We discuss various analytic and numerical methods that have been used to get option prices within a framework of the VG model. We show that some popular methods, for instance, Carr-Madan’s FFT method [1] could blow up for certain values of the model parameters even for an European vanilla option. Alternative methods - one originally proposed by Lewis, and Black-Scholes-wise method are considered that seem to work fine for any value of the VG parameters. Test examples are given to demonstrate efficiency of these methods. Convergency of all methods is also discussed.

Rutgers University, New Jersey,

Department of mathematics

aitkin@math.rutgers.edu

1 Introduction

This paper summarizes some results of work originally initiated by

Peter Carr. It supposes to investigate various numerical and

analytical methods of option pricing using VG model in order to find

out which algorithm is most efficient.

Let us first give a brief overview of the VG model. The Variance Gamma

(VG for short) process was proposed by Madan and Seneta (see

[MadanSeneta1990]) to describe stock price dynamics instead of the

Brownian motion in the original Black-Scholes model. Two new

parameters: skewness and kurtosis are introduced in

order to describe asymmetry and fat tails of real life distributions.

The VG process is defined by evaluating Brownian motion with drift at a

random time specified by gamma process. In other words, the VG model

with parameter vector assumes that the forward

price satisfies the following equation

(1)

where

(2)

and is a Gamma process playing the role of

time in this case with unit mean rate and density function given by

The probability density function for the VG process may be written as

(4)

or after integration over

(5)

where is the modified Bessel function of the second kind. The

characteristic function for the VG

process has remarkably simple form

(6)

Another derivation of this expression could be obtained when

conditioning on time change like in Romano-Touzi for stochastic

volatility models

(7)

(8)

Now, to prevent arbitrage, we need be a martingale, and, since

is already an independent increment process, all we need is

(9)

or

(10)

This tells us that

(11)

Note that from the definition of above, in order to have a

risk neutral measure for VG model, its parameters must obey an

inequality:

(12)

Note that risk neutral parameters do not have

to be equal to their statistical counterparts.

Accordingly, the characteristic function of the VG process is

(13)

Statistical parameters of VG distribution may be calculated from the

historical data on stock prices. In particular we have to find the

values of the parameters and such that

the folloiwng expression is maximized:

(14)

where are given by Eq.5 and

are observed returns per time , i.e. .

2 Pricing European option

The value of European option on a stock when the risk neutral

dynamics is given by Eq. (1) is

(15)

where is time until expiration, is continuous dividend and

is payoff function that has the following form

(16)

Direct calculation allows us to derive the put-call parity relation

identical to Black-Scholes case

(17)

There are several methods to price a European option under the VG

model. One method uses the closed form solution derived in

[2]. Although the expression is analytic it requires

computation of modified Bessel functions, and hence may not be as fast

as we would like our pricing model to be. Therefore, FFT method has

been widely utilized to obtain a more efficient pricer. Few flavors of

the FFT method has been previously discussed with regard to the VG model.

First of all the FFT method of Carr and Madan [1],

nowadays almost standard in math finance, was applied to the VG model

to price the European vanilla option since the characteristic function

of the log-return process has a very simple form given above. Further

we intend to show, that unfortunately this method blows up at some

values of the VG parameters.

Mike Konikov and Dilip Madan [3] proposed another

interesting method based on the definition of the VG process as being a

time changed Brownian motion, where the time change is assumed

independent of the Brownian motion. This method was described in detail

in [3] while has not been implemented yet.

Also Mike Konikov and I independently implemented a modification of the FFT

method - the Fractional Fourier Transform, which is described in detail

in [4, 5]. This method usually allows

acceleration of the pricing function by factor 8-10, while for the VG model it

still demonstrates same problem as the original FFT.

Below we discuss why the Carr and Madan FFT approach fails for the VG model.

We propose another method, which originally has been developed in a general form by Lewis [6],

that seems to be free of such problems.

