2. Econophysics Laboratory, 5-9-7-B Higashi-cho, Koganei-shi, Tokyo 184-0011, Japan. kaizoji@icu.ac.jp, http://subsite.icu.ac.jp/people/kaizoji/

Statistical properties of absolute log-returns and a stochastic model of stock markets with heterogeneous agents

Abstract

This paper is intended as an investigation of the statistical properties of absolute log-returns, defined as the absolute value of the logarithmic price change, for the Nikkei 225 index in the 28-year period from January 4, 1975 to December 30, 2002. We divided the time series of the Nikkei 225 index into two periods, an inflationary period and a deflationary period. We have previously [18] found that the distribution of absolute log-returns can be approximated by the power-law distribution in the inflationary period, while the distribution of absolute log-returns is well described by the exponential distribution in the deflationary period.

To further explore these empirical findings, we have introduced a model of stock markets which was proposed in [19,20]. In this model, the stock market is composed of two groups of traders: the fundamentalists, who believe that the asset price will return to the fundamental price, and the interacting traders, who can be noise traders. We show through numerical simulation of the model that when the number of interacting traders is greater than the number of fundamentalists, the power-law distribution of absolute log-returns is generated by the interacting traders’ herd behavior, and, inversely, when the number of fundamentalists is greater than the number of interacting traders, the exponential distribution of absolute log-returns is generated.

Key words: absolute log-returns; exponential laws; power laws; inflation; deflation; a stochastic model of stock markets; heterogeneous agents.

1 Introduction

Over the past few decades a considerable number of studies have been made of distributions of financial data. In the early studies, studies of daily fluctuations of commodity prices led Mandelbrot 1 and Fama 2 to propose that the associated distribution function is a power-law distribution with an exponent close to . More recently, some researchers have quantitatively reinvestigated the tick-by-tick data set of stock prices, which includes approximately million records, and found that the probability distribution of log-returns and volatility satisfies a power law with an exponent close to [3-6]. Theorists also use various versions of multiplicative random processes in the theoretical modeling of returns and volatility. An important goal of these market models is to explain the main stylized facts such as power laws observed in financial markets [7-17].

In this present study, we first examined the statistical properties of absolute log-returns, defined as the absolute value of the logarithmic price change, for the Nikkei 225 index. We divided the time series of the index into two periods, an inflationary period and a deflationary period. Using this division, we found that the distribution of the absolute log-returns can be approximated by the power-law distribution in the inflationary period, while the distribution of absolute log-returns is well-described by the exponential distribution in the deflationary period111We have previously reported these empirical findings [18] and analyzed the results from a slightly different perspective..

We then performed numerical simulations of the model of stock markets proposed in our previous works [19,20] in order to provide an explanation of the empirical findings. In our model, the stock market is composed of two typical groups of traders: the fundamentalists who believe that the asset price will return to the fundamental price, and the interacting traders who tend to be influenced by the investment attitudes of other traders. We show that our model can reproduce the above-mentioned statistical properties of absolute log-returns. In particular, we show the following:

-

•

When (i) the number of interacting traders is greater than the number of fundamentalists, and (ii) the interaction among interacting traders is strong, a power-law distribution of absolute log-returns is generated.

-

•

Inversely, when (i) the number of fundamentalists is greater than the number of interacting traders, and (ii) the interaction among interacting traders is weak, the exponential distribution of absolute log-returns is generated.

Thus the numerical simulation helps account for the empirical findings.

The rest of the paper is organized as follows: the next section reviews briefly the empirical findings. Section 3 describes the stochastic model, section 4 provides the results of the numerical simulation, and section 5 gives concluding remarks.

