Empirical Distributions of Log-Returns:

between the Stretched Exponential and the Power Law?

Abstract

A large consensus now seems to take for granted that the distributions of empirical returns of financial time series are regularly varying, with a tail exponent close to . First, we show by synthetic tests performed on time series with time dependence in the volatility with both Pareto and Stretched-Exponential distributions that for sample of moderate size, the standard generalized extreme value (GEV) estimator is quite inefficient due to the possibly slow convergence toward the asymptotic theoretical distribution and the existence of biases in presence of dependence between data. Thus it cannot distinguish reliably between rapidly and regularly varying classes of distributions. The Generalized Pareto distribution (GPD) estimator works better, but still lacks power in the presence of strong dependence. Then, we use a parametric representation of the tail of the distributions of returns of 100 years of daily return of the Dow Jones Industrial Average and over 1 years of -minutes returns of the Nasdaq Composite index, encompassing both a regularly varying distribution in one limit of the parameters and rapidly varying distributions of the class of the Stretched-Exponential (SE) and Log-Weibull distributions in other limits. Using the method of nested hypothesis testing (Wilks’ theorem), we conclude that both the SE distributions and Pareto distributions provide reliable descriptions of the data and cannot be distinguished for sufficiently high thresholds. However, the exponent of the Pareto increases with the quantiles and its growth does not seem exhausted for the highest quantiles of three out of the four tail distributions investigated here. Correlatively, the exponent of the SE model decreases and seems to tend to zero. Based on the discovery that the SE distribution tends to the Pareto distribution in a certain limit such that the Pareto (or power law) distribution can be approximated with any desired accuracy on an arbitrary interval by a suitable adjustment of the parameters of the SE distribution, we demonstrate that Wilks’ test of nested hypothesis still works for the non-exactly nested comparison between the SE and Pareto distributions. The SE distribution is found significantly better over the whole quantile range but becomes unnecessary beyond the quantiles compared with the Pareto law. Similar conclusions hold for the log-Weibull model with respect to the Pareto distribution. Summing up all the evidence provided by our battery of tests, it seems that the tails ultimately decay slower than any SE but probably faster than power laws with reasonable exponents. Thus, from a practical view point, the log-Weibull model, which provides a smooth interpolation between SE and PD, can be considered as an appropriate approximation of the sample distributions. We finally discuss the implications of our results on the “moment condition failure” and for risk estimation and management.

key-words: Extreme-Value Estimators, Non-Nested Hypothesis Testing, Pareto distribution, Weibull distribution

1 Motivation of the study

The determination of the precise shape of the tail of the distribution of returns is a major issue both from a practical and from an academic point of view. For practitioners, it is crucial to accurately estimate the low value quantiles of the distribution of returns (profit and loss) because they are involved in almost all the modern risk management methods. From an academic perspective, many economic and financial theories rely on a specific parameterization of the distributions whose parameters are intended to represent the “macroscopic” variables the agents are sensitive to.

The distribution of returns is one of the most basic characteristics of the markets and many papers have been devoted to it. Contrarily to the average or expected return, for which economic theory provides guidelines to assess them in relation with risk premium, firm size or book-to-market equity (see for instance \citeasnounFF96), the functional form of the distribution of returns, and especially of extreme returns, is much less constrained and still a topic of active debate. Naively, the central limit theorem would lead to a Gaussian distribution for sufficiently large time intervals over which the return is estimated. Taking the continuous time limit such that any finite time interval is seen as the sum of an infinite number of increments thus leads to the paradigm of log-normal distributions of prices and equivalently of Gaussian distributions of returns, based on the pioneering work of \citeasnounBachelier00 later improved by \citeasnounSamuelson. The log-normal paradigm has been the starting point of many financial theories such as \citeasnounMarkovitz59’s portfolio selection method, \citeasnounSharpe64’s market equilibrium model or \citeasnounBS73’s rational option pricing theory. However, for real financial data, the convergence in distribution to a Gaussian law is very slow [Campbell, BP00, for instance], much slower than predicted for independent returns. As table 1 shows, the excess kurtosis (which is zero for a normal distribution) remains large even for monthly returns, testifying (i) of significant deviations from normality, (ii) of the heavy tail behavior of the distributions of returns and (iii) of significant dependences between returns [Campbell].

Another idea rooted in economic theory consists in invoking the “Gibrat principle” [Simon] initially used to account for the growth of cities and of wealth through a mechanism combining stochastic multiplicative and additive noises [LSR96, SC97, Biham98, DS98] leading to a Pareto distribution of sizes [Champenowne, Gabaix]. Rational bubble models a la \citeasnounBlanchardwat can also be cast in this mathematical framework of stochastic recurrence equations and leads to distribution with power law tails, albeit with a strong constraint on the tail exponent [LuxSor, MalSor]. These frameworks suggest that an alternative and natural way to capture the heavy tail character of the distributions of returns is to use distributions with power-like tails (Pareto, Generalized Pareto, stable laws) or more generally, regularly-varying distributions [BGT87] 111The general representation of a regularly varying distribution is given by , where is a slowly varying function, that is, lim for any finite ., the later encompassing all the former.

In the early 1960s, \citeasnounMandelbrot63 and \citeasnounFama65 presented evidence that distributions of returns can be well approximated by a symmetric Lévy stable law with tail index about . These estimates of the power tail index have recently been confirmed by \citeasnounMRP98, and slightly different indices of the stable law () were suggested by \citenameMS95 \citeyearMS95,MS00. On the other hand, there are numerous evidences of a larger value of the tail index [Longin96, GDDMOP97, GMAS98, GMAS98_2, Plerouetal99, MDP98, Farmer99, Lux00]. See also the various alternative parameterizations in term of the Student distribution [Blattberg, kon], or Pearson type-VII distributions [Naga], which all have an asymptotic power law tail and are regularly varying. Thus, a general conclusion of this group of authors concerning tail fatness can be formulated as follows: tails of the distribution of returns are heavier than a Gaussian tail and heavier than an exponential tail; they certainly admit the existence of a finite variance (), whereas the existence of the third (skewness) and the fourth (kurtosis) moments is questionable.

These apparent contradictory results actually do not apply to the same quantiles of the distributions of returns. Indeed, \citeasnounMS95 have shown that the distribution of returns can be described accurately by a Lévy law only within a limited range of perhaps up to 4 standard deviations, while a faster decay of the distribution is observed beyond. This almost-but-not-quite Lévy stable description explains (in part) the slow convergence of the returns distribution to the Gaussian law under time aggregation [Sorbook]. And it is precisely outside this range where the Lévy law applies that a tail index of about three have been estimated. This can be seen from the fact that most authors who have reported a tail index have used some optimality criteria for choosing the sample fractions (i.e., the largest values) for the estimation of the tail index. Thus, unlike the authors supporting stable laws, they have used only a fraction of the largest (positive tail) and smallest (negative tail) sample values.

It would thus seem that all has been said on the distributions of returns. However, there are dissenting views in the literature. Indeed, the class of regularly varying distributions is not the sole one able to account for the large kurtosis and fat-tailness of the distributions of returns. Some recent works suggest alternative descriptions for the distributions of returns. For instance, \citeasnounGJ98 claim that the distribution of returns on the French stock market decays faster than any power law. \citeasnouncontdub have proposed to use exponentially truncated stable distributions, \citeasnounBarndorff, \citeasnounEberlein and \citeasnounPrause have respectively considered normal inverse Gaussian and (generalized) hyperbolic distributions, which asymptotically decay as , while \citeasnounLS99 suggest to fit the distributions of stock returns by the Stretched-Exponential (SE) law. These results, challenging the traditional hypothesis of power-like tail, offer a new representation of the returns distributions and need to be tested rigorously on a statistical ground.

A priori, one could assert that \citeasnounLongin96’s results should rule out the exponential and Stretched-Exponential hypotheses. Indeed, his results, based on extreme value theory, show that the distributions of log-returns belong to the maximum domain of attraction of the Fréchet distribution, so that they are necessarily regularly varying power-like laws. However, his study, like almost all others on this subject, has been performed under the assumption that (1) financial time series are made of independent and identically distributed returns and (2) the corresponding distributions of returns belong to one of only three possible maximum domains of attraction. However, these assumptions are not fulfilled in general. While \citeasnounSmith85’s results indicate that the dependence of the data does not constitute a major problem in the limit of large samples, we shall see that it can significantly bias standard statistical methods for samples of size commonly used in extreme tails studies. Moreover, Longin’s conclusions are essentially based on an aggregation procedure which stresses the central part of the distribution while smoothing the characteristics of the tail, which are essential in characterizing the tail behavior.

In addition, real financial time series exhibit GARCH effects [Bollerslev86, BEN94] leading to heteroscedasticity and to clustering of high threshold exceedances due to a long memory of the volatility. These rather complex dependent structures make difficult if not questionable the blind application of standard statistical tools for data analysis. In particular, the existence of significant dependence in the return volatility leads to the existence of a significant bias and an increase of the true standard deviation of the statistical estimators of tail indices. Indeed, there are now many examples showing that dependences and long memories as well as nonlinearities mislead standard statistical tests [AEL99, GT99, for instance]. Consider the Hill’s and Pickand’s estimators, which play an important role in the study of the tails of distributions. It is often overlooked that, for dependent time series, Hill’s estimator remains only consistent but not asymptotically efficient [RLdH98]. Moreover, for financial time series with a dependence structure described by a IGARCH process, \citeasnounKP97 have shown that the standard deviation of Hill’s estimator obtained by a bootstrap method can be seven to eight time larger than the standard deviation derived under the asymptotic normality assumption. These figures are even worse for Pickand’s estimator.