3 Carr-Madan’s FFT approach and the VG model

Let us start with a short description of the Carr-Madan FFT method. It was

worked out for models where the characteristic function of underlying price

process () is available. Therefore, the vanilla options can be priced very

efficiently using FFT as described in Carr and Madan [1]. The

characteristic function of the price process is given by

(18)

where . Note that the above representation holds for all

models and is not just restricted to Lévy models where the characteristic

functions have a time homogeneity constraint that ,

where is the Lévy characteristic exponent.

Once the characteristic function is available, then the vanilla call option can

be priced using Carr-Madan’s FFT formula:

(19)

where

(20)

The integral in the first equation can be computed using FFT, and as a result

we get call option prices for a variety of strikes. For complete details, see

Carr & Madan paper [1].

The put option values can just be constructed from Put-Call

symmetry.

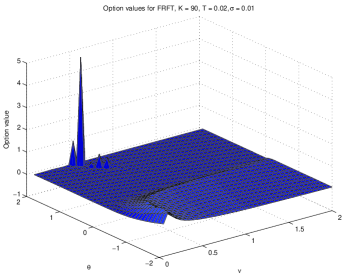

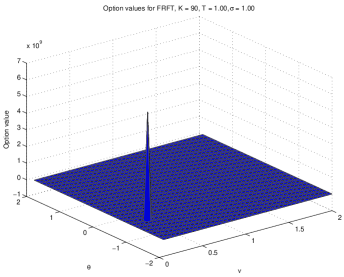

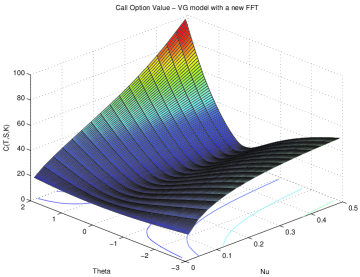

Figure 1: European option values in VG model at

obtained with FRFT.

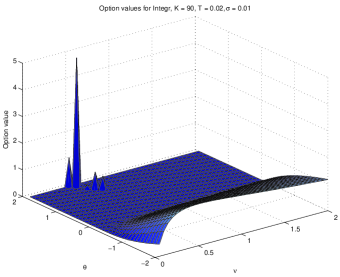

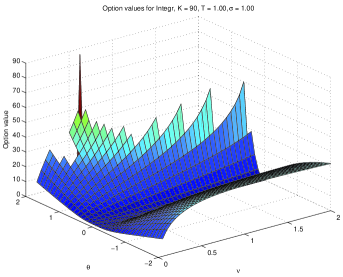

Figure 2: European option values in VG model at

obtained with the adaptive integration.

Parameter in Eq. (19) must be positive. Usually

works well for various models. It is important that the denominator in

Eq. (20) has only imaginary roots while integration in

Eq. (19) is provided along real . Thus, the integrand of

Eq. (19) is well-behaved.

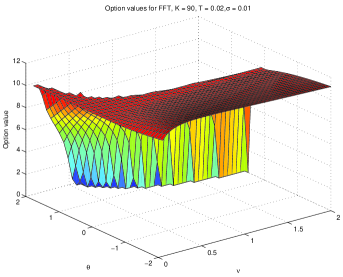

But as it turned out, this is not the case for the VG model. To show

this let us consider the European call option values obtained by

Mike Konikov by computing FFT of the VG characteristic function

according to Eq. (19).

In Fig. 2 the results of that test obtained using the FRFT

algorithm are given for strike , maturity yrs and volatility

. It is seen that at positive coefficients of skew and coefficients of kurtosis the option value has

a delta-function-wise pick that doesn’t seem to be a real option value

behavior. In Fig. 2 similar results are obtained using a

different method of evaluation of the integral in Eq. (19) - an

adaptive integration. Eventually, in Fig. 4 same test was provided

using a standard FFT method. The results look quite different that allows a

guess that something is wrong with FRFT and the adaptive integration. One could

also note that this test plays with an option with a very short maturity.

