Ab Initio Yield Curve Dynamics

Abstract

We derive an equation of motion for interest-rate yield curves by applying a minimum Fisher information variational approach to the implied probability density. By construction, solutions to the equation of motion recover observed bond prices. More significantly, the form of the resulting equation explains the success of the Nelson Siegel approach to fitting static yield curves and the empirically observed modal structure of yield curves. A practical numerical implementation of this equation of motion is found by using the Karhunen-Lòeve expansion and Galerkin’s method to formulate a reduced-order model of yield curve dynamics.

keywords:

Bond, interest rate, dynamics, Fisher information, yield curve, term structure, principal-component analysis, proper orthogonal decomposition, Karhunen-Lòeve, Galerkin, Fokker-Planck.PACS:

89.65.Gh , 89.70.+c, and ††thanks: We thank Prof. Ewan Wright for helpful discussions and encouragement. Yield curves are remarkable in that the fluctuations of these structures can be explained largely by a few modes and that the shape of these modes is largely independent of the market of origin: a combination of parsimony and explanatory power rarely seen in financial economics. While these modes play a fundamental role in fixed-income analysis and risk management, both the origin of this modal structure and the relationship between this modal structure and a formal description of yield curve dynamics remain unclear. The purpose of this letter is to show that this modal structure is a natural consequence of the information structure of the yield curve and that this information structure, in turn, implies an equation of motion for yield curve dynamics.

Our application of Fisher information to yield curve dynamics is an extension of prior work [1, 2, 3] using this approach to derive equations of motion in physics and static probability densities in asset pricing theory111The relationship between Fisher information and related approaches such as maximum entropy [4] and minimum local cross entropy [5] in the context of financial economics is discussed in [3].. Though less well known as a measure of information in physics and mathematical finance than Shannon entropy, the concept of Fisher information predates Shannon’s and other information statistics, and remains central to the field of statistical measurement theory [6]. Fundamentally, it provides a representation of the amount of information in the results of experimental measurements of an unknown parameter of a stochastic system. Fisher information appears most famously in the Cramer-Rao inequality that defines the lower bound on variance/upper bound on efficiency of a parameter estimate given a parameter dependent stochastic process. It also provides the basis for a comprehensive alternative approach to the derivation of probability laws in physics and other sciences [1, 2, 7].

In the present work, the aim of our approach is to derive a differential equation for yield curve dynamics, ab initio, with the minimal imposition of prior assumption, save that bond price observations exist, and that a stochastic process underlies the dynamics. In a sense our approach is an inversion of the perspective of a maximum likelihood estimate, where one would solve for the most likely parameter values given observations within the context of a pre-assumed model. Here we apply “minimum presumption” by deriving the stochastic model that is implied by minimizing Fisher information given known parameter measurements (bond prices).

A yield curve is a representation of the rate of interest paid by a fixed-income investment, such as a bond, as a function of the length of time of that investment. The interest rate over a given time interval, between say today and a point of time in the future, determines the value at the beginning of the time interval of a cash flow to be paid at the end of the interval; also known as the present value of the cash flow. Since the value of any security is the present value of all future cash flows, yield curve fluctuations give rise to fluctuations in present value and, thus, play an important role in the variance of security prices.

The notion that a modal structure underlies yield curve dynamics comes from common empirical experience with two related yield-curve measurements - the construction of static yield curves from observed market prices and the analysis of correlations between corresponding points in the time evolution of successive static yield curves. Yield curves are inferred from observed fixed-income security prices and as the prices of these securities change over time so does the yield curve. Yield curves are usually generated after the close of each trading session and this process can therefore be viewed as a stroboscopic measurement of the yield curve. Yield curves can assume a variety of shapes and many methods have been proposed for their construction222See, for example, [8] and references therein.. Of these methods, the Nelson Siegel approach [9] of representing yield curves as solutions of differential equations has gained wide acceptance in the finance industry [10] and in academic research on yield-curve structure [11, 12, 13, 14, 15]. In using a second-order differential equation to represent the yield curve the Nelson Siegel approach is essentially a proposal that yield curves can be represented effectively by a modal expansion and the practical success of this approach to yield curve fitting in markets around the world is a measure of the correctness of this assertion.

