SUNY-NTG 98-02

Valuation of path-dependent American options

using a Monte Carlo approach

H. Sorge 111 E-mail: sorge@alba.physics.sunysb.edu

Department of Physics and Astronomy,

State University of New York at Stony Brook, NY 11794-3800

Abstract

It is shown how to obtain accurate values for American options using Monte Carlo simulation. The main feature of the novel algorithm consists of tracking the boundary between exercise and hold regions via optimization of a certain payoff function. We compare estimates from simulation for some types of claims with results from binomial tree calculations and find very good agreement. The novel method allows to calculate so far untractable path-dependent option values.

Pricing of options is an important area of research in the finance community. The field has been pioneered by Black and Scholes (1973). They made a major breakthrough by deriving a formula for the price of any contingent claim which depends on a non-dividend-paying stock. Using the assumption of no arbitrage, they were able to show that the price of a derivative security can be expressed as the expected value of its discounted payoffs. The expectation is taken under the assumption of a risk-neutral evolution of the value of the underlying security. Merton (1973) generalized these ideas to situations in which the interest rates themselves fluctuate in time. Due to the complexity of the underlying dynamics, numerical methods have become increasingly popular in modern finance. They are used for a variety of purposes, for instance valuation of securities and stress testing of portfolios. Analytical solutions for problems in finance have been found only for rather special cases. For instance, in order to gain the solution for prices of European options Black and Scholes had to assume that the evolution of the underlying asset price (more precisely its natural logarithm) follows a so-called Wiener process with time-independent volatility. European options can be exercised only at expiration date. In contrast, American-style options which can be exercised during the whole lifetime of the option can be valued only numerically. Furthermore, numerical methods have to be employed if the dimension of the problem increases (more than one state variable) or in case of more realistic approaches to the stochastic process like for some no-arbitrage models of interest rate evolution.

The Monte Carlo approach lends itself very naturally to the evaluation of security prices and interest rates. Schematically, it consists of the following steps. First, sample paths of the state variables (asset prices and so on) over the relevant time horizon are generated. The cash flows of the securities on each sample path are evaluated, as determined by the structure of the security in question. The discounted cash flows are averaged over the sample paths. The Monte Carlo method is very flexible, since it does not depend much on the specific nature of the underlying stochastic process. Its accuracy is also independent on the dimensionality of the problem which is its dominant advantage over more traditional numerical integration methods. It is outside the scope of this paper to discuss the various facets of recent research on the use of Monte Carlo in the finance area. The reader may consult the concise recent reviews of Boyle, Broadie, and Glassermann (1997) on these topics. In particular, they report on recent progress in developing more efficient Monte Carlo algorithms. Standard Monte Carlo methods converge notoriously slow (with 1/, being the number of sampled paths). A central goal of recent research activity has therefore been the refinement of variance reduction techniques (antithetic and control variates), importance sampling and low-discrepancy random number sequences. If the development in sciences like physics is any guide, Monte Carlo applications in finance will become even more important. With computational prowess further increasing the Monte Carlo method may even shed its ‘brute force’ image from the past which was founded on its rather slow convergence property.

Boyle (1977) was the first to propose the use of Monte Carlo methods for option pricing in the literature. Since the exercise date of European contingent claims is fixed, the mechanics of a price evaluation of European options employing the Monte Carlo method is rather straightforward. Let us begin by collecting the notation for the most important variables which we are going to use throughout the rest of the paper. In general, we follow the notation in Hull’s book (1993), except that the present time for which the option price is calculated is designated to be “0” (without loss of generality).

=

the value of the state (asset price, …) at time

underlying the derivative security

(which may be a single variable or a vector),

=

the initial value of the state variables,

X

=

strike price of the option,

p

=

path on which the underlying state evolves in time,

=

the value of the option if exercised at time

( for a simple Call and

for a Put),

=

instantaneous risk-less interest rate at time ,

=

volatility (standard deviation) of state variable

or their components respectively,

T

=

the lifetime of the option contract (expiration date),

=

the option value at time .

We may easily estimate the European option value from a Monte Carlo path sample for the variables related to the derivative security. These paths need to be generated with probabilities determined by the underlying stochastic process. The option value at the expiration date has been specified in the option contract. In general, it may depend on the path of the relevant state variables between closing the contract and expiration date. Each pathwise final option value from the simulation is discounted backward in time to determine its value at time 0. Since we do not know at time =0 yet on which path the underlying variables will evolve, the average over all paths is taken to estimate the present option value:

| (1) |

The discount factor includes the risk-free interest rate , possibly averaged over the lifetime of the option. For simplicity, it is assumed in eq. (1) that all sampled paths have equal probability. Generalization to a situation in which paths are characterized by different probabilities which may arise e.g. in the context of Monte Carlo optimization by importance sampling is straightforward.

The pricing of options which may be exercised prior to the expiration date by Monte Carlo simulation is more involved. Here, the owner holds the right to exercise the option at several (Bermudan) or possibly infinitely many (American) ‘decision dates’. Many types of American contingent claims trade on exchanges and in the over-the-counter market. Examples include options, swaptions, binary options and Asian options. It has been shown by Roll (1977), Geske (1979), and Whaley (1981) that exercise of call options which give the owner the right to purchase some underlying asset at the agreed-on strike price is usually unfavorable before expiration date, except close to ex-dividend dates. The situation is much less clear-cut in case of put options which give the owner the right to sell the asset at the strike price. In these situations the ‘naive’ Monte Carlo is encountering unsurmountable difficulties. In order to decide whether it is more favorable at some intermediate time to hold or exercise the option the owner needs to compare the expected payoff in the two cases. The maximum of the two forms the option value at that time which – after discounting and taking the expectation value – leads to the following expression for the option at closing date:

| (2) |

The angular brackets denote the expectation value with respect to the (risk-free) probability measure. The path-dependent times are the so-called optimum stopping times which may be any of the decision dates.

