12\AOSMAKETITLE

2006 \AOSvol00 \AOSno00 \AOSpp000–000 \AOSReceivedReceived \AOSAMSPrimary 62H20; secondary 62E99 \AOSKeywordscorrelation, covariance, test of independence, spectral decomposition, eigenvalues, eigenfunctions, Hilbert-Schmidt operator, Fréchet bounds, contingency tables, phi-square, canonical correlation, Cramér-von Mises tests, rank tests, Fredholm integral equation of the second kind. \AOStitleON A NEW CORRELATION COEFFICIENT, ITS ORTHOGONAL DECOMPOSITION AND ASSOCIATED TESTS OF INDEPENDENCE\AOSauthorWicher Bergsma111Supported by The Netherlands Organization for Scientific Research (NWO), Project Number 400-20-001. \AOSaffilLondon School of Economics and Political Science\AOSlrhWicher Bergsma\AOSrrhA new correlation coefficient\AOSAbstractA possible drawback of the ordinary correlation coefficient for two real random variables and is that zero correlation does not imply independence. In this paper we introduce a new correlation coefficient which assumes values between zero and one, equalling zero iff the two variables are independent and equalling one iff the two variables are linearly related. The coefficients and are shown to be closely related algebraically, and they coincide for distributions on a contingency table. We derive an orthogonal decomposition of as a positively weighted sum of squared ordinary correlations between certain marginal eigenfunctions. Estimation of and its component correlations and their asymptotic distributions are discussed, and we develop visual tools for assessing the nature of a possible association in a bivariate data set. The paper includes consideration of grade (rank) versions of as well as the use of for contingency table analysis. As a special case a new generalization of the Cramér-von Mises test to ordered samples is obtained.

3

Contents:

1 Introduction

We introduce a correlation coefficient which has the potential advantage compared to the ordinary correlation that it detects arbitrary forms of association between two real random variables and . In fact , to be defined below, can be viewed as a simple modification of , as we now show. The ordinary covariance is defined as

and the ordinary correlation as

Now suppose that , and are iid with distribution function , that and have marginal distributions and , and that and are iid replications of . Then with

| (1) |

it is easy to verify that

| (2) |

Now straightforward algebra based on the left hand side of (1) shows that we can rewrite as

Replacing the squares in by absolute values then gives

| (3) |

and we can define a new ‘covariance’ by replacing by in (2):

Now we can also define

Thus, whereas the squared covariance and are based on squared differences, and are based on absolute differences. In this paper we demonstrate the perhaps surprising result that , such that iff and are independent, and iff and are linearly related. A further main result we give is an orthogonal decomposition of in terms of component correlations between eigenfunctions of and .

Based on their formulas, the following statistical interpretation of and can be given: they measure how much two observations which are ‘far’ apart tend to occur with observations which are ‘far’ apart, and similarly how much two observations which are ‘close’ together tend to occur with observations which are ‘close’ together.

This paper is organized as follows. In Section 2, the properties of the kernel function are investigated in detail. Some general properties are given, including conditions for its existence and a proof that it is positive, and a large part of the section is devoted to the spectral decomposition of . We show that if is square integrable, it has a mean square convergent spectral decomposition in terms of the eigenvalues and vectors of . For discrete , a set of difference equations is given which has this eigensystem as its solution, and for continuous an analogous differential equation is given. The numerical solution of these equations is treated in some detail. Closed form solutions are only available in some special cases, for example, if belongs to the uniform distribution on , the eigenfunctions of are the Fourier cosine functions.

The results of Section 2 are used in Section 3 to derive properties of . We demonstrate the aforementioned result that , such that iff and are independent, and iff and are linearly related. Furthermore, a decomposition of is given in terms of a sum of squared correlations between marginal eigenfunctions of and weighted with the product of the corresponding marginal eigenvalues. We give a parameterization of the likelihood in terms of component correlations of and the marginal eigenfunctions, somewhat analogous to the well-known canonical correlation decomposition. Fréchet bounds for the component correlations are discussed, which gives some insight into the possible structure of the dependence between two random variables. Finally in this section, component correlations for the normal distribution are discussed as an illustration.

In Section 4, we derive sample and unbiased estimators of and related estimates of , which can be calculated in time . The asymptotic distributions of the estimators under independence, which is a mixture of chi-squares, is derived. Finally, small sample permutation tests and Bonferroni corrections for testing the significance of component correlations are discussed.

Section 5 concerns grade versions of and , copulas, and rank tests. Rank statistics, obtained from the grade versions of and , are discussed. It is shown that the two sample Cramér-von Mises statistic is obtained as a special case, as well as a new generalization to the case of ordered samples. Furthermore, it is shown that is a weighted mean of phi-square coefficients obtained from collapsing the distribution onto a table with respect to cut-points .

In Section 6 we propose a methodology for gaining an understanding of the association between two variables from a data set. The methodology is based on combining hypothesis tests with visual tools for displaying how much individual observations contribute to the association.

Although many of the results of the present paper are new, we have, naturally, also borrowed much from the literature, particularly concerning the eigensystems and orthogonal decompositions. Some important references here are ? (?, ?), ? (?) and ? (?), among others. However, the focus of much of the literature we refer to is on studying power of hypothesis tests. The aim of this paper, on the other hand, is on providing a meaningful coefficient for describing association, which we hope leads to a useful methodology for gaining an understanding of the association between two variables, and, along the way, to tests with high power against salient alternatives, the salience of the alternatives being determined by the size of .

Throughout this paper, we use the following conventions and assumptions. We assume that , and are iid with marginal distribution functions and , respectively, and joint distribution function . We impose no restrictions on the distributions, i.e., they may be continuous, discrete, or mixed continuous-discrete. For simplification of some of the derivations, we define distribution functions in the following slightly non-standard way:

and

2 Properties of the kernel function

In this section a detailed description is given of the kernel function defined by (3). Section 2.1 concerns existence, continuity, positivity, square integrability, existence of the trace and the shape of the graph of . Methods for verifying whether several of these properties hold are given. In Section 2.2, under the assumption of square integrability of , its spectral decomposition is given, and some properties of the associated eigenvalues and functions are derived. The eigensystem is the solution to an integral equation which may be difficult to solve. The problem is reformulated in terms of difference equations for the discrete case in Section 2.3 and in terms of a differential equation for the continuous case in Section 2.4. Both rewrites appear much easier to solve than the integral equation. In Section 2.5, efficient numerical approximation of the eigensystem of for continuous is discussed. For several well-known distributions, including the uniform and the normal, closed form solutions or numerical approximations of (parts of) the eigensystem are given. A new distribution is introduced which has the seemingly rare property that is square integrable but has infinite trace. In Section 2.6 the relation between and a kernel introduced by ? (?) is given. We are not aware of the kernel , depending on , having been described previously.

2.1 Key properties of

The kernel exists if is finite for some . The kernel is positive if

| (4) |

for every function for which the expectation exists. The kernel is square integrable if

| (5) |

is finite. The kernel is trace class if its trace

is finite. In several lemmas below we give some relatively easily verifiable conditions for checking whether these properties hold for . The final Lemma 4 concerns the shape of the graph of .

The next lemma may simplify verification of the existence of , and asserts continuity and positivity as well as giving another integral representation of . First we need the following notation:

Note that

| (7) | |||||

| (8) |

Lemma 1

If exists it exists on . It is then continuous and positive, with equality in (4) only for the constant function, and has the representation

Proof We first show continuity of on its domain. Let . Then if and ,

Hence, is continuous and bounded on any finite domain. Therefore, if exists in one point it exists on .

