Asymptotics of Plancherel measures for symmetric groups

Abstract.

We consider the asymptotics of the Plancherel measures on partitions of as goes to infinity. We prove that the local structure of a Plancherel typical partition in the middle of the limit shape converges to a determinantal point process with the discrete sine kernel.

On the edges of the limit shape, we prove that the joint distribution of suitably scaled 1st, 2nd, and so on rows of a Plancherel typical diagram converges to the corresponding distribution for eigenvalues of random Hermitian matrices (given by the Airy kernel). This proves a conjecture due to Baik, Deift, and Johansson by methods different from the Riemann-Hilbert techniques used in their original papers [2, 3] and from the combinatorial proof given in [23].

Our approach is based on an exact determinantal formula for the correlation functions of the poissonized Plancherel measures in terms of a new kernel involving Bessel functions. Our asymptotic analysis relies on the classical asymptotic formulas for the Bessel functions and depoissonization techniques.

1. Introduction

1.1. Plancherel measures

Given a finite group , by the corresponding Plancherel measure we mean the probability measure on the set of irreducible representations of which assigns to a representation the weight . For the symmetric group , the set is the set of partitions of the number , which we shall identify with Young diagrams with squares throughout this paper. The Plancherel measure on partitions arises naturally in representation–theoretic, combinatorial, and probabilistic problems. For example, the Plancherel distribution of the first part of a partition coincides with the distribution of the longest increasing subsequence of a uniformly distributed random permutation [28].

We denote the Plancherel measure on partitions of by

| (1.1) |

where is the dimension of the corresponding representation of . The asymptotic properties of these measures as have been studied very intensively, see the References and below.

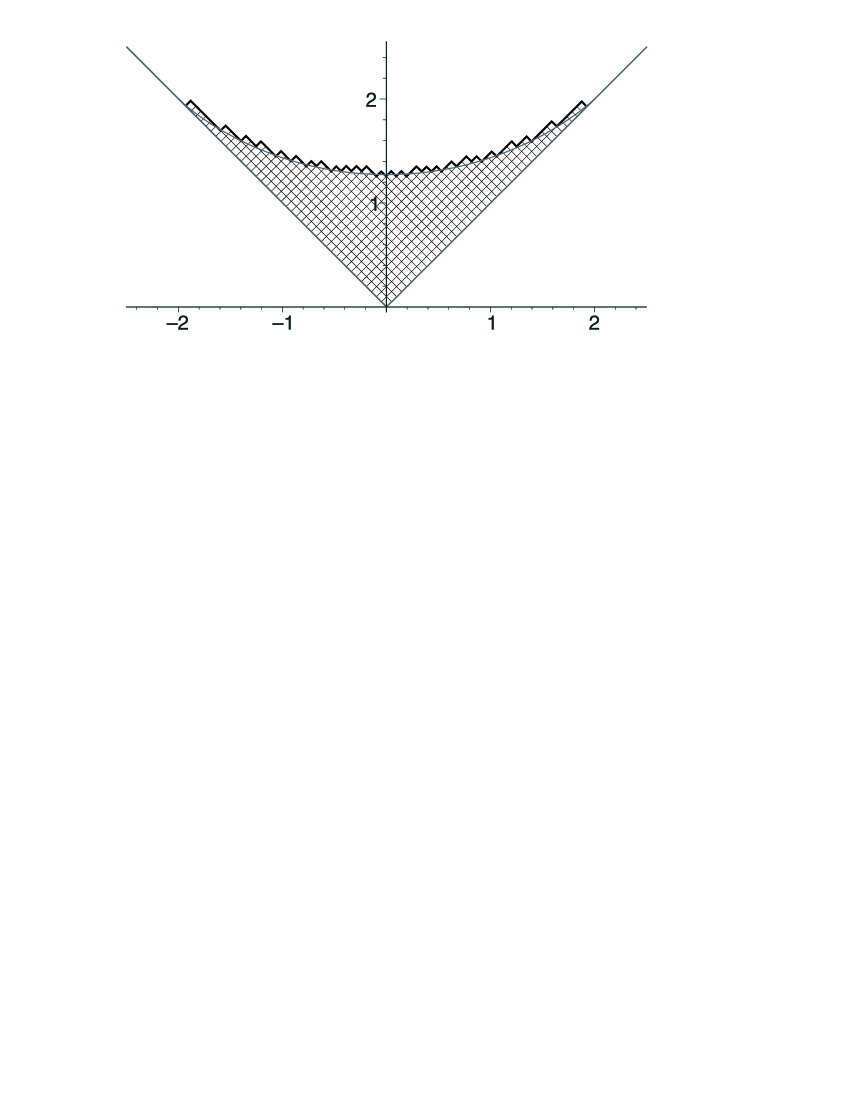

In the seventies, Logan and Shepp [21] and, independently, Vershik and Kerov [36, 38] discovered the following measure concentration phenomenon for as . Let be a partition of and let and be the usual coordinates on the diagrams, namely, the row number and the column number. Introduce new coordinates and by

that is, we flip the diagram, rotate it as in Figure 1, and scale it by the factor of in both directions.

After this scaling, the Plancherel measures converge as (see [21, 36, 38] for precise statements) to the delta measure supported on the following shape:

where the function is defined by

The function is plotted in Figure 1. As explained in great detail in [20], this limit shape is very closely connected to Wigner’s semicircle law for distribution of eigenvalues of a random matrices, see also [17, 18, 19].

From a different point of view, the connection with random matrices was observed in [2, 3], and also in the earlier papers [14, 25, 26]. In [2], Baik, Deift, and Johansson made the following conjecture. They conjectured that in the limit and after proper scaling the joint distribution of , becomes identical to the joint distribution of largest eigenvalues of a Gaussian random Hermitian matrix (which is known to be the so-called Airy ensemble, see Section 1.4). They proved this for the individual distribution of and in [2] and [3], respectively. A combinatorial proof of the full conjecture was given by one of us in [23]. It was based on an interplay between maps on surfaces and ramified coverings of the sphere.