2 The Empirical Results [18]

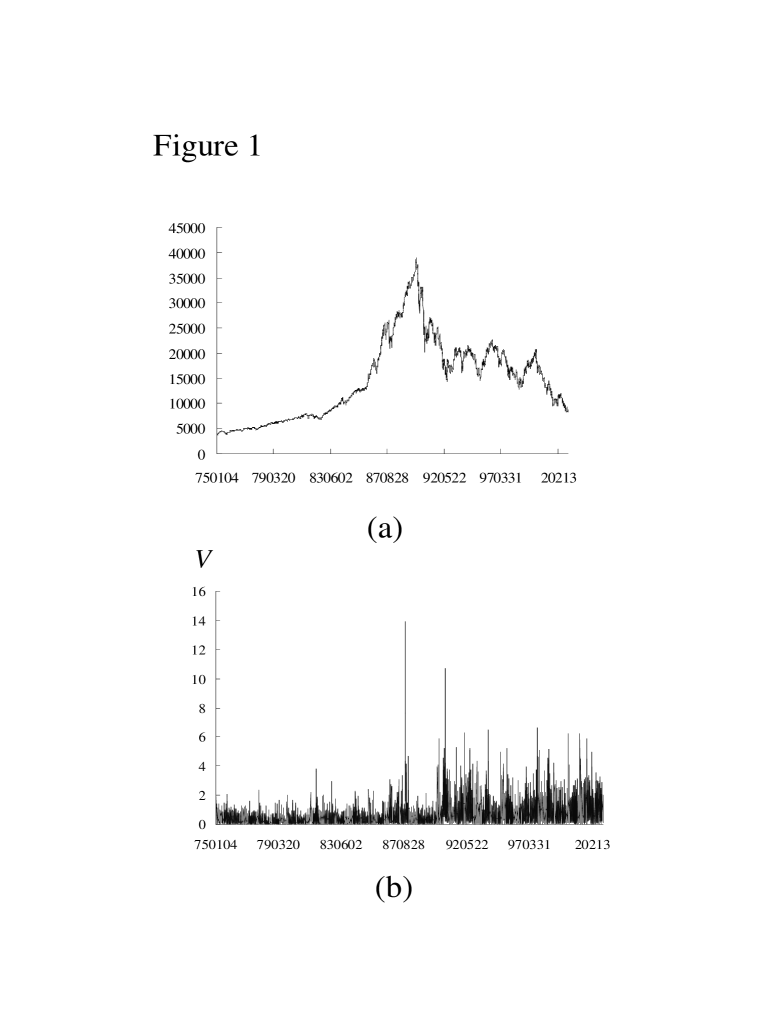

In this section we discuss the statistical properties of the absolute log-returns for the Nikkei 225 index in the 28-year period from January 4, 1975 to December 30, 2002. Figure 1(a) shows the time series of the Nikkei 225 index throughout the entire period. The Nikkei 225 index reached a high of almost 40,000 yen on the last trading day of the decade of the 1980s. However, the index had declined to 14,309 yen, a drop of approximately 63 percent by mid-August 1992. It follows from the figure that we can divide the time series of the Nikkei 225 index into two periods, an inflationary period from January 4, 1975 to December 29, 1989, and a deflationary period from January 4, 1990 to December 29, 2002. We define the return as the change in the logarithm of the index , where denotes the index at data . The term volatility represents a generic measure of the magnitude of market fluctuations. Thus, many different quantitative definitions of volatility are used in the literature. In this study, we define the volatility as the absolute value of the return, . Figure 1(b) shows the time series of the absolute log-return of the Nikkei 225 index.