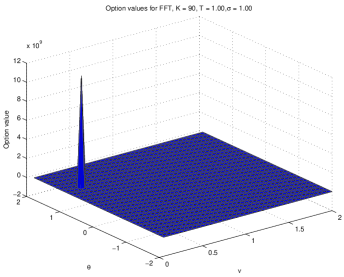

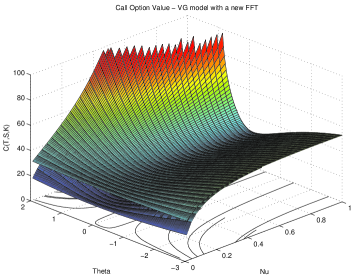

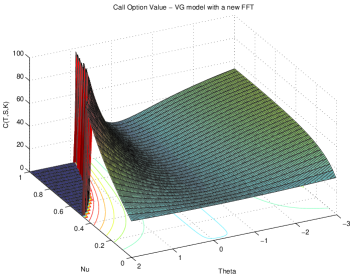

Therefore, to let us make another test with a longer maturity. In

Fig. 4-6 the results of the test that uses

same integration procedures, but for the option with ,

are presented. It is seen that for longer maturities FFT also blows up almost

at the same region of the model parameters. Moreover, it occurs not only at

positive value of the skew coefficient but at negative as well. Thus, the

problem lies not in the numerical method that was used to evaluate the integral

in the Eq. (19), but in the integral itself.

Figure 3: European option values in VG model at

obtained with FFT.

Figure 4: European option values in VG model at

obtained with the FFT.

Figure 5: European option values in VG model at

obtained with the FRFT.

Figure 6: European option values in VG model at

obtained with the adaptive integration.

Now having expression Eq. (6) for the VG characteristic

function let us substitute it and Eq. (20) into the

Eq. (19) that gives

(21)

where . At small close to zero the second term

in the denominator of the Eq. (21) is close to 1. Therefore at

small the denominator has no real roots. To understand what happens at

larger maturities, let us put and

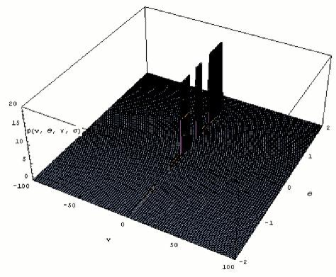

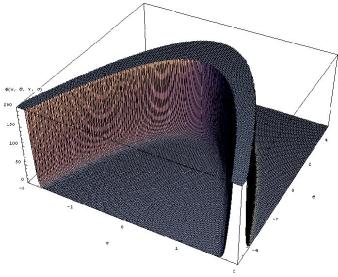

see how the denominator behaves as a function of and . The results

of this test obtained with the help of Mathematica package are given in

Fig 8.

It is seen that at at positive the characteristic function has

a singularity. To investigate it in more detail, we assume and plot the

denominator as a function of and (see Fig. 8). As

follows from this Figure in the interval there exists a value

of that makes the integrand in the Eq. (21) singular.

This means that singularity of the integrand can not be eliminated, and thus

the Carr-Madan FFT method can not be used together with the VG model for

pricing European vanilla options. Using FRFT or adaptive integration that both

are slight modifications of the FFT, also doesn’t help.

Note that for the VG model the authors of [1] derived

condition which keeps the characteristic function to be finite, that reads

(22)

Figure 7: Denominator of the Eq. (21) at as a function of and .

Figure 8: Denominator of the Eq. (21) at as a function of and .

Also as can be seen, for and corresponding to the

above mentioned tests becomes negative that doesn’t allow using this

method to price the options in terms of strike.

In order to solve these problems one needs to find another way how to

regularize the integrand, i.e. eliminate doing it in the way as Carr and Madan

did it using a regularization factor .

4 Lewis’s regularization

Another approach of how to apply FFT to the pricing of European options was

proposed by Alan Lewis [6]. Lewis notes that a general integral

representation of the European call option value with a vanilla payoff is

(23)

where is a stock price that under a pricing measure evolves

as , is the cost of carry, is the

expiration time for some option, is some Levy process satisfying

, and is the density of the log-return

distribution .