The question then arises whether the many results and seemingly almost consensus obtained by ignoring the limitations of usual statistical tools could have led to erroneous conclusions about the tail behavior of the distributions of returns. Here, we propose to investigate once more this delicate problem of the tail behavior of distributions of returns in order to shed new lights 222\citeasnounPicoli have also presented fits comparing the relative merits of SE and so-called -exponentials (which are similar to Student distribution with power law tails) for the description of the frequency distributions of basketball baskets, cyclone victims, brand-name drugs by retail sales, and highway length.. To this aim, we investigate two time series: the daily returns of the Dow Jones Industrial Average (DJ) Index over a century (kindly provided by Prof. H.-C. G. Bothmer) and the five-minutes returns of the Nasdaq Composite index (ND) over one year from April 1997 to May 1998 obtained from Bloomberg. These two sets of data have been chosen since they are typical of the data sets used in most previous studies. Their size (about data points), while significant compared with those used in investment and portfolio analysis, is however much smaller than recent data-intensive studies using ten of millions of data points [GMAS98, GMAS98_2, Plerouetal99, matia, mizumo].

First, we show by synthetic tests performed on time series with time dependence in the volatility with both Pareto and Stretched-Exponential distributions that for sample of moderate size, the standard generalized extreme value (GEV) estimator is quite inefficient due to the possibly slow convergence toward the asymptotic theoretical distribution and the existence of biases in presence of dependence between data. Thus it cannot distinguish reliably between rapidly and regularly varying classes of distributions. The Generalized Pareto distribution (GPD) estimator works better, but still lacks power in the presence of strong dependence. Then, we use a parametric representation of the tail of the distributions of returns of our two time series, encompassing both a regularly varying distribution in one limit of the parameters and rapidly varying distributions of the class of the Stretched-Exponential (SE) and Log-Weibull distributions in other limits.

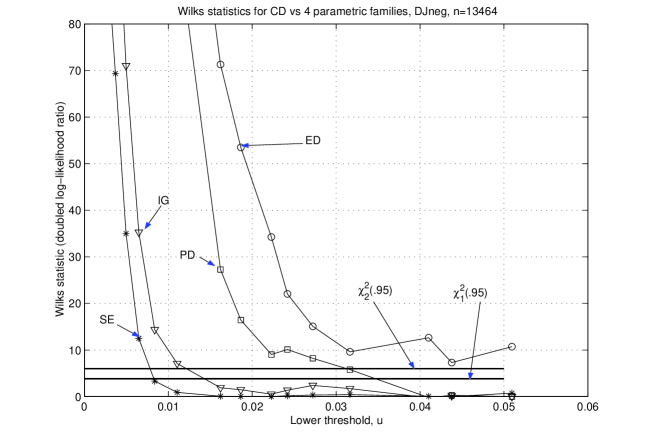

Using the method of nested hypothesis testing (Wilks’ theorem), our second conclusion is that none of the standard parametric family distributions (Pareto, exponential, stretched-exponential, incomplete Gamma and Log-Weibull) fits satisfactorily the DJ and ND data on the whole range of either positive or negative returns. While this is also true for the family of stretched exponential and the log-Weibull distributions, these families appear to be the best among the five considered parametric families, in so far as they are able to fit the data over the largest interval. For the high quantiles (far in the tails), both the SE distributions and Pareto distributions provide reliable descriptions of the data and cannot be distinguished for sufficiently high thresholds. However, the exponent of the Pareto increases with the quantiles and its growth does not seem exhausted for the highest quantiles of three out of the four tail distributions investigated here. Correlatively, the exponent of the SE model decreases and seems to tend to zero

Based on the discovery presented here that the SE distribution tends to the Pareto distribution in a certain limit such that the Pareto (or power law) distribution can be approximated with any desired accuracy on an arbitrary interval by a suitable adjustment of the parameters of the SE distribution, we demonstrate that Wilks’ test of nested hypothesis still works for the non-exactly nested comparison between the SE and Pareto distributions. The SE distribution is found significantly better over the whole quantile range but becomes unnecessary beyond the quantiles compared with the Pareto law. The log-Weibull model seems to be a good candidate since it provides a smooth interpolation between the SE and PD models. The log-Weibull distribution is at least as good as the Stretched-Exponential model, on a large range of data, but again, the Pareto distribution is ultimately the most parsimonious.

Collectively, these results suggest that the extreme tails of the true distribution of returns of our two data sets are fatter that any stretched-exponential, strictly speaking -i.e., with a strickly positive fractional exponent- but thinner than any power law. Thus, notwithstanding our best efforts, we cannot conclude on the exact nature of the far-tail of distributions of returns.

As already mentioned, other works have proposed the so-called inverse-cubic law () based on the analysis of distributions of returns of high-frequency data aggregated over hundreds up to thousands of stocks. This aggregating procedure leads to novel problems of interpretation. We think that the relevant question for most practical applications is not to determine what is the true asymptotic tail but what is the best effective description of the tails in the domain of useful applications. As we shall show below, it may be that the extreme asymptotic tail is a regularly varying function with tail index for daily returns, but this is not very useful if this tail describes events whose recurrence time is a century or more. Our present work must thus be gauged as an attempt to provide a simple efficient effective description of the tails of distribution of returns covering most of the range of interest for practical applications. We feel that the efforts requested to go deeper in the tails beyond the tails analyzed here, while of great interest from a scientific point of view to potentially help unravel market mechanisms, may be too artificial and unreachable to have significant applications.

The paper is organized as follows.

The next section is devoted to the presentation of our two data sets and to some of their basic statistical properties, emphasizing their fat tailed behavior. We discuss, in particular, the importance of the so-called “lunch effect” for the tail properties of intra-day returns. We then obtain the well-known presence of a significant temporal dependence structure and study the possible non-stationary character of these time series.

Section 3 attempts to account for the temporal dependence of our time series and investigates its effect on the determination of the extreme behavior of the tails of the distribution of returns. In this goal, we build a simple long memory stochastic volatility process whose stationary distributions are by construction either asymptotically regularly varying or exponential. We show that, due to the time dependence on the volatility, the estimation with standard statistical estimators may become unreliable due to the significant bias and increase of the standard deviation of these estimators. These results justify our re-examination of previous claims of regularly varying tails.

To fit our two data sets, section 4 proposes two general parametric representations of the distribution of returns encompassing both a regularly varying distribution in one limit of the parameters and rapidly varying distributions of the class of stretched exponential and log-Weibull distributions in another limit. The use of regularly varying distributions have been justified above. From a theoretical view point, the class of stretched exponentials is motivated in part by the fact that the large deviations of multiplicative processes are generically distributed with stretched exponential distributions [FrischSor]. Stretched exponential distributions are also parsimonious examples of the important subset of sub-exponentials, that is, of the general class of distributions decaying slower than an exponential. This class of sub-exponentials share several important properties of heavy-tailed distributions [EKM97], not shared by exponentials or distributions decreasing faster than exponentials. The interest of the log-Weibull comes from the smooth interpolation it provides between any Stretched-Exponential and any Pareto distributions.

The descriptive power of these different hypotheses are compared in section 5. We first consider nested hypotheses and use Wilks’ test to compare each distribution (Pareto, Exponential, Gamma and Stretched Exponential) with the most general parameterization which encompasses all of them. It appears that both the stretched-exponential and the Pareto distributions are the best and most parsimonious models compatible with the data with a slight advantage in favor of the stretched exponential model. Then, in order to directly compare the descriptive power of these two models, we use the important remark that, in a certain limit where the exponent of the stretched exponential pdf goes to zero, the stretched exponential pdf tends to the Pareto distribution. Thus, the Pareto (or power law) distribution can be approximated with any desired accuracy on an arbitrary interval by a suitable adjustment of the parameters of the stretched exponential pdf. This allows us to demonstrate in Appendix D that Wilks’ test also applies to this non-exactly nested comparison between the SE and Pareto models. We find that the SE distribution is significantly better over the whole quantile range but becomes unnecessary beyond the quantiles compared with the Pareto law. Similar results are found for the comparison of the Log-Weibull versus the Pareto distributions.

Section 6 summarizes our results and presents the conclusions of our study for risk management purposes.

2 Some basic statistical features

2.1 The data

We use two sets of data. The first sample consists in the daily returns333Throughout the paper, we will use compound returns, i.e., log-returns. of the Dow Jones Industrial Average Index (DJ) over the time interval from May 27, 1896 to May 31, 2000, which represents a sample size . The second data set contains the high-frequency (5 minutes) returns of Nasdaq Composite (ND) index for the period from April 8, 1997 to May 29, 1998 which represents n=22123 data points. The choice of these two data sets is justified by their similarity with (1) the data set of daily returns used by \citeasnounLongin96 particularly and (2) the high frequency data used by \citeasnounGDDMOP97, \citeasnounLux00, \citeasnounMDP98 among others.

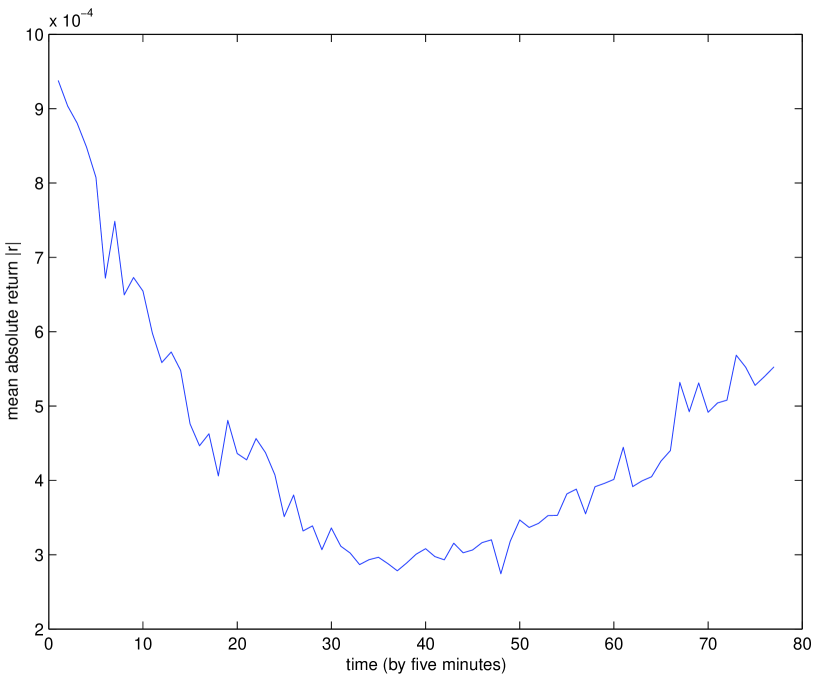

For the intra-day Nasdaq data, there are two caveats that must be addressed. First, in order to remove the effect of overnight price jumps, we have determined the returns separately for each of 289 days contained in the Nasdaq data and have taken the union of all these 289 return data sets to obtain a global return data set. Second, the volatility of intra-day data are known to exhibit a U-shape, also called “lunch-effect”, that is, an abnormally high volatility at the begining and the end of the trading day compared with a low volatility at the approximate time of lunch. Such effect is present in our data, as depicted on figure 1, where the average absolute returns are shown as a function of the time within a trading day. It is desirable to correct the data from this systematic effect. This has been performed by renormalizing the 5 minutes-returns at a given moment of the trading day by the corresponding average absolute return at the same moment. We shall refer to this time series as the corrected Nasdaq returns in contrast with the raw (incorrect) Nasdaq returns and we shall examine both data sets for comparison.

