On the gap between an empirical distribution and

an exponential distribution of waiting times

for price changes in a financial market

Abstract

We analyze waiting times for price changes in a foreign currency exchange rate. Recent empirical studies of high frequency financial data support that trades in financial markets do not follow a Poisson process and the waiting times between trades are not exponentially distributed. Here we show that our data is well approximated by a Weibull distribution rather than an exponential distribution in a non-asymptotic regime. Moreover, we quantitatively evaluate how much an empirical data is far from an exponential distribution using a Weibull fit. Finally, we discuss a phase transition between a Weibull-law and a power-law in the asymptotic long waiting time regime.

pacs:

89.65.GhI INTRODUCTION

It seems natural to assume that trades in financial markets arrive according to a Poisson process and the waiting times, which are the time intervals between trades, follow an exponential distribution rf:1 ; rf:2 . However, on the other hand, recent empirical studies rf:3 ; rf:4 ; rf:5 ; rf:6 observed that the waiting time distribution is non-exponential in different markets. Therefore, in order to understand market behavior quantitatively and systematically, it would be important to check validity of the exponential distribution hypothesis.

In this paper, we test validity of the exponential distribution hypothesis of waiting times for price changes using a real market data. Then we evaluate a gap quantitatively between an empirical distribution of waiting times and an exponential distribution. In order to measure the gap, we introduce a more general distribution which includes an exponential distribution as a special case. It is desirable that the distribution can quantify the gap using a small number of parameters. That is, by fitting such a distribution to a real market data, we would like to determine how much an empirical data is far from an exponential distribution through the parameters. For this purpose, one of the good example is a Weibull distribution rf:7 . A Weibull distribution is often used to model the time to failure and described by two parameters and as follows.

| (1) | |||||

| (2) |

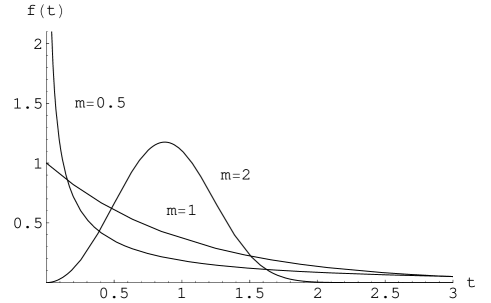

where is the scale parameter and is the shape parameter. Since the distribution shape is characterized by only one parameter , we focus on the parameter in the following. FIG. 1 shows some of probability density functions for different m’s such as . As is clear from FIG. 1 and equation (1), a Weibull distribution is reduced to an exponential distribution when . Consequently, we can evaluate the gap by examining how much the estimated value is far from . Therefore, the purpose of this paper is to test validity of the exponential distribution hypothesis using a real market data and measure the gap quantitatively between an empirical distribution and an exponential distribution by fitting a Weibull distribution to the data.

It should be noted that we focus on a non-asymptotic regime for relatively short waiting times, since almost all events occur in this regime. We discuss the asymptotic behavior for long time regimes in Section 4.

The paper is organized as follows. In Section 2, we explain our data and test the exponentianl hypothesis of waiting times. In Section 3, by fitting a Weibull distribution to the empirical data, we measure concretely the gap between the empirical data and an exponential distribution in two different ways. In Section 4, we discuss the asymptotic behavior for long waiting time regime. Finally, we present our conclusions in Section 5.

II Analysis of waiting times for price changes

II.1 Data

In this paper, we analyze Sony bank USD/JPY rate as a real market data. Sony bank rate is that the Sony bank rf:8 offers to their customers on their online foreign exchange trading service via the internet. The Sony bank rate depends on the market rate, but not customers’ order. If the market rate changes by 0.1 yen and over, the Sony bank rate is updated to the market rate. Conversely, if the market changes by less than 0.1 yen, the Sony bank does not move and keep the previous rate. In other words, Sony bank rate is produced by filtering market rate using the sort of window with the width of 0.1 yen. In principle, the Sony bank rate is provided while the market is open. Currently, about 130,000 customers use this service. Our data set is about 31,000 data for the period of September 2002 to May 2004. According to the update rule, the mean time intervals between price changes of the Sony bank rate (20 minutes) rf:9 is longer than the one of the market rate ( 7 seconds).

