also ]DEMOCRITOS

Emergence of time-horizon invariant correlation structure in financial returns by subtraction of the market mode

Abstract

We investigate the emergence of a structure in the correlation matrix of assets’ returns as the time-horizon over which returns are computed increases from the minutes to the daily scale. We analyze data from different stock markets (New York, Paris, London, Milano) and with different methods. Result crucially depends on whether the data is restricted to the “internal” dynamics of the market, where the “center of mass” motion (the market mode) is removed or not. If the market mode is not removed, we find that the structure emerges, as the time-horizon increases, from splitting a single large cluster. In NYSE we find that when the market mode is removed, the structure of correlation at the daily scale is already well defined at the 5 minutes time-horizon, and this structure accounts for 80 % of the classification of stocks in economic sectors. Similar results, though less sharp, are found for the other markets. We also find that the structure of correlations in the overnight returns is markedly different from that of intraday activity.

pacs:

89.75.Hc , 05.90.+mI Introduction

Besides their intrinsic interest, financial markets have also attracted a great deal of attention as a paradigm of complex systems of interacting agents. In this view, the correlation between different assets are one of the signatures of the complexity of the system’s interactions and, as such, have been the focus of intense recent research JPB-book ; MantegnaStanley . The central object of study is the empirical covariance matrix of a set of assets, whose elements are the Pearson’s correlation coefficients between the log–returns of assets and over a time-horizon , measured on historical time series of length . Early studies have focused mainly on daily returns ( day) and have shown that the bulk of the eigenvalue distribution of the correlation matrix is dominated by noise and described very well by random matrix theory jpb-rmt ; Stanley . This “noise” band of noisy eigenvalues shrinks as as the length of dataset increases, but it is significant for typical cases where and are of the order of some hundreds. The few large eigenvalues which leak out of the noise background contain significant information about market’s structure. The taxonomy built with different methods mantegna ; Stanley ; giada ; states from financial correlations alone bears remarkable similarity with a classification in economic sectors. This agrees with the expectation that companies engaged in similar economic activities are affected by economic factors in a similar way. With respect to their dynamical properties, it has been found that, financial correlations are persistent over time kertesz and that they follow recurrent patterns states .

Furthermore, correlations “build up” as the time-horizon on which returns are measured increases, and they saturate for returns on the scale of some days Drozdztau ; jpb0507111 . This behavior, known as the Epps effectepps , is a manifestation of the process of mutual information exchange across assets. It quantifies how this information flow is ultimately “incorporated” into correlations, in much the same way as information on single assets is incorporated into their prices. Interestingly, it was found that such a process is much faster today than in the past and more pronounced for more capitalized stocks Drozdztau . It has also been remarked blm01 ; AdP that the structure of correlations changes as the time-horizon over which returns are defined increases, i.e. that “pictorially, the market appears as an embryo which progressively forms and differentiates over time” jpb0507111 .

Here we shall take a closer look on the dependence of the structure of correlations on the time-horizon and show that the observed evolution of the market structure is due, to some extent, to the dynamics of the market mode. Global correlations play a dominant role at high frequency, thus giving rise to correlation structures which are much more clustered than at the daily scale. However, if global correlations are removed, the structure of correlations at the daily scale, is largely preserved across time-horizons, down to a scale of 5 minutes for the most liquid market we have analyzed. Loosely speaking, the network structure, after removing the market mode, appears fully formed and differentiated already at small scales, it only grows in size (of correlations) as the time-horizon increases.

The effect of disentangling the effect of the market mode when computing pairwise correlations between stocks is analogous to decomposing the dynamics of a complex interacting system in that of its center of mass and of its internal coordinates. This is obvious in physics, where the center of mass dynamics is determined by external forces, whereas internal coordinates mainly respond to inter-particle interaction forces. By analogy, our results suggest that in order to understand the dynamics of inter-asset correlations, it makes sense to eliminate the effect of the “center of mass”.

The paper is organized as follows: in the next Section we discuss the datasets and how we build correlation matrices. Then we shall discuss the results of data clustering approach in Section III first for NYSE and then for the other markets. The following Section deals with the Minimal Spanning Trees approach. Finally we shall summarize our results and offer some concluding remarks.

II The data

In this paper we empirically investigate the ensemble behaviour of price returns for different markets: the New York Stock Exchange (NYSE), the London Stock Exchange (LSE), the Paris Bourse (PB) and the Borsa Italiana (BI). All data refer to year 2002.

The NYSE data are taken from the Trades and Quotes (TAQ) database maintained by NYSE NYSE . In particular, 100 highly capitalized stocks were considered. For each stock and for each trading day we consider the time series of stock prices recorded transaction by transaction. Since transactions for different stocks do not happen simultaneously, we divide each trading day (lasting ) into intervals of length . For each trading day, we define intraday stock price proxies of asset , with . The proxy is defined as the transaction price detected nearest to the end of the interval (this is one possible way to deal with high-frequency financial data Dacorogna2001 ). By using these proxies, we compute the price returns

| (1) |

at time-horizons . The time-horizon used are minutes. For NYSE, values of are large enough that all the considered stocks have at least one transaction in each time interval.

