time , the SFs are piecewise constant between maturities of traded options. This considerably simplifies computation of matrix exponentials.

For the dependence of on the grid index (i.e., for the dependence), we proceed as follows. Let be a set of strikes for traded options across all maturities, expressed in terms of the -space as, e.g., in Proposition 3 of Carr et al., (2011). We assume that all these strikes correspond to different nodes on our grid.141414This is because our grid is constructed in such a way that it puts all strikes exactly at some nodes, plus add some nodes in between and beyond the range of quoted strikes. We then model the speed factors for all values of by picking exactly free values at locations , and using linear interpolation for points in between. In other words, our speed factors are piecewise-linear in , while the anchor points at selected nodes serve as free parameters for calibration to option quotes. Any consistent set of option quotes can be exactly matched by the present method.151515Alternatively, if the number of liquid option quotes per maturity is large while the calibration speed is an issue, then some strikes can be omitted from the set of anchor points at the price of giving up an exact calibration for these omitted strikes, while keeping an exact calibration for the other strikes. For example, one can be guided by the size of quoted bid-ask spreads in deciding which strikes could be skipped without much sacrifice to accuracy while gaining in performance. To preserve no-arbitrage for the omitted strikes, one should use a monotonic interpolation in the probability space.

Note that calibration of local volatility models without assuming availability of a complete set of option quotes (i.e., when the number of option quotes is less then the number of nodes on a grid) has been previously discussed in the literature. In particular, a recent paper by Lipton & Sepp, (2011) analyzes a setting where the local volatility function is piecewise-flat between quoted strikes (or between mid-points) using Laplace-transform based methods. Unlike their method, which is exact in 1D, our approach is based on numerical optimization, but it is extendable to a multivariate setting (2D and higher) along the same lines as in 1D. In addition, a piecewise-linear volatility model appears to be a less drastic approximation than a piecewise-flat model.

4.3 Calibration of the USLV(1,0) Model

Calibration of the speed factors in the above setting is straightforward. The anchor points introduced above serve as parameters of optimization. Given a multidimensional optimizer, at each iteration we first construct the generator matrix given the current set of the anchor points. After that, finite-time probability distributions are computed by taking matrix exponentials of the generator. As the mathematical structure of our model is essentially the same for the and cases (one or two factors for the term structure), we postpone presenting details of this procedure until the next section where we introduce an version of our model. Theoretical option prices for a given set of model parameters are then computed using these probability distributions. Finally the optimizer adjusts the current set of free parameters to decrease the error between the model and the market.

5 USLV(2,0): Two Curve Factors

With two factors for the curve (), we assume the following vector-valued SDE for the dynamics of :

| (50) |

where two Brownian motions are independent, and the volatility matrix is defined as follows:

| (55) |

Here is a scalar function of the state variable , and are the values of at time . An explicit specification of this function will be given below. Note that components and defined by Eq.(50) and Eq.(55) are correlated with correlation coefficient .

Our first objective is to approximate the dynamics given by Eq.(50) by a 2D Markov chain. To this end, we start with a Markov generator corresponding to the 2D diffusion given by Eq.(50):

| (56) |

where is an arbitrary function (a value function or a transition density) of backward variables (with forward variables treated as parameters). The generator specifies the continuous-space backward equation

Note that in order to be probabilistically interpretable as a generator of a Markov chain, a discrete version of the generator should have all nondiagonal elements nonnegative, and all diagonal elements negative, such that all rows sum up to one. These remarks are important as not any discretization of gives rise to a valid Markov chain generator. For example, using a central divided difference to approximate the mixed derivatives in Eq.(56) would not preserve nonnegativity of nondiagonal elements of .

With these remarks in mind, and given a two-dimensional grid161616For simplicity, in this section we assume that our one-dimensional grids are uniform with the same number of grid points per each dimension. Therefore, , . For analysis of a nonuniform grid, see Appendix A. of values of with nodes per dimension, we approximate second derivatives by divided differences. Derivatives , are represented using the central differences

while for the mixed derivative we take uncentered differences which preserve nonnegativity:

Using this in Eq.(56) and regrouping terms, we obtain

| (57) |

where we introduced the following compact notation:

| (58) | ||||

| (61) | ||||

| (64) |

where .

