Delta Hedged Option Valuation with Underlying Non-Gaussian Returns

Abstract

The standard Black-Scholes theory of option pricing is extended to cope with underlying return fluctuations described by general probability distributions. A Langevin process and its related Fokker-Planck equation are devised to model the market stochastic dynamics, allowing us to write and formally solve the generalized Black-Scholes equation implied by dynamical hedging. A systematic expansion around a non-perturbative starting point is then implemented, recovering the Matacz’s conjectured option pricing expression. We perform an application of our formalism to the real stock market and find clear evidence that while past financial time series can be used to evaluate option prices before the expiry date with reasonable accuracy, the stochastic character of volatility is an essential ingredient that should necessarily be taken into account in analytical option price modeling.

pacs:

89.65.Gh, 05.10.GgThere has been a great interest in the study of the stochastic dynamics of financial markets through ideas and techniques borrowed from the statistical physics context. A set of well-established phenomenological results, universally valid across global markets, yields the motivating ground for the search of relevant models bouch-pott ; mant-stan ; voit .

A flurry of activity, in particular, has been related to the problem of option price valuation. Options are contracts which assure to its owner the right to negotiate (i.e, to sell or to buy) for an agreed value, an arbitrary financial asset (stocks of some company, for instance) at a future date. The writer of the option contract, on the other hand, is assumed to comply with the option owner’s decision on the expiry date. Options are a crucial element in the modern markets, since they can be used, as convincingly shown by Black and Scholes bs , to reduce portfolio risk.

The Black-Scholes theory of option pricing is a closed analytical formulation where risk vanishes via the procedure of dynamical (also called “delta”) hedging, applied to what one might call “log-normal efficient markets”. Real markets, however, exhibit strong deviations of log-normality in the statistical fluctuations of stock index returns, and are only approximately efficient.

Our aim in this letter is to introduce a theoretical framework for option pricing which is general enough to account for important features of real markets. We also perform empirical tests, taking the London market as the arena where theory and facts can be compared. More concretely, we report in this work observational results concerning options of european style, based on the FTSE 100 index, denoted from now on as ft .

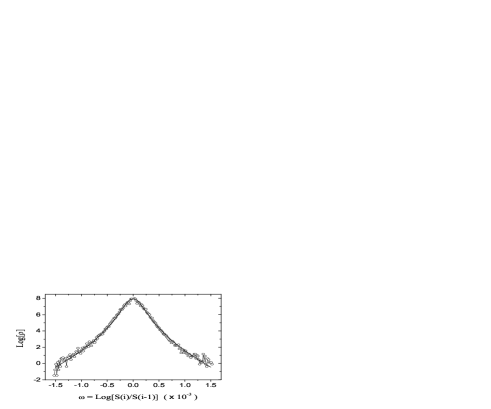

To start with, we note, in fact, that the returns of the FTSE 100 index do not follow log-normal statistics for small time horizons. We have considered a financial time series of 242993 minutes (roughly, two years) ending on 17th november, 2005. The probability distribution function (pdf) of the returns given by , taken at one minute intervals is shown in Fig.1. We verify that the Student t-distribution with three degrees of freedom conjectured by Borland borland provides a good fit to the data. A slightly better fitting is produced if a smooth gaussian envelope is introduced to truncate the distribution at the far tails, viz:

| (1) |

A time-dependent family of self-similar Tsallis distributions comment1 , , with variance , was previously considered in option price modeling borland . The time parameter refers here to the time horizon of return fluctuations, while is indicated from empirical pdfs. Even though suggestive results were found by Borland for a set of option prices taken from the real market, the time dependence of the variance disagrees with observations. It is well-established that the variance of return fluctuations grows linearly with the time horizon within a certain range of days, and that the return pdfs are not self-similar (there is a crossover to the log-normal profile). A further difficulty has to do with the matching between the theoretical and observed volatilities. As reported in Ref. borland , for instance, the model volatility needed to reproduce the volatility smiles of options based on the SP500 futures in june 2001 is set to . However, as the analysis of the SP500 futures time series reveals, the actual volatility for that period was considerably smaller, close to comment2 .

The essential reason for the specific choice of in the above pdf is that it is related to a formerly known Langevin equation, which leads, on its turn, to a partial differential equation for option prices. An alternative and more general point of view – to be pursued here – is not to advance, a priori, any hypothesis on the form of the return pdfs, while still dealing with a Langevin description of return fluctuations.

Le us assume, therefore, that at time the underlying index is and that its subsequent values are given by

| (2) |

where is a dynamic random variable described, at time , by an arbitrary pdf . We take at . Observe that it is a simple exercise to write, from Eq. (2), the formal expression for the pdf of returns with time horizon , in a statistically stationary regime.

