Asset Price Dynamics in a Financial Market with Heterogeneous Trading Strategies and Time Delays

Abstract

In this paper we present a continuous time dynamical model of heterogeneous agents interacting in a financial market where transactions are cleared by a market maker. The market is composed of fundamentalist, trend following and contrarian agents who process information from the market with different time delays. Each class of investor is characterized by path dependent risk aversion. We also allow for the possibility of evolutionary switching between trend following and contrarian strategies. We find that the system shows periodic, quasi-periodic and chaotic dynamics as well as synchronization between technical traders. Furthermore, the model is able to generate time series of returns that exhibit statistical properties similar to those of the SP500 index, which is characterized by excess kurtosis, volatility clustering and long memory.

Key words Dynamic asset pricing; Heterogeneous agents; Complex dynamics; Chaos; Stock market dynamics;

PACS 89.65.Gh, 89.75-k, 89.75.Fb, 89.90.+n

1 Introduction

In recent years there has been a growing disaffection with the standard paradigm of efficient markets and rational expectations. In an efficient market, asset prices are the outcome of the trading of rational agents, who forecast the expected price by exploiting all the information available and know that other traders are rational. This implies that prices must equal the fundamental prices and therefore changes in prices are only caused by changes in the fundamental value. In real markets, however, traders have different information on traded assets and process information differently, therefore the assumption of homogeneous rational traders may not be appropriate. The efficient market hypothesis motivates the use of random walk increments in financial time series modeling: if news about fundamentals are normally distributed, the returns on an asset will be normal as well. However the random walk assumption does not allow the replication of some stylized facts of real financial markets, such as volatility clustering, excess kurtosis, autocorrelation in square and absolute returns, bubbles and crashes. Recently a large number of models that take into account heterogeneity in financial markets has been proposed. contributions to this literature include [1, 2, 3, 4, 11, 12]. [13] analyze a market composed of a continuum of fundamentalists who show delays in information processing. These models allow for the formation of speculative bubbles, which may be triggered by news about fundamentals and reinforced by technical trading. Because of the presence of nonlinearities according to which different investors interact with one another, these models are capable of generating stable equilibria, periodic, quasi-periodic dynamics and strange attractors. This paper builds on the model of [13], which is inspired by the models of thermodynamics of [7], [9], [10] and analyzes a financial market in which there are only fundamental investors who trade according to the mispricing of the asset with delays which are uniformly distributed from initial to current time. We generalize [13] by introducing a continuum of technical traders who behave as either trend followers or contrarians and a switching rule between these technical trading rules. We will analyze how the interaction of different types of investors with path dependent risk aversion determines the dynamics and the statistical properties of the system as key parameters are changed.

2 The model

Let us consider a security continuously traded at price Assume that this security is in fixed supply, so that the price is only driven by excess demand. Let us assume that the excess demand is a function of the current price and the fundamental value . A market maker takes a long position whenever the excess demand is negative and a short position whenever the demand excess is positive so as to clear the market. The market maker adjusts the price in the direction of the excess demand with speed equal to . The instantaneous rate of return is:

| (1) |

the fundamental value is assumed to grow at a constant rate g, therefore:

| (2) |

The market is composed of an infinite number of investors, who choose among three different investment strategies. Let us assume that a fraction of investors follows a fundamentalist strategy and a fraction follows a technical analysis strategy. The fraction of technical analysts is in turn composed of a fraction of trend followers and a fraction of contrarians. Let , and be respectively the demands of fundamentalists, trend followers and contrarians rescaled by the proportions of agents who trades according to a given strategy. The excess demand for the security is thus given:

| (3) |

Each trader operate with a delay equal to , that is, the demand of a particular trader at time depends on her decision variable at time . Time delays are uniformly distributed in the interval . Fundamentalists react to differences between price and fundamental value. The demand of fundamentalists operating with delay is:

| (4) |

where is a parameter that measures the speed of reaction of fundamental traders; we will assume that throughout the paper. This demand function implies that the fundamentalists believe that the price tends to the fundamental value in the long run and reacts to the percentage mispricing of the asset in symmetric way with respect to underpricing and overpricing. If time delays are uniformly distributed, the market demand of fundamentalists is given by:

| (5) |

time differential yields:

| (6) |

Following [13], let us modify equation (6) by introducing the variable and adding a term to the RHS:222[13] introduce the variable , which is a liner transformation of , and utilize it instead of in the simulations. We will continue to utilize without any loss of generality.