We next derive the integral representation of . We have

| (9) |

and with the th largest number in the set , we have

| (12) | |||||

Now we can derive the desired result first using (9), then applying Fubini’s theorem which is justified because (12) is finite, and finally using (7):

| (13) | |||||

Finally, we show positivity of . Let be nonconstant. Then using (13) and Fubini’s theorem,

Hence, is positive. If is constant it is easily verified that the expression is zero. \endproof

Note that from the lemma, it follows that for checking existence of , it suffices to check existence of . Now has the following convenient representations

| (14) | |||||

These representations are immediately verified from (3) and from the representation of given in Lemma 1.

An example of a random variable for which does not exist is , where has a Cauchy distribution. This can be verified by checking that (14) does not converge.

By giving some alternative representations of (5), the next lemma may be helpful in the verification of square integrability of :

Lemma 2

We have:

| (15) |

Proof To prove the first equality, write . Then, since for example and , we obtain

It may now be verified that equals 0 if or , and equals otherwise. Hence, and because , we have

which is the first part of the lemma.

To prove the second equality, first note that

| (16) |

We now have using Lemma 1, Fubini’s theorem (for justification see proof of Lemma 1) and (16),

\endproof

An example of a distribution for which exists but is not square integrable is the Cauchy distribution. In particular, , so exists. In this case, nonexistence of can most easily be verified using the right hand side of (15) and a computer algebra package such as provided in Mathematica.

The next lemma may be helpful in verifying whether or not is trace class:

Lemma 3

We have

which is finite iff has finite mean.

Proof The first equality follows directly from (3), the second is well-known and can be found using similar techniques as in the proof of the second equality in Lemma 2. As is well-known, integration by parts leads to the representation of the mean as

so the mean exists iff the terms on the right hand side exists. Now since

and

it follows that

exists iff exists. \endproof

The quantity is also called Gini’s mean difference. Note that, by Lemmas 2 and 3, both and can be used as measures of dispersion.

An example of a distribution function for which is square integrable but not trace class is given in Example 2 in the next subsection.

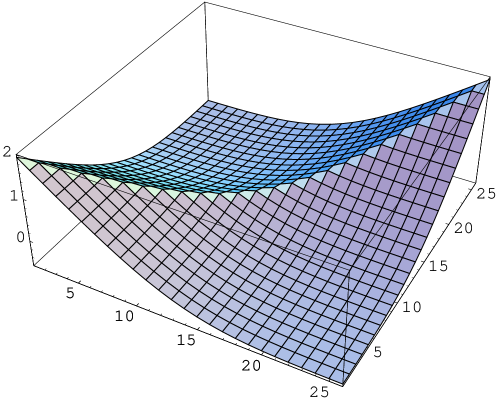

We conclude this section with a lemma concerning the shape of the graph of . In Figure 1 a representation of the graph of with the CDF of the normal distribution is given. The statements of Lemma 4 can be verified in the plot. Then:

Lemma 4

Suppose is such that exists. Then:

-

1.

For given , is strictly decreasing in on the domain and strictly increasing in on the domain .

-

2.

is strictly increasing in on the domain and strictly decreasing in on the domain .

Proof Part 1: With such that and , we obtain using Lemma 1 that

where the strict inequality holds because . This proves the strict decreasingness part, the strict increasingness is proven by appropriately reversing signs in the above.

Part 2: For we have

which is positive if and negative if , proving the monotonicity relations. \endproof

2.2 Spectral decomposition of

A sequence of random variables is said to converge to in mean square if

For a distribution function , we define

as the set of square integrable functions with respect to . A set of functions is said to be orthonormal if

| (17) |

(with the Kronecker delta) and

An orthonormal system is complete if for any function there exist numbers such that

with convergence in mean square. Then the system is also called a basis of . A number is called an eigenvalue of with corresponding eigenvector if and

| (18) |

Then we have:

Theorem 1

Suppose is square integrable. Then there exists a complete system of orthonormal functions of consisting of eigenfunctions of , the corresponding eigenvalues being nonnegative. Each is continuous and satisfies

| (19) |

if . Furthermore, has the spectral decomposition

| (20) |

where convergence is in mean square.

Proof A continuous square integrable kernel on a sigma-finite measure space is a Hilbert-Schmidt kernel which by a generalization of Mercer’s theorem has the desired spectral decomposition ( ?). It is easy to verify that is a -finite measure space, so the operator mapping the function to is a Hilbert-Schmidt operator. Nonnegativity of the eigenvalues follows from positivity of (see Lemma 1). Furthermore, from (18), so for nonzero . \endproof

Note that if is a solution to (18), then so is . To identify the solutions, we proceed as follows. A function is initially positive if there exists a such that and for all . Without loss of generality, we may assume that the are initially positive. We also assume the eigenvalues are ordered: . An interesting property of eigenfunctions of homogeneous positive Fredholm integral equations of the second kind is that they are oscillating, in the sense that for every , has distinct zeroes and no more than local extremes.

Some further results are as follows:

Lemma 5

For square integrable :

-

1.

if finite,

-

2.

.

Proof From the spectral decomposition (20) and Fubini’s theorem,

For the second part, the desired result is obtained by Parseval’s theorem. \endproof

As an example, we consider the dichotomous case which is the simplest possible and has closed form solutions:

Example 1

Consider the dichotomous case that . Then

The eigenvalues are and the eigenfunctions are and

which has mean zero and variance one. Now .

Equation (18) is a homogeneous Fredholm integral equation of the second kind based on the degenerate kernel (see, for example, ?). In general these equations are difficult to solve. In Sections 2.3 and 2.4, (18) is reduced to a simpler problem for the discrete and continuous case, respectively. We conclude this section with an alternative formula to (18) for finding the eigensystem which we use in the next two subsections. With

we have:

Lemma 6

The nonzero eigenvalues and eigenvectors of are solutions to the equation

for all .

Proof Substitution of the expression for of Lemma 1 into (18) yields

The Lemma follows from this and since by (19) as . \endproof

We have the following interesting implication:

Corollary 1

If is an interval with zero probability mass, i.e., , then a solution to (18) is linear on .

Proof If then from its definition it follows that is constant on . Therefore, for any , we obtain from Lemma 6 that

for some constant . Hence, is linear on . \endproof

Note that for discrete distributions, it follows that the eigenfunctions are piecewise linear.

2.3 Obtaining the eigensystem in the discrete case

We consider the case that is a.s. in a finite set, say . We use the shorthand and assume without loss of generality that and for all . Then we obtain:

Lemma 7

With the nonzero eigenvalues and eigenvectors of are solutions to the equations

Proof First note that from the definition for ,

It follows that

| (21) |

The first two displayed equations of the lemma now follow from (21), Lemma 6 and from . From (21) we further obtain

| (22) |

Again from Lemma 6, we have

Multiplying these equations by and respectively, taking differences and the use of 22 yields

which completes the proof. \endproof

More details on difference equations of the form given in Lemma 7 can be found in ? (?). Lemma 7 allows fast and memory efficient computation of the eigenvalues and vectors. In matrix notation, we must solve the generalized eigenvalue problem

where is the eigenvector with corresponding eigenvalue , is a diagonal matrix with the coordinates of on the main diagonal, and

This method can also be used for fast approximation of continuous systems (see Section 2.5). The exact solution for continuous systems is given in the next subsection.

