Aging in financial market

Abstract

We analyze the data of the Italian and U.S. futures on the stock markets and we test the validity of the Continuous Time Random Walk assumption for the survival probability of the returns time series via a renewal aging experiment. We also study the survival probability of returns sign and apply a coarse graining procedure to reveal the renewal aspects of the process underlying its dynamics.

keywords:

Waiting-time; subordination; continuous time random walk; statistical finance;PACS: 05.40.-a, 89.65.Gh, 02.50.Cw, 05.60.-k, 47.55.Mh

,

1 Introduction

In the last few years there has been an increasing interest for the subject of fractional derivatives and for the physical, biological, sociological and econophysical application of this theoretical tool. We refer the reader to the recent mini-review of Scalas [1], who addresses this issue with a special emphasis on the econophysical application. There is close connection between fractional calculus and Continuous Time Random Walk (CTRW) perspective [2], and consequently with the subject of non-Markov master equations [3]. However, these connections, and the formal equivalence of the equations motion for the probability time evolution as well, do not necessarily imply physical equivalence. For instance, the generalized diffusion equation discussed in Refs. [4, 5], in the super-diffusional case is incompatible with the CTRW perspective, insofar as there are no renewal events, resetting to zero the system’s memory.

In the case of financial market, there have been recently several contributions, related to some different extents, to the subject of fractional derivatives and CTRW [6, 8, 9, 10, 11, 12, 7]. Of special interest for this paper is the fact that the authors of Ref. [6] using fractional calculus made the theoretical prediction that the high-frequency financial market data generate a Survival Probability (SP) with the form of a Mittag-Leffler function. The later paper of Ref. [8], an empirical analysis, confirmed the theoretical prediction of Ref. [6], even though the restriction to short times forced the authors of Ref. [8] to approximate the Mittag-Leffler SP with a stretched exponential.

In this paper we show how to go beyond this limit, so as to reveal the Mittag-Leffler SP in its entirety. To realize this purpose, we study the SP for two different financial markets, the futures on the Italian stock index, SP MIB, and the futures on the US SP500. We discuss the emergence of a Mittag-Leffler SP from the returns time series at our disposal. However, in principle, the mere analysis of the form of the SP is not yet enough to ensure that the dynamics of financial market are compatible with the CTRW perspective. This is so because, as earlier pointed out, the formal equivalence between two generalized master equations, one of Liouville origin [13] and the other of CTRW origin, does not ensure the full dynamic equivalence (see also [5]).

In the last few years it became clear that CTRW yields renewal aging [14], and the authors of Refs. [15, 16] have proposed numerical experiments to assess this important property in physical systems. We plan to use the prescription of Ref. [16] as an efficient method to establish the renewal nature of the financial market process. Proving renewal aging is equivalent to ruling out the possibility that the generalized master equation generating the Mittag-Leffler SP might have a Liouville origin, with trajectory memory and no renewal event. It has to pointed out, however, that the aging experiment must be done with caution. In fact, as shown in Ref. [16], the renewal event might be masked by a cloud of secondary events, of Poisson nature, generating the wrong impression that the process is not renewal, and that its memory is a property of the individual trajectories. The authors of Ref. [17] denoted these producing camouflage events as pseudo events, and have established that in the case of heart beating analysis they are generated by the data processing procedure itself used for the statistical analysis. In other cases, the pseudo events can be triggered by the renewal events: for instance, the authors of Ref. [18], studied the seismic fluctuations in South California and made the conjecture that the main shocks are renewal events, triggering the Omori after shocks, which are an example of pseudo events in this case. The main shocks are not necessarily the seismic fluctuations of large intensity, and the seismic fluctuation caused by them might be larger, thereby making the renewal events invisible.

How to detect the renewal events? This is a challenging issue that has been mainly addressed so far through the scaling analysis. There are reasons to believe that when the time series is converted into a diffusion process, after a long-time transition, the critical events reveal their presence through the anomalous asymptotic scaling. This condition, of course, requires that the critical renewal events do not obey Poisson statistics. On the other hand, if the ratio of the number of critical to pseudo events is small, the transition to the anomalous scaling regime might be so slow as to occur outside the range of the numerical analysis of real data [19].