To ensure that all parameters are nonnegative, we impose the following constraint on the step size given a chosen step :

| (65) |

Assuming Eq.(65) is satisfied, we can interpret Eq.(57) as a generator matrix of a 2D Markov chain. We can write it in a matrix form as follows:

| (66) |

As we deal with a two-factor setting, the matrix elements of the generator carry four indices rather than two. To sum over two indices corresponding to the - and -states in Eq.(66), it is convenient to group all transitions according to the change of one variable (e.g., ). We obtain

| (67) | |||

Here terms in the first, second, and third row correspond to transitions , , and in the -dimension, respectively.

Mathematically, this is expressed via the following tridiagonal block-matrix form for the resulting “one-dimensional” Markov chain generator :

| (73) |

where all matrices have dimension , i.e., the dimension of our one-dimensional grids.171717If grids in and have different lengths and , then the size of these matrices will be . Explicit expressions for these matrices can be found from Eq.(5):

| (74) | |||

while all other elements of these matrices vanish. Note that this implies that the generator Eq.(73) is “doubly” sparse, as matrices and are themselves sparse; see also a comment at the end of this section.

The block-tridiagonal matrix structure Eq.(73) of the Markov chain generator is characteristic of so-called quasi-birth-death (QBD) processes. A QBD process is a bivariate Markov chain of a special type of dynamics of two components. The first component, , called the “level,” follows a birth-and-death (BD) process on either a finite or infinite set of states. Conditional on the realization of the -component at a given step , the second component , called the “phase,” follows another Markov process. For a short review of QBD processes, see, e.g., Kharoufeh, (2011). Note that in our particular case, follows another BD process, while the support of is finite. QBD processes with finite support are called finite QBD processes.

The symbols and in Eq.(73) stand for local (without change of level), backward and forward (the level is changed by one unit up or down) moves, respectively. Note that as long as the matrices and depend on level via the discretized local volatility function , our QBD process with generator Eq.(73) is a level-dependent (or nonlinear) finite QBD, denoted sometimes as a (finite) LDQBD in the literature.

It is easy to check that Eq.(73) with elements defined as in Eq.(5) is a valid Markov generator where all off-diagonal elements are positive, diagonal elements are negative and each row in sums to zero.

After the QBD generator matrix is constructed according to Eq.(73), a matrix of finite-time transition probabilities with matrix elements

| (75) |

can be computed by solving the forward Kolmogorov equation

| (76) |

For a given interval where the generator does not depend on time, the solution of the forward equation is

where is a state vector at time , and stands for the matrix exponential of .

A few remarks on the complexity of the method just presented are in order here. We have managed to map the two-factor continuous-space dynamics Eq.(50) on the state space onto a QBD process with generator Eq.(73). The latter can formally be viewed as a one-dimensional Markov chain in an extended linear space whose basis is formed by elements of a Kroneker product of grid values (and properly rearranged to form a QBD structure). Therefore, computation of transition probabilities Eq.(76) in our two-factor model is, at least formally, as simple as a corresponding calculation for a one-factor model, and reduces to computation of a single matrix exponential, albeit of a larger matrix.181818Here in addition to various efficient algorithms for computing a matrix exponential of a sparse matrix, one could use splitting in different dimensions that would take into account a block-diagonal form of the generator matrix .

While naively the generator has free parameters, their actual number is much lower due to sparsity of the matrix. It is simple to find that the number of nonzero elements that need to be stored scales as . For example, for our matrix would be of size with only 109,002 non-zero elements. Matrices of such sizes can well be handled by modern matrix exponentiation methods (see below).191919While a randomization method that we describe in the following section may not be the most efficient method when the norm of matrix is large (Sidje & Stewart, (1999)), it is very convenient for introducing stochastic volatility via a stochastic time change. We therefore stick to this approach in what follows.

5.1 Transient Probabilities of QBD Chain by Randomization

It is well known that a direct computation of a matrix exponential with a Markov generator via a straightforward use of a Taylor series expansion as is in general not a good idea (see Moler & van Loan, (2003)). The main reason for this is that severe roundoff errors might accumulate (especially when the matrix is large) due to the fact that the generator has both positive and negative entries. In addition, matrices become nonsparse even if the original matrix is sparse, as is the case for the QBD process.

An efficient method of choice for dealing with matrix exponentials for large matrices is known as Jensen’s randomization; see, e.g., Gross & Miller, (1984), or Haverkort, (2001) for a more recent review. The method proceeds as follows. We start with choosing a parameter , and define the matrix

| (77) |

With our choice of , all entries of are between 0 and 1, and all rows sum to 1. This means that is a stochastic matrix that describes a discrete-time Markov chain “related” to the original continuous-time Markov chain with generator . We now want to discuss in more detail the sense in which these two Markov chains are “related.”

