Moody’s Correlated Binomial Default Distributions for Inhomogeneous Portfolios

Abstract

This paper generalizes Moody’s correlated binomial default distribution for homogeneous (exchangeable) credit portfolio, which is introduced by Witt, to the case of inhomogeneous portfolios. As inhomogeneous portfolios, we consider two cases. In the first case, we treat a portfolio whose assets have uniform default correlation and non-uniform default probabilities. We obtain the default probability distribution and study the effect of the inhomogeneity on it. The second case corresponds to a portfolio with inhomogeneous default correlation. Assets are categorized in several different sectors and the inter-sector and intra-sector correlations are not the same. We construct the joint default probabilities and obtain the default probability distribution. We show that as the number of assets in each sector decreases, inter-sector correlation becomes more important than intra-sector correlation. We study the maximum values of the inter-sector default correlation. Our generalization method can be applied to any correlated binomial default distribution model which has explicit relations to the conditional default probabilities or conditional default correlations, e.g. Credit Risk+, implied default distributions. We also compare some popular CDO pricing models from the viewpoint of the range of the implied tranche correlation.

1 Introduction

The modeling of portfolio credit risk and default correlation are hot topics and pose entirely new problems [1, 2, 3, 4, 5]. CDOs are financial innovations to securitize portfolios of defaultable assets. Many probabilistic models have been studied in order to price CDO tranches [6, 7, 8, 9, 10, 11, 12, 3, 13, 14, 15]. Most of them are implemented with Monte Carlo simulations and as the number of names in a portfolio increases, the computational time increases. The Factor approach uses a small number of latent factors that induce the default dependency [11]. Conditionally on the latent variables values, default events are independent. It becomes easy to calculate the loss (default) distribution function. Along this line, some semi-explicit expressions of most relevant quantities were obtained [16].

On the other hand, correlated binomial models were also proposed to describe the default dependency structures. The first one is a one-factor exchangeable version of CreditRisk + [17, 18, 19]. The aggregate loss distribution function is given by the beta-binomial distribution (BBD). The second one is Moody’s correlated binomial default distribution model, which was introduced by Witt [20].( hereafter the MCB model) The authors also consider the applicability of the long-range Ising model [21, 22]. These models use Bernoulli random variables. Differences stem from different definitions of the conditional correlations [23]. In the MCB model [20], the conditional default correlation between assets is set to be constant irrespective of the number of defaults. Those of BBD decay with an increase in default. We are able to adapt a suitable form for the conditional correlations. Recently it has become possible to calibrate from implied default distributions [24]. By using the “implied correlated” binomial model, whose conditional correlations are those of the implied distribution, it may become easy to estimate hedge ratios and so forth.

The advantage of these correlated binomial models come from the fact that they are easier to evaluate than other more refined models. If a probabilistic model is implemented by a Monte Carlo simulation, the evaluation of the price of these derivatives consumes much computer time and the inverse process to obtain the model parameters becomes tedious work. With the above correlated binomial models, one can estimate the model parameters from the CDO premiums more easily. However, these models are formulated only for homogeneous portfolios, where the assets are exchangeable and they have the same default probability and default correlation . Generalization to more realistic inhomogeneous portfolios where assets have different default probabilities and different default correlations should be done.

In this paper, we show how to generalize Moody’s correlated binomial default distribution (MCB) model to two types of inhomogeneous portfolios. Our generalization method can be applied to other correlated binomial models, including implied correlated binomial distributions, by changing the condition on . We obtain the default probability function and examine the dependence of the expected loss rates of the tranches on the inhomogeneities. With the proposed model, we also estimate the implied values of the default correlation. Comparison of the range of the tranche correlations with those of the Gaussian copula model and BBD model are also performed.

About the organization in this paper, we start with a short review of Moody’s correlated binomial default distribution (MCB) model in Section 2. The dependence of on the number of defaults is compared with the BBD and Gaussian copula. Section 3 is the main part of the paper. We show how to couple multiple MCB models as a portfolios credit risk model for inhomogeneous portfolio. In the first subsection, we couple two Bernoulli random variables and recall on the limit of the correlation between them. In the next subsection, we couple an MCB model of assets with a random variable and we study the maximum value of the correlation between and . Then we couple two MCB models with and assets. Choosing the model parameters properly, we construct an MCB model for an inhomogeneous default probability case and obtain the default distribution function. The last subsection is devoted to an inhomogeneous default correlation case. Assets are categorized in different sectors and inter-sector and intra-sector default correlations are not the same. We consider a portfolio with sectors and th sector contains assets. Within each sector, the portfolio is homogeneous and it has parameters as and . The inter-sector default correlations are not the same and they depend on the choice of sector pairs. We construct the joint default probabilities and the default probability function for the portfolio explicitly. In Section 4, using the above results, we estimate the implied default correlation for each tranche from a CDO’s market quotes ( iTraxx-CJ Series 2). We compare the range of the correlations of MCBs, BBD and the Gaussian copula model. We conclude with some remarks and future problems.

2 Moody’s correlated binomial default distribution

We review the definitions and some properties of Moody’s correlated binomial default distribution (MCB) model. We consider a homogeneous portfolio, which is composed of exchangeable assets. Here the term “homogeneous” means that the constituent assets are exchangeable and their default probabilities and default correlations are uniform. We denote them as and . Bernoulli random variables show the states of the -th assets. means that the asset is defaulted and the non-default state is represented as . The joint default probabilities are denoted as

| (1) |

In order to determine , we need conditions for them. Here corresponds to the number of possible configurations and comes from the overall normalization condition for the joint probabilities. From the assumption of the homogeneity for the portfolio, the number of degrees of freedom of the joint probabilities are reduced. The probability for defaults and non-defaults is the same for any configuration with . The number of defaults is ranged from to and considering the overall normalization condition, remaining degrees of freedom are .

In the MCB model, the conditional default probabilities are introduced. We denote as the default probability for any assets under the condition that any other assets of the portfolio are defaulted. To exemplify the situation concretely, we take the assets as the first of assets, we denote them with as . The condition that they are defaulted is written concisely as . The conditional default probability for -th assets under the condition of defaults can then be written as

| (2) |

Here, means the expected value of random variable under condition is satisfied. takes for -th asset default, corresponds to its default probability under condition . Of course, any asset from can be chosen in the evaluation of the expected value for under the condition that . is nothing but the default probability .

independent conditional default probabilities are determined by the following condition on the default correlations.

| (3) |

Here, is defined as

| (4) |

The conditions on the default correlations give us the following recursion relations for as

| (5) |

These recursion relations can be solved to give as

| (6) |

increases with and as for .