In this paper we find that the procedure adopted in Ref. [16] has also the surprising effect of disclosing the hidden power-law tail of the Mittag-Leffler function predicted by the theory of Refs. [6, 7, 8]. We propose also a coarse-graining procedure that has the effect of erasing many pseudo events so to make the resulting process almost completely renewal.

2 Aging of a non Poisson renewal process

To illustrate the basic concepts underlying the method used in this paper, consider the paradigmatic case of a particle moving with the following equation of motion:

| (1) |

with , and . When the particle reaches it is back injected uniformly between and to a totally random initial position. Thus we define as event the arrival of the particle at the border , and we prove with a straightforward algebra that the time distance between two consecutive events yields a waiting time distribution with the following form:

| (2) |

where is the time it takes for the particle to reach the border, moving from the initial random position, and:

| (3) |

This is therefore a simple prescription to create a non-Poisson renewal process. It is also evident that, when , , thereby making the waiting time distribution become an exponential function.

Let us use the dynamic model of Eq. (1) to illustrate the concept of renewal aging. For this purpose, let us imagine that the first back injection occurs at time , the time origin. We define this condition as system preparation at time . We define Eq. (2) as the brand new waiting time distribution, insofar as it is produced by preparing and observing the system at the same time . Eq. (2) predicts the time we have to wait to observe the next back injection. If observation begins at time , and many back injections might have possibly occurred at earlier times, we obtain the waiting time distribution . This waiting time distribution predicts the probability of the first back injection, with the system prepared at , and observation beginning at time . The function of Poisson systems is independent of , and in the non-Poisson case it turns out to depend on . An exact formula for exists [21], but it is not a simple analytical expression. In this paper we shall use instead the following approximated expression:

| (4) |

where is a suitable normalization constant. The validity of Eq. (4) has been already tested for several values of (see, for instance [16] for an application on blinking quantum dots) proving itself to be very reliable. In the following Sections, instead of the waiting time distribution , we shall use the SP. The SP is defined as follows:

| (5) |

It represents the probability that no events occurred between and . The corresponding to Eq. (4) will be denoted by means of the symbol .

It is worthwhile spending some more words on the property of renewal aging, on which the main tenet of this paper rests. Renewal aging is a property of non-Poisson renewal systems that emerges at the level of ensemble. If we consider an ensemble of trajectories, all of them being different realizations of the same experiment, and therefore all of them being statistically equivalent, the distribution of the first back injection times shows renewal aging, that is, a marked dependence on the time at which observation begins. This does not conflict with the fact that at the level of the single trajectories every event resets to zero the system’s memory, thereby producing a condition where every event is completely uncorrelated with the previous ones.

3 Illustration of the data under study and empirical analysis of the survival probability

The data set avaliable to us consists of all the transactions extracted from the futures on the Italian stock index222As of 22 March 2004 the old futures contract on MIB30, called FIB30, has been replaced by the S&P MIB Futures, because the stock index MIB30 has been replaced by the S&P MIB., ranging from January 2000 to December 2002, and all the transactions extracted from the futures US stock index, SP500, ranging from January 1993 to January 2001. We have all the transactions but we use only the next-to-expiration ones, with the markets expiring quarterly. A futures is a standardized contract that rules the exchange of a good at a given time, called maturity. The futures belongs to a larger category of contracts, called derivatives, that move nowadays almost of the total amount of money on a market and for this reason they have become one of the main investigating fields.

In the financial markets the price movements are recorded. Thanks to the introduction of computers, it has become possible to increase the frequency of registration and therefore explore what is called high-frequency regime. In this paper we focus our attention on this regime. In finance it is common to use, instead of the price movement, the return, defined as the difference of two consecutive logarithmic prices.