The LSE data are taken from the “Rebuild Order Book” database, maintained by LSE LSE . In particular, we consider only the electronic transactions for 92 highly traded stocks belonging to the SET1 segment of the LSE market. The trading activity has been defined in terms of the total number of transactions (electronic and manual) occurred in 2002. However, most of the transactions, a mean value of for the 92 stocks, are of the electronic type. This market is commonly believed to be very active and can be regarded as a realization of a “liquid” market. For each stock and for each trading day we consider the time series of stock price recorded transaction by transaction and generate intraday stock price proxies according to the procedure explained above. For the LSE data, the time-horizon used were minutes. Each trading day lasts .

The PB data are taken from the “Historical Market Data” database, maintained by EURONEXT EURONEXT . In particular, we consider the electronic transactions of two subsets of stocks traded in the year 2002. For each stock and for each trading day, lasting , we consider the time series of stock price recorded transaction by transaction and generate intraday stock price proxies according to the procedure explained above. One first set, which will be analyzed in Section III, consists of the most frequently traded stocks at time-horizons seconds, for . An analogous dataset was derived considering tick time: . This choice was considered in order to probe the region of very high frequencies and to assess the relevance of time inhomogeneity of trading activity at intraday time scales. In this respect, it is worth to remark that for small stocks were not traded in each time interval. A second dataset, that will be considered in Section IV, instead consisted of stocks which were continuosly traded in the entire 2002 (i.e. in each time interval) over time-horizon of minutes.

The BI data are taken from the “Dati Intraday” database, maintained by Borsa Italiana BI . In particular, we consider only the electronic transactions occurred for 30 stocks continuosly traded in the entire year 2002. For each stock and for each trading day we consider the time series of stock price recorded transaction by transaction and generate intraday stock price proxies according to the procedure explained above. For the BI data, the time-horizon used were minutes. Each trading day lasts .

For all markets, in addition to the intraday time-horizons, we have considered returns on the daily time-horizon

| (2) | |||||

| (3) | |||||

| (4) |

corresponding to intraday, daily and overnight returns, respectively. Here and are the open and closure prices of stock in day .

Each stock can be associated to an economic sector of activity. For the NYSE data we considered the classification scheme given in the web–site http://finance.yahoo.com/, for the LSE and BI data we considered the classification scheme used in the web–site www.euroland.com, for the PB data we considered the classification scheme used in the web–site http://www.euronext.com/. The relevant economic sectors are reported in Table 1.

| COLOR | ||

|---|---|---|

| 1 | Technology | red |

| 2 | Financial | green |

| 3 | Energy | blue |

| 4 | Consumer non-Cyclical | yellow |

| 5 | Consumer Cyclical | brown |

| 6 | Healthcare | grey |

| 7 | Basic Materials | violet |

| 8 | Services | cyan |

| 9 | Utilities | magenta |

| 10 | Capital Goods | light green |

| 11 | Transportation | maroon |

| 12 | Conglomerates | orange |

Given the price return at a selected time-horizon , we built the correlation matrices in the usual way

| (5) |

Here and in what follows, denotes time average.

In order to disentangle different components of the dynamics and to understand their effect, we considered also series of datasets derived from . In all derived datasets we subtract a particular component of market dynamics from the rest. When the structure of the derived dataset differ substancially from that of the matrix we can conclude that the decomposition is meaningful and informative.

First we removed the “center of mass” dynamics:

| (6) |

From this, a covariance matrix was computed in the same way as in Eq. (5).

In a further dataset we removed the effect of the market index from . This was done first considering the time-series of the corresponding market index at the same time-horizon and then estimating the coefficients of a one factor model

| (7) |

The residuals were used to build the covariance matrix . We could build the time series only in the case of NYSE data, for which we had access to intraday data of the SP500 composite index.

In all datasets we computed an “endogenous” market index using the market average return

Using this instead of the market index in Eq. (7) and considering the residues , we computed a further covariance matrix .

Finally, we produced a dataset by removing the contribution of the largest eigenvector of the matrix . This can be done by zeroing the largest eigenvalue of , as discussed in Ref. Stanley . An alternative method, which we prefer, is that of removing the “optimal” factor, which is obtained by minimizing

on , and . The residues resulting from this operation coincide with the time-series obtained from by subtracting the leading contribution of its singular value decomposition. We call the correlation matrix of the residues .

In summary, we consider the original time-series (set ), the one obtained subtracting the average market return (set ) and those obtained from the residues of a one factor model with the market index (set ), the average market return (set ) and the optimal factor (set ). Set represents a case where the market mode is exogenously determined whereas in sets and it is determined by the data itself. This allows us to understand how much an index, such as SP500 which is a weighted average, accounts for the collective dynamics of the market.

