Optimal Investment Horizons for Stocks and Markets

Abstract

The inverse statistics is the distribution of waiting times needed to achieve a predefined level of return obtained from (detrended) historic asset prices [1, 2]. Such a distribution typically goes through a maximum at a time coined the optimal investment horizon, , which defines the most likely waiting time for obtaining a given return . By considering equal positive and negative levels of return, we reported in [2] on a quantitative gain/loss asymmetry most pronounced for short horizons. In the present paper, the inverse statistics for 2/3 of the individual stocks presently in the DJIA is investigated. We show that this gain/loss asymmetry established for the DJIA surprisingly is not present in the time series of the individual stocks nor their average. This observation points towards some kind of collective movement of the stocks of the index (synchronization).

keywords:

Econophysics , Fractional Statistics , Statistical PhysicsPACS:

05.30.P , 89.65.GWhat drives prices? This question has been studied for centuries with quantitative theories dating back at least to Bachelier [3], who proposed the random walk hypothesis for price trajectories. In order to qualify different pricing models etc., the financial industry has performed many statistical studies establishing a number of stylized facts as well as benchmarking for the performance of various financial instruments with respect to investment returns and in its complement, risk taking. Due to this focus on returns and risk, most financial studies essentially amount to measuring two-point correlations in one way or another, most commonly by studying the distribution of returns calculated over some pre-defined fixed time period [4].

In recent publications [1, 2], the present authors have proposed to “invert” the standard return-distribution problem and instead study the probability distribution of waiting times needed to reach a fixed level of return for the first time. This is in the literature known as the first passage time-problem and the solution is known analytically for a Brownian motion as the inverse gamma (Levy) distribution , (with ), where one for large (waiting) times recovers the well-known first return probability for a random walk .

Historical financial time series such as the DJIA, SP500 and Nasdaq possess an often close to exponential positive drift over the time scales of decades due to the overall growth of the economy modulated with times of recession, wars etc. Hence, one can obviously not compare directly the empirical probability distribution for positive and negative levels of return. As the focus of the present paper will be on such a comparison, we must ideally eliminate the effect of this drift. We have chosen to remove the drift based on the use of wavelets, which has the advantages of being non-parametric and hence does not depend on certain economic assumptions. This technique has been described in detail elsewhere [1] and for the present purpose, it suffices to say that this wavelet technique enables a separation of the original time series into a short scale (detrended) time series and a (long time-scale) drift term so that . Based on for some historical time period of the DJIA, the empirical investment horizon distributions, , needed to obtain a pre-defined return level for the first time can easily be calculated for different ’s. As is stationary over time scales beyond that of the applied wavelet (for a time larger than say 1000 days) it is straightforward to compare positive and negative levels of return.

As the empirical logarithmic stock price process is known not to be Brownian, we have suggested to use a generalized (shifted) inverse gamma distribution

| (1) |

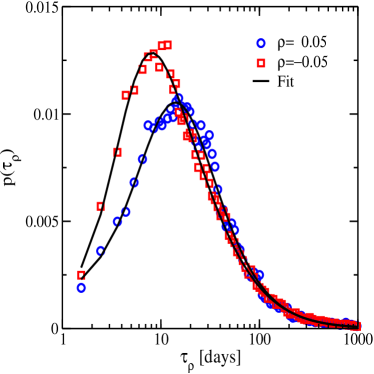

where the reasons behind are purely technical and depends on short-scale drift due to the fact that we are using the daily close. The results so far have been very encouraging with respect to excellent parametrization of the empirical probability distributions for three major stock markets, namely DJIA, SP500 and Nasdaq; cf. Fig. 1(a), for a example using the DJIA and ref. [5] for the others. The choice of is such that it is sufficiently large to be above the “noise level”, quantified by the historical volatility and sufficiently small to occur quite frequently in order to obtain reasonable statistics. For all three indices, the tail-exponent of the distributions parameterized by Eq. (1) are indistinguishable from the “random walk value” of , which is not very surprising. What is both surprising and very interesting is that these three major US stock markets (DJIA, SP500 and Nasdaq) exhibit a very distinct gain/loss asymmetry, i.e., the distributions are not invariant to a change of sign in the return . Furthermore, this gain/loss asymmetry quantified by the optimal investment horizon defined as the peak position of the distributions has for at least the DJIA a surprisingly simple asymptotically power law like relationship with the return level , see [2] for more details.