2.4 Obtaining the eigensystem in the continuous case

If is differentiable, the problem of finding the eigenvalues and vectors can be reduced to a differential equation which is sometimes easier to solve:

Lemma 8

Suppose is the derivative of . Then the nonzero eigenvalues and eigenvectors of are solutions to the equation

| (24) |

subject to the side condition

Proof Letting in Lemma 6 we obtain

Differentiating both sides with respect to yields (24). Finally, since by (19) as , the side condition follows. \endproof

Equation (24) leads to an interesting observation on the behavior of the eigenfunctions : the second derivative is proportional to the local density times . As mentioned in Section 2.2 and as follows from the theory of Sturm-Liouville differential equations, the eigenfunctions oscillate. Now if the local density is low, the oscillatory behavior will be slower. In particular, on intervals where the local density is zero the second derivative of an eigenfunction is zero so the eigenfunction is linear. (NB: this also holds for non-continuous distributions, see Corollary 1).

If is both differentiable and invertible, we can reformulate differential equation (24) in the standard Sturm-Liouville form:

Lemma 9

Suppose is invertible. Let and suppose is twice differentiable. Then the eigenvalues and eigenvectors are solutions to the equation

| (25) |

subject to the side condition

Proof Note that

so that

From this the side condition follows. Substituting into the left hand side of (24) yields

Hence dividing both sides of (24) by yields the desired result. \endproofNote that for the the orthonormality condition (17) reduces to

In general, the differential equations (24) and (25) do not have closed form solutions (i.e., solutions in terms of well-known functions). We obtained the solutions for the uniform, the logistic and the exponential distributions which are given in Table 1, where is the th Legendre polynomial, is the th Bessel function of the first kind, the th zero of and

Numerical solutions were obtained for the normal, Laplace and chi-square distribution with one degree of freedom, see the next subsection for details on obtaining these solutions. For the normal and Laplace distributions we obtained the exact value of and for the normal distribution of using Lemmas 2 and 3 combined with results for order statistics by ? (?) and ? (?) summarized in ? (?) and using Mathematica.

We also obtained a closed form expression for the eigensystem for the distribution introduced in the next example. It is an example of a distribution for which is square integrable but not trace class, i.e., by Lemma 5, is finite but . We are not aware of any previous studies of this distribution.

Example 2

With standard normally distributed, let be defined as the following function of :

where the convention is used that for ,

Close to zero, has approximately a normal density, but for large values the density is much lower, that is, has much heavier tails than a standard normal.

With the distribution function of , we now show that is square integrable but not trace class. To show this, we shall derive an expression for to be plugged into Equation (25) so that it can be solved. The derivation involves the so-called complex error function. The error function is defined as

Note that the CDF of the standard normal distribution is . The imaginary error function is defined as

(Here . See ?, for some of the properties of erf and erfi.) We define the inverse as the unique real satisfying .

We see that

Now since has a standard normal distribution we obtain for the CDF of :

From this,

Some tedious but straightforward algebra then gives

Plugging this expression into (25) leads to the solution

where is the th Hermite polynomial. The ‘’ symbol is used to indicate that the expression for needs to be suitably normalized. This solution of (25) was derived by ? (?), who provided a method for solving differential equations of the form for certain types of weights , including . Note that for we obtain

It is well-known that here is divergent and .

| Distribution | Logistic | Uniform | Normal | |

|---|---|---|---|---|

| 0.5000 | 0.6079 | 0.5269 | ||

| 0.1667 | 0.1520 | 0.1635 | ||

| 0.0833 | 0.0675 | 0.0795 | ||

| 0.0500 | 0.0380 | 0.0470 | ||

| Distribution | Exponential | Laplace | Chi-square | Example 2 |

| 0.6360 | ||||

| 0.1458 | 0.1399 | |||

| 0.5453 | 0.4611 | 0.5567 | 0 | |

| 0.1627 | 0.1816 | 0.1615 | 0 | |

| 0.0774 | 0.0875 | 0.0758 | 0 | |

| 0.0451 | 0.0542 | 0.0438 | 0 |

No closed form expression is available.

Expression not normalized.

2.5 Discrete approximation of the continuous case

For many continuous distribution functions the differential equations (24) and (25) do not have a closed form solution and the first eigenvalues and eigenfunctions can be approximated by using a discrete approximation of and solving the difference equations of Lemma 7. For , let and let be a discrete random variable with . The eigenvalues and eigenvectors of , with the distribution function of , can then be calculated using the method of Section 2.3. For large , this method seems to give good approximations of the eigenvalues and eigenvectors of . An idea of the quality of the approximations can be gained from Table 2. The numerical results in Table 1 were obtained using this method. For further details on discrete approximations of eigenvalues and vectors of kernels see ? (?).

To obtain a good approximation, should of course be chosen as large as possible. Using Mathematica 5.2 on a Pentium IV computer at 3.0MHz, using no special routines for calculating the eigensytem of tridiagonal matrices, calculation of a complete solution for took 29 seconds. We expect that using software with such special routines, it is possible to obtain solutions of the first few eigenvalues and eigenvectors much more quickly and for much larger .

| True value | Estimate () | Estimate () | |

|---|---|---|---|

| 1 | 0.99303 | 0.99931 | |

| 0.28987 | 0.29027 | 0.28988 | |

| 0.50000 | 0.50370 | 0.50035 | |

| 9.0909 | 9.3093 | 9.1056 | |

| 9.9010 | 9.9708 | 9.9145 | |

| 9.9900 | - | 9.9970 |

For calculation of the eigensystem from a sample, see Section 4.1.

2.6 Relation to Anderson-Darling kernel

A related kernel was studied by ? (?) and ? (?), among others, in the context of Cramér-von Mises tests. With a nonnegative weight function, they considered the kernel

The kernel is closely related to the kernel : with , we obtain

Note that this conversion does not work for discrete . The eigensystem for is given by the set of solutions to (25) with replaced by the weight function ( ?).

Other closely related kernels have been given in the context of two-sample tests by ? (?) and ? (?). (See Section 5.2 for the relation between two-sample tests and tests of independence.)

3 Properties of and

We now apply the results of Section 2 in order to derive properties of and . In Section 3.1, some key properties are derived, including that , with iff and iff and are linearly related. In Section 3.2 we give a decomposition of and as weighted sums of squared correlations between the marginal eigenfunctions of and , weighted by functions of the eigenvalues. In Section 3.3, we describe a decomposition of the likelihood in terms of marginal eigenfunctions and component correlations of . In Section 3.4, Fréchet bound for the component correlations are given, which gives some insight into their meaning.

3.1 Key properties of and

Some key properties of and of , are given in the following theorem:

Theorem 2

Suppose and and are real random variables for which the marginal kernels and exist. Then:

-

1.

If , , and are constants, then and .

-

2.

with equality iff .

-

3.

If and then with equality iff and are a.s. linearly related.

-

4.

If both and are dichotomous then and

-

5.

With the th order statistic in a sample of size , .

The proof of the theorem is given at the end of this section. Note that and so the condition in Part 3 is equivalent to square integrability of the marginal kernels. From Theorem 2, Parts 2 and 3, we immediately have the following:

Corollary 2

Suppose and . Then , with iff and iff and are a.s. linearly related.

