NON PARAMETRIC THRESHOLD ESTIMATION FOR MODELS

WITH STOCHASTIC DIFFUSION COEFFICIENT AND JUMPS

Cecilia Mancini

Università di Firenze, Dipartimento di matematica per le decisioni,

via C.Lombroso, 6/17, 50134 Florence, Italy, tel. +39 055 4796808, fax +39 055 4796800

cecilia.mancini@dmd.unifi.it

Summary

We consider a stochastic process driven by a diffusion and jumps.

We devise a technique, which is based on a discrete record

of observations, for identifying the times when jumps larger than a suitably

defined threshold occurred. The technique allows also

jump size estimation. We prove the consistency of a nonparametric estimator of

the integrated infinitesimal variance of the process continuous part when the jump component with infinite activity

is Lévy.

Central limit results are proved in the case where the jump component has

finite activity.

Some simulations illustrate the reliability of the methodology in finite

samples.111

AMS 2000 subject classifications. Primary: 62G05,

62G20, 62M99; secondary: 7M05 37M10.

The results of this paper were presented:

to the 3rd World Congress of the Bachelier Finance Society, Chicago, 21-24 July 2004;

to the workshop Quantitative Methods in Finance, Newton Institute, Cambridge, 31/1/05 - 4/2/05;

to the 9th World Congress of the Econometric Society, London, 19th - 24th August 2005,

http://www.econ.ucl.ac.uk/eswc2005/

Key words: discrete observations, non parametric estimation, models with stochastic diffusion coefficient and jumps, threshold, integrated infinitesimal variance of the continuous component, asymptotic properties.

1 Introduction

We consider a stochastic process starting from at time and such that

| (1) |

where and are progressively

measurable processes,

is a standard Brownian motion and is a pure jump process. A

jump process is said to have finite activity (FA) when it

makes a.s. a finite number of jumps in each finite time interval,

otherwise it is said to have infinite activity (IA). We

provide an estimate of , denoted by ,

given discrete observations . The

estimator is consistent both when has FA and when the IA

component of is Lévy. stands for Integral of the

infinitesimal Variance of the continuous part of ; is also called integrated volatility in the

financial econometric literature. When has FA we also give an

estimate of jump times and sizes, while, when has IA we can

identify the instants when jumps are larger than a given threshold.

These results have important applications in financial

econometrics, see the reviews in Andersen et al. (2005) and Barndorff-Nielsen

and Shephard (2006).

The method we propose here extends previous work in Mancini (2001)

and Mancini (2004) allowing for infinite jump activity and very mild

assumptions on and .

Nonparametric estimation of the diffusion coefficient has

been studied, in absence of the jump component, e.g. by

Barndorff-Nielsen and Shephard (2002). For a review see Fan (2005).

However, the inclusion of jumps within financial models seems to be

more and more necessary for practical applications (Das, 2002;

Piazzesi, 2005; Bates, 2002).

In the literature on non parametric inference for stochastic processes

driven by diffusions plus jumps, several approaches have been

proposed to separate the diffusion part and the jump part given

discrete observations.

Berman (1965) defined power variation estimators of the sum of

given powers of the jumps.

Recently these have been recovered and developed in

Barndorff-Nielsen and Shephard (2004a), Woerner (2006) and Jacod (2006).

Barndorff-Nielsen and Shephard (2004a, 2004b) define and use the

bipower and the multipower variation processes to

estimate for given values of , and in

particular they focus on . They assume that is

independent of the leading Brownian motion (in the financial

literature this is called no leverage assumption) and that

the jump process has finite activity. In particular they build a

test for the presence of jumps in the data generating process.

Barndorff-Nielsen et al. (2006) and Woerner (2006) show that, in

particular cases, the consistency and central limit theorem of the

multipower variation estimators

can be extended in the presence of infinite activity jump processes.

