Correlation of coming limit price with order book in stock markets

Abstract

We examine the correlation of the limit price with the order book, when a limit order comes. We analyzed the Rebuild Order Book of Stock Exchange Electronic Trading Service, which is the centralized order book market of London Stock Exchange. As a result, the limit price is broadly distributed around the best price according to a power-law, and it isn’t randomly drawn from the distribution, but has a strong correlation with the size of cumulative unexecuted limit orders on the price. It was also found that the limit price, on the coarse-grained price scale, tends to gather around the price which has a large size of cumulative unexecuted limit orders.

keywords:

Limit order , Order book , Stock market , Data analysisPACS:

07.05.Kf , 89.65.Gh1 Introduction

The fat tail of the price fluctuation and the long memory of the volatility are common features observed in financial markets employing the continuous double auction as the mechanism for price formation [1, 2, 3, 4]. The origin of such features is an important problem to be solved in econophysics and finance, and still under debated. Many models that give rise to one of those or both features have been proposed [5].

Among those models, Maslov has studied a simple model of markets driven by continuous double auctions [6]. In his model, traders choose one from the two types of orders at random. One is a market order to sell or buy at the best available price at the time when the trader places the order. The other is a limit order to sell or buy with the specification of the limit price, which is the worst allowable price for the trader. A new limit order to sell (buy) is placed above (below) the current market price with a random offset drawn from a uniform distribution in a given interval. The size of order is fixed for simplicity. Numerical simulation has shown that the distribution of the price fluctuation generated by this model has a power-law tail, and the volatility has a long range correlation. Although his model has some unsatisfactory details about the statistics of the price fluctuation [7], the approach of microscopic market models to this problem is convincing, because they describe the actual process of price formation from the ultimate microscopic description level. Several authors have proposed the market models in the same class [8, 9, 10].

The way traders select a limit price is random and non-strategic in Maslov’s model. It is a simplification of the actual way of traders to select a limit order. In the paper [10], traders are assumed to be mimetic, and prefer the limit price which has a large stock of limit orders, when they place limit orders. Incorporating this tendency of coming limit price into the microscopic model of stock market, the author reproduces the price fluctuation with the more real statistics depending on the parameter of the model.

In this paper, we empirically examine the correlation of the limit price with the condition of order book at the time when a limit order comes. We analyze the Rebuild Order Book of Stock Exchange Electronic Trading Service (SETS), which is the centralized order book market of London Stock Exchange. As a result, the selected limit price is broadly distributed according to a power-law, and it isn’t randomly drawn from the distribution, but has a strong correlation with the size of cumulative unexecuted limit orders on the price. It was also found by the price scale transformation of the conditional probability that the limit price, on the coarse-grained price scale, tends to gather around the price which has a large size of cumulative unexecuted limit orders.

2 Rebuild Order Book and our data

We analyze the Rebuild Order Book of SETS. In this section, we give a brief description of the Rebuild Order Book and our data. SETS is fully automated order book trading service of London Stock Exchange [11]. The order book holds details of all orders. A coming new order to sell or buy will be fully or partially executed against existing orders on the order book, if both requirements agree. The unexecuted portion of the order will be stored on the order book. The Rebuild Order Book is composed of 3 files. Order detail file contains details of new orders, their prices, sizes and so on. Order history file contains a history of each order and the method by which it is removed, that is, deletion, expiry, partial match and full match. Trade report contains details of every trade, that is, the price, the size and so on. Merge of these files and sort of records by the time stamp enable us to pursue the occurrence and the change of each order.

We study the Rebuild Order Book of the 6 months since July to December in 2004. Our data contains all orders and transactions of the selected 13 stocks listed on SETS. The selected stocks are most actively traded in the period, which are the stocks of top 13 bargains in July 2004. There are millions of limit orders, cancellations and executions in our data. The stocks we analyzed are Astrazeneca (AZN), Barclays (BARCS), BT Group (BT), BP. (BP), Diageo (DGE), Glaxosmithkline (GSK), HBOS (HBOS), HSBA HLDGS (HSBA), Lloyds Tsb Group (LLOY), Shell Tranport & Trading Co. (SHEL), Tesco (TSCO), Royal Bank Scot (RBS) and Vodafone Group (VOD), belonging to various industries, that is, bank, beverages, oil & Gas, telecommunication services and so on.

3 Results of data analysis and discussions

The purpose of this paper is to examine the correlation of the limit price with the condition of order book at the time when a limit order comes. In this section, we report some results of analysis on the data described in the previous section.

