Application of Zhangs Square Root Law and Herding to Financial Markets

Abstract

We apply an asymmetric version of Kirman’s herding model to volatile financial markets. In the relation between returns and agent concentration we use the square root law proposed by Zhang. This can be derived by extending the idea of a critical mean field theory suggested by Plerou et al. We show that this model is equivalent to the so called 3/2-model of stochastic volatility. The description of the unconditional distribution for the absolute returns is in good agreement with the DAX independent whether one uses the square root or a conventional linear relation. Only the statistic of extreme events prefers the former. The description of the autocorrelations are in much better agreement for the square root law. The volatility clusters are described by a scaling law for the distribution of returns conditional to the value at the previous day in good agreement with the data.

keywords:

Econophysics , Financial Market , Volatility , Stochastic ProcessesPACS:

89.90.+n , 02.50.-r , 05.40.+j , 05.45.Tp1 Introduction

Any model for the price or index of a financial market should

account for the following so called stylized facts [1, 2].

(i): The sign of the return cannot be predicted. In most models

this fact is build in by assuming the return proportional to an iid

noise.

(ii): The probability for having an absolute return larger than decays for

large as a power law . The tail index seems to be

universal [3] in the range 3-4. A precise determination of for

dayly returns is hampered

by the impossibility to reach the asymtotic regime in the data. Therefore

one should require a good description of all returns.

(iii): Returns are not independent. They form so called

volatility cluster. A quantitative measure of this effect may be the

distribution of first passage times [4]. In this paper we

use the distribution of the returns conditional to the value of the

previous day.

(iv): Absolute returns are correlated. In the case of high frequency

data a hyperbolic decay of the autocorrelation

indicates a long memory process. For dayly returns it behaves

neither as a power law nor a simple exponential expected from

a Markov process.

To acchieve these properties one can distinguish two schools. The first are

the stochastic volatility models. Here one assumes the return to be an iid

noise multiplied with

a volatility factor , where typically

follows a Markov process. Examples

are the GARCH model [6] and its continuous time version [7].

Other posibilities are the CIR-model [8] or

the 3/2 model [9] discussed in ref [10]. The multifractal

model [11] implements fact (iv) by occurence of many time

scales. Any model for dayly returns faces the following

difficulty. The quality of

data for dayly returns does not allow to estimate reliably more than three

parameters, for example a scale parameter given by the first moment,

a combination of parameters describing the tail index and a rate constant

for the time dependence as in GARCH(1,1). Therefore the parsimonity

principle invoked by Calvet and Fisher [11] is rather

a must and not a freedom.

For stochastic volatility models a second difficulty arrises, that

the choice of the free parameters is

dictated by mathematical convenience. Their relation to market properties

remains obscure. This difficulty is avoided in agent or microscopic

models (for a recent review see ref [12] and the references

given therein). The behaviour of

the agents may be characterized by utility functions [13]. The

observed power law (fact (ii)) motivates the use of critical physical

models as the application of percolation by Cont-Bouchaud [14].

The percolation cluster are interpreted as herding behaviour of the agents.

In the Lux-Marchesi model [15] a herding mechanism appears

explicitly in the transition probabilities

between chartists and fundamentalistic traders. This leads to an intermittent

behaviour of agent numbers and thereby also for the returns.

To see whether herding alone can describe the stylized facts a symmetric

Kirman model [16] has been studied [17]. Quantitative

agreement with the data could be acchieved [18] within an asymmetric

Kirman model. In the latter agents differ slightly from those in

the Lux-Marchesi model that the two types of chartists (optimists

and pessimists) are replaced by one sort of agents (noise traders). The

difference between optimists and pessimists is described by an iid

random number. With this approximation the return behaves similar to a

stochastic volatility model, except follows a Markov process

instead of . In this paper we apply the Kirman model with a further

simplification. In empirical investigations it has been found

[18, 19] that fundamentalists are much less affected by herding

than noise traders, which implicates a very asymmetric herding model. In

the limit of large asymmetry the number of free parameters is reduced

from three to two. In the spirit of parsimonity we adopt this approach.

For an application to financial markets an equation of state is needed

relating the return to ratios of agent numbers. In a Walrasian market

[18] the volatility factor depends linearely on

the concentration of agents. The model using the simplified Kirman

model and this linear relation has been studied in [19]. In this

paper we adopt another equation of state. In contrast to a Walrasian market

the time for an agreement of the agents on a common return ought to be

finite. Assuming a random walk Zhang [20, 21]

concluded that itself should be proportional to the agent concentration.