Let us study the distribution of waiting times of the two data sets avaliable to us. In a recent paper, Mainardi et. al [7] studied the tick-by-tick dynamics of the BUND futures traded at LIFFE. The outcome of their analysis confirmed the statement of a previous paper by Scalas et al. [6] in which the authors argued the SP to be a Mittag-Leffler function. The Mittag-Leffler function is an important entire transcendental function [20], successfully adopted in econophysics [6]. It can expressed as a power series in the complex plane:

| (6) |

where is the order of the function. The interested reader can consult, among the others, Refs. [6, 7, 20] for a complete treatment of the properties of the Mittag-Leffler function. In a later paper Raberto et al. [8] analyzed the statistical properties the SP of General Electric stock returns and found that it was compatible with a stretched exponential, which it is known to represent the limit of a Mittag-Leffler function of argument () and order for when .

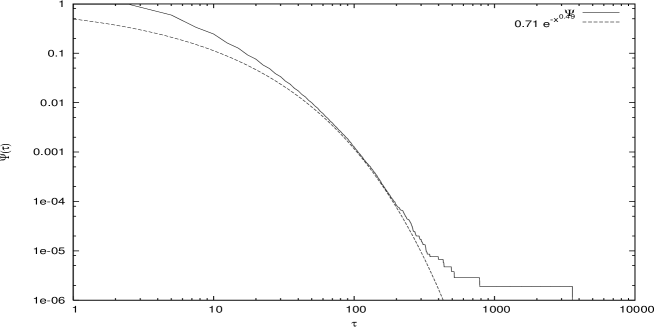

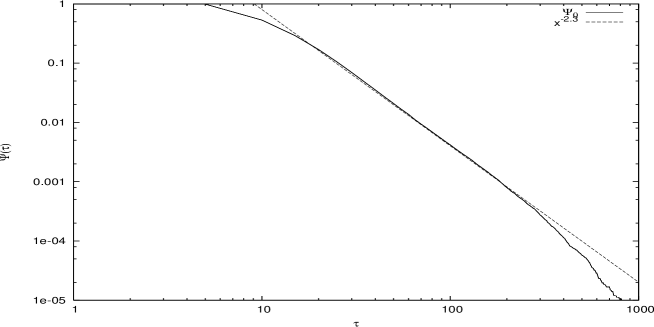

We approach the problem of the statistical analysis of our data set keeping in mind the interesting results of these authors [6, 7]. In the spirit of these papers, we build the SP for the tick-by-tick dynamics of the returns, and we obtain the results of Figs. 1 and 2.

In the case of the Italian futures the best fitting function is a stretched exponential , with and . This result is in line with Ref. [8], where a similar behavior was found for the SP, thereby implying the absence of the inverse power law tail for the Mittag-Leffler function. In the case of the US futures, Fig. 2, we observe instead an inverse power law function for the SP of returns. The index is . In this case we would be tempted to rule out the theory of the authors of Refs. [6, 7, 8]. In either cases, however, there are no compelling arguments to prove the CTRW origin of these SP, although in the former case the result is so close to the theory of Refs. [6, 7, 8] as to make it natural to consider it to be a renewal process. In the next Section we shall illustrate an aging experiment which will help us to make progresses towards the important goal of proving the renewal nature of these economic processes.

