On Consistent and Calibrated Inference about

the Parameters of Sampling Distributions

Tomaž Podobnik1), 2),***e-mail: Tomaz.Podobnik@ijs.si

and Tomi Živko2),†††e-mail: Tomi.Zivko@ijs.si

1)Physics Department, University of Ljubljana, Slovenia

2)”Jožef Stefan” Institute, Ljubljana, Slovenia

The theory of probability, based on very general rules referred to as the Cox-Pólya-Jaynes Desiderata, can be used both as a theory of random mass phenomena and as a quantitative theory of plausible inference about the parameters of sampling distributions. The existing applications of the Desiderata must be extended in order to allow for consistent inferences in the limit of complete a priori ignorance about the values of the parameters. Since the limits of consistent quantitative inference from incomplete information can clearly be established, the developed theory is necessarily an effective one. It is interesting to note that when applying the Desiderata strictly, we find no contradictions between the so-called Bayesian and frequentist schools of inductive reasoning.

Ljubljana, August 2005

As for prophecies, they will pass away; as for tongues, they will

cease; as for knowledge, it will pass away. For we know in part

and we prophesy in part.

1 Corinthians 13, 8-9.

1 Introduction

The term inference ([1], p. 436) stands for two kinds of reasoning ([2], p. xix): deductive or demonstrative reasoning whenever enough information is at hand to permit it, and inductive or plausible reasoning when not all of the necessary information is available. “The difference between the two kinds of reasoning is great and manifold. Demonstrative reasoning is safe, beyond controversy, and final. Plausible reasoning is hazardous, controversial, and provisional. Demonstrative reasoning penetrates the science just as far as mathematics does, but is in itself (as mathematics is in itself) incapable of yielding essentially new knowledge about the world around us. Anything new that we learn about the world involves plausible reasoning, which is the only kind of reasoning for which we care in everyday affairs. Demonstrative reasoning has rigid standards, codified and clarified by logic (formal or demonstrative logic111A branch of mathematics, also referred to as deductive logic.), which is the theory of demonstrative reasoning. The standards of plausible reasoning are fluid, and there is no theory of such reasoning that could be compared to demonstrative logic in clarity or would command comparable consensus.” So George Pólya in the Preface to his Mathematics and Plausible Reasoning ([3], p. v).

In the second volume [4] of the work he collects patterns of plausible reasoning and dissects our intuitive common sense into a set of elementary qualitative desiderata that represent basic rules of inductive reasoning. When formulating his views in mathematical terms ([4], Chapter XV), he recognizes his rules to be in a close agreement with the calculus of probability as developed by Laplace in the late 18th century [5], but Pólya advances a thesis that when applying the calculus of probability to plausible reasoning, it should be applied only qualitatively (see, for example, [4], pp. 136-139), i.e. numerical values should be strictly avoided.

In the present paper we formulate a quantitative theory of inductive reasoning, in particular a consistent theory of quantitative inference about the parameters of sampling distributions. In Section 2 we adopt the basic qualitative rules of plausible reasoning, the so-called Cox-Pólya-Jaynes Desiderata, and review some of the well known results of their direct applications, such as Cox’s and Bayes’ Theorems. In addition, we clearly establish the lack of such applications in the limit of complete prior ignorance about the inferred parameter, with such ignorance representing the natural starting point of an inference. In other words, Bayes’ Theorem that can be used for updating probabilities, cannot directly be used in the step of probability assignment.

We carefully define the state of complete prior ignorance about the inferred parameter in Section 3. In particular, throughout the present paper we never question the specified model, i.e. the form of the sampling probability distribution is always known beyond the required precision. What we are completely ignorant about at the beginning of reasoning is the value of the inferred parameter.

In Section 4 we define location, dispersion and scale parameters and briefly review some of the properties of sampling distributions determined by these parameters. A separate section is devoted to the invariance of such distributions, a property that turns out to be of decisive importance when constructing a consistent theory of inductive reasoning. We also show that invariance of both the form of the sampling distribution and its domain, under a continuous (or Lie) group, is found only in problems of inference about parameters that can be reduced to inference about location parameters.

In Section 6 we extend the applications of the Desiderata in order to allow for a consistent assignment and not just for updating of probability distributions for the inferred parameters. The so-called Consistency Theorem is obtained by making use of Bayes’ Theorem and by requiring that if a conclusion can be reasoned out in more than one way, then every possible way must lead to the same result, in particular by requiring logically independent pieces of information to be commutative. The form of the Consistency Theorem is very similar to that of Bayes’ Theorem, but there is also a fundamental difference between the two since in the former a consistency factor is used instead of the prior probability distribution. Hence, the consistency factor cannot be subject to any of the requirements such as normalization or invariance with respect to a one-to-one parameter transformation, that are perfectly legitimate for well defined probability distributions.

Instead, the form of the consistency factor is determined in a way that preserves the logical consistency of our reasoning. By consistency we mean that, among other things, if in two problems of inference our state of knowledge is the same, then we must assign the same probabilities in both. In Section 7 we find that the basic Desiderata uniquely determine the form of consistency factors for sampling distributions whose form and domain are invariant under a Lie group of transformations. It is therefore only for those problems reducible to inference about location parameters that we can give an assurance of consistency to our parameter inference. The form of consistency factors for such distributions is then determined throughout Sections 8-10, while in Section 11 we discuss under what circumstances the present theory is guaranteed to be consistent in the case of pre-constrained parameters.

In Section 12 we make verifiable predictions that are based on the presented theory, thus elevating its status above the level of a mere speculation. The predictions are made in terms of long run relative frequencies. We show that a consistent inference is necessarily also a calibrated one, i.e. that consistently predicted frequencies always coincide with (a one-to-one function of) actual frequencies of occurrence. This important result speaks in favour of a complete reconciliation between the so-called Bayesian and frequentist schools of plausible reasoning.

In counting experiments the invariance of sampling distributions is clearly missing and so the consistency factors cannot be uniquely determined by following the basic Desiderata. The remedy is to collect enough data so that the sampling distribution approaches its dense limit. Until then, our reasoning is necessarily based on some ad hoc prescriptions that can (and very often will) lead to logically unacceptable results, as is demonstrated in Section 14. In such cases it might therefore be the best to refrain from quantitative inferences, i.e. to remain on a qualitative level.

In Section 15 we briefly review conceptual and practical difficulties and paradoxes caused by using Bayes’ Theorem instead of the Consistency Theorem in the limit of complete ignorance about the inferred parameters. The problem is contained in the self-contradicting non-informative prior probability distributions. Long-lasting arguments over this subject led, inter alia, to a split in the theory of inductive reasoning and it is in this way that the Bayesian and the frequentist schools emerged. In our view, the splitting into (at first glance) almost diametrically opposed schools is highly artificial, provided that the two schools strictly obey their basic rules, i.e. that they refrain from using ad hoc shortcuts on the course of inference. For regardless how close to our intuitive reasoning these ad hoc procedures may be, how well they may have performed in some other previous inferences, and how respectable their names may sound (e.g. the principle of insufficient reason or its sophisticated version - the principle of maximum entropy, the principle of group invariance, the principle of maximum likelihood, and the principle of reduction), they will in general inevitably lead not only to contradictions between the two schools of thought, but also to inferences that are neither consistent nor calibrated.

There are also two appendices to the present paper. The first one contains, for the sake of completeness, a proof of Cox’s Theorem, while in the second one, the so-called marginalization paradox, is extensively discussed.

2 Basic rules and their applications

Let n hypothesis or an event be an unambiguous proposition , i.e. a statement that can be either true or false. As we are in general not certain about either of the two possibilities, the classical logic of deductive reasoning [6] is to be extended in order to allow for plausible or inductive inferences based on incomplete information.

Let (a state of) information summarize the information that we have about some set of propositions , called the basis of , and their relations to each other. The domain of is the logical closure of , that is, the union of . A state of information is not restricted to containing only deductive information; it can also contain imprecise or insufficient information that says nothing with certainty, but still affects one’s opinion about a certain proposition. Such kind of information can also be updated: we write for a state of information obtained from by adding additional information ( evidence) that proposition is true.

Now, let be a state of information of a given person and be a proposition in the domain of . Then, we introduce the (degree of) plausibility as a degree of belief of the person that is true given the information in . We say that is the knowledge base for the assigned plausibility . In the present paper we assume all considered plausibilities to be subject to very general requirements that can be listed in the following three basic Cox-Pólya-Jaynes Desiderata ([2], § 1.7, pp. 17-19):

- I.

-

Degrees of plausibilities are represented by real numbers.

That is, plausibilities are numerically encoded states of knowledge about propositions. Formally, an assigned plausibility can be regarded as a function:

where is the set of possible states of information about some set of propositions.