We use this approach in the present paper. It

offers two desirable properties. Since in stochastic volatility models

and in herding models the concentration proportional to

follow simple Markov processes,

one might be able to show the equivalence of the latter with one of the

stochastic volatility models. Secondly one can use the empirical observation of

Plerou et al [22], that the return and the imbalanced volume

satisfy the same relation as the order parameter and an external field

in a critical mean field theory. In the framework of a universal

[23] there ought to be another equation for the return at zero

field. We will show that Zhang’s law emerges within such a model

naturally from risk aversity.

Whether the Walrasian linear relation or Zhang’s law are correct can be decided

at present only empirically. We will compare our model and the results from ref

[19] with the probability density function (hereafter abbreviated

with pdf ) and the autocorrelation function with the empirical returns

derived from the DAX.

The paper is organized in the following way. In section 2 we describe

our version of the Kirman model and in section 3 a derivation

of Zhang’s law. The

resulting unconditional pdf and the common pdf for two absolute returns

at different times

are given in section 4. The square root law together with a

Gaussian noise allows analytical calculation of various observables.

As examples we treat the autocorrelation function and the pdf conditional on the value of the previous day. These predictions we confront with the data in

section 5. In section 6 we make some concluding remarks.

2 Kirman’s Herding Model

We want to describe the changes of prices in a stock market with different agents which can change their strategy as function of time. Apart from the specification of an agent model a relation between the relative changes (return) of the stock index and the agent numbers is needed which will be treated in the next section. As herding model we use the Kirman model [16] discussed by Alfarano et al [18]. It is defined by the transition probability between two types of behaviour. denotes the mood of noise traders and a conservative or fundamentalistic strategy. The probabilities per unit time to change opinion are given by

| (1) |

The parameters correspond to spontaneous changes of mind. The second terms in equ (2) are proportional to the agent numbers in the new state and therefore describe the herding effect. Despite of the extensive character of this Markov process leads for a large number of agents to a non trivial equilibrium distribution for intensive ratios as . As shown in [18] the master equation belonging to (2) leads to a Fokker Planck equation (hereafter abreviated by FPE) for the pdf and a Langevin equation for . In application of the model it turned out [18, 19] that in most cases holds. This means that fundmentalists are much less influenced by herding than noise traders. Invoking the parsimonity principle we consider the limit of large . For the ratio

| (2) |

it is shown in appendix A that one obtains the following FPE

| (3) |

with the parameter describing the equilibrium pdf. This implies, that the number of fundamentalists is much smaller than that of the noise traders. If we transform the Langevin equation belonging to (3) to the variable

| (4) |

we obtain a well known model of stochastic volatility, the so called 3/2 model [9] provided we identify in the relation between the return and a Gaussian noise

| (5) |

with the volatility factor . Equ (4) corresponds to a

special version of the 3/2 model where drift and diffusion constants are

related to ensure existence of an equilibrium pdf for .

From follows

another frequently used model [8].

The limit of large affects also the time scales. As shown in the

appendix the process (2) should be applied to micro time steps

, whereas the variable changes with the observed time scale

. Both are related by .

Eliminating with (2) we get

| (6) |

which shows an explicit dependency of the agent ratio

on the time resolution .

As shown in [9] the FPE can be solved analytically for

the equilibrium pdf

| (7) |

and for the conditional pdf with

| (8) |

denotes the Bessel function with imaginary argument. The kernel has the following convolution property

| (9) |

and can be used for the time evolution of

| (10) |

3 Derivation of Zhang’s Law

The problem of this section deals with relation of agent ratio to the observable return . The small decay time in the autocorrelation of the returns suggests that the dynamic of the price is much faster than the change of agent numbers. The extreme case of an instantaneous Walrasian market has been assumed in ref [18] to model the behaviour of agents in the Lux-Marchesi model[15]. With the additional assumption that the change between optimistic and pessimistic noise traders occurs also on a fast time scale one gets [18] a linear relation between the return and the agent ratio . Using for small values of one gets

| (11) |

The noise incorporates many

changes during due to the noise traders.