In this paper we study the local structure of a typical Plancherel diagram both in the bulk of the limit shape and on its edge, where by the study of the edge we mean the study of the behavior of , , and so on.

We employ an analytic approach based on an exact formula in terms of Bessel functions for the correlation functions of the so-called poissonization of the Plancherel measures , see Theorem 1 in the following section, and the so-called depoissonization techniques, see Section 1.4.

The exact formula in Theorem 1 is a limit case of a formula from [6], see also the recent paper [24] for a more general result. The use of poissonization and depoissonization is very much in the spirit of [2, 14, 35] and represents a well known in statistical mechanics principle of the equivalence of ensembles.

Our main results are the following two. In the bulk of the limit shape , we prove that the local structure of a Plancherel typical partition converges to a determinantal point process with the discrete sine kernel, see Theorem 3. This result is parallel to the corresponding result for random matrices. On the edge of the limit shape, we give an analytic proof of the Baik-Deift-Johansson conjecture, see Theorem 4. These results will be stated in Subsections 1.3 and 1.4 of the present Introduction, respectively.

1.2. Poissonization and correlation functions

For , consider the poissonization of the measures

This is a probability measure on the set of all partitions. Our first result is the computation of the correlation functions of the measures .

By correlation functions we mean the following. By definition, set

Also, following [37], define the modified Frobenius coordinates of a partition by

| (1.2) |

where stands for the symmetric difference of two sets, is the number of squares on the diagonal of , and ’s and ’s are the usual Frobenius coordinates of . Recall that is the number of squares in the th row to the right of the diagonal, and is number of squares in the th column below the diagonal. The equality (1.2) is a well known combinatorial fact discovered by Frobenius, see Ex. I.1.15(a) in [22]. Note that, in contrast to , the set is infinite and, moreover, it contains all but finitely many negative integers.

The sets and have the following nice geometric interpretation. Let the diagram be flipped and rotated as in Figure 1, but not scaled. Denote by a piecewise linear function with whose graph if given by the upper boundary of completed by the lines

Then

In other words, if we consider as a history of a walk on then are those moments when a step is made in the negative direction. It is therefore natural to call the descent set of . As we shall see, the correspondence is a very convenient way to encode the local structure of the boundary of .

The halves in the definition of have the following interpretation: one splits the diagonal squares in half and gives half to the rows and half to the columns.

Definition 1.1.

The correlation functions of are the probabilities that the sets or, similarly, contain a fixed subset . More precisely, we set

| (1.3) | |||||

| (1.4) |

Theorem 1.

For any we have

where the kernel is given by the following formula

| (1.5) |

The functions are defined by

| (1.6) | ||||

| (1.7) |

where is the Bessel function of order and argument .

This theorem is established in Section 2.1, see also Remark 1.2 below. By the complementation principle, see Sections A.3 and 2.2, Theorem 1 is equivalent to the following

Theorem 2.

For any we have

| (1.8) |

Here the kernel is given by the following formula

| (1.9) |

where .

Remark 1.2.

Theorem 1 is a limit case of Theorem 3.3 of [6]. For the reader’s convenience a direct proof of it is given in Section 2. Another proof of the results of [6] will appear in [7]. Various limit cases of the results of [6] are discussed in [8]. By different methods, the formula (1.8) was obtained by K. Johansson [15].

Remark 1.3.

Observe that all Bessel functions involved in the above formulas are of integer order. Also note that the ratios like are entire functions of and because is an entire function of . In particular, the values are well defined. Various denominator–free formulas for the kernel are given in Section 2.1.

1.3. Asymptotics in the bulk of the spectrum

Given a sequence of subsets

where is some fixed integer, we call this sequence regular if the following limits

| (1.10) | ||||

| (1.11) |

exist, finite or infinite. Here . Observe that if is finite then for .

In the case when can be represented as and the distance between and goes to as we shall say that the sequence splits; otherwise, we call it nonsplit. Obviously, is nonsplit if and only if all stay at a finite distance from each other.

Define the correlation functions of the measures by the same rule as in (1.4)

We are interested in the limit of as . This limit will be computed in Theorem 3 below. As we shall see, if splits, then the limit correlations factor accordingly.

Introduce the following discrete sine kernel which is a translation invariant kernel on the lattice

depending on a real parameter :

Here is the Tchebyshev polynomials of the second kind. We agree that

and also that

The following result describes the local structure of a Plancherel typical partition.

Theorem 3.

We prove this theorem in Section 3.

Remark 1.4.

Notice that, in particular, Theorem 3 implies that, as , the shape of a typical partition near any point of the limit curve is described by a stationary random process. For distinct points on the curve these random processes are independent.

Remark 1.5.

Remark 1.6.

The discrete sine kernel was studied before, see [40, 41], mainly as a model case for the continuous sine kernel. In particular, the asymptotics of Toeplitz determinants built from the discrete sign kernel was obtained by H. Widom in [41] answering a question of F. Dyson. As pointed out by S. Kerov, this asymptotics has interesting consequences for the Plancherel measures.

Remark 1.7.

Note that, in particular, Theorem 3 implies that the limit density (the 1-point correlation function) is given by

| (1.14) |

This is in agreement with the Logan-Shepp-Vershik-Kerov result about the limit shape . More concretely, the function is related to the density (1.14) by

which can be interpreted as follows. Approximately, we have

Set . Then the above relation reads and it should be satisfied on the boundary of the limit shape. Since , we conclude that

as was to be shown.

Remark 1.8.

The discrete sine-kernel becomes especially nice near the diagonal, that is, where . Indeed,

1.4. Behavior near the edge of the spectrum and the Airy ensemble

The discrete sine kernel vanishes if . Therefore, it follows from Theorem 3 that the limit correlations vanish if for some . However, as will be shown below in Proposition 4.1, after a suitable scaling near the edge , the correlation functions converge to the correlation functions given by the Airy kernel [11, 32]

Here is the Airy function:

| (1.15) |

In fact, the following more precise statement is true about the behavior of the Plancherel measure near the edge . By symmetry, everything we say about the edge applies to the opposite edge .

