Fixed point theorem for simple quantum strategies in quantum market games

Abstract

A simple but nontrivial class of the quantum strategies in buying-selling games is presented. The player moves are a rational buying and an unconditional selling. The possibility of gaining extremal profits in such the games is considered. The entangled merchants hypothesis is proposed.

1 Projective geometry approach to profits

Half thousand years ago Fra Luca Pacioli, a teacher of Leonardo da Vinci set standards of Venice accounting (i.e. the double accounting) and for the theory of perspective. In the author opinion this is not accidental because projective geometry approach forms a natural language of description of the market reality. Let us consider the simplest possible market event of exchanging two goods which we would call the asset and the money and denote them by and , respectively. Let and denote some given amounts of the asset and the money, respectively. If the assets are exchanged in the proportion then in the context of selling processes we call the logarithmic quotation for the asset

| (1) |

the demand profit. Respectively, in context of buying, we call the number

| (2) |

the supply profit. From projective geometry point of view any market can be represented in the -dimensional real projective space, that is -dimensional vector space (one real coordinate for each asset) subject to the equivalence relation for and . For example we identify all portfolios having assets in the same proportions. In this context separate profits or , gained by selling or buying respectively, are not invariant (coordinate free). The profit gained during the whole buying-selling cycle is given by the logarithm of an appropriate anharmonic (cross) ratio [1], and is an invariant (e.g. its numerical value does not depend on units chosen to measure the assets). The anharmonic ratio for four points lying on a given line, is the double ratio of lengths of segments and is denoted by . In our case the anharmonic ratio in question, , concerns the pair of points:

| (3) |

and the pair , . The last pair results from the crossing of the hypersurfaces and corresponding to the portfolios consisting of only one asset or , respectively and the line . The dots represent other coordinates (not necessary equal for both points). The line connecting and may be represented by one-parameter family of vectors with -coordinates given as:

| (4) |

This implies that the values of corresponding to the points and are given by the conditions: , . Substitution of Equation leads to

| (5) |

The calculation of the logarithm of the cross ratio on the line gives

| (6) |

This quantity for successive transactions is the unique (up to some factor) additive invariant of projective transformations.

2 Quantum market games

Traders usually employ intuitive strategies that if perceived as objective ”being” are not easily describable in a quantitative way. But these relations form natural objects of interests of accountants and econometricians that deal with market reality. This situation has an analog in physical phenomena. In the Ithaca interpretation of quantum mechanics ”correlations have physical reality; that which they correlate does not” [2]. Besides, only quantum theory allows to consider self-conscious entities [3]. In the series of articles posed by the author with Jan Sładkowski111full texts of these papers are available at the web site http://alpha.uwb.edu.pl/ep/sj the quantum theory of games [4, 5, 6] is generalized on the infinite-dimensional Hilbert space and used to description of some fundamental market phenomena. These models give many interesting results, unattainable in the framework of classical theories. For example, quantum theory predicts the property of undividity of attention of traders (no cloning theorem), the sudden and violent changes of prices can be explained by the quantum Zeno phenomenon. The theory unifies also the English auction with the Vickrey’s one attenuating the motivation properties of the latter. There are apparent analogies with quantum thermodynamics that allow to interpret market equilibrium as a state with vanishing financial risk flow. In this article the author present another amazing property of quantum market games222see also J. Sładkowski, ”Giffen paradoxes in quantum market games”, in the current issue. In this formalism, each player modify his strategy by acting on the Hilbert space with tactics . The strategies can be interpreted as superpositions of trading decisions. For a trader they form the ”quantum board”. The tactics are linear, usually unitary operators, and the strategy functions have integrable square modulus. The French method of presenting demans/supply curves is based on the assumption that the demand is a function of prices and is usually referred to as the Cournot convention. In this way Born interpretation of the product lead us to define supply curve as the cumulative distribution function . The player buying quantum tactics are Fourier transforms of his tactics in selling processes and, consequently, the appropriate observables and are canonical ones, , where the economic dimensionless constant describes the minimal inclination of the player to risk (by analogy with quantum harmonic oscillator, see below). One strategy works in two different occasions. This is a property that does not occur in any classical theory.

