ELECTRICITY REAL OPTIONS VALUATION

Abstract

In this paper a real option approach for the valuation of real assets is presented. Two continuous time models used for valuation are described: geometric Brownian motion model and interest rate model. The valuation for electricity spread option under Vasicek interest model is placed and the formulas for parameter estimators are calculated. The theoretical part is confronted with real data from electricity market.

02.30.Cj, 02.50.Ey, 02.70.-c

1 Introduction

The liberalization of electricity market caused that modeling on this market became very important skill. It helps us to minimize loss and hedge our position. It is a very interesting fact that spread option could be used for valuation some real assets as power plants or transmission lines. But before that we need to know the spread option price formula. Very popular model used for option valuation is the geometric Brownian motion model but it is not very efficient. In the 2005 the idea of modeling domestic electricity market using interest rate model was introduced by Hinz, Grafenstein, Verschue and Wilhelm [1]. They valuated European call option written on power forward contract under Heath Jarrow Morton model and, in this way, created very interesting class of models.

The aim of my work is the valuation and calibration of electricity spread option under interest rate model applied for electricity market. I start with assumption of Vasicek model and using martingale methodology [2] valuate spread option. Using the maximum likelihood function methodology I estimate model parameters. I compare constructed model with geometric Brownian motion model by applying both models to real option valuation. I make simulations to show the difference between to discussed models.

My paper is organized in the following way. At the beginning (Section 2) I describe what does it mean that we bought a spread option, next (Section 3) I introduce the reader into real options world. In Section 4 I describe valuation methodology for spread option under interest rate model and present also option price formula for geometric Brownian motion model. The calibration methods for both models are described in Section 5. At the end, in Section 6, all theoretical deliberation are confronted with real data and some simulation results are presented.

2 Electricity Spread Options

In this section two interesting cross commodity derivatives on electricity market are described. The first one is the spark spread option, which is based on fact that some power plants convert gas into electricity. The underlying instrument is the difference between the gas and electricity prices (the spark spread). The basic parameter connected with this kind of instrument is the heat rate, the ratio which describes the amount of gas required to generate 1 MWh of electricity. The definition of such an instrument has a form [3, 4]: An European spark spread call option written on fuel , at fixed swap ratio , gives its holder the right, but not the obligation to pay K times the unit price of fuel at the options maturity and receive the price of one unit of electricity.

It is easy to imagine such kind of option which better fits the Polish electricity market. We should assume that the underlying instrument is the difference between the carbon and electricity prices. But in this time there is no possibility of valuation of such an option because we don’t have the representative carbon price. Generally, if we assume that and are respectively future price of 1MWh of electricity and the future price of the unit of fuel and K is the swap ratio than we could describe the payoff of the European electricity-fuel spread call option as

and the payoff of the European electricity-fuel spread put option has form

The second derivative is the locational spread option. It is based on fact that transmission of power from one location to another is very popular transaction. It is normal, for transmission system, that the power is moved from the place of lower price to the place of higher price and this is why the transaction is profitable. The whole transaction depends on the difference between the electricity prices and also on delivery costs and for hedging we could use options. This kind of instrument could be defined in following way [3]: An European call option on the locational spread between the location one and location two, with maturity , gives its holder the right but not the obligation to pay the price of one unit of electricity at location one at time T and receive the price of units of electricity at location two. Assume that and are the electricity prices at the first location and second location respectively. The payoff of the European locational spread call option is given by

The put option is defined similar and the payoff of the European electricity-fuel spread put option has form

3 Real Options

Suppose that for describing the commodity we use three qualities : G - the nature of good, t - time when it is available, L - location where it is available. We could define [5] a real option as technology to physically convert one or more input commodities into an output commodity . For example most of power plants are real option because they give us the right to convert fuel into electricity. The transmission line is also real option. It gives us the right to change the electricity in one location into electricity in second location. The works of Deng, Johnson and Sogomonian [6, 3] contain two formulas defining how to valuate generation and transmission assets. If we define that is a one unit of the time-t right to use generation asset we could say that it is the value of just maturing, time-t call option on the spread between electricity and fuel prices and the one unit value of capacity of power plant using some fuel is given by

where is the length of power plant life.

Similar if we define that is a one unit the time-t right to convert one unit of electricity in location A into one unit of electricity in location B we could say that it is the value of just maturing,time-t call option on the spread between electricity prices in location A and B . The one unit value of such transmission asset is given by

where is the length of transmission network life.

4 Valuation methods

In this section I present the widely known geometric Brownian motion model and I valuate the call spread option for the new, interest rate model using martingale methodology. All calculations are described below.