A single path provides clearly insufficient information to evaluate the option value in case of non-exercise at any of the decision dates. The insufficiency of the naive Monte Carlo method to deal with the optimum stopping problem has lead some authors like Hull (1993) to the claim in the literature that “Monte Carlo simulation can only be used for European-style options”. On the other side, evaluation of American-style Options via Monte Carlo simulation has found already some consideration in the literature as reviewed Boyle, Broadie, and Glassermann (1997). Their common denominator is a ‘clever’ estimate of the option prices on the decision dates by bundling subsets of paths. These authors noted that the suggested algorithms cannot be considered satisfactory yet. Either some approximations may lead to uncontroled errors affecting the simulation results or the required large computational effort limits their applicability, e.g. to a small number of exercise dates.

In this paper we are suggesting a completely different strategy to calculate American-style put and call option prices via Monte Carlo simulation. During the sampling of the paths we do not attempt to estimate the expectation of the payoff if the owner continues to hold the option. Instead, we use the sampled paths to evaluate the boundary between the early-exercise region and the hold region in the space of variables entering into the option contract. The location of this boundary is the crucial piece of information whose knowledge allows the straightforward use of the Monte Carlo procedure for option price estimation. We treat the valuation of American options as an optimization problem of a certain payoff function which depends on the set of sampled paths. This function depends also on the exercise policy, i.e. the boundary between the early-exercise region and the complementary hold region (YES-NO boundary in the following). Maximation of the payoff function provides an estimator of the YES-NO boundary which gets arbitrarily close to the true location of the boundary with increasing number of sampled paths. For the plain vanilla put and call options, the boundary is rather simple at any exercise date, a point for one state variable, a line for a two-dimensional space of state variables and so on. After the boundary has been estimated the price estimation proceeds as for European options, because the option prices for points on the boundary are known. The only difference to price estimation of European options as in eq. (1) is that – concerning paths crossing the YES-NO boundary – each pathwise option value is discounted starting from the point at which the path crosses the boundary for the first time:

| (3) |

Time denotes the earliest time at which the -th path crosses the YES-NO boundary (if at all). Otherwise equals the time until expiration of the option (). is the agreed-on payoff from exercising the option at time under the assumption that path represents the realized evolution of the underlying state variables. Here we have tacitly assumed that the starting point lies in the NO region. Of course, the algorithm is able to handle the other possibility – immediate exercise – as well. In this case calculation of the option price is trivial, however.

In a later section of this paper we will demonstrate that the novel Monte Carlo algorithm achieves an accuracy in the determination of American option values which compares well with corresponding calculations for European options. We compare the results for a spectrum of standard American Puts with results from binomial tree calculations. This method originally introduced by Cox, Ross, Rubinstein (1979) is widely used for option valuation. Here we assume an ideal Wiener-type stochastic process for a single state variable, because a binomial tree is well suited to provide very accurate results in this situation. Of course, this comparison serves mostly illustrative purposes to show that the method works at finite . Lateron, we are going to present numerical results for path-dependent American options. We consider two cases, Puts on either the geometric or the arithmetic average over the lifetime of the option. Assuming again an underlying ideal Wiener process we may compare the Monte Carlo estimations to results from binomial tree calculations. While options on the geometric average can be priced by the tree method to arbitrary accuracy no such tree method is available for options contingent on the arithmetic average value. Some approximative method has been suggested to express the latter option prices by the corresponding prices in case of geometric averaging. Therefore we will compare the approximative formula to our more accurate procedure. In general, it is envisioned that the novel Monte Carlo approach and some variants will be applied for valuation problems which cannot or not easily be tackled by other methods. Such problems encompass stochastic processes with Non-Markov properties,stochastic volatilities, multi-dimensional state variables and other path-dependent American options.

I Valuation of American-style options as an optimization problem

Let us assume in the following that the underlying state variables whose values determine the value of an option at exercise dates follow a known stochastic process. Generally, a stochastic process is specified by defining the state space, an index parameter (usually the time) and the dependence relation between the random variables. The latter is usually given in terms of a stochastic integro-differential equation containing some deterministic drift terms and random changes in addition, notably diffusion or jump processes. Memory or so-called non-Markov effects may readily be included into the transition probabilities. Non-Markov models have found recently considerable interest in the finance community, because the Heath, Jarrow and Morton (1992) approach to interest rate evolution can be shown to possess Non-Markovian features, in general. We assume ‘smoothness’ for the transition probability density function which determines the probabilities – based on a path’s evolution history – that the path will comes close to any element of the state space at some time in the future. These are supposed to be continuous functions of the path variables. A discrete set of sequentially selected random points in time is often called a “chain”. A path is the corresponding generalization for a continuous time evolution.

At first, we will restrict ourselves to options and stochastic processes which result in the following simple property of the YES-NO boundary:

-

A1:

“The boundary between YES and NO regions at any given decision time is a simply connected hypersurface in the state space with dimension of one unit less than the dimension of the state space.”

As a consequence of the assumption, there are no disconnected pieces of YES or NO regions at a given time either. With the exception of some pathological cases, assumption A1 will be compatible only with option payoffs contingent on the values of the state variables at exercise date. Instead of specifying these pathological stochastic processes we simply require here:

-

A2:

“The payoff from exercising an option is only a function of the state variables at the exercise date but not at earlier times, i.e. .”

In general, the topology of exercise and hold regions of American options may be more complicated than allowed by our assumptions. Two examples are some types of barrier options and path-dependent options. Suppose the owner of a barrier option receives only some payoff if a security stays within some specified range of values at exercise date. Therefore the option will not be exercised for ‘too small’ and ‘too large’ values of the underlying which leads to two disconnected NO regions. Another perhaps more interesting example of options not covered by the assumption stated above are American path-dependent options whose valuation we will return to later in this section. Here the payoff depends on the values which the underlying state variables have taken in the past, e.g. on the arithmetic mean within some time interval. Projected into the space of state variables at any given time YES and NO region are completely scrambled. It may be optimal to exercise or hold an option for the same present value of the state variables depending on the different histories of each path. Lateron, we will show that a redefinition of the state space enables us to cover the case of path-dependent options by the same algorithm.

We should also mention that the assumption A2 restricts the memory properties of the underlying stochastic process. They should not spoil the assumed property of the YES-NO boundary in the state space. This simply means that although the future evolution of each path may depend on the past, the ‘average outcome’ determining the decision whether to exercise the option at present time is not influenced by the past but of Markovian nature.