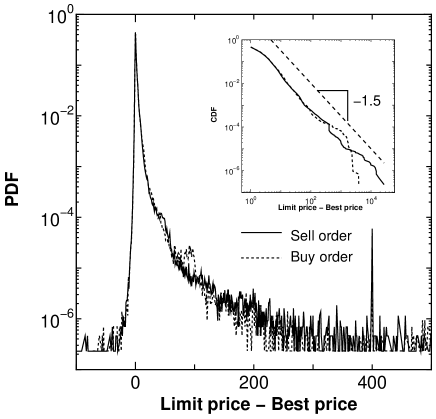

First of all, we show that the coming limit price is broadly distributed around the best price at the time when the order comes. Figure 1 is the semi-log plot of the probability distribution function of relative limit price: (for sell limit orders), (for buy limit orders). The unit of price is the tick size of each stock. The inset is the log-log plot of the cumulative distribution function for limit orders placed on the book. The exponent of the power-law tail of the relative limit price for orders placed on the book is near -1.5, and the value is consistent with the previous work of this kind [12].

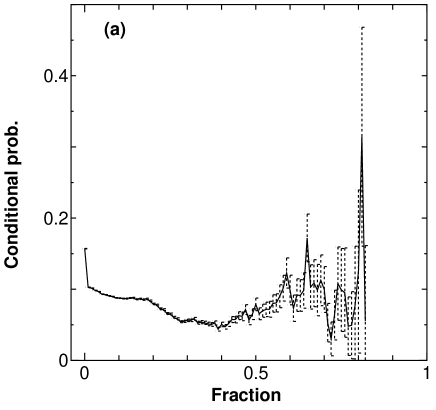

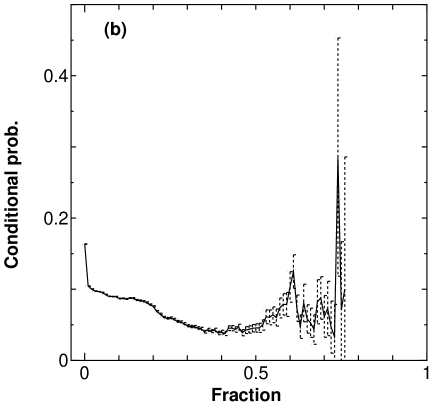

Second, we examine the correlation of the selection of limit price with the cumulative size of unexecuted limit orders at each price. Let us consider a situation of the order book. There may be several prices at which unexecuted limit orders are stored. Each price may hold a fraction of whole unexecuted orders. Then, which price will be selected as a coming limit price? Figure 2 shows the conditional probability that a coming limit order is placed at the price holding a given fraction of all limit orders. In both sides of order, The conditional probability decreases with fraction while is smaller than about 0.4, and increases with while is smaller than about 0.6. The cumulative size of unexecuted limit orders at each price influences the probability of the selection of the price. However, the conditional probability is not a monotonically increasing function of .

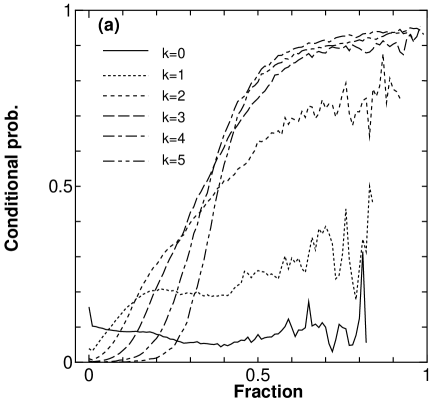

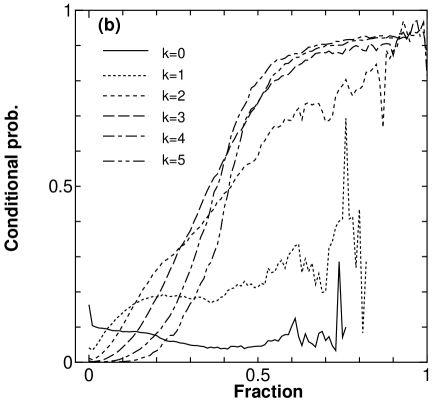

Next, we perform the scale transformation of price, and renormalize the conditional probability. We group the relative price and into the group , where the relative price is defined by the equation and for sell and buy orders respectively. On the coarse-grained price scale, we call the group the best price (ask/bid), and the group the relative price again. Repeating this procedure k-times, we have the scale transformation of the relative price, . When the stochastic variable denote the cumulative size of limit order at the price and the binary stochastic variable the selection of the price , the renormalization of the conditional probability for each price is defined by the equation:

| (1) |

The conditional probability , on the coarse-grained price scale, is expressed by the weighted average . The results for to ( means the original price scale) are shown in Fig. 3. On the coarse-grained price scales , the conditional probabilities are monotonically increasing function of . It means that the limit price, on the coarse-grained price scale, tends to gather around the price which has a large size of cumulative unexecuted limit orders.

