On Estimation of Hurst Scaling Exponent through Discrete Wavelets

Abstract

We study the scaling behavior of the fluctuations, as extracted through wavelet coefficients based on discrete wavelets. The analysis is carried out on a variety of physical data sets, as well as Gaussian white noise and binomial multi-fractal model time series and the results are compared with continuous wavelet based average wavelet coefficient method. It is found that high-pass coefficients of wavelets, belonging to the Daubechies family are quite good in estimating the true power in the fluctuations in a non-stationary time series. Hence, the fluctuation functions based on discrete wavelet coefficients find the Hurst scaling exponents accurately.

keywords:

Time series , fluctuations , fractals , Discrete wavelets , Hurst exponentPACS:

05.45.Tp , 89.65.Gh , 05.45.Df , 52.25Gj1 Introduction

Fractals exhibiting self-similar behavior, are ubiquitous in nature mandel . They manifest in areas ranging from financial markets to natural sciences. Several techniques have been developed to study the correlations and scaling properties of time series exhibiting self-similar behavior; some of these data sets are non-stationary in character. Various methods like R/S analysis (hur, ), structure function method feder , wavelet transform modulus maxima arn1 , detrended fluctuation analysis and its variants khu ; gopi ; ple ; chen ; matia ; krs ; phand ; xu ; peng ; net , average wavelet coefficient method awc and a recently developed discrete wavelet based approach by the present authors, have been employed for the characterization of fluctuations mani1 ; mani2 .

Wavelets, through their multi-resolution and localization abilities, are well suited for extracting fluctuations at various scales from local trends over appropriate window sizes daub ; mall . The nature of the fluctuations extracted partly depend on the choice of the wavelets, which are designed to have properties useful for a desired analysis. For example, the Daubechies family of wavelets satisfy vanishing moment conditions, which make them ideal to separate polynomial trends in a data set. In a number of wavelet based approach for characterizing self-similar data, wavelet high-pass coefficients are used in finding the fluctuation function or other related quantities. For example, in the average wavelet coefficient method, continuous wavelet transform is used to find the variations through the corresponding wavelet coefficients, from which the Hurst scaling exponent is computed.

The goal of the present article is to analyze the self-similar properties of the fluctuations, as extracted through discrete wavelet coefficients, for the purpose of checking its efficacy vis-a-vis the continuous wavelet based method. The study is carried out on Gaussian white noise and binomial multifractal model time series, as well as a number of physical data sets. It is found that the fluctuation function based on discrete wavelet coefficients is accurate in estimating Hurst scaling exponent. It is worth emphasizing that continuous wavelets, because of their over completeness tend to overestimate the power. In comparison, the discrete wavelets provide a complete orthonormal basis, ensuring that fluctuations are independent at each level.

The paper is organized as follows. In the following section, we study the nature of the fluctuations extracted through the wavelet coefficients. In Sec.III, we then proceed to the detailed analysis of fluctuations of Gaussian white noise and binomial multi-fractal model and compare the discrete wavelet based result with average wavelet coefficient method. Subsequently, we carry out analysis of the fluctuations in the data of observed ionization current and potentials in tokamak plasma, time series constructed from random matrix ensembles and the financial data sets belonging to NASDAQ and Bombay stock exchange (BSE) composite indices. Finally, we conclude after summarizing our findings and giving future directions of work.

2 Fluctuations in the wavelet domain

In discrete wavelet transform it is well-known that, a given signal belonging to space can be represented in a nested vector space spanned by the scaling functions alone. This basic requirement of multi-resolution analysis (MRA) can be formally written as ram ,

| (1) |

with and . This provides a successive approximation of a given signal in terms of low-pass or approximation coefficients. It is clear that, the space that contains high resolution signals will also contain signals of lower resolution. The signal or time series can be approximated at a level of ones choice, for use in finding the local trend over a desired window. The fluctuations can then be obtained by subtracting the above trend from the signal. We have followed this approach earlier for extracting the fluctuations, by elimination of local polynomial trends through the Daubechies wavelets mani1 ; mani2 .