II.2 Waiting times for price changes

A waiting time between th price change and th price change is defined as follows.

| (3) |

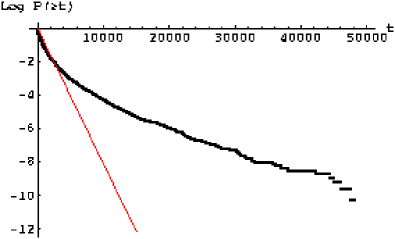

where is the time when th price change occurs. First of all, we plot a survival function of waiting time , which is the cumulative probability of the waiting times greater or equal to seconds, on a semi-log scale in FIG. 2. It shows that the waiting time for price changes is not exponentially distributed. If the distribution is exponential as is widely assumed, the data should be roughly on a straight line on the semi-log scale. However, we observe that the plotted data in FIG. 2 is not a straight line. The right panel of FIG. 2 shows that the gap is already visible in the very short waiting times regime. This fact is consistent with recent empirical evidence observed in different markets rf:3 ; rf:4 ; rf:5 ; rf:6 . Thus, we find that the non-exponential waiting time distribution appears not only in market rate but also in the data has been sampled by filtering market rate using the window with the width of 0.1 yen. The non-exponential waiting time distribution also means that the arrival process for price change is not a Poisson process.

|

However, this semi-log plot of the cumulative probability is not enough to evaluate the gap quantitatively between an empirical distribution and an exponential distribution. As we explained in the previous section, we now quantify the gap by fitting a Webull distribution to the data. In particular, we check the gap visually by a Weibull paper analysis.

III The gap between empirical and exponentianl distriutions

III.1 Weibull paper analysis

A Weibull paper analysis is often used to check a Weibull model assumption. A Weibull cumulative distribution function can be rewritten as

| (4) |

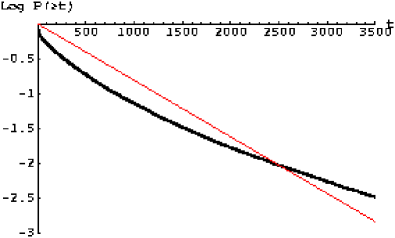

is a linear function of with a slope . Namely, the data from a Weibull distribution are plotted on a straight line on Weibull paper. As a special case, the slope is 1 when the data follow an exponential distribution. Therefore, the slope of the line on Weibull paper is a quantitative indicator which enable us to evaluate the gap. In FIG. 3, our data is roughly on a straight line with the estimated slope , which is apparently different from exponential distribution with . It shows that the waiting time distribution of the Sony bank USD/JPY rate is well approximated by a Weibull distribution with , rather than an exponential distribution.

III.2 Divergence measurements

The gap can be also discussed by using divergence measurements. In the previous section, we showed the empirical waiting time distribution is approximated by a Weibull distribution. Thus, we replaced the gap between an exponential distribution and the empirical data with the gap between an exponential distribution and a Weibull distribution. However, in this section, we actually measure both of them by considering a gap between two distributions as a divergence measurement. For example, we calculate Kullback-Leibler (KL) divergence and Hellinger distance. These two divergence measurements between the empirical distribution and a model distribution are written respectively

| KL divergence | (5) | ||||

| Helliger distance | (6) |

| KL divergence | Hellinger distance | |

|---|---|---|

| Q=Weibull | 0.19 | 0.21 |

| Q=exponential | 0.49 | 0.36 |

TABLE 1 gives KL divergence and Hellinger distance when is the fitted Weibull distribution with and the fitted exponential distribution. Both divergence measurements show that the Weibull distribution is closer than the exponential distribution to the empirical distribution. Especially, Hellinger distance which is a distance metric shows that the difference is about 1.7 times. This fact correponds to the result in the previous section that the Weibull distribution is a better approximation than exponential distribution.

As a result, we conclude that the gap can be evaluated by two different methods which are a Weibull paper analysis and divergence measurements. This is a main result of this paper.

