Automatic Trading Agent. RMT based Portfolio Theory and

Portfolio Selection

††thanks: snarska@th.if.uj.edu.pl

jakub@krzych.art.pl

Abstract

Portfolio theory is a very powerful tool in the modern investment

theory. It is helpful in estimating risk of an investor’s

portfolio, which arises from our lack of information, uncertainty

and incomplete knowledge of reality, which forbids a perfect

prediction of future price changes. Despite of many advantages

this tool is not known and is not widely used among investors on

Warsaw Stock Exchange. The main reason for abandoning this method

is a high level of complexity and immense calculations. The aim of

this paper is to introduce an automatic decision - making system,

which allows a single investor to use such complex methods of

Modern Portfolio Theory (MPT). The key tool in MPT is an analysis

of an empirical covariance matrix. This matrix, obtained from

historical data is biased by such a high amount of statistical

uncertainty, that it can be seen as random. By bringing into

practice the ideas of Random Matrix Theory (RMT), the noise is

removed or significantly reduced, so the future risk and return

are better estimated and controlled. This concepts are applied to

the Warsaw Stock Exchange Simulator http://gra.onet.pl. The

result of the simulation is 18% level of gains in comparison for

respective 10% loss of the

Warsaw Stock Exchange main index WIG.

Keywords: Random Matrix Theory,

Gaussian Filtering, Portfolio Optimization

1 Portfolio theory - setting the stage

Investments in stock securities like shares, currencies or

different types of derivatives are generally treated as very

risky. Ability to predict future movements in prices (price

changes) allows one to

minimize the risk.

Modern Portfolio Theory (MPT) refers to an investment strategy

that seeks to construct an optimal portfolio by considering the

relationship between risk and return. MPT suggests that the

fundamental issue of capital investment should no longer be to

pick out dominant stocks but to diversify the wealth among many

different assets. The success of investment does not purely depend

on return, but also on the risk, which has to be taken into

account. Risk itself is influenced by the correlations between

different assets, thus the portfolio selection process represents

Let us briefly remind several key tools and concepts, that MPT

uses, i.e. the Markowitz’s Model, which is crucial in further

analysis.

1.1 Elementary definitions and the Markowitz’s Model

The efficient portfolio theory was first introduced by Harry M.Markowitz in [8]. He decided not to analyze the return, risk and volatility of single stocks in a portfolio, but considering portfolio (groups of shares) as a whole. In order to manage this problem, he introduced a simple statistical measure - correlation, which links up the changes in prices of an individual assets with all other changes in price of assets in a given portfolio.

1.1.1 Construction of an efficient portfolio of multiple assets

Consider quotations of the -th stock and introduce a vector of returns ,where , is the observed realization of a random variable .Denote - time series of prices for a certain stock . Then

| (1) |

and is a natural logarithm. Then the expected return of a single asset is given by

| (2) |

If additionally denotes the number of assets in a portfolio, then is a vector of weights (ratio of different stocks in a portfolio). We have to then impose a budget constraint

| (3) |

where is a vector of ones. If additionally the short sell is excluded. Denoting as a vector of expected returns of single stocks, we see, that an expected return of a whole portfolio is a linear combination of returns of assets in a portfolio

To calculate the risk of a given portfolio we introduce a certain metric of interdependence between different random variables. The most natural one is the statistic measure - covariance , which expresses the interdependence of variables and in all observed discrete times .

| (4) |

Now we are ready to define the variance of a portfolio as

| (5) |

1.1.2 Optimization of a Portfolio

We can calculate the return and risk of any given portfolio. Now we have to find and choose the effective portfolios. Since it is the quadratic programming problem, it will be done in two steps

-

1.

First; the portfolio with minimal risk of all possible portfolios will be selected (the return rate is equal to zero, ie )

-

2.