Bandi and Nguyen (2003) and Johannes (2004)

assume that and that

has FA bounded jumps. They use Nadaraya Watson kernels to obtain

pointwise estimators of the functions and and

aggregate information about . Mancini and Renò (2006) combine the

kernel and the threshold methods

to improve the estimation of the jump part and they extend the results

to the infinite jump activity framework.

Our contribution to the extant literature can be summarized as

follows. First,

in the FA case, threshold estimation is a

more effective way to identify intervals where

jumped. Second,

the threshold estimator of is more efficient (in the Cramer-Rao

inequality lower

bound sense) than the multipower variation estimators. Finally, the

consistency of the threshold estimator holds even under leverage and

when the observations are not equally spaced, both in the FA and in

the IA of jump cases. An alternative extension has been made in

Jacod (2006), where, in order

to obtain a central limit theorem, the diffusion coefficient dynamics

has to be specified.

The good performance of our estimator on finite samples of realistic

length is shown within three different simulated models.

An outline of the paper is as follows: in section 2 we introduce the

framework and the notations; in section 3 we deal with the case

where has FA: we show that by the threshold method we can

asymptotically identify each instant of jump. As a consequence we

obtain threshold estimators of and of each

stochastic size of the occurred jumps. Using results in

Barndorff-Nielsen et al. (2005) and in Barndorff-Nielsen and

Shephard (2006) we show the asymptotic normality of ,

whatever the dynamics for . Moreover we find the asymptotic

distribution of the estimation error of the sizes of jump under the

no leverage assumption and when the jump component is a compound

Poisson process. Section 4 is devoted to the case when the

underlying process contains an infinite activity Lévy jump part: in

a quite simple way we show that the threshold estimator of is

still consistent, even under leverage and when the observations are

not equally spaced. Section 5 shows the performance of the estimator

of in finite samples within three different simulated models.

Section 6 concludes.

Acknowledgements. I’m sincerely grateful to Rama Cont, Jean Jacod and Roberto Renò for the important comments on this work. I also want to thank PierLuigi Zezza. I thank Sergio Vessella and Marcello Galeotti who supported this research by MIUR grant number 2002013279 and Progetto Strategico.

2 The framework

On the filtered probability space (, , , P), let be a standard Brownian motion and be a pure jump process given by , where has FA and has IA and is Lèvy. Let be a real process starting from and such that

| (2) |

where , are progressively measurable processes which guarantee that (2) has a unique strong solution on which is adapted and right continuous with left limits (se e.g. Ikeda and Watanabe, 1981; Protter, 1990). Suppose that on the finite and fixed time horizon we dispose of a discrete record of observations of a realization of , with , for a given lag , .

When is a pure jump Lévy process, we can always decompose it as the sum of the jumps larger than one and the sum of the compensated jumps smaller than one, as follows

| (3) |

where is the Poisson random measure of the jumps of ,

is the compensated

measure, and is the Lévy measure of (see Sato, 1999 or

Ikeda and Watanabe, 1981). is a square integrable

martingale with infinite activity of jump.

For each , .

is a compound Poisson process with finite activity of jump, and we can also write

, where is a Poisson

process with constant intensity , jumping at times denoted

by , and each , also

denoted , is the size of the jump occurred at

. The random variables are i.i.d. and

independent of .

More generally a FA jump process is of the form

, where is a non explosive

counting process and the random variables are not

necessarily i.i.d., nor independent of

.

Denote by the first instant a jump occurs within

, if ; by the size of this first jump within , if ; by

.

Next section deals with the FA case where ,

while in section 4 we allow to have infinite

activity, where is Lévy.

Further notations.

For any semimartingale , let us denote by the increment and

by the size of the jump (eventually) occurred at time .

is the quadratic variation process associated to .

is the estimator of the quadratic variation .

denotes the sigma-algebra generated by the process .

is the process given by the stochastic integral .

.

. This quantity is called in the econometric literature integrated quarticity of .