Consider the random point process on whose correlation functions are given by the determinants

and let

be its random configuration. We call the random variables ’s the Airy ensemble. It is known [11, 32] that the Airy ensemble describes the behavior of the (properly scaled) 1st, 2nd, and so on largest eigenvalues of a Gaussian random Hermitian matrix. The distribution of individual eigenvalues was obtained by Tracy and Widom in [32] in terms of certain Painlevé transcendents.

It has been conjectured by Baik, Deift, and Johansson that the random variables

converge, in distribution and together with all moments, to the Airy ensemble. They verified this conjecture for individual distribution of and in [2] and [3], respectively. In particular, in the case of , this generalizes the result of [36, 38] that in probability as . The computation of was known as the Ulam problem; different solutions to this problem were given in [1, 14, 29].

Convergence of all expectations of the form

| (1.16) |

to the corresponding quantities for the Airy ensembles was established in [23]. The proof in [23] was based on a combinatorial interpretation of (1.16) as the asymptotics in a certain enumeration problem for random surfaces.

In the present paper we use different ideas to prove the following

Theorem 4.

As , the random variables converge, in joint distribution, to the Airy ensemble.

1.5. Poissonization and depoissonization

We obtain Theorems 3 and 4 from Theorem 1 using the so-called depoissonization techniques. We recall that the fundamental idea of depoissonization is the following.

Given a sequence its poissonization is, by definition, the function

| (1.17) |

Provided the ’s grow not too rapidly this is an entire function of . In combinatorics, it is usually called the exponential generating function of the sequence . Various methods of extracting asymptotics of sequences from their generating functions are classically known and widely used, see for example [35] where such methods are used to obtain the limit shape of a typical partition under various measures on the set of partitions.

A probabilistic way to look at the generating function (1.17) is the following. If then is the expectation of where is a Poisson random variable with parameter . Because has mean and standard deviation , one expects that

| (1.18) |

provided the variations of for are small. One possible regularity condition on which implies (1.18) is monotonicity. In a very general and very convenient form, a depoissonization lemma for nonincreasing nonnegative was established by K. Johansson in [14]. We use this lemma in Section 4 to prove Theorem 4.

Another approach to depoissonization is to use a contour integral

| (1.19) |

where is any contour around . Suppose, for a moment, that is constant . The function has a unique critical point . If we choose as the contour , then only neighborhoods of size contribute to the asymptotics of (1.19). Therefore, for general , we still expect that provided the overall growth of is under control and the variations of for are small, the asymptotically significant contribution to (1.19) will come from . That is, we still expect (1.18) to be valid. See, for example, [13] for a comprehensive discussion and survey of this approach.

We use this approach to prove Theorem 3 in Section 3. The growth conditions on which are suitable in our situation are spelled out in Lemma 3.1.

In our case, the functions are combinations of the Bessel functions. Their asymptotic behavior as can be obtained directly from the classical results on asymptotics of Bessel functions which are discussed, for example, in the fundamental Watson’s treatise [39]. These asymptotic formulas for Bessel functions are derived using the integral representations of Bessel functions and the steepest descent method. The different behavior of the asymptotics in the bulk of the spectrum, near the edges of the spectrum, and outside of is produced by the different location of the saddle point in these three cases.

1.6. Organization of the paper

Section 2 contains the proof of Theorems 1 and 2 and also various formulas for the kernels and . We also discuss a difference operator which commutes with and its possible applications.

Section 3 deals with the behavior of the Plancherel measure in the bulk of the spectrum; there we prove Theorem 3. Theorem 4 and a similar result (Theorem 5) for the poissonized measure are established in Section 4.

At the end of the paper there is an Appendix, where we collected some necessary results about Fredholm determinants, point processes, and convergence of trace class operators.

1.7. Acknowledgements

In many different ways, our work was inspired by the work of J. Baik, P. Deift, and K. Johansson, on the one hand, and by the work of A. Vershik and S. Kerov, on the other. It is our great pleasure to thank them for this inspiration and for many fruitful discussions.

2. Correlation functions of the measures

2.1. Proof of Theorem 1

As noted above, Theorem 1 is a limit case of Theorem 3.3 of [6]. That theorem concerns a family of probability measures on partitions of , where are certain parameters. When the parameters go to infinity, tends to the Plancherel measure . Theorem 3.3 in [6] gives a determinantal formula for the correlation functions of the measure

| (2.1) |

in terms of a certain hypergeometric kernel. Here and is an additional parameter. As and , the negative binomial distribution in (2.1) tends to the Poisson distribution with parameter . In the same limit, the hypergeometric kernel becomes the kernel of Theorem 1. The Bessel functions appear as a suitable degeneration of hypergeometric functions.

Recently, these results of [6] were considerably generalized in [24], where it was shown how this type of correlation functions computations can be done using simple commutations relations in the infinite wedge space.

For the reader’s convenience, we present here a direct and elementary proof which uses the same ideas as in [6] plus an additional technical trick, namely, differentiation with respect to which kills denominators. This trick yields an denominator–free integral formula for the kernel , see Proposition 2.7. Our proof here is a verification, not deduction. For more conceptual approaches the reader is referred to [7, 24].

Let . Introduce the following kernel

We shall consider the kernels and as operators in the space on .

We recall that simple multiplicative formulas (for example, the hook formula) are known for the number in (1.1). For our purposes, it is convenient to rewrite the hook formula in the following determinantal form. Let be the Frobenius coordinates of , see Section 1.2. We have

| (2.2) |

The following proposition is a straightforward computation using (2.2).

Proposition 2.1.

Let be a partition. Then

| (2.3) |

where are the modified Frobenius coordinates of .

Let be the push-forward of under the map . Note that the image of consists of sets having equally many positive and negative elements. For other , the right-hand side of (2.3) can be easily seen to vanish. Therefore is a determinantal point process (see the Appendix) corresponding to , that is, its configuration probabilities are determinants of the form (2.3).