4 Aging of the survival probability

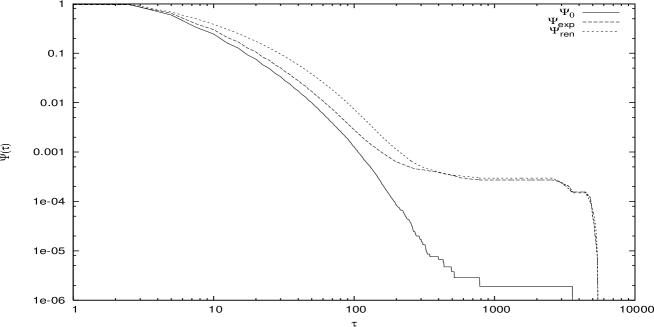

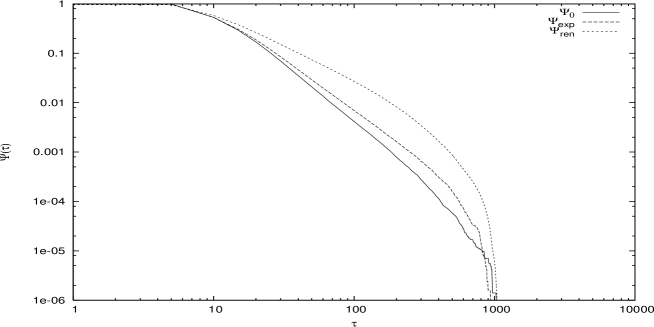

As earlier mentioned, we devote this section to examining our data by means of a procedure applied in a previous article [16]. This technique turns the SP of the original time series, , into two SP’s, denoted as and . The former is derived from the original time series by means of an aging numerical experiment that we describe hereby. The latter is derived from the of the original time series, as follows. First we turn the experimental into by means of Eq. (4), then we derive from this aged waiting time distribution the corresponding SP, thereby producing . In the ideal case of a renewal system we would obtain . According to Ref. [16], the existence of pseudo events would reduce the aging effect till to its total annihilation when the number of pseudo events becomes very large.

The formula of Eq. (4) is based on probabilistic arguments, and consequently, on the ideal use of a Gibbs ensemble of sequences. We have only one sequence, and we have to turn it into a set of Gibbs sequences, prepared in the same way at time and observed at a later time . This is done as follows. The first sequence of the Gibbs ensemble is: , , , , the superscript indicating the sequence and the subscript the chronological order of waiting times; the second sequence is obtained from the first by erasing the first waiting time, thereby yielding , ; the third sequence is obtained from the second again erasing the first waiting time, thus yielding , , and so on. All these sequences are examined in the absolute time representation, where time is denoted by the symbol and the time of an event occurrence is denoted by the symbol , with the superscript indicating the system of the ensemble built up with the procedure earlier described. Note that , , . All the systems of this ensemble have been prepared in the same way, with a back injection occurring at time . At this stage we fix the observation time , and for the -th system of the ensemble we monitor the first event occurring after this time, at time and the corresponding time distance . This allows us to define the experimental waiting time distribution and from it . In the case where there is no aging, we should obtain . The ideal renewal condition should yield .

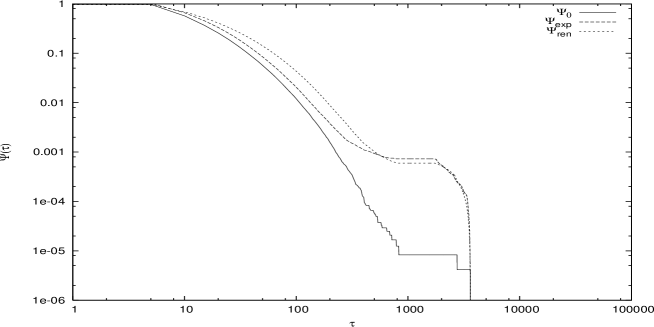

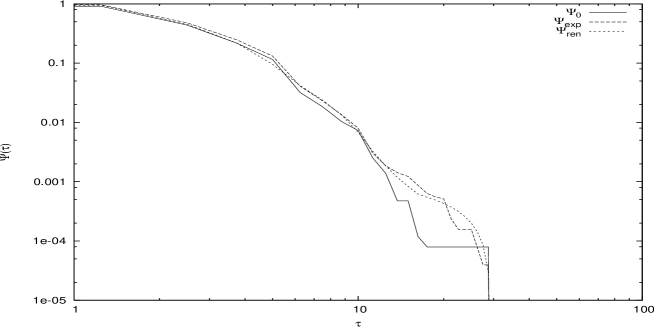

Fig. 3 illustrates the result of this analysis applied to the Italian futures index, for . Clear aging

effects are evident, slightly reduced in the first part of the plot, where, on the other hand, also the renewal aging is significantly reduced, but

