On the strategy frequency problem in batch Minority Games

A De Martino1, I Pérez Castillo2,3, and D

Sherrington3CNR-INFM, Dipartimento di Fisica, Università di

Roma “La Sapienza”, p. le A. Moro 2, 00185 Roma, Italy

Dipartimento di Fisica, Università di Roma “La

Sapienza”, p. le A. Moro 2, 00185 Roma, Italy

Rudolf Peierls Centre for Theoretical Physics,

University of Oxford, 1 Keble Road, Oxford, OX1 3NP, United Kingdom

andrea.demartino@roma1.infn.it,isaac@thphys.ox.ac.uk,

d.sherrington1@physics.ox.ac.uk

Abstract

Ergodic stationary states of Minority Games with strategies per

agent can be characterised in terms of the asymptotic probabilities

with which an agent uses of his strategies. We propose

here a simple and general method to calculate these quantities in

batch canonical and grand-canonical models. Known analytic theories

are easily recovered as limiting cases and, as a further

application, the strategy frequency problem for the batch

grand-canonical Minority Game with is solved. The

generalization of these ideas to multi-asset models is also

presented. Though similarly based on response function techniques,

our approach is alternative to the one recently employed by Shayeghi

and Coolen for canonical batch Minority Games with arbitrary number

of strategies.

1 Introduction

The mathematical theory of Minority Games (MGs) with strategies

per agent, particularly for what concerns their ergodic behaviour,

largely rests on the possibility of separating the contribution to

macroscopic quantities coming from “frozen” agents from that of

“fickle” ones [1, 2]. Frozen agents are those who use

just one of their strategies asymptotically, whereas fickle agents

flip between their strategies even in the steady state. That these

two groups have different impact on the physical properties of MGs is

clear if one thinks that frozen agents are insensitive to small

perturbations and thus they do not contribute to the susceptibility of

the system. More generally, when agents dispose of strategies

each, the relevant quantity to calculate is the probability with which

an agent uses of his strategies (),

knowledge of which provides all interesting physical observables. On

the technical level, this is a rather complicated problem that has

been tackled only recently in [3] for the canonical

-strategy batch MG. Here we propose an alternative method to

derive the desired statistics in generic canonical or grand-canonical

[4] settings with strategies per agent. This approach has

the advantage of being simpler from a mathematical viewpoint and, as

we will show, easily exportable to other versions of the MG. As in

[3], we resort to path-integral techniques, allowing for a

description of the multi-agent dynamics in terms of the behavior of a

single, effective agent subject to a non-trivially correlated noise.

The central idea of the method we propose is to exchange the

integration over the effective noise for one over frequencies using a

simple invertible mapping from one set of variables to the other and

the transformation law of probability distributions. We show that

available theories are easily recovered in known cases and, as a

further application, solve the strategy frequency problem for the

grand-canonical MG with . Since a similar issue arises in the

context of multi-asset MGs [5], we also discuss the

(straightforward though heavier from a notational viewpoint)

generalisation of this idea to models in which traders may invest in

assets.

Since path integrals are by now a somewhat standard technique to deal

with MGs, we shall skip mathematical details and focus our analysis on

the resulting effective dynamics and specifically on the strategy

frequency problem. Moreover, we shall reduce the discussion of the

economic meaning of the model to the minimum. The interested reader

will find extensive accounts in [1, 2, 6].

2 Model definitions, TTI steady states and the strategy frequency problem

We consider a market for a single asset with agents, labeled by

. At each time step ,

agents receive an information pattern

chosen randomly and independently with uniform probability and, based

on this, they formulate their bids (represented simply by a variable

encoding the agent’s decision, e.g. to buy or sell the asset). The

most interesting phenomenology is obtained when scales linearly

with ; their ratio, denoted as , is the model’s main

control parameter. Every agent disposes of trading strategies

, each prescribing a binary

action , drawn randomly and uniformly, and

independently for each strategy and pattern . The performance

of every strategy is monitored by a score function

which is updated by

(1)

Here, are real constants representing positive or

negative incentives for the agents to trade, with a factor

ensuring a non-trivial behavior in the limit .

is instead the (normalized) excess demand at time ,

(2)

where is the bid formulated by agent at time

. If we denote by the strategy chosen by at

time , then the bid submitted by is given by

(3)

The terms impose that the

agent performs the action dictated by his selected strategy. The term

, with

, denotes a filter linked to the score of

the selected strategies. We focus our attention on two cases:

•

Taking to be the Heaviside function, one has

so that the filter consists in either submitting

( for ) or not submitting

( for ) the bid. This version of

the game is usually called grand-canonical MG [4].