Wavelets also provide a decomposition of a signal in terms of wavelet coefficients and one low-pass coefficient:

| (2) |

and

| (3) |

Wavelet coefficients represent variations of the signal at different scales. For example, level one coefficients capture the highest frequency components, corresponding to variations at highest resolution and other wavelet coefficients represent variations at progressively higher scales or lower resolutions. As mentioned earlier, these coefficients can differ significantly from the true fluctuations in the data sets. Below, we explore this aspect through the estimation of Hurst exponents.

Let () be the time series of length . First one determines the ”profile” (say ), which is cumulative sum of series after subtracting the mean.

| (4) |

Next, we obtain the statistics of scale dependence by transforming the profile of the time series into wavelet space, the coefficients of wavelets at various scales are used to determine the fluctuation function. The high frequency details are captured by the lower scale wavelet coefficients and the higher scales capture the low frequency details. By convolving the discrete wavelet transform over the given time series, the wavelet coefficients are obtained for various scales:

| (5) |

Here ’’ is the scaling index and represents the translation variable. Since discrete wavelet transform satisfies orthogonality condition, it can provide the information of time series at various scales unambiguously. Performing wavelet transform using Daubechies basis, the polynomial trends in the time series are eliminated. In the analysis carried out below we make use of the Daubechies-4 wavelets. As has been observed earlier, small fluctuations are least affected by this basis and straight line trends (akin to a linear fit) are removed through the use of this wavelet mani1 .

The wavelet power is calculated by summing the squares of the coefficient values for each level:

| (6) |

To characterize the time series, the fluctuation function at a level is obtained from the cumulative power spectrum:

| (7) |

The scaling behavior is then obtained through,

| (8) |

Here is the Hurst scaling exponent, which can be obtained from the slope of the log-log plot of vs scales . It is well known that Hurst exponent is one of the fractal measures, which varies from . For persistent time series and uncorrelated series. for anti-persistent time series.