compatible with the predictions of the renewal theory in the second

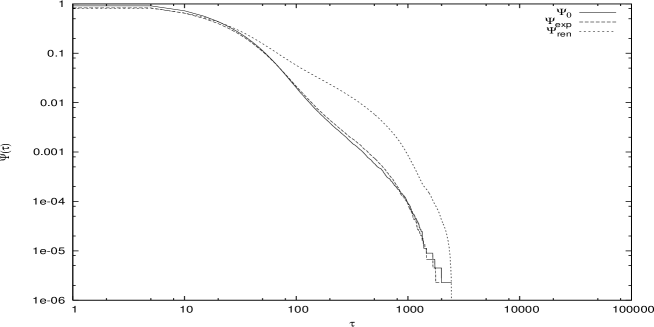

part. Fig. 4 reports the same experiment for the US stock

futures index, with . In this case, is faster than

in the whole observed time regime. A weak form of aging is found, but there are no time regions where it correspond to the renewal theory prediction. We believe that the reduced aging is due to microstructure, inducing correlations in the high-frequency returns, see [22, 23, 8]. It is well known that, for instance, bid-ask spread causes

spurious serial correlations in the time series of returns, with extinction

time of the order of some minutes. The aging experiment is sensitive to

time correlated events (pseudo events), time correlation being a property conflicting with the renewal

assumption of the process, thereby explaining the results of

Fig. 4.

It is also worth noticing the emergence of a

distinct power law tail in the last part of Fig. 3. This could be a sign of

a hidden Mittag-Leffler-type function as SP, whose presence could be revealed

by means of a renewal aging experiment.

In conclusion, our analysis proves that the CTRW is a reliable model for the Italian futures index, while in the US futures index the renewal properties are weakened by significant serial correlations in the return time series.

5 Aging and sign change as a visible event

We move now our attention to a different aspect of the trade action: we study for how long the fluctuation making the walker (return) move, maintains the same sign. Thus, the waiting time is now determined by the time distance between two consecutive changes of sign. We evaluate the SP of this sequence and study its renewal properties via the renewal aging analysis. Also in this case, we expect to find reduced aging effects, due to the presence of negative serial correlations in the time series of returns, with extinction times of the order of some minutes [22]. Figs. 5 and 6 show the results of our analysis.

As we can see in Fig. 5, in the case of the Italian market, again aging effects are present. As in the case of the tick-by-tick SP, the aging is reduced and we can safely impute this behavior to the presence of negative serial correlation in the time series of returns. However, in the final part of the plot, we have a good agreement with the renewal assumption for the dynamics of the market. Regarding the US futures index, Fig. 6 shows the result in this case. We can see that in this case the aging is almost totally suppressed. Again we explain this effect invoking the presence of strong correlations in the time series of returns.

It is important to notice that in the special case where the change of sign of the fluctuation driving the walker’s motion is as random as a fair coin tossing, the new waiting time distribution has the same power as the original [24]. We see that Figs. 5 and 6 illustrate a situation that it is qualitatively similar to that of Figs. 3 and Figs. 4, respectively. This suggests that the change of sign is a random process, or a process with a modest correlation that might be responsible for the significantly reduced aging effect of the Italian market, which is, in fact, even weaker than in the case of Fig. 4.

6 Coarse graining procedure

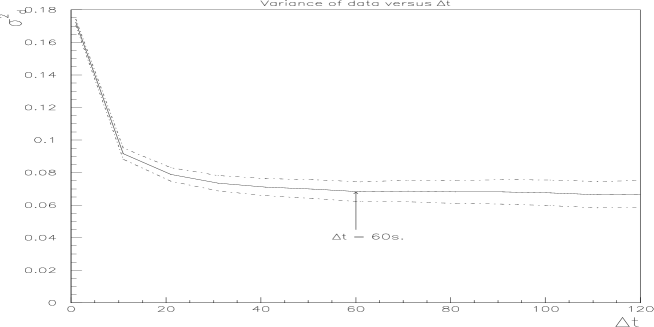

We have earlier mentioned that the memory generated by microstructures may hide the renewal nature of the process, which we believe to be the genuine property of the trading action. In the economic literature a coarse graining procedure is usually applied to raw data to get rid of these memory properties. Following Ref. [22, 23] we apply the following tick coarse graining. Let us denote by the time window under study, with trading day, that is, 495 minutes, we construct a grid of points, with denoting the grid spacing. At every point in time, we define the event (price) as the event (price) of the last transaction before that point. Different choices, like linear interpolation, are known to introduce spurious autocorrelation, see, for instance, Ref. [25]. However, selecting the length of the intervals is conditioned by the following tradeoff. If the interval is too narrow, microstructure effects, such as the bid-ask bounce, remain, which would induce a spurious negative serial correlation. On the other hand, if the interval is too large, there is a loss in the total number of data. In order to assess the proper length of the interval we study the daily variance of the distribution; if the dynamics of the process is a stochastic differential equation with no drift, then the integrated variance on the time window must coincide with its expected value for every value of the grid spacing , see, for instance, Ref. [26].