•

If , the filter is absent and agents are forced to

play no matter how bad their scores perform. This corresponds to the

standard canonical MG.

It remains to describe how is chosen. We assume

generically that at each time step agent employs a rule described

by a function , namely

(4)

For example, the standard MG with corresponds to . (This generalises easily

to the case of traders with decision noise [7].) At this

stage, we assume that the ’s are chosen randomly and

independently across agents (from some distribution) and introduce the

density of the mappings as

(5)

with a functional Dirac delta. A similar random

choice is made for incentives (albeit in general with a different and

uncorrelated distribution) and we define their density as

(6)

with .

We will work out the ‘batch’ version of the model, which is obtained

by averaging (1) over information patterns

[8]. After a time re-scaling (we denote the re-scaled time as

), one obtains the ‘batch’ dynamics

(7)

where is a (small) external perturbation added for

later use. In dynamical studies, one is interested in the average bid

autocorrelation function

(8)

and in the average response function

(9)

where and denote, respectively,

averages over paths and disorder. Assuming that

for all , in the limit the

multi-agent dynamics (7) can be described in terms of a

self-consistent stochastic process for a single, effective agent

endowed with strategies, characterized by score functions

, “spin” variable

and filter

. This process can be derived by introducing a

generating function of the original dynamics and averaging over

disorder [9]. Details of the calculation follow closely those

of similar models reported in the literature (see e.g. [2]).

The effective dynamics ultimately reads

(10)

where is a coloured Gaussian noise with first moments

given by

(11)

(12)

and where

(13)

(14)

are the correlation and response functions, respectively.

We focus henceforth on ergodic steady-state properties, and more

precisely on time-translation invariant (TTI) solutions of

(13) and (14). To do so we require that (a)

two-time quantities are Toeplitz-type matrices, i.e.

, , and that (b) there is no

anomalous integrated response, i.e.

. We denote

time-averages as

(15)

Rewriting the scores as and averaging over time

we obtain

(16)

where we have defined ,

and

(17)

In what follows, we set (the response function

can be equally evaluated by a derivative with respect to the effective

noise ). Note that (16) describes an ensemble

of processes, since in the stationary limit the noise variables

are Gaussian distributed,

viz.

(18)

where the persistent autocorrelation and susceptibility can be computed

through

(19)

(20)

The coefficients have

the meaning of frequencies. Indeed, is the frequency of use

of strategy when the filter takes the value . Clearly,

(21)

Equation (16) is the staring point of our analysis.The problem

consists specifically in calculating the statistics of the frequency

variables. For the sake of clarity, we shall now work out the

mathematical details of the strategy frequency problem in the case

recently addressed in the literature, namely that of the canonical MG

() with strategies [3]. Following sections

will address more complicated versions of the model.

3 Canonical batch Minority Game with strategies

Recalling that for canonical models , in this section we simplify

the notation and write in place of . Furthermore, in

order to make direct contact with the case discussed in

[3], we assume that for each

and that the density is a

-distribution with

(22)

The stationary state equations now greatly simplify: for each we

have

(23)

where is the frequency of use of strategy . The statistics of

the frequencies can be evaluated as follows. Consider the case in

which the effective agent uses a subset of strategies

(). Due

to the rule (22) this automatically implies that

(24)

(25)

with a generic value of the score velocity. In turn, one has that

, the rest of the frequencies being

identically zero. Let us split the Gaussian variables in two groups:

(26)

We have

(27)

(28)

where The

family of equations (27) defines an invertible

mapping

whose Jacobian is given by

(29)

where is the cardinality of . We now

have all the information required to compute the frequency

distribution in this case. By simply invoking the transformation law

of probability distribution for the -variables,

i.e.