In this Walrasian approach the price change is set instantaneously, a

closed order book is assumed and the agents have to accept any new return

irrespectively of their risk aversity. Considering for example the XETRA market

these assumptions seem to be questionable. Removing the first assumption

Zhang [20] assumed

the time needed to get the new price is proportional to the demand, which

is linear in the agent numbers. Describing the evolution of the price

by a random walk the return will be proportional to the square root

of the agent numbers. Therefore the linear relation (11)

should be replaced by the so called sqare root law given by

| (12) |

It has been applied [21] in context of the percolation model

of Cont-Bouchaud [14] in order to obtain a tail index larger than 2.

Equ (12) agrees with the return obtained in the 3/2 stochastic model.

Therefore the parameters of the latter can be related to the

behaviour of agents.

To obtain a less qualitative derivation of (12) and to include

the effect of risk aversity and an unbalanced order book we start with an

observation made by Plerou et al [22], who showed empirically

that the absolute return increases with the imbalanced volume

at small time intervalls and small as

| (13) |

with an exponent . At large and the return saturates as . As suggested already in ref [22] this could be interpreted as an equation of state in a critical mean field theory if corresponds to a scalar order parameter and to an external field. As dynamical fields in such a theory we use the return expected by agent of type . After time equilibrium is reached at a common return . A critical mean field theory with a scalar order parameter is described by the universal model [23]. This is defined by the following cost or energy functional

| (14) |

The first term is a positive definite quadratic form in the differences describing the interaction between the agents. We assume it strong enough that in equilibrium the mean field value for is independent of . This means the agents reach a common value for their expected absolute return. We normalize by . The terms lead to large cost functions for large . They account for the risk aversity of the agents. We expect that noise traders are much less affected by risk aversity than fundamentalists and can set to zero. Since the disordered phase is not observed, the coefficients in the quadratic term in (14) must be positive. A negative contribution to the cost function of the noise traders can be interpreted as ’happy loser’ effect [20], that fundamentalists are willing to accept a loss of money restricted by their risk aversity. The analogous term for the fundamentalists can be neglected by setting . The last term in (14) corresponds to the coupling of the return to an imbalanced volume. If this coupling is independent of the coefficient can be set without loss of generality to 1. In the limit of large agent numbers the model is solved by a constant with negligeable variance. The value of is given by the minimum of (14). With the above discussed approximations reads

| (15) |

Introducing the parameter by

| (16) |

the value of making to a minimum satifies the following mean field equation

| (17) |

The solution of (17) can be written as

| (18) |

Equ (18) expresses the scaling property of the critical theory. , and may be rescaled by the same factor without altering the results. The scaling function does not depend on any parameter. Its behaviour near and is given by

| (19) |

If only the leading terms are kept, for historical reasons the first form is called the zero field equation of state and the second the critical isotherm. The latter written in reads as

| (20) |

where we recover (13) for . For we get another equation of state

| (21) |

which reproduces the square root law of Zhang. The size of depends on the time resolution , if we use the Kirman model of the previous section. Inserting equ (6) for the agent ratios we get

| (22) |

Therefore the empirical relation (13) should hold only at small time scales in agreement with the data [22]. For large time scales the Zhang’s law ought to be applied. In addition we have the prediction, that the rate factor in (12) should vary with as

| (23) |

This power law is in nice agreement with the observed [30] power of

0.51.

There are still two problems within our derivation of the square root law.

The application of a critical theory is confined to small values of the

fields. At finite values the scaling law (18) may no longer

valid. Secondly the return does not saturate as required by the data,

but will increase as (20) for large . There exist of course

many models which have the same small field expansion as (14).

Even if we restrict ourselves to a minimal model of Ising spins which

has been used in ref [22] to describe the saturation there will

be an extra parameter for the distance from the scaling law (18).

As shown in appendix B for a spin model the mean field equation

(17) should be replaced by

| (24) |

with a parameter describing the deviation from the critical region. For we recover the critical mean field equation. Finite may be adjusted to the observed saturation of the return with the unbalanced volume . Therefore the critical isotherm (20) is very model dependent. On the other side the zero field equation for is almost unchanged. In the case of (24) we obtain

| (25) |

with a -dependent constant which is the non zero solution of

| (26) |

Since this constant can be absorbed into the rate constant ,

the square root

law appears to be robust against deviation from criticality. In appendix

B we also replaced the Ising spin model by a compact model,

which leads to the same conclusions.

At present stage of research

only empirical observations can decide on the possibilities (12)

or (11). In the present paper

we want to discuss whether there are advantages of the square root

law (12) over the linear relation (11).