To this end, we substitute as given by Eq.(77) into the solution of the forward equation:

Using a Taylor series expansion for the matrix exponential in this expression, we obtain

| (78) |

where

are Poisson probabilities, i.e., probabilities of observing events by time for a Poisson process with intensity . Note that a naive Taylor expansion of the matrix exponential behaves badly, but the new expansion is much better behaved: roundoff errors are now largely eliminated as all entries of matrix are between 0 and 1. Moreover, different terms are weighted by the Poisson probabilities, so that the expansion is expected to converge fast when the product is not too large.

We note that the construction given by Eq.(78) can be interpreted as a discrete-time Markov chain (DTMC) () with transition matrix subordinated to a Poisson process where the latter serves as a randomized “operational time” for , so that the subordinated process is now defined as (see, e.g., Feller, (1968)). We will return to the topic of subordinated processes in Sect. 7.1.

It is important to point out that the method just presented can be used without a matrix-matrix multiplication (as Eq.(78) would naively suggest). Let be the probability distribution vector in the DTMC with transition matrix after epochs. This vector can be computed recursively:

| (79) |

Using the vector , the state probabilities Eq.(78) in the original CTMC are computed as follows:

Therefore, computationally the algorithm amounts to a series of vector-matrix multiplications that can be done very efficiently for matrices of sizes typical for our problem. Moreover, the recursive procedure of Eq.(5.1) preserves the sparsity of , thus enabling a substantial acceleration of the vector-matrix multiplication.

In practice, the infinite sum in Eq.(78) is truncated at some value . This value can be adaptively controlled within the algorithm itself, as a theoretical upper bound for an error resulting from the truncation is available as discussed, e.g., by Gross and Miller (1984).

5.2 Calibration of Speed Factors in USLV(2,0)

Summarizing our results for the USLV(2,0) model so far, we see that the mathematical structure of the (2,0) model is similar to that of the (1,0) model. Indeed, for the latter our Markov chain construction gives rise to a nonlinear birth-death (BD) process modulated by 1D speed factors (SFs) . After a proper parametrization as described in Sect. 4.2, SFs are calibrated to market option quotes. For the (2,0) case (two factors for the term structure), the resulting Markov chain is a nonlinear quasi-birth-death process, again modulated by a set of SFs . In terms of computational complexity, the two cases are essentially the same, as both amount to calculation of matrix exponentials of a Markov chain generator (albeit in different dimensions).

Calibration of the (2,0) model is done by the fitting function in Eq.(50). To this end, we proceed similarly to the one-factor case. We assume that function is a function of single argument, , where are some weights (e.g., ). For calibration purposes, we could parametrize this function in a piecewise-linear way, i.e., in exactly the same way as we did before for the model. The number of free parameters (anchor points) and their locations would be chosen based on a particular set of instruments available for calibration.

To continue with our theoretical construction of the model, in what follows we assume that the stage of construction of a (2,0) (or (1,0)) version of the USLV model is completed along the lines described here. In what follows, we refer to these SFs as 1D SFs, in order to differentiate them from another set of speed factors (2D SFs) that will be introduced below when we add stochastic volatility to the model.

Finally, we note that while the main purpose of the USLV(2,0) model for our purposes is to use it as a building block in the construction of a full-blown USLV(2,2) model with stochastic volatility, the pure local volatility USLV(2,0) model can also be useful in its own right, e.g., as a way of pricing European vanilla options with illiquid strikes in terms of prices of liquidly traded options.

6 USLV(2,2): Two Curves and Two Volatility Factors

Once we have a calibrated USLV(2,0) model, introduction of stochastic volatility in this framework amounts to two things: (i) introducing new dynamics for volatility drivers, and (ii) making sure the model still calibrates to available option prices. This produces a calibrated USLV(2,2) model.

Let us note that stochastic volatility dynamics can be introduced in our framework in two ways. In the first approach, we follow the formulation of a continuous-time Markov chain (CTMC) dynamics, which we now augment by 2D dynamics of “spot” variance factors. For numerical implementation, the model is then put on a time grid with a uniform time step . All calculations (see below) are done to accuracy, which assumes that should be sufficiently small.202020For example, we might need to use daily or more frequent steps, depending on the level of volatility, with this approach. With this method, we solve the forward and backward Kolmogorov equations one step at a time, similarly to finite difference methods.