Assumption A1 allows us to define coordinates in the dimensional state space such that any element of the state space can be uniquely characterized by some point of the YES-NO boundary and an additional coordinate

| (4) |

in a peculiar way. For any path passing through at present time the following inequalities hold between the payoff from exercising the option and the option value if the option is being held at least until the next exercise date:

| (5) |

The content of eq. (5) is to provide convenient coordinates from which one can easily read off whether point is a boundary point (), in the YES () or in the NO () region. The knowledge of all or just their signs is tantamount to finding the YES-NO boundary itself. Unfortunately, a straightforward application of the inequalities as expressed in eq. (5) to determine the boundary is prohibitive. Estimating the expected payoff from holding the option and comparing it to the payoff from exercising would require a ‘new simulation within the simulation’. Such a procedure becomes numerically awkward and would severely restrict the complexity of the problem to be tackled, concerning e.g. the nature of the stochastic process and the number of exercise dates.

We will proceed now to estimate the location of the YES-NO boundary based on a set of sampled paths. For this purpose it will be necessary to evolve the state variables backward in time. This feature of the novel Monte Carlo approach which it shares with all other numerical approaches to option pricing like the binomial tree method is caused by the boundary conditions of the problem. The option price is a specified function of the state variables only on the expiration date. Of course, the location of the YES-NO boundary is also trivially determined at expiration time. For a simple call or put option on a single asset it is the point .

The continuous time process will be presented as a sequence of time steps which add up to the lifetime of the contract . The time steps are supposed to match the distance between decision times exactly if a finite number of exercise opportunities has been specified in the option contract. For American options which give the owner the right of exercise at any time this is an approximation. However, choosing ‘small’ time steps the results will be close to the continuum limit. The current time for which the location of the YES-NO boundary is being sought can be represented by the integer index (with for American options). Since the location of the YES-NO boundary will be determined step by step moving backward in time, it is implicitly assumed from now on that the YES-NO boundary has already been determined for later times +1,+2,…, (within the usual uncertainties due to the numerical imprecision). Therefore we are able to evaluate for each path 222 For the ease of reading we are using calligraphic letters in this paper when dealing with functions of paths or path segments. its payoff from optimal exercise at later times:

| (6) |

The path-dependent payoff has been discounted to time in eq. (6). represents the earliest time (under the constraint ) at which path crosses the boundary from the NO region into the YES region or equals if the path stays within the NO region for all times between and . (For the latter case =0, of course.) We have used the subscript for the argument of to emphasize that the payoff defined above depends only on the values of the path variables for times but not on the past evolution of the state. So far, we are not able to calculate the discounted pathwise payoff , i.e. for time . This would require the knowledge of the YES-NO boundary at time . However, the path-dependent payoffs given in eq. (6) enter into the expression for the value of the option at time subject to the condition that the option is not immediately exercised (and, of course, that the state variables have evolved along path so far):

The integration over all future path segments in eq. (I Valuation of American-style options as an optimization problem)

is an ordinary multiple integral (but a path integral in the continuous time limit). denotes the transition probability density function and describes the probability (density) to evolve along the path segment in the future up to time depending on the present – and previous (for Non-Markov processes) – states of path .

Next we define a continuous path in the state space by letting be a continuous parameter within some range such that all are elements of the state space and vice versa. Let us assume for a moment that we know already that this line intersects with the YES-NO boundary but we do not know which point it is. (Somebody else has constructed the path .) Can we estimate the value of the YES-NO boundary point using the information provided by the path sample and obtain its correct value in the limit ? The answer is positive. We are able to construct a function of the states whose only maximum is at , i.e. the boundary point, for . It is clear that our ability to define such a function has important repercussions for the question how to find the YES-NO boundary. The virtue of path is to provide us with the knowledge that it has exactly one intersection point with the YES-NO boundary. We do not necessarily need this information. Instead, we may search for the global maximum on continuous paths connecting points in the YES region with points in the NO region. According to statement A1 they will cut through the YES-NO boundary at least once. (It will not hurt the search procedure, if we accidentally hit the boundary several times reflected by several local maxima.) It is also rather straightforward to determine selected points which are in either the YES or the NO region for sure. For instance, points lie in the NO region if the payoff from exercising is zero. Or the point with zero value of the underlying is certainly an element of the YES region for a plain vanilla Put, because the payoff cannot get any better.

In order to proceed with the proof of our conjecture we define a – generally suboptimal – exercise policy for all paths intersecting with at time which depends on an arbitrary point . We define a preliminary “YES” region (with the quotation marks reminding us that the true YES boundary may be different) as to cover all paths with state variable which fulfill . For instance, in case of a plain vanilla put (call) option on a single underlying asset we may declare that lies in the “YES” region if it fulfills the condition ( . The pathwise payoff from the -dependent policy is

| (8) |

It is clear that the pathwise payoffs will sometimes be larger for ‘wrong’ boundary points () than for the correct one. This reflects the additional information about the future which is encoded in the path segment . The essential point is now to sum over all paths which removes this bias:

| (9) |

The function depends on time, the sampled paths intersecting with (of number ) and on . Our central proposition can be stated now as follows:

-

P1:

“Taking the limit of infinitely many paths, has one extremum which is a maximum within the one-dimensional domain . Its position is the intersection point of with the YES-NO boundary =.”

In order to prove proposition P1 we are going to rearrange the sum in eq. (9). We put all paths which have essentially the same transition probability density function into the same (albeit infinitesimally small) ‘bin’. Here we need the assumption stated above that the transition probability density function is a continuous function of the path variables. After ‘binning’ and taking the limit eq. (9) turns into

| (10) |

The transition probability density function appears in eq. (10), because relative frequencies approach the probabilities which are governing the random selection of paths according to Bernoulli’s law of large numbers. The probability density to have a path segment close to needs to be defined in accordance with the integration measure and is normalized to one.

The quantity in brackets on the right hand side of eq. (10)

| (11) |

can be readily evaluated using eqs. (I Valuation of American-style options as an optimization problem) and (8) to be

| (14) |

coincides with the option price , except for values in a certain range. Furthermore, on virtue of eq. (5) is always smaller than for such chosen values:

The conditions of eq. (I Valuation of American-style options as an optimization problem) together with the positiveness of the weight factors in eq. (10) guarantee that

| (18) | |||||

This completes the proof of proposition P1.