4 Unconditional probability and 2-point function

Suppose one observes a time serie of the absolute returns . We assume the time to be an integer by absorbing the time step in the rate factor . Only the combined process with the history of the herding variables is a Markov process. This property is expressed by the following recursion formula for the pdf

| (27) |

Assuming the sqare root law (12) with a Gaussian noise the conditional distribution is given by

| (28) |

with the normalization constant .

To calculate the pdf for the absolute returns the solution of the

recursion (27) has to be integrated over all variables.

The sqare root law

leads to an exponential dependence of as function of , which matches

with the exponentials in allowing analytical calculations. In principal

the recursion (27) can be used to compute . The singularity

of for presents a problem, if one encounters a small value

of the rate . For the determination of the

parameters and two simpler cases are sufficient and we

defer an approximative solution of the recursion (27) to a future

publication [24].

The common pdf for the absolute returns at and

is obtained from the times iterated recursion

(27) by integrating over and all

intermediate . The latter integration

eliminates the corresponding

-factors and we can use the convolution property (9) of to

perform the intermediate integration leading to

| (29) | |||||

For large the operator converges to the equilibrium distribution independent of . Therefore factorizes in the limit of large as

| (30) |

with the equilibrium pdf

| (31) |

This Pareto like distribution becomes at large a power law with a tail index determined by the herding parameter

| (32) |

From equ (31) all equilibrium moments may be calculated ( see equ (82) in the appendix). For example the second moment

| (33) |

will be used for expressing in terms of and the observable

second moment in equilibrium

111Expectation values taken with the equilibrium pdf (31) will

be denoted by .

To derive an explicit form of the two point function

we take in equ (29) large with finite . Analogue to

the previous case the distribution factorizes and we obtain

| (34) |

The integrations in (34) can be carried out and is expressed in terms of hypergeometric functions. The exact form is given in appendix C. An interesting property of is that it depends only on a combination but not each of the variables and separately. Such a behaviour implies scaling laws. We demonstrate this scaling law in the simple case of and neglected terms of order . As shown in appendix C the conditional pdf is given by

| (35) |

If we eliminate with equ (33) and introduce the scaling variable by

| (36) |

we get

| (37) |

The conditional distribution of is independent of the previous

return . From this we can determine , since only at the

true the data for

with different will collapse into a single scaling function

. This function can be compared with the predicted curve

(37).

Knowing the two point function the autocorrelation of can be derived

(see appendix D ). The ratio

| (38) |

involves again a hypergeometric function. For negative values of the variance of exists and we find the autocorrelation function

| (39) |

If we expand for large the hypergeometric function we find with the leading term an exponentially decay

| (40) |

For small and finite the deviation from the exponential dependence (40) and the exact expression (39) may be substantial. It is interesting to note that for the ratio becomes singular at . Applying Eulers relation to the hypergeometric function one observes for the ratio

| (41) |

a power law in . This does not mean a long memory since neither the variance exists nor it consists in a large effect. The example given by Lillo et al.[28] shows that Markov processes may lead to power law in also with existing variance.

5 Empirical Comparison with the DAX

In this section we want to estimate the parameters of the model described in the previous section from a time serie of absolute returns of the DAX[25] during 1973-2002. The most efficient method would be using a maximum likelihood fit. The bad analytical properties of make this task prohibitive unless is large. As less efficient but tractable method to estimate and is to use fits to the unconditional pdf given in equ (31). In presence of correlations the sample of length can be still considered as a representative subset of an infinite time serie if holds. A small rate parameter may cause a problem. To see this we divide the data in 5 subsamples of similar statistics. Here and in all subsequent estimates we fix by equ(33) in terms of and . We checked that in each case a free variation of did not alter the results. The estimates of in each sample are given in table 1. They behave rather erratic and probability is rather low indicating a poor descripition of the data. This effect is due to the volatility clusters which are by no means equally distributed over the subsamples.