The modal structure of the yield curve is also implied in the eigenstructure of the two-point correlation function constructed from yield curves. Specifically, diagonalization of the covariance matrix of yield changes along the yield curve produces an eigenstructure where most of the variance - as measured by summing the normalized eigenvalues - is explained by the first few eigenmodes [16, 17, 18]. The consistency of the general shape of the eigenmodes derived from empirical yield curve data and the explanatory power of the truncated expansions in those eigenmodes is surprisingly robust over time and largely independent of the country in which the interest rates are set [19, 20, 21]. While this analysis motivated the use of yield-curve modes by fixed-income strategists and risk managers some time ago, an explicit link between yield-curve modes and dynamics appeared in comparatively recently research demonstrating the eigenstructure to be consistent with both the existence of a line tension along the yield curve and a diffusion-like equation of motion for yield curves [22]. This notion of a line tension along the yield curve has found further expression in descriptions of the yield curve as a vibrating string [23]. While the yield curve phenomenology just described can be described well by modal expansions there as been little to motivate why this should be the case and it is to this question that we now turn.

We begin with a more formal description of the notion of present value mentioned above. The yield curve is closely related to the function known as the discount function that gives the value at time (i.e. the present value) of a unit of currency (e.g. dollar) to be paid at time in the future

| (1) |

where is the “spot rate” yield curve at time t, specifying the continuously compounded interest rate for borrowing over the period , and is known as the “forward rate” yield curve at time t, specifying the interest rate for instantaneous borrowing over .

Our explanation for the existence of dynamic yield-curve modes builds on our recent application of Fisher information methods [2, 3] to the construction of well-mannered, static yield curves from a finite set of discount functions or observed bond prices. Our approach, based on deriving yield curves that extremize Fisher information, is facilitated by associating such yield curves with complementary probability density functions where the time to maturity is taken to be an abstract random variable [24, 25]. We assume the associated probability density satisfies and is related to the discount factor via

| (2) |

Discount factors are, however, not always observable. Coupon bonds, on the other hand, are commonly available with prices related to the discount factor by

| (3) |

where indicates the number of remaining coupon payments and is the cash flow at time in the future. For a typical coupon bond is equal to the coupon payment for and equal to the final coupon payment plus the principal payment for .

In these expressions one can see that discount factors and bond prices share a common structure as averages of known functions. Discount factors are the average of and coupon bond prices are the average of where is the Heaviside step function. Generally, where observed data such as discount factors and the prices of bonds can be expressed as averages of known functions at a static point in time, we may write

| (4) |

and the probability density function implicit in the observed data can be obtained by forming a Lagrangian using Fisher information [26] in its shift-invariant form

| (5) |

Employing the usual variational approach we obtain [2]

| (6) | |||||

| (7) |

where the ’s are Lagrange multipliers that enter by incorporating a normalization constraint on () and observed data () into the Fisher information Lagrangian.

This is equivalent to an approximate use of the extreme physical information (EPI) approach [1, 2, 7] wherein the constraint equations (Eq. 4) are used in place of the fundamental source information J required by EPI. This replacement amounts to a technical (as compared with fundamental) approach to valuation.

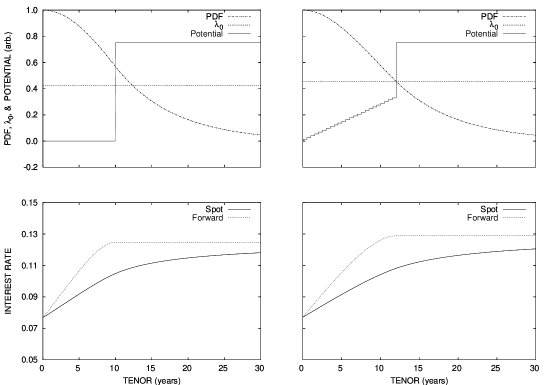

In a recent communication [3] we exploited the formal equivalence of Eq. 7 and the time-independent Schroedinger wave equation (SWE) to calculate the equilibrium densities implicit in security prices as shown in Fig. 1.