In addition to the first Desideratum, we adopt two natural but nonessential conventions:

-

•

a greater degree of belief shall correspond to a greater number;

-

•

the plausibility of a hypothesis that we are certain about (e.g. the plausibility of a tautology) equals 1.

By referring to the conventions as being nonessential we mean that we could have equally well adopted a convention that the plausibility of a tautology equals a different positive constant, or that a greater degree of probability should correspond to a smaller number. Nevertheless, according to the above Desideratum and the two conventions, the assigned plausibilities can range within an interval , where is plausibility of the false proposition.

We say that a state of information is consistent if there is no proposition for which plausibilities for being true and for being false can both equal unity. That is, based on consistent information both a proposition and its denial cannot be true. In order to avoid ambiguities, we restrict ourselves to considering only plausibilities that are assigned upon consistent states of information.

- II.

-

Assignment of plausibilities must be in qualitative correspondence with common sense.

In our case, the concept of common sense stands for the following conditions:

-

•

Since plausible reasoning is a generalization of deductive logic, it must be consistent with the results of Boolean algebra [7] - the algebra of deductive logic.

-

•

Microscopic changes in the knowledge base should not cause macroscopic changes in the plausibilities assigned. In addition, for every considered proposition there exists some set of possible consistent states of knowledge such that , with , can take any of the values within a continuous interval (continuity requirement).

-

•

We assume that the degree of belief that is false depends in some way on the plausibility that is true. In addition, when old information is updated into in such a way that the plausibility of is increased, , it must produce a decrease in the plausibility that is false, . That is, we assume that there exists a continuous, twice differentiable, strictly decreasing function of plausibility , such that

-

•

Plausibility , assigned to a hypothesis that two non-contradictory hypotheses, and , are simultaneously true, is assumed to be completely determined by the values of , , and . Then it can be shown (see Lemma 1 in Appendix A) that evident inconsistencies are avoided only if depends solely on and , i.e. if there exists a function such that

We further require for the function to be strictly increasing and twice differentiable in both of its arguments. By strictly increasing we mean that if the knowledge base is updated to in such a way that the plausibility of is increased, , but the plausibility remains the same, , this can only produce an increase in the plausibility that both and are true, , in which the equality can hold only if is impossible given and . Likewise, given information such that and , we require that .

- III.

-

Assignment of plausibilities must be a consistent procedure:

- a)

-

If a conclusion can be reasoned out in more than one way, then every possible way must lead to the same result.

- b)

-

When assigning plausibilities, we must always take into account all of the evidence we have relevant to a hypothesis. We do not arbitrarily ignore some of the information and base our conclusion only on what remains.

- c)

-

Equivalent states of knowledge must be always represented by equivalent plausibility assignments. For example, if in two problems our state of knowledge is the same (except perhaps for the labelling of the propositions), then we must assign the same plausibilities in both.

The requirement of consistency plays a special rôle among various requirements which a theoretical system, or an axiomatic system, must satisfy. It can be regarded as the first of the requirements to be satisfied by every theoretical system, be it empirical or non-empirical. As for an empirical system, however, besides being consistent, it should satisfy a further criterion: it must be falsifiable ([8], § 24, pp. 91-92). According to this criterion, statements, or systems of statements, convey information about the empirical world only if they are capable of clashing with experience; or more precisely, only if they can be systematically tested, that is to say, if they can be subjected (in accordance with a methodological decision) to tests which might result in their refutation. In so far as a scientific statement speaks about reality, it must be falsifiable: and in so far as it is not falsifiable, it does not speak about reality [9]. Since every degree of belief is to be assigned on the basis of available evidence, our aim is clearly to formulate an empirical theory of plausible reasoning, i.e. a theory that speaks about reality. We therefore add an additional requirement, an operational Desideratum, to the original Cox-Pólya-Jaynes Desiderata:

- IV.

-

A theory of plausible inference must specify operations that ensure the falsifiability of every assigned degree of plausibility.

Richard Cox showed [10] that the following can be deduced when plausibilities satisfy Desiderata I.-III.b:

- 1.

-

Suppose that plausibilities , , , and can be assigned. Then there exists a continuous strictly increasing function of each of these plausibilities,

such that

(1) and

Every compositum of function and a plausibility assignment , , or in a simplified notation, is referred to as the probability for to be true given available information , and the above equation (1) is referred to as the product rule. Note that every probability is at the same time also a plausibility, i.e. it is consistent with the basic Desiderata.

- 2.

-

Probabilities and sum up to the probability of a certain event, i.e. sum up to unity:

(2) which is referred to as the sum rule.

The above results are usually referred to as Cox’s Theorem (for a proof of the Theorem see Appendix A). Note that the product and the sum rule, being only relations between probabilities, do not of themselves assign numerical values to any of the probabilities arising in a specific problem. The only numerical values, considered thus far, are those corresponding to certainty and impossibility, one and zero, respectively, of which the former is a mere consequence of a convention, adopted along with Desideratum I, rather than required by the rules of the Theorem. Moreover, it is hardly to be supposed that every reasonable expectation should have a precise numerical value [10], nor is there any guarantee that every state of information about a particular proposition will meet the continuity requirement of the common sense Desideratum.

The product and the sum rule are unique in the sense that any set of rules for manipulating our degrees of belief, represented by real numbers, is either isomorphic to (1) and (2), i.e. different from (1) and (2) only in form but not in content, or inconsistent. Thus, we could have chosen any other set of plausibilities that are one-to-one functions of the corresponding probabilities , and then adequately adapt the product and the sum rule. For example, if we choose such that

with being an arbitrary positive number, the corresponding product rule for remains the same while the sum rule reads:

As another example, we could have chosen zero to represent the plausibility of a proposition that we are certain about, and a plausibility such that:

Then, the appropriate product and sum rules for would have read:

and

The freedom to choose an arbitrary plausibility function to represent our degree of belief is analogous to gauge invariance in field theories where potentials (i.e. functions that the fields are expressed by) are not rigidly fixed. The predictions of field theories are unchanged if the potentials are transformed according to specific rules, i.e. if the potentials are subjects to gauge transformations. Then we choose one particular form of potential, i.e. we choose a particular gauge, not because it is more correct than any other, but because it is more convenient for the particular problem that we are solving within a filed theory. For the same reason we choose probabilities and not any other plausibilities to represent our degrees of belief: not because they are more correct, but because it is for probabilities that the product and the sum rule take the simplest forms. We comment on the choice of probability, that we adhere to throughout the present paper, again in Section 12 when we discuss the relation between probability and frequency.

Once the probabilities are chosen from all possible plausibility functions, i.e once the gauge is fixed, the incompleteness of the concept of plausibility is removed: the product and the sum rules, (1) and (2), are the fundamental equations of probability theory, while all other equations for manipulating probabilities follow from their repeated applications. For example, it is in this way that we obtain the general sum rule that either or is true:

| (3) |

Suppose now that propositions form an exhaustive set of mutually exclusive propositions. The propositions are mutually exclusive if the evidence implies that no two of them can be true simultaneously,

and exhaustive if one of them must be true,

A classical textbook example of such a set would be six hypotheses arising from tossing a die, where index corresponds to the particular number thrown.

The hypotheses of a set are unambiguously classified by assigning one or more numerical indices. Deciding between the hypotheses and estimating the index are practically the same thing:

| (4) |

with the corresponding normalization

| (5) |

We denote probabilities by capital when arguments are propositions, and by small when arguments are numerical values. By assigning probability to every possible value of the index we specify how our degree of belief is distributed among the hypotheses of the set , i.e. we specify the (sampling) probability distribution for .

The distribution of one’s degree of belief in hypotheses labelled by different values of index may be equivalently represented by the cumulative distribution function (cdf), defined as

| (6) |

where permissible values of the index range from to . The probability for taking a value between and can thus be expressed by cdf’s simply as:

In addition, for an exhaustive sets of hypotheses the normalization condition (5) implies:

In many cases of practical importance the hypotheses of a set become very numerous and dense. For example, when predicting the decay time of an unstable particle, we start with a countable set of hypotheses that the decay time of that specific particle would be, for instance, seconds. But such a set is not an exhaustive one since the decay time could also be or seconds. Further refinement of the original propositions leads to a dense set of hypotheses where neighbouring hypotheses, i.e. hypotheses with nearly the same index value, become barely distinguishable. In such cases there cannot be a sharply defined hypothesis that is strongly favoured over all others. Instead, it only makes sense to consider probabilities for index in a certain interval of its permissible range. In this way index transforms into a continuous variable with a continuous sampling probability distribution:

| (7) |

Every continuous distribution can be expressed by a probability density function (pdf), :

| (8) |

Using pdf’s we can now rewrite the product rule (1) as

| (9) |

and the normalization (5) by replacing summation over discrete indices by integration over a dense domain :

| (10) |

The sum in the cdf (6) for a discrete variable is replaced by an integral for a continuous variable :

| (11) |

where ranges from to . Since the probability can be expressed by the cdf’s as:

the normalization (10) implies:

Suppose we have a continuous variable that is related functionally to a variable by a one-to-one relation:

being differentiable in and vice versa. Let and . Since the inferences about and are based on equivalent pieces of information and (the transformations of the variables correspond only to relabellings of hypotheses), Desideratum III.c implies the following equality:

| (12) |

where

| (13) | |||||

with and being the pdf’s for and , respectively. That is, assigned probabilities must be invariant under variate transformations.