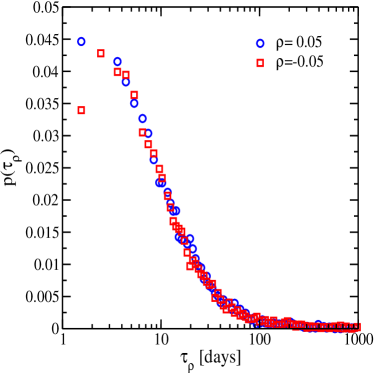

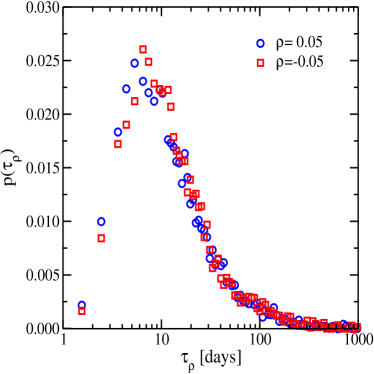

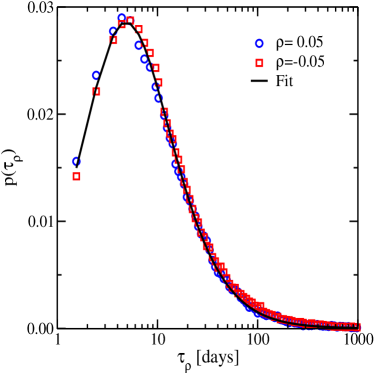

In order to further investigate the origin of the gain/loss asymmetry in DJIA, we simply compare the gain and loss distributions of the DJIA with the corresponding distributions for a single stocks in the DJIA as well as their average. An obvious problem with this approach is that the stocks in the DJIA changes with time and hence an exact correspondence between the DJIA and the single stocks in the DJIA is impossible to obtain if one at the same time wants good statistics. This is the trade-off, where we have put the emphasis on good statistics. The 21 company stocks analyzed and presently in the DJIA (by the change of April 2004) are listed in Table 1 together with their date of entry as well as the time period of the data set analyzed. In Figs. 1(c) and (c) we show the waiting time distributions for 2 companies in the DJIA, which are representative for the distributions obtained for all the companies listed in Table 1. We see that, for a return level , the value of the optimal investment horizon, i.e. the position of the peak in the distribution, ranges from around 2 days to around 10 days depending on the company. More importantly, it is clear from just looking at the figures that, within the statistical precision of the data, the distributions are the same for both positive and negative values of . In order to further quantify this invariance with respect to the sign of , we have averaged the (company) gain and loss distributions separately in order to obtain an average behavior for the stocks listed in Table 1. The result of this averaging process (Fig. 1(d)) is nothing less that an almost perfect agreement between the gain and loss distributions with a peak position around 5 days for both distributions. This means that the optimal investment horizon for the average of these selected individual stocks is approximately half that of the loss distribution for the DJIA and approximately one fourth of that for the gain distribution. In other words, it is twice as slow to move the DJIA down and four times as slow to move the DJIA up compared to the average time to move one of its stocks up or down. That market losses in general are faster than gains must also be attributed to human psychology; people are in general much more risk adverse than risk taking.