(30)

from whence

(31)

and the restriction over the distribution of the

y-variables, we have that the contribution to the frequency

distribution of the subset of strategies with score ,

denoted , reads

(32)

where we have used the fact that the noise distribution factorises,

i.e. and emphasised

through the Dirac -distributions the constraints over the

frequencies111We consider Dirac delta contributions coming from

the boundary of the integration region to be unity..

denotes instead average over the

statistics of the y-variables.

Now the whole frequency distribution is simply given by the sum over

all possible partitions of (empty set not

included). Thus the average over the initial set of Gaussian variables

is converted to average over the frequency distribution:

(33)

A further simplification is allowed here if one restricts the

attention to subsets with by considering the

frequency distribution of strategies. By standard application of

combinatorics, one has

(34)

and, in turn,

(35)

Now if we denote by the fraction of agents using

strategies, then

(36)

It easy to see that for and we obtain

(37)

(38)

which, after some straightforward manipulations, is identified with

the corresponding formulas of [3].

4 Grand-canonical MG with one asset and strategies

We now turn our attention to the grand-canonical version of the MG

with strategies strategies per agent. This is obtained by

taking, in addition to the rules used in the previous section,

instead of .

Now the stationary state equations read, for each ,

(39)

where we set and denoted by the probability

that the agent is inactive, that is the probability that . In

this case the value of the frequencies for do not enter in the

relevant equations which determine the quantities of interest of the

model. We proceed to calculate the statistics of the frequencies

and to relate all quantities to such

statistics. As before, let be a

subset of strategies being used, so that

(40)

(41)

Now we must distinguish three cases: if , the agent is always

active, that is ; if instead , the agent is sometimes

inactive, that is ; finally if then and

the agent never invests.

1.

Case . Here the analysis follows closely the

one performed for the canonical -strategy MG. The agent is in the

market and represents the frequency of the strategy

being used. This implies that ,

and with

. We then split the stationary equations

(39) into two parts and write

(42)

(43)

where we have defined the functions

(44)

and, as before, denoted as the Gaussian variables in the

subset and as those not belonging to this

subset. The set of equations (42) defines an invertible

mapping

whose Jacobian reads

(45)

with the cardinality of the subset

. Proceeding as in the previous section, that is using

the transformation law of probability distributions, we find that the

contribution to the the frequency distribution of the subset

of strategies, denoted

, reads

(46)

2.

Case . We now must take into account the fact

that with . The stationary equations become

(47)

(48)

with

(49)

The set of equations defines

an invertible mapping whose Jacobian is

(50)

Therefore the contribution to the frequency distribution in this cases

reads

3.

Case . Finally, if all score velocities are

negative then the agent is not on the market and therefore for

all with

(51)

and correspondingly

(52)

As was easily expected, the probability that an agent stays out of the

market decreases as increases, which reflects the simple fact that

the availability of larger strategic alternatives increases the

likelihood that an agent has a profitable strategy among his pool.

Gathering these contributions we finally obtain the probability

distribution of the frequencies and velocity for the subset

of strategies of active players and the fraction

of inactive players

(54)

The frequency distribution is simply given by the sum over all

possible partition of (empty set not included). Thus

the average over the initial set of Gaussian variables is converted to

average over the frequency distribution

(55)

Within this framework, the persistent correlation and susceptibility

read

(56)

(57)

where the expression in the expression for the

susceptibility must be understood as

(58)

Interesting information is also provided by the fraction of active agents using a certain subset

of strategies

(59)

To quantify our findings we now consider the cases for and

explicitly.

4.1 (the standard GCMG)

Here the frequency variable represents the frequency with which the

agent invests. Its distribution becomes

(60)

with . From here we have the

following expression for the persistent correlation, susceptibility

and fraction of active and inactive agents

(61)

(62)

(63)

(64)

where we have obviously that

since the probability is indeed normalised. Taking for

the incentives the distribution

(65)

where denotes the fraction of speculators and that of

producers, one easily sees that the above equations coincide with

those derived for the GCMG (see e.g. [2, 10]).

4.2

The stationary state equations now take the form (39), with

. It is now convenient to consider the following

cases in detail.

1.

Case for each .