By (low case) we denote generically a constant.

means ”limit in probability”; means ”limit in distribution”.

If is a r.v., indicates the mixed

Gaussian law having characteristic function .

3 Finite activity jumps

3.1 Consistency

An important variable related to and containing is the quadratic variation at

| (4) |

An estimate

of is given by ,

since

where is a finite

partition of , and

.

We consider in this section the case in which has FA,

so that

(4) becomes

and the quadratic variation gives us only an aggregate information regarding both and the jump sizes. In order to estimate the contribution of to , the key point is to exclude the time intervals where jumped. The following theorem provides an instrument to asymptotically identifying such intervals.

Theorem 3.1.

Suppose that is a finite activity jump

process where is a non explosive counting process and the random

variables satisfy .

Suppose also that

1) a.s.

2) a.s. and

;

3) is a deterministic function of the lag between the

observations, s.t.

then for P-almost all s.t. we have

| (5) |

Assumption 3) indicates how to choose the threshold . The absolute value of the increments of any path of the Brownian motion (and thus of a stochastic integral with respect to the Brownian motion) tends a.s. to zero as the deterministic function . Therefore, for small , when we find that the squared increment is larger than some jumps had to be occurred.

For the proof we need the following preliminary remarks.

The Paul Lévy law for the modulus of continuity of Brownian motion’s paths (see e.g. Karatzas and Shreve, 1999, theorem 9.25) implies that

The stochastic integral is a time changed Brownian motion (Revuz and Yor 2001, theorems 1.9 and 1.10): defined the pseudo-inverse of , , then

| (6) |

where is a Brownian motion.

As a consequence, under assumptions 1) and 2) of theorem 3.1, by Karatzas and Shreve (1999, theorem 9.25) and the monotonicity of the function it follows that a.s. for small

where is a finite r.v..

Proof of the theorem. First we show that a.s., for small , it holds that , then we will see that a.s., for small , it holds also that , and that will conclude our proof.

1) For each set : to show that a.s., for small , it is sufficient to prove that a.s., for small , To evaluate the , remark that a.s.

In particular, for small , , as we need.

2) Now we establish the other inequality. For any set . In order to prove that a.s., for small , it is sufficient to show that a.s., for small , . In order to evaluate remark that

the first term tends a.s. to zero uniformly with respect to . Since for small we have that for each , then the other terms become

The contribution of the first term within brackets tends a.s. to zero uniformly on . Note that the assumption on guarantees that , thus a.s.

∎

Remarks.

i) Assumption 1) simply asks for the sequence keeping bounded as . It is satisfied if, for example, is bounded pathwise on . In particular assumption 1) is satisfied in a model with mean reverting drift .

If we assume that in equation (2) and are processes having right continuous paths with left limits (càdlàg), then assumptions 1) and 2) are immediately satisfied, since a.s. such paths are bounded on [0,T].

ii) Note that a FA Lévy process satisfies that , since (jumps occurring with zero size are not jumps). E.g. this is the case for a compound Poisson process with Gaussian sizes of jump.

iii) Frequently, in practice, the lag between the observations of an available record is not constant (not equally spaced observations). Theorem 3.1, and thus also (7) below, is still valid. In fact if we set , all the fundamental ingredients of the proof of theorem 3.1 hold:

by the monotonicity of Moreover, using (6), it still holds that

since

It is asymptotically equivalent to directly compare each with

the relative : a.s. for small we have, for each

,

∎

Define

The consistency of is a consequence of theorem 3.1, which is needed in order to asymptotically identify and exclude each jump instant.

Corollary 3.2.

Under the assumptions of theorem 3.1 we have

| (7) |

Proof. Since a.s. for small we have uniformly on , then

which coincides with since ∎

3.2 Central limit theorems

As a corollary of theorem 2.2 in Barndorff-Nielsen et al. (2005), from our theorem

3.1 we obtain a threshold estimator of , which is alternative to the power variation

estimator. An estimate of is needed in

order to give the asymptotic law of the approximation error

. We reach a

central limit result for

whatever the dynamics for .