These important issues are illustrated by Fig. 7, which shows the integrated variance of the Italian futures index versus the length of the interval. In accordance with the earlier remarks, we see that, when the spacing is too narrow, the variance increases. This fact is well known and can be imputed to the presence of microstructure effects [27]. We decide to use an interval spacing of seconds for the Italian futures, and seconds for the US futures, where we assume the integrated daily variance to be constant. Indeed, the percentage of empty intervals in the two case has been estimated, respectively, to be below and below .

We are now properly equipped to establish if the nature of the process is compatible with the renewal assumption. The discussion of the results emerging from the application of this procedure will be the argument of the next Section.

7 Pseudo events, critical events and renewal aging

The adoption of the coarse graining procedure described in the previous section should make it possible to confirm our conviction that the weakening of the aging effects depends on pseudo events. As already stated above, the presence of microstructure effects implies high-frequency spurious correlation effects in the time series of returns, that is, the real event is “floating” in a sea of pseudo events. We argue that, if we were able to distinguish the real event from the pseudo events, and create the waiting time distribution of the real events, the resulting distribution, if markedly non exponential, should obey the condition of renewal aging. The coarse graining has the effect of reducing the number of pseudo events, thereby disclosing the true nature of the financial market.

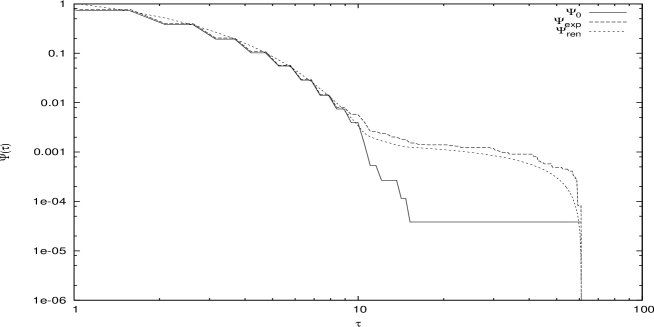

Fig. 8 and Fig. 9 show the results of the aging experiment on the Italian

futures index and on the US futures index, respectively. We see that in both cases the aging effect is very close to the predictions of the renewal theory. It is worth noticing that according to Fig. 8, the aging

experiment in the long time region makes, again, an inverse power law tail emerge for both and . The shape of the function

becomes a Mittag-Leffler type with and . This

behavior remains unchanged for larger values of , therefore suggesting

that the aging experiment reveals the genuine nature of the process,

this being represented by the Mittag-Leffler SP found by the authors of

Ref. [7]. We think that this may become an efficient way to assess the

hidden renewal nature of the experimental time series and we plan to devote

further study to this issue in a later publication.

The fact that the aging effect in the US market is weaker than in the Italian market is not due to the non-renewal nature of the US market, but it seems to depend on the fact that the Mittag-Leffler form of the SP is lacking in this case. We cannot rule out the possibility that also the US market obeys the theory of Ref. [6]. In fact, our results suggest that in this case the stretched-exponential regime of the US market is more extended than that of the Italian market. We note that in the short-time regime of Fig. 8, namely, in the stretched-exponential time region, aging is virtually absent, in spite of the renewal character of this process. Thus, the reduced aging cannot be used as a sign of departure from the renewal condition. We think that the more significant aging effect in the large time regime of Fig. 9 is a sign that also in this case the inverse power law of the Mittag-Leffler function is made to emerge by the aging experiment.