In the graphs on the left-hand side of Fig. 1 we see the results for a single discount factor with a price of 35% of par and a tenor of 10 years. The upper-left graph illustrates the elements of Eq. 2 with the potential term of the SWE () being a single step function. The amplitude of the potential well described by the step function, , the level of and the probability density function (PDF) , all follow from a self-consistent field calculation with the pair corresponding to the ground state of Eq. 7 subject to the constraint given by Eq. 2. The lower-left graph shows the spot and forward yield curves that follow from the PDF in the upper graph as defined by Eq. 1.

The results of this analysis for a 6.75% coupon bond making semi-annual payments with a maturity date of November 15, 2006, a price of 77.055% of par, and a pricing date of October 31, 1994 [27] are shown on the right-hand side of Fig. 1. The stepped structure of the potential function is a result of the cumulative sum of the coupon payments with the final large step being due to the principal payment. Unlike the discount factor, there is no analytic solution to Eq. 7 for the coupon bond. This type of potential is, however, ideally suited to the transfer matrix method of solution [28] and that is the approach we used to calculate the PDF solution shown in the upper-right graph. The calculation of a general yield curve from a collection of coupon bonds is a straightforward extension of this approach.

The general solution to the SWE with potentials of this form is commonly expressed as a series expansion of modes and these modes have been used to go beyond the equilibrium solutions illustrated in Fig. 1 to describe non-equilibrium phenomena in physics [29, 30, 31]. It is with these modes that the modal structure of the yield curve follows directly from the Fisher information structure of the yield curve (cf. Eq. 8 below). This result also provides an information-theoretic derivation of the Nelson Siegel approach. Of interest as well is the behavior of the solutions illustrated in Fig. 1 in the range of tenor where there are no observed security prices. The solution to Eq. 7 is known to be an exponential decay which leads to a constant interest rate: a result consistent with most priors concerning long-term interest rates.

The temporal evolution of yield curves now follows directly from the known relationship between solutions of Eq. 7 and those of the Fokker -Planck equation333Formally, the Fokker-Planck equation can be obtained from our Fisher Information based variational approach by incorporating a Lagrangian term enforcing the constraint that total probability density is conserved under time evolution [32].[33, 34]. Specifically, the solutions of Eq. 7 can be used to construct a general solution [33]

| (8) |

to the Fokker-Planck equation

| (9) |

where the potential function is related to the ground state via

| (10) |

Taken together, Eqs. 7 through 10 explain the existence of a modal structure of yield curves and provide a theoretical basis for the common ansatz that a diffusion process underlies interest-rate dynamics [8, 18, 35, 36].

There are a variety of ways to solve Eq. 8, but the observation that the the eigenstructure of the two-point correlation function is dominated by a few modes suggests that this infinite series can be reduced to a few terms using the Karhunen-Lòeve expansion444This approach appears under a variety of names including factor analysis, principal-component analysis, and proper orthogonal decomposition. together with the Galerkin approximation [37, 38, 39, 40]. Specifically, writing Eq. 8 in the slightly more general form where , substituting this into the Fokker-Planck equation written suggestively as , and projecting along the eigenfunctions one obtains

| (11) | |||||

| (12) |

Truncating the series expansion for at gives a Galerkin approximation of order [39] and this truncation is justified in our case because of the dominance to the two-point correlation function by a few modes.

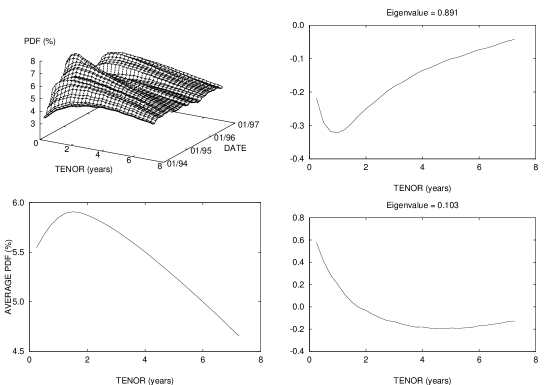

An example of applying this approach to the dynamics of the Eurodollar yield curve is illustrated in Fig. 2. The probability density function implicit in the Eurodollar futures market from the beginning of 1994 to the end of 1996 is shown in the upper-left panel of the figure and the average of these density functions is shown in the lower-left panel555The probability density function was obtained from constant-maturity Eurodollar futures prices as discussed in [22]. Using the method of snapshots [37] we obtained the eigenstructure shown partially in the two right-hand panels of Fig. 2. As the normalized eigenvalues indicate, more than 99% of the variance of this system is contained in the first two modes. Thus a Galerkin approximation of order 2 would be expected to provide an adequate representation of yield curve dynamics.