From these conditional default probabilities , the joint default probabilities for the configuration are given as

| (7) |

The normalization condition for is guaranteed by the following decomposition of unity.

| (8) |

The probability for defaults is

| (9) | |||||

We modify the above MCB model as follows. In the MCB model, the default correlation is set to be constant irrespective of the number of default (see(3)). We change the condition as

| (10) |

Here, we introduce a parameter and the default correlation under defaults decay as . If we set , the modified model reduces to the original MCB model.

There are two motivations for the modification. The first one is that it is mathematically necessary to couple multiple MCB models. We discuss the mechanism in greater detail in the next section. Here, we only comment on the limit value of as . The modification changes the recursive relation for to

| (11) |

is calculated as

| (12) |

Here is defined as .

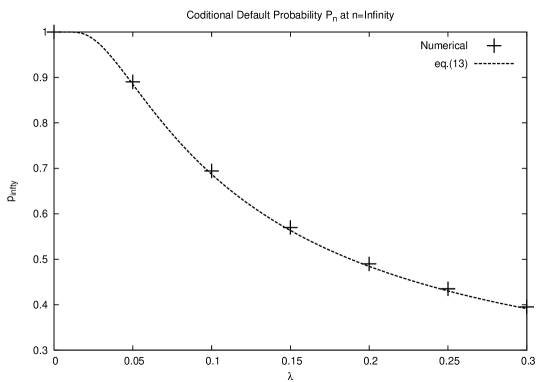

increases with , however the increase is reduced by the decay of the correlation with . The limit value of with is roughly estimated as

| (13) |

For , and for . In Figure 2, we show the enumerated data for and the results from eq.(13). As increases, decreases and the dependence is well described by eq.(13).

The second motivation is that popular CDO pricing models have decaying correlation with . The BBD model’s is given as [23]

| (14) |

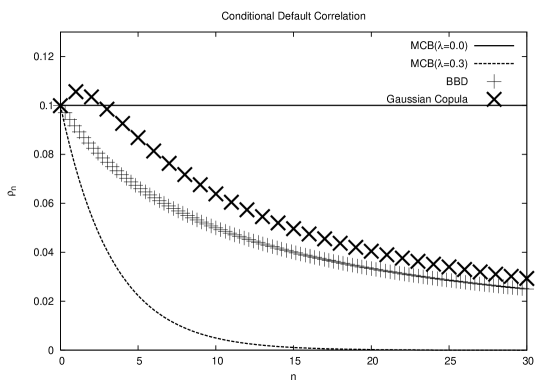

In the Gaussian copula model, we do not have the explicit form for . From its aggregate loss distribution function, it is possible to estimate them. In Figure 3, we show for the MCB, BBD and Gaussian copula models. We set and . The Gaussian copula’s does not show monotonic dependence on . After a small peak,. it decays to zero. In order to mimic the Gaussian copula model within the framework of a correlated binomial model, such a dependence should be incorporated in the assumption on .

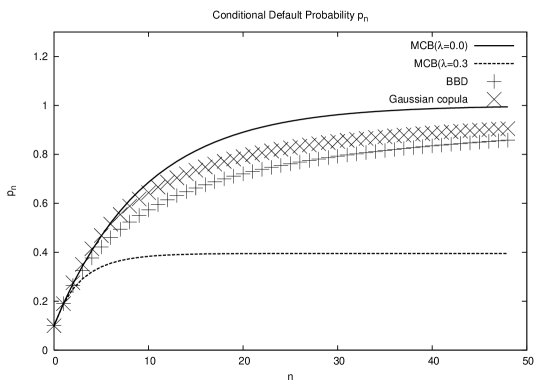

Figure 4 depicts in the same setting. With the same and , all curves pass through at and at . After , the behaviors of depend on the models’ definitions on . saturate to about for MCB, which means that a large scale avalanche does not occur and the loss distribution function has a short tail. In MCB with and Gaussian copula models, their saturate to 1. The behaviors are reflected in the fat and long tails in their loss distribution.

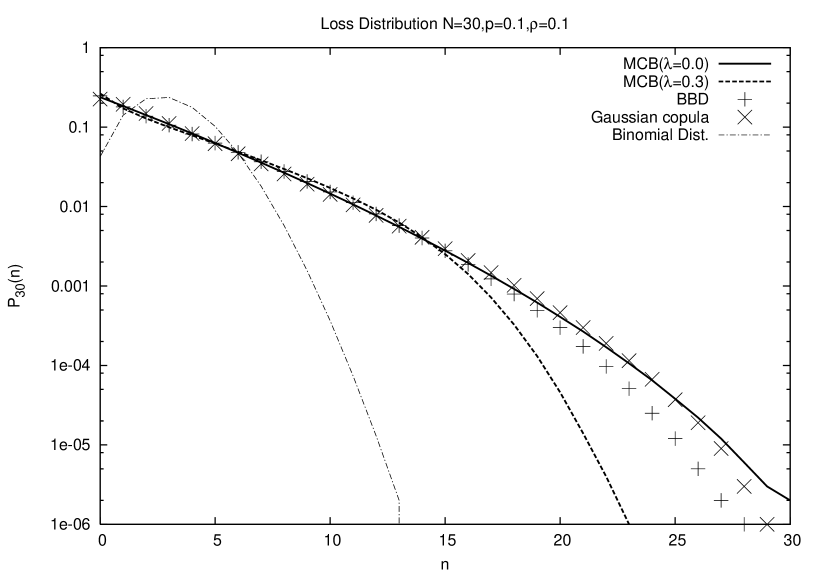

Figure 5 shows the semi-log plot of for the MCB, BBD and Gaussian copula models. We also plot the binomial distribution Bin. The default correlation shifts the peak of the binomial distribution to and comes to have a long tail. MCB, BBD and Gaussian copula have almost the same bulk shape. In particular, in MCB, even if we change , has almost the same shape for . The bulk shape of is mainly determined by with small . s with large comes from very rare events and contains information about the tails of the distributions. They do not affect the bulk part significantly .

