Ideal-gas like market models with savings: quenched and annealed cases

Abstract

We analyze the ideal gas like models of markets and review the different cases where a ‘savings’ factor changes the nature and shape of the distribution of wealth. These models can produce similar distribution of wealth as observed across varied economies. We present a more realistic model where the saving factor can vary over time (annealed savings) and yet produces Pareto distribution of wealth in certain cases. We discuss the relevance of such models in the context of wealth distribution, and address some recent issues in the context of these models.

pacs:

89.20.Hh,89.75.Hc,89.75.Da,43.38.SiI Introduction

The study of wealth distribution cc:EWD05 in a society has remained an intriguing problem since Vilfredo Pareto who first observed cc:Pareto:1897 that the number of rich people with wealth decay following an inverse:

| (1) |

is number density of people possessing wealth , and is known as the Pareto exponent. This exponent generally assumes a value between and in varied economies cc:realdatag ; cc:realdataln ; cc:Sinha:2006 . It is also known that for low and medium income, the number density falls off much faster: exponentially cc:realdatag or in a log-normal way cc:realdataln .

In recent years, easy availability of data has helped in the analysis of wealth or income distributions in various societies cc:EWD05 . It is now more or less established that the distribution has a power-law tail for the large (about 5% of the population) wealth/income cc:realdatag ; cc:realdataln ; cc:Sinha:2006 , while the majority (around 95%) low income distribution fits well to Gibbs or log-normal form.

There has been several attempts to model a simple economy with minimum trading ingredients, which involve a wealth exchange process cc:othermodels that produce a distribution of wealth similar to that observed in the real market. We are particularly interested in microscopic models of markets where the (economic) trading activity is considered as a scattering process cc:marjit ; cc:Dragulescu:2000 ; cc:Chakraborti:2000 ; cc:Hayes:2002 ; cc:Chatterjee:2004 ; cc:Chatterjee:2003 ; cc:Chakrabarti:2004 ; cc:Slanina:2004 (see also Ref. cc:ESTP:KG for a recent extensive review). We concentrate on models that incorporate ‘savings’ as an essential ingredient in a trading process, and reproduces the salient features seen across wealth distributions in varied economies (see Ref. cc:EWD:CC for a review). Angle cc:Angle:1986 studied inequality processes which can be mapped to the savings wealth models is certain cases; see Ref. cc:Angle:2006 for a detailed review.

These studies also show (and discussed briefly here) how the distribution of savings can be modified to reproduce the salient features of empirical distributions of wealth – namely the shape of the distribution for the low and middle wealth and the tunable Pareto exponent. In all these models cc:Chakraborti:2000 ; cc:Hayes:2002 ; cc:Chatterjee:2004 ; cc:Chatterjee:2003 ; cc:Chakrabarti:2004 , ‘savings’ was introduced as an annealed parameter that remained invariant with time (or trading).

Apart from a brief summary of the established results in such models, here we report some new results for annealed cases, where the saving factor can change with time, as one would expect in a real trading process. We report cases where the wealth distribution is still described by a Pareto law. We also forward some justification of the various assumptions in such models.

II Ideal-gas like models of trading

We first consider an ideal-gas model of a closed economic system. Wealth is measured in terms of the amount of money possessed by an individual. Production is not allowed i.e, total money is fixed and also there is no migration of population i.e, total number of agents is fixed, and the only economic activity is confined to trading. Each agent , individual or corporate, possess money at time . In any trading, a pair of agents and randomly exchange their money cc:marjit ; cc:Dragulescu:2000 ; cc:Chakraborti:2000 , such that their total money is (locally) conserved and none end up with negative money (, i.e, debt not allowed):

| (2) |

time () changes by one unit after each trading. The steady-state () distribution of money is Gibbs one:

| (3) |

No matter how uniform or justified the initial distribution is, the eventual steady state corresponds to Gibbs distribution where most of the people end up with very little money. This follows from the conservation of money and additivity of entropy:

| (4) |

This steady state result is quite robust and realistic. Several variations of the trading, and of the ‘lattice’ (on which the agents can be put and each agent trade with its ‘lattice neighbors’ only) — compact, fractal or small-world like cc:EWD05 , does not affect the distribution.