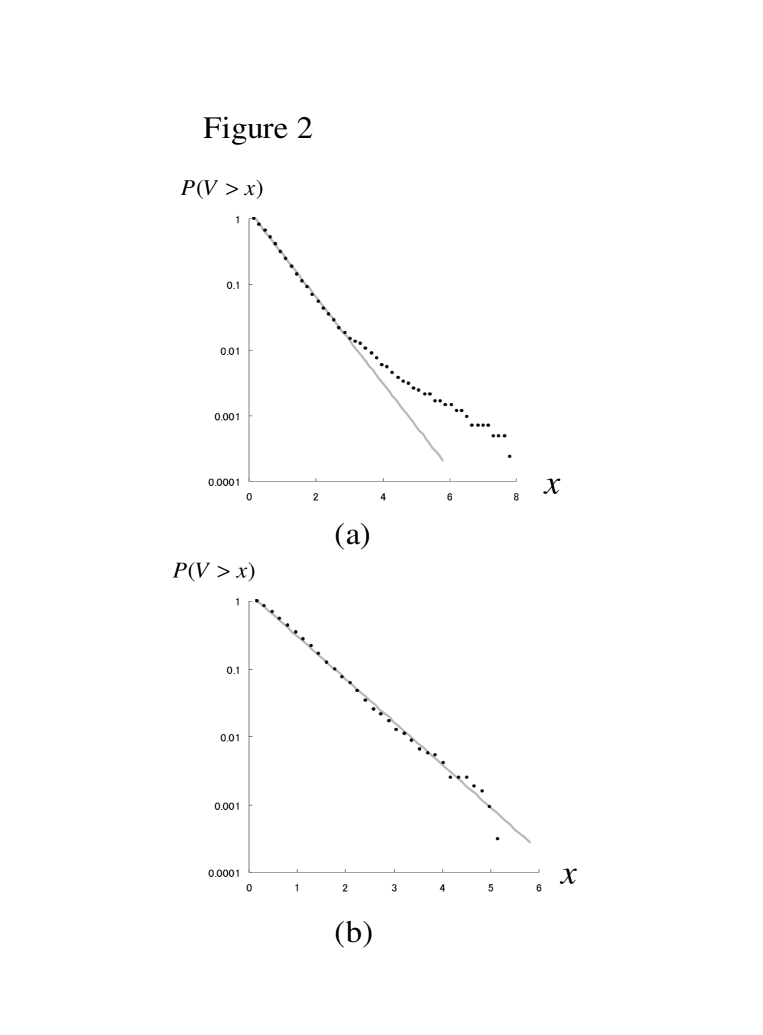

Figure 2(a) and 2(b) show the semi-log plots of the complementary cumulative distribution function of the absolute log-returns for the Nikkei 225 index in the inflationary and deflationary periods, respectively. We found that the complementary cumulative distribution function of the absolute log-returns for the deflationary period is accurately described by an exponential distribution in the whole range of the absolute log-returns . We estimate the parameter using the least-square method, and we estimate,

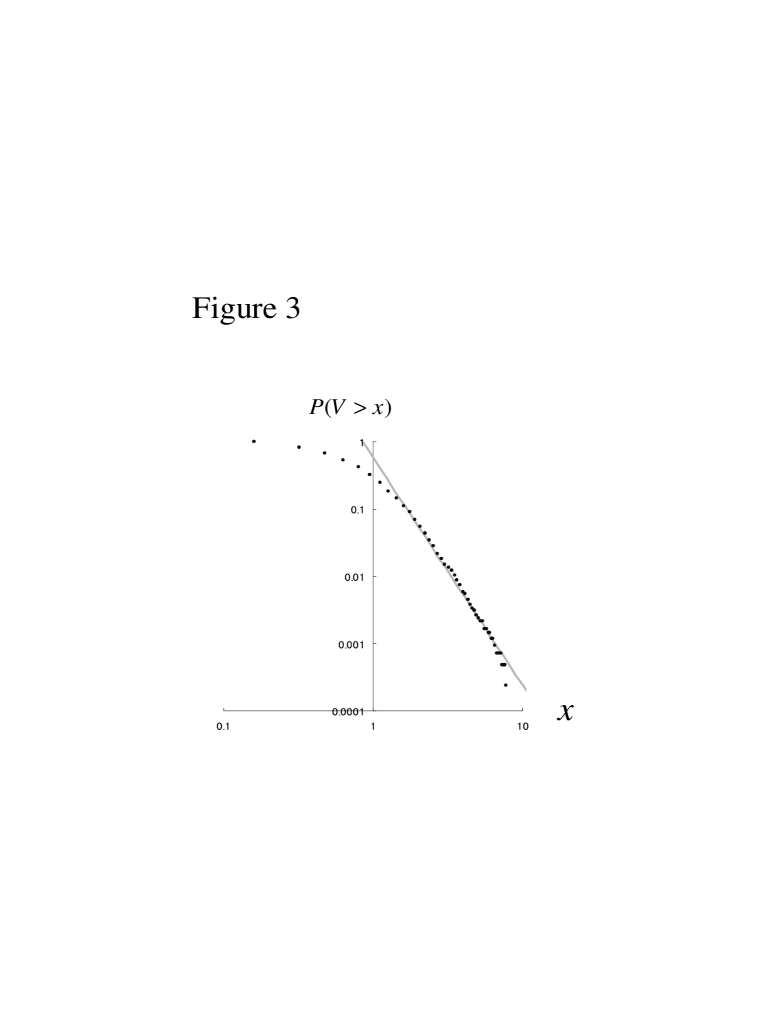

In contrast, the other hand the complementary cumulative distribution function of the absolute log-returns for the inflationary period fits the exponential law for low values of , and it deviates from the exponential distribution as the absolute log-return increases. Figure 3 shows the log-log plot of the complementary cumulative distribution function of the absolute log-returns in the inflationary period. It is apparent that this plot tends to a linear function for high values of , indicating that the complementary cumulative distribution function of the absolute log-returns is consistent with power law asymptotic behavior . The value of estimated by the least squared method in ,

In summary, we find that the distribution of absolute log-returns for stock price indices can be approximated by the power-law distribution in the inflationary period, while the distribution is accurately described by the exponential distribution in the deflationary period.