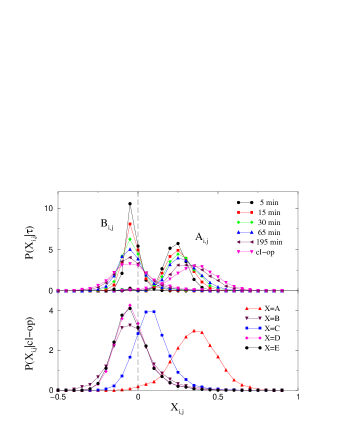

The distribution of matrix elements is shown in Fig. 1 as a function of time-horizon (top, for the sets and ) and for different datasets at the intraday time-horizon. We observe that the distribution spreads out as the time-horizon increases, as a manifestation of the Epps effect. However, while the distribution of is centered around a positive value, that of correlations of derived datasets is peaked on values close to zero and is narrower. For set ( and ) the peak is at slightly negative values, whereas for set it occurs at positive values. This suggests that the removal of correlations is more efficient when the single factor is computed from the data. This already shows that the dynamics of the mean already explains the correlations better than the market index.

We also find that intraday and overnight returns have distinctly different distribution of correlation coefficients. This difference is particularly pronounced in dataset which again suggest that the market index is even less explicative of the market’s collective behavior at these scales.

Correlation and were found to have a distribution which is similar to that of . This anticipates a generic conclusion: the subtraction of a global component from the dynamics is most meaningful when it eliminates (either implicitly as in or explicitly as in ) the market mode by setting the corresponding eigenvalue to zero.

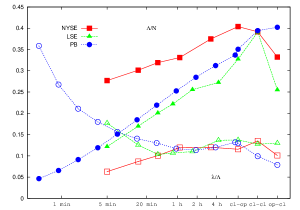

Before analyzing the structure of correlations, it is of interest to provide some estimate of the relative strength of global correlations and of noise in the correlation matrices . Fig. 2 plots the share of correlation carried by the largest eigenvalue (which is , by normalization) for NYSE, LSE and PB, as a function of time-horizon . As a manifestation of Epps effect epps , this increases with in a way which is reasonably well approximated by a logarithmic growth. The ratio of the second largest eigenvalue to the largest, which could be taken as a measure of the relative strength of inter-asset correlations against global correlations, has a declining trend with for small time-horizons and then saturates at around .

III Data Clustering

We performed data clustering analysis following the method of Ref. giada . Here we only sketch the basic idea of the method and we refer the interested reader to Ref. giada for details. In brief, assume we wish to cluster standardized 111The time series are derived from by normalization to zero average and unit variance. E.g. . time series in groups having a similar dynamics. First we assign a cluster label to each time series, specifying which cluster it belongs to. Then we assume that is generated according to the model

| (8) |

where and are independent gaussian variables with mean zero and unitary variance. Here describes the component of the dynamics which is common to all time series with whereas describes idiosyncratic fluctuations. Eq. (8) is consistent with a correlation matrix which has a block diagonal structure for : if and otherwise. The parameters entering Eq. (8) as well as the cluster structure can be determined by maximum likelihood estimation. Approximate maximization of the log-likelihood can be done following an hierarchical clustering procedure 222We choose this simple option, rather than more elaborate maximization procedures based e.g. on simulated annealing, because for the data sets used the optimal configuration we find depend only marginally on the algorithm used.: start with clusters, each composed of a single asset (). From the configuration with clusters, compute the log-likelihood of all configurations obtained by merging two clusters. The configuration with clusters is the one corresponding to the maximal log-likelihood . This operation can be iterated with going from to , and the optimal configuration can be chosen as that for which is maximal. This also predicts the optimal number of clusters which describes our dataset. This method has already been used to analyze stock market data: in Refs. giada the emergent clusters were found to be highly correlated with economic activity. Furthermore the method was extended to perform noise undressing. In Ref. states the method has been applied to investigate market dynamics, showing that well defined recurrent states of market wide activity can be defined.

Here we apply this method to investigate how the structure of market’s correlations evolves as the time lag increases from the high-frequency range to the daily scale. We shall first focus on NYSE and then discuss the differences found in other markets.

III.1 NYSE

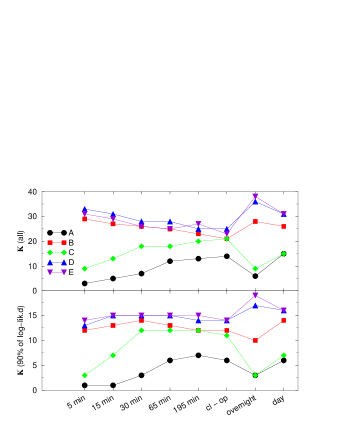

Fig. 3 shows the evolution of the number of clusters with the time-horizon for the different datasets in the NYSE. For we find fewer clusters then with other methods and the number of clusters increases with . This is consistent with results of Refs. blm01 which observe an evolution of the structure of correlations, where more and more details are added as the time-horizon increases. The other datasets, however, reveal that this is due to the fact that includes the correlations induced by the common factor. When this is removed, as for and , we find that the number of clusters which accounts for most of the log-likelihood is remarkably stable from the 5 min to the intraday scale. When the S&P500 index is removed from the data (), we find a fast evolution of the structure between 5 min and 30 min and then the number of clusters saturates to a constant level. Again, in all cases, a significant variation takes place in the overnight and hence at the daily (cl-cl) scale.