As stated above we may turn things around and construct the YES-NO boundary from a set of lines in state space which connect elements of the YES and NO region. The global maximum of function along each line is the supposed intersection point with the YES-NO boundary. This process may be iterated until the desired precision is reached. This standard optimization procedure becomes particularly simple in case of plain vanilla options. Since the YES-NO boundary is just a point at any exercise date, its location is already completely specified with one iteration step. The determination of the YES-NO boundary at time (index ) enables us to calculate the pathwise payoff at this time. Going step-by-step backward in time we may finally calculate the pathwise payoffs at initial time whose average determines the option value at contract time.

The presented optimization technique may be used in the problem of valuation of American path-dependent options as well. Here the payoff from exercising the option depends on some function of the state variables in the past which we will denote as in the following. For instance, may be the – arithmetic or geometric – average of any state variable over some time window or the value at some specified time(s) of the past (look-back options). For simplicity, we restrict ourselves here to stochastic processes of Markovian nature whose parameters have been specified. In this case the exercise decision at any time before expiry is a function of just two – each possibly vector-valued – variables, the values of the state variables and of the path-dependent variable , both taken at the decision time. The difference between standard path-dependent and plain vanilla options is just that the role of the current value of the underlying variable in plain-vanilla contracts is played by in path-dependent contracts, e.g. Max for a Put. The topology of the exercise region for this kind of path-dependent options is very simple but only in the space of state variables enlarged by the additional dimension(s) of . The YES-NO boundary in the - space is again simply connected. Only its projection into the space leads to a scrambling of YES and NO regions. This suggests immediately how the suggested optimization technique may be applied for the case of these path-dependent options. We equip the space of states with additional dimensions by declaring to be one of the stochastic variables. Of course, the stochastic character of this variable is rather funny. Its change with time is completely deterministic and of Non-Markovian type. However, these features are in accordance with the basic assumptions entering into the proof of proposition P1. The complications of such path-dependent option contracts just result in a higher dimension of the space in which we have to track the YES-NO boundary.

We are now in a position to compare our novel strategy for an extraction of American-style option prices from Monte Carlo simulation to previously suggested ones. Boyle, Broadie, and Glassermann discuss mainly three strategies in their review paper to overcome the inherent limitations of the naive Monte Carlo procedure: the bundling algorithm invented by Tilley (1993), the stratified state aggregation algorithm suggested by Barraquand and Martineau (1995) and Broadie and Glassermann’s (1995) algorithm based on simulated trees. In Tilley’s approach bundles of paths which are ‘close’ in state space at given time are considered to emanate from one single point for the purpose of option valuation. This introduces some error whose magnitude cannot be easily controled. The bias of the exercise decision will be very strong if a bundle contains only few paths. Such a situation is likely to emerge in situations in which there are many exercise dates or several state variables. Barraquand and Martineau introduce another type of ‘bundling’, however, in the payoff space. Our approach shares similarities with Tilley’s algorithm in the sense that it contains an implicit ‘bundling’ of paths (called ‘binning’) in the proof of the proposition P1. However, we have actually never to carry out this bundling in a numerical calculation, because we stick to an optimization of the ‘inclusive’ function which sums up all bins. Broadie and Glassermann proposed an algorithm based on a ‘bushy tree’ structure in state space which avoids partitioning of the state or payoff space. In their model many branches emanate from each node. This process is replicated as often as there are decision times in the problem. The replication process effectively limits to small numbers (on the order of 4) in practical computations. They also discuss the problem that the suggested estimators of the option prices tend to be biased in ‘up’ or ‘down’ direction. and converge only to the correct value in the limit . This problem is of great relevance for practical calculations (which are always at finite ). They use the idea to calculate two estimators – one biased low and the other high – to obtain confidence limits from the simulations. Lateron, we are going to apply this idea in the framework of our approach.

II Simulation results for American options

In this paper we will only consider stochastic processes of rather simple nature, so-called ideal Wiener or diffusion processes (for the of any state variables). In physics these processes are usually called Brownian motion. Such processes seem to be most commonly used in valuation problems. Furthermore, numerical techniques have been developed to calculate prices for plain vanilla and other simple types of American options. In particular, the binomial tree method may provide very accurate values and will be used as a benchmark here against which the results from the Monte Carlo simulations are being tested. In this section we will restrict ourselves to Puts on the current value and on the – geometric or arithmetic – average of one single underlying security. An ideal Wiener process can be characterized by the differential transition law

| (19) |

governing the change of the state variable within a time interval . is a random number drawn from a normal distribution with mean 0 and variance 1. is in general the drift velocity which may be replaced by the risk-free instantaneous interest rate using arbitrage arguments. Sometimes one needs to follow an ideal Wiener process only backward in time, e.g. in case of Monte Carlo estimation of plain vanilla options. Using the bridge construction – start and final value are known – a random value at intermediate time may be chosen according to

| (20) |

After having fixed final and start values, iterative use of eq. (20) may be employed to generate a time reverted copy of the standard diffusive Wiener-type motion. For the simulation results presented below we have used a simple importance sampling scheme. The exercise value of strongly out-of-the money options at expiry will be zero on most paths. Therefore the weight of the rare paths resulting in nonzero option value has been artificially enhanced in the path generation process. Of course, the enhancement factors are taken out again in the calculation of the path-averaged prices.

In its most simple form the Monte Carlo algorithm which is suitable for valuation of American-style options consists of the following steps:

- (1)

-

Generate path sample.

- (2)

-

Go step-by-step backward in time starting at expiry.

- (3)

-

Track the YES-NO boundary by employing the optimization of function along arbitrary paths connecting YES and NO region (cf. eq. (9)).

- (4)

-

Evaluate the pathwise payoffs at the earlier time analogous to eq. (6).

- (5)

-

Repeat the process until the contract time is reached.

- (6)

-

Average the pathwise payoffs discounted to initial time over the whole path sample (cf. eq. (3)).