•

If , then and

(66)

Inverting this mapping we obtain a contribution to the probability

distribution which reads

(67)

with .

•

If , we have with and

correspondingly

(68)

with .

2.

Case for with . Proceeding as before:

•

If , then and , so that

(69)

with .

•

If we have instead

(70)

with .

3.

Case . Now . This happens with

probability

(71)

As usual, we divide the population of agents into two groups,

speculators and producers. As before, the producers have only

one strategy and play at every time step (adopting the notation of

[4], we write ), whereas the speculator have

strategies each (we write ). The equations for ,

and the fraction of speculators using strategies

() take a simpler form when, for speculators,

for each . In this case, for the quantity

( with ) and one

finds

(72)

whereas

(73)

(74)

(75)

(76)

with

(77)

(Note that . Furthermore, .)

Solving (4.2) for all other quantities can be immediately

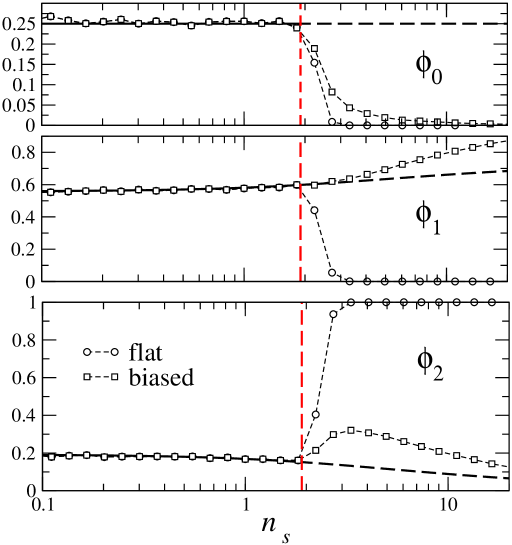

evaluated. Fig. 1 reports the behaviour of ,

and as a function of for .

Figure 1: Top to bottom: the fraction of speculators using

, and both of their strategies versus at .

Markers denote results of on-line simulations of systems with

averaged over disorder samples per point. ‘Flat’

refers to initial conditions with for all

speculators . ‘Biased’ denotes instead initial states with

and . Continuous lines are

analytic results, and they have been continued as dashed lines in

the non-ergodic region. The dotted lines joining the markers are a

guide for the eye. The dashed vertical line marks the critical point

above which the ergodic theory breaks down.

The point where simulations and theory depart can be computed assuming

that (implying the onset of anomalous response). This

gives the critical point , above which the ergodicity

assumptions fail and the steady state depends on initial

conditions. Thus this model displays the standard phase transition

with ergodicity breaking characterizing the original

GCMG. Similarly to what happens in the canonical MG, the critical

point (which in general depends on ), decreases as increases,

a reflection of the fact that agents .

5 Generalisation to models with assets

Multi-asset Minority Games have been introduced in [5] but we

shall discuss here a slightly more general version of the same

model. One considers a market with assets

and agents. At each

time step , agents receive information patterns

chosen randomly and

independently for each with uniform probability and, based on

these, they formulate their bids (one bid per asset at each time

step). is taken to scale linearly with and we will

denote their ratios as . For each asset

, every agent disposes of trading strategies

that prescribe a binary action

, drawn randomly and uniformly,

and independently for each asset, strategy and pattern. The

performance of every strategy foe each asset is monitored by a score

function which is updated by the following rule

(78)

where are real constants representing positive

or negative incentives for the agents to trade, and

is the excess demand of asset at time ,

(79)

where denotes the bid formulated by agent in

asset at time . Let

be the strategies he

chooses for each asset and let

denote the subset of assets

in which agent trades at time . We then write the bid

explicitly in the following form:

(80)

Here, the terms

preserve the meaning they had in the single-asset model. The new term

(81)

defines the set of assets in which agent is active. We assume now

that

(82)

(83)

with and generic functions describing the strategy

and asset selection rule. In the model described in [5],

and with

.

The batch dynamics can be analysed in terms of effective

processes for a single representative agent:

(84)

where is again a coloured Gaussian noise,

viz.