The central point of the Lewis’s work is to represent the

Eq. (23) as a convolution integral and then apply a Parseval

identity

(24)

where the hat over function denotes its Fourier transform.

The idea behind this formula is that the Fourier transform of a transition

probability density for a Levy process to reach after the elapse of

time is a well-known characteristic function, which plays an important role

in mathematical finance. For Levy processes it is , and typically has an analytic extension (a

generalized Fourier transform) , regular in

some strip parallel to the real z-axis.

Now suppose that the generalized Fourier transform of the payoff

function

and the characteristic function both exist (we will

discuss this below). Then from a chain of equalities the call option

value can be expressed as follows

Here , Im . This is a formal

derivation which becomes a valid proof if all the integrals in

Eq. (4) exist.

The Fourier transform of the vanilla payoff can be easily found by a direct

integration

(26)

Note that if z were real, this regular Fourier transform would not exist. As

shown in [7], payoff transforms for typical claims

exist and are regular in their own strips in the complex z-plane,

just like characteristic functions.

Above we denoted the strip where the characteristic function is

well-behaved as . Therefore, is defined at the

conjugate strip . Thus, the Eq. (4) is defined at the

strip , where it has the form

(27)

and .

The characteristic function of the VG process has been given by the

Eq. (13) and is defined in the strip Im

, where

(28)

This condition can be relaxed by assuming in the Eq. (28) 111In other words, if it is valid at , it

will be valid for any . Accordingly, is defined in

the strip Im .

Now let us choose Im in the form

(29)

Taking into account the Eq. (12) which makes a constrain on the

available values of the VG parameters, it is easy to see that defined in

such a way obeys the inequality . On the other hand, as

also can be easily seen, at any value of and positive

volatilities , and the equality is reached when . It means,

that Im lies in the strip as well as in the strip

, i. e. .

Now one more trick with contour integration. The integrand in

Eq. (27) is regular throughout except for simple

poles at and . The pole at has a residue

, and the pole at has a residue

222This is because . The analysis of the

previous paragraph shows that the strip is defined by the

condition , where , and . Therefore we can move the integration contour to . Then by the residue theorem, the call option value must also equal the

integral along Im minus times the residue at . That

gives us a first alternative formula

(30)

For example, with which is symmetrically located between the two

poles, this last formula becomes

(31)

where and

it is taken into account that the integrand is an even function of

its real part. The last integral can be rewritten in the form

(32)

This can be immediately recognized as a standard inverse Fourier

transform, and by derivation the integrand is regular everywhere.

Indeed, , therefore the denominator vanishes

if . Now using the

Eq. (12) one finds that or . Thus,

must be negative to turn the denominator to zero. The last

equality could be also rewritten as . Thus, the denominator vanishes if ,

i.e. must be negative, but it is not! Therefore, the characteristic function in Eq. (32)

doesn’t have singularity at . Thus, a standard FFT or FRFT method can be applied to get the value

of the integral.

In Fig. 11 -11 the results of the European vanilla option

pricing with the VG model conducted by using this new FFT method are displayed.

Two test has been provided with parameters yr,

(Fig. 11) and yr, (Fig. 11). It

is seen that the option value surface is regular in both cases. Zero values

indicates that region, where the VG constrain Eq. (12) is not

respected. The higher values of and are the lower values of

are required to obey this constraint. Therefore, at higher values of

the model is not defined that produces irregularity in the graph. This

effect is better observable in Fig. 11 that is obtained by rotation

of the Fig. 11. The above means that the new FFT method can be used

with no essential problem. A generalization of this method for FRFT is also

straightforward.

In the region of the VG parameters values where an application of the

Carr-Madan FFT procedure doesn’t cause the problem the results of that

method are almost identical to what the described above method gives.

An example of such a comparison is given in Fig. 12 (my NewFFT

Matlab code vs Mike’s FFT code). It is seen that the difference is of

the order of .