3 Risk profile of player strategies

We can describe player strategy independently of representation of this strategy because the Fourier transformation commutes with the risk operator . The parameter measures the risk asymmetry between buying and selling positions. The pure strategies that are consistent with the low of supply (or low of demand) are represented, following Hudson theorem [7], by gaussian functions. Besides the Gibbs mixed strategies represent equilibrium markets leads to the same results as some gaussian strategies with the modified value of the constant . For this reason in typical market games the considerations of models with gaussian strategies will be good enough. When the dispersion of the demand profit tends to the distribution function tends to Dirac strategy . It means that the player fixed withdrawal price below which she or he gives the selling up.

4 The simplest quantum market game

The consequences of games between two Dirac strategies are trivial and they are a special limit case of the class of games analyzed below. Therefore we consider the games of Alice Dirac strategy versus the gaussian strategy of Rest of World (RW). Let us suppose that the RW player proposes price of the asset and Alice accepts or rejects the proposal because this is the most attractive position for Alice. We have the following rules of this game:

-

•

RW proposes with probability the price , and

-

•

Alice:

-

–

sells the asset if , or

-

–

gives up if .

-

–

Alice always buys the asset in this game because the uncertainty (dispersion) of stochastic variable for Dirac strategy is infinite. We assume rational behavior of Alice and therefore we search for her strategy (i.e. value of variable ) which maximize the intensity of her profit [8]:

| (7) |

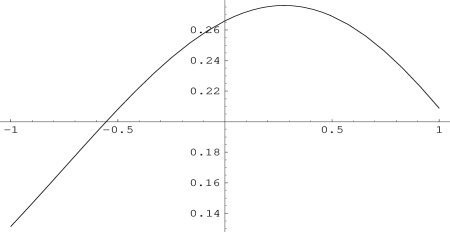

where is the average Alice profit in one selling-buying cycle and is the expected duration of the whole selling-buying cycle in this game. The profit intensity function in the vicinity of extremum is drown in Figure 1.

5 The fixed point theorem

The maximal value of the function , , lies at a fixed point of , that is it fulfills the condition . Such a fixed point exists, attracts on all domain and . When Rest of World play the market game with strategy that has unknown dispersion the above theorem proved in [8] implies natural Alice tactics for maximization her intensity of profit. In -st step of the game Alice shift her strategy to the point

| (8) |

One can easily reverse the buying and selling strategies [8].

When we modify rules of the game, and now Alice will be playing with two entangled quantum strategies (one for buying and one for selling), she will have another benefit of quanta. For the expected intensity of Alice profit from one of her strategy we obtain the equivalent of the above presented theorem again, but with greater value of maximum equal in this case. The details will be presented elsewhere. In context of this result it is natural to put forward the hypothesis that trading with bigger number of entangled quantum strategies give us opportunities of obtaining greater intensities of profits. Then in the future we will meet the inevitable complication of quantum connections on real markets.

References

- [1] R. Courant, H. Robins, What is mathematics?, Oxford University Press, 1996.

- [2] N. D. Mermin, What is quantum mechanics trying to tell us?, American Journal of Physics 66 (1998) 753–767.

- [3] D. Z. Albert, On quantum-mechanical automata, Phys. Lett. 98A (1983) 249–252.

- [4] D. A. Meyer, Quantum strategies, Phys. Rev. Lett. 82 (1999) 1052–1055.

- [5] J. Eisert, M. Wilkens, M. Lewenstein, Quantum games and quantum strategies, Phys. Rev. Lett. 83 (1999) 3077–3080.

- [6] A. P. Flitney, D. Abbott, An introduction to quantum games theory, arXiv:quant-ph/0208069.

- [7] E. W. Piotrowski, J. Sładkowski, Quantum market games, Physica A 312 (2002) 208-216.

- [8] E. W. Piotrowski, J. Sładkowski, The merchandising mathematician model, Physica A, in press; cond-mat/0102174.