As an example that illustrates the above reasoning, imagine two scientists,

say Mr. A and Mr. B, measuring decay times of unstable particles.

Each time they start their clocks at the moment when a particle is produced,

but the clocks run at different speeds, so Mr. A measures a decay time

of the -th particle, and Mr. B

(14)

where is an arbitrary positive constant.

Since is a continuous random variable, there is not much point in considering probabilities and , since both, and are events with zero probability (probability measure). Instead, we should consider probabilities for measuring in certain intervals and , where and are the widths of the two intervals. Due to the different speeds of the two clocks, equivalent events, i.e. equivalent time intervals, are not labelled equally by the two observers: the interval of Mr. A corresponds to the interval of Mr. B. For example, in the case of , the interval no. 10 of Mr. A is split into intervals 46-50 by Mr. B. That is, the variate transformation (14) implies

Then, since the two propositions, and differ only in labelling, Desideratum III.c implies the two probabilities and , assigned by Mr. A and Mr. B, respectively, to be equal:

Note that the logic behind such a reasoning is very similar to the logic of Poincaré’s relativity principle [11] of the special theory of relativity stating that no preferred inertial frame (or no absolute time scale) exists.

The variate transformation (14)

is linear, but it need not be so, as long as it remains one-to-one.

Suppose that Mr. B considers a probability distribution of

a variate

(15)

If Mr. A divides a range of his variate into

intervals of equal widths

Mr. B’s corresponding intervals of highly non-uniform widths

cover the infinite corresponding range of . Despite the non-uniformity of the interval widths, the transformation (15) still represents a mere relabelling of the hypotheses: and are equivalent variates, and and (with and ) are equivalent propositions. Imagine that because of using the transformed variate instead of , Mr. B considers himself inferior to Mr. A. But since the transformation (15) is one-to-one, the inverse transformation

always exists: Mr. B can always obtain from and then make his inference from instead of from .

To sum up, the logic behind Desideratum III.c implies equivalence of all variates, connected via one-to-one transformations: while the specified models (i.e. forms of pdf’s, see below) together with the range of the variates may be changed (this is indicated by using symbol instead of ), the probability content must be invariant under such transformations.

The equality (12) is assured for all intervals and only if ([12], pp. 20-28)

| (16) |

Indeed:

for variate transformations with positive , and

in the case of negative . Inversely, is expressed in terms of as

| (17) |

where is the reciprocal of ,

since any one-to-one transformation from to and then from to must restore the original distribution, and hence

Note that equal information implies equal probabilities, while in general it does not imply equality of pdf’s.

In the bivariate case where

the relations between the pdf’s for and , and , are the following:

| (18) |

and

| (19) |

with the absolute values of the derivatives, and , being replaced by the absolute values of the corresponding Jacobians,

and

respectively.

Special attention is needed if the derivatives in a univariate case, or the Jacobians in a multivariate case, change sign within the domain of the pdf since in that case the variate transformations and are not one-to-one any more. We will meet such a difficulty in Section 4 where it will be overcome on account of the special symmetry of the specific transformation.

In the present paper we consider sampling probability distributions, either discrete or continuous , that can be specified by a mathematical function, determined by the values of its parameters 222We adhere to the common and useful convention of using Greek letters , , , , and for parameters throughout the paper.. In such cases assignment of probabilities to hypotheses from a given set reduces to estimation of the parameters of the distribution: what we try to achieve is to assign probabilities to different values of trhe parameters, i.e. to specify the probability distribution for . Note that the probability distributions for parameters are subjects to the same Desiderata as the distributions for sampling variates. In this paper we will focus on the parameters with dense domains, where the corresponding probability distributions are continuous:

| (20) |

The probability for (20) is assigned upon information that we explicitly split in our notation into evidence from the measurement of the quantity whose probability distribution is determined by , and the additional relevant information . The reason for such splitting of the information will become evident below when we derive Bayes’ Theorem.

The pdf for (20) is subject to the usual normalization,

| (21) |

where integration is performed over the complete range of . In addition, in the case of assigning probabilities for two parameters, and , simultaneously, the product rule (1) can be applied:

| (22) |

Then, with the factors and being properly normalized according to (21), it is easy to see that the marginalization procedure yields

| (23) |

The product rule can also be applied for assigning probabilities to and :

| (24) |

The above equation can be rewritten into Bayes’ Theorem [13, 14],

| (25) |

also referred to as the principle of inverse probability (see [15], § 1.22, p. 28). When the domain of is also dense, the theorem can be written in terms of pdf’s only:

| (26) |

We interpret the theorem in the following way ([16], § 1.3, p.2). We are interested in the probability distribution for and begin with the initial or prior probability, also referred to as the probability a priori, whose pdf reads . It is based on any additional information that we possess beyond the immediate data . Thus, is the probability for prior to taking evidence into account. The posterior probability, also referred to as the probability a posteriori, , is the probability for posterior to adding evidence to our previous information. The likelihood, , tells us how likely is observed, given the value of the parameter that determines the probability distribution for . According to Bayes’ Theorem (25), the only consistent way of obtaining the posterior pdf, , is by multiplying the prior pdf by the likelihood, which is usually referred to as the likelihood principle (see, for example, [2], § 8.5, p. 250). Or, in the words of Jeffreys ([15], § 2.0, p. 57): ”Consequently the whole of the information contained in the observations that is relevant to the posterior probabilities of different hypotheses333i.e. of different values of the inferred parameter(s), is summed up in the values that they give to the likelihood.” Note that with the basic Desiderata being adopted, the term “likelihood principle” becomes inappropriate and might even be misleading, since the fact that all of the information that can be extracted from the datum is contained in the value of the appropriate likelihood, is a mere consequence of application of the basic Desiderata, rather than an additional principle (i.e. a Desideratum) on its own. The denominators and can be obtained by the normalization requirement (21) as:

| (27) |

and

| (28) |

Bayes’ Theorem is thus a rule for updating the information that an inference is based upon. Formally, it is just a special case of the product rule of the Cox theorem. The latter also ensures that (25) is the only consistent way of updating the information and, consequently, our probability distribution for .

Suppose that after we learn a new piece of information, , that we would like to include in our inference about . Then, serves as a prior pdf, i.e. pdf for prior to taking into account. According to (25), the posterior pdf then reads:

| (29) |

where is the likelihood for given , and the additional information .

In the limit of our complete ignorance about the value of a parameter prior to the first evidence , when merely stands for our admission that we possess no prior information relevant to apart from the specified form of the sampling distribution, the complete procedure for manipulating probabilities by using the product rule (1), or Bayes’ Theorem (25), breaks down. This is a direct consequence of the fact that we can only assign probabilities for hypotheses on the basis of available relevant information: ignorance thus allows for no probability assignment . In this event, both the product rule (1) and its derivative, Bayes’ Theorem (25), lack their vital components and cannot be used. In other words, Bayes’ Theorem only allows for updating probabilities that were already assigned prior to their updating, and therefore need be amended for the limit of complete prior ignorance, which is a natural starting point for every sequential updating of information. Our goal in the following sections is to make such an amendment in a consistent way, i.e. to establish when and how probabilities can consistently be assigned.

3 Complete ignorance about parameters

As a starting point, we would like to specify precisely what we mean and what we do not mean by the limit of complete ignorance about the value of a parameter of a given probability distribution for . First of all, ignorance about a distribution parameter is not a synonym for absolute ignorance in every possible respect. For example, throughout the paper we assume as a working hypothesis that the probability for is distributed in a form that is completely known but for the value of its parameter(s) , i.e. the chosen form of the probability distribution for together with its domain - the ranges of the sampling variate(s) and the inferred parameter(s), and , is always assumed to be appropriate beyond the required precision. This assumption is explicitly indicated by the symbol that every probability (or probability density) is conditioned upon.

What we are completely ignorant about is the value of . There is no information at our disposal that would enable us to assign a probability distribution for : it can take any value within its permissible range . Since the value of is completely unknown, then the distribution for becomes undetermined. This is where we then start collecting data that we would like to use for a consistent inference about .