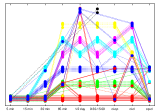

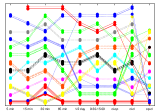

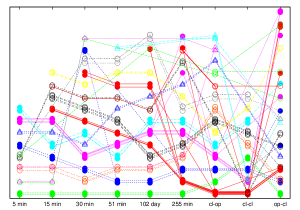

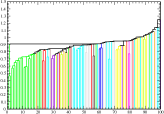

A closer view on the evolution of the cluster structure is presented in Figs. 4. This plots the cluster label as a function of , for each asset belonging to clusters accounting for 90% of the log-likelihood 333Labels are sorted with respect to their contribution to the log-likelihood. E.g. means that asset belongs to the third most relevant cluster at time-horizon .. Hence assets and belonging to the same cluster for all , follow parallel trajectories in the figure. In this representation, cluster splitting and merging can clearly be read off. In dataset and we see considerable splitting of clusters as we move from 5 min to the daily time-horizons. A substantial reshuffling and merging takes place when going to overnight returns. On the contrary, in dataset , and (not shown), cluster membership exhibits a remarkable stability at intraday scales: the vast majority of assets within a cluster at 5 min, follows the same “trajectory” across time-horizons. Some reshuffling takes place in the order of clusters, suggesting that the structure of correlations among sectors evolves with time-horizons. Again, the structure of overnight returns is considerably different.

| (%) | 5 min | 15 min | 30’ | 65 min | 195 min | cl-op | cl-cl | op-cl |

|---|---|---|---|---|---|---|---|---|

| A | 5 | 11 | 42 | 77 | 86 | 100 | 89 | 24 |

| B | 91 | 90 | 91 | 90 | 92 | 90 | 90 | 72 |

| C | 33 | 66 | 84 | 86 | 87 | 92 | 89 | 30 |

| D | 91 | 90 | 92 | 91 | 89 | 92 | 90 | 78 |

| E | 91 | 87 | 90 | 87 | 90 | 90 | 90 | 80 |

In order to make the comparison of different cluster structure quantitative, we have introduced an information distance between any two structures and . In words, this tells us how much the knowledge of the cluster label of a randomly chosen stock , yields information on the value of . Information is quantified by entropy reduction, in the following manner: Let be the fraction of stocks with for and be the fraction of stocks with , among those which have . From these, we can compute the entropies in the usual way and the conditional entropy

The information gain is then given by

| (9) |

Because of the normalization, a value of implies that yields a rather precise information on , so if we shall say that accounts for 80 % of the information contained in . Table 2 shows the values of (in %) between different cluster structures and that obtained from set at 1 day time-horizon. This shows that at this time-horizon, the cluster structure is essentially the same in the five datasets, with an overlap larger than 90 %. An overlap of the same order of magnitude attains for all intraday scales in sets and . Even though the overlap drops down as one moves to overnight returns, the difference is much smaller in sets and than in sets and . This suggests that, even though overnight returns have a structure which is markedly different from that of intraday returns, still removing the market mode allows one to reveal more invariant features.

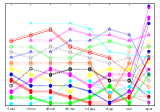

Such invariant features, we claim, are related to economic sectors. In order to support this, we compare the cluster structures with the classification of assets in the sectors of economic activity given in Table 1. The latter, yields a sector label for each stock , for which we can compute an information gain , as above, setting . Fig. 5 shows the behavior of for different datasets across time-horizons. This suggests that the most informative sets are those where the market mode is removed and these account for 80% of the information contained in . For these, the information content is remarkably constant across time-horizons. On the contrary, for set the information gain increases with in the intraday range, as if information on the economic activity of assets were ”released” gradually, as time-horizon increases. It is worth to remark that, for all datasets, overnight returns (specially for sets and ) carry much less information on the economic structure of the market, than intraday returns.

Hence, we conclude that in datasets and the evolution in the cluster structure is due to the interplay between the “center of mass” motion (i.e. the market mode) and the internal dynamics. Indeed when the latter contribution is subtracted from the data, as in datasets , and , we find that the structure of correlations is remarkably stable with the time-horizon. This is consistent with a notion of market’s informational efficiency by which information is incorporated very quickly in market’s returns. From the above analysis, we infer that the information on the relations between assets is efficiently incorporated in returns over time-horizons shorter than 5 min in NYSE.

III.2 Other markets

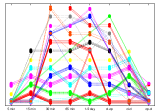

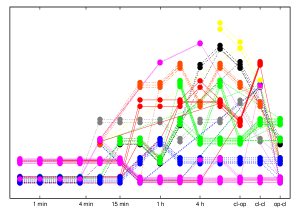

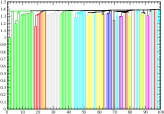

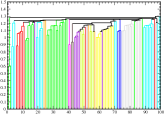

We have performed data clustering analysis also on LSE and PB data. Again we found that removing the market mode allows one to reveal the structure of correlations much more clearly. Indeed, while set is characterized by one or two clusters at intraday time scales, set are characterized by a richer structure, as shown in Figs. 6 and 7. In both cases, we see that a significant part of the structure forms at intermediate time-horizons of - minutes. In PB data, we pushed our analysis to ultra-high frequency, probing very short time scales. We found that for 5 min barely any structure can be seen in the correlation matrix. As for NYSE, we found that the cluster structure of set is poorly correlated with the classification of assets in economic sectors, whereas datasets and cluster in a way which reflects up to 70% of the (entropy of a) classification in economic sectors for LSE, and that this information content is roughly constant across time (intraday) scales.