The Dow Jones daily returns also exhibit some non-stationarity. Indeed, one can observe a clear excess volatility roughly covering the time of the bubble ending in the October 1929 crash following by the Great Depression. To investigate the influence of such non-stationarity, time interval, the statistical study exposed below has been performed twice: first with the entire sample, and after having removed the period from 1927 to 1936 from the sample. The results are somewhat different, but on the whole, the conclusions about the nature of the tail are the same. Thus, only the results concerning the whole sample will be detailed in the paper.

Although the distributions of positive and negative returns are known to be very similar [JR01, for instance], we have chosen to treat them separately. For the Dow Jones, this gives us positive and negative data points while, for the Nasdaq, we have positive and negative data points.

Table 1 summarizes the main statistical properties of these two time series (both for the raw and for the corrected Nasdaq returns) in terms of the average returns, their standard deviations, the skewness and the excess kurtosis for four time scales of five minutes, an hour, one day and one month. The Dow Jones exhibits a significantly negative skewness, which can be ascribed to the impact of the market crashes. The raw Nasdaq returns are significantly positively skewed while the returns corrected for the “lunch effect” are negatively skewed, showing that the lunch effect plays an important role in the shaping of the distribution of the intra-day returns. Note also the important decrease of the kurtosis after correction of the Nasdaq returns for lunch effect, confirming the strong impact of the lunch effect. In all cases, the excess-kurtosis are high and remains significant even after a time aggregation of one month. The Jarque-Bera’s test [Cromwell], a joint statistic using skewness and kurtosis coefficients, is used to reject the normality assumption for these time series.

2.2 Existence of time dependence

It is well-known that financial time series exhibit complex dependence structures like heteroscedasticity or non-linearities. These properties are clearly observed in our two times series. For instance, we have estimated the statistical characteristic (for positive random variables) called coefficient of variation

| (1) |

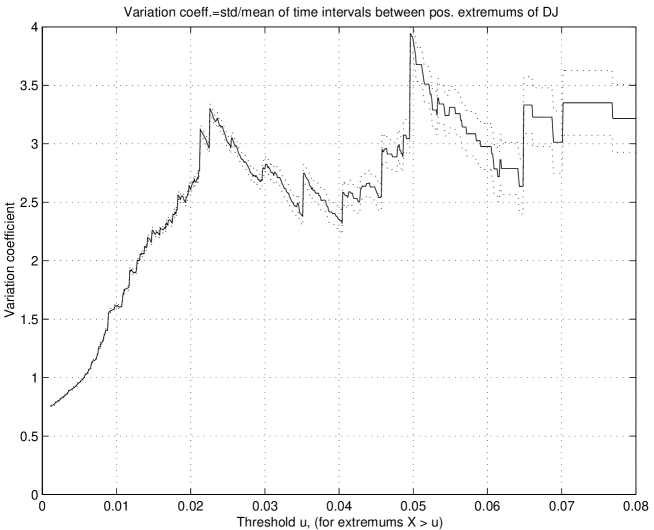

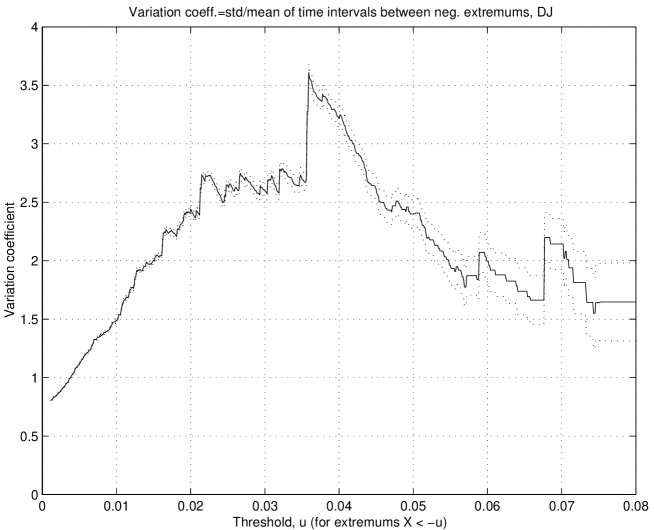

which is often used as a testing statistic of the randomness property of a time series. It can be applied to a sequence of points (or, intervals generated by these points on the line). If these points are “absolutely random,” that is, generated by a Poissonian flow, then the intervals between them are distributed according to an exponential distribution for which . If , the process is close to a periodic oscillation. Values are associated with a clustering phenomenon. We estimated for extrema and as function of threshold (both for positive and for negative extrema). The results are shown in figure 2 for the Dow Jones daily returns. As the results are essentially the same for the Nasdaq, we do not show them. Figure 2 shows that, in the main range , containing of the sample, increases with , indicating that the “clustering” property becomes stronger as the threshold increases. The coefficient of variation has also been estimated for the Dow Jones when the time interval from 1927 to 1936 is removed. Its maximum value decreases by one, but it still significantly increases with the threshold .

We have then applied several formal statistical tests of independence. We have first performed the Lagrange multiplier test proposed by \citeasnounEngle84 which leads to the test statistic, where denotes the sample size and is the determination coefficient of the regression of the squared centered returns on a constant and on of their lags . Under the null hypothesis of homoscedastic time series, follows a -statistic with degrees of freedom. The test has been performed up to and, in every case, the null hypothesis is strongly rejected, at any usual significance level. Thus, the time series are heteroskedastic and exhibit volatility clustering. We have also performed a BDS test [BDS87] which allows us to detect not only volatility clustering, like in the previous test, but also departure from iid-ness due to non-linearities. Again, we strongly rejects the null-hypothesis of iid data, at any usual significance level, confirming the Lagrange multiplier test.

3 Can long memory processes lead to misleading measures of extreme properties?

Since the descriptive statistics given in the previous section have clearly shown the existence of a significant temporal dependence structure, it is important to consider the possibility that it can lead to erroneous conclusions on the estimated parameters as previously shown by \citeasnounKP97 for integrated GARCH processes. We first briefly recall the standard procedures used to investigate extremal properties, stressing the problems and drawbacks arising from the existence of temporal dependence. We then perform a numerical simulation to study the behavior of the estimators in presence of dependence. We put particular emphasis on the possible appearance of significant biases due to dependence in the data set. Finally, we present the results on the extremal properties of our two DJ and ND data sets in the light of the bootstrap results.

3.1 Some theoretical results

Two limit theorems allow one to study the extremal properties and to determine the maximum domain of attraction (MDA) of a distribution function in two forms.

First, consider a sample of iid realizations . Let denotes the maximum of this sample. Then, the Gnedenko theorem states that, if, after an adequate centering and normalization, the distribution of converges to a non-degenerate distribution as goes to infinity, this limit distribution is then necessarily the Generalized Extreme Value (GEV) distribution defined by

| (2) |

When , should be understood as

| (3) |

Thus, for large enough

| (4) |

for some value of the centering parameter , scale factor and tail index . It should be noted that the existence of non-degenerate limit distribution of properly centered and normalized is a rather strong limitation. There are a lot of distribution functions that do not satisfy this limitation, e.g., infinitely alternating functions between a power-like and an exponential behavior.

The second limit theorem is called after Gnedenko-Pickands-Balkema-de Haan (GPBH) and its formulation is as follows. In order to state the GPBH theorem, we define the right endpoint of a distribution function as . Let us call the function

| (5) |

the excess distribution function (DF). Then, this DF belongs to the Maximum Domain of Attraction of defined by eq.(2) if and only if there exists a positive scale-function , depending on the threshold , such that

| (6) |

where

| (7) |

By taking the limit , expression (7) leads to the exponential distribution. The support of the distribution function (7) is defined as follows:

| (8) |

Thus, the Generalized Pareto Distribution has a finite support for .

The form parameter is of paramount importance for the form of the limiting distribution. Its sign determines three possible limiting forms of the distribution of maxima: If , then the limit distribution is the Fréchet power-like distribution; If , then the limit distribution is the Gumbel (double-exponential) distribution; If , then the limit distribution has a support bounded from above. All these three distributions are united in eq.(2) by this parameterization. The determination of the parameter is the central problem of extreme value analysis. Indeed, it allows one to determine the maximum domain of attraction of the underling distribution. When , the underlying distribution belongs to the Fréchet maximum domain of attraction and is regularly varying (power-like tail). When , it belongs to the Gumbel Maximum Domain of Attraction and is rapidly varying (exponential tail), while if it belongs to the Weibull Maximum Domain of Attraction and has a finite right endpoint.

3.2 Examples of slow convergence to limit GEV and GPD distributions

There exist two ways of estimating . First, if there is a sample of maxima (taken from sub-samples of sufficiently large size), then one can fit to this sample the GEV distribution, thus estimating the parameters by Maximum Likelihood method. Alternatively, one can prefer the distribution of exceedances over a large threshold given by the GPD (7), whose tail index can be estimated with Pickands’ estimator or by Maximum Likelihood, as previously. Hill’s estimator cannot be used since it assumes , while the essence of extreme value analysis is, as we said, to test for the class of limit distributions without excluding any possibility, and not only to determine the quantitative value of an exponent. Each of these methods has its advantages and drawbacks, especially when one has to study dependent data, as we show below.