Secondly; we will find the minimum variance portfolio among portfolios of arbitrary chosen return rate and then find the efficient frontier iteratively

Minimal Risk Portfolio

We have to find the vector of weights . In order to do

it we need to know perfectly the covariance matrix 111This

is a very strong assumption, since as we shall see later,

covariance matrix derived from empirical data contains a high

amount of noise and statistical uncertainty.. Let is the

function of risk, depending of portfolio composition

| (6) |

with linear constraint (3)

| (7) |

Our task is to minimize the function under the linear constraint (3). This can be done in a convenient way by using the method of Lagrange multipliers. We get the Lagrange function in a form:

| (8) |

Standard methods of finding the minimum of a multivariate function with a boundary condition lead to the system of equations with unknown quantities

| (9) |

Minimal Variance Portfolio

Second task contains one

more restriction, that the expected return of a portfolio have

to obey:

| (10) |

Then the Lagrange function reads:

| (11) |

which gives us

| (12) |

In this case we have to deal with the system of equations with unknown quantities, which is solvable in general case.

2 Covariance Matrix and Portfolio Construction

Covariance

Matrix plays an important role in the risk measurement and

portfolio optimization. Modern Portfolio Theories assume, that

covariances or equivalently correlations between different stocks

are perfectly known and can exactly be derived from the past data.

In practice it is quite opposite. Empirical Covariance Matrices,

built from historical data enclose such a high amount of noise,

that at first look they can be treated as random. This means, that

future risk and return of a portfolio are not well estimated and

controlled. Only after the proper denoising procedure is involved,

one can construct an efficient portfolio using Markowitz’s

result.

In this section we will briefly explain how using the RMT

one can reduce the bias of the empirical Covariance Matrix.

2.1 Gaussian Correlated Variables

Suppose now, that the returns from different stocks are Gaussian random variables. The joint probability distribution function can be then written as:

| (13) |

where is the element of the inverse

covariance matrix.

It is well known result, that any set of

correlated Gaussian random variables can always be decomposed into

a linear combination of independent Gaussian random variables. The

converse is also true, since the sum of Gaussian random variables

is also a Gaussian random variable. In other words, correlated

Gaussian random variables are fully characterized by their

covariance (or correlation) matrix.222This is not true in

general case, when one needs to describe the interdependence of

non Gaussian correlated variables

2.1.1 Covariance estimator:

The simplest way to construct the covariance matrix estimator for Gaussian random variables is to deal with historical time series of returns. The empirical covariance matrix of returns can be then expressed through the equation (4)

2.2 RMT based data filtering and denoising procedure- the shrinkage method

For any practical use of Modern Portfolio Theory, it would be necessary to obtain reliable estimates for covariance matrices of real-life financial returns (based on historical data).Thus a reliable empirical determination of a covariance matrix turns out to be difficult. If one considers assets, the covariance matrix need to be determined from time series of length . Typically is not very large compared to and one should expect that the determination of the covariances is noisy. This noise cannot be removed by simply increasing the number of independent measurement of the investigated financial market, because economic events, that affect the market are unique and cannot be repeated. Therefore the structure of the matrix estimator is dominated by ’measurement’ noise. From our point of view it is interesting to compare the properties of an empirical covariance matrix to a purely random matrix, well defined in the sense of Random Matrix Theory [5]. Deviations from the RMT might then suggest the presence of true information.

2.2.1 Gaussian filtering

We will assume here that the only randomness in the model comes from the Gaussian Probability Distribution. In order to describe the filtering procedure we will first summarize some well known universal properties of the random matrices.

2.2.2 RMT predictions for behaviour of eigenvalues

Let denotes matrix, whose entries are i.i.d. random variables, which are normally distributed with zero mean and unit variance. As and while is kept fixed, the probability density function for the eigenvalues of the Wishart matrix is given by (Marčenko, Pastur [7])