Theorem 3.3 (power variation estimator: theorem 2.2 in Barndorff-Nielsen and al. (2005), case ).

If , where is predictable and locally bounded and is càdlàg, then for

∎

In the light of this result we now state the following asymptotic properties of the threshold estimator of .

Proposition 3.4.

Under the same assumptions as in theorem 3.1 and the assumptions of theorem 2.2 in Barndorff-Nielsen et al. (2005) we have that

Proof. By theorem 3.1

The latter coincides with

| (8) |

since

| (9) |

Finally (8) coincides with , as Barndorff-Nielsen et al. (2005) have shown. ∎

Finally, as a corollary of theorem 1 in

Barndorff-Nielsen and Shephard (2006) we have the following result

of asymptotic normality

for our estimator

Theorem 3.5 (Theorem 1 in Barndorff-Nielsen and Shephard (2006)).

If , where and are càdlàg processes then, as

where is a Brownian motion independent of (recall from the notations that ).∎

Proposition 3.6.

Under the assumptions of theorem 3.1 and if is cadlag and locally bounded, is cadlag and -measurable, then we have

Proof. Denoting by the continuous process given by , for all , similarly as in (9)

coincides with

The first factor tends in law to , by Barndorff-Nielsen and Shephard result (2006, theorem 1). However (Jacod and Protter, 1998) is independent on the whole . Now the assumption ensures that is independent of and thus, conditionally on , is again a Brownian motion and is Gaussian with law . Thus, conditionally on , we have that . However the convergence in distribution holds even without conditioning. ∎

Remarks.

i) A comparison with the bipower variation (BPV) estimator shows that the advantages of the non parametric threshold method are al least two.

The threshold estimator of is efficient (in the Cramer-Rao inequality lower bound sense), in fact we showed that tends in distribution to , while Barndorff-Nielsen and Shephard (2004b, p.29) show that (under the further assumption that is a diffusion) the limit law is . In particular the threshold estimator is efficient (see Aït-Sahalia, 2004 for constant ).

Moreover, since we asymptotically identify each jump instant, we can apply known estimation methods for diffusion processes also to jump-diffusion processes as soon as we have eliminated the jumps (see e.g. Mancini and Renò, 2006).

ii) In Mancini and Renò (2006) we show that it is possible to consider also a time varying threshold, which is particularly important for the practical application of the estimator.∎

By theorem 3.1 and by the fact that, for small , the probability of more than one jump over an interval is low, it is clear that an estimator of each jump instant is obtained through

Moreover a natural estimate of each realized jump size is given by

since when a jump occurs then the contribution of to is asymptotically negligible. In

Mancini (2004) we have shown the consistency of each

when . However we only gave a lower

bound for the speed of convergence when the coefficients

and are stochastic processes. Here we show that, at least under

the no leverage assumption and when is Lévy,

the speed is exactly .

Theorem 3.7.

If is a compound Poisson process, if a.s. for some (which is the case if is càdlàg), if is an adapted stochastic process with continuous paths, if is independent of and , with , if the threshold is chosen as in theorem 3.1 then

Proof.

by theorem 3.1, a.s. for small , the first term vanishes. The third term tends to zero in probability, since

Therefore we only have to compute the

| (10) |

However, since for small

as , (10) coincides with

Let us compute the characteristic function

conditionally on , are independent Gaussian random variables with law . Since and are independent (Ikeda and Watanabe, 1981), our characteristic function equals

| (11) |

However , and

where, for each , are suitable points belonging to . Therefore (Chung, 1974, p.199) (11) tends to which coincides with (Cont and Tankov, p.78) the characteristic function of a mixed Gaussian r.v. where and ∎

4 Infinite activity jumps

Let us now consider the case when has possibly infinite activity. Denote

| (12) |

and note that since , then as

In fact our threshold estimator is still able to extract from the observed data. The reason is that now

and the threshold cuts off all the jumps of and the jumps of larger, in absolute value, than

. However such jumps are all jumps of when .