In the second approach, we deal with arbitrary time lines which do not necessarily have small time steps. For example, we may want to model the values of underlying factors only on a sparse set of “interesting” dates (e.g., coupon dates, call dates etc.). Essentially, by taking matrix exponentials of the generator, we aim here to achieve a functionality similar to the USLV(1,0) and USLV(2,0) models (or any CTMC model, for that matter), which are capable of computing finite-time transition probabilities directly.212121To the extent that one-step methods, such as the Runge-Kutta method, can be viewed as particular ways to compute matrix exponentials (see Moler & van Loan, (2003)), what we mean here by “direct” calculations are other methods of computing matrix exponentials that might in some cases be more efficient than one-step methods.

Respectively, in what follows we present two versions of the USLV(2,2) model. In the first version, we assume a Markov dynamics in the pair where is a bivariate “spot” variance driver. In the second version, we instead assume a Markov dynamics in a pair of and an integrated bivariate variance, or, more generally, a bivariate stochastic time subordinator (see below). We will use the notation for the latter in what follows. For reasons that will become clear shortly, we will refer to these two versions of the model as the activity-rate-based model (AR-USLV), or the implied-time-change-based model (ITC-USLV), respectively.

On the theoretical side, it turns out that both approaches can be viewed in a unified way by interpreting them as particular realizations of a stochastic time change of the original QBD Markov chain. We will give more details on this below in Sect. 7.1.

On the practical side, we can choose between two numerical methods. With the first method, we can implement both the AR- and ITC-versions of our model in a similar way using a version of the Markovian projection method. The latter reduces calibration of USLV(2,2) to a fast forward induction method in what is essentially a 1D problem, without a need for a forward induction on a full 2D Markov chain.222222Recall that by 1D and 2D, we mean linearized spaces obtained from the pairs and by taking elements of pairwise Kroneker products as new 1D bases. In terms of factor counting, our 1D and 2D Markov chains correspond to the two- and four-factor model specifications, respectively. No new optimization in addition to one performed at the stage of calibration of the USLV(2,0) model is involved here. Therefore, the method is very fast on each given time step, the only potential bottleneck being the necessity to perform such computation repeatedly on a dense time grid. The method is nonparametric in that it solves the problem of calibration of the full-blown USLV(2,2) model via a judicious choice of 2D speed factors (SFs) that are computed off the calibrated 1D SFs of the USLV(2,0) model.

The second method, which is applied below for the ITC-USLV version of our model but in principle could be used for both versions, is to “break the symmetry,” and make the process parametric in one dimension (e.g., ), while keeping it nonparametric in another dimension (resp., ). The idea here is that for the purpose of calculation of finite-time transition probabilities in the -space, we can perform averaging over the randomness due to analytically (or semi-analytically) once a tractable model for subordinator is specified. The averaging over the residual randomness due to is performed numerically. Similarly to the previous case, this calculation can be done in a nonparametric setting, where at each step on our sparse time grid, we introduce just enough free parameters to match observed quotes for options maturing at this time. Differently from the previous case, the recalibration to option quotes in the present setting amounts to a (convex) optimization problem in the dimension equal to the number of option quotes for this maturity.

The two flavors (AR and ITC) of our USLV(2,2) model outlined above thus offer a certain trade-off in terms of complexity. For the AR-USLV(2,2) model, the recalibration is fast for one step, but complexity scales linearly with the number of time steps on a dense grid; i.e., the complexity is . For the ITC-USLV(2,2) model, the complexity is , where is the number of nodes on a sparse time line, and is the number of option quotes per node, independently of , but the part above involves convex optimization in dimension . Based on previous experience with similar models, we expect a compatible performance from the two versions of the USLV(2,2) model, at least for typical cases (e.g., , ). Therefore, in what follows we will present both versions of the model.

Our plan for the reminder of this paper is as follows. In the rest of this section, we describe the AR-USLV(2,2) version of the model, where the Markov pair is , with a bivariate spot variance driver . In Sect. 6.1, we provide a qualitative overview of this version of the model. The following subsections of Sect. 6 provide details of our approach. The ITC-USLV(2,2) version of the model, where the Markov pair is with being a bivariate subordinator, is presented in Sect. 7. As will be shown below, calibration to observed option prices amounts, in this approach, to a construction of an implied time change (ITC) process. Within a particular approach presented in Sect. 7, the ITC process is defined in terms of a bivariate exponential-Lévy process where is a parametric subordinator (e.g., an exponential gamma process), and is a nonparametric subordinator. The latter will be referred to as a time dilaton process, for reasons explained below.