III Savings in Ideal-gas trading market: Quenched case

In any trading, savings come naturally cc:Samuelson:1980 . A saving factor is therefore introduced in the same model cc:Chakraborti:2000 (Ref. cc:Dragulescu:2000 is the model without savings), where each trader at time saves a fraction of its money and trades randomly with the rest. In each of the following two cases, the savings fraction does not vary with time, and hence we call it ‘quenched’ in the terminology of statistical mechanics.

III.1 Fixed or uniform savings

For the case of ‘fixed’ savings, the money exchange rules are:

| (5) |

where

| (6) |

where is a random fraction, coming from the stochastic nature of the trading. is a fraction () which we call the saving factor.

The market (non-interacting at and ) becomes ‘interacting’ for any non-vanishing : For fixed (same for all agents), the steady state distribution of money is sharply decaying on both sides with the most-probable money per agent shifting away from (for ) to as . The self-organizing feature of this market, induced by sheer self-interest of saving by each agent without any global perspective, is very significant as the fraction of paupers decrease with saving fraction and most people possess some fraction of the average money in the market (for , the socialists’ dream is achieved with just people’s self-interest of saving!). Although this fixed saving propensity does not give the Pareto-like power-law distribution yet, the Markovian nature of the scattering or trading processes (eqn. (4)) is lost and the system becomes co-operative. Indirectly through , the agents get to develop a correlation with (start interacting with) each other and the system co-operatively self-organizes cc:Bak:1997 towards a most-probable distribution.

This model has been understood to a certain extent (see e.g, cc:Das:2003 ; cc:Patriarca:2004 ; cc:Repetowicz:2005 ), and argued to resemble a gamma distribution cc:Patriarca:2004 , and partly explained analytically. This model clearly finds its relevance in cases where the economy consists of traders with ‘waged’ income cc:Willis:2004 .

III.2 Distributed savings

In a real society or economy, is a very inhomogeneous parameter: the interest of saving varies from person to person. We move a step closer to the real situation where saving factor is widely distributed within the population cc:Chatterjee:2004 ; cc:Chatterjee:2003 ; cc:Chakrabarti:2004 . The evolution of money in such a trading can be written as:

| (7) |

| (8) |

One again follows the same rules as before, except that

| (9) |

here; and being the saving propensities of agents and . The agents have fixed (over time) saving propensities, distributed independently, randomly and uniformly (white) within an interval to agent saves a random fraction () and this value is quenched for each agent ( are independent of trading or ). is found to follow a strict power-law decay. This decay fits to Pareto law (1) with for several decades. This power law is extremely robust: a distribution

| (10) |

of quenched values among the agents produce power law distributed with Pareto index , irrespective of the value of . For negative values, however, we get an initial (small ) Gibbs-like decay in . In case , the Pareto exponent is modified to , which qualifies for the non-universal exponents in the same model cc:Chatterjee:2004 ; cc:Mohanty:2006 .

This model cc:Chatterjee:2004 has been thoroughly analyzed, and the analytical derivation of the Pareto exponent has been achieved in certain cases cc:Repetowicz:2005 ; cc:Mohanty:2006 ; cc:Chatterjee:2005 . The Pareto exponent has been derived to exactly .

In this model, agents with higher saving propensity tend to hold higher average wealth, which is justified by the fact that the saving propensity in the rich population is always high cc:Dynan:2004 .

IV Savings in Ideal-gas trading market: Annealed case

In a real trading process, the concept of ‘saving factor’ cannot be attributed to a quantity that is invariant with time. A saving factor always changes with time or trading. In earlier works, we reported the case of annealed savings, where the savings factor changes with time in the interval , but does not produce a power law in cc:Chatterjee:2004 . We report below some special cases of annealed saving which produce a power law distribution of .

If one allows the saving factor to vary with time in , the money distribution does not produce a power law tail.