Theorem 4.1.

Let the assumptions 1) (pathwise boundedness condition on ), 2) (pathwise boundedness condition on ) and 3) (choice of the function ) of theorem 3.1 hold. Let be such that has FA with for all , for all ; let be Lévy and be independent of . Then

| (13) |

Jacod (2006) proves the consistency of the threshold estimator when the jump process is a more general pure jump semimartingale, with the choice . The proof we present here is simpler and it allows to understand the contribution of the different jump terms to the estimation bias. Most importantly, the advantage of the approach presented here is that it allows to prove a central limit theorem for without any substantial assumption on , while in Jacod (2006) an assumption on the dynamics of is needed in order to get a CLT. This topic is further developed in Cont and Mancini (2005).

To prove theorem 4.1 we decompose into

the sum of a jump diffusion process, , with stochastic

diffusion coefficient and a finite activity jump part, plus an

infinite activity compensated process of small jumps.

We use corollary 3.2 for the first term, and we show that

the contribution of each is negligible within the truncated

version

of .

Proof. Since , we can write

| (14) |

By corollary 3.2 we know that the first term of the

left hand side tends to zero in probability. We now

show that the of each one of the other three terms of the left hand side is zero.

Let us deal with the second term:

| (15) |

If , since

then . Thus a.s.

| (16) |

The first term is a.s. dominated by

| (17) |

as , since

Moreover

| (18) |

For the second term of (15) we note that by theorem 3.1 for small on we have, uniformly with respect to , . Therefore for small

However, by theorem 3.1, for small a.s. and thus

Let us now deal with (half) the of the third term on the left hand side of (14), which coincides with

| (19) |

In fact if and then , i.e. , so that , and then

| (20) |

Since for small , uniformly in , , then

| (21) |

which tends to zero as in (18).

In order to deal now with (19), note that if and then

so a.s. uniformly in . Therefore a.s. for small , on we have . Thus (19) is dominated by

by the Schwartz inequality and remark 4.2 below.

Finally let us show that last term of the left hand side of (14) tends to zero in probability. Analogously as in (21)

so that last term of (14) coincides with

by remark 4.2. ∎

Remark 4.2.

A.s., for small , uniformly in , on we have that all the jumps are bounded by , that is

More precisely on we have , therefore

are the increments of the process

given by

As a consequence

| (22) |

since last term has expectation , as .

In fact

as , meaning that a.s., uniformly on , tends to zero more quickly than , that is for small , for all , and thus for each . ∎

Remarks.

i) Everything is still valid if we have non equally spaced observations. In fact if we set, as in the remark of the previous section, , the term , we often encounter from equation (17) on, is still negligible, since as , . On each jump size , so that (22) still holds.

ii) Consistently with the results in Barnodrff-Nielsen et al. (2006) for the multipower variations and in Jacod (2006), the asymptotic normality of our estimator of does not hold in general if has an infinite activity Lévy jump component and general cadlag coefficient (Cont and Mancini 2005). Namely the asymptotic normality holds when the jump component has a moderate jump activity (when the Blumenthal-Gatoor index of belongs to ), while the speed of convergence of is less than if the activity of jump of is too wild ().

5 Simulations

In this section we study the performance of our threshold estimator

on finite samples. We implement the threshold estimator within three

different simulated models which are commonly used in finance: a

jump diffusion process with jump part given by a compound Poisson

process with Gaussian jump sizes; a similar model with

stochastic diffusion coefficient correlated with the Brownian motion

driving the dynamics of ; and a model with an

infinite activity (finite variation) Variance Gamma jump part.