6.1 Overview of AR-USLV(2,2)

As was mentioned above, a model obtained from our USLV(2,0) model by adding new state variables (in this case, spot volatility drivers ) would not in general match observed option prices, even if our initial USLV(2,0) model does. Moreover, for any particular parametric model for the dynamics of the pair , we are still not guaranteed that the full model could accurately fit available option quotes even after calibration of parameters of the -process.

In order to reinforce a nearly exact calibration to options for all consistent sets of quotes, we introduce 2D speed factors (SFs) in the full (2,2) model, that play an analogous role to 1D SFs Eq.(43) in the (2,0) version of the model. We then provide a fast scheme to compute 2D SFs based on solving the forward equation on the Markov chain. Our method is similar to one used by Britten-Jones & Neuberger, (2000) (BJN), see also Rossi, (2002), for a lattice-based stochastic local equity model in a (1+1) setting. A similar method was used in the BSLP model by Arnsdorf & Halperin, (2007) for modeling dynamics of credit portfolios. For a similar method used for equity option pricing, see Ren et al., (2007).

A peculiar feature of a BJN-like forward induction method (to be presented in detail below) is that it tries to adjust the -process for any -process. It does not address the problem of calibration of parameters of the -process itself. In certain situations, it might make sense to try to calibrate parameters of the -process as accurately as we can before adding a local volatility layer (so that our change to a parametric model due to introduction of a local volatility would be a minimal tweak of the model). Alternatively, we could try to fit parameters of the -process after we introduce the local volatility layers, but before we compute the 2D SFs. This might be an attractive option for a practical method of model calibration in our setting. The reason is that if such parametric calibration of the -process produces a good but not perfect fit to the data, the role of non-parametric 2D SFs of the model would be to perfect quality of calibration at the price of adding some nonparametricity.232323We hold a view that nonparametricity is “evil,” but it is a “common evil” in the sense that it is used everywhere (for term structure calibration, local volatility models etc.).

Note that while the BJN-like approach does not by itself address the problem of calibration of parameters of the -process for a parametric specification of the dynamics of , this is where we could use Laplace transform based methods for stochastic subordinators, similar to the method presented in Sect. 7 in a slightly different setting. This implies that the calibration method presented later in this section and a method presented in Sect. 7 can in practice be used together for a joint parametric/nonparametric calibration of the AR-USLV(2,2) model.

Yet another possible way to calibrate our model would be as follows. If a trader has a strong view on the relative weights of a spanned (delta-driven) and unspanned (genuine vega) contribution to options’ vegas, and wants the model to behave accordingly, this could be achieved as follows. Assuming that we are able to map constraints like those onto some typical behavior of the set of SFs,242424Such dependence can be established either theoretically, or empirically on the basis of behavior of the model as a function of model parameters. we first fix some set of 1D SFs, and then calibrate parameters of the -process given these SFs. After parameters of the -process are specified in this way, we proceed in the regular way of calibrating the model, by first computing the “true” (market-implied) set of 1D SFs, and then following the forward calibration of 2D SFs in the full-blown model with parameters of the -process just computed at the previous step. Again, a combination of various methods presented below can be used to implement such a calibration strategy.

As a brief summary, our QBD Markov chain stochastic-local volatility offers substantial flexibility in how the model can be calibrated to available market and/or historical data. Different steps/versions of the calibration procedure can be combined (or skipped), depending on the specific needs of an end user. We now proceed with describing our framework.

6.2 QBD Processes and Stochastic Time Changes

We prefer to think of stochastic volatility in terms of a stochastic time change of some “base” process such as a Brownian motion. (See Sect. 7 for more details and relevant references.) As our original two-factor diffusion equation, Eq.(50), has two Brownian drivers, and , we can use two different stochastic clocks on them. This would amount to having a stochastic local volatility model with and .

Such formulation can be useful for asset classes where the short- and long-term option volatilities typically behave differently (e.g., have different typical levels or vol-of-vol), in addition to a different behavior of -factors driving short- and long-term prices of basic instruments (bonds, futures etc.). For example, for modeling commodity derivatives, we might want to have one long-term factor driven by a Brownian driver with its own stochastic clock (stochastic volatility) driver , and another, short-term factor driven by another (possibly correlated) Brownian driver , with its own stochastic clock driver .252525Alternatively, correlated dynamics of two stochastic drivers with each one having its own stochastic volatility factor can be used for pricing hybrid derivatives. This results in a four-factor scenario with correlated long- and short-term factors, each having its own stochastic volatility driver.