Given a sample of size , one considers the -maxima drawn from sub-samples of size (such that ) to estimate the parameters in (4) by Maximum Likelihood. This procedure yields consistent and asymptotically Gaussian estimators, provided that [Smith85]. The properties of the estimators still hold approximately for dependent data, provided that the interdependence of data is weak. However, it is difficult to choose an optimal value of of the sub-samples. It depends both on the size of the entire sample and on the underlying distribution: the maxima drawn from an Exponential distribution are known to converge very quickly to Gumbel’s distribution [HW79], while for the Gaussian law, convergence is particularly slow [Hall79].

The second possibility is to estimate the parameter from the distribution of exceedances (the GPD). For this, one can use either the Maximum Likelihood estimator or Pickands’ estimator. Maximum Likelihood estimators are well-known to be the most efficient ones (at least for and for independent data) but, in this particular case, Pickands’ estimator works reasonably well. Given an ordered sample of size , Pickands’ estimator is given by

| (9) |

For independent and identically distributed data, this estimator is consistent provided that is chosen so that and as . Moreover, is asymptotically normal with variance

| (10) |

In the presence of dependence between data, one can expect an increase of the standard deviation, as reported by \citeasnounKP97. For time dependence of the GARCH class, \citeasnounKP97 have indeed demonstrated a significant increase of the standard deviation of the tail index estimator, such as Hill’s estimator, by a factor more than seven with respect to their asymptotic properties for iid samples. This leads to very inaccurate index estimates for time series with this kind of temporal dependence.

Another problem lies in the determination of the optimal threshold of the GPD, which is in fact related to the optimal determination of the sub-samples size in the case of the estimation of the parameters of the distribution of maximum.

In sum, none of these methods seem really satisfying and each one presents severe drawbacks. The estimation of the parameters of the GEV distribution and of the GPD may be less sensitive to the dependence of the data, but this property is only asymptotic, thus a bootstrap investigation is required to be able to compare the real power of each estimation method for samples of moderate size.

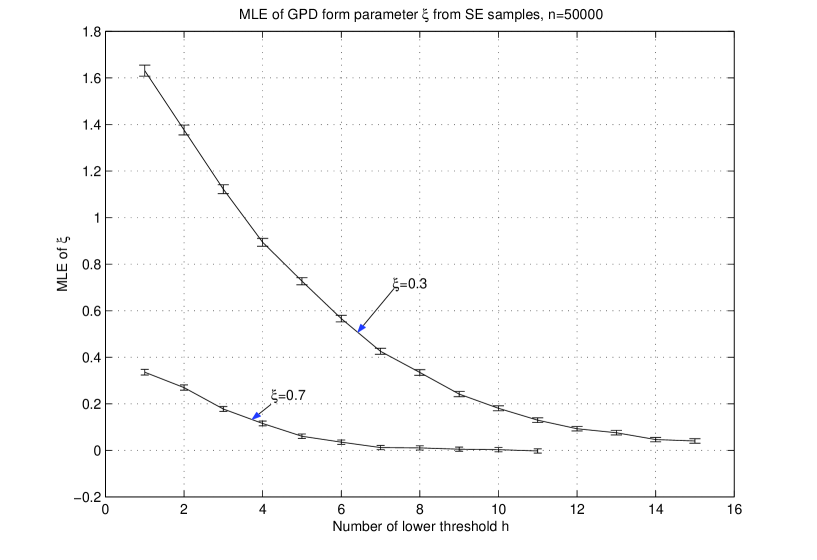

As a first simple example illustrating the possibly very slow convergence to the limit distributions of extreme value theory mentioned above, let us consider a simulated sample of iid Weibull random variables (we thus fulfill the most basic assumption of extreme values theory, i.e, iid-ness). We take two values for the exponent of the Weibull distribution: and , with (scale parameter). An estimation of by the distribution of the GPD of exceedance should give estimated values of close to zero in the limit of large . In order to use the GPD, we have taken the conditional Weibull distribution under condition , where the thresholds are chosen as: and .

For each simulation, the size of the sample above the considered threshold is chosen equal to in order to get small standard deviations. The Maximum-Likelihood estimates of the GPD form parameter are shown in figure 3. For , the threshold gives an estimate with standard deviation equal to , i.e., the estimate for differs significantly from zero (recall that is the correct theoretical limit value). This occurs notwithstanding the huge size of the implied data set; indeed, the probability for is about , so that in order to obtain a data set of conditional samples from an unconditional data set of the size studied here ( realizations above ), the size of such unconditional sample should be approximately times larger than the number of “peaks over threshold”, i.e., it is practically impossible to have such a sample. For , the convergence to the theoretical value zero is even slower. Indeed, even the largest financial datasets for a single asset, drawn from high frequency data, are no larger than or of the order of one million points444One year of data sampled at the minute time scale gives approximately data points. The situation does not change even for data sets one or two orders of magnitudes larger as considered in [GMAS98, GMAS98_2, Plerouetal99], obtained by aggregating thousands of stocks555In this case, another issue arises concerning the fact that the aggregation of returns from different assets may distort the information and the very structure of the tails of the probability density functions (pdf), if they exhibit some intrinsic variability [matia].. Thus, although the GPD form parameter should be zero theoretically in the limit of large sample for the Weibull distribution, this limit cannot be reached for any available sample sizes.

This is a clear illustration that a rapidly varying distribution, like the Weibull distribution with exponent smaller than one, i.e., a Stretched-Exponential distribution, can be mistaken for a Pareto or any other regularly varying distribution for any practical applications.

3.3 Generation of a long memory process with a well-defined stationary distribution

In order to study the performance of the various estimators of the tail index and the influence of interdependence of sample values, we have generated several samples with distinct properties. The first three samples are made of iid realizations drawn respectively from an asymptotic power-law distribution with tail index and from a Stretched-Exponential distribution with exponent and . The other samples contain realizations exhibiting different degrees of time dependence with the same three distributions as for the first three samples: a regularly varying distribution with tail index and a Stretched-Exponential distribution with exponent and . Thus, the three first samples are the iid counterparts of the later ones. The sample with regularly varying iid distributions converges to the Fréchet’s maximum domain of attraction with , while the iid Stretched-Exponential distribution converges to Gumbel’s maximum domain of attraction with . We now study how well can one distinguish between these two distributions belonging to two different maximum domains of attraction.

For the stochastic processes with temporal dependence, we use a simple stochastic volatility model. First, we construct a Markovian Gaussian process whose correlation function is

| (11) |

Varying allows us to change the strength of the time dependence, characterized by the correlation length . When , the iid case is retrieved. In the following, we have chosen and , which correspond to correlation lengths of about 20 and 100 lags respectively. For simplicity, we will refer to the first case as the “short-memory” process, while the second one will be called “long-memory” process. This denomination is only for convenience and does not refer to the conventional distinction between processes with short and long range memory [Beran94].

The next step consists in building the process , defined by

| (12) |

where is the Gaussian distribution function. The process exhibits also a dependence qualitatively similar to that of the process . The precise nature of the temporal dependence of the process is revealed differently by different tools Indeed, if one quantifies dependence by copulas, then the process has the same dependence as because copulas are invariant under a strickly increasing change of variables. Let us recall that a copula is the mathematical embodiment of the dependence structure between different random variables [Joe97, Nelsen98]. The process thus possesses a Gaussian copula dependence structure with long memory and uniform marginals. In contrast, if one quantifies the dependence by the correlation coefficient or the correlation ratio or other reasonable standard measures of dependence, the monotonous change of variable (12) is no more innocuous as the correlation may become as small as one wants under an suitable choice of a strickly increasing transformation (see for instance [Malconcept] for a detailed discussion of the effect of conditioning on correlation measures). However, in the present case, we can calculate exactly the correlation function of the process , which is nothing but the rank (or Spearman) correlation function of the process , so that

| (13) | |||||

| (14) | |||||

| (15) |

For our purpose, the important point is to obtain a process with the correct asymptotic distribution tails together with some dependence: this allows us to probe some impact of the dependence on estimators and show that standard statistical estimators may become unreliable.

In the last step, we define the volatility process

| (16) |

which ensures that the stationary distribution of the volatility is a Pareto distribution with tail index . Such a distribution of the volatility is not realistic in the bulk which is found to be approximately a lognormal distribution for not too large volatilities [SSA00], but is in agreement with the hypothesis of an asymptotic regularly varying distribution. A change of variable more complicated than (16) can provide a more realistic behavior of the volatility on the entire range of the distribution but our main goal is not to provide a realistic stochastic volatility model but only to exhibit a stochastic process with time dependence and well-defined prescribed marginals in order to test the influence of the dependence structure.

The return process is then given by

| (17) |

where the are Gaussian random variables independent from . The construction (17) ensures the de-correlation of the returns at every time lag. The stationary distribution of admits the density

| (18) |

which is regularly varying at infinity since goes to . This completes the construction and characterization of our long memory process with regularly varying stationary distribution.

In order to obtain a process with Stretched-Exponential distribution with long range dependence, we apply to the following increasing mapping

| (19) |

This transformation gives a stretched exponential of index for all values of the return larger than the scale factor . This derives from the fact that the process admits a regularly varying distribution function, characterized by , for some slowly varying function . As a consequence, the stationary distribution of is given by

| (20) | |||||

| (21) |

which is a Stretched-Exponential distribution.

To summarize, starting with a Markovian Gaussian process, we have defined a stochastic process characterized by a stationary distribution function of our choice, thanks to the invariance of the temporal dependence structure (the copula) under strictly increasing change of variable. In particular, this approach gives stochastic processes with a regularly varying marginal distribution and with a stretched-exponential distribution. Notwithstanding the difference in their marginals, these two processes possess by construction exactly the same time dependence. This allows us to compare the impact of the same dependence on these two classes of marginals.