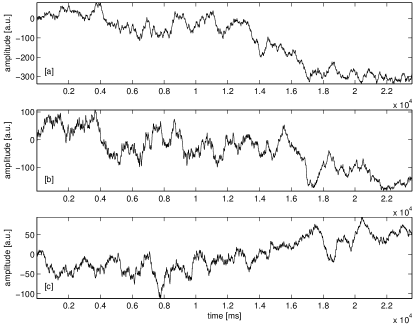

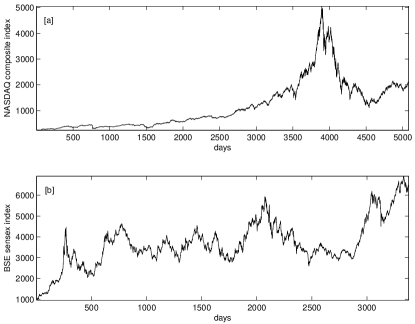

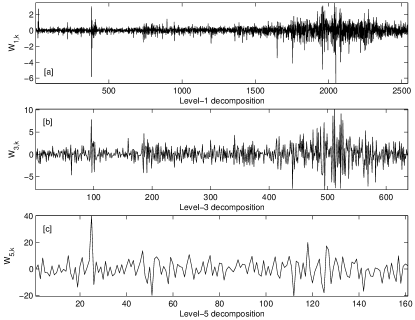

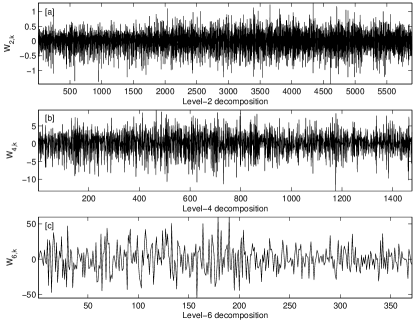

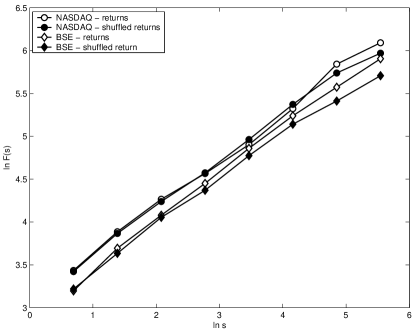

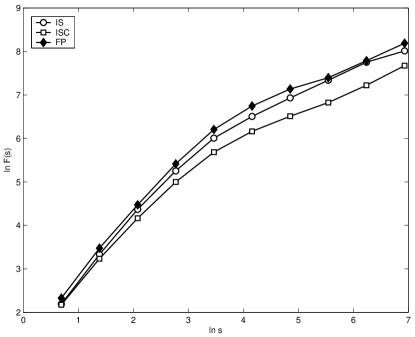

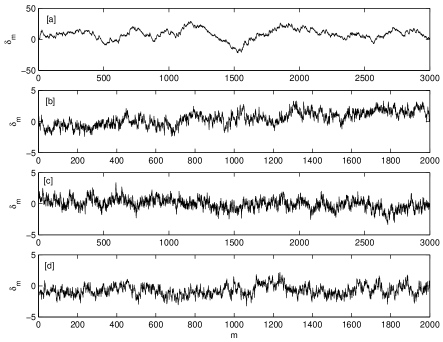

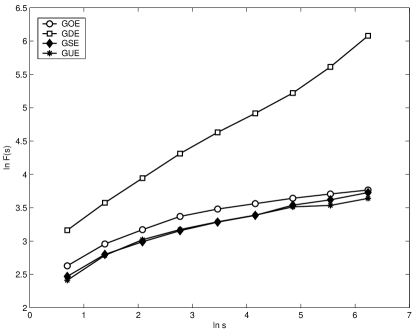

We have analyzed three sets of experimentally observed time series of variables in ohmically heated edge plasma in Aditya tokamak jos . The time series are i) ion saturation current, ii) ion saturation current when the probe is in the limiter shadow, and iii) floating potential, 6mm inside the main plasma. Each time series has about 24,000 data points sampled at 1MHZ jha . These are shown in Fig. 1. The study of fluctuations play an important role in our understanding of turbulent transport of particles and heat in the plasma. In Fig. 2, we show financial time series of NASDAQ composite index and BSE sensex index values. Wavelet coefficients at various scales have been displayed in Fig. 3 and Fig. 4. In Figs. 5 and 6, we have shown versus for the time series of three experimental data sets and financial stock market data, respectively. The scaling exponent , for all the three experimental time series as well as financial data sets shows long range correlations (). We have also analyzed the discrete time series obtained from random matrix ensembles corresponding to Gaussian orthogonal ensemble (GOE), Gaussian symplectic ensemble (GSE) and Gaussian unitary ensemble (GUE). These show long range anti-correlation behaviors . Gaussian diagonal ensemble (GDE) shows uncorrelated behavior, . It is worth mentioning that, we have followed the recent approach of Ref. rela , for converting the random matrix ensemble data to discrete time series ran . In Table-I and II, Hurst exponents of various data sets are given. These results agree with our previous discrete wavelet based approach.

| Data | Hurst (H) |

|---|---|

| NASDAQ - returns | 0.553 |

| NASDAQ - shuffled returns | 0.542 |

| BSE - returns | 0.548 |

| BSE - shuffled returns | 0.518 |

| IC | 0.585 |

| ISC | 0.554 |

| FP | 0.549 |

| GOE | 0.095 |

| GDE | 0.495 |

| GSE | 0.143 |

| GUE | 0.107 |

| Data | |||

|---|---|---|---|

| BMF | 0.8390 | 0.8421 | 0.8433 |

| WGN | 0.5 | 0.5077 | 0.5163 |

3 Conclusion

In conclusion, one needs to be careful in using wavelets for estimating the Hurst exponent. The continuous wavelets provide an over complete basis, because of which the coefficients are not independent, they overestimate the power in the fluctuations. In comparison the discrete wavelet is based on complete orthonormal basis, ensuring that fluctuations are independent at each level. Hence this discrete wavelet approach yields correct values for the Hurst exponent.