In summary, we have derived an equation of motion for yield curves that is consistent with observed statics and dynamics starting from the Fisher information of the probability density function that underlies the discount function. Our derivation leads to a Schroedinger wave equation for the probability amplitude of the density function underlying the discount factor and thus explains why solutions of equations of mathematical physics involving second-order tenor derivatives work so well as a representation of yield curves. This result also provides an explanation for the existence of a line-tension term in the equations of motion found in string models of yield curves. Using the well-known relationship between solutions of the Schroedinger wave equation and the Fokker-Planck equation we obtained an equation of motion for the yield curve consistent with the common ansatz that diffusion processes underly yield-curve dynamics. Since the eigenstructure of the yield-curve two-point correlation function is dominated by a few modes we found that a practical numerical solution to this equation of motion can be had by using the Karhunen-Lòeve expansion together with Galerkin’s method.

References

- [1] B. R. Frieden, Physics from Fisher Information, Cambridge University Press, Cambridge, 1998.

- [2] B. R. Frieden, Science from Fisher Information: A Unification, Cambridge University Press, Cambridge, 2004.

- [3] R. J. Hawkins, B. R. Frieden, Fisher information and equilibrium distributions in econophysics, Physics Letters A 322 (2004) 126–130.

- [4] E. T. Jaynes, Prior probabilities, IEEE Transactions on System Science and Cybernetics SSC-4 (1968) 227–241.

- [5] D. Edelman, The minimum local cross-entropy criterion for inferring risk-neutral price distributions from traded option prices, University College Dublin Graduate School of Business Centre for Financial Markets, Working Paper 2003-47, (2003).

- [6] S. Kullback, Information Theory and Statistics, Wiley, New York, 1959.

- [7] B. R. Frieden, B. H. Soffer, A critical comparison of three information-based approaches to physics, Foundations of Physics Letters 13 (2000) 89–96.

- [8] B. Tuckman, Fixed Income Securities: Tools for Today’s Markets, 2nd Edition, John Wiley & Sons, Hoboken, NJ, 2002.

- [9] C. R. Nelson, A. F. Siegel, Parsimonious modeling of yield curves, Journal of Business 60 (1987) 473–489.

- [10] Bank for International Settlements, Monetary and Economic Department, Basel, Switzerland, Zero-Coupon Yield Curves: Technical Documentation (1999).

- [11] L. Krippner, The OLP model of the yield curve: A new consistent cross-sectional and inter-temporal approach, Victoria University of Wellington, Unpublished Manuscript (2002).

- [12] F. X. Diebold, C. Li, Forecasting the term structure of government bond yields, PIER Working Paper 02-026, Penn Institute for Economic Research, Department of Economics, University of Pennsylvania (2002).

- [13] L. Krippner, Modelling the yield curve with orthonormalised Laguerre polynomials: An intertemporally consistent approach with an economic interpretation, University of Waikato Department of Economics, Working Paper in Economics 1/03 (2003).

- [14] L. Krippner, Modelling the yield curve with orthonormalised Laguerre polynomials: A consistent cross-sectional and inter-temporal approach, University of Waikato Department of Economics, Working Paper in Economics 2/03 (2003).

- [15] F. X. Diebold, G. D. Rudebusch, S. B. Aruoba, The macroeconomy and the yield curve: A nonstructural analysis, Federal Reserve Bank of San Francisco Working Paper 2003-18 (2003).

- [16] K. D. Garbade, Modes of fluctuation in bond yields - an analysis of principal components, Tech. Rep. 20, Bankers Trust Company, New York, N.Y. (1986).