| Intervall | /point | ||

|---|---|---|---|

| 1/1973-10/1978 | 4.3 | 1.4 | 9/19 |

| 11/1978-8/1984 | 3.3 | 1.0 | 31/18 |

| 9/1984-7/1990 | 0.98 | 0.12 | 39/25 |

| 8/1990-3/1996 | 1.04 | 0.15 | 41/22 |

| 4/1996-2/2002 | 1.86 | 0.35 | 21/30 |

| 1/1973-2/2002 | 1.115 | 0.068 | 44/43 |

Taking all data one obtains a good value and the following value of

| (42) |

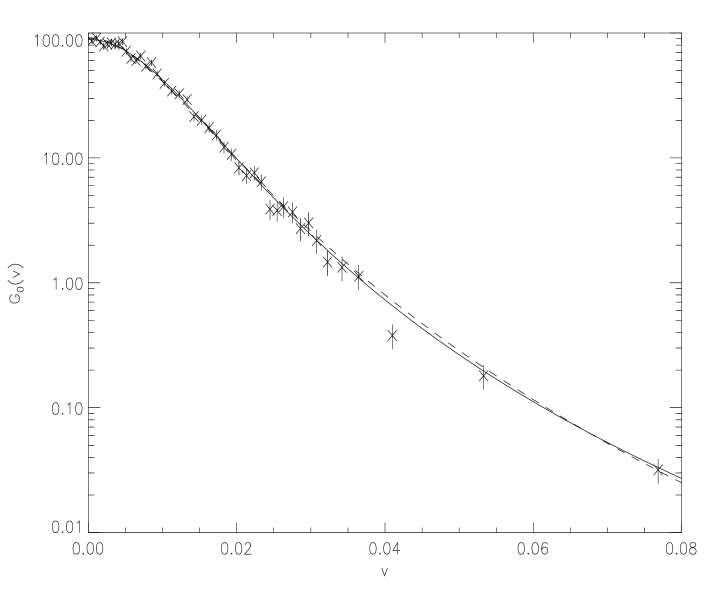

In figure 1 we compare the pdf from equ (31) with the

empirical data.

The agreement is excellent with a -probability of 60%. The values

in the subsamples agree with (42) within two standard deviations.

The value (42) corresponds to a tail index of which

is slightly larger than the the values obtained in other

financial markets [3, 26]. As we discuss lateron this may be an effect

of not having reached the asymtotic regime in the data.

We can compare our model with a model discussed by Alfarano [19]

where the same herding mechanism

is used but the sqare root law replaced by the linear relation (11).

The fit is worse ( -probability 1% ), but in view of

possible systematic errors still acceptable. The difference stems mainly from

the better description of low returns in our model. On a log scale the

fit in the linear model ( dashed line in figure 1 ) can hardly

be distinguished from our model, although the

tail index is 50% larger than in our case.

A - or maximum likelihood fit is dominated by the many

events with low . To judge the

description of extreme events we compare the predicted events with

in both models with the observed number

of events. Since the largest return in figure 1 correponds

to the fits may not be sensible to extreme events with larger .

The values for are given in table 2.

Despite of the large difference in the tail index both models agree with

the observation reasonably well with a preference for the

square root law. Large

differences occur only outside the observable region ().

We also learn that there is no need for an extra mechanism for crash events

as proposed in [27].

| 1985-2002 | 1973-2002 | |||||

|---|---|---|---|---|---|---|

| 5 | 8.1 | 7.6 | 11 | 13.8 | 13.0 | 24 |

| 6 | 3.9 | 3.4 | 6 | 6.6 | 5.7 | 9 |

| 7 | 2.1 | 1.6 | 3 | 3.6 | 2.8 | 6 |

| 9 | 0.8 | 0.5 | 1 | 1.3 | 0.8 | 1 |

| 11 | 0.3 | 0.2 | 0 | 0.6 | 0.3 | 1 |

| 15 | 0.09 | 0.03 | 0 | 0.2 | 0.06 | 0 |

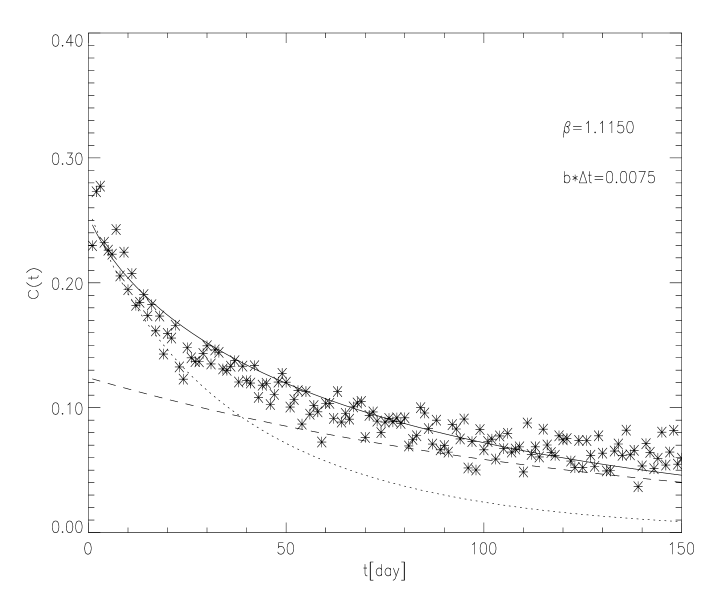

Both models can be distinguished if we consider the time dependence. The parameter can be estimated from the common pdf for pairs given in equ(77) of the appendix. We perform maximum likelihood fits by adding the log likelihoods for all pairs with a time lag . Maximizing with respect to and we obtain