As for the NYSE, we found that overnight returns have a cluster structure which is markedly different from that of intraday returns. Different markets, however, exhibit different patterns in this respect. While the LSE has a fragmented cluster structure of overnight returns similar to NYSE, PB shows a more compact structure.

In contrast with our findings on NYSE data, the cluster structure of set is now markedly different from that of other sets even at the daily scale. This suggests that the role of global correlation is much stronger in LSE and PB.

In order to compare different markets, we performed the Kolmogorov-Smirnov (KS) test NumRec on the distribution of cluster sizes. This provides a value for the hypothesis that two different samples and of cluster sizes can be considered as different populations drawn from the same unknown parent distribution. If this is not the case (i.e. is small), we can conclude that the two samples have a different structure, whereas if is close to one, we cannot reject the hypothesis that the two samples have the same structure. We found that LSE and PB have a cluster size distribution which is different from that of NYSE (), but which are remarkably similar one to the other ().

The similarity between LSE and PB, and their difference with NYSE, is also visible in the dependence of the largest eigenvalues on shown in Fig. 2. Remarkably, the market mode seems stronger in NYSE than in LSE and PB, whereas data clustering suggests the opposite.

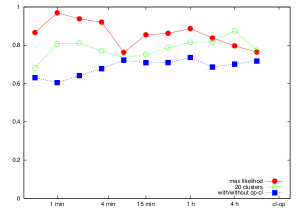

In the case of PB data, we also performed several tests in order to asses the sensitivity of our results on the inhomogeneity of trading activity. One may indeed think that particular times of the day, such as the opening or the closure of the market, peak or lunch break hours, might be characterized by different statistical properties. In order to test for these effect, we removed the first and the last 20 minutes of trading from the data in each day and considered the resulting correlation matrices . We computed the relative information between the maximum likelihood structures obtained in this way and the original ones, at different time scales . The result is that, for set of PB, at all roughly of the structure found in the whole dataset coincides with that obtained eliminating the opening and the closing period (see Fig. 8). An even stronger similarity () was found in NYSE between the structure of intraday correlations and those obtained from returns measured roughly minutes after opening and before closing. We conclude that a significant part of the structure is not affected by the activity at the market opening or at closure.

As a further test to check the effects of time inhomogeneity of trading activity, we compute correlation matrices in tick time for PB, over intervals of ticks, which correspond on average to the time scales used in real time (here a tick is defined as a transaction on any of the stocks considered). The results, shown in Fig. 8, suggest that the structure of market correlation is largely independent of the definition of time, as indeed roughly of the information found with real time is recovered using tick time.

IV Single Linkage Clustering Analysis

In this section we review the results obtained by applying the Single Linkage Clustering Algorithm (SLCA) to the data considered in section II. For each time-horizon considered, the SLCA allows to obtain a Hierarchical Tree (HT) and a Minimum Spanning Tree (MST), which give complementary information about the network structure of the considered set of stocks. Indeed, the HT gives a description of the hierarchical organization of the stocks, while the MST gives an indication about their topological organization. For a review of SLCA in the context of multivariate financial time series we refer to AdP ; Mantegna1999 ; EPJB2004 .

As much as in the previous section, here we apply the SLCA to the different datasets in order to investigate how the structure of market’s correlations evolves as the time-horizon increases from intraday scales to the daily scale. We shall first focus on NYSE and then discuss the differences found in other markets. The colors used in the representation of both the HTs and the MSTs refer to the classification is sectors of economic activity given in Table 1.

IV.1 NYSE

The investigation of NYSE data by using the SLCA reveals that the role of the “center of mass” in the structure of the correlation is twofold. On one side, the level of clustering in all the HTs in the sets where the “center of mass” is removed is at an higher distance than the corresponding HTs of set . Such effect is expected since, by removing the “center of mass”, the mean correlation is now approximately zero, as shown in Fig. 1. On the other side, the cluster structure seems now to be more evident than in the case of the original data.

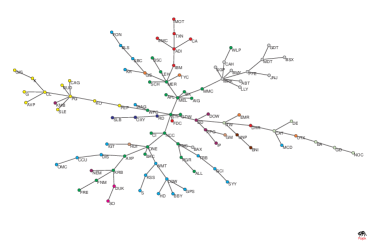

In Figs. 9 we present the data for set (top) and set (bottom) at the two extreme time-horizon of 5 min (left) and 1 at 1 day (right). Contrary to what we find in set (top left), the HT of set at 5 min time-horizon (top right) shows a significant level of structure that, additionally, is similar to the one found at 1 day (op-cl) time-horizon (bottom right).