There are differences in their tails. One sorts the models in the order of thinnest tail to fattest tail, we have

MCB() has almost the same shape as the Gaussian copula. However, it has a bigger tail than the gaussian coupla at . The tail of MCB is short compared with other models. We can understand this behavior from the behavior of .

We also note another role of the damping parameter . In the calculation , there are many cancellations in (9) from the decomposition of . This causes numerical errors in the evaluation and it is difficult to get for , even if we use long double precision variables in the numerical implementation. When we set , the numerical error diminishes greatly and we can obtain even for . This point is important when one uses the MCB model for analysis of the actual CDOs that have at least 50 assets. In addition, with , we can take to be negatively large enough. In S&P’s data, a negative default correlation of or so has been reported [25]. We think that this point is also an advantage of the modified model.

Hereafter, we mainly focus on the generalization of the MCB model. However, the same method and reasoning should be applicable to other correlated binomial models with any assumption on . If we set as in (14), we have Beta-Binomial default distribution models for inhomogeneous portfolios.

3 Generalization to Inhomogeneous Portfolios

In this section we couple multiple MCB models and construct the joint default probabilities and for inhomogeneous portfolios. In addition, we show that the inter-sector default correlation can be set to be large enough by choosing and other parameters. We think that it is possible to use the model as a model for portfolio credit risk.

3.1 Coupling of and : 1+1 MCB model

Before proceeding to the coupling of multiple MCB models, we recall some results for the coupling of two random variables and . The default probability is () for (respectively for ) and the default correlation between them is ,

| (15) |

As in the MCB model, we introduce the conditional default probabilities as

| (16) |

From the default correlation , and are calculated as

| (17) |

In the symmetric (homogeneous) case , the equality holds and they are given as

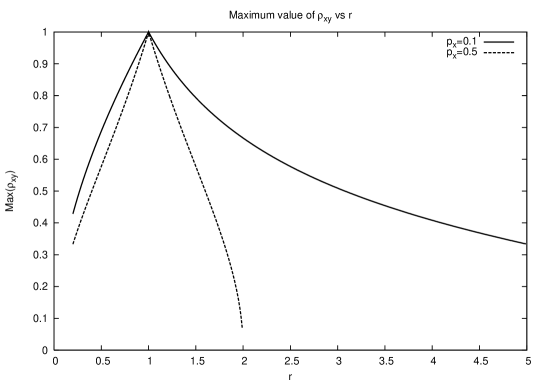

The correlation can be set to be and in the limit . The maximum value of is 1 in the symmetric case. Conversely in the asymmetric case (), cannot set to be . The maximum value of is determined by the condition that and . From these conditions, we derive the following conditions [26] on as

| (18) |

We introduce an asymmetric parameter as

| (19) |

and a function as

| (20) |

The maximum value of is then given as

| (21) |

Here Max represents the maximum value of and Min means that the smaller value of and is taken.

Figure 6 shows Max as a function of the asymmetric (inhomogeneity) parameter . We show two curves, the solid one for and the dotted one for . As the inhomogeneity increases, that is departs from , Max decreases. For fixed , as becomes large, Max becomes small. The reason is that the condition becomes more difficult to satisfy as increase. is a monotonous increasing function of . In the previous section, the conditional default probability becomes smaller as we set larger. When we set a large , we show that it is possible to couple multiple MCB models with strong default correlation.

3.2 MCB model

For the second step, we couple an assets MCB model with one two-valued random variable . We introduce random variables and the default probability and the default correlation for them is and . The default probability for is and the default correlation between and is written as . We assume homogeneity for the assets MCB model and the default correlation between and is independent of the asset index . As in the previous cases, we introduce conditional default probabilities as

| (22) |

The joint default probabilities are calculated by decomposing the following expression with these conditional default probabilities

| (23) |

The joint default probabilities with the condition are

| (24) |

The joint probabilities with the condition are obtained by the following relations.

| (25) |

The explicit form for is

| (26) |

The probability for defaults is given as in eq.(9)

| (27) |

The probability for defaults with is

| (28) |

Using the same argument as for the joint probabilities with , is written as

| (29) |

About the conditional default probabilities , we impose the same conditions as with the homogeneous assets MCB model.

| (30) |

The same recursive relation (11) for is obtained and the is given by

| (31) |

Here is defined as before. Fot the conditions on and , there are two possible ways to realize a strong correlation. The only way to realize a strong correlation between and is

| (32) |

In this case, the relations for and are

| (33) |

The recursive relations are

| (34) | |||||

| (35) |

If we set and , these relations reduce to and and this coupled model is nothing but the assets MCB model.

We write the ratio as and the conditions that and are summarized as

| (36) |

Min is nothing but the condition for Max of the two random variables with default probabilities (see eq.(21)). As explained above, Min takes maximum value at for any value of . It also decrease with the increase of for fixed .

The necessary condition for the model to be self-consistent is that and for all . We discuss and cases separately.

-

•

: increases with and as . The range of is and it is difficult to choose such that for all . If departs much from 1 for some , Max decreases. The choice and is possible, we anticipate that Max decreases from as departs from .

-

•

: The limit value of becomes small (see eq.(13)) and the range of is narrow as compared with the case. It may be possible to choose such that the asymmetric parameter is small for small . In addition, for large , it is easy to satisfy the condition (36) because of the prefactor . We think that Max is large in this case.

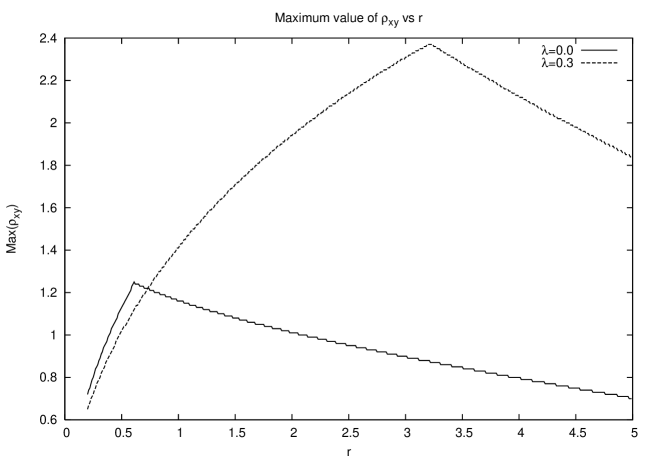

We have checked numerically the values of the joint probabilities for all configurations with and . In figure 7, we show the data of Max for the case (solid line) and (dotted line). In the case, Max near and as departs from 1, Max decreases from . The data for case show that it is possible to set a large Max if we use a large . We can set as strong as several times of .