4.1 Geometric Brownian Motion Model

Suppose that the future prices of commodity are described by following stochastic differential equations

where and , are i.i.d. Brownian motions. It is known fact [5], that the price of the spread call option with swap ratio and time to maturity , written on futures contract with maturity is given by

where

and

4.2 Interest Rate Model

For domestic currency, for example MWh, we denote two processes: , which are the future prices of one unit of commodity. The interest rate functions for such processes are respectively

and

where and , are i.i.d. Brownian motions. We assume that there exist the savings security (for example in USD), with constant interest rate , for which

is the USD price of future delivery of 1 unit of commodity. We know [1] that there exist a martingale measure for which the discounted processes , are martingales. We have

We define the new discounting processes for i=1,2 as

where If we change the measure from to

we know that processes , are -martingales. From interest rate theory we obtain

where

| (1) |

If we change the measure again from to

we know that and are -martingales and similar to the earlier situation, we have

| (2) |

where

| (3) |

After simple calculations we also have

| (4) |

where , and . We also assume that

| (5) |

where and , , are independent Wiener processes. For discounted processes following equation is true

| (6) |

Having the necessary stochastic differential equations we could price the option. We change the measure from to in following way

Process is -martingale. From Ito lemma we know that

where and . Now, for calculation of the option price, we could use the Black-Scholes formula

where

and is the normal cumulative distribution function. For every time point the option price with swap ratio and time to maturity , written on futures contract with maturity is given by

where

This methodology could be used directly for locational spread options and also for fuel-electricity spread options if we assume that the swap ratio between MWh and unit of fuel is one.

5 Historical Calibration

In this section we describe how to fit our models for real, historical data. At the beginning we assume that we are given historical prices of future contracts and , , , in discrete time points and , where and .

For geometric Brownian motion model the calibration methodology is not very complicated. We analyze the returns of future prices of instrument and is its mean, is its variance and correlation parameter is simply the correlation between returns of two instruments. But for interest rate model the calibration is quite complicated, especially for multidimensional HJM model [7]. Calibration for discussed Vasicek model is presented below.

Let us consider following process

From Itô lemma we know that

We could write that because this function depends only from the difference between the maturity time and the time point . If we then consider the process

we know that is normally distributed with mean

and variance

Knowing the form of functions (1),(3) we see that

| (7) |

and

| (8) |

After discretisation and for assumption that , and we could say that the estimator of has the form

where

and we put

It is easy to notice that the correlation parameter between processes and is , so we have

At the end we should calculate also parameters connected with process . From equation (6) we know that for i=1,2

We know that the process

is normally distributed with mean and variance so we have that for

and

where

and

6 Simulation and Conclusion

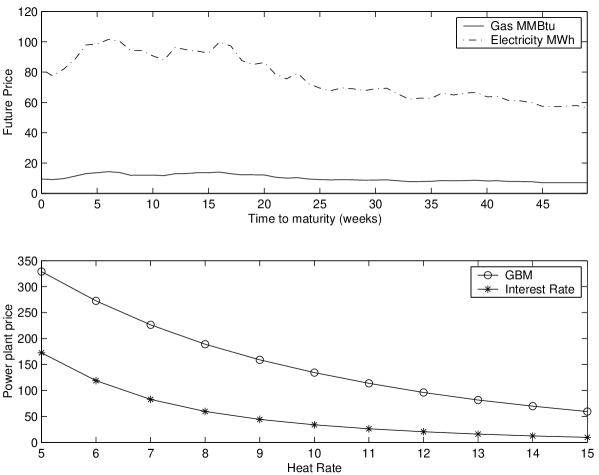

For simulation I used data from New York Mercantile Exchange (NYMEX). I considered historical quotation of future natural gas (Henry Hub) and electricity (PJM) contracts since January, 2004 until March, 2006. The parameters were calculated using calibration methods described before. All estimated parameters are presented in Table 6. I assumed that the constant interest rate is . For valuation of gas fired power plant I assumed that the life-time of the power plant is years and USD, USD.

TABLE I

Estimated parameters for GBM model and for interest rate model using historical data from New York Mercantile Exchange.

| Geometric Brownian Motion | Interest Rate Model |

|---|---|

| 1.0945 | 0.0678 |

| 1.2943 | 0.0042 |

| 4.4098 | 3.7515 |

| 4.8145 | 1.8205 |

| 0.8688 | 0.1892 |

| 0.7266 | |

| 0.0668 |

In Figure 1. we see the value of power plant for the heat rate ranging from 5 to 15 for both presented models. We could notice that there is difference in changes dynamic for analyzed models. The value of power plant for interest rate model is much more smaller than for GBM model and it tends to zero when the heat rate goes up. It is a very good feature, because in reality the value of power plant for heat rate greater than should be close to zero. Looking at work of Deng we could say, that the value of power plant under GBM model is usually too high, so also in this aspect the interest rate model gives better results.

References

- [1] J. Hinz, L. Grafenstein, M. Verschuere, M. Wilhelm, Quantitative Finance 5, 49, (2005).

- [2] M. Musiela, M. Rutkowski Martingale Methods in Financial Modelling, Springer (1997).

- [3] S. Deng, B. Johnson, A. Sogomonian, Proceedings of the Chicago Risk Management Conference (1998).

- [4] A. Weron, R. Weron, Power Exchange: Tools for Risk Management, CIRE, Wrocław, (2000).

- [5] E. Ronn, Real Option and Energy Management: Using Options Methodology to Enhance Capital Budgeting Decisions, Risk Books (2004).

- [6] S. Deng: POWER papers (2000).

- [7] E. Broszkiewicz-Suwaj, A. Weron, Acta Physica Polonica B 37, (2006).