We may compare Corollary 2 to the related well-known result for the ordinary correlation : If and then with if and iff and are a.s. linearly related. The important difference is that is equivalent to but only implies , not vice versa. By Part 5 of Theorem 2, can be used as measures of dispersion for a real random variable . Note the relation with the variance, which can be defined as .

Note that, even though iff and are linearly related, is not a measure of linear association in the following sense: if the slope of the linear regression line of given is zero, need not be equal to zero.

From Lemma 2 and Lemma 3, a sufficient condition for to exist is that and exist. An example showing that this condition is not necessary is Example 2. Note that the existence of the ordinary correlation has the much stronger requirement of finite marginal variances. Summarizing, we have

where the one-way implications are strict.

Part 1 follows directly from the definition.

Part 2: From Lemma 1 we obtain

Furthermore, note that

which is easy to verify. Using these results and the finiteness of each side of (12) which allows us to apply Fubini’s theorem, we obtain

| (26) | |||||

If , the integrand is zero so . It remains to be shown that implies . We next sketch the proof.

If then there is an such that . We now show that if , then there is an open interval, which has as a limit point, such that on that interval. It then follows that (26) is nonzero. Let be the probability mass in , be the marginal probability mass in and be the marginal probability mass in . Denote by the limit approaching from anywhere in one of four open ‘quadrants’ defined by . Then from the definition of , and given in the introduction,

Now if these four expressions cannot all be zero, so there must be an open set, in at least one of the four ‘quadrants’ and with as a limit point, where is nonzero. Hence, (26) cannot be zero.

Part 3: By definition is equivalent to

This is a Cauchy-Schwartz inequality so it holds, and equality holds iff

| (27) |

for some constant . If for certain constants and then it is immediately verified that (27) holds with .

The reverse implication that (27) implies linearity remains to be shown. Suppose that (27) holds. Then

which reduces to

But this is equivalent to

| (28) |

Now without loss of generality suppose and for some and . Substitution into (28) then yields , so the second and third order statistics for and are linearly related. Now the distribution function of the second order statistic for is

and for

It is now straightforward to show that the equation leads to , so and are linearly related.

Part 4: Without loss of generality assume and with probability one. Then and (both and defined in Section 1), so .

Part 5: Since , this follows directly from Lemma 2 \endproof

We conclude this section by giving some representations of in terms of and the (conditional) distribution functions of and . Let

be the conditional distribution function of given .

Lemma 10

The following equalities hold for :

-

1.

-

2.

Part 2: First note that which we write in shorthand . Hence,

\endproof

Note the similarity of Part 1 of Lemma 10 with the formula for the covariance given by ? (?):

3.2 Orthogonal decomposition

Let us assume and are square integrable and have the spectral decompositions

| (29) | |||||

| (30) |

See Lemma 2 on how to check for square integrability. For ease of notation, we write the correlations between marginal eigenfunctions as

We now have the orthogonal decomposition given as follows:

Theorem 3

Suppose and are square integrable with spectral decompositions as above. Then with convergence in mean square,

and

Proof Write

Then straightforward algebra gives

By the Cauchy-Schwartz inequality we obtain

By mean square convergence of the spectral decomposition the latter goes to zero as so

as . Similarly we find

as . It follows that

as , which is the desired result. \endproof

The simplest example of a decomposition is if both variables are dichotomous, say and , we obtain , , and for so that , see Theorem 2, Part 4. In this special case the decomposition consists of just one component.

3.3 Parameterization of the likelihood

Let be the joint density of with corresponding marginal densities and . Since

we can decompose the joint density as:

| (31) |

A similar equation can be given for discrete distributions, and a general treatment can be given using the Radon-Nikodym derivative.

Decomposition (31) may be compared to the well-known canonical correlation decomposition

Here, and are those functions maximizing the correlation between and , subject to the restraint (for ) that they are orthogonal to and , respectively, and is the correlation between and .

3.4 Fréchet bounds for component correlations

Below, we discuss the interpretation and properties of the component correlations. In particular, we look at bounds for the component correlations.

For two random variables and with joint distribution function and marginal distribution functions and , the well-known Fréchet upper bound is defined by

and the Fréchet lower bound is defined by

Then if and only if and if and only if . A more general question is, for functions and , for which the correlation between and is maximal or minimal. Let

and

Then we have:

Lemma 11

For functions and , iff the support of the distribution of is a subset of and and iff the support is a subset of .

Proof Suppose for simplicity that and are standardized. Then iff and iff , and the lemma immediately follows. \endproof

For the dichotomous case we obtain the following:

Example 3

If both variables are dichotomous, say and , we obtain and .

Note that the bounds need not be attainable since it may be the case that, for example, for certain , there is no such that .

Here we are interested in the bounds for the component correlations of . For simplicity, we write . The next example shows that if both and have uniform distributions on , then the component correlations of can attain the bounds and :

Example 4

Suppose and are uniformly distributed on . Then the eigenfunctions are the Fourier cosine functions (see Table 1). The set is formed by the solutions to the equation

and by the solutions of

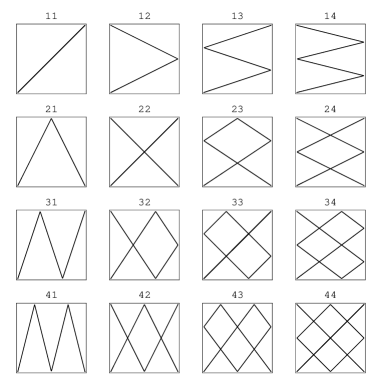

The solutions are plotted in Figure 2, for and . The bounds for the are attainable since for the uniform distribution on and for the uniform distribution on .

Note that, if , then , since . More generally, by the same reasoning, we have for all ,

and

By a symmetry argument, we also have , and there are various other similar implications.

An overview of a large amount of literature on Fréchet bounds is given in ? (?)

4 Estimation and tests of independence

In this section we discuss estimation of and by U- and V-statistics. Roughly speaking, the U-statistic estimator of a parameter is an unbiased estimator based on taking averages ( ?), and the V-statistic estimator is the estimator based on the distribution obtained by assigning a probability weight to each sample point. For , both the U- and V-statistic estimators are available, but for only the latter is. However, we can estimate by a function of U-statistic estimators.

In Section 4.1, it is shown how estimators of and by U- and V-statistics are obtained. In Section 4.2 permutation tests, useful for small samples, are described. In Section 4.3, the asymptotic distribution of these estimators is derived under the null hypothesis of independence. In Section 4.4, Bonferroni corrections for tests of significance of the component correlations are described.

4.1 U and V statistic estimators of

We first give a method for calculating the U- and V-statistic estimators of based on a sample , then we give the related estimates for .

The V-statistic estimator is the value of based on the sample distribution functions and , and is obtained as follows. Let

and

Then we have for ,

and the sample or V-statistic estimator of is given as

Now with

for , the unbiased or U-statistic estimator of is given as

By Hoeffding’s theory of U-statistics we have that is an unbiased estimator of ( ?, ?). Note that but may be negative.

The related estimators of are the following:

For both types of estimators, the computational complexity of the above method is .

The marginal eigenvalues and functions can be computed numerically from and or from and . See also Section 2.5 for computational aspects.

