Violation of market efficiency in transition economies

Abstract

We analyze the European transition economies and show that time series for most of major indices exhibit (i) power-law correlations in their values, power-law correlations in their magnitudes, and (iii) asymmetric probability distribution. We propose a stochastic model that can generate time series with all the previous features found in the empirical data.

pacs:

02.50.-r; 05.40.-a; 87.10.+e; 87.90.+y; 95.75.WxAn interesting question in economics is whether markets in transition economies defer in their behavior from developed capital markets. One way to analyze possible differences in behavior is to test the weak form of market efficiency that states that the present price of a stock comprises all of the information about past price values implying that stock prices at any future time cannot be predicted. In contrast to predominant behavior of financial time series of developed markets characterized by no or very short serial correlations Fama65 ; Gra64 ; Sha77 ; hiemstra , it is believed that financial series of emerging markets exhibit different behavior jagric .

For ten transition economies in east and central Europe with statistics reported in Table 1, we analyze time series of index returns , daily recorded.

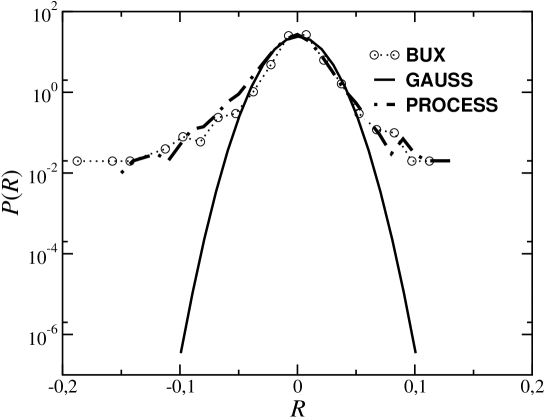

Table 1 shows that none of the index time series exhibits a vanishing skewness defined as a measure of asymmetry — — where and are the expectation and the standard deviation, respectively. Five of time series show positive skewness, i.e., their probability distributions have more pronounced right tail, while the rest five time series exhibit negative skewness. Fig. 1 shows the probability distribution of the BUX index with negative skewness and the Gaussian distribution clearly with vanishing skewness.

Next we calculate the kurtosis defined as that is e.g. for a Gaussian distribution equal to 3. Generally, for a probability distribution with more (less) weight in the tails, the kurtosis is greater (smaller) than 3. Table 1 shows that for none of the ten index time series the observed probability distribution is a Gaussian.

To analyze correlations in time series, we employ the detrended fluctuation analysis (DFA) CKP , the wavelet analysis and the Geweke and Porter-Hudak (GPH) method GPH . The detrended fluctuation function follows a scaling law if the time series is power-law auto-correlated. A DFA scaling exponent corresponds to time series with power-law correlations, and corresponds to time series with no auto-correlations. For GPH method, the process is said to exhibit long memory if the GPH parameter is from the range .

For each of ten indices time series , Table 1 shows the DFA scaling exponent , Hurst exponent calculated by wavelet analysis, and the GPH parameter . We show that DFA and wavelet analysis give similar results. Besides SAX and perhaps WIG20 index, the other indices exhibit power-law serial correlations. Similar results are obtained by GPH method where the relation is expected in presence of power-law correlations.

Next, we calculate the DFA scaling exponents for the time series of . From Table 2 we see that for each index, the time series shows power-law auto-correlations, a common behavior on stock markets, where generally .

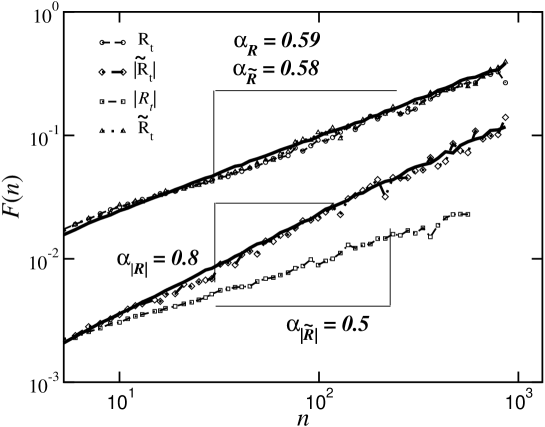

In order to investigate to which degree the ten time series exhibit linear and nonlinear properties Euro ; Ashk20 , we phase randomize the original time series where the procedure changes (does not change) magnitude auto-correlations for a nonlinear (linear) process PodHosk . During phase-randomization procedure one performs a Fourier transform of the original time series and then randomizes the Fourier phases keeping the Fourier amplitudes unchanged. At the end, one calculates an inverse Fourier transform and obtains the surrogate time series .