We also point out that the above MCB model can be used to describe a credit portfolio where one obligor has great exposure. Such an obligor is described by and other obligors are by . If is quite different from , we can couple and with strong by setting a sufficiently large .

3.3 MCB Model : Coupled MCB model

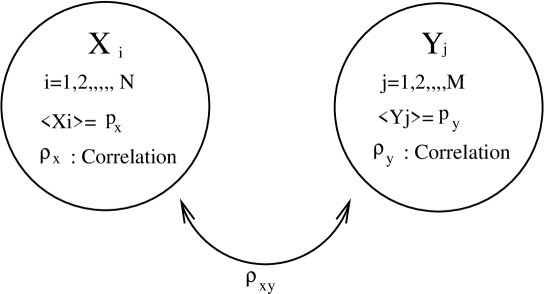

Next we consider a portfolio with two sectors. The first sector has assets and the second has assets. To construct the joint default probabilities for the portfolio, we try to couple two MCB models. The former model’s assets are described by and the states of the latter model’s assets are described by . The default probability and the default correlation in each sector are () and (). The default correlation between the assets in different sectors is denoted as (see Figure 8).

Introducing the conditional default probabilities and as

| (37) | |||||

| (38) |

we impose the following conditions on and

| (39) | |||

| (40) |

The recursive relations for and are

| (41) | |||

| (42) |

Their solutions are, by denoting and ,

| (43) | |||

| (44) |

For the inter-sector correlation, we impose the next conditions on and , which is a natural generalization of case (see eq.(32)).

| (45) |

We obtain the following recursive relations,

| (46) |

Using these relations, we are able to calculate and iteratively starting from and .

The joint default probability for the portfolio configuration is calculated by decomposing the following expression with and

| (47) |

In particular, the probability for defaults in each sector, which is denoted as , is

| (48) |

is easily calculated from as

| (49) |

In decomposing , one can do it in any order. The independence of the order of the decomposition of is guaranteed by (45) and (46). We decompose it as

| (50) |

For the maximum value of , it is necessary to check all values of the joint probabilities. However, model is reduced to or model by choosing or respectively. From the discussions and the results in the previous subsection for the model, we can anticipate as follows.

-

1.

: If and , two MCB models are the same and we can set . Two models merge completely and we have a assets MCB model. As the asymmetry between the two models becomes large ( or ) , Max decreases from .

-

2.

: As increase, Max becomes large. The asymmetry in and diminishes Max.

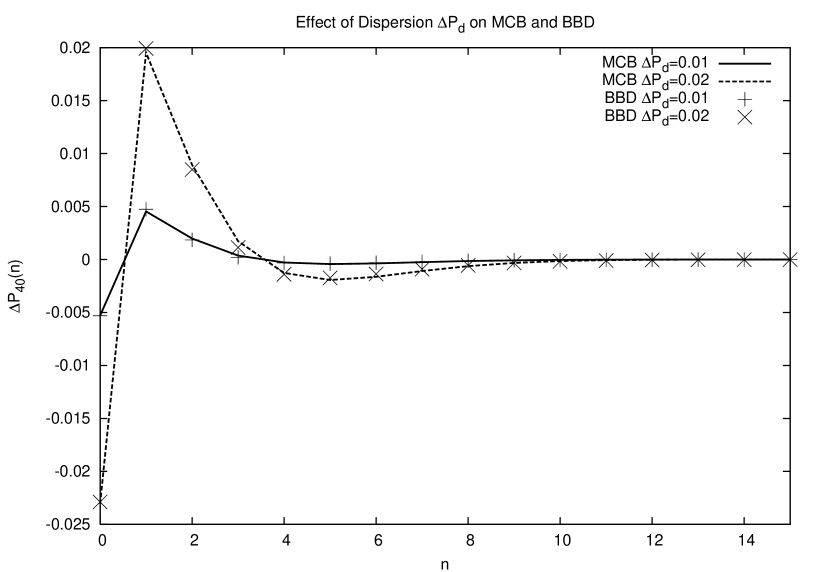

Using the above coupled MCB model, we study the effect of the dispersion of the default probability on and on the evaluation of tranches. More complete analysis about the difference between the usage of individual spreads and of portfolio average spreads in CDO pricing has been performed in [5]. There, the usage of the average spread results in the lower estimation of the equity tranche. We consider a portfolio with assets. The assets in each sector have default probabilities and an intra-sector default correlation . We set the inter-sector default correlation also as . The inhomogeneity in the default probability is controlled by . If we set , the two sector are completely merged to one sector and we have a homogeneous MCB model with and . In figure 9, we shows the default probability difference between the inhomogeneous case with and homogeneous case . is defined as

| (51) |

We set , and . The solid curve represents the data for and the dotted curve stands for the case . We see that is large only for small . We also plot the results for the BBD model. To construct the loss distribution function, it is necessary to change (39) and (40) to

| (52) | |||

| (53) |

Eq.(45) is also changed as

| (54) |

The recursive relations are also changed, but the remaining procedures are the same as for the MCB model. As we have shown in the previous section, the bulk shapes of the loss distribution of MCB and BBD models are almost the same, and the effects of on them are also similar.

To see the effect of on the evaluations of tranches, we need to study the change in the cumulative distribution functions . is defined as

| (55) |

represents the expected loss rate of the th tranche, which is damaged if more than assets default[22]. One of the important properties of is

| (56) |

This identity means that the tranches distribute the portfolio credit risk between them. Another important property of is that the expected loss rate of the layer protection with attachment point and detachment point can be built up from as