| (14) |

for such that where and satisfy

| (15) |

2.2.3 Standard denoising procedure and the shrinkage method:

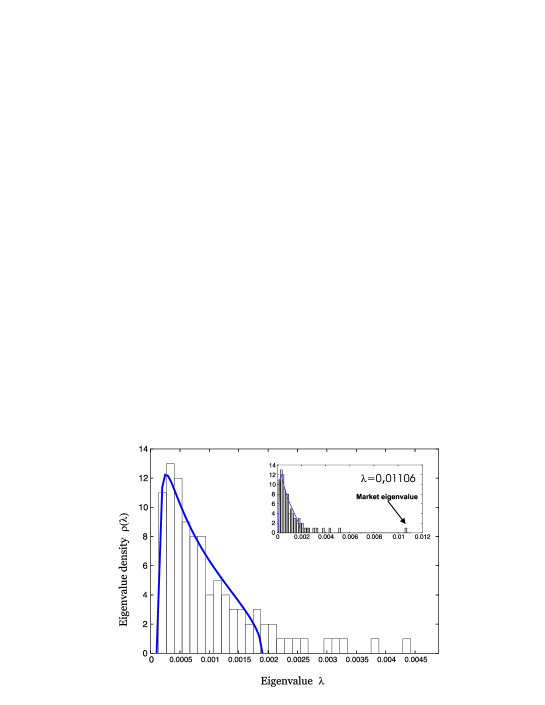

To remove noise we need first to compare the empirical distribution of the eigenvalues of the covariance matrix (4) of stocks (in our case for Warsaw Stock Exchange shares) with theoretical prediction given by ((14) -"Wishart Fit"), based on the assumption that the covariance matrix is random.

If we look closely at Fig. 1 we can observe, that there are several large eigenvalues (the largest one is labeled as the market one, since it consists the information about all the stocks in the market i.e. is closely related to the WIG index), however the greater part of the spectrum is concentrated between and (i.e. The Wishart- fit ). We believe, that behind this Random part of the spectrum there exists single eigenvalue, which carries nontrivial and useful information. Exploiting the knowledge from Linear Algebra,we may rewrite our covariance matrix as:

| (16) |

Here is a diagonal matrix of eigenvalues of the original matrix and is a matrix whose columns are normalized eigenvectors corresponding with proper eigenvalues. Furthermore fulfills the equation:

| (17) |

The trace is conserved, so we write:

| (18) |

Using the (17) and cyclic properties of the trace we get

| (19) |

Following the fact, is a diagonal matrix of eigenvalues one can decompose its trace in the following way:

| (20) |

where is a set of eigenvalues that are predicted by (14) is set of these eigenvalues, which do not obey the RMT conditions. If we now replace by one eigenvalue , we get

| (21) |

This results in squeezing the Random part of the spectrum to a single degenerated eigenvalue. The diagonalized matrix has now only several eigenvalues.

2.3 Covariance Matrix Reconstruction

Due to noise - removing procedures we know exactly the eigenvalues

of the real covariance matrix. But since we have no knowledge of

the original covariance matrix, we do not have enough knowledge of

it’s eigenvectors. The familiarity with of eigenvalues is not

sufficient to find the covariance matrix.

After applying the denoising procedure we will reconstruct the

covariance matrix using the diagonalized matrix with some

eigenvalues shrinked and matrices of eigenvectors calculated for

non-shrinked covariance matrix.

This reconstructed and unbiased

Covariance Matrix is used as an initial Covariance Matrix in

Markowitz Model described above. The new model itself is a part of

automatic investing algorithm described in the next section. The

results are presented in the last section.

3 An Overview of the System - Automatic Investing Algorithm

The Automatic Trading Agent is a client- server application for managing stock portfolios without involving user interference. It consists of three main parts: Virtual Agent, Data Collector and User Interface. Clients running the System on their workstations are able to monitor a stream of data (information about the state of a portfolio) from the ATA server using their web browsers. This part of application is controlled by the User Interface. In addition to different standard portfolio management tools ATA system includes several RMT - based techniques for building an optimal portfolio with the noise effect minimized.The system is designed not only to help a single client choose the right, optimal portfolio with a user-defined level of risk and expected return, but also to diminish user engagement in stock data and information analysis. Once the strategy is fixed, client is able to monitor the future changes in the portfolio; the rest including portfolio optimization, data picking, sending requests and buy / sell orders is done by a decision system - Virtual Agent.

3.1 Database module and Data Collector

This part of the program is responsible for assembling and managing the stock data.It also verifies the database in accordance with the assets available for the transaction platform.

3.1.1 Database

The data are stored on the server as files with daily quotations in a separate folder. Any company is represented by a text file, whose name is the company’s ISIN number. Each file consist of two columns - one representing the dates and the second corresponding daily closing prices.

3.1.2 Data Collection

Data collector is a separate program run by the server each

trading day, one hour after the daily quotations are closed. It

downloads the current quotation from stock exchange data vendors

(in our case http://www.parkiet.com) and writes it down into

the database.