| (7) |

According to the sign of , if there is an excess demand, the term either drives it towards zero (if is positive) or foster it (if is negative). The variable may be interpreted as in indicator of the risk that traders bear and their risk aversion (if is negative traders become risk-seekers). The dynamics for are given by:

| (8) |

where is a factor controlling the variance. Throughout the paper we will assume that is given. The rationale of (8) is that the larger an open position on the asset, the more risk averse the agents become. Let us consider now the behavior of technical traders. As for the fundamentalists, their time delays are uniformly distributed in the interval . A trader operating with delay utilizes the percentage return that occurred at time in a linear prediction rule in order to form an expectation of future returns. Let and be respectively the demands of trend followers and contrarians operating with delay . Without taking risk attitudes into account, technical demands are given by:

| (9) |

Throughout the paper we will assume that and . By integrating (9) with respect to , time differentiating and adding respectively the terms and in order to take into account the risk and risk attitudes of technical traders, we get:

| (10) |

the dynamics for and have the same functional form as :

| (11) |

We will now consider the fraction as given, whereas the fraction of trend followers may be path dependent. In fact, is considered as an endogenous variable because both trend followers and contrarians follow technical trading strategies and therefore may be likely to switch them if one is more profitable than the other. We assume that the more profitable is a strategy, the more investors will choose that strategy. The difference in the absolute return at time between the two strategies is given by .333The use of absolute returns as a measure of evolutionary fitness stems from the absence of wealth in the model, therefore it is not possible to define the percentage return of a strategy. Moreover, must be bounded in the interval and we assume that it tends to move towards 0.5 if both strategies lead to equal profits. These assumption hold if we assume that dynamics for is the following:

| (12) |

where the first term keeps the fraction of trend followers bounded in the interval and is a parameter that measure the speed of switching between the technical strategies. If z=0 or if the proportion of trend followers and contrarians is taken as a constant, then the system may be made stationary by defining the variable , whose time derivative is:

| (13) |

3 Statistical properties

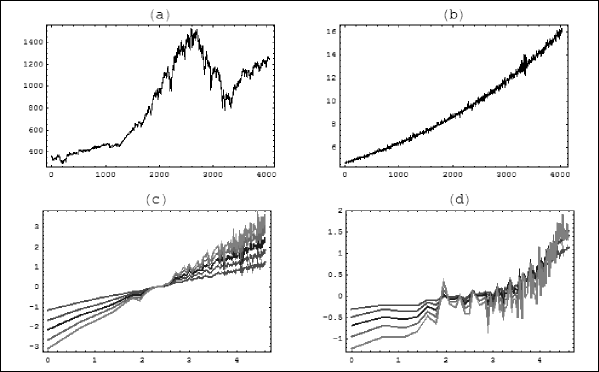

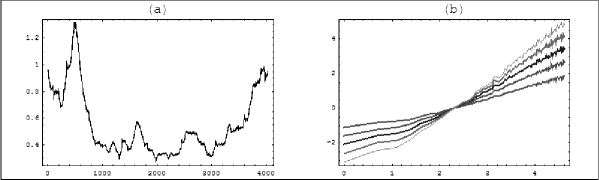

In this section, we analyze the statistical properties of the simulated time series, which have been generated by integrating the system up to time 9035 and recording the price at integer times starting from in order to allow the system to get sufficiently close to the asymptotic dynamics and to have time series as long as the daily time series of the SP500 index between 1 January 1990 and 31 December 2005. The system has been integrated by utilizing Mathematica 5.1. No stochastic elements are added, therefore the features of system-generated time series are endogenous and originate from the nonlinear structure of the systems. The model displays statistical properties similar to those of the index SP500 using various parameter values. In Table (1) there are reported the statistics of the daily returns on the SP500 and on the time series generated by the system with parameters , , , , , , , , and initial values , , , , . We have also reported the value of the largest Lyapunov exponent. The growth rate of the fundamental, , is equal to the mean growth rate of SP500, which in turn has been calculated as the rate that in a continuously compounded capitalization regime implies the same return on the index on the overall period. Since the price moves around the fundamental, the mean of the simulated time series match that of the SP500. The other parameter values have been chosen so as to give rise to statistics similar to those of the SP500 index. As pointed out by [13], kurtosis and volatility clustering are due to the delayed reaction of investors that determines price overshooting. In a multi-agent modeling, such a process is fostered by the interaction among investors who are heterogeneous not only as concerns the time that they need to process information from the market, but also the strategies that they use to predict future prices. Time series are also characterized by long memory and nonlinear structure, which in turn imply that volatility clustering occurs at different time scales. Such characteristics are typical of multifractal process. According to [8], a multifractal process is a continuous time process with stationary increments which satisfy:

| (14) |

under existence conditions given in [8]. Assuming that Table (2) reports the of a regression of against with . is the daily closure of SP500 and the model-generated time series. Figure (1) reports the time series and the - plot after normalizing by subtracting . Time intervals range from 1 to 100 days. There is no apparent crossover up to a scale of 100 days in the SP500 and the linear fit is very good, in accord with the behavior of a multifractal process. Crossover occurs in the simulations for values of between and and the fluctuations are more erratic than those of SP500. Such a behavior underlines the capability of the model to generate dynamics typical of a multifractal process, however the dynamics for the fundamental implies that price is mean-reverting around an exponenential trend, which in turn implies that crossover occurs for smaller time intervals than those of real time series. The introduction of stochastic noises or a feedback between fundamental and price determines more a realistic long-run behavior and scaling properties, as we will show for the latter case in Section 4.4.

4 Sensitivity analysis

In this section we will first

analyze the system dynamics and then we will study the variations in dynamics as some key parameters

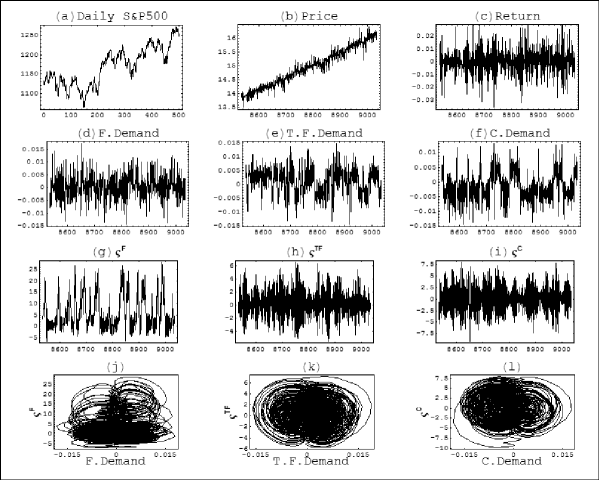

are changed. In Figure (2) there are depicted the time

series of the last 500 observations of prices of SP500 and

model, returns, demands, risk attitudes and the projections of the

phase space on the planes , , . Tables (3,4,5) show statistics

for different parameters values. The demands of technical traders

switch between positive and negative phases, differently from the

fundamentalist demand, which instead tends to move around zero. The

presence of long phases of positive and negative demands of

technical traders, together with the dynamics for the risk aversions

may determine very large price oscillations in both directions. The

increase in the fundamental value triggers a stock price increase

due to the purchases by fundamentalists, which is reinforced by the

action of trend followers. The demand of fundamentalists has smaller

oscillations in the periods where the risk aversion is high, because

a high risk aversion induces the fundamentalists not to open large

positions if the stock is mispriced. Whereas the risk aversion of

fundamentalists follows well defined trends and is on average

positive, those of technical traders tends to oscillate around zero.

As such, technical traders switch between phases in which they are

risk averse and phases in which are risk seekers. The dynamics for

the risk attitudes may be explained in the following way: let us

assume that the price is rising and the demand of trend followers is

positive and greater than . Equation

(11) implies that their risk aversion rises as well. The

increase in price reduces the demand of fundamentalists and

contrarians, but reinforces that of trend followers, which on the

other hand tends to fall because of the increase in their risk

aversion. Once the price falls, the demand of trend followers

approaches zero (eventually becoming negative) and, as a

consequence, their risk aversion falls. The dynamics are also the

same in the case where the cycle is triggered by fundamentalists or

contrarians. Risk attitudes may vary considerably even during phases

in which the demands are almost steady. Indeed it is sufficient that

the absolute value of the demand of investors type remains for a

long time respectively above to get a considerable

change in risk aversion. The time derivatives of the risk attitudes

tend to reach their lower bounds, which are respectively equal to

,

and , only when the demands are

very close to zero.