| (57) |

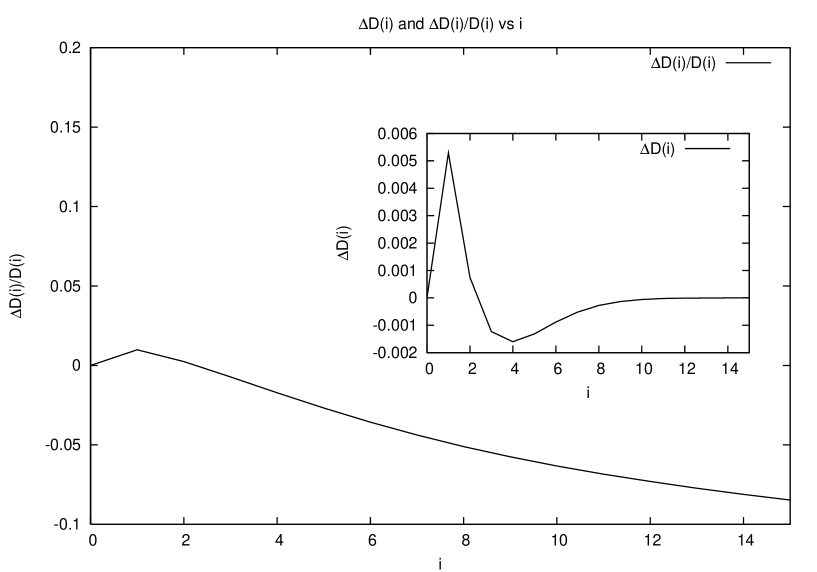

Figure 10 shows the plots of and of the ratio vs . We see that the lower tranches’ expected losses increase by , which is reasonable. The default probability of half the assets of the portfolio increases and the expected losses of the subordinated tranches increase. For the senior tranches, the absolute value of decreases with , however this does not mean that does not have a small effect on them. The absolute value of also decreases with . From Figure 10, we see that the ratio does not necessarily decrease with .

3.4 Multi Sector Case

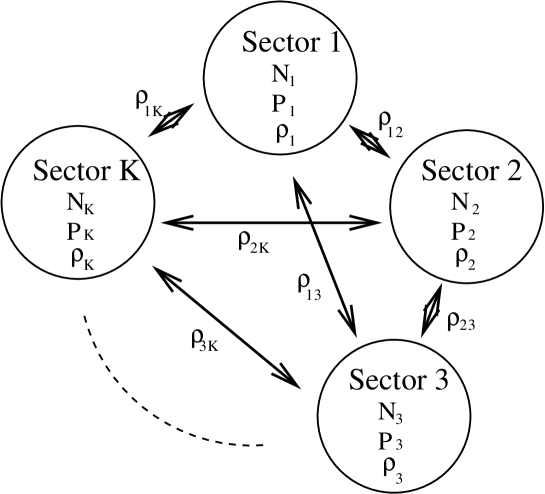

To couple two or more MCB models, we consider a portfolio with assets, which are categorized in different sectors. Figure 11 sketches the structure of the portfolio. The -th sector contains assets and the relation holds. The states of the assets in the -th sector is described by and the default rate and default correlation are denoted as and . For the inter-sector default correlation, we denote this as for the default correlation between the th and th sector. The intra-sector default correlation and inter-sector default correlation are different and the former is larger than the latter in general [27].

We have not yet succeeded in the coupling of three or more MCB models by generalizing the result for the coupled MCB model. The reason is that the self-consistency relations are very rigid restrictions on the MCB model. These relations, for which the two-sectors version is given by (46), assure the independence of the order of the decomposition in the estimation of the expected values of the product of random variables. It is difficult to impose any simple relations on the conditional default probabilities that satisfy the self-consistency relations.

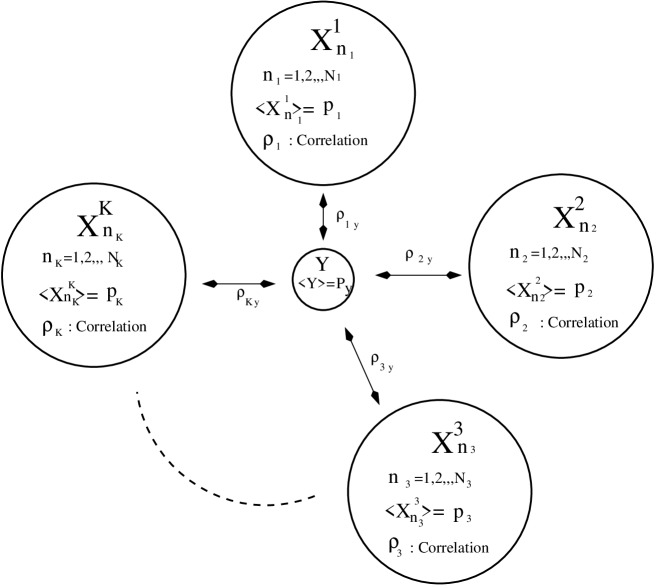

In order to construct the joint default probabilities for the assets states , we do not glue together MCB models directly. Instead, as depicted in figure 12, we glue multiple MCB models through one random variable . More concretely, we prepare sets of MCB models. MCB model is the MCB model coupled with . The probability of is written as . We Introduce the following conditional default probabilities

| (58) |

We also impose the following conditions on and as

| (59) | |||

| (60) |

The joint default probabilities and the conditional joint default probabilities are constructed as before.

| (61) | |||

| (62) |

Packing these conditional default probabilities into a bundle, we construct the joint default probabilities for the total portfolio as

| (63) |

We also obtain the default probability function for default in the -th sector as

| (64) |

From the expression, it it easy to calculate the probability for defaults and we write it as .

For the default correlation between the different sectors, we can show the next relations.

| (65) |

More generally, the conditional inter-sector default correlations obey the following relations.

| (66) |

These relations mean that our construction procedure is natural from the viewpoint of the original MCB model. In particular, in the case, these relations are completely equivalent with those of the coupled MCB model. See (45) and (66). The conditional default probabilities obey the same conditions.

Furthermore, from the results on Max() of the MCB model, we see that the model can induce a realistic magnitude of the inter-sector default correlation. By choosing and properly, it is possible to set as large as several times of .

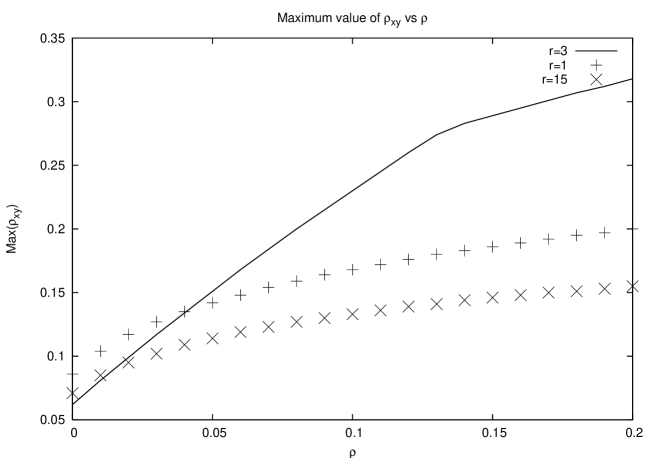

Figure 13 plots Max=Max() as functions of . We set parameters as depicted in the figure. The solid line depicts the data for . The other two curves correspond to () and (). We see that by setting . it is possible to set as large as several times of . If the intra-sector correlation is , we can set . The inter-sector correlations is then . In general, is smaller that , we think that the present model can incorporate a strong enough inter-sector default correlation.