Why are empirically different laws observed? To answer this question, we propose a stochastic model in the following section.

3 A Stochastic Model of Stock Markets [19,20]

Let us consider a stock market where a stock is traded at price . Two groups of traders with different trading strategies, interacting traders and, fundamentalists participate in the trading. The number of fundamentalists and the number of interacting traders are assumed to be constant. The model is designed to describe the movements of the stock price over short periods, such as one day. In the following, a more precise account of the decision-making of each trader type is given.

3.1 Interacting traders

During each time period, an interacting trader may choose to either buy or sell the index, and is assumed to trade a fixed amount of the index in a period of trading. Interacting traders are labeled by an integer . The investment attitude of the interacting trader is represented by the random variable and is defined as follows: If interacting trader is a buyer of the index during a given period, then , otherwise he sells the index, and . Now let us formulate the dynamics of the investment attitude of interacting traders. Consider that the investment attitude of interacting trader is updated with transition probabilities as a function of the average investment attitude over interacting traders according to (transition from seller to buyer) and (transition from buyer to seller), where and denotes the interaction strengths among traders. Using the above transition probabilities, the Ito stochastic differential equation for the average investment attitude is obtained as

| (1) |

where is the Wiener process. To perform the numerical simulation, we consider a discretized version of the stochastic differential equation,

| (2) |

Here, , and . is the increment of the Wiener process or a white noise.

We next assume that the interacting-traders’ excess demand for the index is approximated as . Following [17], we assume that the interaction strengths change randomly in time , and furthermore, define the randomness as , where the parameter is a constant, and is the increment of the Wiener process.

3.2 Fundamentalists

Fundamentalists are assumed to have a reasonable knowledge of the fundamental value of the index . If the price is below the fundamental value , a fundamentalist tends to buy the index (as he estimates the index to be undervalued), and if the price is above the fundamental value, a fundamentalist tends to sell the index. Hence we assume that fundamentalists’ buying or selling order is given by , where is the number of fundamentalists, and parametrizes the strength of the reaction on the discrepancy between the fundamental price and the market price.

3.3 Market price

Let us leave the traders’ decision-making processes and turn to the determination of the market price. We assume the existence of a market clearing system. In the system, a market maker mediates the trading and adjusts the market price to the market clearing values. The market transaction is executed when the buying orders are equal to the selling orders. The balance of demand and supply is written as . The market price is therefore calculated as where . Using the price equation, we can categorize the market situations as follows: If , the market price is equal to the fundamental price . If , the market price exceeds the fundamental price (bull market regime). If , the market price is less than the fundamental price (bear market regime). Using the price equation, the log-return is defined as

| (3) |

For simplicity of analysis we here assume that the fundamental price remains constant.

4 Simulations

We are interested in the statistical properties of time series generated by our model and how they compare with those of real data shown in Section 2. In this section we perform numerical simulation of the model introduced in Section 3.

To this end, we consider two cases with different sets of parameters:

-

1.

Case I: ; ; ; ; ; .

-

2.

Case II: ; ; ; ; ; .

Case I describes the situation of the stock market in the inflationary period. Namely, Case I assumes that (i) a large number of traders participate in trade, and (ii) the number of interacting traders is greater than the number of fundamentalists, and (iii) the interaction among the interacting traders is strong. In contrast, Case II describes the situation of the stock market in the deflationary period. Case II assumes that (i) a small number of traders participates in trade, and (ii) the number of interacting traders is less than the number of fundamentalists, and (iii) the interaction among the interacting traders is weak222For the mathematical explanation and results of the comprehensively numerical simulations of this model, see [20]..