4.1. Effects of changing the proportion of fundamentalists and

technical traders. In order to analyze the effect of the proportion

of fundamentalists and technical traders, we select values of

ranging from 0 to 1 and with a difference of 0.1 between a

simulation and the next. If there are no fundamentalists or if their

proportion is only ten percent, the price goes to infinity, because

technical trading drives the price away from the

fundamental.444 The price goes to zero with other parameter

values. What matters here is that the price does not match the

fundamental in the long run. If the fundamentalists

are able to steer the price to the fundamental value, but prices are

subject to large oscillations induced by technical traders. Such

oscillations become larger and larger as time goes on. In fact

larger departures from the fundamental value are needed for the

fundamentalists to bring the price back close to the fundamental

value. When the departure from the fundamental value

brings about long phases in which the fundamentalists go either long

or short on the asset, determining in this way an increase in their

risk aversion. This in turn implies a lower capability of offsetting

technical traders. The overall demand of the latter presents long

phases in which the demand is either positive or negative, phases in

which it changes sign quickly and phases where the demands of

contrarians and trend followers synchronize and offset each other.

During phases of synchronization the system reduces by one

dimension. When the technical demand is equal or close to zero,

fundamentalists bring the price back close to the fundamental value.

As a consequence of the fact that the total demand does not change

sign for long periods, the price tends to follow a monotonic

trajectory when it is far from the fundamental and to oscillate as

it gets close to it. Thus, the synchronization of technical traders

determines an intermittent behavior in the system with regular

monotonic phases interrupted by chaotic bursts. The time series of

fundamentalist and technical demands are depicted in Table (3).555The Lyapunov exponent is not

reported for because is meaningless when the

dynamics are not bounded. If the proportion of

fundamentalist is sufficiently high as to prevent technical trading

from bringing about larger and larger departures from the

fundamental value. The oscillations have anyway larger amplitudes

than in the case where , and this in turn determines an

increase in the variance and a decrease in the kurtosis. If

fundamentalists account for half of the investors, the demand of

technical traders is generally lower than in the baseline case

because fundamental trading prevents strong changes in the price.

This leaves little room for a persistent phase of fundamentalist

demand and therefore fundamentalists are more likely to became risk

seekers. The higher proportion of fundamentalists determines a more

regular behavior of the system, as denoted by the decrease in

kurtosis. If the fraction of fundamentalists is equal to or greater

than sixty percent, the system no longer converges to a strange

attractor, but to a quasi-periodic attractor, as denoted by the

values of the Lyapunov exponents. If there are only fundamentalists

the attractor becomes strange again and the Lyapunov exponent rises

up to 0.53689, which would indicate a highly chaotic system. However

the rise in the Lyapunov exponent is due to the increase in the

amplitudes of the oscillations that in turn are due to the

overreaction induced by the delayed reaction of fundamentalists,

which brings price above (below) the fundamental price when the

security is originally underpriced (overpriced).

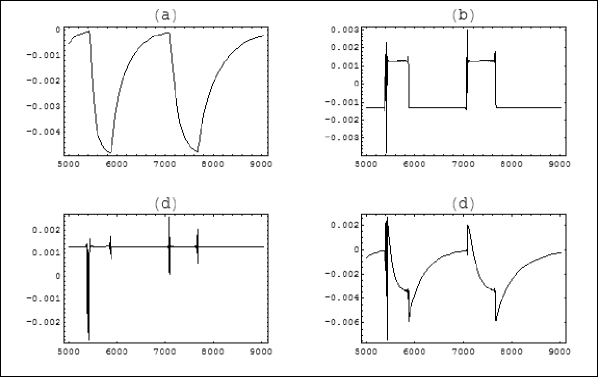

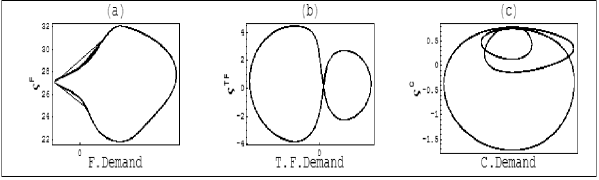

4.2. Effects of changing the speed of expected price adjustment

of fundamentalists. Increasing the speed reaction of

fundamentalists brings about a decrease in the variance because the

price tends to stay close to the fundamental. The system undergoes a

global bifurcation as the parameter is increased,

indeed the dynamics show a cyclical behavior after a transient

chaotic phase. This kind of transition, called attractor

destruction, is a type of crisis-induced intermittency and has been

investigated by [5] and [6]. However, for large

values of the attractor becomes strange again. Because

of the presence of technical traders, which are affected by the

changes in prices triggered by the fundamentalists, it is not

possible to determine what the dynamics eventually are as the

reaction speed of the fundamentalists is further increased. For

instance, if the dynamics are periodic, but if if

the attractor is strange, with a Lyapunov exponent

of 0.240495. The projections of a limit cycle to which the system

converges when are represented in Figure

(4)