(85)

(86)

and where

(87)

(88)

are identified with the bid autocorrelation and response functions of

asset :

(89)

(90)

in the limit . In the above formulas, generalizes

(5) to include the function :

(91)

Proceeding as before, one arrives (with obvious notation) at the

following stationary state process:

(92)

with

(93)

(94)

and where the asset-dependent persistent autocorrelation and

susceptibility are given by

(95)

(96)

Given a subset of assets , then

is the frequency of the asset

being traded by using the strategy when an

action has been taken on the market. The normalization now reads

(97)

Let us discuss the simplest case in which and ,

corresponding to the canonical multi-asset MG (whose particular case

is the subject of [5]). Agents have at their disposal a

set of assets to trade, one each time (i.e.

). We assume that

and that the asset selected at

time is given by

(98)

Following the same line of arguments one obtains the following

expression for the distribution of frequencies for a subset of assets

being traded in the steady state:

(99)

where

(100)

As before the frequency distribution is given by the sum over all

possible partitions of (empty set not included):

(101)

Within this framework, the persistent correlation and susceptibility

read

(102)

(103)

whereas the fraction of agents trading a certain

subset reads

(104)

It is easily checked that satisfies

.

6 Summary and outlook

Minority Games with strategies and/or assets per agent are

intriguing generalizations of the standard MG setup which display a

qualitatively similar global physical picture (e.g. regarding the

transition with ergodicity breaking) but substantially richer patterns

of agent behaviour, directly related to the enlargement of the agents’

strategic endowments. The precise characterization of this aspect,

even in the ergodic regime, poses challenging technical problems which

have started to be analysed only recently. The central issue concerns

the calculation of the statistics of the frequencies with which

subsets of strategies are used. This problem was first tackled in

[3], where an explicit solution is derived in the context

of canonical batch MGs. In this work we have presented an alternative

and mathematically simpler solution method (though the complexity of

the calculations still increases rapidly with ). We have shown

specifically how to recover the theory of the canonical case and

solved explicitly the grand-canonical batch MG with strategies per

agent. The method also generalizes to the recently introduced

multi-asset models.

The method discussed here can be applied to a number of variants of

the basic setup, some of which may be important from an economic

viewpoint (for example in order to study the emergence of cross-asset

correlations). Its main limitation is that, while the effective-agent

dynamics, eqn. (10), holds true in both the ergodic and non-ergodic

phases, our futher focus on time-translational properties limits the

rigour of our conclusions to the ergodic regime. The richness of the

MG dynamics is actually most striking when ergodicity is broken.

Multi-strategy MGs are likely to produce a variety of possible steady

states that may require novel observables to be completely

characterised. Up to now, our understanding of non-ergodic regimes

relies entirely on ad hoc heuristic arguments (see for instance

[8, 11]) which provide a rough picture of the geometry of

steady states and of the role of initial conditions for obtaining

states of high or low volatility, but a more precise characterization

remains elusive. In our opinion, at the present stage of our

theoretical understanding of MGs, any advance in this direction would

be most welcome.

It is a pleasure to thank ACC Coolen and N Shayeghi for useful

discussions. We acknowledge financial support from the EU grant

HPRN-CT-2002-00319 (STIPCO).

References

References

[1]Challet D, Marsili M and Zhang YC 2005 Minority Games

(Oxford University Press, Oxford)

[2]Coolen ACC 2005 The mathematical theory of Minority

Games (Oxford University Press, Oxford)

[3]Shayeghi N and Coolen ACC 2006 J. Phys. A:

Math. Gen.39 13921

[4]Challet D and Marsili M 2003 Phys. Rev. E68

036132

[5]Bianconi G, De Martino A, Ferreira FF and Marsili M 2006

Preprint physics/0603152

[6]De Martino A and Marsili M 2006 J. Phys. A: Math.

Gen.39 R465

[7]Coolen ACC, Heimel JAF and Sherrington D 2001 Phys. Rev. E65 016126

[8]Heimel JAF and Coolen ACC 2001 Phys. Rev. E63 056121

[9]De Dominicis C 1978 Phys. Rev. B18 4913

[10]Challet D, De Martino A, Marsili M and Perez Castillo

I 2006 JSTAT P03004

[11]Marsili M and Challet D 2001 Phys. Rev. E64

056138