Transfer Entropy Analysis of the Stock Market

Abstract

In terms of transfer entropy, we investigate the strength and the direction of information transfer in the US stock market. Through the directionality of the information transfer, the more influential company between the correlated ones can be found and also the market leading companies are selected. Our entropy analysis shows that the companies related with energy industries such as oil, gas, and electricity influence the whole market.

keywords:

Transfer Entropy , Information Flow , Econophysics, Stock MarketPACS:

05.20.Gg , 89.65.Gh , 89.70.+c, , ,

1 Introduction

Recently, economy has become an active research area for physicists. They have investigated stock markets using statistical tools, such as the correlation function, multifractal, spin-glass models, and complex networks [1, 2, 3, 4, 5, 6]. As a consequence, it is now found evident that the interaction therein is highly nonlinear, unstable, and long-ranged.

All those companies in the stock market are interconnected and correlated, and their interactions are regarded as the important internal force of the market. The correlation function is widely used to study the internal inference of the market [7, 8, 9, 10, 11]. However, the correlation function has at least two limitations: First, it measures only linear relations, although a linear model is not a faithful representation of the real interactions in general. Second, all it says is only that two series move together, and not that which affects which: in other words, it lacks directional information. Therefore participants located in hubs are always left open to ambiguity: they can be either the most influential ones or the weakest ones subject to the market trend all along. It should be noted that introducing time-delay can be a good remedy for these limitations. Some authors use such concepts as time-delayed correlation and time-delayed mutual information, and these quantities construct asymmetric matrices by preserving directionality [9, 12]. In case that the length of delay can be appropriately determined, one can also measure the ‘velocity’ whereby the influence spreads. In this paper, however, we rely on a newly-devised variant of information to check its applicability.

Information is an important keyword in analyzing the market or in estimating the stock price of a given company. It is quantified in rigorous mathematical terms [13], and the mutual information, for example, appears as meaningful choice replacing a simple linear correlation even though it still does not specify the direction. The directionality, however, is required to discriminate the more influential one between correlated participants, and can be detected by the transfer entropy (TE) [14].

This concept of TE has been already applied to the analysis of financial time series by Marschinski and Kantz [15]. They calculated the information flow between the Dow Jones and DAX stock indexes and obtained conclusions consistent with empirical observations. While they examined interactions between two huge markets, we may construct its internal structure among all participants.

2 Theoretical Background

Let us consider two processes, and . Transfer entropy [14] from to is defined as follows:

| (1) |

where and represent the states at time of and , respectively.. In terms of relative entropy, it can be rephrased as the distance from the assumption that has no influence on (i.e. ). One may rewrite Eq. (1) as:

| (2) |

from the property of conditional entropy. Then the second equality shows that TE measures the change of entropy rate with knowledge of the process . Eq. (2) is practically useful, since the TE is decomposed into entropy terms and there has been already well developed technique in entropy estimation.

There are two choices in estimating entropy of a given time series. First, the symbolic encoding method divides the range of the given dataset into disjoint intervals and assign one symbol to each interval. The dataset, originally continuous, becomes a discrete symbol sequence. Marschinski and Kantz [15] took this procedure and introduced the concept called effective transfer entropy. The other choice exploits the generalized correlation integral . Prichard and Theiler [16] showed that the following holds for data :

| (3) |

where determines the size of a box in the box-counting algorithm. We define the fraction of data points which lie within of by

| (4) |

where is the Heaviside function, and calculate its numerical value by the help of the box-assisted neighbor search algorithm [17] after embedding the dataset into an appropriate phase space. The generalized correlation integral of order is then given by

| (5) |

Notice that is expressed as an averaged quantity along the trajectory and it implies a kind of ergodicity which converts an ensemble average into a time average, . Temporal correlations are not taken into consideration since the daily data already lacks much of its continuity.