As an inverse problem, we are now interested to find a function , so that be derived from the Langevin equation

| (3) |

where is a random gaussian field, defined by and . Actually, it is not difficult to compute as a functional of . We just write down the Fokker-Planck equation that is satisfied by borland2 ,

| (4) |

to obtain, from the direct integration of (4),

| (5) |

The function is an important element in the option pricing problem, within the dynamical hedging strategy of investment. Considering the writer of an option contract who owns a number of the underlying asset, dynamical hedging, a concept firstly introduced by Black and Scholes, consists of defining option prices as a function of the asset’s value and time , so that , and the “minimal” portfolio is imposed to evolve according to the market risk-free interest rate , as if were converted to cash and safely deposited into an interest earning bank account. Under these conditions, a straightfoward application of Ito’s lemma leads to the generalized Black-Scholes equation,

| (6) |

Exact solutions of this equation may be given in terms of statistical averages. For the case of call options which expire at time , we get

| (7) |

where is a random variable described by some pdf , with being the option’s time to expire. One may check, by direct substitution, that (7) solves, in fact, Eq. (6). The put-call parity relation is also satisfied by our solution, as any bona fide option pricing formula should do. It is worth noting that the case where is constant corresponds to the standard Black-Scholes problem.

In order to develop analytical expressions for , let be the characteristic function associated to the distribution . We may write, without loss of generality, , where . It is clear that and can be computed, in principle, with the help of the cumulant expansion. However, a non-perturbative analysis may be readily addressed when one realizes that is nothing but the characteristic funtion of . The remaining problem, then, is to evaluate the corrections due to and (they are in fact small in realistic cases). Up to first order in , we have and . Using (5), we get . Taking now, as a phenomenological input, that the volatility depends linearly on the time horizon , we write , which implies that

| (8) |

It is not difficult to verify that the above expression is exact when , and leads to an option pricing formula previously proposed by Matacz matacz , which was based on heuristic arguments. However, the usefulness of the approximation given by Eq. (8) is restricted to the cases where the far tails of decay faster than , because of the exponential factor in Eq. (7).

| Strike | 02dec05 | 06dec05 | 09dec05 | |||

| Price | MKT | EP | MKT | EP | MKT | EP |

| 410.5 | NA | X | NA | X | ||

| 50 | 53.5 | |||||

| 13 | 12.5 | |||||

| 2.5 | 2 | |||||

| 0.5 | – | – | ||||

| NA | X | – | 0.0 | – | 0.0 | |

| Strike | 19dec05 | 03jan06 | 12jan06 | |||

| Price | MKT | EP | MKT | EP | MKT | EP |

| 329.5 | NA | X | NA | X | ||

| 28.5 | 93 | |||||

| 8 | 34.5 | |||||

| 2.5 | 9 | |||||

| 0.5 | 2 | 0.5 | ||||

| NA | X | 0.5 | [0.0] | – | 0.0 | |

In a more empirically oriented approach, we may attempt to compute , as defined by Eq. (7), from real or Monte Carlo simulated financial time series, without having any information on the pdf . Since we would not be entitled to use Eq. (5) anymore, it is necessary to rewrite the expression that appears in the definition of in terms of known quantities. Observing that Ito’s lemma yields, from Eq. (3),

| (9) |

we write, for a time series of temporal length ,

| (10) |

where . Substituting (10) into (7), we find, then, a pragmatical formula to work with numerical samples.

A stochastic process was generated from a high-frequency time series of the logarithms of FTSE 100 index, , consisting of 242990 minutes ending on 17th november, 2005 (it is essentially the same data used to establish the histogram depicted in Fig.1). The series was partitioned into 94 pieces of 2585 minutes each (roughly one financial week). In each one of these pieces, the market drift parameter was determined by the least squares method. Then, according to Eq. (2), we define . We have found that improved results are obtained if extremely intense fluctuations are removed from the series, since they are likely to correspond to the market’s reaction to unexpected events (we have checked this assumption in a number of cases). Once the standard deviation for the whole series is , we removed from the series the fluctuations given by (only 144 elements were taken out from the series). A sequence of 3000 samples, separated in time by one hour translations, was used in each option price evaluation. It turns out that the samples are related to a period of reasonably well-behaved volatility (it fluctuates around some stable value). We also introduce a phenomenological factor , so that trials with series of different mean volatilities are obtained in a simple way from the mapping .