The matrix of stocks, which will be used in

further portfolio analysis, is then filled with the data from the

database.The algorithm loads all prices of securities for a

certain time window from the previously defined folder.

3.1.3 Corrections Module

Data are sometimes corrupted during the transfer or from

’measurement’ reasons (i.e. there is no quotation for the certain

stock and the Stock Exchange is unable to state the closing

price). This result in imperfect and incomplete information and

zeros in initial time series. The number of files may also vary,

because it reflects

the list of assets, which are currently available for trading.

This part of the program watches and controls the correctness of

the files, the entries in the database and the number of files.

3.2 Virtual Agent

Virtual Agent is a specific

decision-making system. It’s input are current and historical

stock exchange information and data form the database. On output

it generates specific requests and orders to transaction platform.

In our case it is the Stock Exchange Game structure, based on the

WARSET trading system.

Information conversion and data analysis

is done one hour after WSE the session is closed. All new daily

data are incorporated in the database and then optimal decision is

taken and the sell/ buy request, which will be accomplished the

next day, is sent.

The Virtual Agent build it’s resolutions on

the Effective Portfolio Theory and Random Matrix Theory.

3.2.1 Covariance Matrix Module

This part of the systems offers various types of covariance matrix estimators, which are used in solution of Markowitz’s problem. The module’s default setting is the simplest Gaussian estimator (4), but this can be modified by the user. The Covariance Matrix Module is responsible for building a raw matrix from the data and also for reconstructing it after the denoising procedure.

3.2.2 Denoising and Filtering Module

The Module controls the diagonalization process, which uses the LU decomposition , i.e. calculation of eigenvalues and eigenvectors. The eigenvectors are stored in the system and the eigenvalues are used to reduce the degrees of freedom of the covariance matrix, as it is predicted by RMT. Default denoising procedure is the standard one, introduced by [1].

3.2.3 Portfolio optimization

This module is a separate program, which solves the

Markowitz’s problem and finds the optimal portfolio and then sends

buy / sell order. Before any request is sent, Virtual Agent

verifies it’s own decisions using several criteria. The simplest

one is to check, whether the costs of the predicted transaction

are not higher, than the realized portfolio. If they are, then

Agent sends hold request on the whole portfolio.

Such a

portfolio correction is usually done once a month. 333The

frequency of correction, like all other key parameters can be

increased by the user. The correction means to find once again

the portfolio with fixed level of return and risk accepted,

regarding all the new quotations since the last accomplished

correction.

3.2.4 Corrected Portfolio:

We have to

compare two separate portfolios: the ’old’ one, which pattern is

stored on the remote transaction platform with the ’new’ one,

created using the incorporated quotations. The next step is to

determine an abstract portfolio as a

result of subtractions between the examined portfolios.

Let is the vector of weights of the new portfolio,

and denotes the same vector for the old portfolio,

then the weights of a correction one are:

| (22) |

If a component of is the sell request is sent, and obviously for system performs a buy order. means system holds that certain asset and it’s share in a portfolio does not change.

3.2.5 Transaction costs:

Each change in a portfolio is charged with brockerages (Table: 1). To compensate this effect we need to sell slightly more individual stocks, than it arises from our analysis. The reverse effect has to be applied to buy request.

3.3 Communication and Reporting Modules - User interface

3.3.1 Communication Module

The communication module allows the Virtual Agent to connect to the Game platform and place appropriate orders. This module is a separate script, constructed to be independent of the trading platform. This gives the possibility to replace the Simulator used in the testing period by the real trading platform.

3.3.2 Reporting Module

The User Interface plays the role of the reporting module. It’s external part, accessible for the user is the web page (myricaria.if.uj.edu.pl). Here the investor can follow present information on accounts, the gains and losses figures and the history of all changes, investment strategies and decisions taken. The system user has also a possibility to change the key parameters of the program, such as investment strategy (choice of the level of risk accepted) and the frequency of portfolio corrections.

3.4 Implemented technologies

3.4.1 C# Language

The ATA is completely written in C# language, chosen because of

multi-platform advantage. The programs may be written in one

environment and then run under any platform i.e. Windows and

Linux. the default environment for the ATA is linux server, but

the programming process was made under Windows, so the

multi-platform ability is a must.