It is rather straightforward to calculate entropy from a discrete dataset using symbolic encoding. But determining the partition remains as a serious problem, which is referred to as the generating partition problem. Even for a two-dimensional deterministic system, the partition lines may exhibit considerably complicated geometry [18, 19] and thus should be set up with all extreme caution [20]. Hence the correlation integral method is often recommended if one wants to handle continuous datasets without over-simplification, and we will take this route. In addition, one has to determine the parameter . In a sense, this parameter plays a role of defining the resolution or the scale of concerns, just as the number of symbols does in the symbolic encoding method.

Before discussing how to set , we remark on the finite sampling effect: Though it is pointed out that the case of does not suffer much from finiteness of the number of data [21], then the positivity of entropy is not guaranteed instead [14]. Thus we choose the conventional Shannon entropy, throughout this paper. There have been works done [22, 23, 24] on correcting entropy estimation. These correction methods, however, can be problematic when calculating TE, since the fluctuations in each term of Eq. (2) are not independent and should not be treated separately [25]. We actually found that a proper selection of is quite crucial, and decided to inactivate the correction terms here.

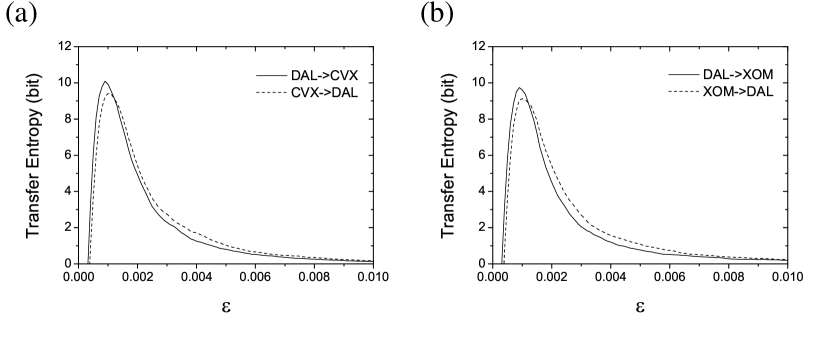

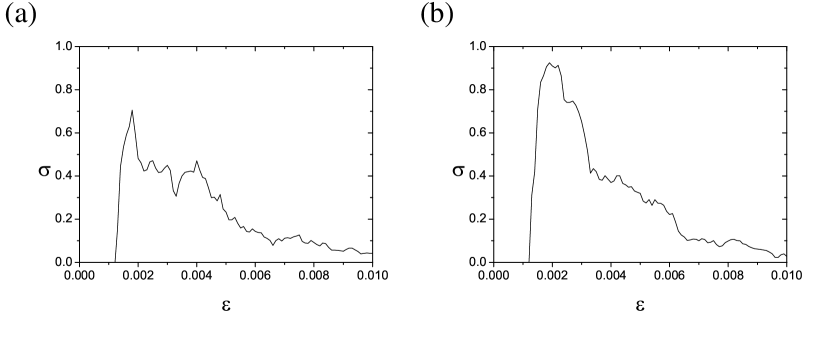

A good value of will discriminate a real effect from zero. Without a priori knowledge, we need to scan the range of in order to find a proper resolution which yields meaningful results from a time series. For reducing the computational time, however, we resort to the empirical observation that an airline company is quite dependent on the oil price while the dependency hardly appears in the opposite direction. Fig. 1 shows this unilateral effect: the major oil companies, Chevron and Exxon Mobile, have influence over Delta Airline. From which maximizes the difference between two directions (Fig. 2), we choose the appropriate scale for analyzing the data. Even in observing the temporal evolution, this value gives good discrimination through the whole period. In Fig. 1, the influence seems reversed on very small length scales. The TE, however, is known to increase monotonically under refinement of the partitions in many cases [25] and the refined partition means the small length scale which is covered by the small in the correlation integral method. Hence we regard this reversal as a finite sample effect in this paper, but it seems worth looking further into the characteristics of TE analysis. And we set in Eq. (1) since other values does not make significant differences.