Corollary 2.2.

.

This follows from the fact that is a probability measure. This is explained in Propositions A.1 and A.4 in the Appendix. Note that, in general, one needs to check that is a trace class operator. However, because of the special form of , it suffices to check a weaker claim – that is a Hilbert–Schmidt operator, which is immediate.

Theorem 1 now follows from general properties of determinantal point processes (see Proposition A.6 in the Appendix) and the following

Proposition 2.3.

.

We shall need three following identities for Bessel functions which are degeneration of the identities (3.13–15) in [6] for the hypergeometric function. The first identity is due to Lommel (see [39], Section 3.2 or [12], 7.2.(60))

| (2.4) |

The other two identities are the following.

Lemma 2.4.

For any and any we have

| (2.5) | |||

| (2.6) |

Proof.

Another identity due to Lommel (see [39], Section 5.23, or [12], 7.15.(10)) reads

Substituting we get (2.5). Substituting yields

| (2.7) |

Let the difference of the left-hand side and the right-hand side in (2.6). Using (2.7) and the recurrence relation

| (2.8) |

we find that . Hence for any it is a periodic function of and it suffices to show that . Clearly, the left-hand side in (2.6) goes to 0 as . From the defining series for it is clear that

| (2.9) |

which implies that the right-hand side of (2.6) also goes to as . This concludes the proof. ∎

Proof of Proposition.

It is convenient to set . Since the operator is invertible we have to check that

This is clearly true for ; therefore, it suffices to check that

| (2.10) |

where and . Using the formulas

| (2.11) | |||||

one computes

where . Similarly,

Now the verification of (2.10) becomes a straightforward application of the formulas (2.5) and (2.6), except for the occurrence of the singularity in those formulas. This singularity is resolved using (2.4). This concludes the proof of Proposition 2.3 and Theorem 1. ∎

2.2. Proof of Theorem 2

Recall that by construction

Let us check that this and Proposition A.8 implies Theorem 2. In Proposition A.8 we substitute

By definition, set

We have the following

Lemma 2.5.

It is clear that since the -factors cancel out of all determinantal formulas, this lemma and Proposition A.8 establish the equivalence of Theorems 1 and 2.

Proof of lemma.

Using the relation

and the definition of one computes

| (2.12) |

Clearly, the relation (2.12) remains valid for . It remains to consider the case . In this case we have to show that

Rewrite it as

| (2.13) |

By (2.14) this is equivalent to

Examine the right–hand side. The terms with vanish because then . The term with is equal to 1, which corresponds to 1 in the left–hand side. Next, the terms with vanish because for these values of , the expression vanishes. Finally, for , set . Then the th term in the second sum is equal to minus the th term in the first sum. Indeed, this follows from the trivial relation

This concludes the proof. ∎

2.3. Various formulas for the kernel

Recall that since is an entire function of , the function is entire in and . We shall now obtain several denominator–free formulas for the kernel .

Proposition 2.6.

| (2.14) |

Proof.

Proposition 2.7.

Suppose . Then

Proof.

Remark 2.8.

Observe that by Proposition 2.7 the operator is a sum of two operators of rank 1.

Proposition 2.9.

| (2.15) |

Proof.

Our argument is similar to an argument due to Tracy and Widom, see the proof of the formula (4.6) in [32]. The recurrence relation (2.8) implies that

| (2.16) |

Consequently, the difference between the left-hand side and the right-hand side of (2.15) is a function which depends only on . Let and go to infinity in such a way that remains fixed. Because of the asymptotics (2.9) both sides in (2.15) tend to zero and, hence, the difference actually is 0. ∎

In the same way as in [32] this results in the following

Corollary 2.10.

For any , the restriction of the kernel to the subset determines a nonnegative trace class operator in the space on that subset.

Proof.

Remark 2.11.

The kernel resembles a Christoffel–Darboux kernel and, in fact, the operator in defined by the kernel is an Hermitian projection operator. Recall that , where is of the form

On can prove that this together with Lemma 2.5 implies that is an Hermitian projection kernel. However, in contrast to a Christoffel–Darboux kernel, it projects to an infinite–dimensional subspace.

2.4. Commuting difference operator

Consider the difference operators and on the lattice ,

Note that as operators on . Consider the following second order difference Sturm–Liouville operator

| (2.17) |

where and are operators of multiplication by certain functions , . The operator (2.17) is self–adjoint in . A straightforward computation shows that

| (2.18) |

It follows that if for a certain then the space of functions vanishing for is invariant under .

Proposition 2.12.

Let denote the operator in obtained by restricting the kernel to . Then the difference Sturm–Liouville operator (2.17) commutes with provided

Proof.

Since is the square of the operator with the kernel , it suffices to check that the latter operator commutes with , with the above choice of and . But this is readily checked using (2.18). ∎

This proposition is a counterpart of a known fact about the Airy kernel, see [32]. Moreover, in the scaling limit when and

the difference operator becomes, for a suitable choice of the constant, the differential operator

which commutes to the Airy operator restricted to . The above differential operator is exactly that of Tracy and Widom [32].

Remark 2.13.

Presumably, this commuting difference operator can be used to obtain, as was done in [32] for the Airy kernel, asymptotic formulas for the eigenvalues of , where and . Such asymptotic formulas may be very useful if one wishes to refine Theorem 4 and to establish convergence of moments in addition to convergence of distribution functions. For individual distributions of and the convergence of moments was obtained, by other methods, in [2, 3].

3. Correlation functions in the bulk of the spectrum

3.1. Proof of Theorem 3

We refer the reader to Section 1.3 of the Introduction for the definition of a regular sequence and the statement of Theorem 3. Also, in this section, we shall be working in the bulk of the spectrum, that is, we shall assume that all numbers defined in (1.10) lie inside . The edges of the spectrum and its exterior will be treated in the next section.

In our proof, we shall follow the strategy explained in Section 1.5. Namely, in order to compute the limit of we shall use the contour integral

compute the asymptotics of for , and estimate away from . Both tasks will be accomplished using classical results about the Bessel functions.