The above picture of two curve drivers each having its own stochastic clock is not lost in our discrete-space Markov chain construction. As we will show next, the structure of our QBD Markov chain Eq.(73) for the case enables introducing two stochastic clocks in the model in an internally consistent way, and without any need of introducing additional ad hoc constraints on the model dynamics. These stochastic clocks will modulate two Markov chain generators. As the latter play the role of stochastic drivers in the discrete-space setting, the resulting “ecosystem” of (discrete-valued) curve and volatility factors bears a strong structural similarity to its continuous-space counterpart.

To explain our construction, we start with representing the Markov generator Eq.(73) in the following form:

| (90) | |||||

| (91) |

where and , with being a vector of ones. Using Eq.(5) and Eq.(5), it can be readily checked that both and defined in Eq.(90) are valid generators in the sense that for both, all off-diagonal elements are positive, all diagonal elements are negative and all rows sum up to zero.

This can be interpreted as follows. The second generator corresponds to an idiosyncratic component of the -dynamics that is independent of the rest of the system, and can be thought of as describing idiosyncratic jumps of that occur without a simultaneous jump of on the same time interval.262626This can also be viewed as a one-dimensional orthogonal projection of two-dimensional dynamics of the pair onto a subspace where no jumps in variable are allowed. In terms of representation of stochastic dynamics of our system, this generator is an avatar of the idiosyncratic Brownian driver in Eq.(50). The first generator describes joint jumps of and , and can be thought of as an avatar of the common Brownian driver in Eq.(50).

As shown in Appendix B, a random time change of a continuous-time Markov chain amounts, in terms of the resulting Markov generator for the chain, to scaling all elements of the original Markov chain generator by a common factor given by the value of the activity rate (intensity of the time change) process.

As they conserve probability separately from each other, two generators and can be seen as representing two different subsystems of our dynamic system in the -space. As a time change acts as a common scaling factor on a generator matrix (see Appendix B), this implies that we can subject two generators, and , to different stochastic clock changes without any problems with laws of probability: after separate time changes, probabilities are still all nonnegative, and sum up to one in each subsystem separately. This gives rise to a discrete-space version of a continuous stochastic volatility model.

To summarize, the (2+2)-factor structure of the original continuous-space system Eq.(50) (i.e. two factors for the term structure and two factors for the volatility) is now naturally mapped onto a corresponding structure in our Markov chain model, where a QBD process is an avatar of a two-dimensional Brownian motion , and two volatility factors are separately introduced as two stochastic clocks for two generators and as explained above. We now discuss specific realizations of this scenario in our model.

6.3 Forward Equation and Transition Probabilities in USLV(2,2)

We assume discrete dynamics of stochastic intensity (stochastic volatility) drivers , with an odd number of discrete states for each driver . Points on a two-dimensional -grid are denoted as . The initial values correspond to the midpoints on the grid.

In practice, we prefer to keep a low number of states (say 3 to 11) per volatility factor. As volatility is unobservable, we feel that maintaining a low number of states might suffice to reproduce most important stylized facts about stochastic volatility such as mean reversion and/or volatility clustering (persistence), alongside its role in providing a better behavior of a forward smile (a non-flattening smile for longer maturities) than typical behavioral patterns observed with local volatility models.

To ease the notation, in this section we use Latin indices to enumerate states ( etc.), and Greek indices to enumerate values of , . However, because we deal with a two-factor setting, both the indices and factor values are now two-component vectors rather than scalars; for example,

| (92) |

A similar representation is used for volatility drivers . In what follows we use both the vectorized and component notations.

We postulate that the 2D dynamics of the pair (where both factors and are two-dimensional) in the USLV model is Markovian. The system is defined in terms of the joint marginal probabilities

and conditional transition probabilities

The forward equation takes the form

| (93) |

The transition probabilities have the following expansion:

| (94) |

where is the Markov generator, and is the 2D Kroneker symbol (with a similar definition for ).

To proceed, we introduce the following conditional probabilities:

| (95) | |||||

The joint probability can now be written as follows:

| (96) |

Using Eq.(94), we obtain

| (97) |

where

| (98) |

is the conditional generator of the -Markov chain.