The situation, described above, is an ideal limiting case that can serve as a reasonable approximation for many real-life situations. For example, even before the first measurement of a decay time of an unknown unstable particle, there is not much room for doubt about the form of the decay time distribution. Due to past experiences with all other unstable particles we feel almost completely certain that the distribution would be exponential (we come back to this point in Section 16 where the possibility of assigning probabilities to specified models is considered).

But before the first measurement, the parameter of the distribution, the average decay time , is completely unknown, so we do not know what value of the first measure decay-time, , to expect: it could be anything between zero and infinity. Inversely, before the first measurement of , the parameter can take any value in the same interval. Note that a hint of a symmetry between the collected data and the inferred parameters is present in the foregoing reasoning. The concept will be extensively exploited during the following sections.

With representing only knowledge about the type of sampling distribution, different states of knowledge and can be enumerated according to the values of and , respectively. In this way, the sets and of possible different states of knowledge become subsets of real numbers, , and the pdf’s and can both be formally expressed as functions

Many of the derivations in the present article automatically require dense ranges for both and , as well as differentiability of pdf’s and . The problems accompanying discrete sets of hypotheses are extensively discussed in Section 14, where inferences about parameters of counting experiments are considered.

4 Location, scale and dispersion parameters

We pay special attention to the so called location, scale, and dispersion parameters of probability distributions. A parameter of a sampling distribution is a location parameter, and a parameter is a dispersion parameter, if the pdf for takes the form

| (30) |

with the range for stretching over the whole real axis, with the range of being an interval on the real axis and with the permissible range of being an interval on the positive half of the real axis. For the time being, let the permissible range of coincide with the entire real axis, , and the range of with its entire positive half, , while we postpone a discussion about pre-constrained parameters until Section 11.

A bivariate pdf for two independent variates, and , both being subject to the same pdf of the form (30), according to the product rule (9) equals the product of univariate pdf’s, and :

| (31) |

The pdf for transformed variates and , and , where

or, inversely,

can be calculated according to (18):

| (32) |

The factor 4 in (32) that ensures appropriate normalization, arises as a product of the absolute value of the Jacobian,

| (33) |

and an additional factor of 2, the latter being a consequence of the symmetry of the pdf for and with respect to the change of sign of the difference . With the sign of the difference inverted, the determinant (33) inverts its sign, too, but its absolute value, as well as the value of the pdf (see (32)), remain unchanged. Therefore both the range with the positive and the range with the negative sign of the Jacobian can be simultaneously taken into account simply by multiplying the pdf by an additional factor of 2.

When inferring the parameters of a sampling distribution of the form (30) it may happen that the value of one of the two parameters is known to a high precision. In such cases the parameter with the precisely determined value is fixed and we only make an inference about the remaining one. Let first the dispersion parameter be fixed to , e.g. to 1, so that the pdf for , given the possible value of and the fixed value ,

| (34) |

is a function of and only. The fixed parameter ( in the present case) is usually (though not always) omitted from explicit expressions.

According to (34) and (11), the cdf for reads:

| (35) |

Note that the form of the above cdf implies the corresponding pdf to be of the form (34), i.e. implies to be a location parameter of a sampling probability distribution for . Indeed:

where

Since the integrand in (35), i.e. the pdf for , is a positive function, and the upper bounds of the integral are strictly decreasing with the increase in the parameter, the cdf is evidently strictly decreasing in .

With the location parameter being fixed to , say to 0, the pdf (30) for reduces to:

| (36) |

When the range of the random variate is bound to the positive half of the real axis,

the corresponding parameter of the sampling distribution,

| (37) |

is usually referred to as the scale parameter. Note that in symmetric cases when

the pdf (36) for with fixed can be reduced to a pdf (37) without any loss of either generality or information. Namely, the pdf for a transformed variate

reads:

where the factor of 2 arises due to shrinkage of the sample space. In such cases dispersion parameters are evidently equivalent to scale parameters.

Any sampling probability distribution determined by a scale parameter, , and a fixed location parameter , can be further transformed into a probability distribution determined by a location parameter (see, for example, [17], § 4.4, p. 144 or [18], § 3.2.2, pp. 22-23):

and a fixed dispersion parameter , say . Namely, a substitution

yields:

| (38) |

As was the case with cdf (35), the cdf for ,

| (39) |

is also monotonically decreasing with increasing value of the parameter.

Some of the most important continuous sampling distributions are determined by one or more parameters of the above mentioned types (see [19], § 4.2, pp. 58-83). In addition, all distributions determined by either location, scale or dispersion parameters share a very important property: they all belong to the invariant families of distributions.

5 Invariant distributions

Let

be a pdf for a random variable from a dense sample space that is determined by the value of parameter from the parameter space . Let there exist a group of transformations of the sample space into itself:

where index denotes the particular element of the group. Since is a group, it is closed under composition of transformation, i.e. a composition of every pair of transformations , , such that

is also contained in . In addition, the group also contains an identity such that

and the inverse transformation for any such that

As a consequence, the transformations are one-to-one, i.e. implies , and onto , i.e. for every there exists an such that (see, for example, [17], § 4.1, p. 143).

Since the transformation is one-to-one, the pdf for the transformed variate according to (16) and (17) reads:

| (40) |

In addition to , let there exist also a set of transformations of the parameter space into itself,

Then:

| (41) |

If for all , and for every there exists such that

| (42) |

the family of distributions is said to be invariant under the group ([17], § 4.1, p. 144 and [20], § 23.10, pp. 300-301).

If a family of distributions is invariant under , then the set of transformations of into itself is also a group, usually referred to as the induced group ([20], § 23.10, p. 300). Namely, according to the definition of invariance, if the pdf for is given by , the pdf for is given by . Hence, the pdf for is given by both and . From the equality of the two it follows that

This shows that is closed under composition. It also shows that is closed under inverses if we let and note that is the identity in .

For example, a sampling distribution for and (32), determined by the values of a location parameter and a dispersion parameter , is invariant under the group of simultaneous location and scale transformations:

| (43) |

where

By fixing the dispersion parameter, the symmetry of the pdf with respect to the scale transformation is broken, leaving only the symmetry with respect to a simultaneous translation of and by an arbitrary real number :

| (44) |

When, on the other hand, the location parameter is fixed to and the dispersion (or scale) of the distribution is unknown, the appropriate pdf (37) is still invariant under the scale transformation:

| (45) |

Let now be an invariant sampling distribution and let be its cdf such that

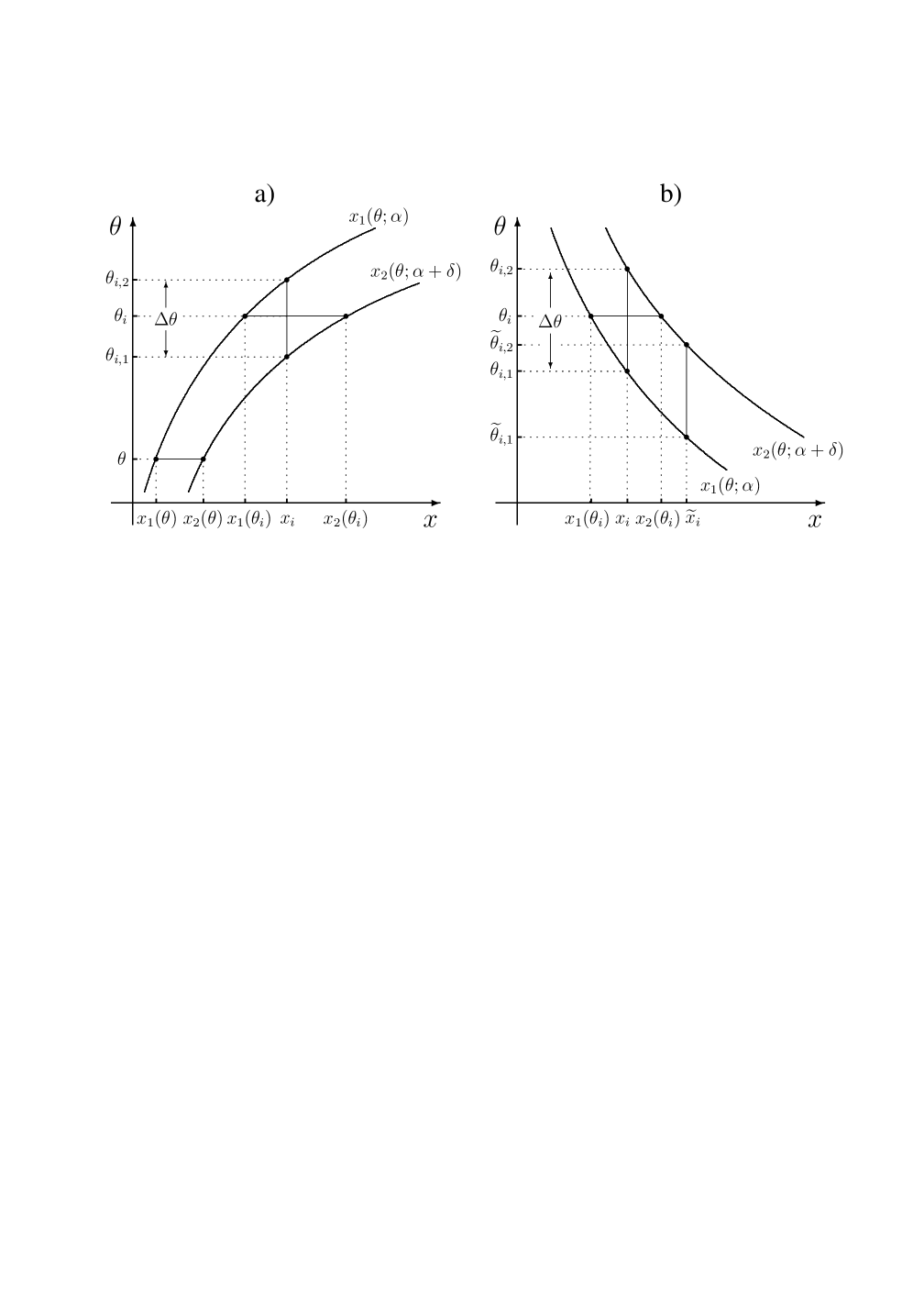

where is the lower bound of the sample space. Then the cdf for , given , reads:

where is the lower bound of the range of . It is easy to show that: the lower and the upper bound of the range of , and , become transformed into the bounds of , and :

and that the cdf for , given , is related to the cdf for , given , as:

Indeed:

where the positive and the negative sign correspond to and to , respectively. Setting to the upper bound of its range, the above equation reads:

Since the cdf’s are limited within , this completes the proof by implying

for every and , and for all .

A very important corollary - the Existence Theorem - can be deduced from the above relations. Let a probability distribution for be invariant under , and let and be continuous groups such that partial derivatives

exist for every and , with both derivatives always being different from zero and finite. In other words, and are to be Lie groups (see, for example, [21], § 7.1-7.2, pp. 126-130). In addition, let the range of the sampling variate also be invariant under , i.e.

Then the cdf for , given , can be rewritten as:

which permits the following conclusions: the cdf is independent of the parameter of the transformations, i.e.

and the parameter enters only through and , i.e.

where denotes differentiation with respect to the -th argument of (we adhere to this notation throughout the present paper, whatever the function and the arguments may be). Then, by combining the two conclusions and by setting we obtain:

| (46) |

where the derivatives and of functions and are defined as reciprocals of the corresponding infinitesimal operators of the Lie groups and :

| (47) |

and

| (48) |

By defining a function ,

| (49) |

(46) can be further reduced to

| (50) |

or to a functional determinant (see [22], § 7.2.1, p. 325),

With being different from zero, and can be expressed as

| (51) |

and

| (52) |

which, inserted in (50), yield:

Since this is to be true for any and , and must be the same functions:

Taking this into account, we multiply equations (51) and (52) by and , respectively, so that their sum reads:

implying the distribution function to be a function of a single variable (49),

| (53) |

By choosing

the cdf of an invariant sampling distribution thus reduces to

which is a cdf of the variate and a location parameter (c.f. eq. (35)). The above reasoning can be summarized as

Theorem 1

A sampling distribution for a continuous variate , given a continuous parameter , with both its form and its domain being invariant under a Lie group , is necessarily reducible (by separate transformations and ) to a sampling distribution for with the parameter being a location parameter.

For example, a pdf for (37) with being a scale parameter and with the location parameter being fixed to zero, is invariant under the group of scale transformations (45). Then, according to (47) and (48), and read:

which, in order to reduce the example to the problem inference about a location parameter , implies the appropriate transformations of the variate and the parameter :

Indeed, this is in perfect agreement with equation (38) of Section 4.

In the following two sections we will see that the invariance of sampling distributions is indispensable when constructing a logically consistent theory of inference about parameters.

6 Consistency Theorem

Suppose that before we received the first evidence, , we had been completely ignorant about the value of the parameter that determines the probability distribution for . We had only known the type of sampling distribution for and the permissible range of the parameter. Let the probability for taking the value in a discrete case, or taking the value in the interval in a continuous case, be denoted by :

| (54) |

In this section we prove the following proposition, henceforth referred to as the Consistency Theorem:

Theorem 2

In order to meet the consistency Desideratum, the pdf for based on only, must be directly proportional to the likelihood (54).

Proof. After having made the first observation, we know the type of sampling distribution and the values of . Therefore, the pdf for given evidence will be proportional to a function ,

| (55) |

whose form we would like to determine. The denominator is just a normalization constant due to (21),

| (56) |

and contains no information about .

Let now be another piece of evidence, independent of , that we would like to include in our inference about . Since is independent of , and subject to the same probability distribution (54) as , its likelihood reads:

In the first section we saw that the only consistent way of updating pdf for is the one in accordance with Bayes’ Theorem (29). With taking the role of the prior pdf for , the pdf posterior to including into our reasoning about is written as:

| (57) |

with the normalization constant being

Nothing prevents us from reversing the order of taking the two pieces of information, and , into account, which results in the following pdf for :

| (58) |

with the appropriate normalization constant ,

Moreover, the consistency Desideratum III.a requires equality of the two results, (57) and (58):

or

| (59) |

The ratio of eq. (59) and its derivative with respect to yields

| (60) |

where we use the notation

Evidently, in order to ensure equality in (60) for all possible values of and , the left and the right side of the equation must be independent of and , respectively, but can depend on the value of the parameter .

Note that at this point, the two sides of equation (60) can, in principle, also depend on the values , , and , determining the admissible ranges of the sampling variate and of the parameter. However, in the following sections we will see that in all problems of parameter inference that can be consistently solved, there is no such explicit dependence.

Taking this dependence into account by introducing a function we obtain

and, after integration of the latter,

| (61) |

where is a consistency factor,

| (62) |

and an arbitrary integration constant. That is, the consistency factor is determined only up to an arbitrary constant factor.

The consistency factor is differentiable by construction. From the form of (62) it is also obvious that if is chosen to be positive, is positive for every defined. Consequently, the normalization factor ,

being an integral of a product of positive factors (61), is also a strictly positive quantity for every defined.

By inserting the solution (61) into (55), we can finally write:

| (63) |

which completes the proof of the Consistency Theorem.

The result is valid for being the likelihood of either a discrete or dense variable . For the latter, the Consistency Theorem can be rewritten by replacing the likelihood with the appropriate likelihood density, ,

| (64) |

where is the corresponding normalization factor,

| (65) |

Evidently, the normalization constant is also determined up to a constant factor , i.e., the consistency factor and the normalization factor are determined up to the same factor.

Similarly, in terms of posterior probabilities and likelihoods instead of the corresponding densities, the Theorem reads:

| (66) |

The form of the Consistency Theorem (66) reminds very much of that of Bayes’ Theorem (25). In both cases, within a specified model, the complete information about the inferred parameter of the model that can be extracted from a measurement , is contained in the value of the appropriate likelihood, . But there is also a fundamental and very important difference between the two Theorems: while in Bayes’ Theorem represents the pdf for prior to including evidence in our inference about , the consistency factor in the Consistency Theorem is just a proportionality coefficient between the pdf for and the likelihood function. The form of the factor depends on the only relevant information that we possess before the first datum is collected, i.e. it depends on the specified sampling model.

In Section 15 we comment on how overlooking this difference led to a long-lasting confusion in plausible reasoning. Before that we show under what conditions the factors can be consistently determined, and uniquely determine them for such cases by following the basic Desiderata.

7 Objective inference and equivalence of information

According to the definition of probability adopted in the first section, every assigned probability is necessarily subjective: no probability distribution can be assigned independently of the experience of the person who is expressing his or her degree of belief. In the words of Bruno de Finetti ([23], Preface, p. x): “Probability does not exist”, meaning that there is no probability per se. For example, when there is not enough relevant information at our disposal, we are simply not in a position to make any probabilistic inferences. That is, even when lacking, information should never be confused with our hopes, fears, value judgments, etc. Since no matter how carefully these are specified, they still represent mere personal biases, prejudices and speculations.

The general Desiderata represent the rules that we have to obey in order to preserve consistency of inference, so it is evident that the adjective subjective does not stand for arbitrary. In fact, in accordance with Desideratum III.c, our goal is that inferences are to be completely objective in the sense that if in two problems the state of knowledge of a person making the inference is the same, then he or she must assign the same probabilities in both. The goal of the present and the following sections is to show when and how information about the specified model and its domain, within the framework of our basic Desiderata (i.e without any additional ad hoc assumptions), uniquely determine the form of consistency factors, the latter being indispensable at the starting point of any parameter inference. Within the Desiderata, only III.a and III.c directly consider equalities of probabilities and can thus provide equations that could determine the form of consistency factors. Since the requirements of Desideratum III.a were extensively exploited already throughout the previous section when the Consistency Theorem was derived, it is only III.c that is left at our disposal to obtain the desired functional equation for .