8 Concluding remarks

This paper confirms the theory proposed by the authors of Refs. [6, 7, 8] to describe the financial market dynamics, with a careful scrutiny of the economic data. The Mittag-Leffler SP, which is the main prediction of this theory, does not emerge in its entirety from the data analyzed in this paper. The statistical inaccuracy of the long-time region obscures the emergence of the inverse power law tail in the US financial market, and the Italian financial market as well. The aging experiment has the surprising effect of making the inverse power law distinctly appear in the long-time regime of the Italian market. The effect is not so evident in the case of the US market, and we think that this is due to fact that the stretched-exponential regime is much more extended than in the case of the Italian market. It is remarkable that the genuinely renewal nature of the trading action is made visible, through the aging experiment, by a proper coarse graining data processing. Our analysis suggests also that the price persistence is not a process with long-range memory, and within the limits of the numerical accuracy, the price change is virtually indistinguishable from the adoption of a fair coin tossing to decide if price has to increase or to decrease.

We hope that the results of this paper may give an important contribution to the foundation of accurate financial models. Furthermore, we are convinced that the procedure illustrated in this article is a significant contribution to the detection of invisible renewal events, the challenge emerging from the results of Ref. [17].

References

- [1] E. Scalas, Physica A, 362, 225-239 (2006).

- [2] E.W. Montroll, G.H. Weiss, J. Math. Phys. 6, 167 (1965).

- [3] V.M. Kenkre, E.W. Montroll, and M.F. Shlesinger, J. Stat. Phys. 9, 45 (1973).

- [4] R. Balescu, Chaos, Solitons and Fractals, xx, www (2006), this issue.

- [5] R. Cakir, A. Krockin, P. Grigolini, xx, www (2006), this issue.

- [6] E. Scalas, R. Gorenflo, F. Mainardi, Physica A, 284, 376 (2000).

- [7] F. Mainardi, M. Raberto, R. Gorenflo, E. Scalas, Physica A, 287, 468-481 (2000).

- [8] M. Raberto, E. Scalas, F. Mainardi, Physica A, 314, 749 (2002).

- [9] M. Kirane, Y. Laskri, N. -e. Tatar, J. Math. Anal. Appl. 312, 488 (2005).

- [10] T. Kaizoji, M. Kaizoji, Physica A, 336, 563 (2005).

- [11] L. Palatella, J. Perelló, M. Montero, J. Masoliver, Physica A, 355, 131 (2005).

- [12] S. -M. Yoon, J.S. Choi, Y. Kim, K. Kim, Physica A, 359, 131 (2006).

- [13] P. Grigolini, Adv. Chem. Phys. , in press (2006).

- [14] E. Barkai and Y.-C. Cheng, J. Chem. Phys. 118, 6167 (2003).

- [15] X. Brokmann, J. -P. Hermier, G. Messin, P. Desbiolles, J. -P. Bouchaud, and M. Dahan, Phys. Rev. Lett. 90, 120601 (2003).

- [16] S. Bianco. P. Grigolini, P. Paradisi, J. Chem. Phys. 123, 174704 (2005).

- [17] P. Allegrini, P. Grigolini, P. Hamilton, L. Palatella, and G. Raffaelli, Phys. Rev. E 65, 041926 (2002).

- [18] M. S. Mega, P. Allegrini, P. Grigolini, V. Latora, L. Palatella, Phys. Rev. 90, 188501 (2003).

- [19] P. Allegrini, F. Barbi, P. Grigolini, submitted to Phys. Rev. E.

- [20] F. Mainardi and R. Gorenflo, J. Comput. and Appl. Mathematics 118, 283 (2000).

- [21] P. Allegrini, G. Aquino, P. Grigolini, L. Palatella, A. Rosa, and B.J. West, Phys. Rev. E 71, 066109 (2005).

- [22] S. Bianco and R. Renò, Journal of Futures Market, 26(1), 61-84 (2006).

- [23] S. Bianco and R. Renò, in preparation.

- [24] G. Zumofen and J. Klafter Phys. Rev. E 47, 851-863 (1993).

- [25] E. Barucci and R. Renò, Econ. Lett., 74, 371-378 (2002).

- [26] O.E. Barndorff-Nielsen and N. Shephard, Journal of the Royal Statistical Society, Series B, 64, 253-280 (2002).

- [27] R. Roll, Journal of Finance, 39(4), 1127-1139 (1984).