Figure 9: European option values in VG model at

obtained with the new FFT method.

Figure 10: European option values in VG model at obtained with the new FFT method.

Figure 11: European option values in VG model at

obtained with the new FFT method (rotated graph).Figure 12: The difference between the European call option values for the VG

model obtained with Carr-Madan FFT method and the new FFT method. Parameters of

the test are:

at various strikes).

5 Black-Scholes-wise method

One more method of regularization of the Fourier kernel for the VG

model has been proposed by Sepp [8] and is also discussed in [9], [10]. The idea is

as follows.

Given characteristic function of the model the

price of a European option can be expressed as

(33)

where for a call(put). Eq. (33) is

a generalization of the Black-Scholes option pricing formula. Note

that by definition, and is a

function of time to expiry and parameters of the model only.

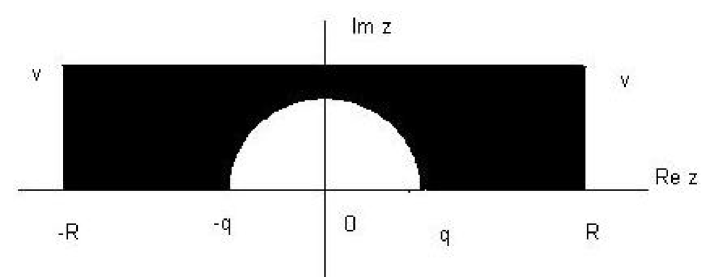

Proof: Assume that has a strip of regularity . First we rewrite Eq. (27) as

Figure 13: Integration contour for

.

In order to evaluate we employ a contour integral over the

contour given by 6 parametric curves (see Fig. (13):

. As the integrand is analytic on

this contour we can apply the Cauchy theorem. Also note that the

integral along curve is a half of the integral along the

whole circle around zero which in turn is equal to . As the integrals along vertical lines

vanish at and at the

integral along the real axis tends to an integral from to

, eventually changing variable we

obtain

(35)

To compute the we use a similar contour build around

the point , i.e. .

Again taking limits and ,

changing variable , we obtain

(36)

Substituting these integrals into the Eq. (5) we obtain

the Eq. (33) .

The difficulty in using FFT to evaluate the

Eqs. (33), as noted by Carr and Madan is the

divergence of the integrands at . Specifically, let us develop

the characteristic function with as

Taylor series in

(37)

In Eq. (30) we have to chose in the first

expression, and in the second one. As it is easy to check in

both cases that the leading term in the expansion under both

integrals is which is just a source of the divergence.The

source of this divergence is a discontinuity of the payoff function

at . Accordingly the Fourier transform of the payoff function

has large high-frequency terms. The Carr-Madan solution is in fact

to dampen the weight of the high frequencies by multiplying the

payoff by an exponential decay function. This will lower the

importance of the singularity, but at the cost of degradation of the

solution accuracy.

As the Eqs. (33) can be used whenever the

characteristic function of the given model is known, we can apply it

to the Black-Scholes model as well that gives us the Black-Scholes

option price which is a well known analytic expression. Now

the idea is to rewrite representation of the option price in

the Eqs. (33) in the form

(38)

The term in braces can now be computed with FFT as

(39)

where ,

and . This is possible

because we have removed the divergence in the integrals. In addition

the magnitude of is smaller than

that of that increases accuracy of the solution.

In more detail, first terms of the expansion of and

in series at small are

(40)

However, an usage of these expressions in the Eq. (39) together with the FFT method produces

an error of the order of . That is why it is better to choose a small , for instance ,

then computing integrands in the Eq. (39) exactly and substituting

.