| (43) |

| (44) |

The value of is compatibel with the estimate (42) from the

equlibrium pdf. The estimate (44) for implies a large decay time

day] in the order of 1/2 year. In the linear model only the

autocorrelation function can be computed. This model cannot describe the

data over large range of time lags. Adjusting to describe the

autocorrelation for small time lags a value

is obtained [19]. In figure 2 we compare the autocorrelation

function given in (39) (solid line) of our model with the values from

DAX. The agreement is good. The leading asymtotic term (40) (dashed

line) shows that the data cannot be described by an exponential behaviour.

The prediction of [19] (dotted line) should be valid only for small

time lags. Therefore the data for the autocorrelation prefer the

square root law.

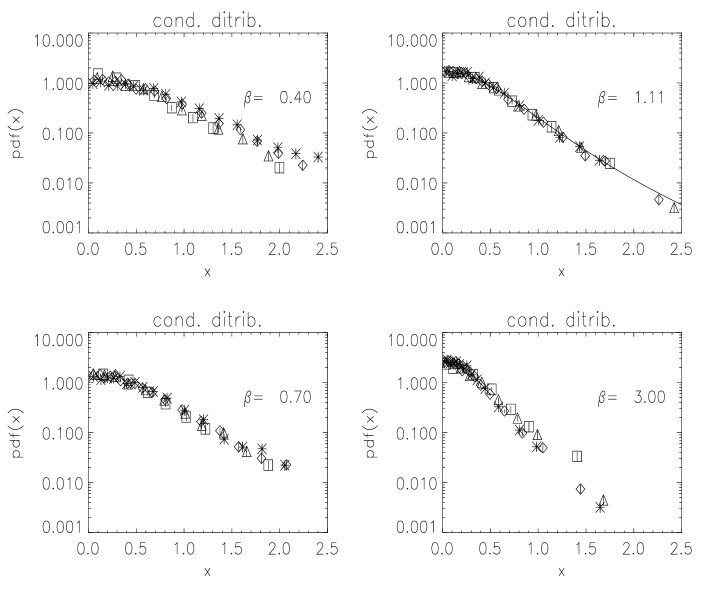

Finally we test the scaling prediction, that the conditional pdf is independent of if one uses the scaling variable

| (45) |

The assumption of small is very well satisfied with (44). In figure 3 we show the distribution of obtained in four intervalls of the normalized absolute return

| (46) |

at . For a the data collapse into a single curve. This curve agrees with the predicted scaling function (37) (solid line). From this agreement we conclude that the model describes the correlation between and well, which is not obvious from the autocorrelation due to the large fluctuation near seen in figure 2. A best fit to the scaling curve (37) leads to which agrees with the previous estimations in (42) and (43). It is very remarkable that three very different methods to determine lead to the same value.

6 Conclusions

The herding model of Kirman has been considered in the limit

that fundamentalists are much less affected by herding than

noise traders. As a

consequence the market consists of many noise traders and few fundamentalists

reflecting the conditions in a real market. Volatility cluster

occur if the fundamentalists dissapear from the market.

This is in contradiction to the results of

the Lux-Marchesi model, where fundamentalists dominate and volatility

clusters appear if chartists rise beyond 30%. Augmenting the herding

model with Zhang’s square root law between price changes and agent ratios

the model turns out to equivalent to the 3/2 model of statistical

volatility. This coincidence allows an interpretation of the parameters

in the latter model in terms of agent behaviour.

Due to the simplicity of our model

various observables can be calculated analytically.

This is important in or maximum likelihood

estimations, where numerically accurate and computationally easy

accessible expressions are required.

Comparing our model with empirical data we find good agreement with the

stylized facts derived from the DAX. The tail index of 4 is in harmony

with universality. Replacing the square root law by a linear relation

one gets a worse but still acceptable value of , however the

tail index increases to 6. This shows that the index depends strongly

whether one uses a Pareto law in the squared return

(as in our model) or in .