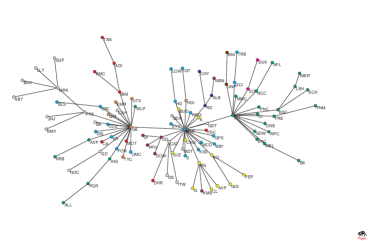

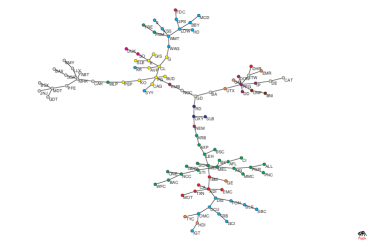

This is also confirmed by comparing the structure of the MST in sets and set . The 5 min MST of set shows a typical structure with a few hubs characterized by an high degree (Fig. 10). The 1 day (op-cl) MST of set indicates that the number of hubs has increased, reflecting the progressive organization of stocks according to their sectors of activity as time-horizon increases (Fig. 11). The MSTs shown in Figs. 12 and 13 for set are markedly different from the corresponding ones for set . No preminent hub is traceable in the two MSTs. In addition, they have a structure which is remarkably similar one another, to the extent that one could not say which is which, on the basis of their statistical structure alone.

In order to quantify the difference between the structure of the MSTs of different datasets at different time-horizons, we performed the Kolmogorov-Smirnov (KS) test NumRec on the degree distributions of MSTs. The results for different sets are collected in table 3 and it largely confirms the conclusions based on visual inspection of Fig. 10 – 13. First, we see that the structure of the MSTs at the extremes of the intraday scale range are markedly different in set and become increasingly similar as we move to set . Second, Table 3 shows that the structure of set is similar to that of other sets at the same time-horizon at day (op-cl), but this is not true at smaller time-horizons.

We also compared the MSTs with random MST (r-MST) generated by uncorrelated random walks of the same length. This reveals that, apart from set , we are not able to detect any statistical feature in the degree distribution which differentiates the MSTs of sets and at day (op-cl) from those generated by pure noise. Even the diameter of the MSTs is not able to discriminate them from those generated by pure noise. However, the similarity of MSTs with r-MST disappears for larger datasets of or stocks of NYSE, for which KS yields values of for all sets, at both 5 min and 1 day (op-cl). Furthermore, MSTs turn out to be considerably more compact than r-MSTs. For example, we find that with the r-MST have a diameter of whereas at 1 day (op-cl) the largest value of the diameter is for set . Finally, in the case of stocks, for set , set , set and set we have also performed the KS test in order to compare the degree distribution of the MSTs at 5 min and 1 day (op-cl). Such tests confirm the result of Table 3, valid for stocks, that the degree distributions are essentially indistinguishable, with p-values which are close to zero. Hence, we conclude that the removal of the “market mode” generates residues whose MSTs still contain non-trivial statistical features, although these are not clearly observable in the case of assets. When considering a larger set, say , the noise threshold lowers enough to reveal a topological organization which is different from the one associated to uncorrelated random walks.

| , | 0.031 | 0.677 | 0.961 | 0.992 | 1.000 |

| 1.000 | 0.047 | 0.021 | 0.001 | 0.000 | |

| 1.000 | 0.794 | 0.894 | 0.677 | 0.794 | |

| , | 0.000 | 0.443 | 0.677 | 0.794 | 0.992 |

| , | 0.556 | 1.000 | 1.000 | 1.000 | 1.000 |

| , | 8 | 17 | 16 | 23 | 23 |

| , | 15 | 26 | 22 | 22 | 25 |

In Fig. 14 we show the HTs relative to set A (left) and set E (right) in the case when the overnight time-horizon is considered. The structure of such trees is different form the ones at intraday time-horizons. In particular, for set A, the HT of Fig. 14 shows that some stocks are highly correlated with each other. However, the organization in economic sectors of activity is less marked than in the corresponding HT at daily time-horizon, see Fig. 9. Such effect is also observable when considering set E, i.e. the right panel of Fig. 14. Here the average level of correlation increases, as expected. It is therefore evident that at the overnight time-horizon the organization of stocks in clusters is different than at intraday time-horizons, i.e. when the market is open.

We have seen above that when removing the market mode the topology of the MSTs has no specific statistical features, even though the distribution of stocks on them is definitely not random. Indeed the cluster structure seen in HTs (Fig. 9) correspond to the fact that companies belonging to the same economic sector appear clustered in the same region of the MST. Again, this shows that the removal of the “center of mass” reveals the organization in sectors of activity already at such a small time-horizons as 5 min. It is worth remarking, though, that the location of sectors themselves along the tree is different at 5 min and at the intraday scale. In other words, the intra-sector structure evolves in time, while the sector composition remains stable.

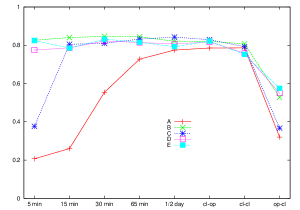

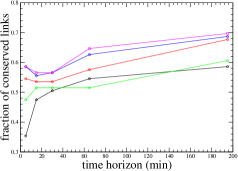

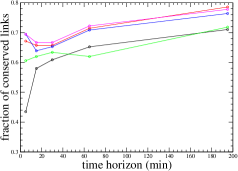

In order to give a quantitative description of this effect, for each set and at each time-horizon we have measured the fraction of the MST links that are conserved with respect to the open-to-close case. The results are reported in Fig. 15. The top panel refers to the case when all links in the MST are considered. The other two panels refer to the case when we also use the information about the economic sectors of activity, see Table 1. In particular, we consider only intra-sector links (middle panel) or only inter-sector links (bottom panel). Ideally, for a better quantitative description we should have considered clusters rather than economic sectors. Unfortunately, the SLCA does not allow a precise identification of what a cluster is. However, in Fig. 5 it is shown that there exists a strict relation between economic sectors and the clusters obtained by using the methodology of Ref. giada . We here somehow make the ansatz that such strict relation persists also in the clusterization given by the SLCA.