4.2 Permutation tests

Under independence, the sample marginal distributions of and are ancillary statistics for and , so by Fisher’s theory of fiducial inference we should condition on the sample marginals when testing for independence using and . If , conditioning on the marginals ensures that and are distribution free, and exact conditional -values can be calculated using the permutation method. Evaluating all permutations quickly becomes computationally prohibitive even for moderately large sample sizes, and we recommend using a set of random permutations. Note that permutation tests may also be applied to the component correlations and .

Permutation tests may be computationally intensive. Using non-optimized software, our experience shows that (bootstrap) permutation tests for up to a several hundred observations are feasible: for , the permutation test based on 1000 random permutations took less than four minutes, and for it took a bit more than one hour. Techniques for the fast exact evaluation of permutation tests using generating functions are described by, among others, ? (?) and ? (?), but it is not clear whether these techniques extend to statistics such as which are not based on ranks.

For categorical data the permutation test is better known as an exact conditional test (where the conditioning is, again, on the marginal distributions), the Fisher exact test being the best known example. There is a large body of literature on fast evaluation of exact conditional -values for contingency tables, for an overview see ? (?) and for more recent developments see ? (?, ?, ?).

If the permutation test is too computationally intensive, an asymptotic test may be done using the results of the next section.

4.3 Asymptotic distribution of estimators under independence

For the asymptotic distribution of the estimators we obtain the following:

Theorem 4

Proof By the ? (?) decomposition we can write with

Since a.s., and we obtain using the Cramér-Wold device that

The proof for is similar; we have

Since we obtain using the Cramér-Wold device that

under the condition that

is finite. Now by Lemma 5, the two factors on the right hand side are finite iff and are trace class, completing the proof. \endproofThe proof is similar to an adaptation by ? (?) of a proof by ? (?). See also ? (?) and ? (?).

Note that by Lemma 3, and are trace class iff and exist. As follows from the theorem and noted earlier by ? (?) for related statistics, the U-statistic estimator has an asymptotic distribution in more cases than the V-statistic estimator. For example, if the marginal distribution of at least one of and is the distribution of Example 2, does not have an asymptotic distribution but does have one.

4.4 Bonferroni corrections for testing significance of component correlations

As well as testing the significance of directly, we can test for the significance of the empirical component correlations . We recommend using rather than for calculating component correlations, since may be negative in which case no component correlations with nonnegative eigenvalues exist.

The proof of Theorem 4 suggests that the component correlations are asymptotically normal and independent. Since there are many component correlations, a simultaneous test of their significance needs a Bonferroni correction. The ordinary Bonferroni correction, i.e., multiplying the exceedance probabilities by the number of tests done, which in this case is , would be unreasonable since the multiplication factor increases rapidly with . Instead we propose dividing the exceedance probability for by

Note that these numbers will converge to zero in probability if at least one of and is not of trace class, i.e., by Lemma 3, if at least one of or does not exist, in which case the correction may not be the most appropriate one.

The idea of looking at components of a test seems to have first appeared in ? (?), where components of the Cramér-von Mises test were investigated. This test is a special case of the tests based on described above (see Section 5.2).

Other related work is by ? (?), who looked at correlations between orthogonal functions of the marginal cumulative distribution functions, in particular, the Legendre polynomials. This work is an extension of the so-called smooth tests of fit of ? (?). Rather than looking at all correlations between the orthogonal functions, they considered just the first few, and developed a selection method based on Schwartz’s rule for determining how many correlations to base the overall test on.

5 Grade versions of and , copulas, and rank tests

For ordinal random variables and , any given scale is arbitrary and it may be desirable to use scales based on the grades and of and . A general way to base and on grades is as follows. For given invertible distribution functions and , we can define

and

Note that

and

With and uniform distribution functions, is to what Spearman’s rho is to the ordinary correlation .

We can use the results of Section 4 to obtain an orthogonal decomposition of and in terms of component correlations. These component correlations then parameterize the copula, which is defined as the joint distribution of . From (31), and since the marginal eigenfunctions of with the uniform distribution are the cosine functions given in Table 1, we obtain the following decomposition of , the density function of the copula:

where . This decomposition was earlier given in ? (?) and ? (?). An overview of copula theory is given in ? (?). Possible drawbacks of using for some given and is the arbitrariness of any choice of and and the loss of scale information, but these issues are hotly debated ( ?).

In Section 5.1, a brief description of rank tests based on is given. In Section 5.2 a generalization of the Cramér-von Mises test to the case of ordered samples is shown to be a special case, and a convenient representation is given. In Section 5.3 we write as a weighted average of -coefficients.

5.1 Rank tests

Rank statistics which are distribution free under independence in the continuous case are obtained as follows. For invertible distribution functions and let

The derivation of the asymptotic distribution of these statistics is slightly more involved than that of the asymptotic distribution of . De Wet (?) has done this derivation for statistics related to . He gave the weights for optimal tests in the Bahadur sense for certain classes of alternatives, such as the bivariate normal.

With and the uniform distribution functions, is a statistic discussed by ? (?), see also ? (?). It can be viewed as a generalization of the ordinary Cramér-von Mises test (see next subsection). Similarly, with and the logistic distribution functions, can be viewed as a generalization of the Anderson-Darling test.

? (?) described a related test, namely based on the U-statistic estimator of

which can be obtained from the representation of in Lemma 10, Part 1, by replacing by . Hoeffding’s coefficient does not fall in the framework of the present paper.

5.2 A new class of -sample Cramér-von Mises tests as a special case

Suppose we have samples, the th sample having iid observations, say . Then a test whether the distributions of the observations in the different samples are equal is called a -sample test. A -sample test can, in fact, be viewed as a test of independence, namely, whether ‘response’ depends on ‘group membership,’ the groups referring to the different samples. Let us consider the case that the score is assigned to sample () . With and let for and . Then it can be seen that the sample test is a test of independence of the observations and the observations. (Note that here the observations are not random). A -sample test can then be based on or .

If samples are ordered but have no numerical scores assigned to them, rank scores can be assigned, for example .

In order to arrive at the Cramér-von Mises test, we now use Lemma 10, Part 2 to give a representation of in terms of the conditional distribution functions. Let be the distribution function of , the response for sample , and let be the proportion of observations in sample . Then we obtain

Some straightforward algebra shows that for the two-sample case this reduces to

A grade version of is

where

In the two-sample case, the sample version of with the uniform distribution function reduces (essentially) to the ordinary Cramér-von Mises statistic, so we have a generalization to the case of ordered samples. With the logistic distribution, reduces to the Anderson-Darling statistic.

A different generalization of the two-sample Cramér-von Mises test was given by ? (?), namely to the case of unordered samples.

5.3 as a weighted -coefficient

From Lemma 10, Part 1, we directly obtain

| (35) |

This result leads to an interesting interpretation of . The coefficient for measuring the dependence in the table obtained by collapsing the distribution with respect to the cut point is given as

| (36) |

Now suppose is such that

Then from (35) we obtain that can be written as a weighted average -square:

where the weight function is defined by

The normalized weight function (integrating to one) is

where

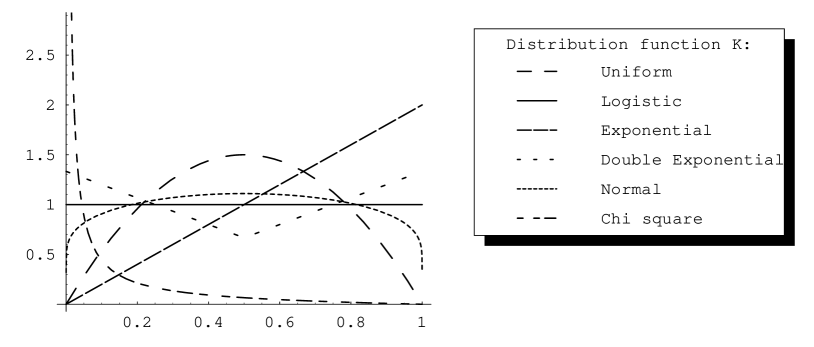

In Figure 3, is plotted for the distribution functions given in Table 1.