We start our proof with the following lemma which formalizes the above informal depoissonization argument. The hypothesis of this lemma is very far from optimal, but it is sufficient for our purposes. For the rest of this section, we fix a number which shall play an auxiliary role.

Lemma 3.1.

Let be a sequence of entire functions

and suppose that there exist such constants and that

| (3.1) | |||

| (3.2) |

as . Then

Proof.

By replacing by , we may assume that . By Cauchy and Stirling formulas, we have

Choose some large and split the circle into 2 parts as follows:

The inequality (3.1) and the equality

imply that the integral decays exponentially provided is large enough. On , the inequality (3.2) applies for sufficiently large and gives

Therefore, the the integral is of the following integral

Hence, and the lemma follows. ∎

Definition 3.2.

Remark 3.3.

Note that we do not require to be entire. Indeed, the kernel may have a square root branching, see the formula (2.14).

By Theorem 2, the correlation functions belong to the algebra generated by sequences of the form

where the sequence is regular which, we recall, means that the limits

exist, finite or infinite. Therefore, we first consider such sequences.

Proposition 3.4.

If is regular then

In the proof of this proposition it will be convenient to allow . For complex sequences we shall require ; the number may be arbitrary.

Lemma 3.5.

Suppose that a sequence is as above and, additionally, suppose that , are bounded and . Then the sequence satisfies (3.2) with and certain .

Proof of Lemma.

We shall use Debye’s asymptotic formulas for Bessel functions of complex order and large complex argument, see, for example, Section 8.6 in [39]. Introduce the following function

The formula (1.9) can be rewritten as follows

| (3.3) |

The asymptotic formulas for Bessel functions imply that

| (3.4) |

where

provided that in such a way that stays in some neighborhood of ; the precise form of this neighborhood can be seen in Figure 22 in Section 8.61 of [39]. Because we assume that

and because , the ratios , stay close to . For future reference, we also point out that the constant in in (3.4) is uniform in provided is bounded away from the endpoints .

First we estimate . The function clearly takes real values on the real line. From the obvious estimate

and the boundedness of , , and we obtain an estimate of the form

| (3.5) |

If then because of the denominator in (3.3) the estimate (3.5) implies that

Since , it follows that in this case the lemma is established.

Assume, therefore, that is finite. Observe that for any bounded increment we have

| (3.6) |

and, in particular, the last term is . Using the trigonometric identity

and observing that

we compute

Since, by hypothesis,

and , the lemma follows. ∎

Remark 3.6.

Below we shall need this lemma for a variable sequence . Therefore, let us spell out explicitly under what conditions on the estimates in Lemma 3.5 remain uniform. We need the sequences and to converge uniformly; then, in particular, the ratios and are uniformly bounded away from . Also, we need and to be uniformly bounded. Finally, we need to be uniformly bounded from below.

Proof of Proposition.

First, we check the condition (3.2). In the case this was done in the previous lemma. Suppose, therefore, that is a regular sequence in and consider the asymptotics of .

Because the function is an entire function of and we have

| (3.7) |

where is arbitrary; we shall take to be some small but fixed number. From the previous lemma we know that

From the above remark it follows that this estimate is uniform in . This implies the property (3.2) for .

To prove the estimate (3.1) we use Schläfli’s integral representation (see Section 6.21 in [39])

| (3.8) |

which is valid for and even for provided or .

If then the second summand in (3.8) vanishes and and the first is uniformly in . This implies the estimate (3.1) provided .

It remains, therefore, to check (3.1) for where is a regular sequence. Again, we use (3.7). Observe, that since the second summand in (3.8) is uniformly small provided is bounded from above and is bounded from below. Therefore, (3.7) produces the (3.1) estimate for . For we use the relation (2.13) and the reccurence (2.16) to obtain the estimate. ∎

Proof of Theorem 3.

Let be a regular sequence and let the numbers and be defined by (1.10), (1.11). We shall assume that for all . The validity of the theorem in the case when for some will be obvious form the results of the next section.

We have

| (3.9) | ||||

| (3.10) |

where the first line is the definition of and the second is Theorem 2. From (3.9) it is obvious that is entire. Therefore, we can apply Lemma 3.1 to it. It is clear that Lemma 3.1, together with Proposition 3.4, implies Theorem 3. The factorization (1.12) follows from the vanishing . ∎

3.2. Asymptotics of

Recall that the correlation functions were defined by

The asymptotics of these correlation functions can be easily obtained from Theorem 3 by complementation, see Sections A.3 and 2.2, and the result is the following.

Let be a regular sequence. If it splits, then the limit factors as in (1.12). Suppose therefore, that is nonsplit. Here one has to distinguish two cases. If or then we shall say that this sequence is off-diagonal. Geometrically, it means that corresponds to modified Frobenius coordinates of only one kind: either the row ones or the column ones. For off-diagonal sequences we obtain from Theorem 3 by complementation that

where is the discrete sine kernel and .

If is nonsplit and diagonal, that is, if it is nonsplit and includes both positive and negative numbers, then one has to assume additionally that the number of positive and negative elements of stabilizes for sufficiently large . In this case the limit correlations are given by the kernel

| (3.11) |

Remark that this kernel is not translation invariant. Note, however, that

provided and have the same sign and similarly for . Therefore, if the subsets and , , have the same number of positive and negative elements then

4. Edge of the spectrum: convergence to the Airy ensemble

4.1. Results and strategy of proof

In this section we prove Theorem 4 which was stated in Section 1.4 of the Introduction. We refer the reader to Section 1.4 for a discussion of the relation between Theorem 4 and the results obtained in [2, 3, 23].

Recall that the Airy kernel was defined as follows

where is the Airy function (1.15). The Airy ensemble is, by definition, a random point process on , whose correlation functions are given by

This ensemble was studied in [32]. We denote by a random configuration of the Airy ensemble. Theorem 4 says that after a proper scaling and normalization, the rows of a Plancherel random partition converge in joint distribution to the Airy ensemble. Namely, the following random variables

converge, in joint distribution, to the Airy ensemble as .