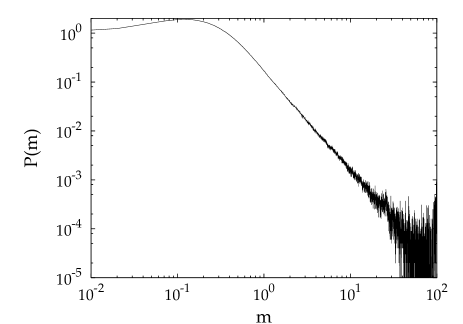

Instead, we propose a slightly different model of an annealed saving case. We associate a parameter () with each agent such that the savings factor randomly assumes a value in the interval at each time or trading. The trading rules are of course unaltered and governed by Eqns. (7) and (8). Now, considering a suitable distribution of over the agents, one can produce money distributions with power-law tail. The only condition that needs to hold is that should be non-vanishing as . Figure 1 shows the case when . Numerical simulations suggest that the behavior of the wealth distribution is similar to the quenched savings case. In other words, only if , it is reflected in the Pareto exponent as .

V Relevance of gas like models

Al these gas-like models of trading markets are based on the assumption of (a) money conservation (globally in the market; as well as locally in any trading) and (b) stochasticity. These points have been criticized strongly (by economists) in the recent literature cc:Gallegati:2006 . In the following, we forward some of the arguments in favour of these assumptions (see also cc:ESOM:2006 ).

V.1 Money conservation

If we view the trading as scattering processes, one can see the equivalence. Of course, in any such ‘money-exchange’ trading process, one receives some profit or service from the other and this does not appear to be completely random, as assumed in the models. However, if we concentrate only on the ‘cash’ exchanged (even using Bank cards!), every trading is a money conserving one (like the elastic scattering process in physics!)

It is also important to note that the frequency of money exchange in such models define a time scale in which the total money in the market does not change. In real economies, the total money changes much slowly, so that in the time scale of exchanges, it is quite reasonable to assume the total money to be conserved in these exchange models. This can also be justified by the fact that the average international foreign currency exchange rates change drastically (say, by more than 10%) very rarely; according to the Reserve Bank of India, the US Dollar remained at INR for the last eight years cc:Sarkar:2006 ! The typical time scale of the exchanges considered here correspond to seconds or minutes and hence the constancy assumption cannot be a major problem.

V.2 Stochasticity

But, are these trading random? Surely not, when looked upon from individual’s point of view: When one maximizes his/her utility by money exchange for the -th commodity, he/she may choose to go to the -th agent and for the -th commodity he/she will go to the -th agent. But since in general, when viewed from a global level, these trading/scattering events will all look random (although for individuals these is a defined choice or utility maximization).

Apart from the choice of the agents for any trade, the traded amount are considered to be random in such models. Some critics argue, this cannot be totally random as the amount is determined by the price of the commodity exchanged. Again, this can be defended very easily. If a little fluctuation over the ‘just price’ occurs in each trade due to the bargain capacities of the agents involved, one can easily demonstrate that after sufficient trading (time, depending on the amount of fluctuation in each trade), the distribution will be determined by the stochasticity, as in the cases of directed random walks or other biased stochastic models in physics.

It may be noted in this context that in the stochastically formulated ideal gas models in physics (developed in late 1800/early 1900) one (physicists) already knew for more than a hundred years, that each of the constituent particle (molecule) follows a precise equation of motion, namely that due to Newton. The assumption of stochasticity here in such models, even though each agent might follow an utility maximizing strategy (like Newton’s equation of motion for molecules), is therefore, not very unusual in the context.

VI Summary and conclusions

We analyze the gas like models of markets. We review the different cases where a quenched ‘savings’ factor changes the nature and shape of the distribution of wealth. Suitable modification in the nature of the ‘savings’ distribution can simulate all observed wealth distributions. We give here some new numerical results for the annealed ‘savings’ case. We find that the more realistic model, where the saving factor randomly varies in time (annealed savings), still produce a Pareto distribution of wealth in certain cases. We also forward some arguments in favour of the assumptions made in such gas-like models.