From Figure 3 we can deduce which -coefficients are given most weight for different marginal distributions. As the reference marginal, we take the logistic, which is the horizontal line in the figure, i.e., assigning uniform weights. We see that for a uniform marginal, the weight goes to zero in the tails. The weights for a normal marginal are for most intermediate between the weights for the uniform and logistic marginals. In contrast to uniform and normal marginals, the Laplace distribution gives more weight to the tails than a logistic marginal. An exponential marginal gives little weight to the lower tail, but much weight to the upper tail. Finally, the chi-square distribution gives very large weight to the lower tail and very small weight to the upper tail. Among the distributions considered, the biggest difference is between the chi-square and the exponential distribution.

6 Data analysis: investigating the nature of the association

Gaining an understanding of the nature of an association between two random variables is probably best viewed as an art rather than a science, and in this section we present some visual tools based on and its components which may be helpful in reaching this objective. For an iid bivariate sample we propose the following two procedures.

Firstly, we calculate from the sample and test its significance. If found to be significant, then for each data point we calculate the weight

Since

the weights give an indication of how much the sample element contributes to , and so can be used to discover the nature of a possible association between and .

Secondly, we calculate the component correlations of and test their significance using the Bonferroni corrections described in Section 4.4. Then for each significant component correlation , we compute the weights

where and are the eigenfunctions belonging to and . Since

the weight is the amount the sample element contributes to (conditionally on the marginals), and so, like , can be used to investigate the association between and .

In this section we show how to visualize the weights and , both for continuous and categorical data, and show how this can be used to gain an understanding of the association. Some artificial continuous data sets are considered in Section 6.1, a real categorical data set is considered in Section 6.2 and a real time series data set is considered in Section 6.3

6.1 Some artificial data sets

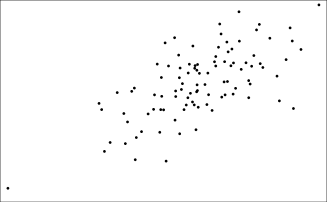

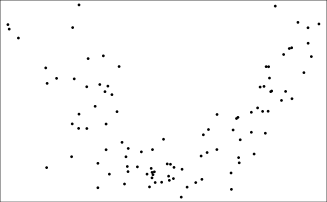

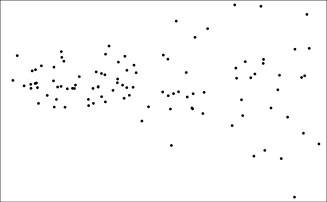

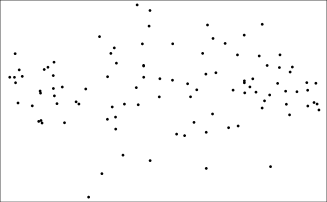

In Figure 4, four artificial data sets are plotted, each consisting of 100 iid points. For completeness, we explain how the data were generated. In the following, is uniformly distributed on and and are iid standard normal random variables, and has a normal distribution with mean zero and standard deviation . The data in Figure 4(a) are from a bivariate normal distribution with . The data in Figure 4(b) are of the form . The data in Figure 4(c) are of the form . Finally, the data in Figure 4(d) are of the form .

For all four data sets, we performed permutation tests for the significance of and its component correlations based on 10,000 random permutations. This took us about 48 minutes for each data set. For the significant component correlations we took 1 million random permutations to get a more accurate -value, and this took about 110 seconds per component correlation. We also computed the ordinary correlation, and, not surprisingly, only for the data in Figure 4(a) it is significantly different from zero. There we found that ().

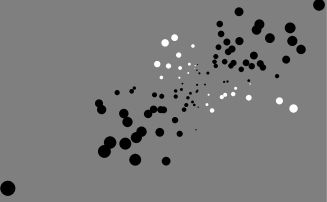

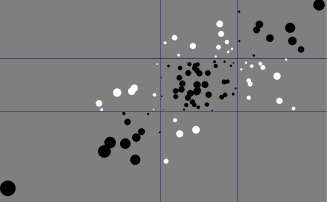

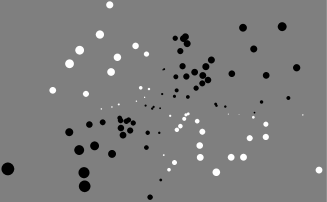

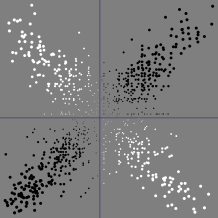

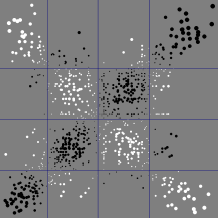

For the data in Figure 4(a), we found that (), i.e., there is significant association. In Figure 5(a), the data are plotted again, this time each sample element is represented with size proportional to ; black dots represent positive and white represent negative . In all these plots, the total area of the dots is scaled to a constant to make it easier to study them. From Figure 5(a),we see that the association seems to consist of a linearity in the data. It may be worthwhile however to check if there are other forms of association present by looking at the component correlations of . We found two significant components: () and (). In Figures 6(a) and 6(b) the weights and are visualized. The interpetation of the black and white dots is the same as above. The gridlines correspond to the zeroes of the marginal eigenfunctions. Therefore, within any rectangle the dots have the same color. Also in this case, the plots point to a linearity in the data.

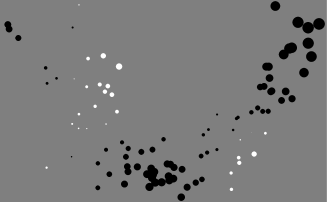

For the data in Figure 4(b), we found () and we found two significant component correlations: () and (). The plots in Figures 5(b), 6(c) and 6(d) all point to a curved relationship.

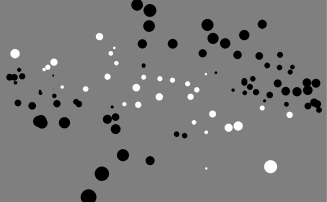

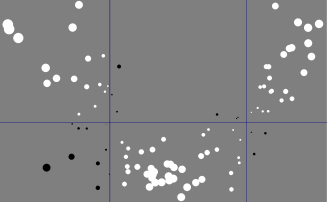

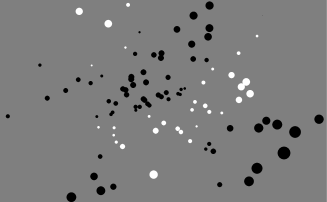

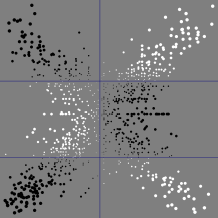

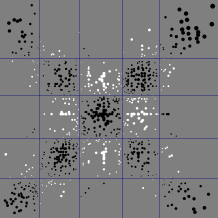

For the data in Figure 4(c), we found that (). There is significant association at the 5% level, but the evidence is not as overwhelming as in the previous two cases. We only found one significant component correlation: (). Figures 5(c) and 6(e) both point towards and increase in dispersion of the variable as increases.