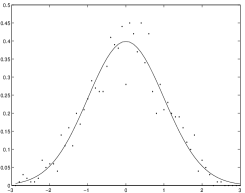

MODEL 1. Let us begin with the case of a jump diffusion process with finite activity compound Poisson jump part. We generated trajectories of a process of kind

with i.i.d. with law , where , and is intentionally chosen higher than a realistic situation, , like as in Aït-Sahalia (2004). To generate each path we discretized EDS (2) and we took equally spaced observations with lag so that . We chose . Figure 1 shows the distribution of the 5000 values assumed by the normalized bias term

| (23) |

versus the standard Gaussian density (continuous line).

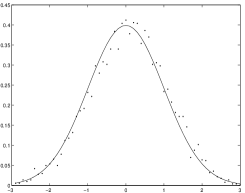

MODEL 2. Let us now consider a process with jump part given by a finite activity compound Poisson process and a stochastic diffusion coefficient correlated with the Brownian motion driving . We generated trajectories of a process of kind

where

Note that

We chose , and a negative correlation coefficient ; then we took , , , so to ensure that a path of within varies most between 0.2 and 0.4. Moreover , give relative amplitudes of the jumps of most between 0.01 and 0.20. Finally we again took equally spaced observations with lag and . Figure 2 shows the distribution of the normalized bias term (23) against the asymptotic density (continuous line).

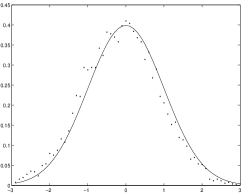

MODEL 3. Figure 3 shows the distribution obtained in the case of a Variance Gamma (VG) jump component. The VG process is a pure jump process with infinite activity and finite variation. We add to it a diffusion component :

The subordinator is a Gamma process having , and are independent Brownian motions; we chose , and . , and are chosen as in Madan (2001); is chosen so that matches the we obtained for model 1. Finally .

6 Conclusions

In this paper we devise a technique for identifying the time

instants of significant jumps for a process driven by diffusion and

jumps, based on a discrete

record of observations, making use of a suitably defined threshold.

We provide a consistent estimate of , extending previous results

(Mancini 2001, 2004) with very mild assumptions on and and, most importantly,

allowing for infinite jump activity.

When has finite activity, we give

a nonparametric estimate of the jump times and sizes, while when

has a pure jump Lévy component with infinite activity we can

identify the instants when jumps are larger than the threshold.

When has FA we also prove central limit results for and for the jump sizes estimates.

Compared with power variations, multipower variations or kernel estimators the threshold method in the FA case is a more effective way to identify each interval where jumped.

We also prove that the threshold estimator of is efficient.

Moreover, our method allows the extension of kernel estimators in diffusion frameworks to

processes driven by diffusions and jumps, provided we eliminate the jumps (Mancini and Renò, 2006).

The consistency of the threshold estimator holds even under leverage, both in FA and IA cases.

The threshold technique holds even when the observations are not equally spaced and also when the threshold

is time varying, which is

particularly important for the practical application of the estimator.

The advantage of the approach presented here is that it allows to prove a central limit theorem for without any substantial assumptions on , while in Jacod (2006) an assumption on the dynamics of is needed in order to get a CLT. This topic is further developed in Cont and Mancini (2005).

The good performance of our estimator on finite samples of realistic length is shown within three different simulated models.

References

Aït-Sahalia, Y. (2004). Disentangling volatility from jumps. Journal of Financial Economics, 74, 487-528

Andersen, T.G., Bollerslev, T., Diebold, F.X. (2005). Parametriuc and nonparametric volatility measurement. In: Handbook of financial econometrics, Y. Aït-Sahalia and L.P. Hansen Eds

Bandi, F.M., and Nguyen, T.H. (2003). On the functional estimation of jump-diffusion models. Journal of Econometrics, 116, 1, pp. 293-328(36)