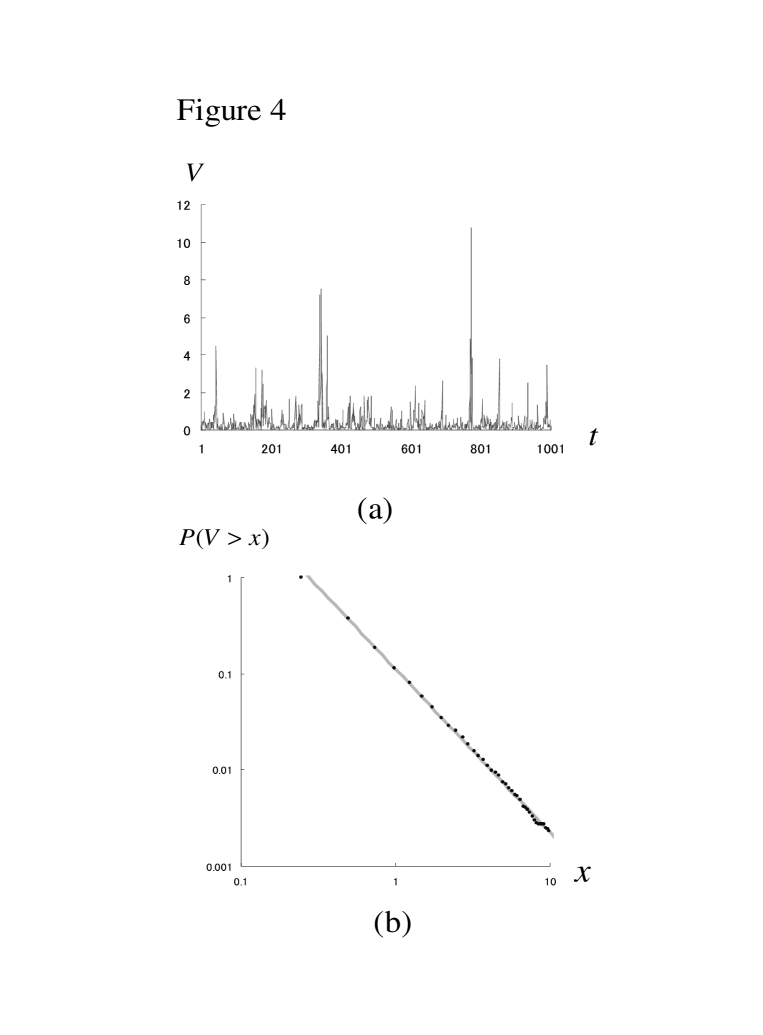

Figure 4(a) displays a typical time series of the absolute log-returns generated numerically from the model with Case I. Figure 4(b) shows the complementary cumulative distribution function in log-log scale, calculated from the model series of the absolute log-returns in Fig. 4(a). The figure shows that the complementary cumulative distribution function of the absolute log-returns is approximated by the power-law distribution with the exponent equal to .