Universality of the tail index and the behaviour of extreme events favor

the square root law. The autocorrelation of the absolute return will

decay exponentially at large time lags. The very small rate

constant ensures that this asymtotic behaviour is reached outside the

region of timelags where the data can be trusted. The reasonable

agreement of the autocorrelation function of our model with the data

is much better than in the linear model. A quantitave measure of the

volatility cluster is expressed by a new scaling law for the pdf

conditional on the value of the previous day, which is again in good

agreement with the data.

The predictions based on a recursive solution of the combined Markov

process of return and agent ratios will be presented in a future

publication.

Acknowlegments: The author thanks Thomas Lux and Simone Alfarano

for stimulating discussions and valuable hints.

Appendix A Asymmetric Kirman Model

In this section we give the changes of the formulae of [18] in the case if one of the parameters describing the spontaneous change of oppinion becomes large. As pointed out in [18] the macroscopic time scale during the returns are observed does not need to coincide with the microscopic time scale over which the agents change oppinion. On the latter scale we have the FPE for derived in [18] from the transition probabilities (2)

| (47) |

For large z will be close to 1. Therefore we introduce the variable by

| (48) |

which remains finite. Transforming (47) into and neglecting terms of the order we find

| (49) |

with the differential operator

| (50) |

The real time scale (f.e. days) is related to by

| (51) |

The limit of large leads to small average values of the number of fundamentalists. By the identification (51) the agent ratio can be expressed in terms of the time scale

| (52) |

Inserting (51) into equ. (49) leads to

| (53) |

which is equivalent to equ. (7) replacing by and by . The FPE (3) ( see [9] ) can be solved by expanding in terms of Laguerre polynomials :

| (54) |

with the equilibrium pdf from equ. (7). The functions are right eigen functions of

| (55) |

The conditional pdf follows from the generating function of the Laguerre polynomials (see [29] ). The convolution property (9) is proven by the orthogonality of

| (56) |

with the expectation value with respect to .

Appendix B Models Outside the Critical Region

A general class of models can be characterized by the following cost functional

| (57) |

The minimum coupling ensures that the system is never in the disordered state. and set the scales for and . A suitable dynamic (Langevin equation, heat bath or Metropolis algorithm) will bring the system into equilibrium, which is a Boltzmann distribution. Expectation values are given by derivatives of the partition sum :

| (58) |

For the measure we can use either a spin or a compact model. reads in these cases

| (59) |

The expectation value of the return is given by

| (60) |

To evaluate we use the Gaus trick for large agent number :

| (61) | |||||

Inserting equ (61) into the integration over can be carried out with the result

| (62) | |||||

For the spin model we set and is given by

| (63) |

whereas in the compact model we use and the function as

| (64) |

In the large -limit is given by the maximum of the integrand at . For the spin model we get

| (65) |

Replacing by the expectation value we find the equation of state

| (66) |

To get the relation with the parameters of the critical model discussed in section 3 we expand equ (66) around small and

| (67) |

Comparing coefficients with the equation of state (18) we get two equations for the three parameters , and . For example the scale parameter for can be chosen arbitrarily. Measuring in units of we set

| (68) |

and express and in terms of the previous parameters and

| (69) |

Inserting these parameters into equ (66) we obtain the equation of state valid also outside the critical region

| (70) |

with

| (71) |

The parameter with describes the distance from the critical behaviour obtained for . The saturation of the return as function of determines the value of . The exact form is model dependent. The analogous calculation for the compact model leads instead of (70) to

| (72) |

It has the same behaviour for , but extrapolates hyperbolically for small to a constant instead of the exponential behaviour obtained from (70).

Appendix C Two Point Function of the Probability Density

From the expansion of the Bessel function in (8) we obtain the following representation for with

| (73) | |||||

Inserting (73) and the noise distribution (28) into equ(34) we obtain after integration over and

| (74) | |||||

The sum corresponds to the serie expansion of the hypergeometric function

| (75) |

At special arguments and holds. Using the scaling variable

| (76) |

we get

| (77) | |||||

With Euler’s relation equ(77) can be rewritten as

| (78) | |||||

If terms of order are negligeable and agrees with the scaling variable from equ (36). Setting in the argument to 1 leads to

| (79) |

This equation is equivalent to (35) if we use

| (80) |

with the equilibrium pdf (31) for .