Acknowledgements We would like to thank Dr. R. Jha for providing the tokamak plasma data for analysis.

References

- (1) B. B. Mandelbrot, The Fractal Geometry of Nature Freeman, San Francisco, 1999.

- (2) H. E. Hurst, Trans. Am. Soc. Civ. Eng. 116 (1951) 770.

- (3) J. Feder, Fractals Plenum Press, New York, 1988.

- (4) A. Arneodo, G. Grasseau, and M. Holshneider, Phys. Rev. Lett. 61 (1988) 2284; J. F. Muzy, E. Bacry, and A. Arneodo, Phys. Rev. E 47 (1993) 875.

- (5) K. Hu, P. Ch. Ivanov, Z. Chen, P. Carpena, and H. E. Stanley, Phys.Rev. E 64 (2001) 11114.

- (6) P. Gopikrishnan, V. Plerou, L. A. N. Amaral, M. Meyer, and H. E. Stanley, Phys. Rev. E 60 (1999) 5305.

- (7) V. Plerou, P. Gopikrishnan, L. A. N. Amaral, M. Meyer, and H. E. Stanley, Phys. Rev. E 60 (1999) 6519.

- (8) Z. Chen, P. Ch. Ivanov, K. Hu, and H. E. Stanley, Phys. Rev. E 65 (2002) 041107.

- (9) K. Matia, Y. Ashkenazy, and H. E. Stanley, Europhys. Lett. 61 (2003) 422.

- (10) R. C. Hwa, C.B. Yang, S. Bershadskii, J.J. Niemela, and K. R. Sreenivasan, Phys. Rev. E 72 (2005) 066308.

- (11) K. Ohashi, L. A. N. Amaral, B. H. Natelson, and Y. Yamamoto, Phys. Rev. E. 68 (2003) 065204(R).

- (12) L. Xu, P. Ch. Ivanov, K. Hu, Z. Chen, A. Carbone, and H.E. Stanley, Phys. Rev. E 71 (2005) 051101.

- (13) C. K. Peng, S. V. Buldyrev, S. Havlin, M. Simons, H. E. Stanley, and A. L. Goldberger, Phys. Rev. E 49 (1994) 1685.

- (14) J. W. Kantelhardt, D. Rybskia, S. A. Zschiegnerb, P. Braunc, E. Koscielny-Bundea, V. Livinae, S. Havline, A. Bundea, and H. E. Stanley, Physica A 330 (2003) 240.

- (15) I. Simonsen, A. Hansen, and O.-M. Nes, Phys. Rev. E 58 (1998) 2779.

- (16) P. Manimaran, P.K. Panigrahi, and J.C. Parikh, Phys. Rev. E 72 (2005) 046120.

- (17) P. Manimaran, P. K. Panigrahi, and J. C. Parikh, eprint: nlin.CD/0601065 (2006).

- (18) I. Daubechies, Ten lectures on wavelets SIAM, Philadelphia, 1992.

- (19) S. Mallat, A Wavelet Tour of Signal Processing Academic Press, 1999.

- (20) C. S. Burrus, R. A. Gopinath, and H. Guo, Introduction to Wavelets and Wavelt Transforms Prentise Hall, New Jersy, 1998.

- (21) B. K. Joseph, R. Jha, P. K. Kaw, S. K. Mattoo, C. V. S. Rao, Y. C. Saxena, and the Aditya team, Phys. Plasmas 4 (1997) 4292.

- (22) R. Jha, P. K. Kaw, D. R. Kulkarni, and J. C. Parikh, Phys. Plasmas 10 (2003) 699.

- (23) E. Faleiro, J. M. Gómez, R. A. Molina, L. Muñoz, A. Relaño, and J. Retamosa, Phys. Rev. Lett. 93 (2004) 244101; A. Relaño, J. Retamosa, E. Faleiro, and J. M. Gómez, Phys. Rev. E 72 (2005) 066219.

- (24) P. Manimaran, P. A. Lakshmi, and P. K. Panigrahi, J. Phys. A: Math. Gen. 39 (2006) L599.