Let

be a sampling pdf for whose parameter we would like to infer. We saw in the preceding section that in the case when this can be done in a consistent way, the pdf for must take the form:

| (67) |

where is the usual normalization factor

| (68) |

Equation (67) with the unknown pdf clearly does not determine uniquely the form of the consistency factors: as long as the normalization integral (68) exists, can be any positive and differentiable function of . Additional constraints (functional equations) are therefore needed to reduce all these functions to a single consistent function, i.e. to the only function that is consistent with our Desiderata.

In the case there exists a group of transformations of the sample space such that , the above pdf for can be expressed as

where

Let there also exist a group of transformations of the parameter space, . We saw already in Section 2 that, according to objectivity Desideratum III.c, the assigned probabilities must be invariant under variate transformations. This is assured if the pdf’s of the original and the transformed variate, and , are related via (16) and (17), so that the pdf for , given a measured , reads:

That is, in order to assign equal probabilities in states of equal knowledge, the pdf for must take the form:

| (69) |

where:

| (70) |

and, for ,

| (71) |

while for the limits of the above integral are to be interchanged444Index in and denotes particular elements of transformation groups, while in and it indicates the lower bounds of the sample and parameter space, respectively.. Note that in general the value of the multiplication constant , up to which the consistency and the normalization factors, (62) and (65), are to be uniquely determined (recall the preceding section), may depend on the value of the transformation parameter .

Equation (69) represents a constraint on consistency factors that is additional to (67), but it also introduces an additional unknown variable, function . For invariant sampling distributions, however, it is easy to demonstrate that the form of the consistency factor must also be invariant under the induced group , i.e. that and must be the same functions. Namely, the forms of consistency factors and depend on information and that we possess about and , respectively, prior to collecting datum : on the forms and domains of sampling distributions, and . In the case where all of these are invariant under particular transformations and :

- a)

-

- b)

-

and

- c)

-

the information equals information and the two consistency factors, and , must be the same functions:

| (72) |

When combined with (70), this implies:

| (73) |

The above functional equation for is the cornerstone of the entire theory of consistent assignment of probabilities to parameters of sampling distributions:

Conjecture 1

Equation (73) is the only functional equation within the basic Desiderata that can be used for determination of consistency factors.

The proof of this conjecture represents an open problem that is still to be solved. It is a serious problem, though, since any additional functional equations for , independent of (73), with solutions different from solutions of (73), would most seriously jeopardize the consistency of the entire probabilistic approach to inferences about the parameters of sampling distributions.

Be that as it may, equation (73) is the only functional equation that we know of that can be used for determination of consistency factors if we want to rely exclusively on our basic Desiderata. All other procedures for determination of (of non-informative prior ’probability’ distributions; see Section 15) that we are aware of involve applications of some additional ad hoc assumptions so that there is absolutely no guarantee that reasonings of such a kind be consistent. Further arguments and examples, supporting the above conjecture by exhibiting the decisive role of the invariance of sampling distributions under group transformations in the process of determination of the consistency factors, are presented in Sections 11, 12, 14 and 15, and in Appendix B.

In case of a two-parametric induced group of parameter transformations , the functional equation for the consistency factor for the inferred parameters and reads:

| (74) |

where stands for the appropriate Jacobian

We will come across functional equation (74) in Section 10, during a simultaneous inference about a location and a scale parameter.

Under what circumstances does a unique solution of the functional equation (73) exist? Let us consider the problem with a sampling distribution being invariant under a discrete group of transformations

| (76) |

where can only take two values,

for both groups, and . That is, the considered distribution possesses parity under simultaneous inversion of sampling and parameter space coordinates. Then, for , functional equation (73) reads:

or, after an inversion ,

Multiplying the two equations yields:

which, when the convention about being positive is invoked, further implies

| (77) |

That is, the consistency factor that corresponds to a sampling distribution being invariant under simultaneous inversions of sampling and parameter space coordinates, must itself possess parity under inversion of parameter space coordinates. But apart from this it can take any form and so in this case the solution of (73) is clearly not unique. It is not difficult to understand that this is a common feature of all solutions based on invariance of the sampling distributions under discrete groups. If the symmetry group is discrete, the sample and the parameter spaces break up in intervals with no connections in terms of group transformations within the points of the same interval. We are then free to choose the form of in one of these intervals (e.g. we can choose for the positive values of in the above example), so it is evident that it is impossible to determine uniquely the form of consistency factors for problems that are invariant only under discrete groups of transformations.

It turns out, however, that for sampling distributions that are invariant under Lie groups, functional equation (73) uniquely determines the form of the corresponding consistency factors. But according to the Existence Theorem of Section 5, the invariance of a sampling distribution under a Lie group is found only when the parameter of the distribution is reducible to a location parameter by one-to-one transformations of both the parameter and the sampling variate. It is therefore sufficient to determine the form of consistency factors for location parameters, which is accomplished in the following three sections.

8 Location parameters

We saw in Section 5 that a sampling distribution, parameterized by a location parameter and by a fixed dispersion parameter , is invariant under the group of translations (44). In such a case the functional equation (73) for reads:

| (78) |

After its differentiation with respect to ,

we set and obtain a simple differential equation with separable variables and ,

| (79) |

with the constant being defined as

The general solution of (79) reads

where is an integration constant. Since all multiplication constants can be put into , we can assume without any loss of generality that , obtaining in this way the general form of the consistency factor for location parameters:

| (80) |

For sampling distributions, symmetric under simultaneous inversions of the sampling and the parameter space, equation (77) implies , i.e. implies uniform consistency factors for location parameters. By invoking the symmetry of the problems of simultaneous inference about a location and a scale parameter in Section 10, we show that further applications of the basic Desiderata and their direct implications also require in the case of problems without space-inversion symmetry.

Based on a measured value , the pdf for a location parameter therefore reads:

| (81) |

Now, as an example, we want to update our inference about the parameter by including additional information in our inference, where is a result of a measurement of that is also subject to the same sampling distribution and independent of . We can write the likelihood density for ,

| (82) |

and the updated pdf for ,

| (83) |

with the appropriate normalization constant, , being:

| (84) |

The update (83) is made in accordance with Bayes’ theorem (29) with the purpose of ensuring our reasoning be consistent.

The product of the likelihood densities and in (83) is equal to the combined likelihood density for the two independent events, and , due to the product rule (9). According to (32), the likelihood density can equivalently be represented by the density for and , , where

| (85) |

Written in terms of the pdf for (83) thus reads:

| (86) |

with the appropriate normalization constant ,

| (87) |

The findings of the present example will become of particular importance in Section 10 where we determine the form of the consistency factor for simultaneous estimation of a location and a dispersion parameter.

9 Inference about scale and dispersion parameters

When, contrary to the preceding section, the inferred dispersion (or scale) parameter is unknown and the location parameter is fixed to , the problem is invariant under the group (45) of scale transformations. In such a case the functional equation (73) for reads:

| (88) |

where

Equation (88) determines the form of the consistency factor for dispersion and scale parameters to be

| (89) |

and

| (90) |

where the value of the constant ,

is yet to be determined in Section 10.

We stressed in Section 4 (c.f. equation (38)) that an assignment of a pdf to a scale parameter (or, equivalently, to a dispersion parameter of a symmetric distribution) can be reduced to an assignment of a pdf, , to a location parameter, :

with

and with being a fixed dispersion parameter. According to the findings of the previous section (see eq. (80)), we can immediately write the appropriate consistency factor:

Making use of eq. (17), the pdf for can be transformed into the pdf for :

| (91) |

where

On the other hand, in order to make a consistent inference, the pdf for , , based on only, must be proportional to the likelihood density (see eq. (64)):

| (92) |

Then, due to Desideratum III.a, the two pdf’s, (91) and (92), must be equal, which implies the form of the consistency factors for scale parameters,

| (93) |

as well as for dispersion parameters,

| (94) |

The same Desideratum implies equality of the factors (89) and (94), as well as equality of the factors (90) and (93), i.e. implies the relation

| (95) |

between the parameters and of the consistency factors of the location and scale parameters. Evidently, if is determined to be zero, this would immediately imply .