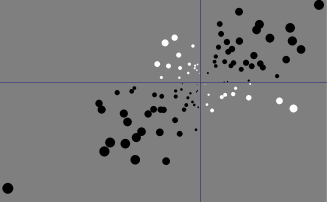

For the data in Figure 4(d), we found that (). This time, the test based on does not yield a significant association. However, there is one significant component correlation: (). Figure 6(f) indicates that the association is due to an increase and then decrease in dispersion. Since is not significant, we should refrain from giving an interpretation based on Figure 5(d).

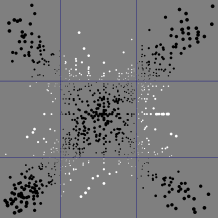

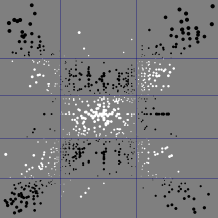

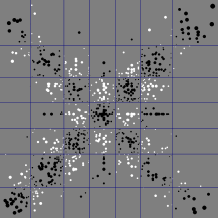

For comparative purposes, we plotted the weights for data drawn from a distribution satisfying independence in Figure 7. Both sets consist of 100 sample elements. The most common pattern is that of Figure 7(a), with two diagonally opposing clusters of black dots and two diagonally opposing clusters of white dots. In a very limited investigation, this type of pattern occured about half of the time. Otherwise more complex patterns were obtained, such as the one in Figure 7(b). These figures indicate that it doesn’t seem to make sense to interpret this kind of plot if is not significant, such as Figure 5(d).

6.2 Mental health data

| Mental Health Status | ||||

| Parents’ | Mild | Moderate | ||

| Socioeconomic | Symptom | Symptom | ||

| Status | Well | Formation | Formation | Impaired |

| A (high) | 64 | 94 | 58 | 46 |

| B | 57 | 94 | 64 | 40 |

| C | 57 | 105 | 65 | 60 |

| D | 72 | 141 | 77 | 94 |

| F | 36 | 97 | 54 | 78 |

| G (low) | 21 | 71 | 54 | 71 |

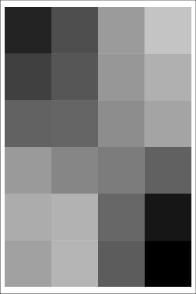

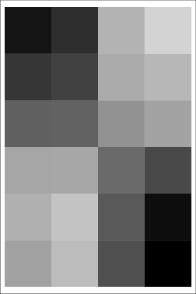

Table 3 describes the relationship between child’s mental impairment and parents’ socioeconomic status for a sample of residents of Manhattan ( ?, ?, and references therein). Goodman used this table to illustrate various association models for categorical data, including the so-called linear by linear association model, the row and columns effects model, and correspondence analysis based on canonical correlations. Here we illustrate the use of and its components as yet an alternative method for analyzing these data. We relied on asymptotic -values because with 1670 observations approximate evaluation of the permutation tests would have been too time consuming using our implementation.

In the categorical case, for an contingency table, it suffices to calculate weights for the cells, i.e., it is not necessary to calculate separately a weight for each individual observation. For an observation in cell , the weight reduces to

where is the proportion of observations in cell . Similarly, the weights belonging to component correlation are

for , , and . Note that

and

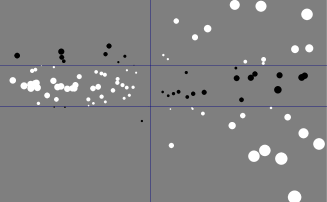

We found that (), i.e., there is significant association in the data. The weights for the cells are represented in Figure 8(a). Here, the grayscale represents the size of : the darker the cell, the larger ; is represented by a fixed intermediate shade of gray. From Figure 8(a), it can be seen that most of the association is of a monotone nature: the higher the parents’ socioeconomic status, the better the mental health status of their children. We also investigated the component correlations and found two components to be significant at the 5% level: () and (). In Figures 8(b) and 8(c) we represented the and using grayscales as above. From Figure 8(b), we see that indicates linearity again. However, in Figure 8(c) we see evidence of some nonlinearity in the data, namely an apparent reversal of the association if only the middle categories ‘Mild Symptom Formation’ and ‘Moderate Symptom Formation’ are considered. Hence, it appears that the association which is present in the data cannot be fully explained by linearity.

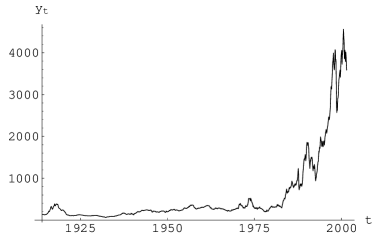

6.3 Norwegian stock exchange

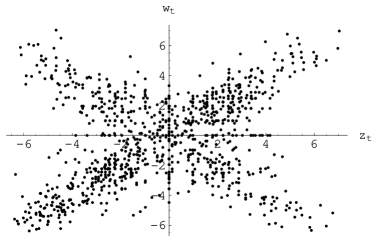

The Norwegian stock exchange data represented in Figure 9(a) yield an example with an especially interesting form of association. In Figure 9(a) the original time series data are plotted. In Figure 9(b) we plotted

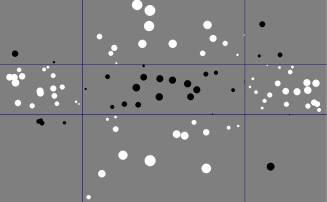

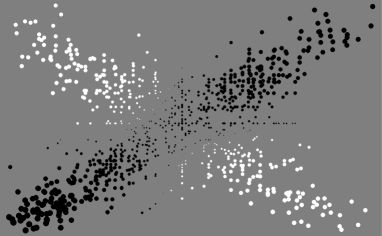

The arcsinh transformation was done to make the marginal distributions less heavy tailed. We found a highly significant association with (). From Figure 9(b) we can already interpret the association: large jumps (up or down) in stock prices tend to be followed by large jumps, and small jumps by small jumps, indicating periods of volatility. In Figure 9(c), the weights are represented by the size and color of the dots (see Section 6.1 for further explanation). This plot points to the same conclusion that large jumps are followed by large jumps and small jumps by small jumps. Note that in this case, not only the positive weights (the black dots) but also the negative weights (the white dots) are highly indicative of association. The plot indicates that the up-arm (with the black dots) is ‘heavier’ than the down-arm (with the white dots), that is, there is evidence that in the data generating process a jump tends to be of the same sign as the previous jump.

Seven component correlations were found to be significant at the 5% level after applying the Bonferroni correction: , , , , , and , all with . In Figure 10, the weights corresponding to the component correlations are represented. Figures 10(c), (d), (f) and (g) point to the cross-like nature of the data. Figures 10(a) and (e) indicate that the up-arm is heavier than the down-arm. We did not find a meaningful explanation for Figure 10(b).