It is convenient to write the second conditional probability in Eq.(95) in the following form:

| (99) | |||||

Note that the term in the second equation is not multiplied by because the second relation in Eq.(95) is not a transition probability but rather a conditional probability where we condition, in particular, on . If , then cancels out in the calculation of the conditional probability. This means that is not a real generator, but rather a “pseudo generator” introduced here to simplify formulae to follow. In its turn, this means that diagonal elements of cannot be made arbitrarily negative, as otherwise we would end up with probabilities reaching outside of the unit interval .

Now we plug Eq.(94) and Eq.(97) into Eq.(96). This produces the following relation (here we omit terms):

| (100) |

A more explicit expression for the generator in terms of auxiliary generators , and can be obtained using the following identity (which can be checked by inspection):

| (101) |

Using Eq.(100) to evaluate different terms in the right-hand side of Eq.(101) in terms of the auxiliary generators, we obtain, after some algebra, the following general representation of generator of USLV(2,2):

| (102) |

Different terms in this expression are interpreted as follows.272727We thank Leonid Malyshkin for proposing a decomposition of the Markov generator in such form, as well as for discussions that helped improve the presentation in this section.

The first term is a generator of idiosyncratic jumps of that proceed without a simultaneous jump of in the interval . Various continuous-space models can be used as a means to parametrize this generator via discretization of the state space. For example, starting with a diffusive model for , we end up with a tridiagonal generator matrix . More details and examples will be given below in Sect. 6.6.

The second term in Eq.(102) is a generator of joint jumps of . Note that it is a valid generator on its own as long as . Again, different specifications of this generator can be considered within our general framework. This will be discussed in some detail below in Sect. 6.7.

Finally, the last term in Eq.(102) is a generator of idiosyncratic jumps of that proceed without a simultaneous jump of . It is determined by the conditional Markov chain generator . This generator plays a special role in our construction. It is special because the conditional Markov chain generator is the only generator in Eq.(102) that impacts prices of European vanilla options, while prices of exotic options will in general depend on all generators that enter Eq.(102). As will be explained in more detail below, this is due to the following relations that follow as long as and :

| (103) | |||||

Note that the fact that theoretical prices of vanilla options computed in USLV(2,2) do not depend on specification of the other generators and in Eq.(102) has a few interesting implications.

First, it suggests a nice “orthogonality” property of model parameters determining various generators that enter Eq.(102), such that parameters driving prices of exotic options can be tuned (or picked) without impacting calibration to vanillas. If prices of some exotic options are available in the marketplace, this can be used to calibrate these two generators, after the model is calibrated to available vanillas.

Second, in a scenario where no reliable pricing information is available for exotic options, we could use this property of the model in order to specify a measure of “exoticness” as, e.g., the amount the price of the given exotic derivative moves under certain functional or parametric tweaks of the first two generators in Eq.(102). Given two exotic options and given tweaks to be performed on the generators in Eq.(102) (such as a common rescaling of all elements) while pricing both options, one of the options from the pair would in general end up being “more exotic” than the other. While these issues will be addressed in a future work, here we concentrate on the problem of calibrating the model to European vanilla option prices.

6.4 Conditional Markov Chain Generator

Clearly, prices of European vanilla options on a given underlying for a set of options maturing at times are only determined by marginal distributions of at these times. An equation driving evolution of marginal -distributions in the full USLV(2,2) model can be obtained by summing over in the forward equation Eq.(93). We obtain

| (104) |

where we used Eq.(103) for the last equality. This justifies the claim we made above: observed prices of European vanilla options impose certain constraints on the conditional Markov chain generator , but not on the other generators appearing in Eq.(102). Rearranging terms in Eq.(104), we obtain

| (105) |

An explicit expression for the conditional Markov chain generator can be obtained using Eq.(96):

| (106) |

From this point onwards, we reserve the notation for a calibrated generator of USLV(2,2), while using the notation for an initial guess for . The latter is assumed to be a valid generator (obtained from some consistent model) that is not necessarily accurately calibrated to the observed market. In what follows, we will refer to the latter as a prior conditional Markov chain generator. While a particular functional relation between the two generators and will be considered in the next section, in the reminder of this section we concentrate on specifying the second, “prior” generator .

As was outlined above (see also Appendix B), we define as a combination of generators and (see Eq.(90)), scaled by two components of :

| (107) |

Recalling the original definition Eq.(73) of the Markov chain generator, we can write this in a matrix form:

| (113) |

where all matrices are obtained by scaling of by :

| (114) |

while elements of are scaled by , except for the diagonal elements:

| (117) |

where is defined in Eq.(90). Using Eq.(5) in Eq.(117), we obtain the explicit expression:

| (120) |

Clearly, conditional on values , diagonal elements of the conditional Markov chain generator Eq.(113) given by the second line of Eq.(117) are negative (as long as Eq.(65) holds), while all off-diagonal elements are positive, and the row-wise sums of elements in Eq.(113) are all zeros. Therefore, Eq.(113) is a valid conditional generator for any fixed values of . The first component modulates transitions between -states (which may or may not be accompanied by transitions between -states), while the second component modulates transitions between -states without simultaneous transitions between -states.