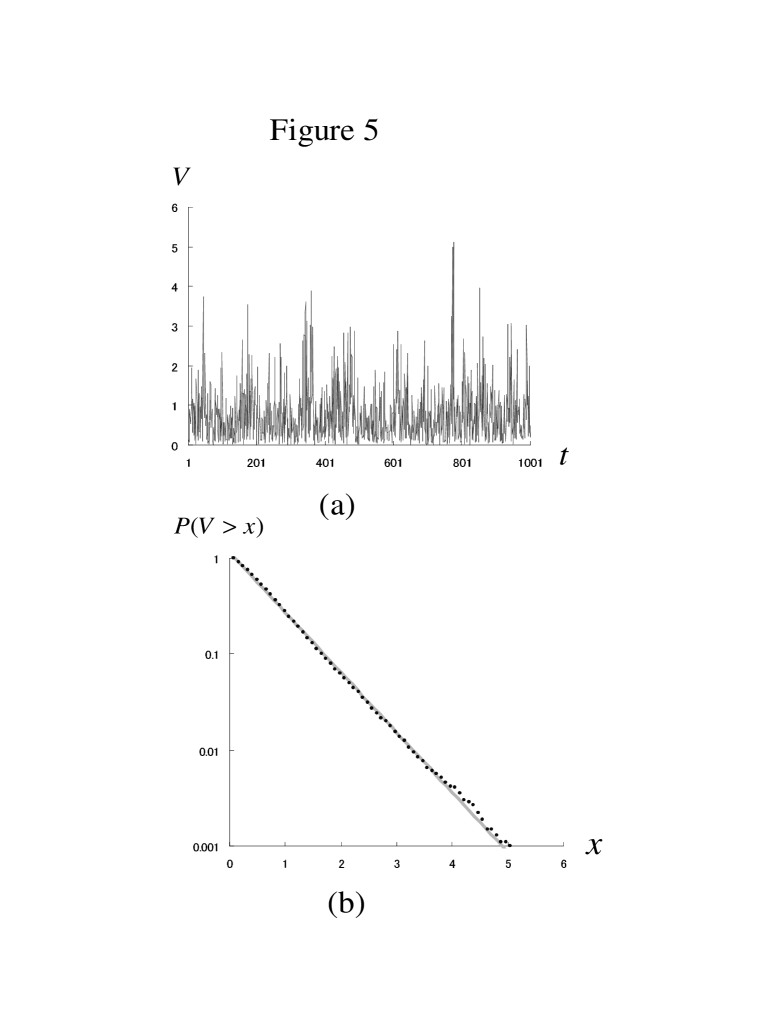

We next perform the numerical simulation of the model with Case II. Figure 5(a) shows a typical time series of the absolute log-returns generated from the model with Case II. Figure 5(b) indicates the semi-log plot of the complementary cumulative distribution function of the absolute log-returns calculated using the model series of the absolute log-returns in Fig. 5(a). The figure shows that the complementary cumulative distribution function of the absolute log-returns is accurately described by the exponential distribution . The estimated parameter is equal to .

5 Concluding remarks

In this paper we first showed the statistical properties of the Nikkei 225 index, that is, (i) in periods of inflation the complementary cumulative distribution function of the absolute log-returns is approximated by the power-law distribution, and (ii) in periods of deflation the complementary cumulative distribution function of the absolute log-returns is accurately described by the exponential distribution.

We next introduced a stochastically macroscopic model of stock markets to explain these empirical findings. In our model, the stock market is composed of two groups of traders: the fundamentalists and the interacting traders. The results of the numerical simulation suggest the following: in the period of inflation, the number of interacting traders strongly influenced by the investment attitudes of others is greater than the number of fundamentalists, who believe that the asset price will return to the fundamental price, so that power-law distribution of the absolute log-returns is generated by interacting traders’ herd behavior. On the other hand, we can deduce that in the period of deflation a number of interacting traders leave the stock markets, and furthermore the interaction among the interacting traders is weak, while most of fundamentalists stay in the market; as such, the exponential law of absolute log-returns is observed.

As a consequence, the model captures the two opposing empirical data sets observed in real financial markets, and provides a reasonable explanation of the empirical findings we presented in section 2. Although the model is simple, it may thus be seen as a reasonable approximation of the absolute log-returns in real stock markets.

6 Acknowledgements

I wish to express my gratitude to Michiyo Kaizoji for her helpful discussion and her assistance in collecting the data, and Enrico Scalas for helpful suggestions and comments. This research was supported in part by the Japan Society for the Promotion of Science (JSPS) under the Grant-in-Aid, No.06632.

References

- (1) B. Mandelbrot, J. Business, 36, 34 (1965).

- (2) E.F. Fama, J. Business, 38, 35 (1965).

- (3) P. Gopikrishnan, et. al., Phys. Rev., 5305 E60 (1999).

- (4) V. Plerou, et. al., Phys. Rev., E60, 6519 (1999).

- (5) Y. Liu, et. al., Phys. Rev. E60, 1390 (1999).

- (6) P. Cizeau, et. Al., Physica A245, 437 (1997).

- (7) P.Bak, M.Paczuski and M. Shubik, Physica A246, 430 (1997).

- (8) D. Challet and Y.-C. Zhang, Physica A246, 407 (1997).

- (9) R. Cont and J. P. Bouchaud, Macroeconomic Dynamics 4, 170 (2000).

- (10) T. Lux, and M. Marchesi, Nature 397, 498 (1999).

- (11) D. Stauffer and D. Sornette, Physica A271, 496 (1999).

- (12) D. Chowdhury and D. Stauffer, Eur. Phys. J. B8, 477 (1999).

- (13) G. Iori, Int. Mod. Phys. C10, 1149 (1999).

- (14) D. Sornette, Physica A284, 355 (2000).

- (15) B.M. Roehner and D. Sornette, Eur. Phys. J. B16, 729 (2000).

- (16) S. Bornholdt, Int. J. Mod. Phys. C12 667 (2001).

- (17) A. Krawiecki, J.A. Holyst and D. Helbing, Phys. Rev. Lett. 89, 158701 (2002).

- (18) T. Kaizoji, Inflation and deflation in financial markets, (2003) available from http://arxiv.org/abs/cond-mat/0401140.

- (19) T. Kaizoji and M. Kaizoji, Advances in Complex Systems 6 (3) (2003) 1.

- (20) T. Kaizoji and M. Kaizoji, Modeling absolute log-returns, unpublished paper (2003).