To prove the relations (65) and (66), in order to calculate the correlation, we need to estimate the next expression.

| (67) |

If we fix the random variable , and are independent. They are coupled by and the above equation is estimated by the average over and as

| (68) |

Here, we denote the conditional default probabilities with the condition as ,

| (69) |

Between and , the next relation holds.

| (70) |

In addition, from the correlation between and , we also have the next relations.

| (71) |

Putting these relations into (68), we can prove the next equations.

| (72) |

Using these relations, we calculate the inter-sector correlation and prove (66).

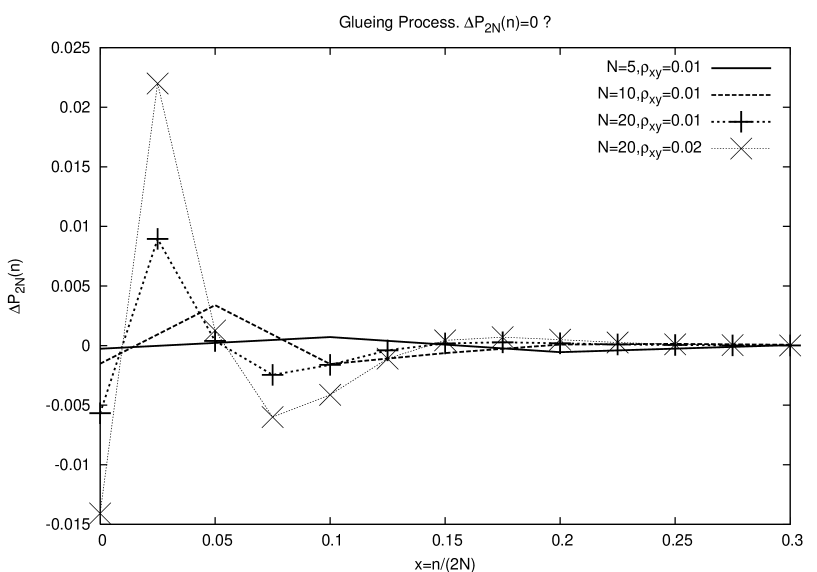

Next we need to check the validity of the above gluing process. We consider the two sector case and their intra-sector parameters are set to be the same as , and in each sector. For the inter-sector default correlation , we set in the above multi-sector model. If the glueing process of the multi-sector model works well, should coincide with of the coupled MCB model in the previous subsection. Figure 14 shows with and . We set and . In addition we also plot the data for and . As the system size becomes large, the discrepancy increases. With the same system size , as the inter-sector correlation increases, the discrepancy also increases. As we have stated previously, these models obey the same conditions on the conditional default probabilities, however the default probability profile does not coincide. The glueing process by the auxiliary random variable may cause changes to the joint probabilities. We have not yet fully understood this point.

With the present model, we study the effects of the inhomogeneous default correlation on the default distribution function and the loss rates . We consider ideal portfolios which have the same default probability and default correlation . The inter-sector default correlations are also set to be the same value as . are also set to be the same . We fix the total number of assets as and compare and between the portfolios with different number of sectors . Of course, between and the relation holds. We set . As the number increases, the average default correlation is governed by the inter-sector correlation and becomes weak.

At the extreme limit case, each sector contains only one asset. In the inter-sector default correlation, is given by the superposition of and . The conditional default probabilities and are given as

| (73) | |||

| (74) |

and are the binomial distributions Bin and Bin.

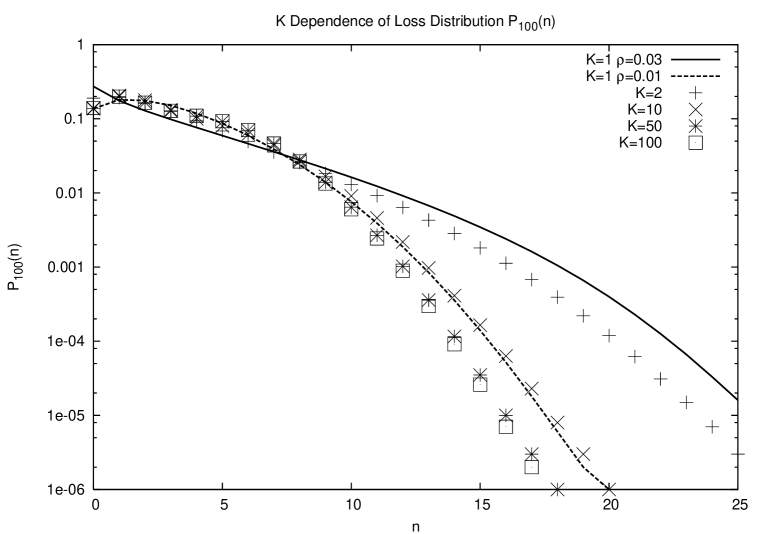

Figure 15 shows the semi-log plot of the default probability for . We set the model parameters as , , and . The solid curve plots the data for and and the dotted line shows the data for and . As increases, the data for each departs from the solid line. At , the data almost shrinks on the dotted line ( and ). The data for almost coincide with those of , whose is given by the superposition of the two binomial distributions. This point is also a drawback of the present model. If the glueing process works perfectly, these data should coincide with the homogeneous portfolio case and . However, this discrepancy is inherent property of the model. Contrary to the discrepancy in the two-sector case, the conditions on the conditional default probabilities are different from those of the homogeneous portfolio. They could cause the difference in .