In the proof of Theorem 4, we shall follow the strategy explained in Section 1.5 of the Introduction. First, we shall prove that under the poissonized measure on the set of partitions , the random variables converge, in joint distribution, to the Airy ensemble as . This result is stated below as Theorem 5. From this, using certain monotonicity and Lemma 4.7 which is due to K. Johansson, we shall conclude that the same is true for the measures as .

The proof of Theorem 5 will be based on the analysis of the behavior of the correlation functions of , , near the point . From the expression for correlation functions of given in Theorem 1 it is clear that this amounts to the study of the asymptotics of when . This asymptotics is classically known and from it we shall derive the following

Proposition 4.1.

Set . We have

uniformly in and on compact sets of .

The prefactor corresponds to the fact that we change the local scale near to get non-vanishing limit correlations.

Using this and verifying certain tail estimates we obtain the following

Theorem 5.

For any fixed and any we have

| (4.1) |

where is the Airy ensemble.

Observe that the limit behavior of is, obviously, identical with the limit behavior of similarly scaled st, nd, an so on maximal Frobenius coordinates.

Proofs of Proposition 4.1 and Theorem 5 are given Section 4.2. In Section 4.3, using a depoissonization argument based on Lemma 4.7 we deduce Theorem 4.

Remark 4.2.

We consider the behavior of any number of initial rows of , where is a Plancherel random partition. By symmetry, same results describe the behavior of any number of initial columns of .

4.2. Proof of Theorem 5

Suppose we have a point process on with determinantal correlation functions

for some kernel . Let be a possibly infinite interval . By we denote the operator in obtained by restricting the kernel on . Assume is a trace class operator. Then the intersection of the random configuration with is finite almost surely and

In particular, the probability that is empty is equal to

More generally, if is a finite family of pairwise nonintersecting intervals such that the operators are trace class then

| (4.2) |

Here operators are considered to be acting in the same Hilbert space, for example, in .

In case of intersecting intervals , the probabilities

are finite linear combinations of expressions of the form (4.2). Therefore, in order to show the convergence in distribution of point processes with determinantal correlation functions, it suffices to show the convergence of expressions of the form (4.2).

The formula (4.2) is discussed, for example, in [33]. It remains valid for processes on a lattice such as in which case the kernel should be an operator on .

As verified, for example, in Proposition A.11 in the Appendix, the right-hand side of (4.2) is continuous in each with respect to the trace norm. We shall show that after a suitable embedding of inside the kernel converges to the Airy kernel as .

Namely, we shall consider a family of embeddings , indexed by a positive number , which are defined by

| (4.3) |

where is the characteristic function of the point and, similarly, the function on the right is the characteristic function of a segment of length . Observe that this embedding is isometric. Let denote the kernel on that is obtained from the kernel on using the embedding (4.3). We shall establish the following

Proposition 4.3.

We have

in the trace norm for all uniformly on compact sets in .

This proposition immediately implies Theorem 5 as follows

Proof of Theorem 5.

Consider the left-hand side of (4.1) and choose for each a pair of functions such that

and as . Then, on the one hand, the probability in left-hand side of (4.1) lies between the corresponding probabilities for and . On the other hand, the probabilities for and can be expressed in the form (4.2) for the kernel and by Propositions 4.3 and continuity of the Airy kernel they converge to one and same limit given by the Airy kernel as . ∎

Now we get to the proofs of Propositions 4.1 and 4.3 which will require some computations. Recall that the Airy function can be expressed in terms of Bessel functions as follows

| (4.4) |

see Section 6.4 in [39]. Also recall that

| (4.5) |

see, for example, the formula 7.23 (1) in [39].

Lemma 4.4.

For any we have

| (4.6) |

moreover, the constant in is uniform in on compact subsets of .

Proof.

Lemma 4.5.

There exist such that for any and we have

| (4.9) | |||||

| (4.10) |

for all .

Proof.

First suppose that . Set . We shall use (4.7) with . Provided is chosen small enough and is sufficiently large, will be close to and we will be able to use Taylor expansions. For we have

and, similarly,

Since the function is concave, we have

The constant here is strictly positive.

Lemma 4.6.

For any there exists such that for all and large enough

Proof.

From (2.15) we have

| (4.11) |

Let us split the sum in (4.11) into two parts

that is, one sum for and the other for , and apply Lemma 4.5 to these two sums. Note that here corresponds to in Lemma 4.5; this produces factors of and does not affect the estimate.

Let the ’s stand for some positive constants not depending on . From (4.9) we obtain the following estimate for the first sum

where

Therefore,

We can choose so that .

Proof of Proposition 4.1.

As shown in [9, 32], the Airy kernel has the following integral representation

| (4.12) |

The formula (4.11) implies that for any integer

| (4.13) |

Let us fix and pick according to Lemma 4.6. Since, by assumption, and lie in compact set of , we can fix such that . Set

Then the inequalities

are satisfied for all in our compact set and Lemma 4.4 applies to the sum in (4.13). We obtain

because the number of summands is and is bounded on subsets of which are bounded from below. Note that

is a Riemann integral sum for the integral

and it converges to this integral as . Since the absolute value of the second term in the right-hand side of (4.13) does not exceed by the choice of , we get

as , and this estimate is uniform on compact sets. Now let and . By (4.5) the integral (4.12) converges uniformly in and on compact sets and we obtain the claim of the proposition. ∎

Proof of Proposition 4.3.

It is clear that Proposition 4.1 implies the convergence of to in the weak operator topology. Therefore, by Proposition A.9, it remains to prove that as . We have

where the correction comes from the fact that may not be a number of the form , . By (4.11) we have

| (4.14) |

Similarly,

| (4.15) |

Since we already established the uniform convergence of kernels on compact sets, it is enough to show that the both (4.14) and (4.15) go to zero as and . For the Airy kernel this is clear from (4.5). For the kernel it is equivalent to the following statement: for any there exists such that for all and large enough we have

| (4.16) |

We shall employ Lemma 4.5 for . Again, we split the sum in (4.16) in two parts

For the first sum Lemma 4.5 gives

where

and the ’s are some positive constants that do not depend on . Since we obtain

This can be made arbitrarily small by taking sufficiently large.