For the BUX index, Fig. 2 shows the DFA functions of the time series and together with of the phase-randomized surrogate time series and . As expected, the curves of and are the same Euro . In contrast, the time series is uncorrelated , while the time series is power-law auto-correlated . Similar behavior in scaling of time series we find for all other 10 indices (see Table 1).

Next we propose a stochastic process to model time series with power-law correlations in both and together with asymmetric probability distributions ASYMM

| (1) | |||||

| (2) |

The weights defined as for scales as , where are scaling parameters. It holds that . If asymmetry parameter is zero, the process is a combination of two fractionally integrated processes in Refs. Granger80 ; Hosk81 and Granger96 . is a Gamma function, and denotes Gaussian white noise with and , where we set to model the variance of empirical data.

In Ref. PodHosk for the case , , we derived the following two scaling relations and between two DFA exponents and and . To model empirical time series with different exponents and , we allow and to be different.

Applied the process to model empirical data, first we calculate DFA exponents and and if , we calculate and from scaling relations and , respectively. For the Hungarian BUX index, from the DFA exponents and (see Table 1) and previous scaling relations, we calculate the parameters and . In Fig. 2 we show the scaling function for both model time series and (solid lines), where we arbitrarily set to account for small skewness in the empirical distribution. After performing phase-randomization procedure, auto-correlations in vanish, while auto-correlations in practically remain the same as in the original time series , that is the same behavior as we found in empirical data. In Fig.1 we also find that calculated for the process fits calculated for the BUX index.

In conclusion, we show that for ten transition economies their market indices analyzed exhibit (i) power-law correlations in index returns, (ii) power-law correlations in the magnitudes, where the probability distributions exhibit (iii) asymmetric behavior. These three properties we model with a stochastic process specified by only three parameters.

| country | ||||||||||

| index | ||||||||||

| st. dev. | 0.022 | 0.014 | 0.014 | 0.007 | 0.010 | 0.019 | 0.014 | |||

| skewness | -0.446 | -0.409 | 0.416 | 1.240 | 2.944 | 0.731 | ||||

| kurtosis | 11.97 | 9.48 | 25.34 | 17.18 | 26.89 | 22.46 | 47.80 | 12.51 | ||

| 0.58 | ||||||||||

| 0.70 | ||||||||||

| 0.57 | ||||||||||

| 0.52 | ||||||||||

| data points | 1522 |

| country | Rus | Pol | Czech | Hun | Slovak | Sloven | Cro | Lith | Latv | Est |

|---|---|---|---|---|---|---|---|---|---|---|

| index | RTS | WIG20 | PX50 | BUX | SAX | SBI | CROEMI | VILSE | RICI | TALSE |

| 0.60 | 0.56 | 0.63 | 0.59 | 0.53 | 0.62 | 0.58 | 0.63 | 0.58 | 0.70 | |

| 0.65 | 0.57 | 0.65 | 0.63 | 0.53 | 0.66 | 0.62 | 0.63 | 0.62 | 0.65 | |

| 0.11 | 0.02 | 0.27 | 0.07 | 0.01 | 0.14 | 0.10 | 0.10 | 0.15 | 0.07 |

References

- (1) E. F. Fama, J. Business 38, 34 (1965).

- (2) C.W.J. Granger and O. Morgenstern (1963).

- (3) J. L. Sharma and R. E. Kennedy, J. Fin Qua Analysis 12(3), 391 (1977)

- (4) C. Hiemstra and J.D. Jones, J. Emp. Finance 4, 373 (1997).

- (5) T. Jagric, B. Podobnik and M. Kolanovic, East. Econ. 72, (2005).

- (6) C.-K. Peng et al., Phys. Rev. E 49, 1685 (1994).

- (7) J. Geweke and S. Porter-Hudak, J. Time Series Analysis 4. 221 (1983)

- (8) J. Theiler et al., Physica D 58, 77 (1992).

- (9) Y. Ashkenazyet al., Phys. Rev. Lett. 86, 1900 (2001).

- (10) B. Podobnik et al., Phys. Rev. E 72, 026121 (2005).

- (11) B. Podobnik et al., Phys. Rev. E 71, 025104 (2005).

- (12) C. W. J. Granger and R. Joyeux, J. Time Series Analysis 1, 15 (1980).

- (13) J. Hosking, Biometrika 68, 165 (1981).

- (14) C. W. J. Granger and Z. Ding, J. Econometrics 73, 61 (1996).

- (15) John T. Barkoulas, Christopher F. Baum, Economies Letters 53, 253 (1996).