3 Data Analysis

This study deals with the daily closure prices of 135 stocks listed on New York Stock Exchange (NYSE) from 1983 to 2003 ( trading days, trading day), obtained through the website [26]. We select stocks which is listed on NYSE over the whole periods. The companies in a stock market are usually grouped into business sectors or industry categories, and our data contain 9 business sectors (Basic Materials, Utilities, Healthcare, Services, Consumer Goods, Financial, Industrial Goods, Conglomerates, Technology) and 69 industry categories. The following method shows how the information flows between the groups:

Suppose that we have a time series data , representing the daily closure price of a company at time . A stock market analysis usually prefers treating the log return value:

| (6) |

to the original price itself, since it satisfies the additive property: . This log return transformation also make the result invariant under the arbitrary scaling of the input data. Therefore, in order to measure the information transfer between two companies, say and , we create the log return time series and from the raw price data. Then one can calculate the transfer entropies and between them from the equalities in the Section 2.

For obtaining an overview of the market, we consider groups of similar companies. Let be a company of the group , and be one of the group . The information flow index between these two groups is defined as a simple sum:

| (7) |

In addition, we define the net information flow index to measure the disparity in influences of the two groups as:

| (8) |

If is positive, we can say that the category influences to the category .

We examine the market with two grouping methods. One is business sector, and the other is industry category. Grouping into business sectors, however, does not exhibit clear directionality: the influence of the sector just alternates from that of the sector. In other words, the difference between and over the whole period is almost 0 (zero). This unclarity comes from the fact that a business sector contains so many diverse companies that its directionality just cancels out. On the other hand, if we construct the asset tree through the minimum spanning tree, each business sector forms a subset of the asset tree and the subsets are connected mainly through the hub. Then, it can be said that each of the business sectors forms a cluster [8] and there are no significant direct links among them.

Hence we employ the industry category grouping, more detailed than the business sectors. We have to exclude the categories which contain only one element, and Table 1 lists the remaining industry categories used in the analysis.

As in our previous observation, it is verified again that oil companies and airline companies are related in a unilateral way: The category 20, Major Oil & Gas, has continuing influence over the category 19, Major Airline, during the whole 14 periods under examination () . One can easily find such relations in other categories: for example, the category 20 always influences on the categories 15 (Independent Oil&Gas), 22 (Oil&Gas Equipment&Services), and 23 (Oil&Gas Refining&Marketing). It also affects the category 27 (Regional Airlines) over 13 periods and maintains its power on the whole market during 11 periods (Fig. 3).

It is well-known that economy greatly depends on the energy supply and price such as oil and gas. Transfer entropy analysis quantitatively proves this empirical fact. The top three influential categories (in terms of periods) are the categories 10 (Diversified Utilities), 12 (Electric Utilities) and 20. All of ten companies in the categories 10 and 12 are again related to the energy industry, such as those for holding, energy delivery, generation, transmission, distribution, and supply of electricity.

On the contrary, an airline company is sensitive to the tone of the market. These companies receive information from other categories almost all the time (category 19: 11 periods, category 27: 12 periods). The category 8 (Credit Services) and the category 9 (Diversified Computer Systems, including only HP and IBM in our data) are also market-sensitive as easily expected.

4 Conclusion

We calculated the transfer entropy with the daily data of the US market. The concept of transfer entropy provides a quantitative value of general correlation and the direction of information. Thus it reveals how the information flows among companies or groups of companies, and discriminates the market-leading companies from the market-sensitive ones. As commonly known, the energy such as natural resources and electricity is shown to greatly affect economic activities and the business barometer. This analysis may be applied to predicting the stock price of a company influenced by other ones.

In short, TE proves its possibility as a promising measure to detect directional information. We suggest that the merits and demerits of TE should be judged in details with respect to those of the classical methods like the correlation matrix theory.