Appendix D Autocorrelation

The easiest way to derive is to perform in equ(34) first the integrations using

| (81) |

with the equilibrium moments

| (82) |

Inserting as in the previous section the expansion (73) and performing the integrations over and we obtain for the ratio

| (83) | |||||

Again the sum is a hypergeometric function leading to

| (84) |

With the help of Euler’s relation we get finally

| (85) |

For large expansion of up to linear terms leads to

| (86) |

For and the expectation value becomes singular. Replacing in equ(84) the function by its value at argument 1 we find the power law given in equ (41)

References

- [1] C. G. de Vries The handbook of International Macroeconomics, Blackwell, Oxford 1994, p. 348.

- [2] A. Pagan Journal of Empirical Finance 3 (1996) 15

- [3] T. Lux and M. Ausloos in A. Bunde et al.(ed.) Theory of Desaster, Berlin 2002, p.373

- [4] F. Wagner Physica A 322 (2003) 607

-

[5]

Y. Liu, P. Gopikrishnan, P. Cizeau, M. Meyer,

C. K. Peng and H. E. Stanley

Phys.Rev E 60 (1999) 1390

P. Gopikrishnan, V. Plerou,L. A. Nunes Amaral, M. Meyer and H. E. Stanley Phys.Rev E 60 (1999) 5305 - [6] R. F. Engle and T. Bollerslev Econometric Reviews 5 (1986) 1

- [7] D. B. Nelson Journ. of Econometrics 45 (1990) 7

- [8] J. C. Cox, J. e. Ingersoll and S. A. Ross Econometrica 53 (1985) 385

- [9] D. Ahn and B. Gao Rev.Fin.Studies 12 (1999) 721

- [10] A. l. Lewis Option Valuation under Stochastic Volatility, Finance Press, Newportbeach 2000

- [11] L. Calvet and A. Fisher Review of Economics & Statistics 84 (2002) 381

- [12] E. Samanidou, E. Zschischang, D. Stauffer and T. Lux in F. Schweitzer (ed.)Microscopic models for Economic Dynamics, Lecture notes in Physics, Springer, Berlin 2002.

-

[13]

G. Kim and H.M. Markowitz Journ. Portfolio

Management 16 (1989) 45

M. Levy, H. Levy and S. Solomon Journal de Physique I 5 (1995) 1087 and Physica A 242 (1997) 90

S. Solomon and R. Richmond, Physica A 299 (2001) 188 O. Biham, Z. F. Huang, O. Malcai and S. Solomon Phys. Rev. E 64 (2001) 101 - [14] R. Cont and J. P. Bouchaud Macroeconomic Dynamics 4 (2000) 170

- [15] T. Lux and M. Marchesi Nature 397 (1999) 397 and Int. Journ. Theor. Appl. Finance 3 (2000) 67

- [16] A. Kirman Quart. Journal Econ. 108 (1993) 137

- [17] S. Alfarano and T. Lux in A. Kirman and G. Teyssiére, eds., Long Memory in Economics and Econometrics, Springer, Berlin 2004

- [18] S. Alfarano, F. Wagner and T. Lux to be published in Computational Economics 2005

- [19] S. Alfarano Thesis, Kiel 2005

- [20] Y.C. Zhang Physica A 269 (1999) 30

- [21] D. Stauffer and D. Sornette Physica A 271 (1999) 496

- [22] V. Plerou, P. Gopikrishnan, X. Gabaix and H. E. Stanley Phys.Rev E 66 (2002) 027104

- [23] J. J. Binney, N. J. Darwick, A. J. Fisher and M. E. J. Newman The Theory of Critical Phenomena, Clarendon Press, Oxford 1992

- [24] S. Alfarano and F. Wagner, to be published

- [25] Data basis of Institut für Weltwirtschaft, Kiel

- [26] M. M.Dacarogna, R. Gençay and U. Müller An Introduction to High-Frequency Finance, Academic Press, Oxford 2001

- [27] A. Johansen, O. Ledoit and D. Sornette Int. Journ. of Theor. and Applied Fin. 3 (2000) 219

- [28] F. Lillo, S. Micciche and R. N. Mantegna arXiv:cond-mat/0203442 (2002)

- [29] A. Erdely Higher Transcendental Functions Volume 2, p.189 McGraw-Hill Inc., New York 1953

- [30] P. Gopikrishnan, V. Plerou, L. A. Nunes Amaral, M. Meyer and H. E. Stanley Phys.Rev E 60 (1999) 5305