Another important advantage of

the language is the intuitive construction of mathematical

formulas and the precision of calculations far beyond the popular

C++ language, which in our case is crucial.

3.4.2 Linux Tools

The Data Collector is a BASH shell script, run by Cron daemon, every fixed number of days. The script also uses Wget to efficiently collect the data via FTP/HTTP. The AWK , SED and GREP allow the script very easily to explore and analyze high amounts of data.

3.4.3 HTML, PHP, CSS

The user interface is prepared as the website. The PHP scripts run by the www server Apache, allow the creation of dynamic HTML websites, where the content changes frequently. The proper view of the website in any internet viewer is controlled by the CSS.

4 Warsaw Stock Exchange Simulator and ATA implementation results

Here we present the results of the whole procedure described above. For our research we have chosen the Warsaw Stock Exchange simulator available via the world world wide web url http://gra.onet.pl, as a testground.

4.1 Rules of the game

There are several steps and rules a user must adhere and execute

to properly use the simulator. First of all, the system needs to

recognize us as its’ users, possessing so called

onet_id. Thus the primary step is to register oneself in

the onet system, by filling out a simple form. Using

onet_id one may now log on http://gra.onet.pl to

create our first account, with PLN as an initial sum of

money for every account. The number of accounts a single user may

open is not limited and the money can be arbitrarily invested.

Sharing more than one account

number, one is able to check different investment strategies.

This game act like a real stock exchange and brockerage house. We

have to start with buy order - choose financial instruments, which

we want to buy and specify their quantity and price limits. If

there are no constraints on price, then the order is realized at

any price. All quotations are delayed minutes, to give the

same chance to the players who cannot follow the quotations in

real time. All orders are cancelable, also with minutes

delay.Each user also has to pay transaction costs as in Table

1

| Value of order | Height of brockerage |

|---|---|

| PLN | PLN |

| –PLN | PLN over PLN |

| –PLN | PLN over PLN |

| PLN | PLN over PLN |

We have constructed a certain portfolio, after our buy order is being accomplished. Now we need to decide, what shares we need to buy / sell / hold to minimize the risk and maximize the return. To win an excellent rank and high gains, one need to be involved and follow the price changes permanently. Most of the steps one need to execute, except the choice of the accepted level of risk, can be done automatically by especially programmed virtual agent.

4.2 Data Selection and Analysis

The WIG index incorporates about stocks, which make about

of all assets quoted during continuous trading. From our

point of view, it is interesting to examine the connections (i.e.

correlations) between these stocks.

In order to conduct further

research and improve the effectiveness of our algorithm, we first

need to identify and choose a stable period in the economy.

We have related it with the period of the lowest volatility of the WIG index. We have started with the conversion of absolute changes of the WIG time series to the relative ones according to

| (23) |

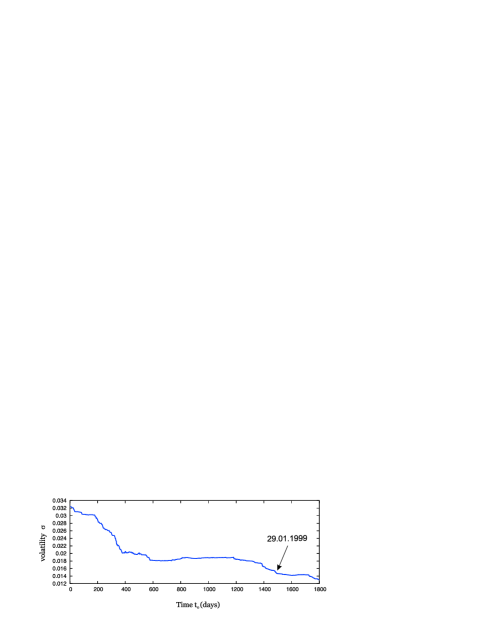

Then for a fixed time window width quotations, the volatility of the time series was calculated:

| (24) |

where is the average over the whole time window .This results can be presented on the diagram:

It is easy to notice, that first few years of quotations are

determined by a relatively high volatility. That is why the period

from to was chosen in further analysis

and

tests.