In the limit of complete prior ignorance about its value, the pdf for given a measured value and the fixed value of therefore reads:

Following the steps of the example of the preceding section, we update the pdf for by including result of an additional measurement in our inference. The updated value of the pdf reads:

with the normalization constant ,

| (96) |

In an analogy with (86) and (87), both the updated pdf for and the corresponding normalization constant can be expressed in terms of and (85), instead of and :

| (97) |

and

| (98) |

10 Simultaneous inference about a location and a dispersion parameter

By fixing neither the location nor the dispersion parameter, an inference about the two parameters is invariant under a simultaneous location and scale transformation (43). The symmetry of the problem implies the following form of the functional equation (74) for the appropriate consistency and normalization factors:

| (99) |

where

In order to solve it, we differentiate equation (99) separately with respect to and , set afterward and , and obtain:

| (100) | |||||

| (101) |

with the constants and being defined as

The general solution of differential functional equation (101) is a function of the form

| (102) |

where is a non-negative function of . When inserted in (100), (102) yields:

which, if it is to be true for all and , further implies and

so that the general form of the consistency factor reads:

| (103) |

where we put all possible multiplication constants in the normalization factor:

| (104) |

Now there is only one step dividing us from a complete determination of consistency factors for location, scale and dispersion parameters. Having established the form (103) of the consistency factor , we can write down a pdf for and given and :

| (105) |

According to the product rule (9), the pdf can also be written as

| (106) |

where is a marginal pdf (see equation (23)):

| (107) |

Then, combination of equations (86-87) and (105-107) leads to:

solvable for any value of if and only if

| (108) |

where is the constant of the consistency factor for location parameters (80). Due to the simple relation (95) between the constant of the consistency factor for the location parameters and the constant of the factors for the scale and dispersion parameters, the above solution also implies

| (109) |

These are highly nontrivial results since they uniquely determine the consistency factors for the location, dispersion and scale parameters (recall eqns. (80), (89) and (90)):

| (110) | |||||

In addition, in order to determine also the value of the constant of the consistency factor (103), we recall that apart from (106), the product rule (9) also allows for the pdf (105) to be written as:

| (111) |

where the marginal distribution now stands for

| (112) |

while the pdf for given , , equals the pdf (97):

| (113) |

Equations (105) and (111-113) combined yield:

with being determined (109) to be 1. Evidently, the solution of the above equation reads:

which finally determines the consistency factor for a symmetric sampling distribution (see eq. (103)),

| (114) |

Now we would like to make use of results obtained in this and preceding sections and address the so-called problem of two means (i.e. two location parameters), also referred to as the Fisher-Behrens problem (see refs. [24] and [25], and § 19.47, pp. 160-162, § 19.48, p. 164 and § 26.28-26.29, pp. 441-442 in ref. [20]). Imagine and being independent quantities, both being subject to Gaussian sampling distributions,

and

with parameters of both distributions being unknown and unconstrained.

After collecting two events, and , from

each of the two samples, we are in a position to make a probabilistic

inference about the unknown parameters. The pdf’s for

and read:

(115)

and

(116)

where

and

Since the two pdf’s are independent, we apply the product rule (9) and write down a pdf for , , and as a product of pdf’s (115) and (116):

By integrating out parameters and we find the marginal pdf for and to be of the form:

Note that the above results were all obtained simply by using some of the applications of basic Desiderata without making any additional assumptions or requiring any new postulates (compare to references [26] and [20], § 26.29, p. 442). We refer to the Fisher-Behrens problem again in Section 15 when we comment on difficulties with inferences about parameters outside the framework of probability.

11 On uniqueness of consistency factors and on consistency of basic rules

In previous sections we saw that the general rules for plausible reasoning - the Cox-Pólya-Jaynes Desiderata - uniquely determine the consistency factors for location, scale and dispersion parameters. In other words, in the limit of complete prior ignorance, there is only one possible way of making a consistent inference about the three types of parameters. According to (63), the pdf, assigned to one or to several of these parameters simultaneously, is to be proportional to the likelihood function, containing the information from one or several measured events that are subject to the distribution determined by the inferred parameter(s), and to the appropriate consistency factor as determined at the end of the preceding section.

Anyone who possesses the same information, but assigns a different probability distribution to a given parameter , e.g. by choosing a ’consistency factor’ of a different form, thus necessarily violates at least one of our basic Desiderata. It is certainly true that nobody has the authority to forbid such violations, but, at the same time, it is also true that anyone coming to the conclusions by violating such basic and general rules being would surely have difficulties in persuading anyone else, who was aware of these violations, to accept his conclusions.

In Section 7 we stressed that a prior information in a problem of inference about a parameter of a sampling distribution, , is equal to corresponding information about an inferred parameter of the sampling distribution for , , only if three requirements are simultaneously met: a) if the sampling distribution is invariant under transformations and , b) if the permissible range of sampling variate , is invariant under , and c) if the permissible range of the inferred parameter , is invariant under transformation . Evidently, for the ranges of parameters and , and the corresponding transformations (43-45), the condition c) is well fulfilled for all and .

But, in practice, we usually face problems with pre-constrained inferred parameters: we possess some additional information that narrows the admissible range. As a simple example, when we are estimating the average lifetime of a newly discovered particle, produced in an experiment with highly energetic protons from an accelerator hitting a fixed target, it is easy to imagine that cannot really be infinite, for in that case there should be many of these particles around as remnants of the Big Bang. In fact, it might well be reasoned that is necessarily even much smaller than billions of years, since in case of being sufficiently large, e.g. of the order of a millisecond, we should have noticed the particles as products of cosmic protons hitting nuclei in the upper layers of the Earth’s atmosphere. The listed two arguments, as well as any possible additional ones, thus lead to a finite interval in the positive half of the real axis. But such an interval is clearly not invariant under parameter transformation and so the above condition c) for the equality of information, , is not fulfilled. How shall we proceed in such cases?

Suppose for a moment that we ignore the fact that the condition c) is not fulfilled. Effectively this is equivalent to a prescription that can often be found in textbooks on the so-called Bayesian inference: to use the same function as in the case of no constraints on the parameter range, and afterwards to chop-off the unconstrained pdf for the inferred parameter, , outside the interval and renormalize the truncated distribution (see, for example, [16], § 3.17, pp. 72-73). It is easy to show that in general such an ad hoc prescription inevitably leads to inconsistencies.

Namely, without the constraints on , in equation (70) is to equal , and consequently is to equal . Then, (70) implies

so the functional equation (75) for the normalization factor reads:

| (117) |

By setting we realize that and are to be the same functions,

| (118) |

or, equivalently,

| (119) |

When inserted in (117), (119) yields

| (120) |

which must be true for any . For (120) thus reads:

| (121) |

On the other hand, by definition (71), should ensure normalization of the pdf for :

| (122) |

Evidently, the equality (118) is assured for all only if

i.e. only if the invariance of the parameter range under the particular group of transformations is exact.