6.4 Discussion

If a researcher investigating the association between two variables decides on the use of , we recommend the following approach. First a test of the significance of should be done, and, if found to be significant, the weights should be visualized as described above in order to determine the nature of the association. If this does not yield the desired insight, it can be worthwhile to investigate the component correlations and visualize the corresponding weights . These components form a (unique) orthogonal decomposition of the ‘infinite-dimensional’ object into ‘one-dimensional’ objects , and the orthogonality ensures, in a limited sense, that the different components measure different things; by the latter we mean that for large samples and close to independence, the sample component correlations are approximately independent. The question may arise: why not investigate correlations between other sets of orthogonal functions? A sketch of an answer is as follows. Because of the various optimality properties of the eigenfunctions in describing the marginal kernels, these component correlations are likely to be a better choice for investigating the deviation of from zero than correlations between arbitrarily chosen functions for the marginal distributions. One way to make this intuitive is as follows: in those regions where the marginal distributions are sparse, the eigenfunctions vary relatively slowly (in second derivative sense, see remark after Lemma 7), and therefore power of a test based on a component correlation will be concentrated in those regions where there are many observations. Thus, if we believe to be a good measure of deviation from independence, then good ‘one-dimensional’ objects to look at are the correlations between the marginal eigenfunctions of and .

Acknowledgements

The author would like to thank the following institutes where he has been employed for providing a stimulating environment in which to carry out this research: The Methodology Department of the Faculty of Social Sciences at Tilburg University (Tilburg, the Netherlands) and EURANDOM (Eindhoven, the Netherlands).

References

- Agarwal Agarwal, R. P. (1992). Difference equations and inequalities. New York: Marcel Dekker.

- Agresti Agresti, A. (1992). A survey of exact inference for contingency tables. Statistical Science, Vol. 7, No. 1, 131-177.

- Agresti Agresti, A. (2002). Categorical Data Analysis, 2nd edition. New York: Wiley.

- Anderson and Darling Anderson, T. W., and Darling, D. A. (1952). Asymptotic theory for certain ‘goodness of fit’ criteria based on stochastic processes. Ann. Math. Stat., 47, 193-212.

- Baglivo, Pagano, and Spino Baglivo, J., Pagano, M., and Spino, C. (1996). Permutation distributions via generating functions, with applications to sensitivity analysis of discrete data. J. Am. Stat. Ass., 91, 1037-1046.

- Baringhaus and Franz Baringhaus, L., and Franz, C. (2004). On a new multivariate two-sample test. Journal of multivariate analysis, 88, 190-206.

- Blum, Kiefer, and Rosenblatt Blum, J. R., Kiefer, J., and Rosenblatt, M. (1961). Distribution free tests of independence based on the sample distribution function. The annals of mathematical statistics, 32, 485-498.

- Booth and Butler Booth, J. G., and Butler, R. (1999). An importance sampling algorithm for exact conditional tests in log-linear models. Biometrica, 86, 321-332.

- Bose and Gupta Bose, R. C., and Gupta, S. S. (1959). Moments of order statistics from a normal population. Biometrika, 46, 433 - 440.

- De Wet De Wet, T. (1980). Cramér-von Mises tests for independence. J. Multivariate Anal., 10, 38-50.

- De Wet De Wet, T. (1987). Degenerate U- and V-statistics. South African Statistical Journal, 21, 99-129.

- De Wet and Venter De Wet, T., and Venter, J. H. (1973). Asymptotic distributions for quadratic forms with application to tests of fit. Annals of Statistics, 1, 380-387.

- Deheuvels Deheuvels, P. (1981). An asymptotic decomposition for multivariate distribution-free tests of independence. J. Multivariate Anal., 11, 102-113.

- Diaconis and Sturmfels Diaconis, P., and Sturmfels, B. (1998). Algebraic algorithms for sampling from conditional distributions. Ann. Stat., 13, 363-397.

- Durbin and Knott Durbin, J., and Knott, M. (1972). Components of the Cramér-von Mises statistics, I. J. R. Statist. Soc. B, 34, 260-307.

- Eagleson Eagleson, G. K. (1979). Orthogonal expansions and U-statistics. Australian Journal of Statistics, 21, 221-237.

- Forster, McDonald, and Smith Forster, J. J., McDonald, J. W., and Smith, P. W. F. (1996). Monte Carlo exact conditional tests for log-linear and logistic models. J. Roy. Stat. Soc. Ser B, 58, 445-453.

- Goodman Goodman, L. A. (1985). The analysis of cross-classified data having ordered and/or unordered categories: association models, correlation models, and asymmetry models for contingency tables with or without missing entries. Ann. Stat., 13, 10-69.

- Govindarajulu Govindarajulu, Z. (1963). On moments of order statistics and quasi-ranges from normal populations. Ann. Math. Statist., 34, 633-651.

- Gregory Gregory, G. G. (1977). Large sample theory for U-statistics. Annals of Statistics, 5, 110-123.

- Hall Hall, P. (1979). On the invariance principle for U-statistics. Stoch. Proc. Appl., 9, 163-174.

- Hoeffding Hoeffding, W. (1940). Masstabinvariante Korrelationtheorie. Schriften Math. Inst Univ. Berlin, 5, 181-233.

- Hoeffding Hoeffding, W. (1948a). A class of statistics with asymptotically normal distribution. Annals of Mathematical Statistics, 19, 293-325.

- Hoeffding Hoeffding, W. (1948b). A non-parametric test of independence. Annals of Mathematical Statistics, 19, 546-557.

- Hoeffding Hoeffding, W. (1961). The strong law of large numbers for U-statistics. Institute of Statistics, University of North Carolina, Mimeograph Series No. 302.

- Johnson, Kotz, and Balakrishnan Johnson, Kotz, and Balakrishnan. (1994). Continuous univariate distributions: volume 1. New York: Wiley.

- Kallenberg and Ledwina Kallenberg, W. C. M., and Ledwina, T. (1999). Data driven rank tests for independence. J. Amer. Statist. Assoc., 94, 285-301.

- Kiefer Kiefer, J. (1959). -sample analogues of the Kolmogorov-Smirnov and Cramér-von Mises tests. Ann. Math. Stat., 30, 420-447.

- Mikosch Mikosch, T. (2006). Copulas: tales and facts (with discussion). Extremes, To appear.

- Nelsen Nelsen, R. B. (2006). An introduction to copulas. New York: Springer.

- Neyman Neyman, J. (1937). “Smooth” tests for goodness of fit. Skand. Aktuarietidskr., 20, 150-199.

- Randles and Wolfe Randles, R. H., and Wolfe, D. A. (1979). Introduction to the theory of nonparametric statistics. New York: Wiley.

- Rüschendorf Rüschendorf, L. (1991). Fréchet bounds and their applications. In G. Dall’Aglio, S. Kotz, and G. Salinetti (Eds.), Advances in probabability distributions with given marginals (p. 151-188). Kluwer.

- Tricomi Tricomi, F. G. (1985). Integral equations. Dover Publications.

- Van de Wiel, Di Bucchianico, and Van der Laan Van de Wiel, M. A., Di Bucchianico, A. D., and Van der Laan, P. (1999). Symbolic computation and exact distributions of nonparametric test statistics. The statistician, 48, 507-516.

- Weisstein Weisstein, E. W. (1999). “Erf” and “Erfi”. From MathWorld–A Wolfram Web Resource. http://mathworld.wolfram.com/Erfi.html.

- Zaanen Zaanen, A. (1960). Linear analysis. Amsterdam: North Holland Publishing Co.

- Zech and Aslan Zech, G., and Aslan, B. (2003). A multivariate two-sample test based on the concept of minimum energy. PHYSTAT2003, 97-100.