3.4 Results of numerical simulations

We have generated replications of each process presented in the previous section, i.e., iid Stretched-Exponential, iid Pareto, short and long memory processes with a Pareto distribution and with a Stretched-Exponential distribution. Each sample contains realizations, which is approximately the number of points in each tail of our real samples.

Panel (a) of table 2 presents the mean values and standard deviations of the Maximum Likelihood estimates of , using the Generalized Extreme Value distribution and the Generalized Pareto Distribution for the three samples of iid data. To estimate the parameters of the GEV distribution and study the influence of the sub-sample size, we have grouped the data in clusters of size and . For the analysis in terms of the GPD, we have considered four different large thresholds , corresponding to the quantiles , , and . The estimates of obtained from the distribution of maxima are compatible (at the confidence level) with the expected value for the Stretched-Exponential with for all cluster sizes and for the Pareto distribution for clusters of size larger than 10. For the Stretched-Exponential with fractional exponent , we obtain an average value larger than over the four different sizes of sub-samples. Except for the largest cluster, this value is significantly different from the theoretical value . This clearly shows that the distribution of the maximum drawn from a Stretched-Exponential distribution with converges very quickly toward the theoretical asymptotic GEV distribution, while for the convergence is extremely slow. Such a fast convergence for is not surprising since, for this value of the fractional index, the Stretched-Exponential distribution remains close to the Exponential distribution, which is known to converge very quickly to the GEV distribution [HW79]. For , the Stretched-Exponential distribution behaves, over a wide range, like the power law - as we shall see in the next section - thus it is not surprising to obtain an estimate of which remains significantly positive.

Overall, the results are slightly better for the Maximum Likelihood estimates obtained from the GPD. Indeed, the bias observed for the Stretched-Exponential with seems smaller for large quantiles than the smallest biases reached by the GEV method. Thus, it appears that the distribution of exceedance converges faster to its asymptotic distribution than the distribution of maximum. However, while in line with the theoretical values, the standard deviations are found almost always larger than in the previous case, which testifies of the higher variability of this estimator. Thus, for such sample sizes, the GEV and GPD Maximum Likelihood estimates should be handled with care and there results interpreted with caution due to possibly important bias and statistical fluctuations. If a small value of seems to allow one to reliably conclude in favor of a rapidly varying distribution, a positive estimate does not appear informative, and in particular does not allow one to reject the rapidly varying behavior of a distribution.

Panel (b) and (c) of table 2 presents the same results for data with short and long memory, respectively. We note the presence of a significant downward bias (with respect to the iid case) in almost every cases for the GPD estimates: the stronger the dependence, the more important is the bias. At the same time, the empirical values of the standard deviations remain comparable with those obtained in the previous case for iid data. The downward bias can be ascribed to the dependence between data. Indeed, positive dependence yields important clustering of extremes and accumulation of realizations around some values, which – for small samples – could (misleadingly) appear as the consequence of the compactness of the support of the underlying distribution. This rationalizes the negative estimates obtained for the Stretched-Exponential distribution with . In other words, for finite sample, the dependence prevents the full exploration of the tails and create clusters that mimics a thinner tail (even if the clusters are occurring all at large values since what is important is the range of exploration of the tail in order to control the value of ).

The situation is different for the GEV estimates which show either an upward or downward bias (with respect to the iid case). Here two effects are competing. On the one hand, the dependence creates a downward bias, as explained above, while, on the other hand, the lack of convergence of the distribution of maxima toward its GEV asymptotic distribution results in an upward bias, as observed on iid data. This last phenomemon is strengthened by the existence of time dependence which leads to decrease the “effective” sample size ( the actual size divided by the correlation length ) and thus slows down the convergence rate toward the asymptotic distribution even more. Interestingly, both the GEV and GPD estimators for the Pareto distribution may be utterly wrong in presence of long range dependence for any cluster sizes.

To summarize, two opposite effects are competing. On the one hand, non-asymptotic effects due to the slow convergence toward the asymptotic GEV or GPD distributions yield an upward or downward bias. This effect seems more pronounced for GEV distributions and becomes more important when the correlation length increases since the “effective” sample size decreases. On the other hand, the presence of dependence in the data induces a downward bias and sometimes an increase of the standard deviation of the estimated values. The qualitative effect can be described as follows: the larger is, the smaller is the -estimate, provided - of course - that the “effective” sample size is kept constant, everything being otherwise taken equal.

These two entangled effects, which sometimes compete and sometimes oppose each other, have also been observed for non-Markovian processes drawn from Gaussian processes with long range correlation. Thus, the existence of an important bias and the increase in the scattering of estimates is a general and genuine progeny of the time dependence. It leads us to the conclusion that the Maximum Likelihood estimators derived from the GEV or GPD distributions are not very efficient for the investigation of the financial data whose sample sizes are moderate and which exhibit complicated serial dependence. The only positive note is that the GPD estimator correctly recovers the range of the index with an uncertainty smaller than for data with a pure Pareto distribution while it is cannot reject the hypothesis that when the data is generated with a Stretched-Exponential distribution, albeit with a very large uncertainty, in other words with little power.

Table 3 focuses on the results given by Pickands’ estimator for the tail index of the GPD. For each thresholds , corresponding to the quantiles , , and respectively, the results of our simulations are given for two particular values of (defined in (9)) corresponding to , which is the largest admissible value, and corresponding to be sufficiently far in the tail of the GPD. Table 3 provides the mean value and the numerically estimated as well as the theoretical (given by (10)) standard deviation of . Panel (a) gives the result for iid data. The mean values do not exhibit a significant bias for the Pareto distribution and the Stretched-Exponential with , but are utterly wrong in the case since the estimates are comparable with those given for the Pareto distribution. In each case, we note a very good agreement between the empirical and theoretical standard deviations, even for the larger quantiles (and thus the smaller samples). Panels (b-c) present the results for dependent data. The estimated standard deviations remains of the same order as the theoretical ones, contrarily to results reported by \citeasnounKP97 for IGARCH processes. However, like these authors, we find that the bias, either positive or negative, becomes very significant and leads one to misclassify a Stretched-Exponential distribution with for a Pareto distribution with . Thus, in presence of dependence, Pickands’ estimator is unreliable.

To summarize, the determination of the maximum domain of attraction with usual estimators does not appear to be a very efficient way to study the extreme properties of dependent times series. Almost all the previous studies which have investigated the tail behavior of asset returns distributions have focused on these methods (see the influential works of \citeasnounLongin96 for instance) and may thus have led to spurious results on the determination of the tail behavior. In particular, our simulations show that rapidly varying function may be mistaken for regularly varying functions. Thus, according to our simulations, this casts doubts on the strength of the conclusion of previous works that the distributions of returns are regularly varying as seems to have been the consensus until now and suggests to re-examine the possibility that the distribution of returns may be rapidly varying as suggested by \citeasnounGJ98 or \citeasnounLS99 for instance. We now turn to this question using the framework of GEV and GDP estimators just described.

3.5 GEV and GPD estimators of the Dow Jones and Nasdaq data sets

We have applied the same analysis as in the previous section on the real samples of the Dow Jones and Nasdaq (raw and corrected) returns. In order to estimate the standard deviations of Pickands’ estimator for the GPD derived from the upper quantiles of these distributions, and of ML-estimators for the distribution of maximum and for the GPD, we have randomly generated one thousand sub-samples, each sub-sample being constituted of ten thousand data points in the positive or negative parts of the samples respectively (with replacement). It should be noted that the ML-estimates themselves were derived from the full samples. The results are given in tables 4 and 5.

These results confirm the confusion about the tail behavior of the returns distributions and it seems impossible to exclude a rapidly varying behavior of their tails. Indeed, even the estimations performed by Maximum Likelihood with the GPD tail index, which have appeared as the least unreliable estimator in our previous tests, does not allow us to clearly reject the hypothesis that the tails of the empirical distributions of returns are rapidly varying, in particular for large quantile values. For the Nasdaq dataset, accounting for the lunch effect does not yield any significant change in the estimations. This observation will be confirmed by the other tests presented in the next sections.

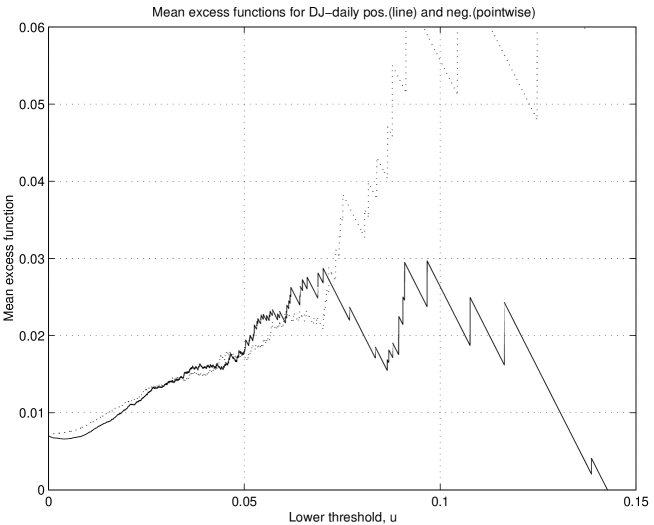

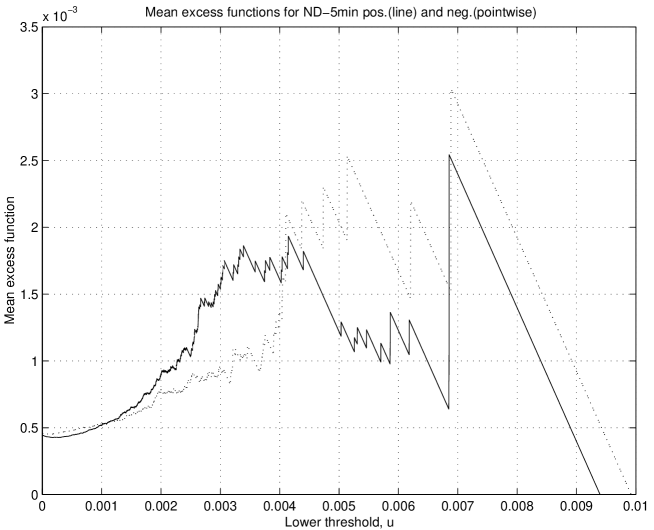

As a last non-parametric attempt to distinguish between a regularly varying tail and a rapidly varying tail of the exponential or Stretched-Exponential families, we study the Mean Excess Function which is one of the known methods that often can help in deciding what parametric family is appropriate for approximation (see for details \citeasnounEKM97). The Mean Excess Function of a random value (also called “shortfall” when applied to negative returns in the context of financial risk management) is defined as

| (22) |

The Mean Excess Function is obviously related to the GPD for sufficiently large threshold and its behavior can be derived in this limit for the three maximum domains of attraction. In addition, more precise results can be given for particular random variables, even in a non-asymptotic regime. Indeed, for an exponential random variable , the is just a constant. For a Pareto random variable, the is a straight increasing line, whereas for the Stretched-Exponential and the Gauss distributions, the is a decreasing function. We evaluated the sample analogues of the [EKM97, p.296] which are shown in figure 4. All attempts to find a constant or a linearly increasing behavior of the on the main central part of the range of returns were ineffective. In the central part of the range of negative returns ; for ND data, and ; for DJ data), the behaves like a convex function which exclude both exponential and power (Pareto) distributions. Thus, the tool does not support using any of these two distributions.