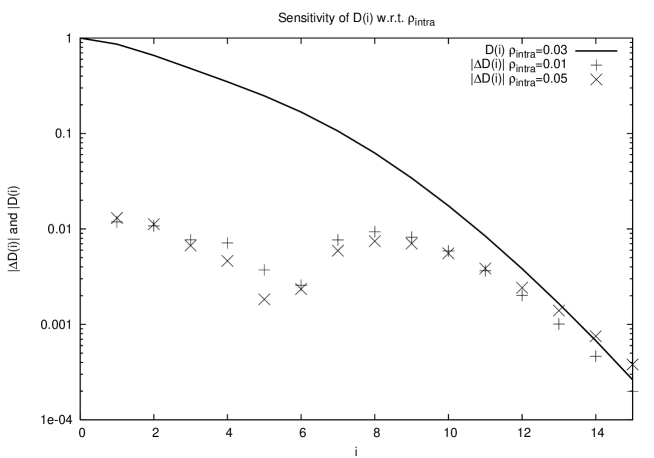

From the above discussions on with different , we think that the inter-sector default correlation is more important than the intra-sector default correlation in cases of a large . In the case, the are roughly given by those of the homogeneous portfolio with . If one estimates the implied values of and from the premium (or ) of the portfolio with large , this point is crucial. In Figure 16, we show for between and . We set the model parameters as in the previous figure. For comparison, we also plot for . represents the expected loss rate of the -th tranche, the magnitude of is important when one estimates the implied default correlation from the premium of the tranche. We see that with small is small as compared with . If we change from , does not change significantly. It is difficult to obtain the implied values of from the premium of the tranche with lower seniority. In contrast with medium values of , the magnitudes of and are almost comparable. is sensitive to the change in and it is not difficult to derive the implied value of .

4 Implied Default Correlation

In the last section, as a concrete example, we try to estimate the implied values of the default correlation from the premium of a synthetic CDO. We treat iTraxx-CJ (Series 2), which is an equally weighted portfolio of 50 CDSs on Japanese companies. The standard attachment points and detachment points are ,,, and . Table 1 shows quotes on July 5,2005. The quote for the transhe shows the upfront payment (as a percent of principal) that must be paid in addition to 300 basis points per year. The other quotes for the other tranches are the annual payment rates in basis points per year. The index indicates the cost of entering into a CDS on all 50 companies underlying the index. The recovery rate is .

| Index | ||||||

|---|---|---|---|---|---|---|

| 5-year Quotes | 15.75 | 113.25 | 42.0 | 30.5 | 15.5 | 24.55 |

In order to get the implied default correlation for each tranche, it is necessary to relate the loss distribution function to the premiums. The premiums are the present value of the expected cash flows. The calculation of this present value involves three terms [29]. We denote by the remaining notional for the tranche after defaults. It is given as

| (75) |

Here, means the smallest integer greater than . For simplicity, we treat the 5-year as one period. The three terms are written as

| (76) |

where is the risk-free rate of interest and we set . By considering the total value of the contract, one can see that the break even spread is given as .

For the index, and and it is possible to estimate the average default probability . Instead, we use the CDS data for each company and estimate the average default probability and its dispersion as

With these parameters, the tranche correlations can be implied from the spreads quoted in the market for particular tranches. These correlations are known as tranche correlations or compound correlations. As a pricing model, we use MCB, BBD and Gaussian copula models. For MCB, we use the following candidates.

-

•

Original MCB model (MCB1). and .

-

•

Short tail MCB model (MCB2). and .

-

•

Short tail MCB model (MCB3). and .

-

•

Disordered MCB model (MCB4). ,, and . MCB model with inhomogeneous default probability.

-

•

Two-sector MCB model (MCB5). , and . Assets are categorized in sectors and .

| Tranches | MCB 1 | MCB 2 | MCB 3 | MCB 4 | MCB5 | BBD | Gaussian |

|---|---|---|---|---|---|---|---|

| 11.79 | 10.8 | 9.96 | 12.88 | 21.2 | 11.4 | 13.8 | |

| 1.27 | 1.18 | 1.13 | 1.36 | 2.45 | 1.26 | 1.35 | |

| 3.16 | 3.08 | 3.09 | 3.46 | 6.32 | 3.15 | 3.23 | |

| 6.16 | 5.95 | 5.90 | 6.65 | 12.15 | 6.11 | 6.31 | |

| 9.78 | 9.67 | 9.90 | 10.67 | 19.97 | 9.73 | 9.46 |

Table 2 shows implied tranche correlations for the 5-year quotes in Table 1. We see a “Correlation Smile”, which is a typical behavior of implied correlations across portfolio tranches [13].

We also find that the implied correlations are different among the models. For MCB, models with a larger have a smaller correlation skew. The correlation for decreases with and other correlations do not change significantly. If a probabilistic model describe the true default distribution, there should not exist any correlation skew. As a model approaches the true distribution, we can expect that the skew decreases. MCB3 is more faithful to the true default distribution. The skew of BBD is between MCB 1 and MCB 2, which is reasonable because the profile of BBD is between MCB1 and MCB2 ( see figure 5). Gaussian copula’s skew range is larger than MCB 1, MCB 2, MCB 3 and BBD.

About the effect of , the implied correlations are considerably different between (MCB 4) and (MCB 2). In the estimation of the implied correlation, we cannot neglect the fluctuation . In particular, for the tranches , the implied value is affected greatly by . As has been discussed in [5], the increase in the dispersion of the default probability increases the loss in the equity tranche. It is necessary to increase the implied correlation to match with the market quote.

In the case (MCB5), the correlation level and correlation skew are very large. This means that if assets are categorized in many sectors and inter-sector correlation is very weak, the loss distribution accumulates around the origin . In order to match with the market quote, a large intra-sector correlation is necessary.

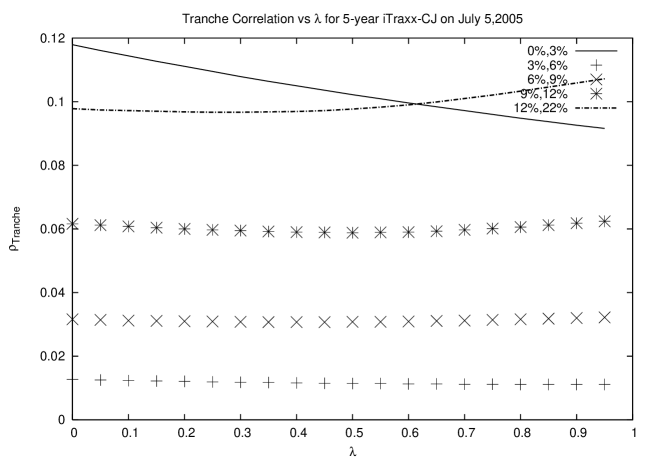

For the estimation of the model parameter , we think that the resulting loss distribution should look closer to the implied loss distribution. That is, the range of tranche correlation skew should be small. Figure 17 shows the tranche correlation vs . As we increase , the skew range becomes small. At , the range becomes minimal. We should calibrate to be .