4.3. Effects of switching between trend following and

contrarian strategies. So far we have dealt with a model where the

proportion between trend followers and contrarians are kept

constant. If such proportions become path dependent. The

higher the value of , the higher the fraction of trend followers

because this strategy is generally more profitable than the

contrarian one, since price grows in the long run. Simulations for

different values of show that a higher proportion of trend

followers causes greater departures from the fundamental value

triggering a reaction by all types of investors. Such dynamics bring

about an increase in the variance and skewness of returns. Skewness

tends to increase because overshooting is positive on average, since

price tends to follow an exponentially growing fundamental. Kurtosis

first tends to increase and then to decrease because the increase in

variance for high values of determines that some returns

previously in the tails of the distribution now approach the center.

4.4. Effects of introducing a feedback between price and

fundamental. We will assume now that the fundamental value is

affected by the asset price. The economic rationale is that a higher

price boosts consumption and, as a consequence, the real economy as

a whole. We assume that the dynamics of the fundamental follows the

differential equation:

| (15) |

The introduction of this kind of feedback induces a unit root behavior in the price time series with scaling properties very to those of S&P500. This is apparent from Figure (5) where there are reported the simulated time series and the plot of against and from the regression analysis. Indeed the values are , , , , .

5 Conclusion

In this paper we have outlined a continuous time deterministic model of a financial market with heterogeneous interacting agents. The dynamical system is able to generate some stylized facts present in real markets, even in a purely deterministic setting: excess kurtosis, volatility clustering and long memory. Even in the case where fundamentalists are the only agents present in the market, they are unable to drive the price back to the fundamental on a steady state trajectory. Moreover, the increase in the fundamentalist reaction speed may even increase the disorder in the system, because the fundamentalists trigger a strong response of technical traders. It may also be possible that, when the fraction of fundamentalists is low, trend followers and contrarians give rise to synchronization in the system, bringing about a dramatic change in the dynamics. The introduction of an evolutionary switching between technical traders leads to an increase in the volatility and in the kurtosis, provided that the speed of switching is not too high because otherwise the increase in the variance makes it less likely that returns will fall in the tails of the distributions. Further research will take into account more realistic distribution functions for the agents, the introduction of stochastic disturbances and a deeper investigation of the interaction between price and fundamental.

References

- [1] A. Beja and M. Goldman, J.Finance 35 (1980), 235-248.

- [2] W. A. Brock and C. H. Hommes, Heteroeneous beleiefs and routes to chaos in a simple asset pricing model, Journal of Economic Dynamics and Control 22 (1998), 1235-1274.

- [3] C. Chiarella, The dynamics of speculative behavior, Annals of Operations Research 37 (1992), 101-124

- [4] C. Chiarella and X.Z. He, Asset Pricing and wealth dynamics under heterogeneous expectations, Quant. Finance 1 (2001), 509-526.

- [5] C. Grebogi, E. Ott and J.A. Yorke, Critical exponent of chaotic transientin nonlinear dynamical systems, Phys. Rev. Lett. 57 (1986), 1284-1287.

- [6] C. Grebogi, E. Ott, F. Romeiras, and J.A. Yorke, Critical exponent for crisis-induced intermittency, Phys. Rev. A 36 (1987), 5365-5380.

- [7] W.G. Hoover, Canonical dynamics: equilibrium phase-space distributions, Phys. Rev. A 31 (1985), 1695-1697.

- [8] B. Mandelbrot, A. Fisher, and L. Calvet, A multifractal model of asset returns, Working paper, Cowles Foundation Discussion Papers 1164 (1997).

- [9] S. Nosè, A molecular dynamics method for simulation in the canonical ensemble, J. Chem. Phys. 81 (1984a), 511-519.

- [10] S. Nosè, Molecular dynamics simulations, Progress of Theoretical Physics Supplement 103 (1984b), 1-49.

- [11] F. Westerhoff, Greed, fear and stock market dynamics, Physica A 343C (2004a), 635-642.

- [12] F. Westerhoff, Market depth and price dynamics: a note, Int. J. Mod. Phys. C 15 (2004b), 1005-1012.