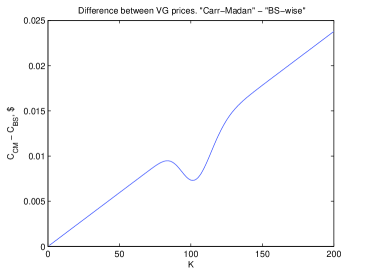

Figure 14: European option values in VG model. Difference between the Carr-Madan solution and Black-Scholes-wise solution

with at

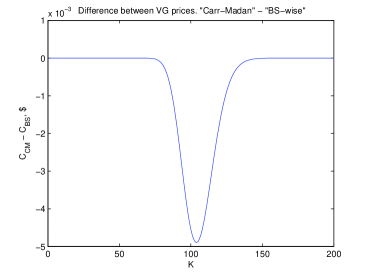

Figure 15: European option values in VG model. Difference between the Carr-Madan solution and Black-Scholes-wise solution

with at

Fig. 15, 15 show the results of our computation of the European option values

under the VG model. Difference between the Carr-Madan solution and Black-Scholes-wise solution

with and at are plotted for 200 strikes.

It is seen that for the first method the difference is of the order of 0.5%.

6 Convergency and performance

Artur Sepp reported in [8] that the convergency of the

Black-Scholes-wise method is approximately 3 times faster than that

of the Lewis method. It could be understood because as we mentioned

above in the limit of small the difference between the VG

solution and the Black-Scholes formula which is under the Fourier

integral is of the second order in while in the Lewis method it

is of the zero order. In other words using the Black-Scholes-wise

formula allows us to remove a part of the FFT error instead substituting it

with the exact analytical solution of the Black-Scholes problem.

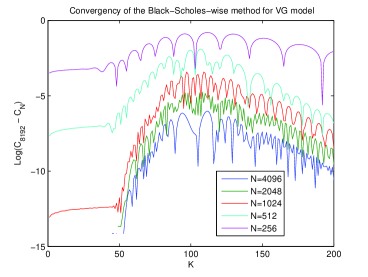

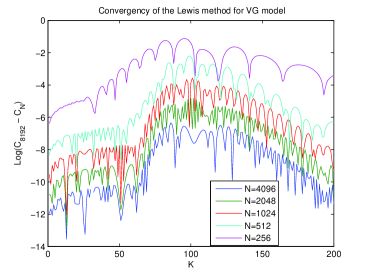

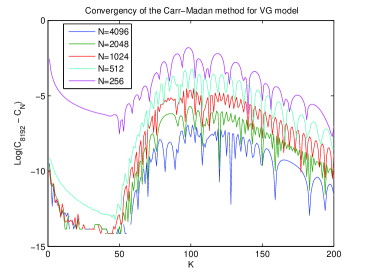

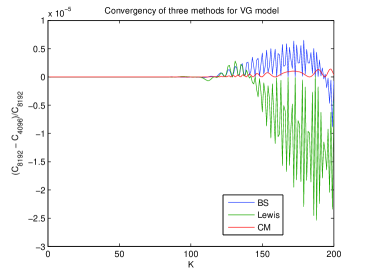

We also fulfilled investigation of how all three methods converge for the VG model.

The results are given in Fig. 17,17,19. We display

difference between the option price obtained with , and that with .

We don’t see much difference in the convergency of the Lewis and Black-Scholes-wise method while

the Carr-Madan methods behaves better at low . In Fig. 19 we also present the ratio

for all three methods. The Carr-Madan still converges better for

out of the money spot prices while convergency of two other methods is similar.

Figure 16: Convergency of the Black-Scholes-wise method. Difference between the

option price obtained with , and that with

.

Figure 17: Convergency of the Lewis method. Difference between the

option price obtained with , and that with

.

Figure 18: Convergency of the Carr-Madan method. Difference between the

option price obtained with , and that with

.

Figure 19: Convergency of all three methods

.

Cont and Tankov also analyze the Lewis method. They emphasize the

fact that the integral in the Eq. (30) is much easier to

approximate at infinity than that in the Carr-Madan method, because

the integrand decays exponentially (due to the presence of

characteristic function). However, the price to pay for this is

having to choose . This choice is a delicate issue because

choosing big leads to slower decay rates at infinity and

bigger truncation errors and when is close to one, the

denominator diverges and the discretization error becomes large. For

models with exponentially decaying tails of Levy measure,

cannot be chosen a priori and must be adjusted depending on the

model parameters.