References

- (1) Econophysics of Wealth Distributions, Eds. A. Chatterjee, S. Yarlagadda, B. K. Chakrabarti, Springer Verlag, Milan (2005)

- (2) V. Pareto, Cours d’economie Politique, F. Rouge, Lausanne and Paris (1897)

- (3) M. Levy, S. Solomon, Physica A 242 90 (1997); A. A. Drăgulescu, V. M. Yakovenko, Physica A 299 213 (2001); H. Aoyama, W. Souma, Y. Fujiwara, Physica A 324 352 (2003)

- (4) A. Banerjee, V. M. Yakovenko, T. Di Matteo, Physica A (2006) also in xxx.arxiv.org/physics/0601176; F. Clementi, M. Gallegati, Physica A 350 427 (2005)

- (5) S. Sinha, Physica A 359 555 (2006)

- (6) S. Sinha, Phys. Scripta T 106 59 (2003); J. C. Ferrero, Physica A 341 575 (2004); J. R. Iglesias, S. Gonçalves, G. Abramson, J. L. Vega, Physica A 342 186 (2004); N. Scafetta, S. Picozzi, B. J. West, Physica D 193 338 (2004)

- (7) B. K. Chakrabarti, S. Marjit, Indian J. Phys. B 69 681 (1995); S. Ispolatov, P. L. Krapivsky, S. Redner, Eur. Phys. J. B 2 267 (1998)

- (8) A. A. Drăgulescu, V. M. Yakovenko, Eur. Phys. J. B 17 723 (2000)

- (9) A. Chakraborti, B. K. Chakrabarti, Eur. Phys. J. B 17 167 (2000)

- (10) B. Hayes, American Scientist, USA 90 (Sept-Oct) 400 (2002)

- (11) A. Chatterjee, B. K. Chakrabarti, S. S. Manna, Physica A 335 155 (2004)

- (12) A. Chatterjee, B. K. Chakrabarti, S. S. Manna, Physica Scripta T 106 36 (2003)

- (13) B. K. Chakrabarti, A. Chatterjee, in Application of Econophysics, Ed. H. Takayasu, Springer, Tokyo (2004) pp. 280-285

- (14) F. Slanina, Phys. Rev. E 69 046102 (2004)

- (15) A. KarGupta, in Econophysics and Sociophysics: Trends and Perspectives, Eds. B. K. Chakrabarti, A. Chakraborti, A. Chatterjee, Wiley-VCH, Berlin, 2006 (in press)

- (16) A. Chatterjee and B. K. Chakrabarti in cc:EWD05

- (17) J. Angle, Social Forces 65 293 (1986)

- (18) J. Angle, Physica A 367 388 (2006)

- (19) P. A. Samuelson, Economics, Mc-Graw Hill Int., Auckland (1980)

- (20) P. Bak, How Nature works, Oxford University Press, Oxford (1997)

- (21) A. Das, S. Yarlagadda, Phys. Scripta T 106 39 (2003)

- (22) M. Patriarca, A. Chakraborti, K. Kaski, Phys. Rev. E 70 016104 (2004)

- (23) P. Repetowicz, S. Hutzler, P. Richmond, Physica A 356 641 (2005)

- (24) J. Mimkes, G. Willis in cc:EWD05

- (25) P. K. Mohanty, Phys. Rev. E 74 in press (2006); also in xxx.arxiv.org/physics/0603141

- (26) A. Chatterjee, B. K. Chakrabarti, R. B. Stinchcombe, Phys. Rev. E 72 026126 (2005)

- (27) K. E. Dynan, J. Skinner, S. P. Zeldes, J. Pol. Econ. 112 397 (2004)

- (28) M. Gallegati, S. Keen, T. Lux, P. Ormerod, Physica A, in press (2006)

- (29) P. Richmond, B. K. Chakrabarti, A. Chatterjee, J. Angle, in Econophysics of Stock and other Markets, Eds. A. Chatterjee, B. K. Chakrabarti, Springer, Milan, p. 244, (2006)

- (30) A. Sarkar, P. Barat, in Econophysics of Stock and other Markets, Eds. A. Chatterjee, B. K. Chakrabarti, Springer, Milan, p. 67, (2006).