For the other part of the sum we have the estimate

which, evidently, goes to zero as . ∎

4.3. Depoissonization and proof of Theorem 4

Fix some and denote by the distribution function of under the Plancherel measure

Also, set

This is the distribution function corresponding to the measure .

The measures can be obtained as distribution at time of a certain random growth process of a Young diagram, see e.g. [38]. This implies that

Also, by construction, is monotone in and similarly

| (4.17) |

We shall use these monotonicity properties together with the following lemma.

Lemma 4.7 (Johansson, [14]).

There exist constants and such that for any nonincreasing sequence

and its exponential generating function

we have for all the following inequalities:

This lemma implies that for all

| (4.18) |

Set

Theorem 5 asserts that

| (4.19) |

where is the corresponding distribution function for the Airy ensemble. Note that is continuous.

Appendix A General properties of determinantal point processes

In this Appendix, we collected some necessary facts about determinantal point processes, their correlation functions, Fredholm determinants, and convergence of trace class operators.

Let be a countable set, let be the set of subsets of and denote by the set of finite subsets of . We call elements of configurations. Let be a kernel on , that is, a function on also viewed as a matrix of an operator in .

By a determinantal point process on (in [10] such processes are called fermion point processes) we mean a probability measure on such that

Here the determinant in the numerator is the usual determinant of linear algebra, whereas the determinant in the denominator is, in general, a Fredholm determinant. Some sufficient conditions under which makes sense are described in the following subsection.

A.1. Fredholm determinants and determinantal processes

Let be a complex Hilbert space, be the algebra of bounded operators in , and , be the ideals of trace class and Hilbert–Schmidt operators, respectively.

Assume we are given a splitting . According to this splitting, write operators in block form , where

The algebra is equipped with a natural -grading. Specifically, given , its even part and odd part are defined as follows

Denote by the set of operators such that is in the trace class while is in the Hilbert–Schmidt class . It is readily seen that is an algebra. We endow it with the topology induced by the trace norm on the even part and the Hilbert–Schmidt norm on the odd part.

It is well known that the determinant makes sense if . It can be characterized as the only function which is continuous in with respect to the trace norm and which coincides with the usual determinant when is a finite–dimensional operator. See, e.g., [30].

Proposition A.1.

The function admits a unique extension to , which is continuous in the topology of that algebra.

Proof.

Corollary A.2.

If is an ascending sequence of projection operators in such that strongly, then

Proof.

Indeed, approximates in the topology of . ∎

Corollary A.3.

If then

Proof.

Indeed, this is true for finite–dimensional , and then we use the continuity argument. ∎

In our particular case, the splitting of will come from a splitting of into two complementary subsets as follows

An operator in will be viewed as an infinite matrix whose rows and columns are indexed by elements of . Given , we denote by the corresponding finite submatrix in .

Proposition A.4.

If then

| (A.2) |

where summation is taken over all finite subsets including the empty set with understanding that .

Proof.

Given a finite subset , we assign to it, in the natural way, a projection operator . Then, by elementary linear algebra,

Assume becomes larger and larger, so that in the limit it covers the whole . Then the left-hand side tends to the left-hand side of (A.2). On the other hand the right-hand side tends to by Corollary A.2. ∎

Remark A.5.

Suppose that , where is of Hilbert–Schmidt class. Then . It is readily seen that for all , and it is worth noting that unless . By Proposition A.4, we can define a probability measure on finite subsets of by

A.2. Correlation functions of determinantal processes

Given , let be the probability that a random configuration contains , that is,

We call the correlation functions. The fundamental fact about determinantal point processes is that their correlation functions have again a determinantal form.

Proposition A.6.

Let be as above and set . Then .

Proof.

We follow the argument in [10], Exercise 5.4.7. Let be an arbitrary function on such that for all but a finite number of ’s. Form the probability generating functional:

Then, viewing as a diagonal matrix, we get

where the last equality is justified by Proposition A.4 applied to the operator .

Now, set , so that for all but finitely many ’s. Then we can rewrite this relation as follows

where the last equality follows by Corollary A.3.

Next, as is in (it is even finite–dimensional), this can be rewritten as

On the other hand, by the very definition of ,

This implies , as desired. ∎

Remark A.7.

If then

A.3. Complementation principle

In this section we discuss a simple but useful observation which was communicated to us by S. Kerov. Consider an arbitrary probability measure on such that its correlation functions

have a determinantal form

for some kernel .

Let be an arbitrary subset of . Consider the symmetric difference mapping

which is an involution in . Let be the image of our probability measure under and let be the correlation functions of the measure . Define a new kernel as follows. Let be the complement of and write the matrix in the block form with respect to the decomposition

By definition, set

We have the following

Proposition A.8.

.

Proof.

Set , . By the inclusion-exclusion principle we have

This alternating sum is easily seen to be identical to the expansion of by linearity using

∎

A.4. Convergence of trace class operators

Let and be Hermitian nonnegative operators in . The following proposition is a special case of Theorem 2.20 in the book [31] (we are grateful to P. Deift for this reference). For the reader’s convenience we give a proof here.

Proposition A.9.

The following conditions are equivalent:

(i) ;

(ii) and in the weak operator topology.

First, prove a lemma:

Lemma A.10.

Let be a nonnegative operator matrix. Then .

Proof of Lemma.

Without loss of generality one can assume that the block is a nonnegative diagonal matrix, . Write the blocks and as matrices, too, and let and be their diagonal entries. Since , we have and therefore

∎

Proof of Proposition A.9.

Clearly, (i) implies (ii). To check the converse claim, write in the block form, , where is of finite size and is small. Write all the ’s in the block form with respect to the same decomposition of the Hilbert space, . Since weakly, we have convergence of finite blocks, , which implies . Since , we get , so that all the traces are small together with provided that is large enough.