Carr and Madan in [1] compare performance of 3 methods for computing VG prices:

VGP which is the analytic formula in Madan, Carr, and Chang;

VGPS which computes delta and the risk-neutral probability of finishing

in-the-money by Fourier inversion of the distribution function, i.e. according to the

Eq. (33); VGFFTC which is a Carr-Madan method using FFT to invert the dampened call price;

VGFFTTV which uses FFT to invert the modified time value. The results are given in Tab. (2). The computation times for the first

two methods involve 160 strike levels. The first 4 rows of Tab. (2) display

4 combinations of parameter settings, while the last 4 rows show computation times in seconds.

case 1

case 2

case 3

case 4

.12

.25

.12

.25

.16

2.0

.16

2.0

-.33

-.10

-.33

-.10

1

1

.25

.25

VGP

22.41

24.81

23.82

24.74

VGPS

288.50

191.06

181.62

197.97

VGFFTC

6.09

6.48

6.72

6.52

VGFFTTV

11.53

11.48

11.57

11.56

Table 1: CPU times for VG pricing. Represented from [1].

case 1

case 2

case 3

case 4

.12

.25

.12

.25

.16

2.0

.16

2.0

-.33

-.10

-.33

-.10

1

1

.25

.25

Lewis

0.031

0.031

0.031

0.031

Carr-Madan

0.047

0.047

0.032

0.032

BS-wise

0.078

0.078

0.062

0.062

Table 2: CPU times for VG pricing. Our calculations.

It is seen that the analytic formula is slow while the slowest (and least

accurate in case 4) method inverts for the delta and for the probability of

paying off.

However, this is not true if one uses a modified method given in the Eq. (39).

Our calculations show that the performance of the Lewis method is same as the Carr-Madan method, and

the performance of the Black-Scholes-wise method is only twice worse (because we need 2 FFT to compute 2 integrals)

(see Tab. 2).

7 Conclusion

We discussed various analytic and numerical methods that have been

used to get option prices within a framework of VG model. We showed

that a popular Carr-Madan’s FFT method [1] blows up

for certain values of the model parameters even for European vanilla option. Alternative methods -

one originally proposed by Lewis, and Black-Scholes-wise method were

considered that seem to work fine for any value of the VG

parameters. Convergency and accuracy of these methods is comparable with that of the Carr-Madan

method, thus making them suitable for being used to price options with the VG model.

References

[1]

Peter Carr and Dilip Madan.

Option valuation using the fast fourier transform.

Journal of Computational Finance, 2(4):61–73, 1999.

[2]

Dilip Madan, Peter Carr, and Eric Chang.

The variance gamma process and option pricing.

European Finance Review, 2:79–105, 1998.

[3]

Dilim Madan and Michael Konikov.

Variance gamma model: Gamma weighted black-scholes implementation.

Technical report, Bloomberg L.P., July 2004.

[4]

D. H. Bailey and P.N. Swarztrauber.

The fractional fourier transform and applications.

SIAM Review, 33(3):389–404, 1991.

[5]

K. Chourdakis.

Option pricing using the fractional fft.

Technical report, 2004.

[6]

Alan L. Lewis.

A simple option formula for general jump-diffusion and other

exponentiallévy processes.

manuscript, Envision Financial Systems and OptionCity.net, Newport

Beach, California, USA, 2001.

[7]

Alan L. Lewis.

Option Valuation under Stochastic Volatility.

Finance Press, Newport Beach, California, USA, 2000.

[8] A. Sepp.

Fourier transform for option pricing under affine jump-diffusions: An overview.

Unpublished Manuscript, available at www.hot.ee/seppar, 2003.

[9] I. Yekutieli.

Pricing European options with fit.

Technical report, Bloomberg L.P., November 2004.

[10] R. Cont and P. Tankov.

Financial modelling with jump processes.

Chapman & Hall, CRC, 2004.