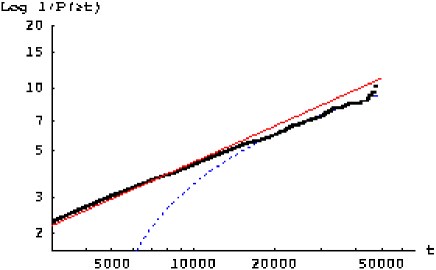

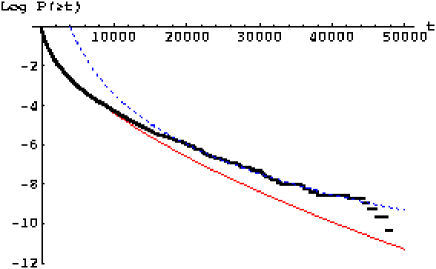

IV Phase transition between a Weibull-law and a power-law

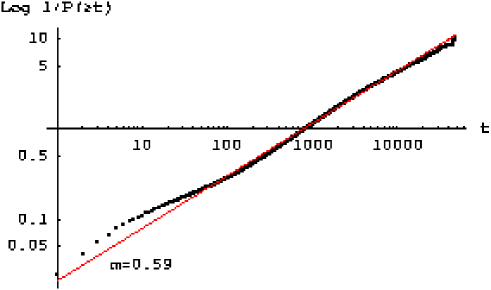

Let us close this paper with a discussion on asymptotic behavior of waiting times. In previous sections, we showed that a Weibull distribution is a better approximation of waiting times in a non-asymtiotic regime rather than an exponential distribution. However, accurately the Weibull fit is not so good in the very short waiting time limit and the very long waiting time limit in FIG 3. It could have different behavior in those two time regimes. In this section, we discuss asymptotic behavior in long time limit which is one of two regimes. We find that the cumulative probability distribution of waiting times greater or equal to 18,000 seconds (= 5 hours) well expressed by a power-law with exponent . Consequently, we find that the behavior changes from a Weibull-law to a power-law at some point . The phase transition is well observed in the Weibull paper for the asymptotic regime and the semi-log scale of in FIG. 4. It should be noted that the number of data for the power-law regime is only 0.3, which is almost an outlier, of total number of waiting times. Since such long waiting times hardly ever happen, we focused on the Weibull fit regime in previous sections.

Similar behavior was reported for the waiting time distribution of BUND futures traded at LIFFE rf:6 . They showed that the waiting time distribution is a good agreement with the Mittag-Leffler function which interpolates between the stretched exponential for short time regime to the power-law for long time. It is interesting that even the Sony bank rate which is filtered market rate firstly moves out from a range of 0.1 yen still have similar property to the market rate itself. However, the exponent values and transition point are different from our case. Our exponent value changes from for a Weibull-law regime to for a power-law regime, whereas, the Mittag-leffler fit for BUND futures can be expressed by a single exponent for both regimes. Moreover, our exponent value for non-asymptotic regime is smaller than for BUND data and our transition point 18,000 seconds is larger than seconds for BUND futures. This could be caused by the window effect which is the sampling method of the Sony bank rate from the market rate. By this sampling method, the waiting times of the Sony bank rate become longer than the one of the market rate on average. The cumulative distribution function of the Weibull distribution with decays slower for as decreases, in other words, there are more long waiting times for as decreases.

On the other hand, the behavior differs from a Weibull fit in short time limit is not resolved. One possible reason is measurement errors but there might be other possible distributions that decay faster than the Weibull distribution. The Mittag-Leffler fit also can not capture the empirical data for short time limit rf:6 .

V CONCLUSION

In this paper, we showed that the waiting time distribution of the Sony bank USD/JPY rate is non-exponential. The result is consistent with the recent empirical evidence rf:3 ; rf:4 ; rf:5 ; rf:6 of market rate. It is interesting that the non-exponential waiting time distribution appears not only in the market rate but also in the Sony bank rate which is filtered market rate using the window with the width of 0.1 yen.

We also showed that the empirical data is well approximated by a Weibull distribution in a non-asymptotic regime, which includes almost all events. Then we measured the gap quantitatively between an empirical waiting time distribution and an exponential distribution by using a Weibull paper analysis and divergence measurements. Finally, we found that the phase transition between a Weibull-law and a power-law in long time asymptotic regime. It should be noted that the events in a power-law regime is only 0.3 of the total events.

In addition, the window effect of the Sony bank rate is can be regarded as the first passage time problem. Further analysis of waiting times in this direction will be reported in our forthcoming article rf:10 .

Acknowledgements.

I would like to appreciate Shigeru Ishi, President of the Sony bank, for kindly providing the Sony bank data and useful discussions. Stimulating discussions with Jun-ichi Inoue of Hokkaido University is acknowledged.References

- (1) D. Easley, R. Engle, M. O’Hara and L. Wu, AFA 2002 Atlanta Meeting.

- (2) N. T. Chan and C. Shelton, Technical Report AI-MEMO 2001-2005, MIT, AI Lab (2001).

- (3) M. Raberto, E. Scalas and F. Mainardi, Physica A. 314 (2002), 749.

- (4) E. Scalas, T. Kaizoji, M. Kirchler, J. Huber and A Tedeschi, Physica A. 366 (2006), 463.

- (5) T. Kaizoji and M. Kaizoji, Physica A. 336 (2004), 563.

- (6) F. Mainardi, M. Raberto, R. Gorenflo and E. Scalas, Phyica A. 287 (2000), 468.

- (7) B. S. Everitt, The Cambridge Dictionary of Statistics, Cambridge University Press (1998).

- (8) http://moneykit.net

- (9) N. Sazuka, Eur. Phys. J. B. 50 (2006), 129.

- (10) J. Inoue and N. Sazuka, in preparation.