- [17] R. Litterman, J. Scheinkman, Common factors affecting bond returns, Journal of Fixed Income (1991) 54–61.

- [18] K. D. Garbade, Fixed Income Analytics, 2nd Edition, MIT, Cambridge, MA, 1996.

- [19] K. D. Garbade, T. J. Urich, Modes of fluctuation in sovereign bond yield curves: An international comparison, Tech. Rep. 42, Bankers Trust Company, New York, N.Y. (1988).

- [20] W. Phoa, Advanced Fixed Income Analytics, Frank J. Fabozzi Associates, New Hope, PA, 1998.

- [21] W. Phoa, Yield curve risk factors: Domestic and global contexts, in: M. Lore, L. Borodovsky (Eds.), Professional’s Handbook of Financial Risk Management, Butterworth Heineman, Burlington, PA, 2000.

- [22] J.-P. Bouchaud, N. Sagna, R. Cont, N. El-Karoui, M. Potters, Phenomenology of the interest rate curve, Applied Mathematical Finance 6 (1999) 209–232.

- [23] P. Santa-Clara, D. Sornette, The dynamics of the forward rate curve with stochastic string shocks, Review of Financial Studies 14 (2001) 149–185.

- [24] D. C. Brody, L. P. Hughston, Interest rates and information geometry, Proc. R. Soc. Lond. A 457 (2001) 1343–1364.

- [25] D. C. Brody, L. P. Hughston, Entropy and information in the interest rate term structure, Quantitative Finance 2 (2002) 70–80.

- [26] R. A. Fisher, Theory of statistical estimation, Proceedings of the Cambridge Philosophical Society 22 (1925) 700–725.

- [27] V. Frishling, J. Yamamura, Fitting a smooth forward rate curve to coupon instruments, J. Fixed Income (1996) 97–103.

- [28] P. Yeh, A. Yariv, C. Hong, Electromagnetic propagation in periodic stratified media. I. General theory, Journal of the Optical Society of America 67 (1977) 423–438.

- [29] B. R. Frieden, A. Plastino, A. R. Plastino, B. H. Soffer, Schroedinger link between nonequilibrium thermodynamics and Fisher information, Physical Review E 66 (2002) 046128.

- [30] B. R. Frieden, A. Plastino, A. R. Plastino, B. H. Soffer, Non-equilibrium thermodynamics and Fisher information: An illustrative example, Physics Letters A 304 (2002) 73–78.

- [31] S. P. Flego, B. R. Frieden, A. Plastino, A. R. Plastino, B. H. Soffer, Nonequilibrium thermodynamics and Fisher information: Sound wave propagation in a dilute gas, Physical Review E 68 (2003) 016105.

- [32] M. Reginatto, F. Lengyel, The diffusion equation and the principle of minimum Fisher information, cond-mat/9910039 (1999).

- [33] N. G. van Kampen, A soluble model for diffusion in a bistable potential, Journal of Statistical Physics 17 (1977) 71–88.

- [34] H. Risken, The Fokker-Planck Equation: Methods of Solution and Applications, 2nd Edition, Vol. 18 of Springer Series in Synergetics, Springer-Verlag, New York, 1996.

- [35] R. Rebonato, Interest-Rate Option Models, John Wiley & Sons, Hoboken, NJ, 1998.

- [36] D. Brigo, F. Mercurio, Interest Rate Models: Theory and Practice, Springer-Verlag, Berlin, 2001.

- [37] L. Sirovich, Turbulence and the dynamics of coherent structures part I: Coherent structures, Quarterly of Applied Mathematics XLV (1987) 561–571.

- [38] L. Sirovich, Turbulence and the dynamics of coherent structures part II: Symmetries and transformations, Quarterly of Applied Mathematics XLV (1987) 573–582.

- [39] L. Sirovich, Turbulence and the dynamics of coherent structures part III: Dynamics and scaling, Quarterly of Applied Mathematics XLV (1987) 583–590.

- [40] K. S. Breuer, L. Sirovich, The use of the Karhunen-Lòeve procedure for the calculation of linear eigenfunctions, Journal of Computational Physics 96 (1991) 277–296.