In the case when we consider all links (top) or only those between stocks in the same sector (middle), in all the cases but one, when the center of mass has been removed, the fraction of conserved links is higher than for set . The middle panel of Fig. 15 shows that 70-80% of the MST links between stocks belonging to the same economic sector are conserved with respect to the open-to-close case, whereas a much smaller fraction is conserved between stocks belonging to different economic sectors. This is consistent with our observation that while sector composition remains stable, intra-sector correlations evolve with the time-horizon. Moreover, such results are also consistent with the ones shown in Fig. 5 that the amount of economic information contained in the clusters is constant.

In this respect, the botton panel of Fig. 15 shows that set and set reveal better than the others the topogical organization within different economic sectors at all time-horizons. Finally, it is worth remarking that set , where the market mode is exogenously given by the SP500 index, gives results which are comparable with those of set .

By summarizing, the investigation of sets , , , and by using the SLCA shows that (i) the removal of the “center of mass” reveals the organization of the sectors within different economic sectors even at small time-horizons and (ii) this is better achieved in set and set , where the “center of mass” is endogeneously obtained either by miminizing the function of Eq. II or by using a mere return market average. Finally, we find that the degree distributions of the MST at different time-horizons are statistically the same, specially in set , according the the Kolmogorov-Smirnov test, but they cannot be distinguished from those of a set of independent random walks, for such a small market (). The distribution of stocks on the MST reflects the organization of stocks in economic sectors, and indeed links between companies in the same sector are “conserved” across time scales.

IV.2 Other markets

The question arises whether the above results have some degree of universality or they are peculiar to the NYSE market. We have therefore repeated the above investigations for different markets, i.e. for LSE, PB and BI. Generally we confirmed the main conclusions: We find that HT of sets and reveal better the organization of stocks in economic sectors than set , and that the structure of HTs for the formers is less dependent on the time-horizon than for the latter. The structure of MSTs has a clear evolution in set as the time-horizon increases (e.g. KS test yields for the degree distributions of MSTs of set between 5 min and 1 day), whereas it has a remarkably stable structure in the other sets (particularly for set , for which between 5 min and 1 day). A comparison of the MST for set for NYSE and LSE yields a KS test value of for all time-horizons . Similar results were found comparing NYSE and PB or BI MSTs. This invariance of the structure of MSTs for set across markets and time-horizons should not be considered as an indication of universality, though. Indeed, as for NYSE, this invariant structure is indistinguishable from that of r-MSTs generated from uncorrelated random walks. Hence, what this allows us to conclude is that markets of such small sizes do not allow to make statements on the similarity of market topology in terms of their MSTs. Indeed, the topology of MSTs for stocks or less, is dominated by noise.

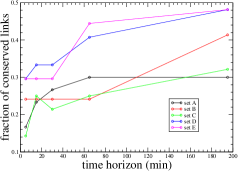

When the market is open, the disposition of stocks on the MSTs, as in NYSE, is consistent with economic classification, across time-horizons. In Figs. 16 we report, for different sets and at each time-horizon, the fraction of the MST links that are conserved with respect to the open-to-close case for LSE (left) and PB (middle) and BI (right). Again, we consider all the links (top), only intra-sector links (middle) or only inter-sector links (bottom). As much as in the NYSE case, the sectors considered here are the economic sectors of activity mentioned above. In the case of LSE data the results are less sharp than in the NYSE case. Set , set and set give results which are more similar to each other with respect to the NYSE case. One possible exception is given by set at 5 min time-horizon. In all cases, it is confirmed that the removal of the “market mode” reveals the organization of stocks in economic sector already at small time-horizons. As an example, the fraction of conserved intra-sector links in set is always ranging between and , while in set such percentage drops to at the smallest time-horizon. At larger time scales. however, the fraction of conserved links for set has roughly the same value that for other sets. This is different from what we found for NYSE, where the fraction of conserved links were systematically smaller for set than for other sets.

When considering the overnight time-horizon, we confirm that the organization of stocks in economic sectors of activity is less evident than in the case when the market is open. However, such differences are less marked than in the NYSE case.

V Conclusions

We found that removing the dynamics of the center of mass i) decreases the level of correlations and ii) makes the cluster structure more evident. Naïvely one would expect that reducing the level of correlations reduces the “signal” and hence enhances the role of noise in the dataset. On this ground, one might expect a less sharply defined structure, i.e. the opposite of ii). The fact that we observe i) and ii) implies that the market mode dynamics bears little or no information on the market structure. It also suggests that the market mode dynamics and the dynamics of “internal coordinates” are to a large extent separable, in much the same manner as in particle systems of classical mechanics, where the center of mass dynamics accounts for the effect of external forces, whereas relative coordinates respond to internal forces arising from inter-particle potentials.