Another problem we have encountered during the analysis of

historical data, was the incomplete information about some of

stocks, which may result in the infinities in relative

changes , when the lack of information was replaced by zeros

in the original time series 444’Zeros’appear when

one is unable to settle the price of an individual stocks, see

Ziêbiec (2003) . The separate ’zeros’ were extrapolated from the

future and previous relative changes of a given time series. In

the case, if more information is lost in the way, one is unable to

predict the further prices then this stock is not very examined in

further research. For the fixed period of days we have

chosen then stocks and we have calculated the average

standard deviation of price changes and average correlation of returns between

stocks

4.3 Simulation on the historical data and it’s results

The next step in testing our system is to check how it works when

the input and output data are historical. The selected time period

was divided into parts. We have assumed, that the initial value of

a portfolio is PLN. We have used here a time window with

variable width . The analysis started with days. Every

day, the - dimension of the matrix was increased

by one, until the final days.

The number of available

stocks and the average number of stocks selected .

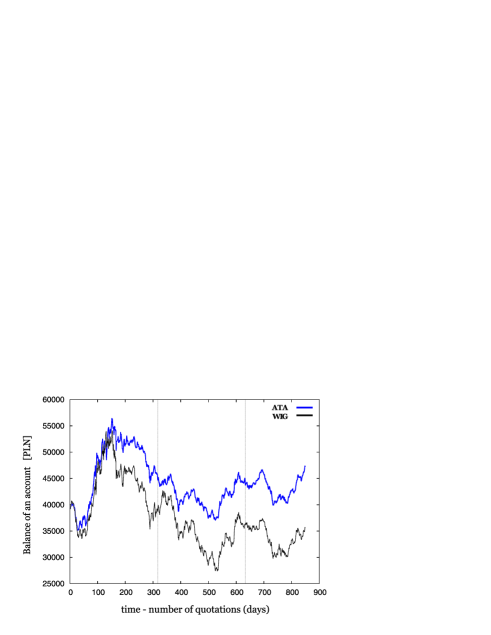

Every days the correction was made. The portfolio went to

the roof on day with PLN a a result. (This is

of the initial value).

The portfolio went to the floor

with PLN after first days.

The result of the

investment after days yields PLN ,which means

the gains compared to the WIG downfall.

Conclusions and Future Work

The aim of this paper was to introduce a simple RMT based mechanism, acting like an virtual trader in a portfolio selection and optimization process.Imposing the results from Random Matrix Theory our program reduces the statistical noise and gives a better estimation of future risk and return for a certain portfolio.However, in this paper only the simplest version of the programm was presented. An improvement of the program, which adopt it’s decisions to the all information available will be the part of our future work. From our point of view, an interesting for further analysis is the hypothesis, that there exist also time correlations between different shares. This fact might be useful in the detection of buy/ sell signals.

References

- [1] J.P.Bouchaud, M.Potters, Theory of Financial Risk. From Statistical Physics to Risk Management 2nd ed., Cambridge University Press, Cambridge 2003

- [2] Z. Burda, A. Görlich, A. Jarosz, J.Jurkiewicz, Signal and Noise in Correlation Matrix, http://arxiv.org/pdf/cond-mat/0305627

- [3] S.Chan, The Impact of Transaction Costs on Portfolio Optimization, Bachelor Thesis, Erasmus University, 2005

- [4] E.J.Elton, M.J.Gruber, Modern Portfolio Theory and Investment Analysis 6th ed., Wiley, New York 2002

- [5] T.Guhr, A.Müller - Groeling, H.A.Weidenmüller, Random matrix theories in quantum physics: common concepts, Phys. Rep. 299 (1998)

- [6] L.Laloux, P.Cizeau, J.P.Bouchaud and M. Potters, Noise Dressing of Financial Correlation Matrices, http://arxiv.org/pdf/cond-mat/9810255/

- [7] V.A. Marčenko, L.A. Pastur, Distribution of eigenvalues for some setes of random matrices, Math USSR Sbornik, 1: 457 -483 (1967)

- [8] Harry M.Markowitz ,Portfolio Selection, The Journal of Finance, Volume 7 No. 1, pp. 77-91 (1952)

- [9] Markus Rudolf, Algorithms for Portfolio Optimization and Portfolio Insurance,Verlag Paul Haupt, Bern, Stuttgart, Wien