Let us discuss now some aspects related to the finite size of the path sample in practical calculations. It is clear that step (6) does not provide an unbiased estimator of the option price at any finite but is biased upward. The reason is that an error is made extracting the YES-NO boundary from the finite size path sample. A deviation of the extracted from the true boundary has its root in the information about the mismatch between frequency distribution of the paths and underlying probabilities which enters into the optimization process. The estimator becomes only asymptotically unbiased. Since we are not able to construct an unbiased estimator, we may get an estimate of the error introduced by the bias in step (6) by constructing an estimator which is downward biased at finite but also asymptotically unbiased. It is very simple to construct such an estimator:

- (6’)

-

Generate a path sample independent from the first one and evaluate the American option prices using the previously calculated YES-NO boundary.

The reason that the prices calculated from this path sample are biased downward mirrors the one for the upward bias in the former case. Here any deviation from the true boundary implies a suboptimal exercise policy.

We hasten to add that the algorithm presented so far has one shortcoming related to the combined effects of finite sample size and well-determined values of the underlying variables at start time. Only with paths crossing the YES-NO boundary its optimal location can be determined, of course. Formally, the proof of proposition P1 requires that the probability densities appearing in eq. (10) be positive-definite in a region covering the YES-NO boundary. However, this condition will be violated in practice at early times, since all sampled paths emanate from a common starting point. On the other side, in such a situation the knowledge of the precise location of the boundary becomes irrelevant for the valuation problem. It suffices to know at this stage on which side of the boundary the vast majority of paths can be found. Two variants with differing degree of sophistication have been developed to determine the earliest time for which the algorithm above is to be used:

- (7a)

-

If the YES-NO boundary gets closest to either one of the endpoints of , e.g. the paths with smallest or largest value for plain vanilla options, it is assumed that the boundary can be found outside the range of the path sample for all earlier times.

- (7b)

-

“Flashlight mechanism”: when the YES-NO boundary moves towards a region only poorly covered by the original path sample, additional path segments are created which evolve in the region of the YES-NO boundary at this time. As far as the proof of proposition P1 is concerned the probability densities in eq. (10) do not need to be consistent with the initial value specification for the pricing problem. Here we make use of this freedom to generate a set of paths whose initial values are tuned to ‘shed light’ on the location of the YES-NO boundary.

Concerning accuracy simulation mode (7b) is only barely noticably superior over mode (7a) for the tested sample of plain vanilla options. All simulation results for more complicated options reported on in this paper have been achieved employing mode (7b) .

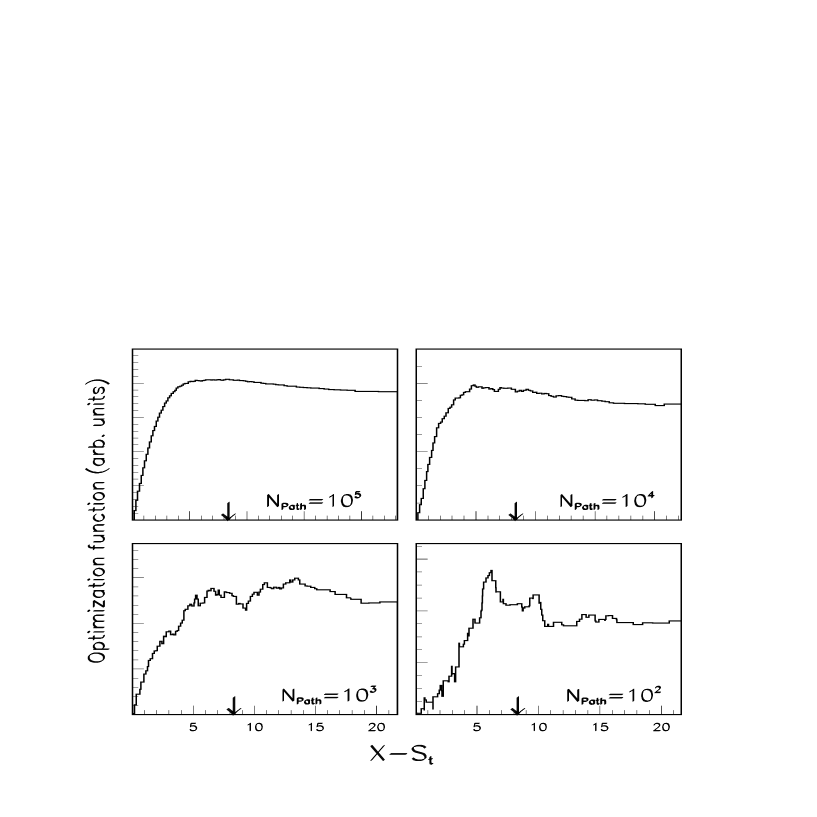

At finite the values and therefore also the maximum of the payoff function do not change between values of its argument which are taken by two neighboring paths. Furthermore, the precision with which the true maximum of function can be estimated from a finite size sample is a multiple () of the typical distance between paths in the region along the YES-NO boundary. Fig. 1 shows the Monte Carlo estimation of the optimization function for a plain vanilla put option on a security of (time-dependent) value in order to illustrate the finite effect. Selected values are displayed at a fixed time but varying the size of the path sample. The true minimum is quite shallow for the selected time as can be seen from the figure. The shallowness is related to the strong time dependence of the location of the YES-NO boundary, because we consider a time shortly before expiry. The location of the maximum can be reliably extracted from the simulations only for rather large samples on the order of paths. One may ask whether in view of the imprecisions associated with any finite sample size it is worthwile to search for the exact maximum of . In fact, a well-chosen ‘smoothing’ procedure which subtracts the white random noise may give more accurate results than taking the real maximum of as a boundary point. For this paper we compared two variants how to determine the YES-NO boundary points:

- (3a)

-

Determine the YES-NO boundary point as the element of the set of all intersection points of the sampled paths with path for which restricted to these points attains a maximum value .

- (3b)

-

Determine the YES-NO boundary point as the element of the set of all grid points for which restricted to these points attains a maximum value . The distance between sites on the grid is lowered stepwise until some pre-defined precision is reached or more than one local extremum appears for the set of values of restricted to the grid sites.