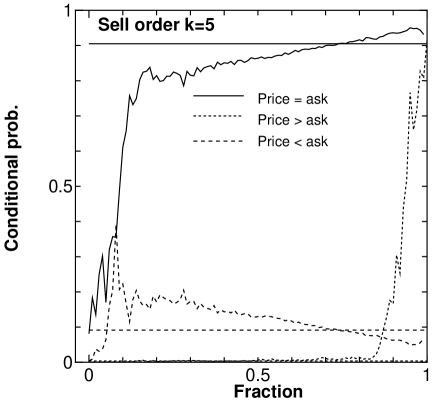

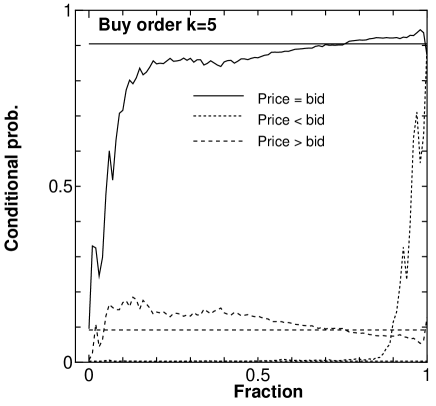

Finally, we study the dependency of the conditional probability on the relative price . We divide the whole prices into three groups, (the best price), (prices on the book) and (prices in the spread), and derive the corresponding conditional probabilities , and . The conditional probability is derived from the equation . The results for sell and buy order on the price scale () are shown in Fig. 4. The unconditional probability that traders select the group is also shown by the horizontal line. On this coarse-grained price scale, each price contains 32 original price levels. In the region of close to 1, the conditional probability that traders select the prices separate from the best price by over 32 original price levels is hundreds times as large as the unconditional probability, which is tiny. In the region , the inequality holds, which means the state such that the stored limit orders are sparse within the distance of 31 original price levels from the best price is stable. As is shown by the simulation in the paper [10], such unequal attractive power of prices has amplified the fluctuation of gaps between occupied price levels, and cause the power-law fluctuation of price changes and the long memory of the volatility. This result agrees with the statement by Farmer et al. in the paper [13]. They has argued that large returns are not caused by large orders, while the large gaps between the occupied price levels on the order book lead to large price changes in each transaction.

4 Conclusions

We have analyzed the Rebuild Order Book of SETS, which is fully automated order book trading service of London Stock Exchange in order to examine the correlation of the limit price with the condition of order book at the time when a limit order comes.

We have found that there is a obvious correlation. Especially on the coarse-grained price scale, our data clearly shows that the limit price tends to gather around the price at which a large size of unexecuted limit orders has been stored. Such unequal attractive power of prices is a promising candidate for the origin of the fat tail of the price fluctuation and the long memory of the volatility.

This work was supported by the Japan Society for the Promotion of Science under the Grant-in-Aid, No. 15201038.

References

- [1] P. Gopikrishnan, M. Meyer, L. A. N. Amaral and H. E. Stanley, Inverse Cubic Law for the Distribution of Stock Price Variations, Eur. Phys. J. B 3 (1998) 139.

- [2] V. Plerou, P. Gopikrishnan, L. A. N. Amaral, M. Meyer, H. E. Stanley, Scaling of the distribution of price fluctuations of individual companies, Phys. Rev. E 60, (1999) 6519.

- [3] Y. Liu, P. Gopikrishnan, Cizeau, Meyer, Peng, H. E. Stanley, Statistical properties of the volatility of price fluctuations, Phys. Rev. E 60, (1999) 1390.

- [4] Cont, R., Empirical properties of asset returns: stylized facts and statistical issues, Quantitative Finance 1 (2001) 223.

- [5] J.-P. Bouchaud, M. Potters, Theory of Financial Risk and Derivtive Pricing, 2nd edition, Cambridge University Press, Cambridge, 2003 and references therein.

- [6] S. Maslov, Simple model of a limit order-driven market, Physica A 278 (2000) 571.

- [7] ¡ltx:note¿T¡/ltx:note¿he exponent of the power-law tail of price fluctuations generated by Maslov’s model is inside the Levy stable region, while the observed value in actual markets is close to -3 [1, 2]. In addition, the Hurst exponent of the price diffusion is H = 1/4 ( under diffusive) , regardless of the range of time window. In actual markets, we have H = 1/2 for long-term, which is the value for free diffusion.

- [8] D. Challet, R. Stinchcombe, Non-constant rates and over-diffusive prices in a simple model of limit order market, Quantitative Finance 3 (2003) 155.

- [9] E. Smith, J. D. Farmer, L. Gillemot, S. Krishnamurthy, Statistical theory of the continuous double auction, Quantitative Finance 3 (2003) 481.

- [10] J. Maskawa, Stock price fluctuations and the mimetic behaviors of traders, 2006, http://arXiv.org/abs/physics/0607202.

- [11] London Stock Exchange, Guide to Trading Services, 2006, available at http://www.londonstockexchange.com/.

- [12] I. Zovko, J. D. Farmer, The power of patience: a behavioral regularity in limit-order placement, Quantitative Finance 2 (2002) 387.

- [13] J. D. Farmer, L. Gillemot, F. Lillo, S. Mike, A. Sen, What really causes large price change?, Quantitative Finance 4 (2004) 383.