How can we rationalize the results we have obtained? In essence, what we have done is to interchange the operations of averaging over the stocks in the DJIA and calculating the inverse statistics for the stocks of this index. Since the DJIA is constructed such that it covers all sectors of the economy under the assumption that this areas are to some degree independent, it seems quite reasonable to assume that a gain/loss in the shares of say Boeing Airways has nothing economically fundamental to do with a corresponding gain/loss in the shares of the Coca-Cola Company especially since the data are detrended. Since the two operations do not even approximately commute, this means that significant inter-stock correlations must exist even for a rather modest return level .

There are several possible scenarios which may explain the observed behavior, but they all amount to more or less the same thing. A down/up-turn in the DJIA may be initiated by a down/up-turn in some particular stock in some particular economical sector. This is followed by a down/up-turn in economically related stocks and so forth. The result is a cascade, or synchronization, of consecutive down/up-turns in all the sectors covered by the DJIA and hence in the DJIA itself. The initiation of this may be some more general new piece of information, which is considered more crucial for one sector than others, but as argued for in length in [6] it may also happen for no obvious reason what so ever. An (rational) example would be that Intel drops significantly due to bad quarterly earnings in turn, by a cascade process, affecting the stock price of IBM and MicroSoft and so forth. As the index, at least from a physicist’s point of view, can be compared to an external “field”, movements in the index due to a single or a few stocks can rapidly spread through most or all sectors, if psychology in general and specifically feed-back loops are important. The observed asymmetry then means that the “field” is not isotropic.

References

- [1] I. Simonsen, M. H. Jensen and A. Johansen, Eur. Phys. J. 27 (2002) 583.

- [2] M. H. Jensen, A. Johansen and I. Simonsen, Physica A 234 (2003) 338.

- [3] L. Bachelier, Théorie de la Spéculation”, 1900, Annales de l’Ecole normale superiure.

- [4] J.-P. Bouchaud and M. Potters, Theory of Financial Risks: From Statistical Physics to Risk Management (Cambridge University Press, Cambridge, 2000).

- [5] A.Johansen, I.Simonsen and M.H.Jensen, Inverse Statistics for Stocks and Markets, preprint submitted to Quantitative Finance, see also http://xyz.lanl.gov/physics/0511091

- [6] R. J. Schiller, Irrational Exuberance, Princeton University Press, 2000

| Company | Entering date | Data period |

|---|---|---|

| Alcoa⋆ | Apr 22, 1959 | 1962.1–1999.8 |

| American Express Company | Aug 30, 1982 | 1977.2–1999.8 |

| ATT† | Mar 14, 1939 | 1984.1–1999.8 |

| Boeing Airways | Jul 08, 1986 | 1962.1–1999.8 |

| Citicorp∙ | Mar 17, 1997 | 1977.0–1999.8 |

| Coca-Cola Company | Mar 12, 1987 | 1970.0–1999.8 |

| DuPont | Nov 20, 1935 | 1962.1–1999.8 |

| Exxon & Mobil∘ | Oct 01, 1928 | 1970.0–1999.8 |

| General Electric | Nov 07, 1907 | 1970.0–1999.8 |

| General Motors | Mar 16, 1915 | 1970.0–1999.8 |

| Goodyear | July 18 1930 | 1970.1–1999.8 |

| Hewlett & Packard | Mar 17, 1997 | 1977.0–1999.8 |

| IBM | Jun 29, 1979 | 1962.0–1999.8 |

| Intel | Nov 01, 1999 | 1986.5–1999.8 |

| International Paper | Jul 03, 1956 | 1970.1–1999.8 |

| Eastman Kodak Company | Jul 18, 1930 | 1962.0–1999.8 |

| McDonald’s Cooperation | Oct 30, 1985 | 1970.1–1999.8 |

| Merck & Company | Jun 29, 1979 | 1970.0–1999.8 |

| Procter & Gamble | May 26, 1932 | 1970.0–1999.8 |

| The Walt Disney Co. | May 06, 1991 | 1962.0–1999.8 |

| Wall Mart | Mar 17, 1997 | 1972.7–1999.8 |