We have computed in this way option premiums based on the London FTSE 100 index (with 1 minute). The results are shown in Tables I and II, where market (MKT) and evaluated prices (EP) are compared. In the tables, NA stands for “not available” data, while X stands for prices we did not evaluate; the values between brackets correspond to instances where the time series extension was not large enough to get accurate predictions. The daily closing values of the FTSE 100 index, , the -factors, and the model and observed mean volatilities ( and , respectively) are reported in the table captions. The numerical errors in the EP columns vary typically from for the larger premiums to for the smaller ones. When comparing the market and numerical results, one should keep in mind the existence of the usual bid-ask spread of option prices.

| Strike | 02dec05 | 06dec05 | 09dec05 | |||

| Price | BS | ST | BS | ST | BS | ST |

| 409.38 | X | X | X | X | ||

| 31.15 | 36.76 | |||||

| 2.55 | 3.51 | |||||

| 0.04 | 0.07 | |||||

| 0.0 | 0.0 | 0.0 | ||||

| X | X | 0.0 | 0.0 | 0.0 | 0.0 | |

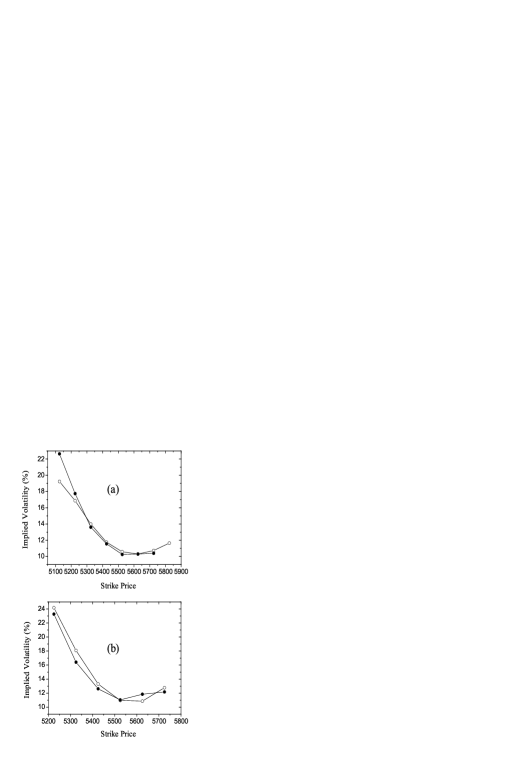

As clearly shown in Fig. 2, we have been able to model volatility smiles which are in good agreement with the market ones. The remarkable feature of these results is that implied volatilities can be obtained from a single model volatility, , which is in fact close to the actual observed market volatility .

We have, along similar lines, evaluated option prices through Monte Carlo simulations. The stochastic process is now generated as independent events from the Student t-distribution with three-degrees of freedom. As shown in Table III, the Black-Scholes (BS) and Student t-distribution-based evaluations (ST) yield relatively close (and not good) answers for option prices. It is important to note the numerical results do not differ too much if Matacz’s analytical option price formula is used with convolutions of the truncated Student t-distribution, Eq. (1), once the log-normal return pdf cores get large enough for time horizons of a few days.

To summarize, we have provided strong evidence, from the empirical analysis of non-gaussian market data, that the combination of delta-hedging strategy and suitable Langevin modeling allows one to compute option premiums with reasonable confidence, from the use of Eqs. (7) and (10). On the other hand, we have found that both the Monte Carlo simulations and the delta-hedging analytical framework based on fat-tailed distributions and time-independent volatilities which are close to the observed averaged values, fail to predict real market option prices. Our results point out that efficient option pricing analytical tools have necessarily to deal with the stochastic nature of volatility fluctuations, a main distinctive aspect of financial time series.

The author thanks Marco Moriconi for a critical reading of the manuscript. This work has been partially supported by FAPERJ.

References

- (1) J.-P. Bouchaud and M. Potters, Theory of Financial Risks - From Statistical Physics to Risk Management, Cambridge University Press, Cambridge (2000).

- (2) R. Mantegna and H.E. Stanley, An Introduction to Econophysics, Cambridge University Press, Cambridge (2000).

- (3) J. Voit, The Statistical Mechanics of Financial Markets, Springer-Verlag (2003).

- (4) F. Black and M. Scholes, J. Polit. Econ. 81, 637 (1973).

- (5) Option premiums based on FTSE 100 index are daily published by the Financial Times at www.ft.com.

- (6) L. Borland, Phys. Rev. Lett. 89, 098701 (2002).

- (7) A distribution is called self-similar if there is, for any , a time-dependent function so that .

- (8) We refer, throughout the paper, to annualized volatilities, computed from the standard deviation of one-minute returns, , as , where we assume 252 trading days per year, and 8.5 market hours per day.

- (9) L. Borland, Phys. Rev. E 57, 6634 (1998).

- (10) A. Matacz, Int. J. Theor. Appl. Finance 3, 143 (2000).