Write and similarly for . Then

In the right-hand side, the first and the third summands are small because of the lemma, while the second summand is small because it is equal to . ∎

Proposition A.11.

The map defines a continuous map from to the algebra of entire functions in variables with the topology of uniform convergence on compact sets.

References

- [1] D. Aldous and P. Diaconis, Hammersley’s interacting particle process and longest increasing subsequences, Prob. Theory and Rel. Fields, 103, 1995, 199–213.

- [2] J. Baik, P. Deift, K. Johansson, On the distribution of the length of the longest increasing subsequence of random permutations, math.CO/9810105.

- [3] by same author, On the distribution of the length of the second row of a Young diagram under Plancherel measure, math.CO/9901118.

- [4] P. Biane, Permutation model for semi-circular systems and quantum random walks, Pacific J. Math., 171, no. 2, 1995, 373–387.

- [5] by same author, Representations of symmetric groups and free probability, preprint, 1998.

- [6] A. Borodin and G. Olshanski, Distribution on partitions, point processes, and the hypergeometric kernel, math.RT/9904010.

- [7] by same author, paper in preparation.

- [8] by same author, Z-measures on partitions, Robinson-Schensted-Knuth correspondence, and random matrix ensembles, math.CO/9905189.

- [9] P. A. Clarkson and J. B. McLeod, A connection formula for the second Painlevé transcendent, Arch. Rat. Mech. Anal., 103, 1988, 97–138.

- [10] D. J. Daley and D. Vere-Jones, An introduction to the theory of point processes, Springer series in statistics, Springer Verlag, 1988.

- [11] P. J. Forrester, The spectrum edge of random matrix ensembles, Nuclear Phys. B, 402, 1993, no. 3, 709–728.

- [12] Higher Transcendental functions, Bateman Manuscript Project, McGraw-Hill, New York, 1953.

- [13] P. Jacquet and W. Szpankowski, Analytical depoissonization and its applications, Theor. Computer Sc., 201, 1998, 1–62.

- [14] K. Johansson, The longest increasing subsequence in a random permutation and a unitary random matrix model, Math. Res. Letters, 5, 1998, 63–82.

- [15] by same author, Discrete orthogonal polynomials and the Plancherel measure, math.CO/9906120.

- [16] S. Kerov, Gaussian limit for the Plancherel measure of the symmetric group, C. R. Acad. Sci. Paris, 316, Série I, 1993, 303–308.

- [17] by same author, Transition probabilities of continual Young diagrams and the Markov moment problem, Func. Anal. Appl., 27, 1993, 104–117.

- [18] by same author, The asymptotics of interlacing roots of orthogonal polynomials, St. Petersburg Math. J., 5, 1994, 925–941.

- [19] by same author, A differential model of growth of Young diagrams, Proceedings of the St. Petersburg Math. Soc., 4, 1996, 167–194.

- [20] by same author, Interlacing measures, Amer. Math. Soc. Transl., 181, Series 2, 1998, 35–83.

- [21] B. F. Logan and L. A. Shepp, A variational problem for random Young tableaux, Adv. Math., 26, 1977, 206–222.

- [22] I. G. Macdonald, Symmetric functions and Hall polynomials, Oxford University Press, 1995.

- [23] A. Okounkov, Random matrices and random permutations, math.CO/9903176

- [24] by same author, Infinite wedge and measures on partitions, math.RT/9907127

- [25] E. M. Rains, Increasing subsequences and the classical groups, Electr. J. of Combinatorics, 5(1), 1998.

- [26] A. Regev, Asymptotic values for degrees associated with strips of Young diagrams, Adv. Math., 41, 1981, 115-136.

- [27] E. Seiler and B. Simon, On finite mass renormalization in the two-dimensional Yukawa model, J. of Math. Phys., 16, 1975, 2289–2293.

- [28] C. Schensted, Longest increasing and decreasing subsequences, Canad. J. Math., 13, 1961, 179-191.

- [29] T. Seppäläinen, A microscopic model for Burgers equation and longest increasing subsequences, Electron. J. Prob., 1, no. 5, 1996.

- [30] B. Simon, Notes on Infinite Determinants of Hilbert Space Operators, Adv. Math., 24, 1977, 244–273.

- [31] by same author, Trace ideals and their applications. London Math. Soc. Lecture Note Ser., 35, Cambridge University Press, 1979, 134 pp.

- [32] C. A. Tracy and H. Widom, Level-spacing distributions and the Airy kernel, Commun. Math. Phys., 159, 1994, 151–174.

- [33] by same author, Introduction to random matrices, Geometric and quantum aspects of integrable systems, Lecture Notes in Phys., 424, 1993, Springer Verlag, pp. 103–130.

- [34] by same author, On the distribution of the lengths of the longest monotone subsequences in random words, math.CO/9904042.

- [35] A. Vershik, Statistical mechanics of combinatorial partitions and their limit configurations, Func. Anal. Appl., 30, no. 2, 1996, 90–105.

- [36] A. Vershik and S. Kerov, Asymptotics of the Plancherel measure of the symmetric group and the limit form of Young tableaux, Soviet Math. Dokl., 18, 1977, 527–531.

- [37] by same author, Asymptotic theory of the characters of a symmetric group Func. Anal. Appl., 15, 1981, no. 4, 246-255.

- [38] by same author, Asymptotics of the maximal and typical dimension of irreducible representations of symmetric group, Func. Anal. Appl., 19, 1985, no.1.

- [39] G. N. Watson, A treatise on the theory of Bessel functions, Cambridge University Press, 1944

- [40] H. Widom, Random Hermitian matrices and (nonrandom) Toeplitz matrices, Toeplitz Operators and Related Topics, the Harold Widom anniversary volume, edited by E. L. Basor and I. Gohberg, Operator Theory: Advances and Application, Vol. 71, Birkhäuser Verlag, 1994, pp. 9–15.

- [41] by same author, The strong Szegö limit theorem for circular arcs, Indiana U. Math. J., 21, 1971, 271–283.