Ultimately, in the limit of infinitely many paths both variants may give the same correct result for the optimization of . However, computation employing variant (3b) is much quicker. It requires a number of operations growing only linearly with while variant (3a) needs at least on the order of operations.

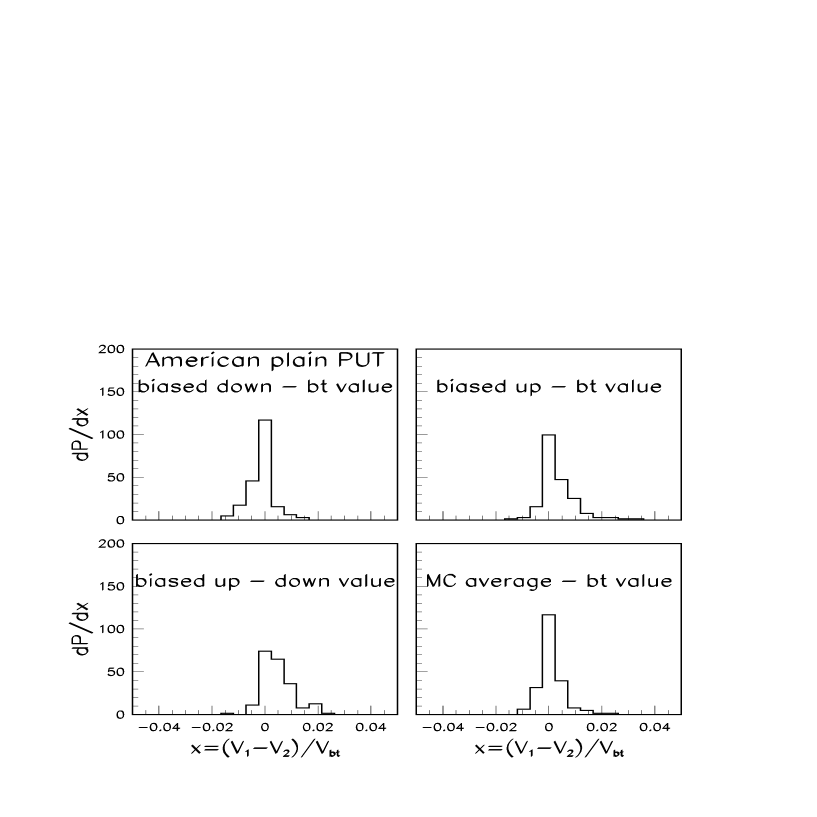

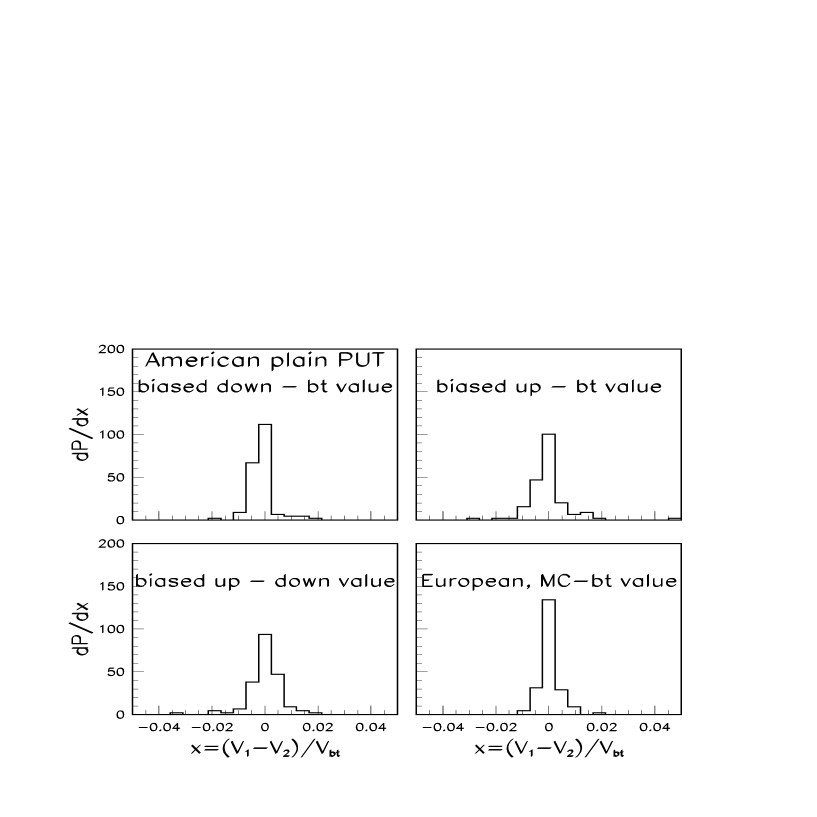

We have generated Monte Carlo estimates for prices of randomly sampled standard American-style put options (see Table I for details). We have employed the two simulation modes (3a) and (3b) to compare their effectiveness. The frequency distribution of the relative errors in the simulation results based on Monte Carlo mode (3a) are shown in Fig. 2, for mode (3b) in Fig. 3. These errors are determined from the normalized difference to the prices extracted from binomial-tree calculations:

The Monte Carlo estimates have been calculated for the path sample which has been used to determine the YES-NO boundary and for an independently generated path sample. The comparison between the results in the two modes reveals that both lead to similar accuracy. In addition, the figures display the distribution of the differences between Monte Carlo values based on the original and the independent path sample. Upward and downward bias are clearly revealed for the simulation results in mode (3a) (lower left panel of Fig. 2). On the other side, the fact that mode (3b) employs only an approximate optimization of the payoff function tends to wash out most of the up- and downward biases. Fig. 3 shows also the error distribution of the corresponding European option estimations. We note that the typical size of the errors is comparable to the results for American puts. The error in both cases is thus dominated by the finite size of the path sample ( in Figs. 2 and 3). The error induced by the bias in the construction of the YES-NO boundary at finite seems to be of less importance.