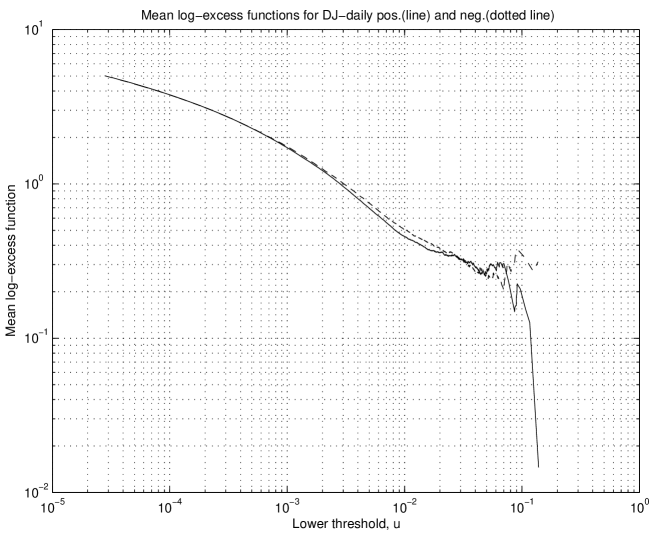

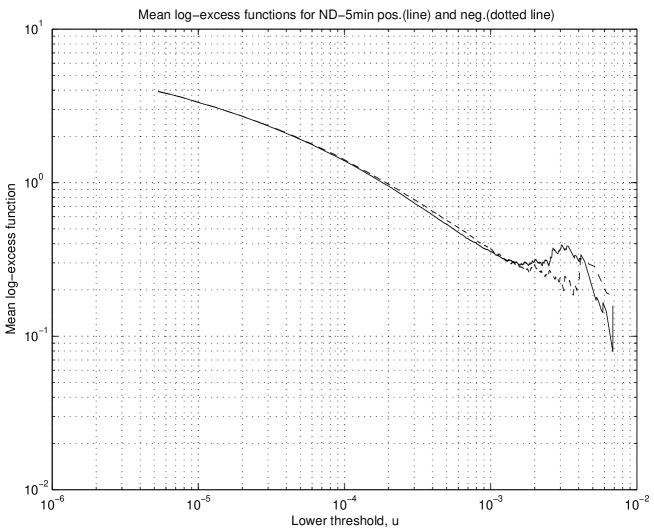

An alternative to the Mean Excess function is provided by the Mean Log-Excess function:

| (23) |

is again related to the GPD (of the variable instead of ) for sufficiently large threhold . In particular, when follows asymtotically a power law, is asymptotically exponentially distributed, so that goes to a constant equal to , where denotes the tail index of the distribution of . For a Stretched-Exponential variable with fractional exponent , it turns out that behaves like a regularly varying function whose tail index equals . Thus, in a double logarithmic plot, such a behavior is characterized by a decreasing straigth line with slope . Sample estimates of are shown in figure 5. On about of the range of the sample, the Mean Log-Excess functions behaves as expected for Stretched-Exponentially distributed variables, while in the tail range (about of the largest values), the results are very confusing, due to the importance of the statistical fluctuations. Such behavior of in the tails cannot be attributed definitely to a regularly varying or to a Stretched-Exponentially distributed random variable. Therefore, a change of regime cannot be excluded in the extreme tail of the distributions.

In view of the stalemate reached with the above non-parametric approaches and in particular with the standard extreme value estimators, the sequel of this paper is devoted to the investigation of a parametric approach in order to decide which class of extreme value distributions, rapidly versus regularly varying, accounts best for the empirical distributions of returns.

4 Fitting distributions of returns with parametric densities

Since our previous results lead to doubt the validity of the rejection of the hypothesis that the distribution of returns are rapidly varying, we now propose to pit a parametric champion for this class of functions against the Pareto champion of regularly varying functions. To represent the class of rapidly varying functions, we propose the family of Stretched-Exponentials. As discussed in the introduction, the class of stretched exponentials is motivated in part from a theoretical view point by the fact that the large deviations of multiplicative processes are generically distributed with stretched exponential distributions [FrischSor]. Stretched exponential distributions are also parsimonious examples of sub-exponential distributions with fat tails for instance in the sense of the asymptotic probability weight of the maximum compared with the sum of large samples [Feller]. Notwithstanding their fat-tailness, Stretched Exponential distributions have all their moments finite666However, they do not admit an exponential moment, which leads to problems in the reconstruction of the distribution from the knowledge of their moments [SO94]., in contrast with regularly varying distributions for which moments of order equal to or larger than the index are not defined. This property may provide a substantial advantage to exploit in generalizations of the mean-variance portfolio theory using higher-order moments [R73, FL97, HS99, SSA00, AS01, JM02, MSmm02, for instance ]. Moreover, the existence of all moments is an important property allowing for an efficient estimation of any high-order moment, since it ensures that the estimators are asymptotically Gaussian. In particular, for Stretched-Exponentially distributed random variables, the variance, skewness and kurtosis can be well estimated, contrarily to random variables with regularly varying distribution with tail index in the range .

4.1 Definition of two parametric families

4.1.1 A general -parameters family of distributions

We thus consider a general -parameters family of distributions and its particular restrictions corresponding to some fixed value(s) of two (one) parameters. This family is defined by its density function given by:

| (24) |

Here, are unknown parameters, is a known lower threshold that will be varied for the purposes of our analysis and is a normalizing constant given by the expression:

| (25) |

where denotes the (non-normalized) incomplete Gamma function. The parameter ranges from minus infinity to infinity while and range from zero to infinity. In the particular case where , the parameter also needs to be positive to ensure the normalization of the probability density function (pdf). The interval of definition of this family is the positive semi-axis. Negative log-returns will be studied by taking their absolute values. The family (24) includes several well-known pdf’s often used in different applications. We enumerate them.

-

1.

The Pareto distribution:

(26) which corresponds to the set of parameters with . Several works have attempted to derive or justified the existence of a power tail of the distribution of returns from agent-based models [chalmar], from optimal trading of large funds with sizes distributed according to the Zipf law [gabaixstan] or from stochastic processes [SF02, Biham98, 2002].

-

2.

The Weibull distribution:

(27) with parameter set and normalization constant . This distribution is said to be a “Stretched-Exponential” distribution when the exponent is smaller than , namely when the distribution decays more slowly than an exponential distribution.

-

3.

The exponential distribution:

(28) with parameter set and normalization constant . For sufficiently high quantiles, the exponential behavior can for instance derive, from the hyperbolic model introduced by \citeasnounEberlein or from a simple model where stock price dynamics is governed by a geometrical (multiplicative) Brownian motion with stochastic variance. \citeasnounDragu have found an excellent fit of the Dow-Jones index for time lags from 1 to 250 trading days with a model with an asymptotic exponential tail of the distribution of log-returns.

-

4.

The incomplete Gamma distribution:

(29) with parameter set and normalization . Such an asymptotic tail behavior can, for instance, be observed for the generalized hyperbolic models, whose description can be found in \citeasnounPrause.

Thus, the Pareto distribution (PD) and exponential distribution (ED) are one-parameter families, whereas the stretched exponential (SE) and the incomplete Gamma distribution (IG) are two-parameter families. The comprehensive distribution (CD) given by equation (24) contains three unknown parameters.

Interesting links between these different models reveal themselves under specific asymptotic conditions. Very interesting for our present study is the behavior of the (SE) model when and . In this limit, and provided that

| (30) |

the (SE) model goes to the Pareto model. Indeed, we can write

| (31) | |||||

which is the pdf of the (PD) model with tail index . The condition (30) comes naturally from the properties of the maximum-likelihood estimator of the scale parameter given by equation (52) in Appendix A. It implies that, as , the characteristic scale of the (SE) model must also go to zero with to ensure the convergence of the (SE) model towards the (PD) model.

This shows that the Pareto model can be approximated with any desired accuracy on an arbitrary interval by the (SE) model with parameters satisfying equation (30) where the arrow is replaced by an equality. Although the value does not give strickly speaking a Stretched-Exponential distribution, the limit provides any desired approximation to the Pareto distribution, uniformly on any finite interval . This deep relationship between the SE and PD models allows us to understand why it can be very difficult to decide, on a statistical basis, which of these models fits the data best.

Another interesting behavior is obtained in the limit , where the Pareto model tends to the Exponential model [BP00]. Indeed, provided that the scale parameter of the power law is simultaneously scaled as , we can write the tail of the cumulative distribution function of the PD as which is indeed of the form for large . Then, for . This shows that the Exponential model can be approximated with any desired accuracy on intervals by the (PD) model with parameters satisfying , for any positive constant A. Although the value does not give strickly speaking a Exponential distribution, the limit provides any desired approximation to the Exponential distribution, uniformly on any finite interval . This limit is thus less general that the SE PD limit since it is valid only asymptotically for while can be finite in the SE PD limit.