5 Concluding Remarks

In this paper, we generalize Moody’s correlated binomial default distribution to the inhomogeneous portfolio cases. As the inhomogeneity, we consider the non-uniformity in the default probability and in the default correlation and . To treat the former case, we construct a coupled MCB model and obtain the default probability function . The inhomogeneity in causes changes in the expected loss rates of the tranches with lower seniority.

In order to treat the inhomogeneity in the default correlation, we construct a multi-sector MCB model by glueing multiple MCB models by an auxiliary random variable . We cannot take out the joining lines between the MCB models, for small portfolio and small , the construction works well. For the inhomogeneity in , we divide a homogeneous portfolio into sectors. We set and see the effect of the increase in on . As the sector number increases, the inter-sector correlation becomes more important than the intra-sector default correlation . With large , the default correlation is governed by only. The CDOs, whose assets are categorized in many sectors, should be treated more carefully than .

In order to check the validity of the MCB model and our generalization method, more careful treatment and calibration should be done. We assume that decays exponentially with . With such a modification, the skew of the correlations diminishes, however, the skew remains significantly. Other models for should be considered. For this purpose, it is necessary to study the implied loss distribution directly. Recently, Hull and White [28, 29] developed a method to derive the implied loss distribution and to obtain the implied copula function from the market quotes of CDOs. The authors proposed a calibration method for from the implied loss function [24]. By incorporating this information in the MCB model’s framework, we may have a “Perfect” correlated binomial default distribution model which reflects market quotes completely. We think that our generalization method provides important information based directly on the market quotes.

6 Acknowledgement

This research was partially supported by the Ministry of Education, Science, Sports and Culture, Grant-in-Aid for Challenging Exploratory Research ,21654054, 2009.

References

References

- [1] Fabozzi, F. J. and L. S. Goodman, 2001 Investing in Collateralized Debt Obligations, U.S. John Wiley & Sons.

- [2] Schönbucher, P. ,2003,Credit Derivatives Pricing Models : Model, Pricing and Implementation , U.S. John Wiley & Sons.

- [3] Duffie, D. and K.J.Singleton, 2003, Credit Risk-Pricing, Measurement and Management (Princeton : Princeton University Press).

- [4] Hull, J., M. Predescu and A. White, 2005, The Valuation of Correlation-Dependent Credit Derivatives Using a Structural Model, Working Paper, University of Toronto.

- [5] Finger, C. C., 2005,Issues in the Pricing of Synthetic CDOs, Journal of Credit Risk, 1(1).

- [6] Cifuettes, A. and G. O’Connor, 1996, The Binomial Expansion Method Applied to CBO/CLO Analysis, Working Paper (Moody’s Investors Service).

- [7] Martin, R. , Thompson, K. and C. Browne, 2001,How dependent are defaults, Risk Magazine,14(7) 87-90.

- [8] Finger, C. C., 2000,A Comparison of stochastic default rate models, Working Paper (The RiskMetrics Group).

- [9] Duffie, D. and N. Gârleau, 2001,Risk and the Valuation of Collateralized Debt Obligation, Financial Analyst Journal 57(1) 41-59.

- [10] Li, D. ,2000,On Default Correlation: a Copula Approach, The Journal of Fixed Income 9(4) 43.

- [11] Vasicek, O.,1987,Probability of Loss on Loan Portfolio , Working Paper (KMV Corporation).

- [12] Schönbucher, P. and D. Schubert, 2001,Copula Dependent Default Risk in Intensity Models, Working paper (Bonn University).

- [13] Andersen, L., J.Sidenius and S.Basu, 2003, All your Hedges in one Basket,RISK, 67-72.

- [14] Davis, M. and V. Lo ,Infectious defaults, Quantitative Finance, 1, 382-387.

- [15] Zhou, C. , 2001, An analysis of default correlation and multiple defaults, Review of Financial Studies 4,555-576.

- [16] Laurent J-P. and J. Gregory, 2003, Basket Default Swaps, CDO’s and Factor Copulas, Journal of Risk7(4),103-122.

- [17] CREDIT-SUISSE-FINANCIAL-PRODUCTS, 1997, CreditRisk+ a Credit Risk Management Framework, Technical Document.

- [18] Frey, R. , Mcneil, A. and M. Nyfeler, 2001, Copulas and Credit Models, Risk, October, 111-113.

- [19] Frey, R. and A. McNeil, 2002,VaR and Expected Shortfall in Portfolios of Dependent Credit Risks: Conceptual and Practical Insights, Journal of Banking and Finance, 1317-1344.

- [20] Witt, G. ,2004, Moody’s Correlated Binomial Default Distribution, Working Paper (Moody’s Investors Service) August 10.

- [21] Molins, J. and E.Vives, 2004,Long range Ising Model for credit risk modeling in homogeneous portfolios, Preprint arXiv:cond-mat/0401378.

- [22] Kitsukawa, K., Mori, S. and M. Hisakado,2006,Evaluation of Tranche in Securitization and Long-range Ising Model, Physica A 368 191-206.

- [23] Hisakado, M, Kitsukawa, K. and S. Mori ,2006,Correlated Binomial Models and Correlation Structures, J.Phys. A39 15365.

- [24] Mori, S, Kitsukawa, K. and M. Hisakado, 2008, Correlation Structures of Correlated Binomial Models and Implied Default Distribution, J.Phys.Soc.Jpn 77,vol.11,114802-114808.

- [25] Standard & Poor’s CreditPro 7.00, 2005.

- [26] Lucas, D., J, 1995, Default Correlation and Credit Analysis, Journal of Fixed Income, March, 76.

- [27] Jobst, N. J. and A. de Servigny, 2005,An Empirical Analysis of Equity Default Swaps (II): Multivariate insights, Working Paper (S&P).

- [28] Hull, J. and A. White, 2005,The Perfect Copula, Working Paper,(University of Toronto).

- [29] Hull, J. and A. White, 2006,Valuing Credit Derivatives Using an Implied Copula Approach, Working Paper (University of Toronto).