- [13] S. Thurner, E.J. Dockner, A. Gaunersdorfer, S. Thurner, E.J. Dockner, and A. Gaunersdorfer, Asset price dynamics in a model of investors operating on different time horizon, Working paper, SFB-WP 93, University of Vienna (2002).

| Mean | Variance | Skewness | Kurtosis | Jar.Bera | Lyap.exp. | |

|---|---|---|---|---|---|---|

| SP500 | 0.0003597 | 0.0001026 | -0.0146 | 6.700 | 421.9 | |

| Model | 0.0003617 | 0.0001100 | -0.0293 | 6.115 | 1632 | 0.2500 |

} SP500 0.9870 0.9854 0.9820 0.9771 0.9707 Model 0.848 0.8287 0.7980 0.7492 0.6769

| Mean | Variance | Skewness | Kurtosis | Jar.Bera | Lyap.exp. | |

|---|---|---|---|---|---|---|

| 0.2 | 0.004344 | 0.00527 | 0.7748 | 3.330 | 421.9 | |

| 0.3 | 0.00088 | 0.001154 | 0.1378 | 4.107 | 218 | 0.269 |

| 0.4 | 0.0003631 | 0.0001100 | -0.02968 | 6.115 | 1631 | 0.2500 |

| 0.5 | 0.0003317 | 0.00004472 | 0.2504 | 5.153 | 821.1 | 0.1718 |

| 0.6 | 0.0004837 | 0.0003519 | 0.02186 | 1.595 | 331.9 | 0.1118 |

| 0.7 | 0.0005229 | 0.0004317 | 0.01568 | 1.514 | 370.8 | 0.03375 |

| 0.8 | 0.000437 | 0.0002437 | 0.01894 | 1.774 | 252.7 | 0.03621 |

| 0.9 | 0.0004538 | 0.0002923 | 0.130 | 6.439 | 1999 | 0.03992 |

| 1 | 0.0005047 | 0.0003806 | 0.6031 | 22.05 | 61275 | 0.536 |

| Mean | Variance | Skewness | Kurtosis | Jar.Bera | Lyap.exp. | |

|---|---|---|---|---|---|---|

| 19/15 | 0.0005586 | 0.000495 | 0.1102 | 3.876 | 137.1 | 0.2446 |

| 38/15 | 0.0004701 | 0.0003267 | 0.134 | 4.030 | 190.4 | 0.2222 |

| 57/15 | 0.0004320 | 0.0002342 | -0.01053 | 3.660 | 73.46 | 0.2639 |

| 76/15 | 0.0003842 | 0.0001536 | 0.02541 | 3.694 | 81.51 | 0.248 |

| 95/15 | 0.0003631 | 0.0001100 | -0.02968 | 6.115 | 1631 | 0.2500 |

| 114/15 | 0.0003550 | 0.00009703 | 0.05448 | 6.398 | 1942 | 0.2242 |

| 133/15 | 0.0003584 | 0.0001020 | 0.1003 | 4.627 | 451.7 | 0.05490 |

| 152/15 | 0.0003565 | 0.0001000 | 0.04832 | 4.922 | 622.6 | 0.2196 |

| 171/15 | 0.0003468 | 0.00007810 | -0.155 | 1.819 | 250.6 | 0.2118 |

| 190/15 | 0.00034 | 0.00007369 | 0.0004368 | 5.462 | 1019 | 0.002247 |

| 190 | 0.0003355 | 0.00005448 | -0.06733 | 1.931 | 194.9 | 0.07157 |

| 300 | 0.0004425 | 0.0002832 | 0.2366 | 3.589 | 96.09 | 0.2404 |

| z | Mean | Variance | Skewness | Kurtosis | Jar.Bera |

|---|---|---|---|---|---|

| 5 | 0.000359 | 0.0001042 | 0.06756 | 6.268 | 1798 |

| 10 | 0.0003588 | 0.0001083 | 0.1103 | 5.439 | 1007 |

| 20 | 0.0003643 | 0.0001146 | 0.08794 | 5.663 | 1197 |

| 30 | 0.0003838 | 0.0001539 | 0.1881 | 10.533 | 9560 |

| 40 | 0.0003900 | 0.0001465 | 0.1540 | 8.243 | 4635 |

| 60 | 0.0004234 | 0.0002252 | 0.3276 | 7.064 | 2848 |

| 80 | 0.0004667 | 0.0003244 | 0.3391 | 7.810 | 3965 |