In practice, our reasoning would still be sufficiently consistent if

| (123) |

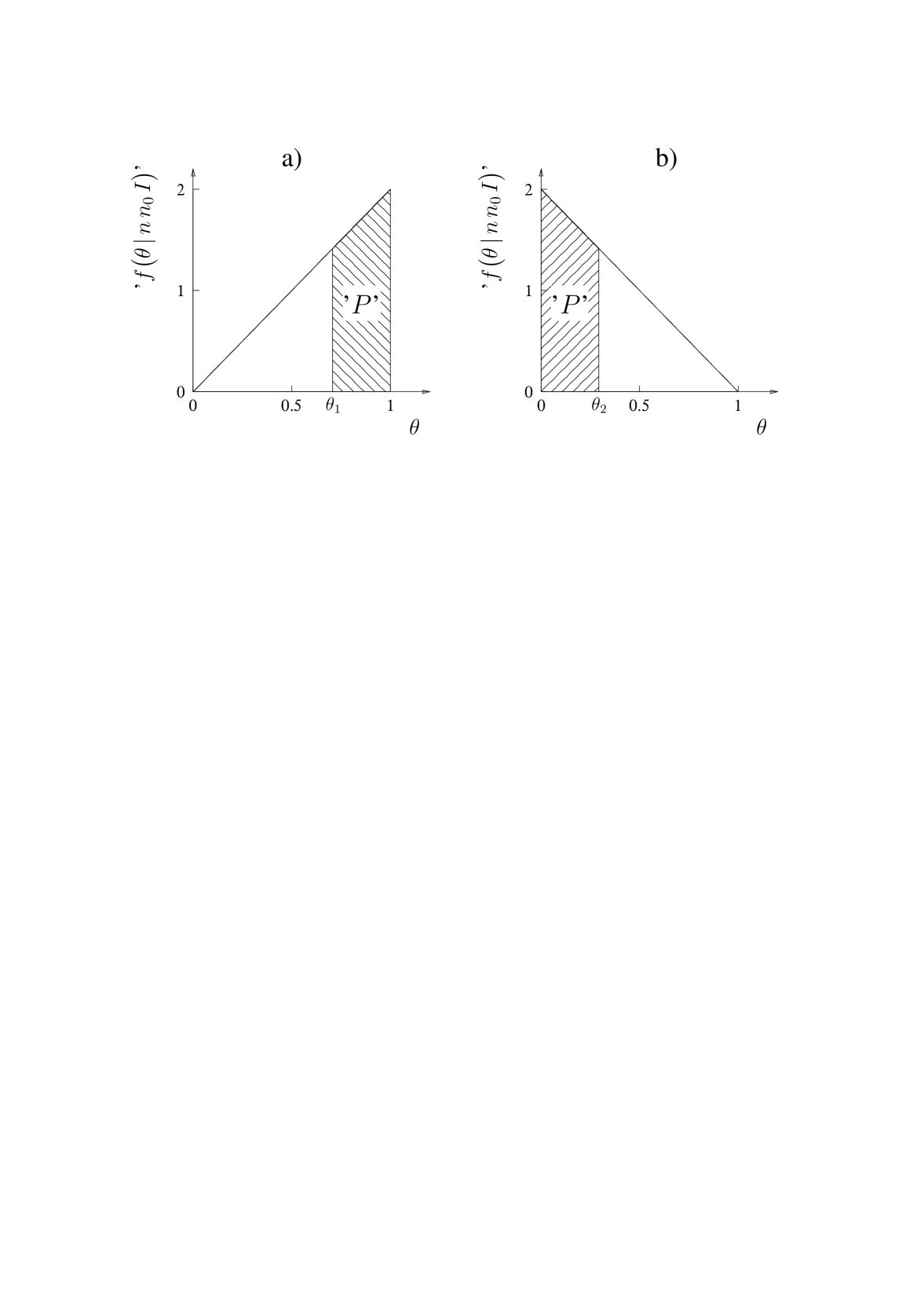

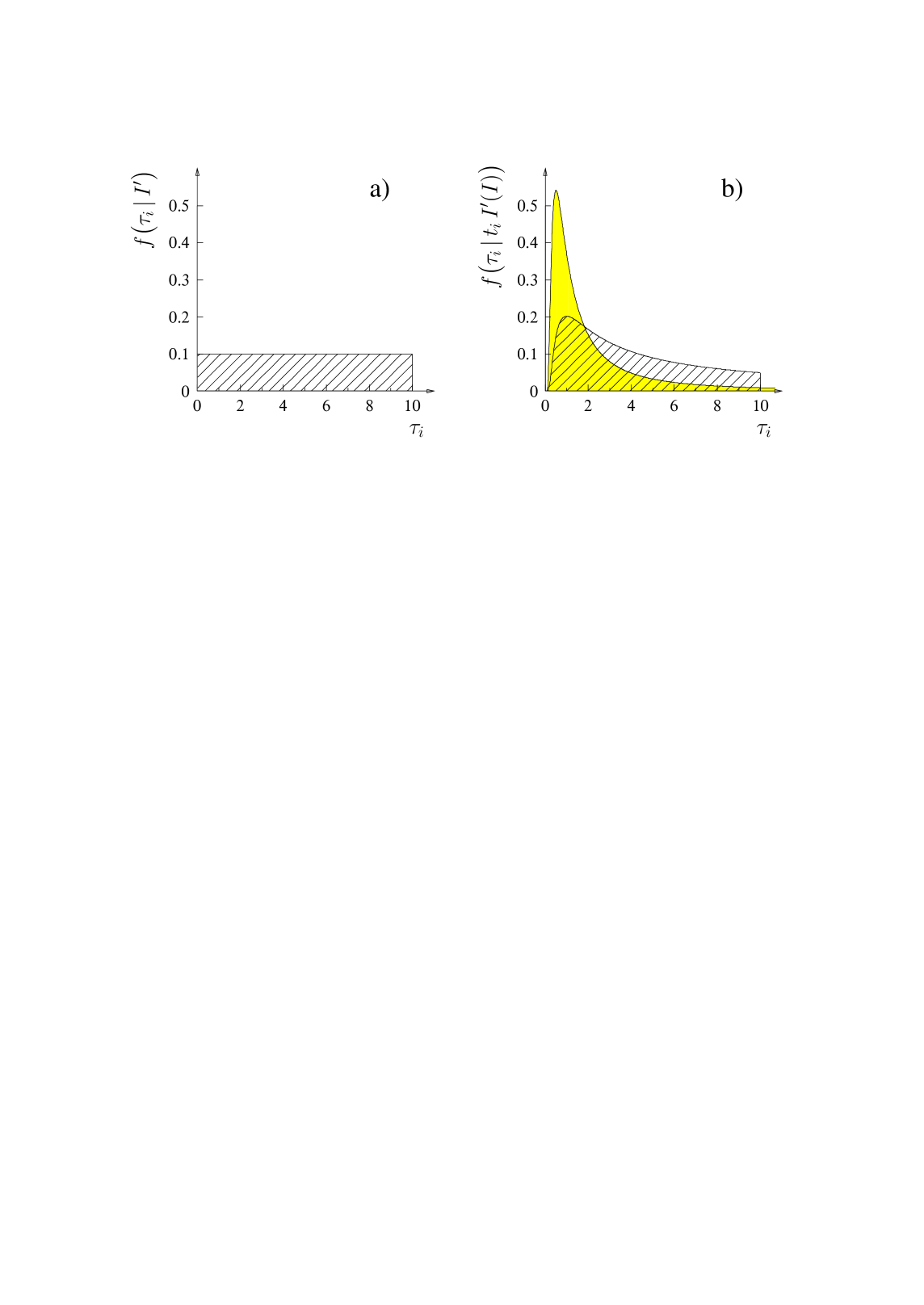

i.e. if the integrals and of the unconstrained pdf for outside the allowed region (see Figure 1),

| (124) |

are sufficiently small.

That is, if the conditions (123) are fulfilled, normalization factors (121) and (122) are equal beyond the precision required for the particular inference. As admitted above, the invariance of the admissible parameter range, and consequently also the consistency of our reasoning, is not exact in such a case since for extremely large or extremely small values of measured decay times the equality (117) would not hold. But once has been recorded, it is very likely that the value of the inferred would also be of the same order of magnitude, i.e. it would be extremely unlikely for to be much smaller or much larger than . Then, with , it is also very unlikely that we would ever observe an event orders of magnitude different from .

On the other hand, if the conditions (123) are not fulfilled (see, for example, Figure 1.a), our reasoning is clearly not consistent: by applying the two equally valid normalization factors, (121) and (122), we are able to arrive at significantly different probabilities for the same proposition, e.g. , which is in direct contradiction with the consistency Desideratum III.a. The additional information that narrows the interval may still be very useful, but it is just that consistent probabilistic reasoning is impossible in such a situation.

In order to avoid such an inconsistency, we could have ignored the information, additional to , and stretched to the whole positive half of the real axis. But this is not a solution either, since in this way we would have been arbitrarily ignoring some of the available information and basing our conclusions on what remains. Acting in explicit contradiction with Desideratum III.b, we would have allowed ideology to break into our inference, which is inadmissible for any scientifically respectable reasoning.

Thus, the only consistent solution to our problem of inference about the pre-constrained parameter would be provided by recording additional independent decay times,, of particles of the same type. Then, the unconstrained probability distribution for , based on the recorded data, is described by the following pdf:

where is an average of the recorded decay times:

The distribution narrows as increases (see Figure 1.b). Therefore, by collecting enough data, the inconsistency is diminished beyond the required level: by diminishing the integrals and of the unconstrained pdf for outside the constrained domain, the limits and that caused the inconsistencies become irrelevant.

Our theory of consistent inference about parameters is therefore valid only if certain conditions are fulfilled, i.e. in the limit . Such a theory is referred to as an effective theory, with the term coming from physics where all theories are effective. The precision of predictions of an effective theory is estimated by the proximity of the actual conditions to the ideal limit. The values of integrals (124), compared to zero, can thus serve as an estimate of the precision of our probabilistic inference about the pre-constrained parameters.

12 Calibration

The most striking achievement of the physical sciences is prediction.

Georg Pólya ([4], Chapter XIV, § 4, p. 64)

Thus far our theory of plausible inference about parameters has been developed by following Desiderata I.-III. only, while the implications of the operational Desideratum have not yet been considered. According to the latter Desideratum, in order to exceed the level of a mere speculation, our theory of inference about parameters must be exposed, i.e. must be able to make predictions that can be verified by experiments. The magnitudes considered by physicists such as mass, electric charge or reaction velocity have an operational definition: the physicist knows very well which operations he or she has to perform if he or she wishes to ascertain the magnitude of an electric charge, for example ([4], Chapter XV, § 4, p. 117). Is there a way for probability as a measure of a personal degree of belief to become operational, too?