6.5 Fast Calibration of USLV(2,2) by 1D Forward Induction

In this section, we present a fast calibration algorithm that enables a recalibration of the full 2D USLV(2,2) model starting from a calibrated 1D USLV(2,0) without using a forward induction on a full-blown 2D Markov chain. It uses a recursive procedure of “integrating in” the stochastic volatility process. Our method is similar to Arnsdorf & Halperin, (2007). In its turn, a fast calibration method on a 2D Markov chain used in Arnsdorf & Halperin, (2007) is similar to an algorithm originally developed by Britten-Jones and Neuberger (BJN)282828 This approach was later popularized by Piterbarg, (2006) under the name “Markovian projection.” Note that both BJN and Peterbarg cite the work by Dupire on the link between stochastic and local volatility models. Dupire’s approach seems to provide a common basis for both the BJN and Markov projection methods..

Recalling our previous notation where we used symbols and for the calibrated and “prior” conditional Markov chain generator, we assume the following relation between them:

| (121) |

Here are adjustment factors that will be used below to calibrate the full-blown USLV(2,2) model.292929The theoretical interpretation of adjustment factors is that they provide “risk-neutralizing” drift corrections to the dynamics in the presence of stochastic volalitity; see a related discussion in Britten-Jones & Neuberger, (2000) and Rossi, (2002). Note that Eq.(121) defines a valid generator as long as and is a valid generator, as all nondiagonal elements of are non-negative, all diagonal elements are negative, and all rows sum up to zero.

The purpose of introducing the adjustment factors in Eq.(121) is to provide degrees of freedom needed for calibration to option prices in the (2,2) model in a way similar to the way the 1D speed factors were used above to calibrate the (2,0) model without stochastic volatility. As will be shown below, such calibration can be done in a numerically efficient way by reutilizing results of a previous calibration in a local volatility USLV(2,0) model. Note that after calibration of USLV(2,2) is done via a choice of multiplicative adjustment factors , the latter can be combined with the 1D SFs that appear in the “prior” generator to produce 2D SFs .

To proceed, we first plug Eq.(121) into Eq.(105). This yields

| (122) |

This can be compared to the forward equation obtained in the USLV(2,0) model where we have the following definition of the generator:

| (123) |

while the forward equation has the form

| (124) |

Comparing Eq.(122) and Eq.(124), we find that marginal distributions in both the USLV(2,2) and USLV(2,0) models are matched at each node provided we make the following choice for adjustment factors in Eq.(121):

| (125) |

We now use our key result Eq.(125) to set up a convenient and fast forward-induction method for the calibration of USLV(2,2) that utilizes the results of the 1D calibration of the -Markov chain of the USLV(2,0) model with a calibrated generator , starting with a “prior” conditional generator of the USLV(2,2) model.

We assume that the 1D calibration of the -Markov chain is performed as discussed above. We start with the initial conditions for the 2D and 1D probability distributions, correspondingly,

| (126) |

where and are indices corresponding to the initial values of and (which we assume to be known), respectively. Using Eq.(125), we solve for :

| (127) |

Note that for , the correction factors at time are undefined. However, this does not pose any problem as such states are unachievable at time , and therefore play no role in the dynamics. If desired, these parameters can be assigned some dummy values that would not have any impact on any numerical results produced with the model.

Next we use the forward equation on interval to compute the joint probability , which is then used to compute the adjustments for all nodes at time , and so on. As a result, we have a full 2D USLV(2,2) Markov chain calibrated to the set of option quotes using a fast and effective algorithm.

6.6 Generator of Idiosyncratic Dynamics of

In this section, we provide some examples of specification of the first generator, , in Eq.(102). We recall that by construction of the model, the choice of this generator in USLV(2,2) has no impact on the quality of calibration of the model to prices of European vanilla options in a calibration set, while in general it does impact prices of exotic options produced by the model.

As was mentioned above, for practical applications we typically have in mind a low (e.g., 3 to 11) number of possible states per dimension of the stochastic volatility factor. This has two implications.