References

- [1] W.B. Arthur, S. N. Durlauf, D. A. Lane, The Economy as an Evolving Complex System II, (Perseus Books, 1997)

- [2] R. N. Mantegna, H. E. Stanley, An Introduction to Econophysics, (Cambridge University Press, 2000)

- [3] J.-P. Bouchaud, M. Potters, Theory of Financial Risks (Cambridge University Press, 2000)

- [4] B. B. Mandelbrot, Quant. Finance 1 (2001) 124.

- [5] L. Kullmann, J. Kertész, R.N. Mantegna, Physica A 287 (2000) 412.

- [6] L. Giada, M. Marsili, Physica A 315 (2002) 650.

- [7] R. N. Mantegna, Eur. Phys. J. B, 11 (1999) 193

- [8] J.-P. Onnela, A. Chakraborti, K. Kaski, J. Kertész, A. Kanto, Phys. Rev. E 68 (2003) 056110.

- [9] L. Kullmann, J. Kertész, K. Kaski, Phys. Rev. E 66 (2002) 026125.

- [10] V. Plerou, P. Gopikrishnan, B. Resonow, L.A. Nunes Amaral, H.E. Stanley, Phys. Rev. Lett. 83 (1999) 1471.

- [11] W.-S. Jung, S. Chae, J.-S. Yang, H.-T. Moon, to be published in Physica A, arXiv.org:physics/0504009.

- [12] T. Schreiber, J. Phys. A - Math. Gen. 23 (1990) L393.

- [13] C. E. Shannon, W. Weaver, The Mathematical Theory of Information (University of Illinois Press, 1994).

- [14] T. Schreiber, Phys. Rev. Lett 85 (2000) 461.

- [15] R. Marschinski, H. Kantz, Eur. Phys. J. B 30 (2002) 275.

- [16] D. Prichard, J. Theiler, Physica D 84 (1995) 476.

- [17] H. Kantz, T. Schreiber, Nonlinear Time Series Analysis, (Cambridge University Press, 1997).

- [18] P. Grassberger, H. Kantz, Phys. Lett. A 113 (1985) 235.

- [19] F. Christiansen, A. Politi, Phys. Rev. E 51 (1995) R3811.

- [20] E. M. Bollt, T. Stanford, Y.-C. Lai, K. Zyczkowski, Phys. Rev. Lett. 85 (2000) 3524.

- [21] P. Grassberger, I. Procaccia, Physica D, 9 (1983) 189.

- [22] P. Grassberger, Phys. Lett. A 128 (1988) 369.

- [23] H. Herzel, A. O. Schmitt, W. Ebeling, Chaos Soliton. Fract. 4 (1994) 97.

- [24] M. S. Roulston, Physica D 125 (1999) 285.

- [25] A. Kaiser, T. Schreiber, Physica D 166 (2002) 43.

- [26] http://finance.yahoo.com

| # | industry category |

|---|---|

| 1 | Aerospace/Defense |

| 2 | Auto Manufacturers |

| 3 | Beverages |

| 4 | Business Equipment |

| 5 | Chemicals |

| 6 | Communication Equipment |

| 7 | Conglomerates |

| 8 | Credit Services |

| 9 | Diversified Computer Systems |

| 10 | Diversified Utilities |

| 11 | Drug Manufacturers |

| 12 | Electric Utilities |

| 13 | Farm&Construction Machinery |

| 14 | Health Care Plans |

| 15 | Independent Oil&Gas |

| 16 | Industrial Metals&Minerals |

| 17 | Information Technology Services |

| 18 | Lumber, Wood Production |

| 19 | Major Airlines |

| 20 | Major Oil&Gas |

| 21 | Medical Instruments&Supplies |

| 22 | Oil&Gas Equipment&Services |

| 23 | Oil&Gas Refining&Marketing |

| 24 | Personal Products |

| 25 | Processing Systems&Products |

| 26 | Railroads |

| 27 | Regional Airlines |

| 28 | Specialty Chemicals |

| 29 | Etc. |