4.1.2 The log-Weibull family of distributions

Let us also introduce the two-parameter log-Weibull family:

| (32) |

whose density is

| (33) |

This family of pdf interpolates smoothly between the Stretched-Exponential and Pareto classes. It recovers the Pareto family for , in which case the parameter is the tail exponent. For larger than , the tail of the log-Weibull is thinner than any Pareto distribution but heavier than any Stretched-Exponential777A generalization of the SLE to the following three-parameter family also contains the SE family in some formal limit. Consider indeed for , which has the same tail as expression (32). Taking together with with finite yields .. In particular, when equals two, the log-normal distribution is retrieved (above threshold ). For smaller than , the tails of the SLE are even heavier than any Pareto distributions. This range of parameter is probably not useful except maybe to account of “outliers” in the spirit of \citeasnounJS02; this will require a specific investigation.

4.2 Methodology

We start with fitting our two data sets (DJ and ND) by the five distributions enumerated above (24) and (26-29). Our first goal is to show that no single parametric representation among any of the cited pdf’s fits the whole range of the data sets. Recall that we analyze separately positive and negative returns (the later being converted to the positive semi-axis). We shall use in our analysis a movable lower threshold , restricting by this threshold our sample to observations satisfying to .

In addition to estimating the parameters involved in each representation (24,26-29) by maximum likelihood for each particular threshold 888The estimators and their asymptotic properties are derived in Appendix A., we need a characterization of the goodness-of-fit. For this, we propose to use a distance between the estimated distribution and the sample distribution. Many distances can be used: mean-squared error, Kullback-Liebler distance999 This distance (or divergence, strictly speaking) is the natural distance associated with maximum-likelihood estimation since it is for these values of the estimated parameters that the distance between the true model and the assumed model reaches its minimum., Kolmogorov distance, Sherman distance (as in \citeasnounLongin96) or Anderson-Darling distance, to cite a few. We can also use one of these distances to determine the parameters of each pdf according to the criterion of minimizing the distance between the estimated distribution and the sample distribution. The chosen distance is thus useful both for characterizing and for estimating the parametric pdf. In the later case, once an estimation of the parameters of particular distribution family has been obtained according to the selected distance, we need to quantify the statistical significance of the fit. This requires to derive the statistics associated with the chosen distance. These statistics are known for most of the distances cited above, in the limit of large sample.

We have chosen the Anderson-Darling distance to derive our estimated parameters and perform our tests of goodness of fit. The Anderson-Darling distance between a theoretical distribution function and its empirical analog , estimated from a sample of realizations, is evaluated as follows:

| (34) | |||||

| (35) |

where , and is its ordered sample. If the sample is drawn from a population with distribution function , the Anderson-Darling statistics (ADS) has a standard AD-distribution free of the theoretical df F(x) [AD52], similarly to the for the -statistic, or the Kolmogorov distribution for the Kolmogorov statistic. It should be noted that the ADS weights the squared difference in eq.(34) by which is nothing but the inverse of the variance of the difference in square brackets. The AD distance thus emphasizes more the tails of the distribution than, say, the Kolmogorov distance which is determined by the maximum absolute deviation of from or the mean-squared error, which is mostly controlled by the middle of range of the distribution. Since we have to insert the estimated parameters into the ADS, this statistic does not obey any more the standard AD-distribution: the ADS decreases because the use of the fitting parameters ensures a better fit to the sample distribution. However, we can still use the standard quantiles of the AD-distribution as upper boundaries of the ADS. If the observed ADS is larger than the standard quantile with a high significance level , we can then conclude that the null hypothesis is rejected with significance level larger than . If we wish to estimate the real significance level of the ADS in the case where it does not exceed the standard quantile of a high significance level, we are forced to use some other method of estimation of the significance level of the ADS, such as the bootstrap method.

In the following, the estimates minimizing the Anderson-Darling distance will be refered to as AD-estimates. The maximum likelihood estimates (ML-estimates) are asymptotically more efficient than AD-estimates for independent data and under the condition that the null hypothesis (given by one of the four distributions (26-29), for instance) corresponds to the true data generating model. When this is not the case, the AD-estimates provide a better practical tool for approximating sample distributions compared with the ML-estimates.

We have determined the AD-estimates for standard significance levels given in table 6. The corresponding sample quantiles corresponding to these significance levels or thresholds for our samples are also shown in table 6. Despite the fact that thresholds vary from sample to sample, they always corresponded to the same fixed set of significance levels throughout the paper and allows us to compare the goodness-of-fit for samples of different sizes.

4.3 Empirical results

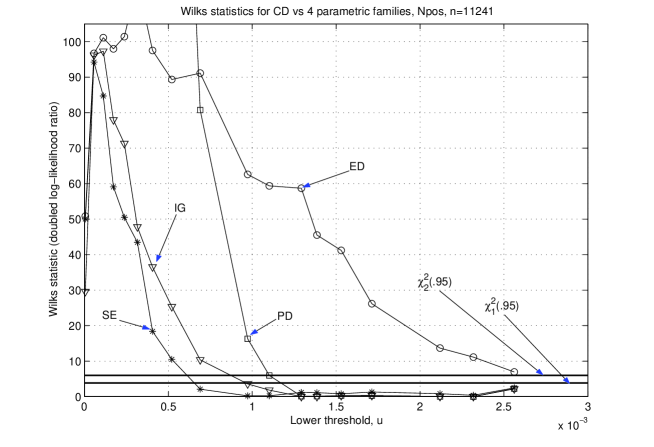

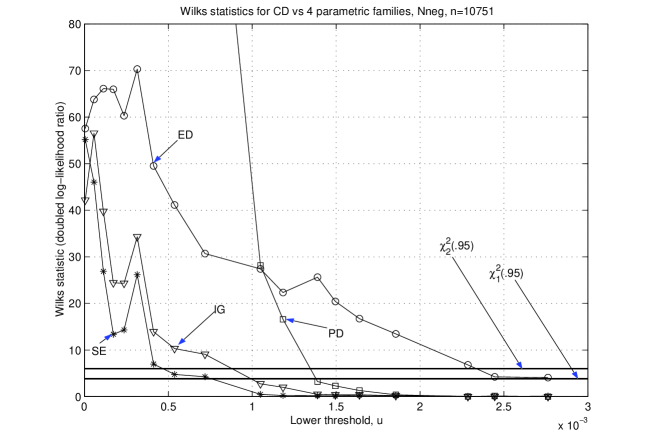

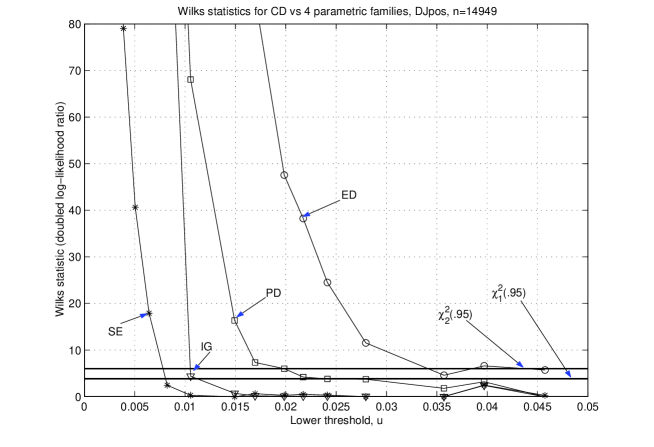

The Anderson-Darling statistics (ADS) for six parametric distributions (Weibull or Stretched-Exponential, Generalized Pareto, Gamma, Exponential, Pareto and Log-Weibull) are shown in table 7 for two quantile ranges, the first top half of the table corresponding to the lowest thresholds while the second bottom half corresponds to the highest ones. For the lowest thresholds, the ADS rejects all distributions, except the Stretched-Exponential for the Nasdaq. Thus, none of the considered distributions is really adequate to model the data over such large ranges. For the highest quantiles, only the exponential model is rejected at the confidence level. The Log-Weibull and the Stretched-Exponential distributions are the best, just above the Pareto distribution and the Incomplete Gamma that cannot be rejected. We now present an analysis of each case in more details.

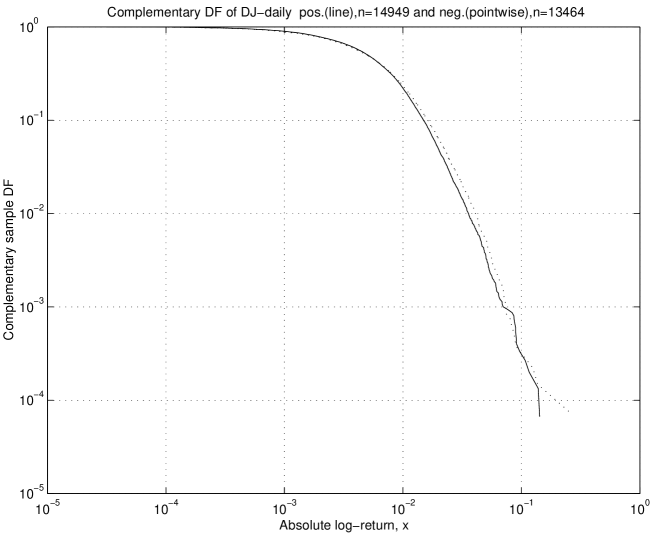

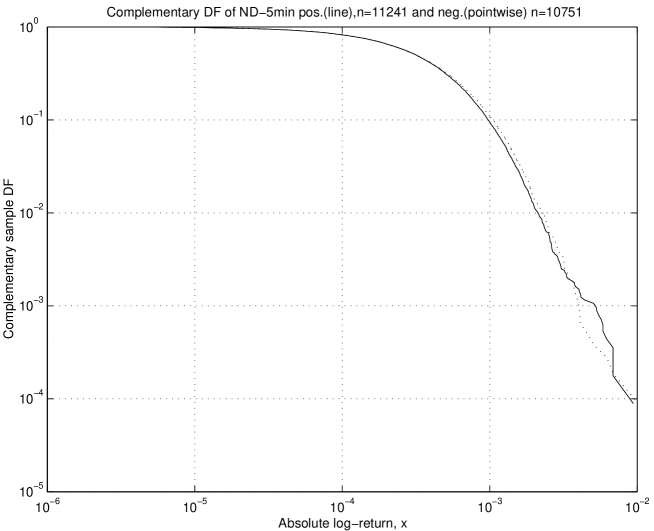

4.3.1 Pareto distribution

Figure 6a shows the cumulative sample distribution function for the Dow Jones Industrial Average index, and in figure 6b the cumulative sample distribution function for the Nasdaq Composite index. The mismatch between the Pareto distribution and the data can be seen with the naked eye: if samples were taken from a Pareto population, the graph in double log-scale should be a straight line. Even in the tails, this is doubtful. To formalize this impression, we calculate the Hill and AD estimators for each threshold . Denoting the ordered sub-sample of values exceeding where is the size of this sub-sample, the Hill maximum likelihood estimate of parameter is [Hill75]

| (36) |

The standard deviations of can be estimated as

| (37) |

under the assumption of iid data, but very severely underestimate the true standard deviation when samples exhibit dependence, as reported by \citeasnounKP97.