Let us turn now to the case of put options contingent on the geometric or arithmetic mean value of the underlying variable. As discussed in the preceeding section exercise and hold regions and therefore the YES-NO boundary are simply connected in the space. The boundary is therefore one-dimensional in this space. We have chosen a very simple procedure in order to track the boundary. These options are not directly contingent on the current value at any of the decision times which makes the more relevant variable. Therefore we sort the sampled paths into bins covering the relevant region. Ignoring the differences between values inside each bin we have reduced the optimization problem again to finding the value at which the payoff function attains maximum value. This optimization proceeds as described already for plain vanilla options. For the calculations described here we have taken the number of bins in direction to be 20.

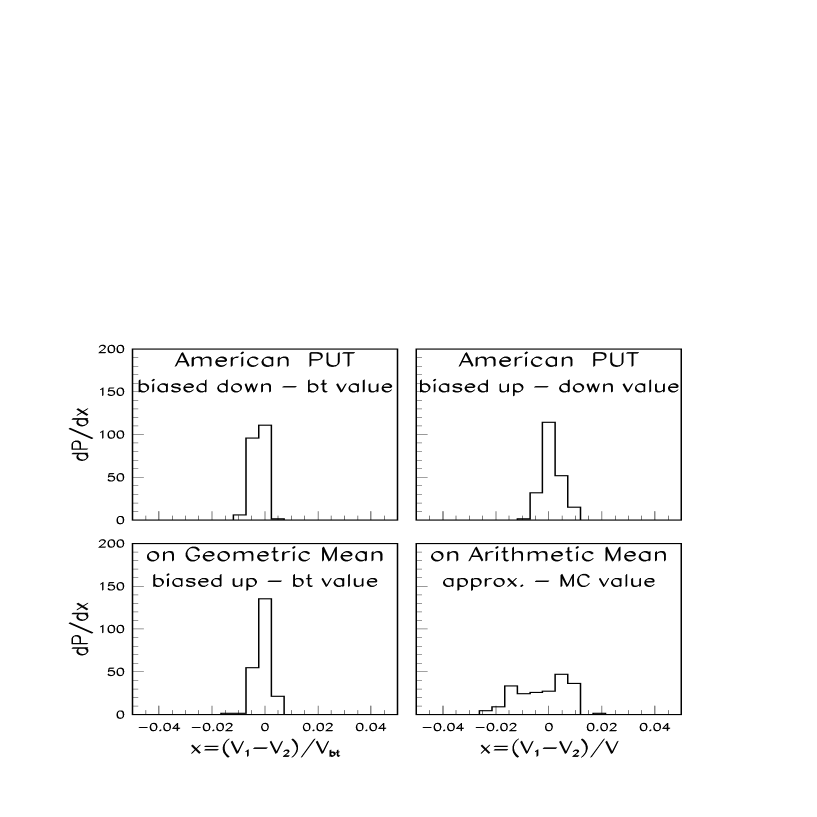

Monte Carlo simulation results for a randomly generated sample of put options contingent on geometric averages are presented in Fig. 4. As before, errors in the simulation have been calculated in case of geometric averaging by comparing the Monte Carlo estimations for the option prices to binomial tree results. Here we consider only averages over the whole lifetime of the option. This is an problem for the binomial-tree method, being the number of time steps. Allowing the time window for the averaging to slide would increase the storage and CPU time requirements by one power of . In contrast, the Monte Carlo approach is not impacted severely by such a generalization.

A comparison with the corresponding errors of the simulation results for European options under the same conditions (not shown) reveals again that the errors are dominated by the finite size of the path sample and not by the uncertainty in determining the YES-NO boundary. The effect of upward and downward bias in the estimations due to choosing either the original or the independently generated path sample are very weak as can be seen from the lower left panel of Fig. 4. As explained before this is a direct result of the approximations in the optimization procedure (3b) . It is noteworthy that the bias from parametrizing the YES-NO boundary on a grid (in direction) is stronger than either bias from taking one of the two path samples. The representation of the YES-NO boundary on a grid tends to underestimate the option prices because of the coarse graining procedure involved. The small nonstatistical downward net bias can be read off from the average deviation between Monte Carlo estimation and binomial tree results for the options contingent on geometric averages. It amounts to - 0.24 % for the results based on the original path sample and - 0.1 % for the independent path sample.

Results for prices of options contingent on arithmetic averages over the whole lifetime of the option are also included in Fig. 4 (lower right panel). Since no other accurate method is available, we present the distribution of relative deviations between the values based on an approximate formula suggested by Ritchken, Sankarasubramanian, and Vijh (1989) and the simulation results. The approximate formula relates the price for a claim contingent on the arithmetic average to the corresponding option price using geometric averaging via

| (21) |

Here () denotes “value of American (European) option”. The subscript () refers to arithmetic (geometric) averaging. The superscripts and characterize the method of calculation, binomial tree and Monte Carlo respectively. Fig. 4 shows that the approximation works reasonably well.

III Conclusions

We have shown in this paper how to construct Monte Carlo algorithms for American option valuation. We are in the lucky situation that the suggested algorithm turns out to be conceptually simpler than the other algorithms suggested so far. It depends only linearly on the number of sampled paths and exercise dates which makes it computationally feasable to get close to the continuum limit for these two variables. Thus no price is to be paid for the accuracy of this novel Monte Carlo algorithm in terms of more CPU time or exceedingly large storage requirements. The crucial element, the optimization of a certain payoff function of the path sample, turns out to be numerically rather stable. The tracking of the YES-NO boundary is achieved most precisely in those regions of the state space covered densely by sampled paths, i.e. where it is needed for the option price estimation. There is a further reason for the algorithm’s stability. In case a maximum turns out to be shallow and is therefore not easily found by the algorithm, the option price does not depend much on the exact location of the boundary between early-exercise and hold region. Indeed, we have demonstrated that the errors in the simulation results are typically dominated by the statistical errors if the size of the path sample is on the order of . This points to one important direction of future research. Paskov and Traub (1995) have shown that the replacement of pseudo-random numbers in the traditional Monte Carlo approach by a series of so-called quasi-random numbers may lead to a spectacular gain in the precision of the achievable results, at least for some problems. The reason is that the quasi-random numbers are distributed more evenly. By using appropriately chosen sequences of quasi-random numbers sample sizes for estimation of European options could be reduced by orders of magnitude, without loss of accuracy. It would open new dimensions for the applications of the novel Monte Carlo algorithm if this would also hold true for American options. Moreover, we would like to add that the extraction of sensitivity coefficients – usually called the “Greeks” – employing the novel Monte Carlo algorithm is as straightforward as for previously considered situations, e.g. by Fu and Hu (1995).