It is not difficult to imagine components of trading activity which might contribute to the dynamics of the “center of mass” or to relative coordinates. It is worth to remark, in this respect, that a simple phenomenological model for the dynamics of the market mode, taking into account the impact of trading in risk minimization strategies, has been recently proposed pfolio . Besides reproducing the main statistical properties of the dynamics of the largest eigenvalue of the covariance matrix, this model also shows that the behavior of the market mode is largely insensitive to a finer structure of correlations. The invariance of the structure of “internal” correlations across time scales, and its similarity with economic classification, instead suggests that the dynamics of relative coordinates might be related to the ways in which information on different assets diffuses in the market.

The finding of a scale-invariant correlation structure is non-trivial, in several respects. First, its origin suggests a fine balance between signal and noise across time-horizons: On one hand, the growth of correlations implicit in the Epps effect implies that the “signal” gets stronger as the time scale increases. On the other, random matrix theory suggests that the strength of “noise” due to finite sampling, is more severe at large time-horizons than at short ones. Indeed, the length of the time series decreases as , which implies a spread in the eigenvalues due to noise dressing. This latter effect allows us to detect weak correlation structures with an high precision at small time scales.

Secondly, the scale invariance of correlation structure might have important implications for risk management, because it suggests that correlations on short time scales might be used as a proxy for correlations on longer time-horizons. If the structure of correlations at short time scales can be computed using shorter time series, this might allows us to detect structural changes more efficiently.

Finally, uncovering the dynamical origin of such a complex phenomenology poses exciting challenges to theoretical modeling of multi-asset markets.

VI Acknowledgments

Authors acknowledge support from research projects MIUR 449/97 “High frequency dynamics in financial markets”, M.M. acknowledges support from EU-STREP project n. 516446 COMPLEXMARKETS. S. M. acknowledges support from MIUR-FIRB RBNE01CW3M “Cellular Self-Organizing nets and chaotic nonlinear dynamics to model and control complex systems”, from the EU-STREP projects n. 012911 “Human behavior through dynamics of complex social networks: an interdisciplinary approach”. We wish to thank Dr. Claudia Coronnello for assistance in the preparation of data.

References

- (1) J.-P. Bouchaud, M. Potters Theory of financial risk and derivative pricing: from statistical physics to risk management (Cambridge University Press, Cambridge, 2003).

- (2) R. Mantegna, E. Stanley, Introduction to Econophysics (Cambridge University Press, 1999).

- (3) L. Laloux, P. Cizeau, J.-P. Bouchaud, M. Potters, Phys. Rev. Lett., 83 (7) 1467-1470, (1999).

- (4) V, Plerou, P. Gopikrishnan, B. Rosenow, L. A. N. Amaral, H. E. Stanley, Phys. Rev. Lett., 83 (7) 1471-1474, (1999).

- (5) G. Bonanno, G. Caldarelli, F. Lillo, R. N. Mantegna Phys. Rev. E, 68 (4) 046130, (2003).

- (6) L. Giada, M. Marsili, Phys. Rev. E, 63 (6) 061101, (2001); Physica A, 315 57-71, (2002).

- (7) M. Marsili, Quant. Fin., 2 297-302, (2002).

- (8) J.-P. Onnela, A. Chakraborti, K. Kaski, J. Kertesz, A. Kanto, Phys. Rev. E, 68 (5) 056110, (2003).

- (9) J. Kwapien, S. Drodz, J. Speth, Physica A, 337 231-242, (2004).

- (10) M. Potters, J.-P. Bouchaud and L. Laloux, J. Stat. Mech., P08010 (2005)

- (11) T.W. Epps, J. Am. Stat. Assoc., 74 291, (1974).

- (12) G. Bonanno, F. Lillo, R.N. Mantegna, Quantitative Finance, 1, 96 (2001).

- (13) C. Coronnello, M. Tumminello, F. Lillo, S. Miccichè, R. N. Mantegna, Acta Physica Polonica B, 36 (9) 2653-2679, (2005); M. Tumminello, T. Di Matteo, T. Aste, R.N. Mantegna, DOI: 10.1140/epjb/e2006-00414-4; M. Tumminello, C. Coronnello, F. Lillo, S. Miccichè, R. N. Mantegna, e-print physics/0605251.

- (14) www.nysedata.com

- (15) M. M. Dacorogna, R. Gencay, U. A. Müller, R. B. Olsen, O.V. Pictet, An Introduction to High-Frequency Finance, Academic Press (2001).

- (16) www.rebuildorderbook.com

- (17) www.euronext.com

- (18) www.borsaitaliana.it

- (19) W.H. Press, S.A. Teukolsky, W.T. Veterling, B.P. Flannery, Numerical Recipes in Fortran: the art of scientific computing, (Cambridge University Press, Cambridge, 2nd Ed., 1992).

- (20) R.N. Mantegna, Eur. Phys. J. B 11, 193 (1999).

- (21) G. Bonanno, G. Caldarelli, F. Lillo, S. Miccichè, N. Vandewalle, R.N. Mantegna, Eur. Phys. J. B, 38 363, (2004).

- (22) G. Raffaelli, M. Marsili, JSTAT L08001 (2006).