Barndorff-Nielsen, O.E., Gravensen, S.E., Jacod, J., Podolskij, M. and Shephard, N. (2005). A central limit theorem for realised power and bipower variation of continuous semimartingales. To appear in From Stochastic Analysis to Mathematical Finance, Festschrift for Albert Shiryaev

Barndorff-Nielsen, O.E., Shephard (2002). Econometric analysis of realized volatility and its use in estimating stochastic volatility models. Journal of the Royal Statistical Society, Series B, 64, 253-280

Barndorff-Nielsen, O.E. and Shephard, N. (2004a). Power and bipower variation with stochastic volatility and jumps (with discussion). Journal of Financial Econometrics 2, 1-48

Barndorff-Nielsen, O.E. and Shephard, N. (2004b). Econometrics of testing for jumps in financial economics using bipower variation. Journal of Financial Econometrics, 2006, 4, 1-30

Barndorff-Nielsen, O.E. and Shephard, N. (2006): Variation, jumps and high frequency data in financial econometrics. In Advanced in Economics and Econometrics. Theory and Applications, Ninth World Congress Eds Richard Blundell, Persson Torsten, Whitney K Newey, Econometric Society Monographs, Cambridge University Press

Barndorff-Nielsen, O.E., Shephard, N., Winkel, M. (2006), Limit theorems for multipower variation in the presence of jumps. Stochastic Processes and Their Applications, 2006, 116, 796-806

Berman, S.M. (1965). Sign-invariant random variables and stochastic processes with sign invariant increments. Trans. Amer. Math. Soc, 119, 216-243

Chung, K.L. (1974). A course in probability theory. Academic Press Inc.

Cont, R. and Mancini, C. (2005). Detecting the presence of a diffusion and the nature of the jumps in asset prices. Working paper

Cont, R. and Tankov, P. (2004). Financial modelling with jump processes. Chapman& Hall - CRC

Das, S. (2002). The surprise element: jumps in interest rates. Journal of Econometrics, 106, 27-65

Fan, J. (2005). A selective overview of nonparametric methods in finance. Statistical Science 20 (4), 317-337

Ikeda, N., Watanabe, S. (1981). Stochastic differential equations and diffusion processes. North Holland

Jacod, J. (2006). Asymptotic properties of realized power variations and associated functionals of semimartingales. arXiv, 20 April 2006 n. 0023146

Jacod, J., Protter, P. (1998). Asymptotic error distributions for the Euler method for stochastic differential equations. The Annals of Probability 26, 267-307

Johannes, M. (2004). The statistical and economic role of jumps in continuous-time interest rate models. The Journal of finance, 59, 227-260.

Karatzas, I., Shreve, S.E. (1999): Brownian motion and stochastic calculus. Springer

Madan, D.B. (2001) Purely discontinuous asset price processes. Advances in Mathematical Finance Eds. J. Cvitanic, E. Jouini and M. Musiela, Cambridge University Press

Mancini, C. (2001). Disentangling the jumps of the diffusion in a geometric jumping Brownian motion. Giornale dell’Istituto Italiano degli Attuari, Volume LXIV, Roma, 19-47

Mancini, C., (2004). Estimation of the parameters of jump of a general Poisson-diffusion model. Scandinavian Actuarial Journal, 2004, 1:42-52

Mancini, C., Renò, R. (2006). Threshold estimation of jump-diffusion models and interest rate modeling. working paper

Piazzesi, M. (2005). Bond Yields and the Federal Reserve. Journal of Political Economy 113 (2), 311-344

Protter, P., (1990) Stochastic integration and differential equations. Springer-Verlag

Revuz, D., Yor, M. (2001) Continuous martingales and Brownian motion. Springer

Sato, K., (1999). Lévy Processes and infinitely divisible distributions. Cambridge University Press

Woerner, J. (2006): Power and Multipower variation: inference for high frequency data. In Stochastic Finance, eds A.N. Shiryaev, M. do Rosário Grossinho, P. Oliviera, M. Esquivel, Springer, 343-364.