We have presented some simulations for option types for which other means of calculation are known. However, the Monte Carlo algorithm presented here provides unique opportunities to evaluate path-dependent option prices for which no other methods are available or computationally feasible. One example, the case of options contingent on arithmetic averages has been discussed already in this paper. Another candidate are “look-back” options of American style. Usually, look-back options allow the owner to buy or sell an asset for a price dependent on the values of the asset during the whole lifetime until expiry, in the simplest case the minimum or maximum. Restricting the time window for the look back but allowing for early exercise adds American features to these rather common options. Another virtue of the presented Monte Carlo algorithm is to allow option valuation for more complicated stochastic processes than Wiener-type diffusion.

References:

J. Barraquand and D. Martineau, 1995, Numerical valuation of High Dimensional Multivariate American Securities, Journal of Financial and Quantitative Analysis 30, 383-405.

F. Black, and M. Scholes, 1973, The Pricing of Options and Corporate Liabilities, Journal of Political Economy 81, 637-654.

P. Boyle, 1977, Options: A Monte Carlo Approach, Journal of Financial Economics 4 , 323-338.

P. Boyle, M. Broadie, and P. Glassermann, 1997, Monte Carlo Methods for Security Pricing, in Risk Publication Group, ed.: Pre-Course Material for RISKTM Training Course (January 1997) ‘Monte Carlo Techniques For effective Risk Management And Option Pricing’, (Risk Publication Group, London).

M. Broadie, and P. Glassermann, 1995, Pricing American-Style Securities Using Simulation, Working paper (Columbia University), to appear in Journal of Economic Dynamics and Control .

J.C. Cox, S.A. Ross, and M. Rubinstein, 1979, Option Pricing: A Simplified Approach, Journal of Financial Economics 7, 229-263.

M.C. Fu and J.Q. Hu, 1995, Sensitivity Analysis For Monte Carlo Simulation Of Option Pricing, Probability in the Engineering and Informational Sciences 9, 417-446.

R. Geske, 1979, A Note on an Analytic Valuation Formula for Unprotected American Call Options with Known Dividends, Journal of Financial Economics 7, 375-380.

D. Heath, R. Jarrow and A. Morton, 1992, Bond Pricing and the Term Structure of Interest Rates: A New Methodology, Econometrica 60, 77-105.

J.C. Hull, 1993. Options, futures, and other derivative securities, (Prentice-Hall, Englewood Cliffs).

R.C. Merton, 1973, Theory of Rational Option Pricing, Bell Journal of Economics and Management Science 4, 141-183.

S. Paskov, and J. Traub, 1995, Faster Valuation of financial Derivatives, Journal of Portfolio Management 22, 113-120.

P. Ritchken, L. Sankarasubramanian, and A.M. Vijh, 1989, The Valuation of Path Dependent Contracts on the Average, Working Paper, Case Western Reserve University and University of Southern California.

R. Roll, 1977, An Analytic Formula for Unprotected American Call Options on Stocks with Known Dividends, Journal of Financial Economics 5, 251-258.

J.A. Tilley, 1993, Valuing American Options in a Path Simulation Model, Transactions of the Society of Actuaries 45, 83-104.

R. Whaley, 1981, On the Valuation of American Call Options on Stocks with Known Dividends, Journal of Financial Economics 9, 207-211.

Table I: Parameters for random ideal Wiener processes and put options

| Parameters: | X | T | |||

|---|---|---|---|---|---|

| mean value | 0.10 | 0.40 | 100.0 | 100.0 | 0.50 |

| standard deviation | 0.05 | 0.20 | 50.0 | 50.0 | 0.25 |

Caption: Mean values of riskless interest rate , volatility , start price , strike price and time until expiry are given in first row, their standard deviations respectively in second row. The random values are chosen according to independent normal distributions. In a second step, some parameter values may be rejected and replaced by other random values if they are nonpositive. Furthermore, strike price is required to be within a 2 (1) range around the mean value at maturity for options contingent on the current (average) value. This constraint could be relaxed using a more sophisticated importance sampling scheme. The number of evenly spaced time steps for the Monte Carlo simulation and the binomial-tree calculations has been fixed arbitrarily to be equal 100.

Figure Captions:

Figure 1:

Monte Carlo estimation of the optimization function for a plain vanilla put option. Option and stochastic process parameters are chosen as in Hull’s book (1993), Example 14.1. The Monte Carlo simulation with number of time steps equal 50 has been repeated varying the total number of sampled paths: , , and . Only the function values at time step 45 are displayed for 100 values of the argument . The location of the YES-NO boundary according to a binomial-tree calculation is pointed at by an arrow.

Figure 2:

Frequency distribution of the relative errors in simulation estimates of a sample of plain put option prices. The error is determined from the normalized difference to the prices extracted from binomial-tree calculations. The Monte Carlo estimates are calculated for the path sample which has been used to determine the YES-NO boundary (biased up) as well as for an independently generated path sample (biased down) and the average of the two samples (MC average). In addition, the figure displays the distribution of the difference between upward and downward biased Monte Carlo values (lower left panel). Each path sample encompasses generated paths per option. The Monte Carlo simulation employed the mode in which the ‘global maximum’ of the optimization function was searched.

Figure 3:

The content of this figure is the same as in the previous figure, with the exception of two features. The mode of the Monte Carlo simulation has been to look up the maximum of the optimization function on a grid (see text). Furthermore, the distribution of errors for the averaged Monte Carlo values which looks very similar to the corresponding distributions of upward and downward biased estimates is not displayed. Instead, the distribution of the errors for the corresponding European option values is displayed (in the lower right panel).

Figure 4:

Frequency distribution of deviations between simulation estimates of put option prices on geometric (left side) and arithmetic average values (right side) and benchmark calculations. The benchmark for the prices on geometric averages is provided by the rather accurate binomial-tree method, and for the arithmetic averages by the approximate formula eq. (21).