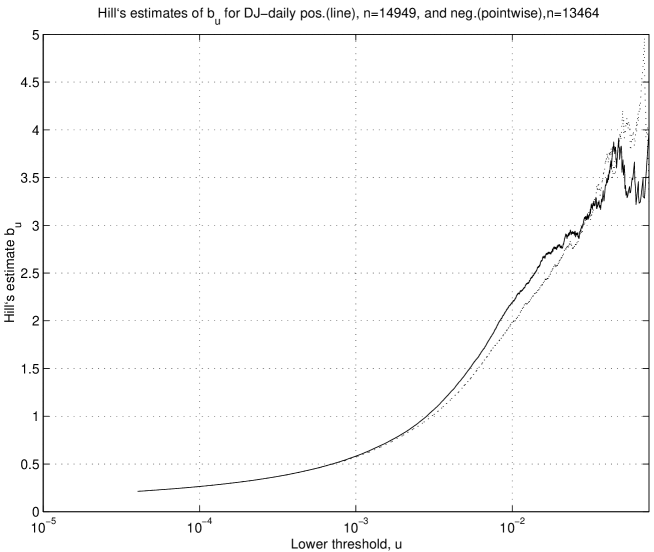

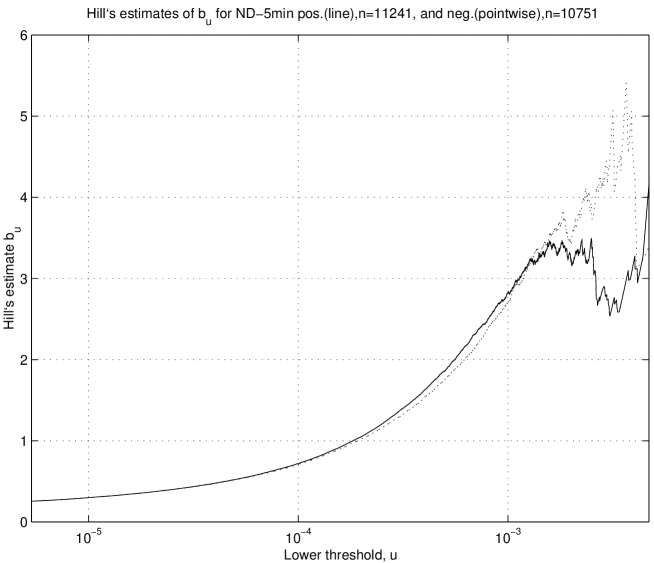

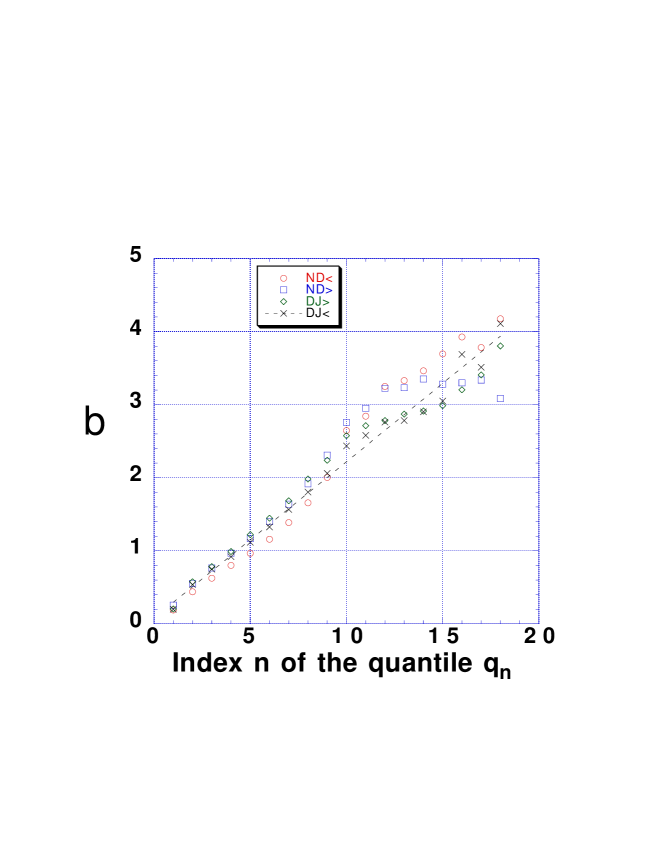

Figure 7a and 7b shows the Hill estimates as a function of for the Dow Jones and for the Nasdaq. Instead of an approximately constant exponent (as would be the case for true Pareto samples), the tail index estimator increases until , beyond which it seems to slow its growth and oscillates around a value up to the threshold . It should be noted that the interval contains of the sample whereas the interval contains only of the sample. The behavior of for the ND shown in figure 7b is similar: Hill’s estimate seems to slow its growth already at corresponding to the quantile. Are these slowdowns of the growth of genuine signatures of a possible constant well-defined asymptotic value that would qualify a regularly varying function?

As a first answer to this question, table 8 compares the AD-estimates of the tail exponent with the corresponding maximum likelihood estimates for the 18 intervals . Both maximum likelihood and Anderson-Darling estimates of steadily increase with the threshold (except for the highest quantiles of the positive tail of the Nasdaq). The corresponding figures for positive and negative returns are very close to each other and almost never significantly different at the usual confidence level. Some slight non-monotonicity of the increase for the highest thresholds can be explained by small sample sizes. One can observe that both MLE and ADS estimates continue increasing as the interval of estimation is contracting to the extreme values. It seems that their growth potential has not been exhausted even for the largest quantile , except for the positive tail of the Nasdaq sample. This statement might not be very strong as the standard deviations of the tail index estimators also grow when exploring the largest quantiles. However, the non-exhausted growth is observed for three samples out of the four tails. Moreover, this effect is seen for several threshold values while random fluctuations would distort the -curve in a random manner rather than according to the increasing trend observed in three out of four tails.

Assuming that the observation, that the sample distribution can be approximated by a Pareto distribution with a growing index , is correct, an important question arises: how far beyond the sample this growth will continue? Judging from table 8, we can think this growth is still not exhausted. Figure 8 suggests a specific form of this growth, by plotting the hill estimator for all four data sets (positive and negative branches of the distribution of returns for the DJ and for the ND) as a function of the index of the quantiles or standard significance levels given in table 6. Similar results are obtained with the AD estimates. Apart from the positive branch of the ND data set, all other three branches suggest a continuous growth of the Hill estimator as a function of . Since the quantiles given in table 6 have been chosen to converge to approximately exponentially as

| (38) |

the linear fit of as a function of shown as the dashed line in figure 8 corresponds to

| (39) |

Expression (39) suggests an unbound logarithmic growth of as the quantile approaches . For instance, for a quantile , expression (39) predicts . For a quantile , expression (39) predicts , and so on. Each time the quantile is divided by a factor , the apparent exponent is increased by the additive constant : . This very slow growth uncovered here may be an explanation for the belief and possibly mistaken conclusion that the Hill and other estimators of the tail index tends to a constant for high quantiles. Indeed, it is now clear that the slowdowns of the growth of seen in figures 7 decorated by large fluctuations due to small size effects is mostly the result of a dilatation of the data expressed in terms of threshold . When recast in the more natural logarithm scale of the quantiles , this slowdown disappears. Of course, it is impossible to know how long this growth given by (39) may go on as the quantile tends to . In other words, how can we escape from the sample range when estimating quantiles? How can we estimate the so-called “high quantiles” at the level where is the total number of sampled points. \citeasnounEKM97 have summarized the situation in this way: “there is no free lunch when it comes to high quantiles estimation!” It is possible that will grow without limit as would be the case if the true underlying distribution was rapidly varying. Alternatively, may saturate to a large value, as predicted for instance by the traditional GARCH model which yields tails indices which can reach [EP01, SP99] or by the recent multifractal random walk (MRW) model which gives an asymptotic tail exponent in the range [Muzyetal, musor]. According to (39), a value (respectively ) would be attained for (respectively )! If one believes in the prediction of the MRW model, the tail of the distribution of returns is regularly varying but this insight is completely useless for all practical purposes due to the astronomically high statistics that would be needed to sample this regime. In this context, we cannot hope to get access to the true nature of the pdf of returns but only strive to define the best effective or apparent most parsimonious and robust model. By comparing distributions of aggregated returns with their corresponding reshuffled counterparts, \citeasnounViswanathan suggest that the fat tail nature of the returns result mainly from the existence of long-range dependence, in agreement with the construction of GARCH and MRW processes.

4.3.2 Weibull distributions

Let us now fit our data with the Weibull (SE) distribution (27). The Anderson-Darling statistics (ADS) for this case are shown in table 7. The ML-estimates and AD-estimates of the form parameter are represented in table 9. Table 7 shows that, for the highest quantiles, the ADS for the Stretched-Exponential is the smallest of all ADS, suggesting that the SE is the best model of all. Moreover, for the lowest quantiles, it is the sole model not systematically rejected at the level.